Contract Catering Market Size, Share, Trends and Forecast by Contract Type, Mode of Contract, End User, and Region, 2026-2034

Global Contract Catering Market Size, Share, Trends & Forecast (2026-2034)

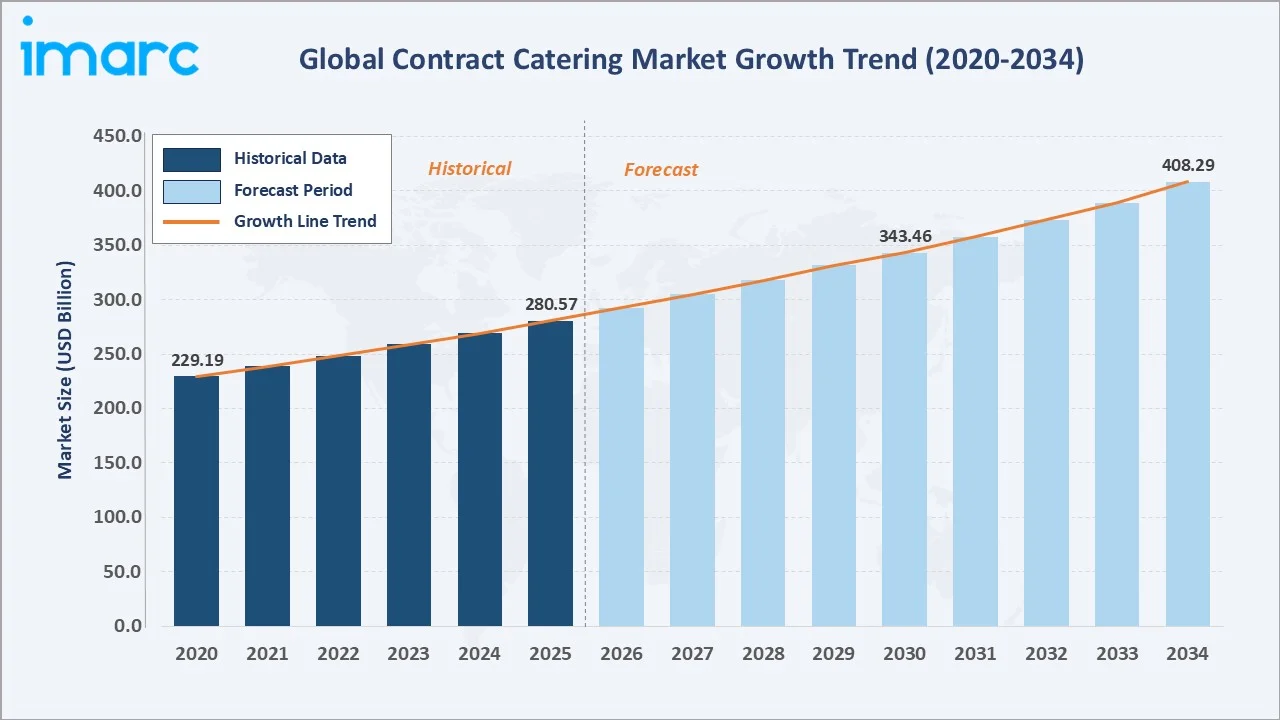

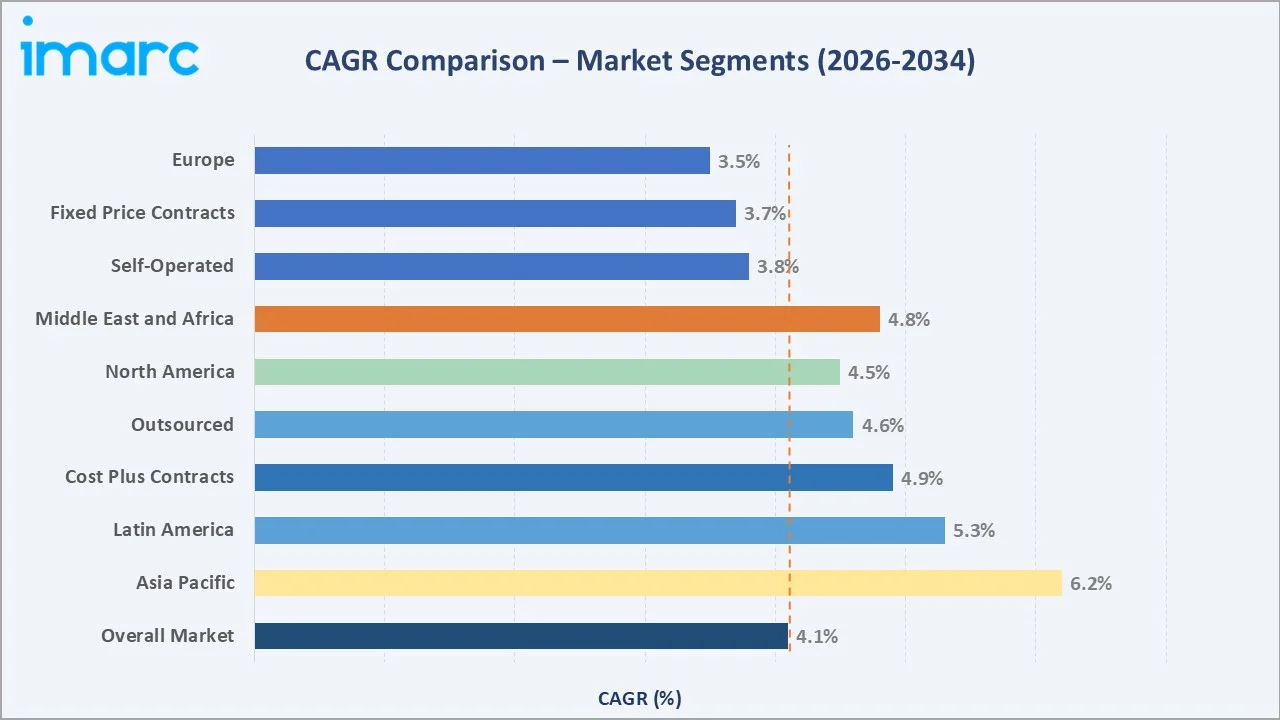

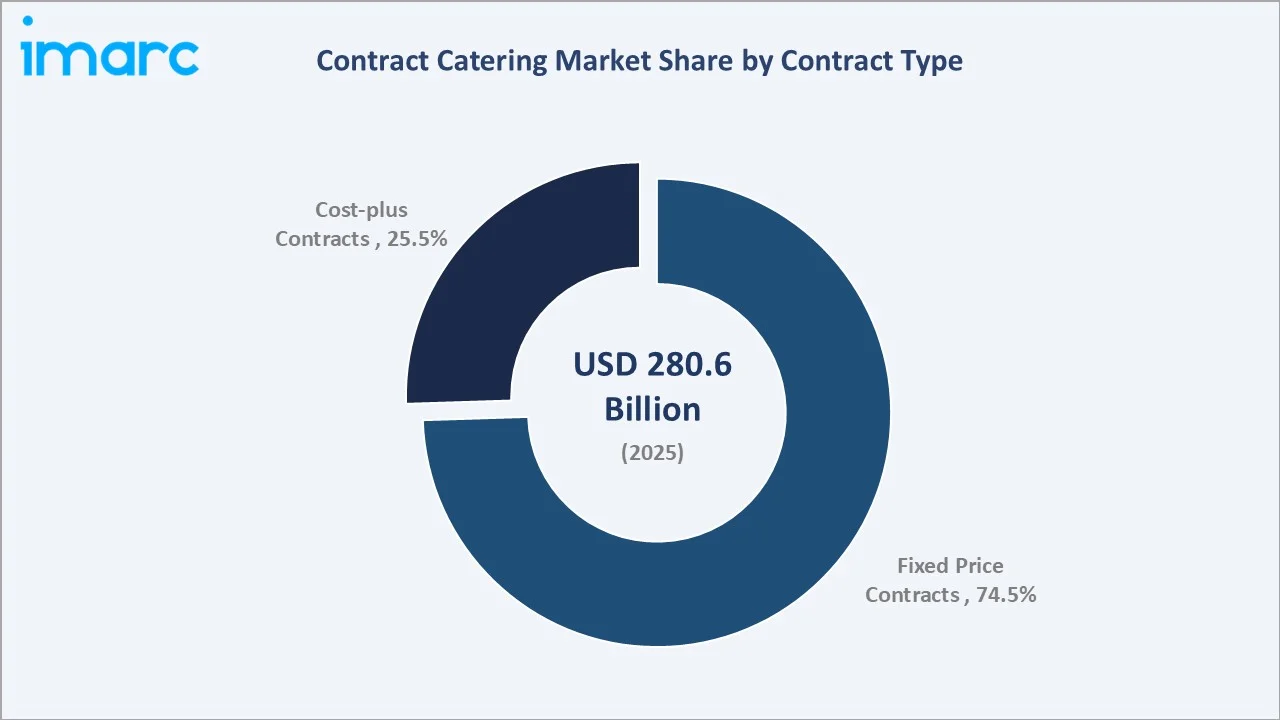

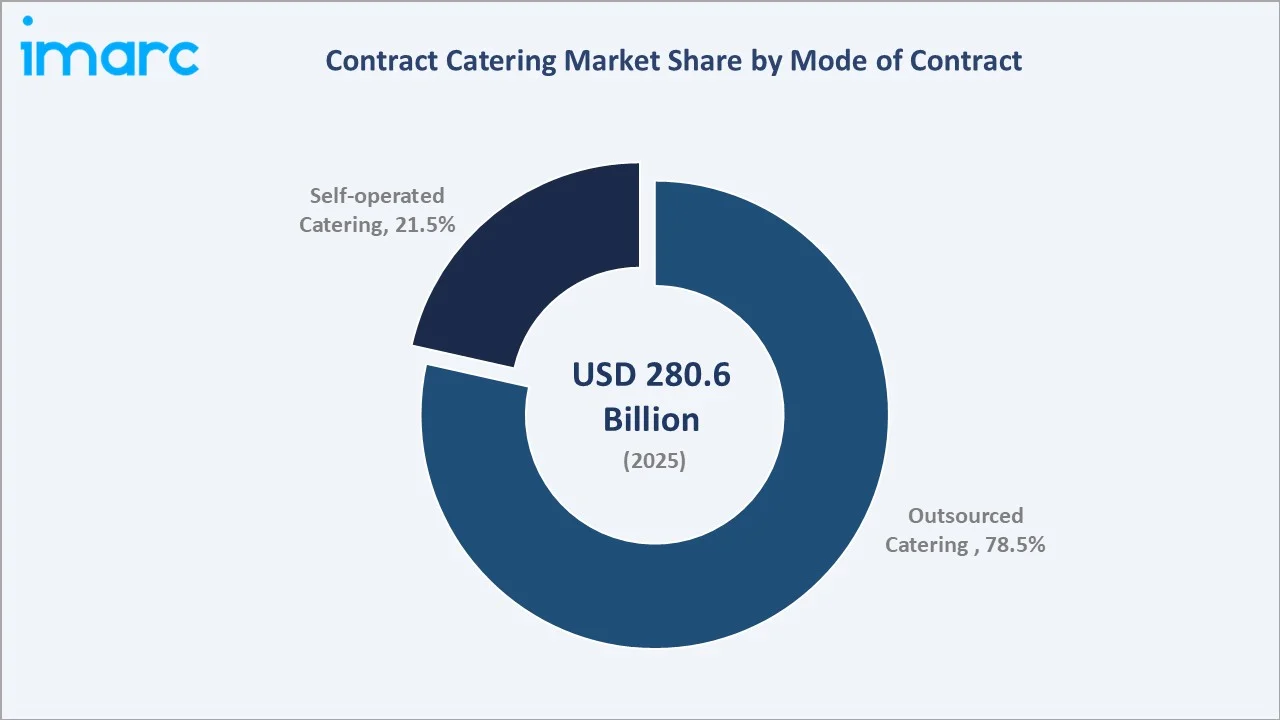

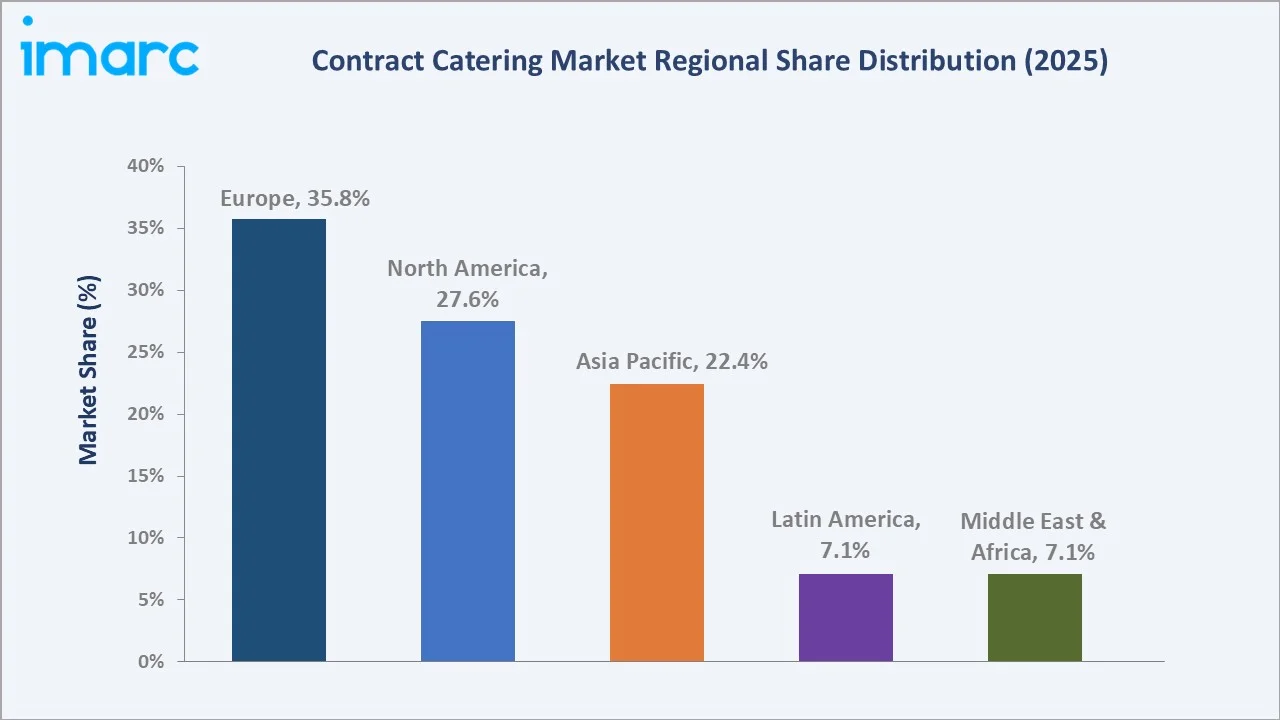

The global contract catering market size was valued at USD 280.6 Billion in 2025 and is projected to reach USD 408.3 Billion by 2034, at a CAGR of 4.1% during 2026-2034. Rising corporate outsourcing of food services, expanding institutional end-user bases across education and healthcare, growing demand for diverse and nutritious meal options, and strengthening sustainability mandates are collectively driving contract catering market growth. Fixed