Copper Pipes and Tubes Market Size, Share, Trends and Forecast by Finish Type, Outer Diameter, End-User, and Region, 2026-2034

Copper Pipes and Tubes Market Size and Share:

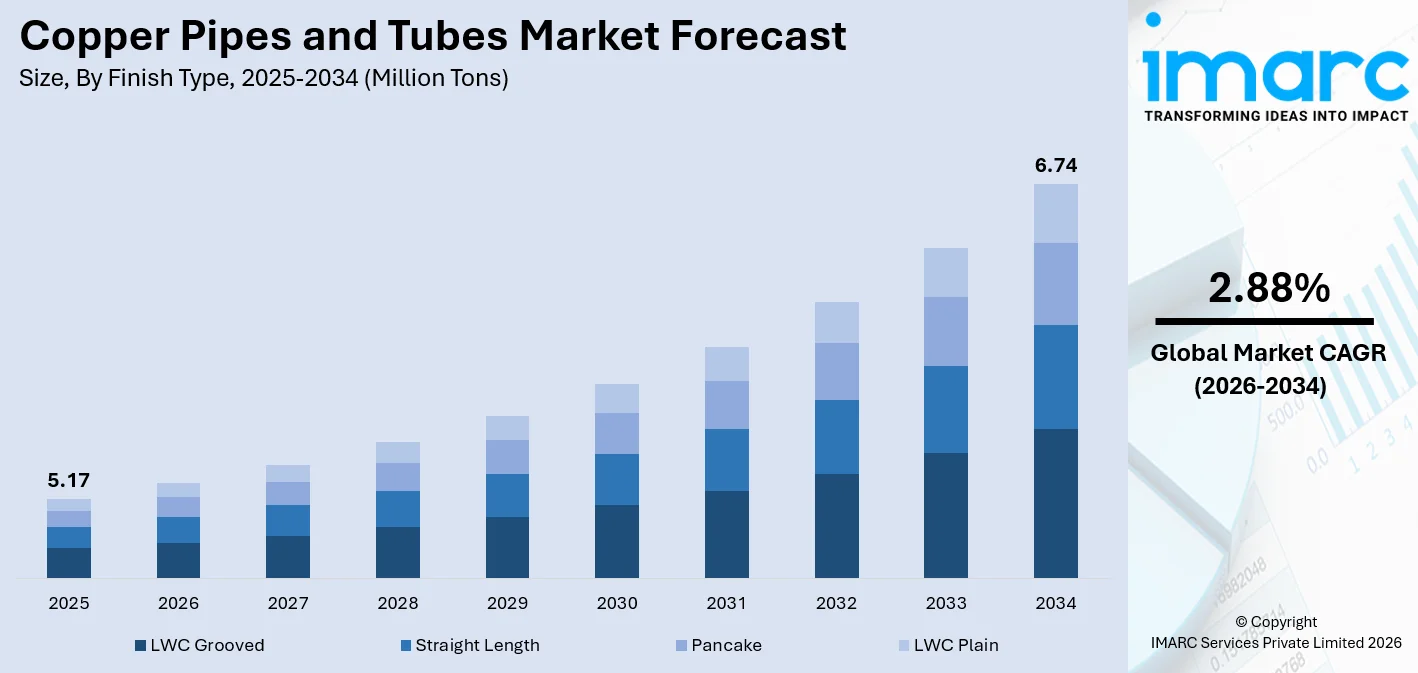

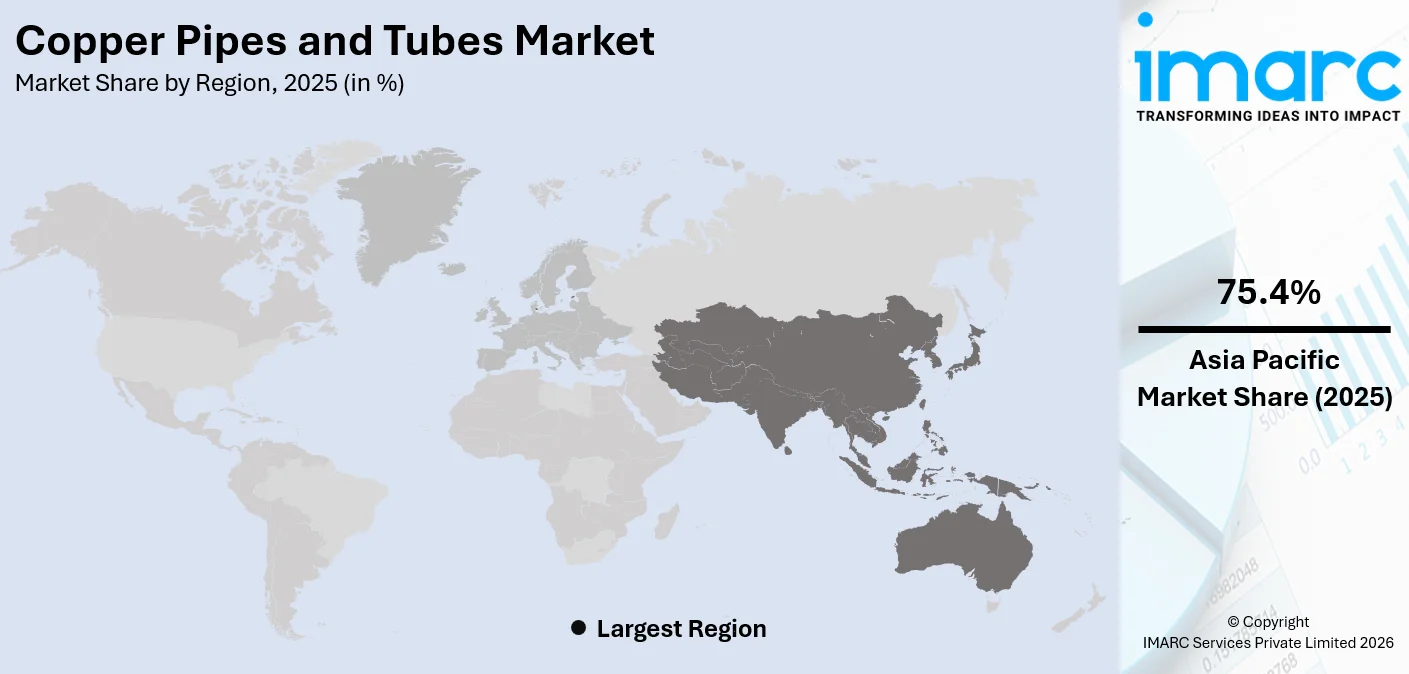

The global copper pipes and tubes market size reached 5.17 Million Tons in 2025. Looking forward, IMARC Group estimates the market to reach 6.74 Million Tons by 2034, exhibiting a CAGR of 2.88% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 75.4% in 2025. The region's prominence is underpinned by its large-scale manufacturing base concentrated in China and India, extensive construction and urbanization activity, strong HVAC adoption driven by rising temperatures. The growing incomes, and sustained government support for residential and commercial infrastructure development are further contributing to the copper pipes and tubes market share.

The global copper pipes and tubes market is propelled by rising demand from construction, HVAC, plumbing, and industrial sectors. Copper pipes are widely used in residential and commercial buildings for water supply, heating, and gas distribution due to their durability, corrosion resistance, and ability to withstand high temperatures and pressures. Rapid urbanization and infrastructure development in emerging economies are increasing the installation of plumbing and sanitation systems, which supports market demand. The growth of air conditioning and refrigeration systems are catalyzing the demand for copper tubing because of its superior thermal conductivity and reliability in heat exchange applications. In addition, the shift toward energy-efficient buildings and sustainable construction materials is encouraging the use of recyclable metals, such as copper. Ongoing investments in renewable energy systems and industrial machinery further contribute to steady demand for copper pipes and tubes across multiple end-use industries.

The United States is emerging as an important market for copper pipes and tubes due to its well-established construction sector, advanced HVAC industry, and strict building standards that emphasize durable and high-performance piping materials. Demand is further supported by ongoing investments in manufacturing capacity that strengthen domestic supply for cooling and industrial applications. Reflecting this trend, Wieland announced a USD 27 Million investment in 2024 to expand its copper manufacturing facility in Pine Hall, North Carolina, which was expected to create 50 new jobs. The expansion planned to introduce new production lines for Tech Tubes and Cold Plates used in HVAC systems, electronics cooling, aerospace, and defense applications. Such investments help enhance domestic production capabilities and support rising demand for energy-efficient cooling technologies and advanced copper tubing solutions across multiple industrial sectors in the United States.

