Contrast Media Market Report by Type (Iodinated Contrast Media, Gadolinium-based Contrast Media, Microbubble Contrast Media, Barium-based Contrast Media), Modality (X-ray/Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound), Application (Radiology, Interventional Radiology, Interventional Cardiology), Route of Administration (Intravenous/Intrarterial, Oral Route, Rectal Route, and Others), End User (Hospital, Clinics and Ambulatory Surgery Centers, Diagnostic Imaging Centers), and Region 2026-2034

Global Contrast Media Market:

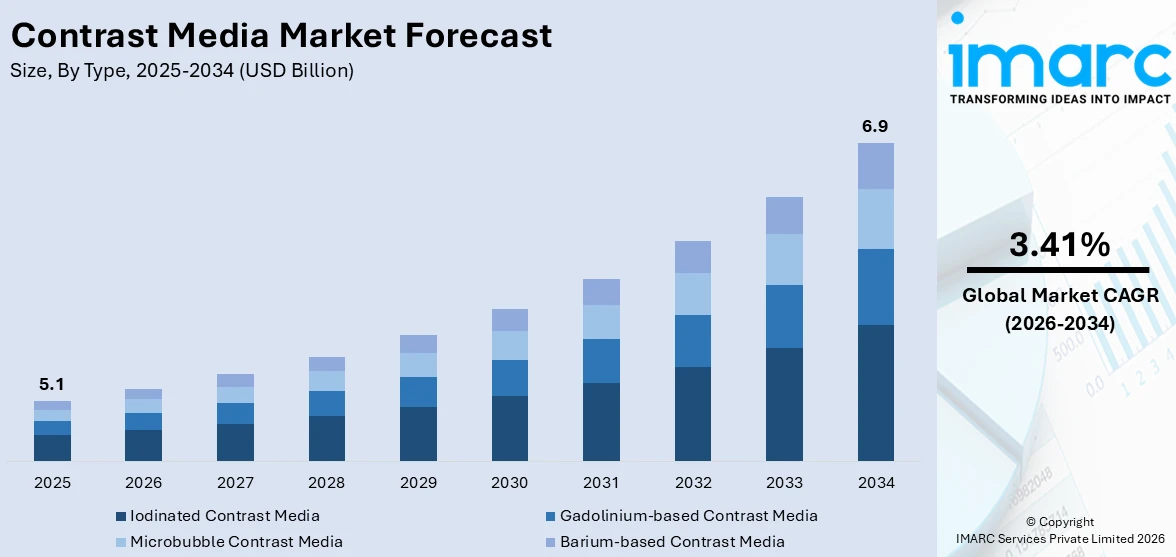

The global contrast media market size reached USD 5.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 6.9 Billion by 2034, exhibiting a growth rate (CAGR) of 3.41% during 2026-2034. North America exhibits a clear dominance in the market, attributed to the escalating demand for radiopharmaceuticals. Moreover, the increasing demand for diagnostic imaging procedures, owing to the growing prevalence of neurological, cancer, and cardiovascular diseases, is one of the key factors stimulating the market growth.

Market Size & Forecasts:

- Contrast media market was valued at USD 5.1 Billion in 2025.

- The market is projected to reach USD 6.9 Billion by 2034, at a CAGR of 3.41% from 2026-2034.

Dominant Segments:

- Type: Iodinated contrast media exhibits a clear dominance in the market as it contains iodine atoms, which can be used for x-ray-based imaging modalities, such as computed tomography (CT).

- Modality: X-ray/computed tomography (CT) accounts for the majority of the total market share propelled by the inflating popularity of diagnostic imaging procedures.

- Application: Interventional cardiology currently holds the largest market share, owing to the escalating demand for techniques, such as coronary angiography and percutaneous coronary interventions (PCI), which widely rely on contrast media to visualize the heart's vascular structure and function.