Price Contracts dominate with a 74.5% share in 2025, while the Outsourced mode of contract accounts for 78.5% of the global market. Europe leads regional demand with a 35.8% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 280.6 Billion |

|

Forecast Market Size (2034) |

USD 408.3 Billion |

|

CAGR (2026-2034) |

4.1% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (35.8% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Contract Type |

Fixed Price Contracts (74.5%, 2025) |

|

Leading Mode of Contract |

Outsourced (78.5%, 2025) |

The chart shows contract catering market growth from 2020–2034, with post-pandemic recovery driving history and outsourcing trends supporting forecasts.

To get more information on this market, Request Sample

CAGR analysis identifies Fixed Price Contracts and Outsourced Mode as the fastest-growing segments in the global contract catering market through 2034.

Executive Summary

The global contract catering market is transforming due to corporate outsourcing, growing nutritional awareness, and digitalized food services. Valued at USD 280.6 billion in 2025, it is projected to reach USD 408.3 billion by 2034, at a 4.1% CAGR. Rising operational complexity and cost pressures are accelerating outsourcing, with corporate, healthcare, and education sectors driving majority demand.

Fixed price contracts lead the market with a 74.5% share in 2025, driven by demand for cost predictability and financial planning. Outsourced contracts hold 78.5% of global revenue, highlighting preference for third-party catering. Key trends include plant-based menus, smart kitchen adoption, responsible sourcing, and increasing regulatory focus on food safety and compliance standards.