To get more information on this market Request Sample

Copper Pipes and Tubes Market Trends:

Expansion of Construction and Infrastructure Development

Rapid expansion in residential, commercial, and industrial construction is a major factor supporting the growth of the copper pipes and tubes market. Copper piping is widely used in plumbing, water distribution, and mechanical building systems because of its durability, corrosion resistance, long service life, and ability to maintain water quality. Increasing urbanization, population growth, and investments in infrastructure development are creating sustained demand for reliable piping materials across housing projects, office complexes, healthcare facilities, and public infrastructure. Reflecting this momentum in construction activity, Saudi Arabia announced in 2026, the launch of the USD 26 billion “New Dammam” seaside residential development in the Eastern Province. The project will include more than 15,000 housing plots along with commercial zones, parks, and waterfront residences designed to accommodate over 180,000 residents. Large-scale developments of this nature significantly expand the need for plumbing and building service systems, thereby supporting consistent demand for copper pipes and tubes used in modern construction and infrastructure projects worldwide.

Growing Demand from Water Distribution and Plumbing Systems

Rising investments in water supply and distribution infrastructure are strengthening the demand for durable piping materials, thereby contributing to the growth of the copper pipes and tubes market. Copper pipes are widely used in potable water systems due to their corrosion resistance, structural strength, and ability to maintain water quality over extended service periods. Modern plumbing standards increasingly emphasize materials that provide long-term reliability under varying pressure and temperature conditions, making copper a preferred option in residential buildings, hotels, hospitals, and institutional facilities. Reflecting the scale of infrastructure investment driving this demand, China announced plans in 2025 to invest more than 5.4 trillion yuan (approximately USD 756.9 billion) in water conservancy infrastructure under the 14th Five-Year Plan covering 2021–2025. The initiative included large reservoirs, irrigation systems, water diversion projects, and extensive dike networks. Such large-scale investments in water infrastructure significantly expand the need for efficient distribution systems, thereby supporting consistent demand for copper pipes and tubes used in plumbing and water management applications.

Increasing Emphasis on Copper Recycling and Resource Efficiency

The growing focus on copper recycling and efficient resource utilization is supporting the growth of the copper pipes and tubes market by strengthening the availability of domestic raw materials. Recycling provides an additional and reliable source of copper feedstock, helping stabilize long-term supply for downstream manufacturers producing components for cooling systems, refrigeration equipment, and industrial applications. Improved recovery of copper from scrap also supports resource efficiency while reducing dependence on imported concentrates. This approach is increasingly important as demand for copper-based products rises across infrastructure, HVAC, and manufacturing sectors. Reflecting this trend, Hindalco Industries announced in 2024 an investment of INR 2,450 Crore in Gujarat that includes the establishment of India’s first copper and e-waste recycling plant at Dahej, designed to process 300 to 350 kilotons of scrap annually. Alongside the recycling facility, the company also planned to expand its copper smelting capacity at Dahej and develop a copper tube manufacturing unit in Vadodara to support air-conditioning and refrigeration applications.

Copper Pipes and Tubes Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global copper pipes and tubes market, along with forecast at the global and regional levels from 2026-2034. The market has been categorized based on finish type, outer diameter, and end-user.

Analysis by Finish Type:

- LWC Grooved

- Straight Length

- Pancake

- LWC Plain

LWC grooved holds 32.0% of the market share. This light wall coil tube features internal helical grooves that enhance heat transfer efficiency by creating turbulence in refrigerant flow, allowing systems to achieve higher thermal performance with reduced material usage. The design improves energy efficiency and supports compact equipment configurations commonly used in modern cooling technologies. As a result, the LWC grooved tube is widely specified in the manufacturing of split air conditioners, heat pumps, and commercial chillers. Its coil format also provides practical advantages during installation, as the flexible structure allows easier handling, transportation, and bending during system assembly. Installers can route the tubing efficiently through confined installation spaces without compromising structural integrity. The copper pipes and tubes market forecast indicates sustained growth driven by increasing demand from HVAC, refrigeration, and energy-efficient cooling applications.