- Route of Administration: Intravenous/intrarterial route exhibits a clear dominance in the contrast media market share, owing to their effectiveness in delivering contrast agents directly into the bloodstream, thereby ensuring rapid distribution throughout the targeted organs or body.

- Region: North America leads the market due to the presence of major pharmaceutical companies and regulatory support from bodies like the FDA.

Key Players:

- The leading companies in the market include Bayer AG, Beijing Beilu Pharmaceuticals Company Limited, Bracco Group, FUJIFILM Sonosite, Inc., GE HealthCare, Guerbet, iMAX, JB Pharma, Jodas Expoim Pvt. Ltd., Lantheus, SANOCHEMIA Pharmazeutika GmbH, TAEJOON PHARM Co. Ltd., Trivitron Healthcare, etc.

Key Drivers of Market Growth:

- Increasing Diagnostic Imaging Procedures: The increase in diagnostic imaging, such as MRI, CT, and X-ray procedures, is driving the constant use of contrast agents to provide more distinct images and enhance diagnostic capabilities.

- Increasing Prevalence of Chronic Diseases: The growing occurrence of chronic ailments like cancer, cardiovascular disease, and neurological disorders is necessitating sustained use of contrast-enhanced imaging for effective diagnosis and monitoring of treatment.

- Technological Developments: Consecutive advancements in contrast media compositions, such as the creation of safer and more effective agents with fewer side effects, are improving clinical results and widening their scope of application.

- Increasing Healthcare Infrastructure: Repeated investments in healthcare facilities, especially in developing countries, are making more sophisticated diagnostic services accessible, thus increasing the demand for contrast media.

- Positive Reimbursement Policies: Governments and commercial payers are favorably supporting diagnostic imaging procedures via reimbursement programs, leading to continued use of contrast agents within regular clinical practice.

Future Outlook:

- Strong Growth Outlook: Contrast media business is witnessing steady growth with favorable global healthcare expenditure, growing diagnostic capabilities, and technological improvements in imaging technologies.

- Market Evolution: The business is ever-developing, with contrast agents becoming more and more incorporated into precision medicine and interventional care, opening the door to broader application across clinical specialties and geographies.

Contrast media market is experiencing dynamic evolution, and various trends are driving its current and future path. Regulatory organizations are making regulations stricter regarding the safety, efficacy, and environmental toxicity of contrast agents. Producers are embracing compliance by incorporating sustainable production methodologies and enhancing waste control mechanisms. Gadolinium retention in the environment issues are inviting more scrutiny, paving the way for biodegradable and reduced-dose formulations. Organizations are aligning their businesses with changing regulatory paradigms to maintain long-term market sustainability. As the healthcare sector is transitioning toward outpatient procedures, imaging centers and ambulatory service providers are emerging as principal end users of contrast media. Such imaging centers are placing emphasis on high-throughput imaging services based on fast-acting and economical contrast agents. Suppliers are also modifying their product lines to address the service requirements of outpatient clinics, focusing on convenience, storage space, and quick patient turnaround.

To get more information on this market Request Sample

Contrast Media Industry Trends:

Rising Use of Diagnostic Imaging Studies

The healthcare systems of the world are conducting more diagnostic imaging tests, such as computed tomography (CT) scans, X-rays, magnetic resonance imaging (MRI), and ultrasounds, as a routine part of clinical evaluation. Diagnostic centers and hospitals are increasingly using contrast-enhanced studies to obtain better visualization of internal organs, blood vessels, and disease processes. Physicians are making more use of contrast agents to enhance the sensitivity and specificity of imaging findings, thus enhancing diagnosis and treatment planning. This increased demand for imaging is based on the aging population, rise in chronic disease incidence, and greater emphasis on preventive medicine. With medical imaging increasingly becoming an important part of contemporary medicine, contrast medium consumption is growing correspondingly. Another crucial aspect is that advances in imaging technologies are also being incorporated into clinical practices by healthcare providers. As per World Health Organization (WHO), worldwide, life expectancy at birth hit 73.3 years in 2024, a rise of 8.4 years since 1995. The global population of individuals aged 60 and above is expected to reach 1.4 billion by 2030. This trend is further going to drive the need for efficient diagnostic imaging solutions for the geriatric population.