Europe leads the global contract catering market with a 35.8% share in 2025, supported by mature corporate catering in the UK, France, and Germany. North America holds 27.6%, driven by employer dining, universities, and healthcare outsourcing. Asia Pacific accounts for 22.4% and is the fastest-growing region, fuelled by urbanization, workforce expansion, and rising institutional quality expectations.

Key Market Insights

|

Insight |

Data |

|

Largest Contract Type Segment |

Fixed Price Contracts – 74.5% share (2025) |

|

Second Contract Type Segment |

Cost Plus Contracts – 25.5% share (2025) |

|

Leading Mode of Contract |

Outsourced – 78.5% share (2025) |

|

Leading Region |

Europe – 35.8% revenue share (2025) |

|

Second Region |

North America – 27.6% revenue share (2025) |

|

Top Companies |

Compass Group, Sodexo, Aramark, Elior, ISS A/S, Eurest |

Key Analytical Observations Supporting The Above Data:

- Fixed Price Contracts' 74.5% dominance in 2025 reflects institutional clients' preference for predictable cost structures and transparent financial planning across multi-year service agreements.

- Cost Plus Contracts at 25.5% in 2025 serve specialized segments where ingredient costs are highly variable – such as premium corporate dining and remote site catering – where flexibility in pricing is a necessary operational requirement.

- The Outsourced segment's 78.5% share in 2025 validates the structural trend of organizations divesting non-core food operations to gain access to specialist catering expertise, technology platforms, and economies of scale unavailable to self-operated models.

- Europe's 35.8% global dominance in 2025 reflects the region's mature and highly regulated food service industry, with the UK, France, and Germany each hosting large-scale national catering operators managing thousands of client sites.

- Asia Pacific's position as the fastest-growing region is underpinned by rapid workforce expansion, urbanization, and government investment in institutional food programs across China, India, and ASEAN nations.

- Compass Group and Sodexo together generated over USD 65 Billion revenue in 2024, reinforcing their leadership in the global contract catering market.

Global Contract Catering Market Overview

Contract catering involves outsourced food and beverage services delivered under formal agreements. Services include menu planning, sourcing, preparation, serving, and hygiene management across corporates, education, healthcare, defence, and airports. The ecosystem includes raw material suppliers, logistics providers, kitchen equipment manufacturers, regulatory authorities, and client organizations supporting end-to-end food service operations.

Contract catering spans corporate cafeterias, university dining, hospital meal programs, military bases, stadium concessions, and airport food services. Growth is driven by increasing white-collar employment, expanding institutional infrastructure, rising per-capita income in emerging markets, and stronger regulatory requirements focused on food safety and service compliance.

Market Dynamics

To evaluate market opportunities, Request Sample

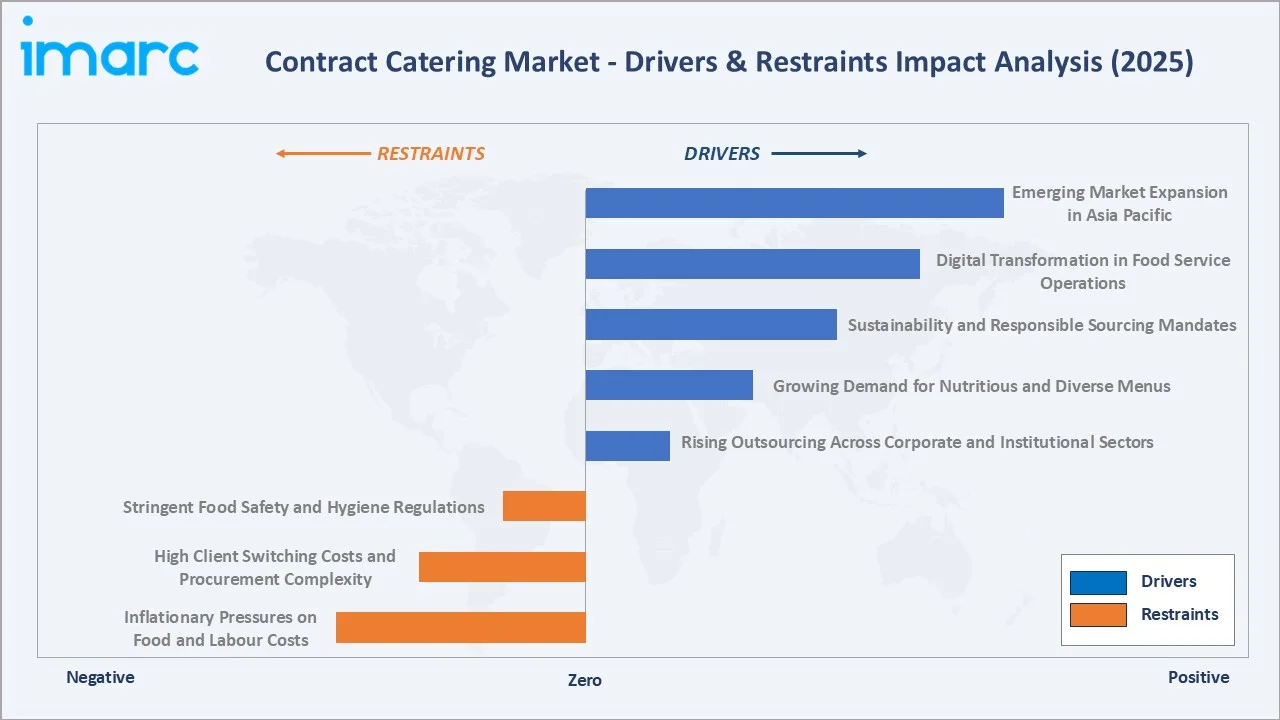

Market Drivers

- Rising Outsourcing Across Corporate and Institutional Sectors: Rising outsourcing across corporate and institutional sectors is driving contract catering demand, as organizations increasingly delegate food services to specialized providers to improve operational efficiency, reduce costs, and focus on core business functions.