Analysis by Outer Diameter:

- 3/8, 1/2, 5/8 Inch

- 3/4, 7/8, 1 Inch

- Above 1 Inch

The 3/8, 1/2, and 5/8 inch leads the market, accounting for a share of 45.0%. Small-diameter copper tubes within this size range are widely used in residential and light commercial HVAC systems, refrigeration equipment, and precision fluid distribution networks. Their popularity is largely due to compatibility with standard connection specifications used in split air conditioners, mini-split units, and packaged terminal air-conditioning systems. These sizes are frequently specified by HVAC installers and equipment manufacturers because they enable efficient refrigerant circulation while maintaining system performance. The relatively compact cross-sections support controlled refrigerant flow, reduce material usage per installation, and simplify bending and installation during system assembly. In addition, these tubes are easier to transport, store, and integrate within compact equipment designs. As demand for residential cooling systems and energy-efficient HVAC installations continues to expand globally, small-diameter copper tubes remain the most widely adopted sizes across the HVAC supply chain. These developments highlight evolving copper pipes and tubes market trends driven by increasing demand for efficient and compact HVAC system components.

Analysis by End-User:

Access the comprehensive market breakdown Request Sample

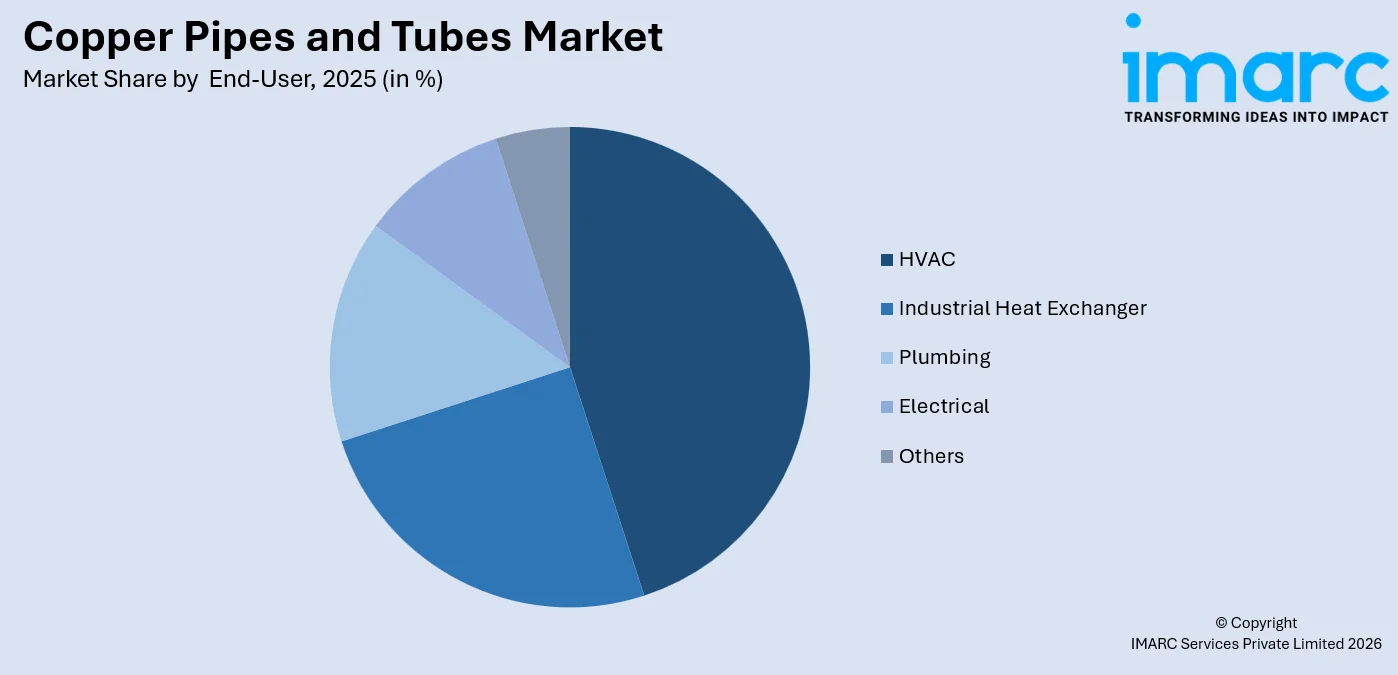

- HVAC

- Industrial Heat Exchanger

- Plumbing

- Electrical

- Others

HVAC dominates the market, with a share of 44.0%. Copper is widely used in HVAC systems due to its high thermal conductivity, corrosion resistance, durability, and ability to withstand pressure in refrigerant circulation applications. Copper tubing forms a critical component of heat exchangers, condenser units, evaporator coils, and refrigerant line sets used across residential, commercial, and industrial cooling systems. The push for energy-efficient air conditioning technologies has also encouraged the use of advanced tube designs that enhance heat transfer efficiency. Reflecting the growing demand for cooling infrastructure, India’s HVAC market is projected to expand at a CAGR of 14.89% during 2026–2034, according to IMARC Group. As cooling requirements rise across residential buildings, commercial spaces, and industrial facilities, the HVAC sector continues to generate significant demand for copper pipes and tubes used in refrigeration and climate control systems. This development contributes to a positive copper pipes and tubes market outlook owing to the rising demand from HVAC applications.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- Asia Pacific

- Europe

- North America

- Middle East and Africa

- Latin America

Asia Pacific, accounting for 75.4% of the share, enjoys the leading position in the market. The region's dominance is because of its large manufacturing base, competitive production costs, and strong availability of raw materials. Rapid urban development, industrial expansion, and rising demand for HVAC and refrigeration systems across countries continue to strengthen regional consumption of copper tubing. In addition to manufacturing scale, the region is also focusing on strengthening quality standards and industry collaboration to support long-term growth. Reflecting