Cooling Tower Market Size, Share, Trends and Forecast by Tower Type, Flow Type, Design, Construction Material, End-User, and Region 2026-2034

Global Cooling Tower Market Size, Share, Trends & Forecast (2026-2034)

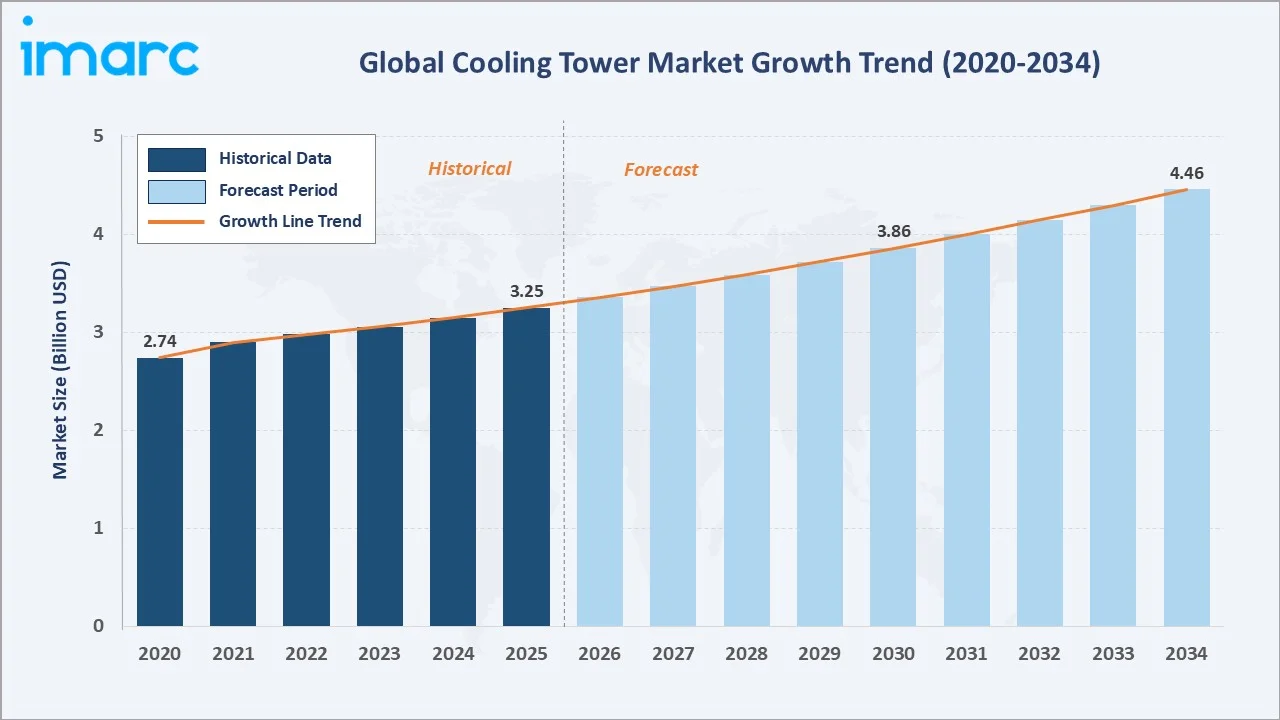

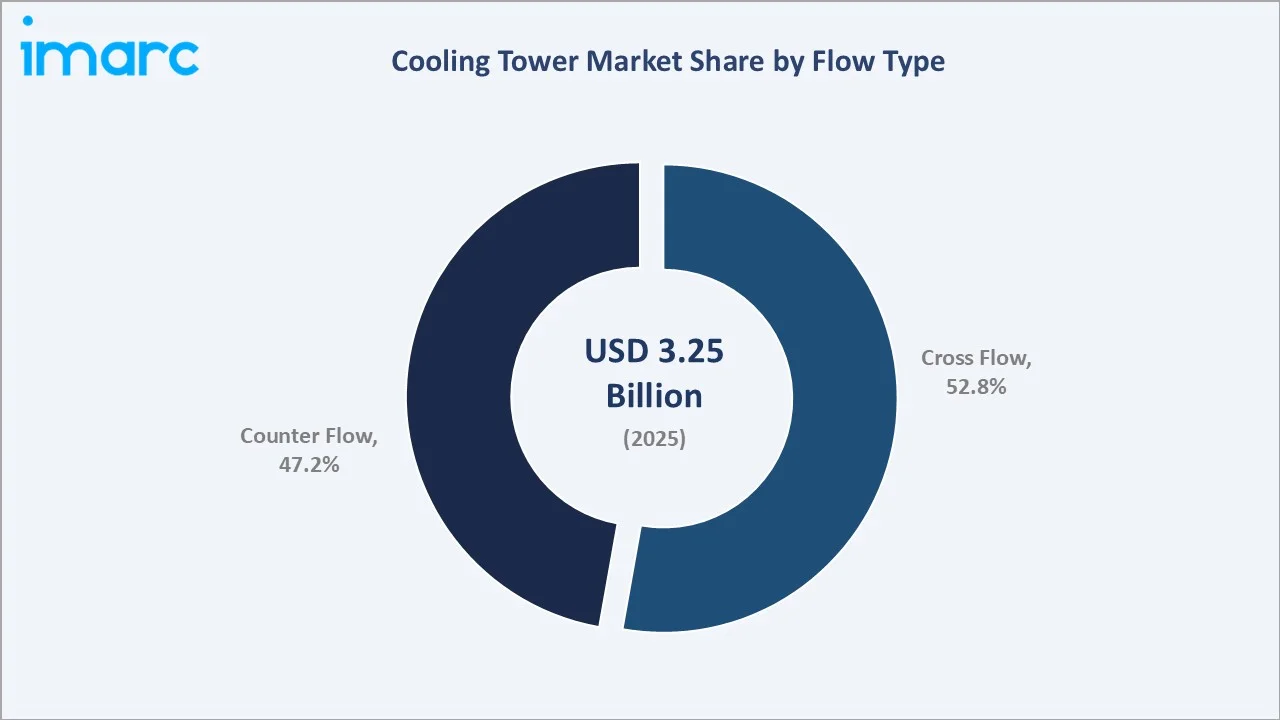

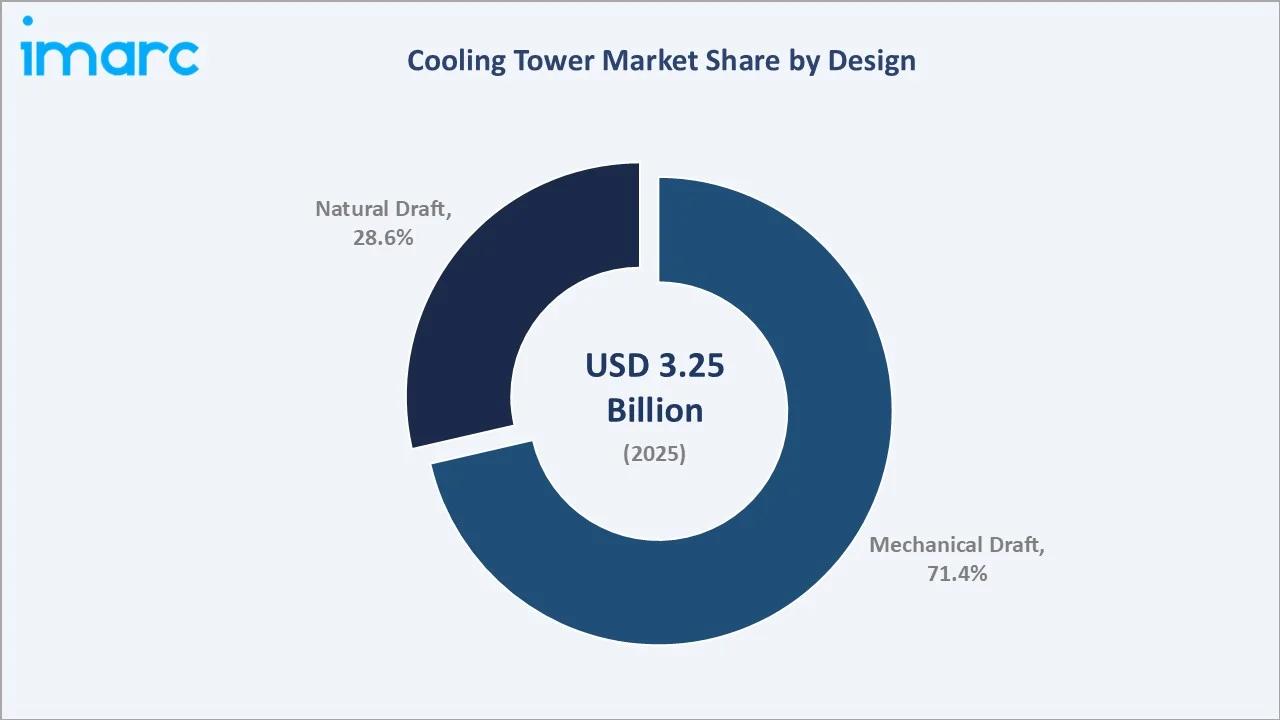

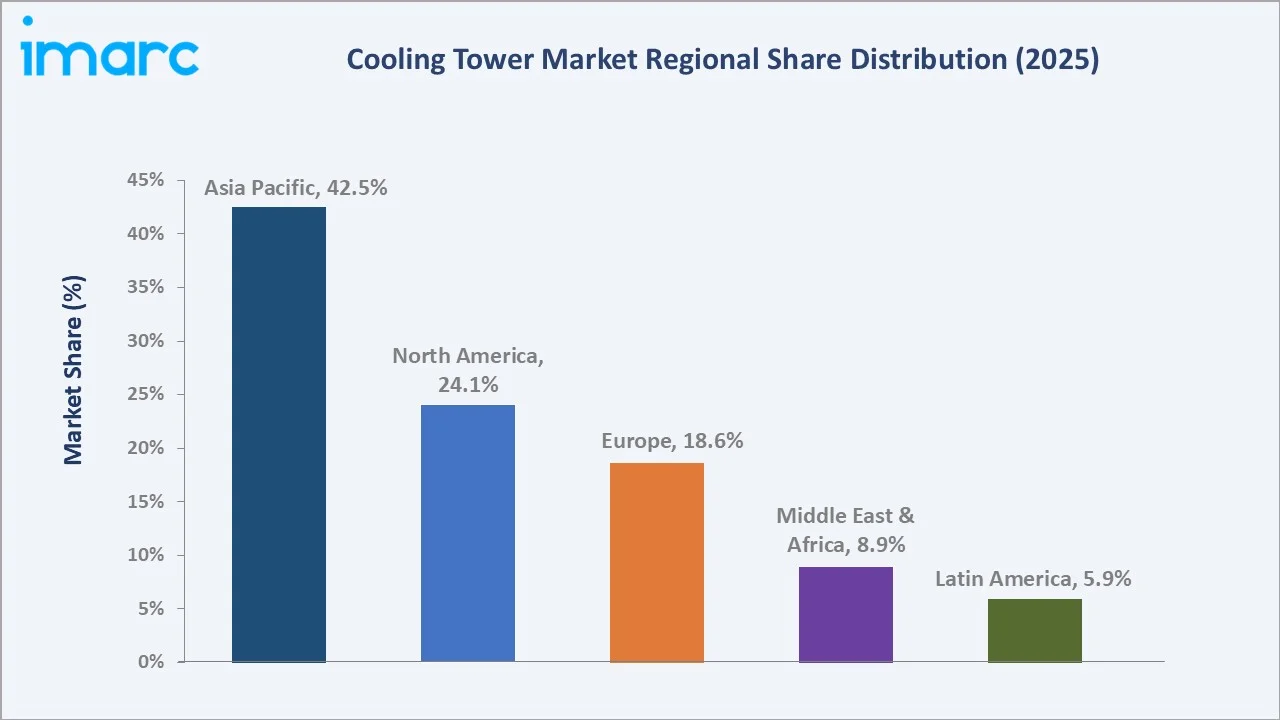

The global cooling tower market size was valued at USD 3.25 Billion in 2025 and is projected to reach USD 4.46 Billion by 2034, exhibiting a CAGR of 3.48% during the forecast period 2026-2034. Rising industrial cooling demand across power generation, surging HVAC adoption in commercial construction, with global electricity demand rising 4.3% in 2024 per IEA, the rapid growth of hyperscale data centers with operational capacity exceeding 40 GW in 2024, and increasing investments in water-efficient and energy-saving tower designs are driving the cooling tower market growth. Cross Flow leads flow type at 52.8% in 2025, while Mechanical Draft dominates the design segment at 71.4%. Asia Pacific accounts for 42.5% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.25 Billion |

|

Forecast Market Size (2034) |

USD 4.46 Billion |

|

CAGR (2026-2034) |

3.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (42.5% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Flow Type |