- Growing Demand for Nutritious and Diverse Menus: Post-pandemic health awareness is shifting demand toward nutritious, allergen-transparent, and diverse menus. Contract caterers are expanding plant-based and healthier offerings, increasingly influencing client preferences and procurement requirements across corporate and healthcare sectors.

- Sustainability and Responsible Sourcing Mandates: Corporate ESG frameworks increasingly require catering partners to demonstrate responsible sourcing, including local procurement, fair trade certification, food waste reduction, and sustainable packaging. Caterers aligning with these sustainability standards gain competitive advantage, particularly among multinational clients with enterprise-level sustainability reporting requirements.

- Digital Transformation in Food Service Operations: Technology adoption, including AI-driven planning, digital ordering, and smart kitchens, is improving contract catering efficiency, reducing food waste, enhancing forecasting, and optimizing procurement across operations.

Market Restraints

- Inflationary Pressures on Food and Labour Costs: Global food commodity inflation and rising labor costs across the UK, U.S., and Australia compressed contract catering margins between 2021 and 2023. Food prices surged, with UK inflation reaching 19.1% and U.S. food inflation peaking above 11.4%, creating profitability pressure for fixed-price and long-duration catering contracts.

- High Client Switching Costs and Procurement Complexity: Switching catering providers causes operational disruption, staff retraining, and regulatory re-certification, creating institutional inertia and limiting new entrants’ ability to replace incumbent operators.

- Stringent Food Safety and Hygiene Regulations: Stringent food safety regulations require caterers to implement HACCP, allergen management, and traceability systems, increasing operational complexity and compliance costs across contract catering operations.

Market Opportunities

- Emerging Market Expansion in Asia Pacific: Rapid urbanization, expanding Tier-2 corporate offices, and government feeding programs across India, Indonesia, and Vietnam are boosting contract catering demand. India’s PM-POSHAN program alone serves about 120 million children daily.

- Healthcare and Senior Care Catering Growth: Aging populations across Europe, North America, and Japan are driving structural demand growth for specialized senior care nutrition services – among the highest-margin sub-segments within the broader contract catering industry.

- Technology-Enabled Personalized Dining Experiences: AI-powered personalization, digital ordering, and smart menu planning help contract caterers enhance service quality, improve operational efficiency, and differentiate offerings, supporting premium contract positioning.

Market Challenges

- Skilled Labour Shortages: The food service sector faces persistent shortages of trained chefs, nutritionists, and kitchen managers across North America, Europe, and Australia, limiting operators' capacity to scale new site openings and maintain service consistency.

- Contract Margin Compression on Long-Term Fixed-Price Agreements: Multi-year fixed-price contracts created profitability risks during inflation, as food and labor costs rose faster than pricing adjustments. Companies including Sodexo and Elior reported margin pressure and contract renegotiations, highlighting the financial impact of legacy contracts during 2022–2024.

- Supply Chain Disruptions and Ingredient Sourcing Risk: Geopolitical instability, climate-related agricultural yield variability, and logistics disruptions continue to create supply chain fragility for caterers dependent on global ingredient sourcing.

Emerging Market Trends

1. Plant-Based and Flexitarian Menu Integration

Catering operators are reformulating menus to include plant-based proteins, vegan options, and flexitarian meals. Compass Group expanded plant-forward offerings globally to support sustainability goals and meet growing demand for healthier, lower-carbon food choices.

2. Smart Kitchen Technology and Automation Adoption

IoT-enabled kitchen technologies, including connected equipment and real-time monitoring, are improving operational efficiency. Smart kitchen platforms used by major caterers have reduced food waste by around 25–30% while ensuring consistent quality across locations.

3. Digital Ordering and Cashless Payment Ecosystems

Mobile ordering, QR-code menus, and contactless payments are becoming standard in contract catering, improving convenience, reducing queues, and enhancing diner engagement across workplace and institutional food service environments.

4. Personalized Nutrition and Allergen Management

Advanced dietary management platforms enabling clients to specify allergen-free, therapeutic, or performance-nutrition meal preferences are emerging as key service differentiators. Healthcare and corporate wellness sector clients are actively prioritizing caterers capable of delivering individualized dietary management at scale.

5. Sustainability Reporting Integration in Catering Contracts

Contract caterers increasingly provide measurable sustainability metrics such as carbon footprint, food waste reduction, and responsible sourcing, as ESG-driven procurement processes make environmental performance reporting a standard contractual requirement.