these efforts, BIS Chennai organized a “Manak Manthan” stakeholder consultation in 2025 to review the draft revised Indian standard for wrought copper tubes used in refrigeration and air-conditioning. The discussion involved manufacturers, laboratories, industry bodies, and academic experts to gather feedback on updates to IS 10773. Such initiatives help align product standards with evolving industry requirements, supporting efficient and globally competitive copper tube manufacturing across the region.

Key Regional Takeaways:

North America Copper Pipes and Tubes Market Analysis

North America represents a mature market for copper pipes and tubes, because of stringent building codes, well-established HVAC replacement cycles, and the growing demand from energy-efficient infrastructure. The United States remains a vital market in the region, where copper tubing is widely used in residential plumbing, commercial HVAC systems, and industrial heat exchanger applications due to its durability and thermal efficiency. Continuous renovation of aging buildings and modernization of water and heating systems are also sustaining demand for high-performance copper piping materials. Reflecting the scale of construction activity supporting this market, the U.S. Census Bureau reported that approximately 1,425,200 housing units were authorized by building permits in 2025. This level of residential development contributes significantly to copper tubing consumption for plumbing and climate control systems. In parallel, Canada’s urban densification and expansion of residential and commercial infrastructure are further supporting regional demand. As North America advances toward energy-efficient building systems and upgraded infrastructure, copper pipes and tubes continue to play a critical role in supporting reliable plumbing, heating, and cooling installations across the region.

United States Copper Pipes and Tubes Market Analysis

The United States copper pipes and tubes market is supported by strong demand from HVAC systems, plumbing infrastructure, and industrial heat exchanger applications, reinforced by well-established building standards and modernization of construction infrastructure. Residential construction, renovation activities, and upgrades to aging water distribution systems continue to generate steady demand for durable and corrosion-resistant piping materials such as copper. In addition, industrial sectors including automotive manufacturing, energy infrastructure, and defense equipment require high-performance copper tubing for thermal management and fluid transfer systems. Reflecting the ongoing strengthening of domestic production capacity, Wieland broke ground in 2025 on a USD 500 million modernization project at its East Alton, Illinois facility. The project includes the installation of a new state-of-the-art hot rolling mill designed to expand copper and copper alloy manufacturing capacity and improve production efficiency. By enhancing supply capabilities for sectors such as automotive, defense, and energy infrastructure, investments of this scale help reinforce the domestic copper manufacturing base. Such industrial upgrades support stable supply chains for copper pipes and tubes while meeting the evolving requirements of construction, engineering, and infrastructure markets across the United States.