Cross Flow (52.8%, 2025) |

|

Leading Design |

Mechanical Draft (71.4%, 2025) |

The global cooling tower market growth trajectory from 2020 through 2034, contrasting a steady historical expansion base against a sustained forecast curve powered by industrial capex recovery, rising power sector investments, hyperscale data center build-out, and water-efficient tower adoption.

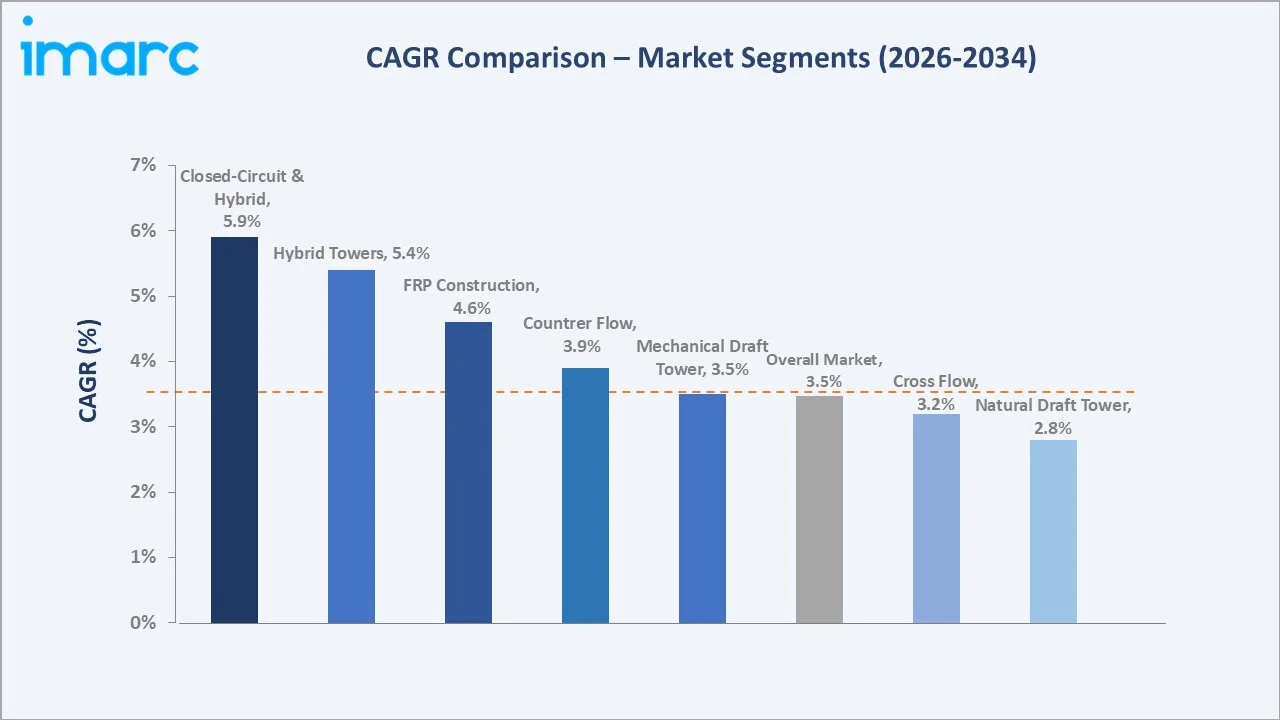

Segment-level share comparisons highlighting closed-circuit and hybrid cooling towers as the fastest-growing sub-categories within the global cooling tower industry analysis through 2034.

Executive Summary

The global cooling tower market is undergoing steady expansion, driven by the convergence of industrial electrification, rising thermal management needs in data centers, and water-efficient cooling infrastructure modernization. Valued at USD 3.25 Billion in 2025, the market is forecast to reach USD 4.46 Billion by 2034 at a CAGR of 3.48%.

Cross Flow commands the dominant flow-type share at 52.8% in 2025, driven by its low-maintenance configuration, gravity-fed water distribution, ease of access to internal components, and strong fit with large-scale HVAC and process cooling installations. Counter Flow at 47.2% remains highly competitive, preferred in applications requiring higher thermal performance, smaller footprint, and improved water conservation across chemical, refinery, and data center sites.

Asia Pacific dominates with a 42.5% global revenue share in 2025, led by China, the world's largest power producer with over 1,400 GW of installed thermal capacity, alongside India's rapid HVAC expansion and ASEAN petrochemical build-out. North America holds 24.1% in 2025, and Europe 18.6%, with both regions anchored by data center procurement, aging power plant retrofits, and strict water-use and Legionella compliance mandates that favor hybrid and closed-circuit tower configurations.

Key Market Insights

|

Insight |

Data |

|

Largest Flow Type |

Cross Flow - 52.8% share (2025) |

|

Leading Design |

Mechanical Draft - 71.4% share (2025) |

|

Leading Region |

Asia Pacific - 42.5% revenue share (2025) |

|

Second Region |

North America - 24.1% revenue share (2025) |

|

Top Companies |

SPX Cooling Tech, LLC, Amsted Industries, John Cockerill, Johnson Controls |

Key Analytical Observations Supporting the Above Data:

- Cross Flow's 52.8% dominance in 2025 reflects the industry-wide preference for low-maintenance gravity-fed designs across HVAC, commercial buildings, and mid-scale power applications.