Increasing Incidence of Chronic and Lifestyle Diseases

The burden of chronic and lifestyle-related diseases, such as cancer, cardiovascular disorders, diabetes, and neurological complications is being managed by the healthcare sector of the world. Doctors are increasingly using contrast-enhanced imaging to diagnose, monitor, and treat such diseases more efficiently. In oncology, for example, contrast agents are assisting radiologists in defining tumor margins, metastatic extent, and treatment response more clearly. In cardiology, contrast media are assisting in the assessment of coronary artery diseases, cardiac perfusion, and structural disorders. Neurological illnesses like stroke and multiple sclerosis are also necessitating contrast imaging for their proper evaluation and monitoring. With these long-term illnesses becoming increasingly common due to factors like aging populations, sedentary lifestyles, and environmental issues, demand for cutting-edge diagnostic imaging is gaining traction. This increase in disease burden is encouraging healthcare providers to make investments in imaging capacities, thereby constantly facilitating the development of the contrast media market in various regions of the world and varying healthcare systems. In 2024, A research group from IOCB Prague, in partnership with the University of Tübingen in Germany and the Faculty of Science at Charles University, created a novel type of contrast agent suitable for use in both magnetic resonance imaging (MRI) and positron emission tomography (PET). This advancement addressed a significant challenge that had formerly obstructed the combination of these two imaging methods into one device.

Innovation in Contrast Agent Formulations

Pharma companies are proactively investing in research and development (R&D) to develop more sophisticated, safer, and targeted contrast media formulations. Researchers are creating low-osmolar and iso-osmolar iodine-based agents, macrocyclic gadolinium-based agents, and biodegradable microbubble agents with better safety profiles and fewer adverse effects. These innovations are reducing the risk of complications like contrast-induced nephropathy and nephrogenic systemic fibrosis, particularly in patients with impaired renal function. Researchers are also designing agents with greater imaging accuracy and quicker clearance from the body. The growth of targeted and molecular contrast agents for particular disease indicators is also enhancing diagnostic precision. These progressive developments are allowing better personalized and effective imaging, improving patient outcomes and clinical decision-making. IMARC Group predicts that the global precision diagnostics market is projected to attain USD 207.0 Billion by 2033.

Contrast Media Market Growth Drivers:

Development of Healthcare Infrastructure in Emerging Markets

The emerging markets are witnessing fast-paced healthcare change through rising government expenditure, private investment, and global aid. Diagnostic centers and hospitals in these markets are increasing their capabilities by making investments in advanced imaging technology and adding contrast-enhanced procedures to everyday use. Governments are also introducing public health programs that include early disease detection, which is stimulating broader applications of diagnostic imaging. Improved access to affordable health insurance and expanding middle classes are also facilitating access to quality healthcare services, such as contrast-based diagnostics. With the growth of healthcare infrastructure, demand for contrast media is rising. Pharmaceutical firms are countering by entering the markets, establishing local alliances, and offering products aligned to local needs.

Artificial Intelligence (AI) and Imaging Technology integration

Medical imaging is undergoing digitalization, with artificial intelligence (AI) and machine learning (ML) technologies increasingly forming an integral part of diagnostic practice. Radiologists and imaging facilities are increasingly adopting AI to improve image interpretation, streamline repetitive tasks, and maximize contrast agent usage. AI algorithms are assisting with accurate quantification of contrast uptake, enabling clinicians to determine optimal contrast dosage according to patient-specific features. These devices are also enhancing early abnormal detection, minimizing human mistake, and optimizing overall imaging efficiency. Machine manufacturers are steadily incorporating AI functionality into CT, MRI, and ultrasound machines, allowing real-time feedback and automatic adjustment of image parameters. This technology convergence is enhancing diagnostic performance while minimizing contrast agent volume, supporting both cost-effectiveness and patient safety.