Europe Copper Pipes and Tubes Market Analysis

Europe’s copper pipes and tubes market is driven by strong regulatory emphasis on energy efficiency, building modernization, and the growing adoption of heat pump and low-carbon heating systems across residential and commercial infrastructure. Many European countries are implementing renovation programs to upgrade aging building stock and improve energy performance, which increases the need for high-efficiency plumbing and thermal distribution systems that frequently rely on copper tubing. These upgrades often involve retrofitting heating networks, improving water distribution infrastructure, and installing energy-efficient HVAC technologies. Reflecting the scale of infrastructure activity in the region, the UK government released an updated Infrastructure Pipeline in 2026 outlining 734 projects valued at approximately £718 billion in planned public and private investment over the next decade. Such large-scale infrastructure and construction initiatives are expected to drive sustained demand for durable and energy-efficient piping materials, reinforcing the role of copper pipes and tubes in supporting Europe’s transition toward more sustainable and efficient building systems.

Asia-Pacific Copper Pipes and Tubes Market Analysis

Asia Pacific leads the global copper pipes and tubes market attributed to its extensive manufacturing capacity, strong industrial base, and rising demand from construction, HVAC, and refrigeration sectors. Rapid infrastructure development and expanding urban economies across the region are encouraging investments in domestic copper processing and component manufacturing. This momentum is further supported by efforts to strengthen local production capabilities and reduce reliance on imports. Reflecting this trend, Adani Enterprises announced a strategic partnership with MetTube in 2025 to develop copper tube manufacturing in India through cross-investments in Kutch Copper Tubes Ltd. and MetTube Copper India Pvt. Ltd. The collaboration combined Adani’s infrastructure expertise with MetTube’s manufacturing capabilities to expand domestic production capacity for applications in HVAC systems, refrigeration equipment, and energy-efficient infrastructure, reinforcing Asia Pacific’s leadership in the global copper pipes and tubes market.

Latin America Copper Pipes and Tubes Market Analysis

Latin America holds a strategically significant position in the global copper pipes and tubes market due to its strong resource base and expanding industrial demand. The region benefits from abundant copper reserves that support raw material availability for tube and pipe manufacturing while also supplying international markets. This advantage is reinforced by Chile’s dominant role in global copper production. According to the United States Geological Survey, Chile accounted for about 24% of global copper production in 2024, making it the world’s largest copper producer. This large-scale output strengthens supply chain stability for manufacturers. Furthermore, the rising demand from construction, refrigeration, and HVAC applications in countries, such as Brazil and Mexico is supporting the region’s consumption of copper pipes and tubes.

Middle East and Africa Copper Pipes and Tubes Market Analysis

The Middle East and Africa region is emerging as an important market for copper pipes and tubes, supported by large-scale infrastructure development and strong demand for cooling systems in hot climatic conditions. Construction growth across residential, commercial, and hospitality sectors is increasing the need for reliable plumbing and HVAC installations where copper tubing is widely used. This trend is particularly visible in the Gulf region’s expanding real estate sector. Reflecting this momentum, the UAE recorded strong property market activity, with total real estate transactions reaching approximately AED 893 billion by the end of 2024, across Dubai, Abu Dhabi, Sharjah, and Ajman. Such large-scale property development projects are driving the demand for durable piping materials, reinforcing the copper pipes and tubes market growth across the region.

Competitive Landscape:

The global copper pipes and tubes market is moderately consolidated, with a combination of large integrated producers and specialized regional manufacturers competing across finish type, outer diameter, and end-user segments. Leading players compete on the basis of production scale, vertical integration from copper refining through tube fabrication, proprietary tube geometries, and sustainability credentials, including recycled copper content and low-carbon production methods. Strategic priorities consist of capacity expansion in high-growth regions, technological investment in precision tube drawing and inner-groove forming technologies, and the development of application-specific product lines for next-generation HVAC refrigerants. Long-term supply agreements with HVAC original equipment manufacturers and plumbing distributors provide revenue stability. Mergers and acquisitions (M&A) are actively reshaping the competitive structure, with leading firms expanding geographic reach and application portfolios through targeted acquisitions to strengthen their position across the HVAC and construction supply chains.