- Mechanical Draft leads the design segment at 71.4% in 2025, driven by factory-assembled FRP packaged units, fan-assisted precise airflow control, and broad suitability for industrial and commercial retrofit projects across chemical, refinery, and data center applications.

- Asia Pacific's 42.5% global dominance in 2025 reflects China's role as the world's largest electricity producer, alongside India's National Infrastructure Pipeline-driven commercial HVAC and process cooling expansion.

- The global data center industry is a rising incremental demand channel; IEA projects data center electricity consumption reaching 945 TWh by 2030, structurally lifting high-efficiency closed-circuit and hybrid tower deployments globally.

- Water-use regulation and sustainability mandates are reshaping tower specifications; hybrid and closed-circuit designs are capturing share from conventional evaporative systems in water-stressed regions, including the Middle East, California, and southern Europe.

Global Cooling Tower Market Overview

Cooling towers are specialized heat-rejection devices that extract waste heat from process or building water systems by transferring it into the atmosphere through evaporative or dry cooling. Modern towers combine structural fill media, drift eliminators, fan systems, and pumps to support reliable thermal performance. They serve as a critical backbone of thermal management infrastructure for power generation, HVAC, process industries, and data centers.

Applications span power generation, HVAC for commercial buildings, petrochemicals, oil and gas refining, food and beverage, pharmaceuticals, and increasingly hyperscale data centers where high-reliability cooling is mission-critical.

Macroeconomic enablers include rising global electricity consumption, industrial capex recovery exceeding USD 150 billion in petrochemicals alone, and regulatory tailwinds from water-efficiency mandates in the EU and US EPA frameworks, all of which directly lift cooling tower order volumes across new-build and retrofit segments.

Market Dynamics

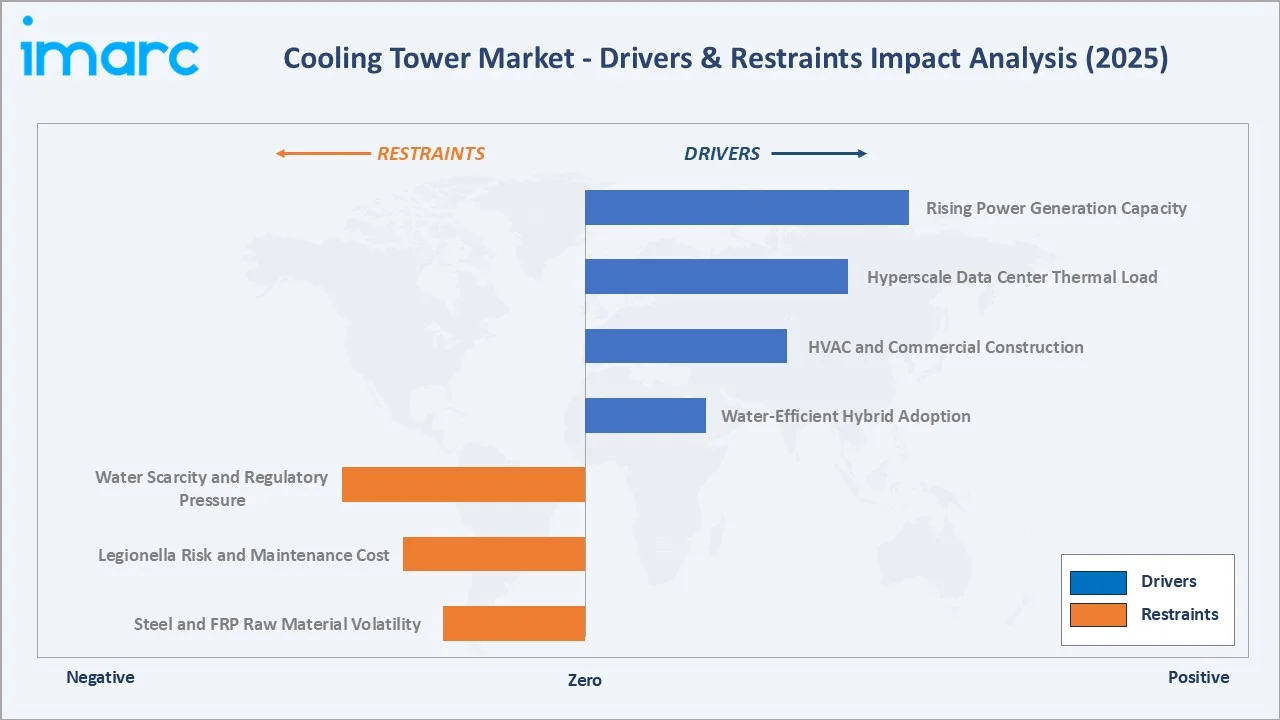

Market Drivers

- Rising Power Generation Capacity: Global installed thermal and nuclear capacity continues to expand, with IEA reporting over 29,000 TWh of electricity generated globally in 2024. Each new thermal or combined-cycle plant requires large-scale cooling tower infrastructure, and aging plant retrofits are driving replacement demand across the US, Europe, and Japan.

- Hyperscale Data Center Thermal Load: The global data center industry is projected to consume 945 TWh of electricity by 2030, nearly double 2024 levels (IEA). AI-driven compute densification is pushing rack heat loads above 40 kW, creating sustained demand for high-efficiency evaporative, closed-circuit, and hybrid cooling tower systems.

- HVAC and Commercial Construction: Global commercial construction spending surpassed USD 4 trillion in 2024, led by Asia Pacific and the Middle East. District cooling projects in the GCC and high-rise cooling needs in China and India are directly lifting HVAC-grade cooling tower procurement.

Market Restraints

- Water Scarcity and Regulatory Pressure: Evaporative cooling towers consume significant make-up water, making them a compliance challenge in water-stressed regions. EPA and EU regulations are tightening discharge and biocide rules, raising the total cost of ownership for operators.

- Legionella Risk and Maintenance Cost: Cooling towers are recognized vectors for Legionella contamination. Compliance with ASHRAE 188, OSHA, and state-level rules adds continuous monitoring and water treatment expenditure that can deter smaller facility operators from expansion.