Growing Demand for Minimally Invasive and Image-Guided Interventions

Minimally invasive interventions are increasingly becoming the treatment method of choice in a vast majority of clinical situations because they have shorter recovery times, fewer complications, and fewer hospital stays. Interventional radiology, specifically, is picking up pace as doctors carry out image-guided procedures like angiography, embolization, biopsy, and stent placement. Such procedures depend significantly on contrast media to obtain real-time imaging of internal structure and to direct instruments with high accuracy. Hospitals and surgical centers are constantly increasing their capabilities in interventional radiology and endovascular therapies, raising the use of contrast agents in both diagnostic and therapeutic applications. This trend is driven by technological advances in imaging technologies and procedure-specific contrast preparations. As minimally invasive methods become routine practice in ever more medical specialties, the need for contrast-enhanced imaging is increasing.

Contrast Media Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with the contrast media market forecast at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on the type, modality, application, route of administration, and end user.

Breakup by Type:

- Iodinated Contrast Media

- Gadolinium-based Contrast Media

- Microbubble Contrast Media

- Barium-based Contrast Media

Among these, iodinated contrast media currently exhibits a clear dominance in the market

The report has provided a detailed breakup and analysis of the market based on the type. This includes iodinated contrast media, gadolinium-based contrast media, microbubble contrast media, and barium-based contrast media. According to the report, iodinated contrast media represented the largest segmentation.

Iodinated contrast media refer to contrast agents that contain iodine atoms used for x-ray-based imaging modalities, such as computed tomography (CT). Moreover, they can also be used in angiography, venography, fluoroscopy, and even occasionally, plain radiography. Besides this, key players are launching iodinated contrast media agents, as they enhance the diagnostic capabilities of CT and other radiographic imaging techniques. For example, in July 2022, Fresenius Kabi introduced the generic iodinated contrast media agent to alleviate the shortage. In addition to this, in October 2022, GE Healthcare entered into a long-term agreement with Chile-based mining company Sociedad Quimica y Minera de Chile S.A. (SQM) to secure its supply of iodine, a key ingredient for contrast media products used in computed tomography (CT) procedures globally.

Breakup by Modality:

- X-ray/Computed Tomography (CT)

- Magnetic Resonance Imaging (MRI)

- Ultrasound

Currently, X-ray/computed tomography (CT) accounts for the majority of the total market share

The report has provided a detailed breakup and analysis of the market based on the modality. This includes x-ray/computed tomography (CT), magnetic resonance imaging (MRI), and ultrasound. According to the report, x-ray/computed tomography (CT) represented the largest segmentation.

The growth in this segmentation is propelled by the inflating popularity of diagnostic imaging procedures. Additionally, these imaging techniques are fundamental in medical diagnostics due to their ability to provide quick, detailed views of the body's internal structures, thereby making them crucial for the early diagnosis, detection, and management of diseases. Besides this, various technological advancements in X-ray and CT imaging technologies to expand their application in clinical practice are elevating the contrast media market prices. For instance, in September 2023, Smiths Detection developed its HI-SCAN 6040 CTiX, an advanced cabin baggage screening system based on computed tomography (CT) technology, for the market across India. Similarly, in November 2023, Annalise.ai introduced the Annalise Triage software platform for chest X-rays and non-contrast head CT.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