The report provides a comprehensive analysis of the competitive landscape in the copper pipes and tubes market with detailed profiles of all major companies, including:

- Furukawa Electric Co., Ltd.

- KME Germany GmbH

- Kobe Steel, Ltd.

- Luvata (Mitsubishi Materials Corporation)

- MetTube Sdn Bhd

- Mueller Industries Inc.

- KMCT Corporation

- Cerro Flow Products LLC

- Golden Dragon Precise Copper Tube Group Inc.

- Mehta Tubes Limited

- Qingdao Hongtai Metal Co., Ltd.

- Shanghai Hailiang Copper Tubes Co., Ltd.

Latest News and Developments:

- In February 2026, Lawton Tubes began construction of a £20 million headquarters and manufacturing facility in Coventry to expand production capacity and support the growing demand for copper products. The new solar-powered site will include large-scale warehousing, manufacturing space, and automated technologies to improve operational efficiency. The expansion aimed to serve rising demand from sectors, such as construction, renewable energy, data centers, and national infrastructure projects.

- In October 2025, JTL Industries announced the launch of Continuous Cast (CC) Copper as part of its expansion into the non-ferrous segment to serve high-growth sectors. The company plans to scale monthly production from about 100 MT to 200 MT initially, targeting 500 MT by the end of Q4. The new copper product is designed for applications in electric vehicles, renewable energy systems, and infrastructure components.

Copper Pipes and Tubes Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Finish Types Covered | LWC Grooved, Straight Length, Pan Cake, LWC Plain |

| Outer Diameters Covered | 3/8, 1/2, 5/8 Inch, 3/4, 7/8, 1 Inch, Above 1 Inch |

| End-Users Covered | HVAC, Industrial Heat Exchanger, Plumbing, Electrical, Others |

| Regions Covered | Asia Pacific, Europe, North America, Middle East and Africa, Latin America |

| Companies Covered | Furukawa Electric Co., Ltd., KME Germany GmbH, Kobe Steel, Ltd., Luvata (Mitsubishi Materials Corporation), MetTube Sdn Bhd, Mueller Industries Inc., KMCT Corporation, Cerro Flow Products LLC, Golden Dragon Precise Copper Tube Group Inc., Mehta Tubes Limited, Qingdao Hongtai Metal Co., Ltd., Shanghai Hailiang Copper Tubes Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the copper pipes and tubes market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global copper pipes and tubes market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the copper pipes and tubes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Copper Pipes and Tubes Market Report

The copper pipes and tubes market reached a volume of 5.17 Million Tons in 2025.

The copper pipes and tubes market is projected to exhibit a CAGR of 2.88% during 2026-2034, reaching a value of 6.74 Million Tons by 2034.

The copper pipes and tubes market is driven by expanding construction and infrastructure development, increasing demand for durable plumbing and water distribution systems, rising urbanization and population growth, stronger investments in public utilities and building services, and growing emphasis on copper recycling and resource efficiency to ensure stable raw material supply.

Asia Pacific currently dominates the copper pipes and tubes market, accounting for a share of 75.4%. The region's leadership is driven by China's dominant copper manufacturing capacity, India's expanding HVAC and residential construction sectors, government-backed urbanization programs, and the highest concentration of HVAC equipment production globally.

Some of the major players in the copper pipes and tubes market include Furukawa Electric Co., Ltd, KME Germany GmbH, Kobe Steel, Ltd., Luvata (Mitsubishi Materials Corporation), MetTube Sdn Bhd, Mueller Industries Inc., KMCT Corporation, Cerro Flow Products LLC, Golden Dragon Precise Copper Tube Group Inc., Mehta Tubes Limited, Qingdao Hongtai Metal Co., Ltd., Shanghai Hailiang Copper Tubes Co., Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)