Market Opportunities

- Hybrid and Closed-Circuit Systems: Hybrid wet-dry towers reduce water use by 40-60% versus conventional evaporative systems. Rising ESG scrutiny and drought conditions in California, Spain, and the GCC are creating a strong premium-priced upgrade channel for Tier-1 OEMs.

- Digital Monitoring and Predictive Maintenance: IoT-enabled towers with chemical-dosing analytics, vibration sensors, and fan-speed optimization are emerging as a differentiated value layer. Operators report 8-12% energy savings post-digital retrofit, supporting measurable ROI.

- Data Center Heat Reuse: Emerging heat-reuse models in Northern Europe and Japan, where data center waste heat is redirected to district heating networks, are opening new revenue-sharing opportunities for integrated cooling and heat-recovery tower suppliers.

Market Challenges

- Steel and FRP Raw Material Volatility: Fiber-reinforced plastic and structural steel account for 35-55% of tower capex. Raw material price swings of 15-20% during 2022-2024 squeezed OEM margins and delayed large project deliveries.

- Long Project Cycles: Large field-erected towers have 18-30-month delivery cycles, exposing OEMs to macroeconomic risk, currency volatility, and commissioning delays, particularly in emerging-market EPC contracts.

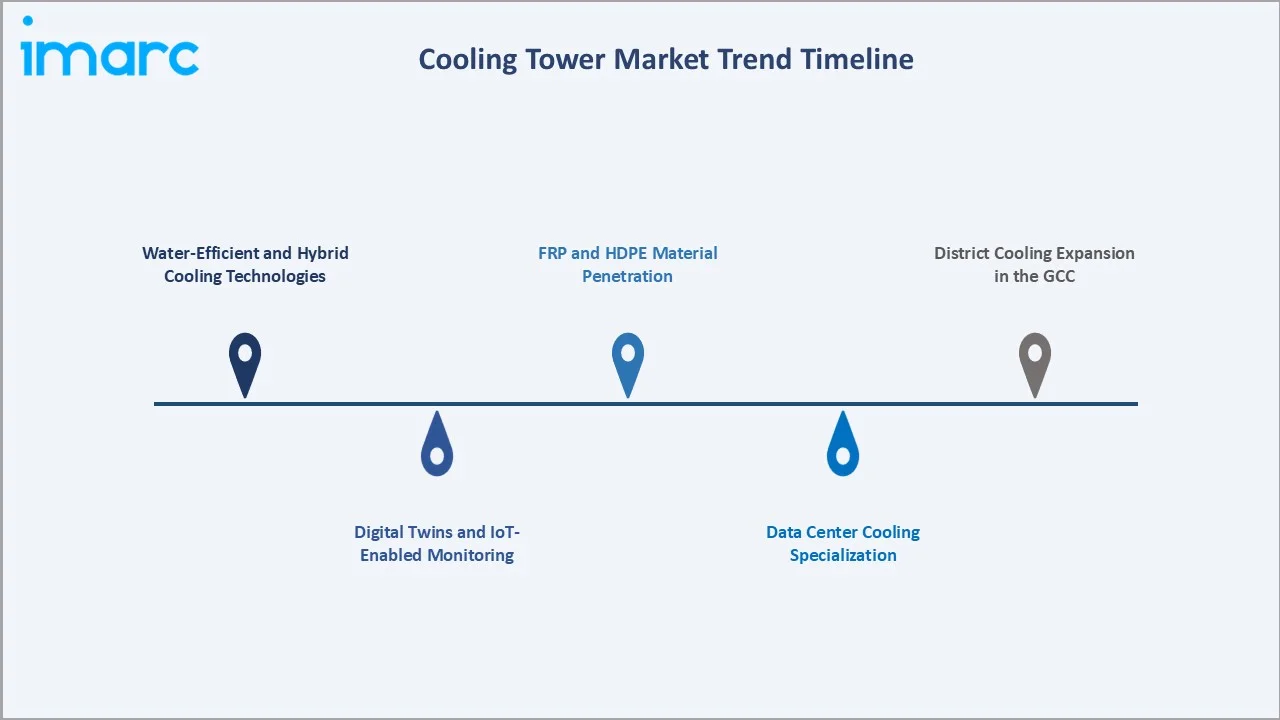

Emerging Market Trends

1. Water-Efficient and Hybrid Cooling Technologies

Hybrid wet-dry towers and plume-abatement systems are gaining traction as water availability becomes a board-level concern. Major OEMs, including SPX Cooling Technologies and Baltimore Aircoil, have launched next-generation plume-abated and low-water-use platforms, with adoption accelerating in California, Spain, the UAE, and Saudi Arabia.

2. Digital Twins and IoT-Enabled Monitoring

Condition-based monitoring, driven by IoT sensors and cloud analytics, is becoming a standard feature on new tower installations. Johnson Controls, SPX, and Thermax have rolled out digital platforms that cut unplanned downtime by up to 25% and reduce annual water and energy spend by 8-12%.

3. Data Center Cooling Specialization

Hyperscale operators are moving from traditional chillers to dedicated cooling tower loops paired with closed-circuit heat exchangers. Operators report up to 30% reduction in PUE (power usage effectiveness) by deploying evaporative and hybrid towers versus air-cooled alternatives.

4. FRP and HDPE Material Penetration

Fiber-reinforced plastic and high-density polyethylene components are replacing steel in corrosive applications such as chemical plants and coastal sites. FRP towers deliver 20-25-year service life with 40% lower maintenance cost versus galvanized steel equivalents.

5. District Cooling Expansion in the GCC

District cooling in Dubai, Abu Dhabi, and Riyadh is scaling rapidly, with over 30 GW of district cooling capacity under development across the GCC. Each mega-project requires multi-cell mechanical draft counter-flow towers, creating a clear pipeline for global Tier-1 suppliers.