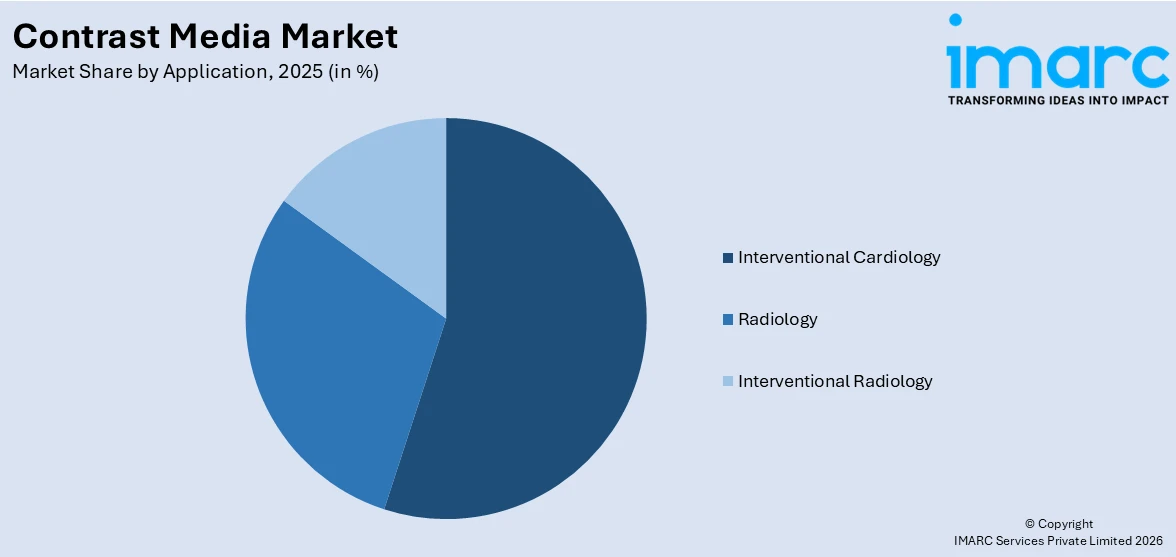

- Radiology

- Interventional Radiology

- Interventional Cardiology

Among these, interventional cardiology currently holds the largest market share

The report has provided a detailed breakup and analysis of the market based on the application. This includes radiology, interventional radiology, and interventional cardiology. According to the report, interventional cardiology represented the largest segmentation.

The escalating demand for techniques, such as coronary angiography and percutaneous coronary interventions (PCI), which widely rely on contrast media to visualize the heart's vascular structure and function, is stimulating the segment's growth. Furthermore, the increasing prevalence of cardiovascular diseases, coupled with advancements in cardiac imaging technologies, are increasing the number of these procedures. Apart from this, the launch of medical programs related to interventional cardiology will continue to bolster the market in the coming years. For example, in May 2024, the Society for Cardiovascular Angiography & Interventions (SCAI) started its SCAI scientific sessions in Long Beach, California, bringing together more than 1,800 researchers, clinicians, and innovators in the field of interventional cardiology and endovascular medicine.

Breakup by Route of Administration:

- Intravenous/Intrarterial

- Oral Route

- Rectal Route

- Others

Currently, intravenous/intrarterial route exhibits a clear dominance in the contrast media market share

The report has provided a detailed breakup and analysis of the market based on the route of administration. This includes intravenous/intrarterial, oral route, rectal route, and others. According to the report, intravenous/intrarterial route represented the largest market segmentation.

The intravenous and intraarterial routes of administration find widespread applications, owing to their effectiveness in delivering contrast agents directly into the bloodstream, thereby ensuring rapid distribution throughout the targeted organs or body. This method is pivotal for enhancing the clarity of images in several diagnostic imaging procedures, including MRI, CT scans, and angiography. The intravenous route is particularly prevalent because it can be used for a wide range of imaging studies that require a systemic distribution of the contrast agent and is relatively easy to administer. For instance, in May 2023, Guerbet, one of the global leaders in medical imaging, announced that based on the scientific and clinical evidence, the ACR Committee on Drugs and Contrast Media classified elucirem as a Group II agent.6 and indicated for use in adults and children aged two years and older. On the other hand, the intraarterial route offers a more targeted approach. It is used in procedures, including coronary angiograms, where the contrast media is injected directly into the arteries of the heart to obtain detailed images of the coronary circulation.