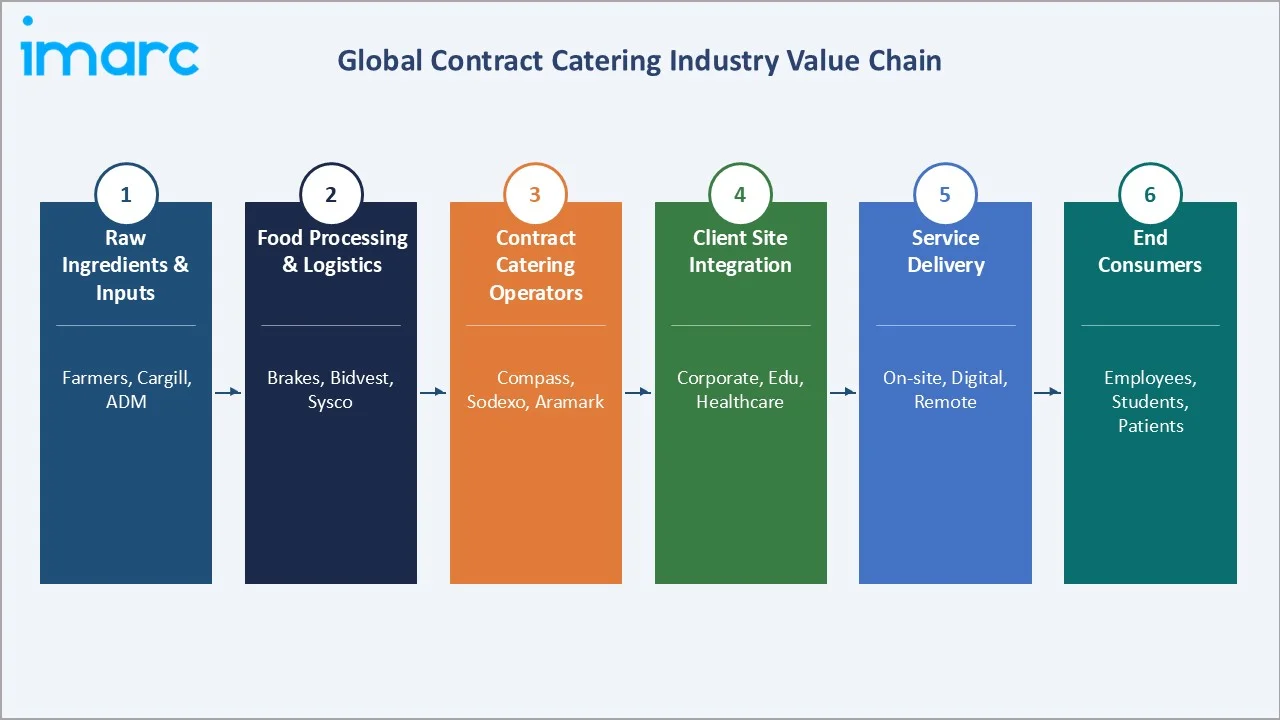

Industry Value Chain Analysis

The contract catering value chain covers six stages, from raw agricultural inputs to end-consumer meal delivery, each involving unique competitive dynamics, margin structures, and operational complexities.

|

Stage |

Key Players / Examples |

|

Raw Ingredients & Agricultural Inputs |

Farmers, commodity traders, food processors (Cargill, ADM, Sysco foodservice procurement) |

|

Food Manufacturing & Processing |

Prepared food manufacturers, dairy processors, meat processors, bakery suppliers |

|

Logistics & Cold Chain |

Refrigerated logistics providers, last-mile delivery specialists, wholesale distributors (Brakes, Bidvest) |

|

Contract Catering Operations |

Compass Group, Sodexo, Aramark, Elior Group, ISS A/S, Eurest, Cater 2, Genuine Dining |

|

Client Premises Integration |

Corporate offices, schools, hospitals, military bases, airports, sports venues |

|

End Consumers / Diners |

Employees, students, patients, military personnel, sports spectators, air travellers |

Tier-1 global caterers hold the highest value position by integrating sourcing, preparation, and service delivery. Their scale enables better supplier pricing, centralized menus, and technology investments unmatched by smaller operators.

Technology Landscape in the Contract Catering Industry

AI-Powered Menu Planning and Nutritional Optimization

AI platforms analyzing dietary preferences, nutrition targets, costs, and food waste are increasingly used by contract caterers, enabling dynamic menu optimization across multiple sites while improving satisfaction, compliance, and cost efficiency.

Smart Kitchen IoT and Equipment Connectivity

IoT-enabled kitchen equipment allows real-time food safety monitoring and operational control. Smart kitchen technologies improve consistency, enhance efficiency, and support energy optimization across large, geographically dispersed contract catering operations.

Digital Ordering, Cashless Payments, and Pre-Order Platforms

Mobile ordering, QR menus, and cashless payments are becoming standard in contract catering, improving throughput, reducing queues, and generating data that helps optimize menus, enhance forecasting, and reduce food waste.

Sustainability Analytics and ESG Reporting Platforms

Technology platforms measuring carbon emissions, food waste, and sustainable sourcing are gaining adoption as ESG reporting requirements grow. Leading operators like Compass Group and Sodexo now offer sustainability dashboards within client management portals.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Contract Type |

Fixed Price Contracts |

74.5% |

2025 |

|

Mode of Contract |

Outsourced |

78.5% |

2025 |

|

End User |

Business and Industry |

42.5% |

2025 |

|

Region |

Europe |

35.8% |

2025 |

By Contract Type

Fixed price contracts hold a 74.5% share in 2025, driven by institutional demand for pricing predictability and budget control. Caterers absorb input cost risks in exchange for stable, long-term revenue, favoring large, well-capitalized operators with strong procurement capabilities and operational scale.

To access detailed market analysis, Request Sample

Cost-plus contracts account for 25.5% in 2025, primarily used in sectors with high cost volatility such as offshore, military, and premium corporate catering, where maintaining quality and menu flexibility outweighs fixed-price cost constraints.

By Mode of Contract

Outsourced catering holds 78.5% of the global market in 2025, driven by organizations across corporate, healthcare, education, and government sectors increasingly outsourcing food services for operational efficiency and cost benefits.

Self-operated catering, holding 21.5% in 2025, remains common in sectors requiring strict operational control, cultural considerations, or high-security protocols, such as defense facilities and sensitive corporate campuses.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

35.8% |

Mature corporate catering markets in UK, France, Germany; strong regulatory framework; high outsourcing penetration rates |

|

North America |

27.6% |

Large employer food programs, university campus dining, healthcare outsourcing, technology company premium dining |

|

Asia Pacific |

22.4% |

Rapid urbanization, expanding corporate sectors, institutional feeding program investment, India and China workforce growth |

|

Latin America |

7.1% |

Brazil and Mexico corporate sector growth, expanding institutional food programs, growing mid-market catering demand |

|

Middle East & Africa |

7.1% |

GCC remote site catering, Vision 2030 infrastructure expansion, mining and energy sector offshore catering |

Europe commands a 35.8% global revenue share in 2025, reflecting its leadership in the contract catering market. The UK is one of the largest contracts catering markets and home to Compass Group. France hosts Sodexo, while Germany’s large corporate and industrial workforce drives strong catering demand, collectively strengthening Europe’s market leadership.