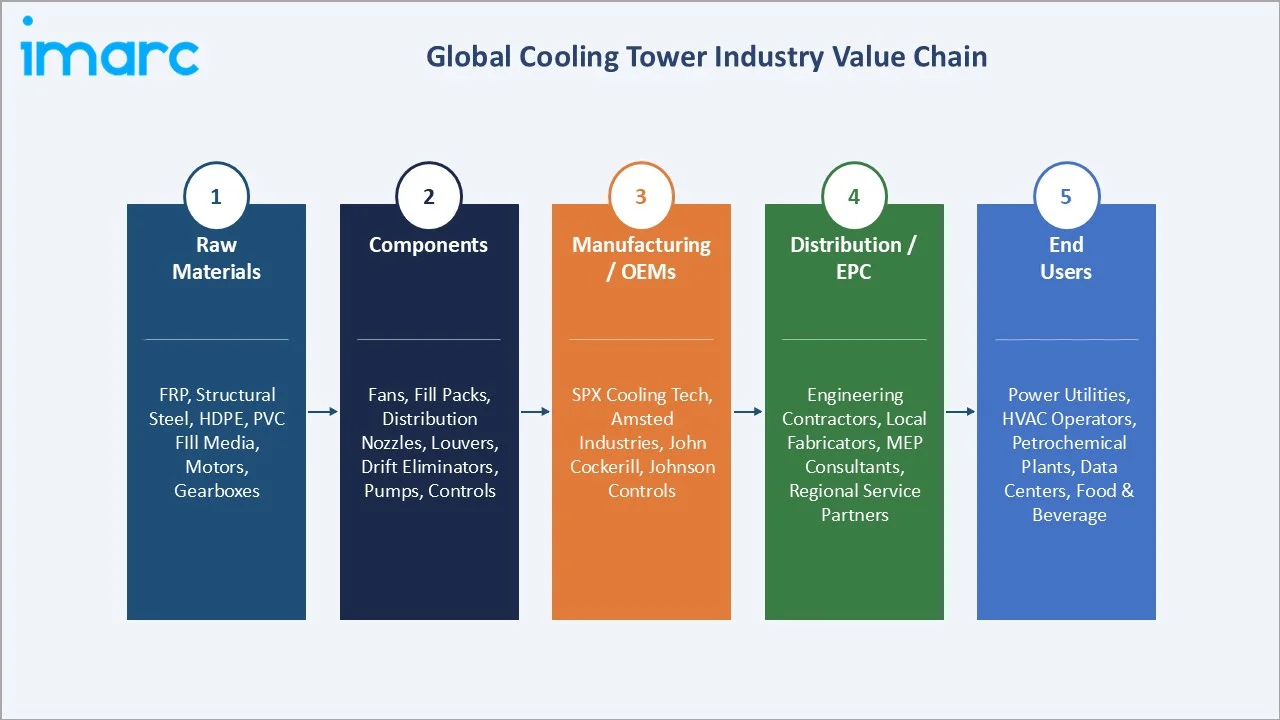

Industry Value Chain Analysis

The cooling tower value chain spans five integrated stages from raw material inputs through end-user operations. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Components |

|

Raw Materials |

FRP, structural steel, HDPE, PVC fill media, motors, gearboxes, drift eliminators |

|

Components |

Fans, fill packs, distribution nozzles, louvers, drift eliminators, pumps, controls. |

|

Manufacturing / OEMs |

SPX Cooling Tech, LLC, Amsted Industries, John Cockerill, Johnson Controls |

|

Distribution / EPC |

Engineering contractors, local fabricators, MEP consultants, regional service partners |

|

End Users |

Power utilities, HVAC operators, petrochemical plants, data centers, food & beverage |

Tier-1 OEMs occupy the highest-value position in the cooling tower chain, integrating material engineering, thermal design, and aftermarket service into multi-year contracts. However, regional fabricators and EPC partners capture 30-40% of project value in field-erected large-scale installations, driving ongoing partnership and co-manufacturing models.

Technology Landscape in the Cooling Tower Industry

Material Innovation: FRP, HDPE, and Advanced Composites

Material science is reshaping tower economics. FRP structural components offer a 20-25-year service life with 35-45% weight reduction versus steel, cutting foundation and shipping costs. HDPE fill media provides enhanced UV and biofouling resistance, extending service intervals from 5-7 years to 10-12 years and lowering the total cost of ownership.

Digital Controls and Predictive Maintenance

Smart variable-frequency drive fans, adaptive water treatment dosing, and predictive vibration analytics are the three core enablers of digital cooling towers. Retrofit deployments deliver 8-12% annual energy savings and 15-20% water savings, supporting paybacks of under 24 months across mid-scale industrial users.

Thermal Performance and Energy Efficiency

Next-generation film-fill packs with high surface-area-to-volume ratios have improved tower approach temperatures by 1-2 degrees C. Combined with high-efficiency axial fans meeting IE4/IE5 motor standards, modern towers now deliver 15-20% energy savings versus a decade-old baseline.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Tower Type | Open-Circuit Cooling Towers | 🔒 | 2025 |

| Flow Type | Cross Flow | 52.8% | 2025 |

| Design | Mechanical Draft Cooling Tower | 71.4% | 2025 |

| Construction Material | Fiber-Reinforced Plastic (FRP) | 🔒 | 2025 |

| End-User | Power Generation | 🔒 | 2025 |

| Region | Asia Pacific | 42.5% | 2025 |

By Flow Type

Cross Flow commands a 52.8% majority share in 2025, reflecting industry-wide preference for simpler gravity-fed water distribution, low pumping head, and easier access to internal components for maintenance. Cross-flow towers dominate HVAC, commercial buildings, and mid-scale power applications where ease of servicing is a key buying criterion.

Counter Flow at 47.2% in 2025 is preferred in applications that require higher thermal efficiency, smaller footprint, and reduced water drift. The counter-flow segment is dominant in refining, chemicals, and high-density data center cooling loops, where compact high-performance designs and lower icing risk in cold climates justify the modestly higher capex.

By Design

Mechanical Draft Cooling Towers dominate the design segment at 71.4% in 2025, driven by factory-assembled FRP packaged units, fan-assisted precise airflow control, and broad suitability across industrial and commercial retrofit projects. Mechanical draft towers are the default specification for most HVAC, chemical, refinery, and data center applications.