Breakup by End User:

- Hospital, Clinics and Ambulatory Surgery Centers

- Diagnostic Imaging Centers

The report has provided a detailed breakup and analysis of the market based on the end-user. This includes hospital, clinics, and ambulatory surgery centers and diagnostic imaging centers.

According to the contrast media market research report, the availability of advanced imaging equipment across hospitals is acting as a significant growth-inducing factor. In addition to this, clinics, particularly those specializing in specific fields like cardiology or oncology, use contrast media for targeted diagnostic purposes. Moreover, ambulatory surgery centers extensively adopt imaging technologies that require contrast media, particularly for preoperative and postoperative assessments. Besides this, diagnostic imaging centers cater to both referrals from hospitals and smaller clinics.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance in the market

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

The expanding healthcare infrastructures and a high rate of medical imaging procedures are driving the regional market. For example, in April 2024, the Northwest Imaging Forums (NWIF) and International Contrast Ultrasound Society (ICUS) announced an educational partnership to aid in training sonographers to perform contrast-enhanced ultrasound (CEUS) examinations and administer intravenous ultrasound contrast agents. Besides this, the presence of major pharmaceutical companies is also acting as another significant growth-inducing factor. For instance, in September 2023, Philips introduced the microvascular imaging super resolution contrast-enhanced ultrasound (CEUS), which was showcased at the International Bubble Conference in Chicago. Furthermore, regulatory support from bodies like the FDA also plays a crucial role in the swift approval and adoption of new contrast agents, which is expected to fuel the regional market in the coming years. For example, in August 2023, Fresenius Kabi, a German healthcare company with headquarters in Illinois, launched an FDA-approved generic substitute for Gadavist, the gadolinium-based contrast agent commonly used during MRI exams.

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Bayer AG

- Beijing Beilu Pharmaceuticals Company Limited

- Bracco Group

- FUJIFILM Sonosite, Inc.

- GE HealthCare

- Guerbet

- iMAX

- JB Pharma

- Jodas Expoim Pvt. Ltd.

- Lantheus

- SANOCHEMIA Pharmazeutika GmbH

- TAEJOON PHARM Co. Ltd.

- Trivitron Healthcare

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Contrast Media Market News:

- June 2025: Fresenius Kabi Canada, a member of the Fresenius group, announced the introduction of Iodixanol Injection 270 and 320 for intravenous and intra-arterial use. Iodixanol Injection serves as a contrast medium employed in angiocardiography, arteriography, CT imaging of the head and body, excretory urography, and venography. Health Canada's NOC authorization of Iodixanol Injection 270 & 320 was awarded on December 17, 2024, following an extensive review of a detailed data set showing pharmaceutical equivalence to the reference medication Visipaque®.

- June 2025: The U.S. Food and Drug Administration (FDA) has broadened the application of Polarean's Xenoview to incorporate children beginning at age 6. The xenon (Xe)-129 gas blend, a hyperpolarized contrast agent for MRI, is an inhalant utilized in assessing lung ventilation in both adults and pediatric patients from the age of 12. According to the company, broadening the indications to cover patients aged 6 and above will raise the number of eligible individuals by around one million.

- May 2025: GE HealthCare has revealed plans to expand its radiation oncology portfolio and to launch the new AI-integrated MR Contour DL at the European Society for Therapeutic Radiology and Oncology (ESTRO) 2025 Congress in Vienna, Austria. The company will present its enhanced Intelligent Radiation Therapy (iRT), a software solution that streamlines intricate workflows, facilitating a quicker transition from diagnosis to treatment and allowing for more accurate radiation therapy.