North America, with 27.6% in 2025, is driven by large U.S. employer dining programs, technology campuses, university food services, and healthcare outsourcing, supporting premium contract catering demand. Asia Pacific at 22.4% is the fastest-growing regional market, fueled by workplace dining expansion in India and large industrial and corporate catering demand across China, driving incremental growth through 2034.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Compass Group PLC |

Eurest / Restaurant Associates |

Leader |

Global scale, multi-sector, technology investment |

|

Sodexo S.A. |

Sodexo / Sodexo Live! |

Leader |

Integrated FM + catering, healthcare specialization |

|

Aramark Corporation |

Aramark / Aramark Refreshments |

Leader |

US campus & stadium, healthcare, corporate dining |

|

Elior Group S.A. |

Elior / Ansamble |

Leader |

European enterprise, education, senior care focus |

|

ISS A/S |

ISS / ISS Food Services |

Challenger |

Integrated FM services, Nordic and European base |

|

BaxterStorey Ltd |

BaxterStorey / Holroyd Howe |

Challenger |

Premium UK corporate and education catering |

|

LSG Group |

LSG Sky Chefs / Retail inMotion |

Challenger |

Airline and airport catering specialization |

|

Genuine Dining Co. |

Genuine Dining |

Emerging |

Independent premium UK workplace dining |

The contract catering market is led by a few global operators alongside fragmented regional players. Compass Group plc, the global leader, reported approximately USD 42.2 billion revenue in FY2024, supported by strong client relationships, broad geographic presence, and large-scale outsourcing capabilities.

Key Company Profiles

Compass Group PLC

Compass Group plc, headquartered in Chertsey, UK, is the world’s largest contract catering company, operating across 30 countries with approximately 580,000 employees. In FY2024, the company reported revenue of $42.2 billion, with 86% generated from Food Services and 14% from Support Services. Revenue contributions were led by Business & Industry (38%), followed by Healthcare & Senior Living (23%), while Education, Sports & Leisure, and Defence, Offshore & Remote collectively accounted for 39% of total revenue.

- Product & Service Portfolio: Eurest (Corporate Dining), Restaurant Associates (Premium Dining), Chartwells (Education), Morrison Healthcare, Levy (Sports & Entertainment), and Canteen (Vending & Micro-markets)

- Recent Developments: In January 2024, Compass Group agreed to acquire CH&CO for approximately £475 million to expand premium catering capabilities. The acquisition was completed in April 2024, adding brands including Gather & Gather, Vacherin, and Company of Cooks.

- Strategic Focus: Compass Group focuses on outsourcing growth, premium culinary brands, operational technology, and expansion in North America, Asia Pacific, and Europe through acquisitions and contract wins.

Sodexo S.A.

Sodexo is headquartered in Issy-les-Moulineaux, France, operating in 45+ countries. FY2024 revenue reached €23.8 billion, up +5.1% year-on-year, driven by organic growth of +7.9%.

- Product & Service Portfolio: On-site Food Services, Integrated Facilities Management, Healthcare & Senior Living Dining, Corporate Dining, and Education Catering.

- Recent Developments: Sodexo completed spin-off of Pluxee (Benefits & Rewards) in February 2024. Leadership Transition, Sodexo appointed Thierry Delaporte as Chief Executive Officer and implemented a separated governance structure in November 2025.

- Strategic Focus: Sodexo focuses on integrated services, healthcare catering, workplace dining, and sustainability-driven solutions supported by WasteWatch analytics and operational digitalization.

Aramark Corporation

Aramark is headquartered in Philadelphia, USA, providing food and facilities services across healthcare, education, business, and sports sectors, with revenues of approximately USD 17.4 Billion in FY2024.

- Product & Service Portfolio: Workplace Dining, Collegiate Dining, Healthcare Food Services, Sports & Entertainment Catering, Corrections Food Services, and International Food Services.

- Recent Developments: Aramark completed the spin-off of its Uniform Services business into Vestis in October 2023, allowing the company to focus on food and facilities management. In 2024, Aramark continued expanding collegiate dining operations, including new multi-year university partnerships such as the University of New Mexico dining services agreement.

- Strategic Focus: Aramark focuses on workplace dining innovation, sustainability, digital ordering, and campus dining modernization across North America and international markets.

Market Concentration Analysis

The global contract catering market is concentrated at the top tier, with Compass Group, Sodexo, and Aramark collectively accounting for 30–35% of global revenue in 2025, driven by scale advantages, broad geographic coverage, and significant technology investments required to secure large institutional contracts.

Market fragmentation increases at regional and local levels, with numerous independent and specialist caterers competing for smaller contracts, school programs, and niche sectors. This creates a bifurcated structure dominated by global leaders at the top while mid- and lower-tier markets remain highly fragmented, typical of mature outsourced services industries.

Consolidation trends continue through acquisition activity, with Compass Group's acquisition of CH&CO in 2024 exemplifying the strategy of global leaders absorbing premium regional independents to upgrade geographic coverage and service capabilities. ESG compliance requirements and technology investment necessities are further accelerating consolidation pressure on smaller operators.

Investment & Growth Opportunities

Fastest-Growing Segments

Healthcare and senior care catering is emerging as a high-growth contract catering segment through 2034, driven by aging populations in Europe, North America, and Japan. Demand for therapeutic nutrition, specialized meals, and clinical compliance is increasing. The global population aged 65+ is projected to reach 1.6 billion by 2050, supporting long-term institutional catering demand.