Natural Draft Cooling Towers at 28.6% in 2025 remain the preferred choice for very large thermal and nuclear power stations, where the hyperboloid shell leverages buoyancy-driven airflow without fan energy. Although capex is high, natural draft towers deliver multi-decade service life and minimal operating cost, which sustains their share in utility-scale installations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

42.5% |

China thermal power, India HVAC growth, ASEAN petrochemical, and data center expansion |

|

North America |

24.1% |

US power retrofits, hyperscale data center boom, HVAC replacement cycle |

|

Europe |

18.6% |

Germany industrial cooling, nuclear retrofit, ESG-driven hybrid adoption, UK data centers |

|

Middle East & Africa |

8.9% |

GCC district cooling, Saudi Vision 2030, petrochemical capex, South Africa power |

|

Latin America |

5.9% |

Brazil industrial cooling, Mexico oil & gas, Chile mining, commercial construction |

Asia Pacific commands a 42.5% global revenue share in 2025, the most dominant regional position in the global cooling tower market. China is the single largest national market, with an installed thermal power capacity exceeding 1,400 GW and continuous industrial capex expansion across petrochemicals and metallurgy. India has emerged as the fastest-growing sub-market, supported by the National Infrastructure Pipeline and rising commercial air-conditioning penetration across metro cities.

North America, with 24.1% in 2025, is anchored by the US market, where hyperscale data center construction, aging power plant retrofits, and HVAC replacement cycles drive consistent order flow. The US data center market alone absorbed over USD 35 billion in 2024 capex (Synergy Research), a significant share of which supports tower procurement in high-density cooling loops.

Europe holds 18.6% in 2025, led by Germany, France, and the UK, with steady retrofit demand across nuclear fleets, district heating integration, and industrial cooling modernization under EU Energy Efficiency Directive targets. Middle East & Africa (8.9%) is a fast-growing region, powered by GCC district cooling megaprojects and Saudi Vision 2030 infrastructure. Latin America (5.9%) is anchored by Brazil and Mexico's industrial cooling demand.

Competitive Landscape

|

Company Name |

Brand |

Market Position |

Core Strength |

|

SPX Cooling Tech, LLC |

Marley |

Leader |

Global scale, Marley brand, field-erected and factory-assembled portfolio |

|

Amsted Industries |

BAC |

Leader |

Closed-circuit leadership, ice thermal storage, hybrid plume-abatement towers |

|

John Cockerill |

Hamon Cooling Solutions |

Challenger |

Large field-erected towers, utility, and petrochemical dominance |

|

Johnson Controls |

YORK |

Leader |

Integrated HVAC portfolio, building controls, smart tower platforms |

|

SPIG-GMAB |

SPIG Cooling Systems |

Challenger |

Industrial cooling, power utility customer base, and environmental services |

|

Brentwood Industries, Inc. |

AccuPac® |

Emerging |

Fill media leadership, components, and global OEM supplier relationships |

|

Delta Cooling Towers, Inc. |

TMX Series |

Emerging |

Engineered-plastic HDPE towers, corrosion-resistant design, HVAC focus |

The global cooling tower competitive landscape is characterized by a small group of global Tier-1 thermal equipment suppliers commanding major utility and industrial contracts, alongside regional specialists that dominate HVAC and mid-market segments. Consolidation pressure is rising as hybrid and digital-enabled platforms demand larger R&D budgets and longer payback horizons.

Key Company Profiles

SPX Cooling Tech, LLC

SPX Cooling Tech, LLC is an engineered heat-rejection solutions company, operating under the iconic Marley brand with installations across more than 100 countries. The company serves power generation, HVAC, industrial, and hyperscale data center markets.

- Product & Platform Portfolio: Marley NC Fiberglass Towers, Marley MH Elite series, Marley Series 10 HVAC towers, field-erected counter-flow towers, closed-circuit coolers, drift eliminators, fan systems, and digital services.

- Recent Developments: In January 2026, SPX Cooling Technologies introduced two industrial-grade cooling tower designs for data centers and mission-critical locations in Europe, the Middle East, and Asia (EMEA) markets: the Marley NC Everest Cooling Tower and the Marley MD Everest Cooling Tower.

- Strategic Focus: SPX's strategy centers on three pillars: premium-segment hybrid and closed-circuit expansion, digital aftermarket services via the Marley ConnectPlus platform, and a strong retrofit-and-parts business anchored in its global installed base of over 50,000 towers.

Amsted Industries

Amsted Industries is a diversified industrial manufacturer participating in the cooling tower market indirectly through engineered components and advanced metal castings used in heavy-duty thermal infrastructure.

- Product & Platform Portfolio: Steel and ductile iron castings, bearings, mechanical drive components, and structural assemblies supporting cooling tower fan systems, gearboxes, and frames.

- Recent Developments: Amsted Industries’ Baltimore Aircoil Company, Inc. announces the release of its enhanced immersion cooling tank designed for high-performance data centers. The tank is powered by CorTex technology and sets a new standard for reliability, flexible high-density design, and efficiency.

- Strategic Focus: High-durability components for harsh environments, alignment with power and industrial sectors, and manufacturing modernization to strengthen OEM/EPC supply relationships.

John Cockerill

John Cockerill is a Belgium-based engineering group providing cooling and heat-rejection solutions for power, industrial, and infrastructure projects globally.

- Product & Platform Portfolio: Natural & mechanical draft cooling towers, wet/dry/hybrid cooling systems, air-cooled condensers, flue gas condensation, and EPC + aftermarket services (retrofit, upgrades, spares).

- Recent Developments: In December 2025, John Cockerill signed a contract for two new Hamon cooling towers for the Rabigh II Power Plant in Saudi Arabia.

- Strategic Focus: Water-efficient hybrid/dry cooling, decarbonization-linked projects, and lifecycle services (retrofit & performance optimization).

Market Concentration Analysis

The global cooling tower market exhibits moderate concentration among the top global OEMs, with SPX Cooling Tech, LLC, Amsted Industries, John Cockerill, and Johnson Controls collectively accounting for approximately 32-38% of global market revenue in 2025. The remaining share is distributed across strong regional players and a long tail of local fabricators.