- April 2025: Bayer and Siemens Healthineers launched multiple innovative diagnostic imaging technologies at the "Expanding the Future of Care" event in Vietnam, attracting almost 120 prominent healthcare professionals, including important representatives from the Vietnam Society of Radiology and Nuclear Medicine and significant hospitals nationwide. MEDRAD® Centargo incorporates state-of-the-art technology that minimizes manual interventions by radiologists and radiographers, facilitating the development of tailored contrast media protocols for accurate dosing and timing.

- February 2025: GE Healthcare announced that it will invest $138 million to enhance a contrast media fill and finish production facility in Ireland. The company is constructing the facility on the premises of an existing location to facilitate the manufacturing of an additional 25 million patient doses annually of contrast media imaging agents by the conclusion of 2027.

- May 2024: A team of researchers led by Professor Cheon Jinwoo, the director of the Center for Nanomedicine (CNM), and Professor Choi Byoung Wook from the Yonsei University College of Medicine developed a high-performance, nanoparticle-based MRI contrast agent, Supramolecular Amorphous-like Iron Oxide (SAIO), for 3D vascular mapping.

- April 2024: Researchers at the University of Michigan accomplished high-resolution and efficient 3D chemical imaging for the first time at the one-nanometer scale.

- March 2024: Samsung Medison and Bracco Imaging entered a Memorandum of Understanding (MoU) agreement to pioneer a new area for diagnostic ultrasound devices and contrast agents at the European Congress of Radiology.

Contrast Media Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Iodinated Contrast Media, Gadolinium-based Contrast Media, Microbubble Contrast Media, Barium-based Contrast Media |

| Modality Covered | X-ray/Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound |

| Applications Covered | Radiology, Interventional Radiology, Interventional Cardiology |

| Route of Administration Covered | Intravenous/Intrarterial, Oral Route, Rectal Route, Others |

| End Users Covered | Hospital, Clinics and Ambulatory Surgery Centers, Diagnostic Imaging Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bayer AG, Beijing Beilu Pharmaceuticals Company Limited, Bracco Group, FUJIFILM Sonosite, Inc., GE HealthCare, Guerbet, iMAX, JB Pharma, Jodas Expoim Pvt. Ltd., Lantheus, SANOCHEMIA Pharmazeutika GmbH, TAEJOON PHARM Co. Ltd., Trivitron Healthcare, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the contrast media market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global contrast media market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the contrast media industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Contrast Media Market Report

The global contrast media market was valued at USD 5.1 Billion in 2025.

We expect the global contrast media market to exhibit a CAGR of 3.41% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic had led to postponement of elective treatment for neurological and cardiovascular diseases to reduce the risk of the coronavirus infection upon hospital visits or interaction with healthcare professionals, thereby negatively impacting the global market for contrast media.

The rising prevalence of various chronic medical disorders, along with the advent of digital solutions for precise and effective management of contrast media, is primarily driving the global contrast media market.

Based on the type, the global contrast media market has been divided into iodinated contrast media, gadolinium-based contrast media, microbubble contrast media, and barium-based contrast media. Among these, iodinated contrast media currently exhibits a clear dominance in the market.

Based on the modality, the global contrast media market can be categorized into x-ray/Computed Tomography (CT), Magnetic Resonance Imaging (MRI), and ultrasound. Currently, x-ray/Computed Tomography (CT) accounts for the majority of the total market share.

Based on the application, the global contrast media market has been segregated into radiology, interventional radiology, and interventional cardiology. Among these, interventional cardiology currently holds the largest market share.

Based on the route of administration, the global contrast media market can be bifurcated into intravenous/intrarterial, oral route, rectal route, and others. Currently, intravenous/intrarterial route exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global contrast media market include Bayer AG, Beijing Beilu Pharmaceuticals Company Limited, Bracco Group, FUJIFILM Sonosite, Inc., GE HealthCare, Guerbet, iMAX, JB Pharma, Jodas Expoim Pvt. Ltd., Lantheus, SANOCHEMIA Pharmazeutika GmbH, TAEJOON PHARM Co. Ltd., and Trivitron Healthcare.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)