Asia Pacific emerging markets, including India, Indonesia, Vietnam, and the Philippines, represent the fastest-growing contract catering opportunity, driven by rapid urbanization and corporate expansion. India's working age population will increase another 63 million by 2030 and 128 million by 2040, with approximately 115 million new jobs expected by 2030, while expanding institutional food programs further support long-term contract catering demand.

Emerging Market Expansion

The Middle East and Africa region – currently at 7.1% of global share in 2025 – offers significant growth opportunity through remote site, oil and gas offshore catering, and GCC infrastructure program feeding contracts. Saudi Arabia's Vision 2030 construction program alone encompasses multiple large-scale infrastructure projects requiring remote site catering services across multi-year contract periods.

Venture & Strategic Investment Trends

Investment activity in food technology platforms applicable to contract catering is intensifying. AI-driven menu optimization, food waste management platforms (Winnow, Leanpath), digital ordering ecosystems, and sustainable packaging suppliers are attracting venture capital and strategic corporate investment from major catering operators seeking technology differentiation.

Future Market Outlook (2026-2034)

The global contract catering market forecast projects sustained value expansion from USD 280.6 Billion in 2025 to USD 408.3 Billion by 2034 at a CAGR of 4.1% – representing a value increase of over USD 127 Billion through the forecast period. Growth will be driven by emerging market penetration, healthcare sector expansion, technology-enabled service differentiation, and the ongoing structural shift from self-operated to outsourced food service management.

Three transformational trends will reshape contract catering through 2034. AI-powered personalized nutrition will enable tailored meals at scale, while carbon-neutral catering commitments will influence sourcing and supplier selection. Additionally, digital platform convergence integrating catering, facilities, and employee services will create bundled workplace experience solutions and redefine traditional contract catering boundaries. These developments will drive operational efficiency, sustainability compliance, and service differentiation across institutional catering markets.

By 2034, contract catering is expected to evolve from traditional food preparation into a technology-driven, sustainability-focused, and personalized service model. Operators investing in AI, digital platforms, and sustainability capabilities are likely to gain competitive advantage and capture higher-value opportunities across corporate, healthcare, and education segments.

Research Methodology

Primary Research

Primary research encompassed structured interviews and surveys conducted in 2024–2025 with contract catering industry stakeholders including senior procurement officers at Fortune 500 corporate clients, operational directors at Tier-1 catering operators, food service consultants, institutional facility managers, and nutritional services directors at healthcare and education clients.

Secondary Research

Secondary sources include company annual reports (Compass Group, Sodexo, Aramark, Elior), trade association publications (British Hospitality Association, NRA, FARE), government institutional food program data (UK Education Act, USDA School Meals Program), food safety regulatory publications (EU Food Safety Authority, FDA), and industry trade media including Contract Catering Magazine and Nation's Restaurant News.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, institutional sector employment data, outsourcing penetration trends, historical market evolution analysis, and scenario analysis under base, optimistic, and conservative macroeconomic assumptions.

Contract Catering Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Contract Types Covered | Fixed Price Contracts, Cost Plus Contracts |

| Mode of Contracts Covered | Outsourced, Self-Operated |

| End Users Covered | Business and Industry, Education, Healthcare and Senior Care, Defence and Offshore, Sports and Leisure, Airports, Others |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Turkey, Saudi Arabia |

| Companies Covered | Compass Group PLC, Sodexo S.A., Aramark Corporation, Elior Group S.A., ISS A/S, BaxterStorey Ltd, LSG Group, Genuine Dining Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the contract catering market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global contract catering market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the contract catering industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Contract Catering Market Report

The global contract catering market was valued at USD 280.6 Billion in 2025, driven by rising institutional outsourcing, corporate food service expansion, and growing demand for nutritious dining solutions.

The market is projected to reach USD 408.3 Billion by 2034, growing at a CAGR of 4.1% during 2026-2034, driven by healthcare catering growth, Asia Pacific expansion, and digital platform adoption.

Fixed Price Contracts lead with a 74.5% share in 2025, driven by institutional clients' preference for budget predictability and long-term financial planning across multi-year service agreements.

Outsourced mode commands a 78.5% share in 2025, driven by organizations seeking specialist expertise, economies of scale, and technology capabilities unavailable through self-operated food service models.

Europe leads with a 35.8% share in 2025, anchored by the UK, France, and Germany's mature corporate catering ecosystems, high outsourcing penetration, and leading global contract catering operator headquarters.

Key drivers include rising corporate outsourcing, health-driven menu demand, sustainability mandates, digital food service transformation, healthcare sector growth, and institutional feeding program expansion.

Asia Pacific is the fastest-growing region, driven by rapid urbanization, corporate sector expansion, India's institutional food programs, and China's industrial campus catering demand growth through 2034.

Leading companies include Compass Group PLC, Sodexo S.A., Aramark Corporation, Elior Group, ISS A/S, BaxterStorey, LSG Group, and Genuine Dining Company.

Cost Plus Contracts hold a 25.5% share in 2025, primarily serving remote offshore sites, premium executive dining, and sectors where ingredient cost variability makes fixed-price risk management impractical.

Outsourced catering growth is driven by operational efficiency benefits, access to culinary expertise, technology platforms, sustainable sourcing capabilities, and regulatory compliance management offered by specialist providers.

AI menu planning, digital ordering, smart kitchens, and sustainability analytics are improving contract catering efficiency, reducing food waste by 20–40% and enhancing diner satisfaction.

Business and Industry represents the largest end-user segment, driven by large corporate campus dining, employee food program outsourcing, and technology company premium food benefit offerings globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)