The market shows a bifurcated structural dynamic. At the utility and large industrial tier, consolidation is occurring; large field-erected projects increasingly go to Tier-1 OEMs with balance-sheet strength and multi-decade references. In parallel, HVAC and packaged segments remain fragmented, with local FRP fabricators in Asia and Latin America serving price-sensitive buyers and creating an active M&A pipeline for global consolidators.

Chinese domestic OEMs are emerging as structural challengers in the world's largest regional market, leveraging lower manufacturing costs and strong government-backed infrastructure project allocation. International Tier-1s are increasingly partnering with local co-manufacturers to maintain relevance in China and India.

Investment & Growth Opportunities

Fastest-Growing Segments

Closed-circuit and hybrid cooling tower systems are the highest-growth sub-segments, projected to outpace the overall market at an estimated 5-6% CAGR through 2034, driven by water-use regulation, ESG scrutiny, and data center demand. FRP-based packaged units are also outpacing the market, supported by corrosion resistance and lower lifecycle cost.

Emerging Market Expansion

India, ASEAN, and the GCC represent the largest incremental geographic opportunity. India's process cooling demand is forecast to expand at a 5-7% CAGR, while GCC district cooling build-out targets 30 GW+ of installed capacity by 2030, each providing a sustained multi-year pipeline for global OEMs and regional EPC partners.

Venture & Private Investment Trends

Private-equity and strategic M&A activity has increased among mid-market cooling equipment manufacturers, reflecting a structural bet on digitization and hybrid technology. Recent investments into digital-twin and predictive-maintenance platforms are building a premium-priced aftermarket software layer on top of installed tower bases.

Future Market Outlook (2026-2034)

The global cooling tower market forecast projects steady value expansion from USD 3.25 Billion in 2025 to USD 4.46 Billion by 2034 at a CAGR of 3.48%, underpinned by power-sector cooling demand, rising HVAC penetration, hyperscale data center build-out, and the transition toward hybrid and closed-circuit water-saving designs across industrial applications.

Three structural shifts are most likely to reshape the cooling tower market through 2034. First, water-scarcity-driven regulation will accelerate hybrid and closed-circuit adoption in the Middle East, southern Europe, and the US Southwest. Second, digital-first cooling systems with integrated IoT analytics and predictive maintenance will emerge as a premium category. Third, hyperscale data centers will establish high-density cooling loops as a distinct specification tier with its own OEM supplier hierarchy.

By 2034, the cooling tower industry is forecast to have transitioned from a commoditized hardware market to a hybrid hardware-plus-software category, with digital services and aftermarket revenue accounting for 18-22% of Tier-1 OEM profitability, versus under 10% in 2024.

Research Methodology

Primary Research

Primary research included over 45 structured interviews conducted in 2024-2025 with cooling tower industry stakeholders: OEM product directors, EPC engineering leads, utility plant operators, data center infrastructure managers, HVAC consultants, and institutional investors in thermal equipment. Primary insights validated market sizing, segmentation, technology adoption timelines, and competitive positioning.

Secondary Research

Secondary sources include IEA World Energy Outlook (2024), ASHRAE publications, CTI (Cooling Technology Institute) standards, EPA water-use and Legionella compliance data, Dell'Oro Group and Synergy Research data center capex trackers, Cushman & Wakefield inventory studies, company annual reports, investor presentations, and trade publications including Process Cooling, HPAC Engineering, and Power Engineering.

Forecasting Models

Market size estimations and growth projections were derived through top-down and bottom-up forecasting models, incorporating GDP growth, industrial capex, electricity demand, HVAC penetration, and historical tower-shipment patterns. Base, optimistic, and conservative scenarios were modeled to capture macroeconomic uncertainty.

Cooling Tower Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Cooling Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Tower Types Covered | Open-Circuit Cooling Towers, Closed-Circuit Cooling Towers, Hybrid Cooling Towers |

| Flow Types Covered | Cross Flow, Counter Flow |

| Designs Covered | Mechanical Draft Cooling Tower, Natural Draft Cooling Tower |

| Construction Materials Covered | Fiber-Reinforced Plastic (FRP), Steel, Concrete, Wood, High-Density Polyethylene (HDPE), Others |

| End-Users Covered | Chemical, HVAC, Petrochemicals and Oil and Gas, Power Generation, Food and Beverages, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | SPX Cooling Tech, LLC, Amsted Industries, John Cockerill, Johnson Controls, SPIG-GMAB, Brentwood Industries, Inc., Delta Cooling Towers, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cooling tower industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key cooling tower companies.

Frequently Asked Questions About the Cooling Tower Market Report

The global cooling tower market was valued at USD 3.25 Billion in 2025, driven by rising power generation, HVAC demand, and data center cooling requirements.

The market is projected to reach USD 4.46 Billion by 2034, growing at a CAGR of 3.48% during 2026 to 2034, supported by industrial capex and water-efficient designs globally.

Cross Flow leads with a 52.8% share in 2025, driven by simpler distribution, lower pumping head, and ease of maintenance across commercial HVAC and mid-scale industrial cooling applications.

Mechanical Draft Cooling Towers dominate with a 71.4% share in 2025, supported by factory-assembled FRP units, precise airflow control, and broad industrial and commercial retrofit suitability.

Asia Pacific leads with a 42.5% share in 2025, driven by China's thermal power capacity, India's HVAC expansion, and petrochemical and data center growth across ASEAN markets.

Key drivers include rising power generation capacity, hyperscale data center cooling demand, commercial HVAC expansion, petrochemical capex, and water-efficient hybrid technology adoption.

Closed-circuit and hybrid towers are the fastest-growing sub-segments at 5-6% CAGR, driven by water-scarcity regulation, ESG scrutiny, and high-density data center cooling loops.

Leading companies include SPX Cooling Tech, LLC, Amsted Industries, John Cockerill, Johnson Controls, SPIG-GMAB, Brentwood Industries, Inc., and Delta Cooling Towers, Inc.

Water scarcity is shifting demand toward hybrid wet-dry and closed-circuit systems that cut make-up water use by 40-60%, particularly across the GCC, southern Europe, and the US Southwest.

Data centers are a structural growth driver, consuming an estimated 945 TWh globally by 2030. High-density AI workloads are lifting demand for evaporative, closed-circuit, and hybrid designs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)