Dairy Industry in Delhi Market Size, Share, Trends and Forecast by Product Type, 2026-2034

Dairy Industry in Delhi Size, Share, Trends & Forecast (2026-2034)

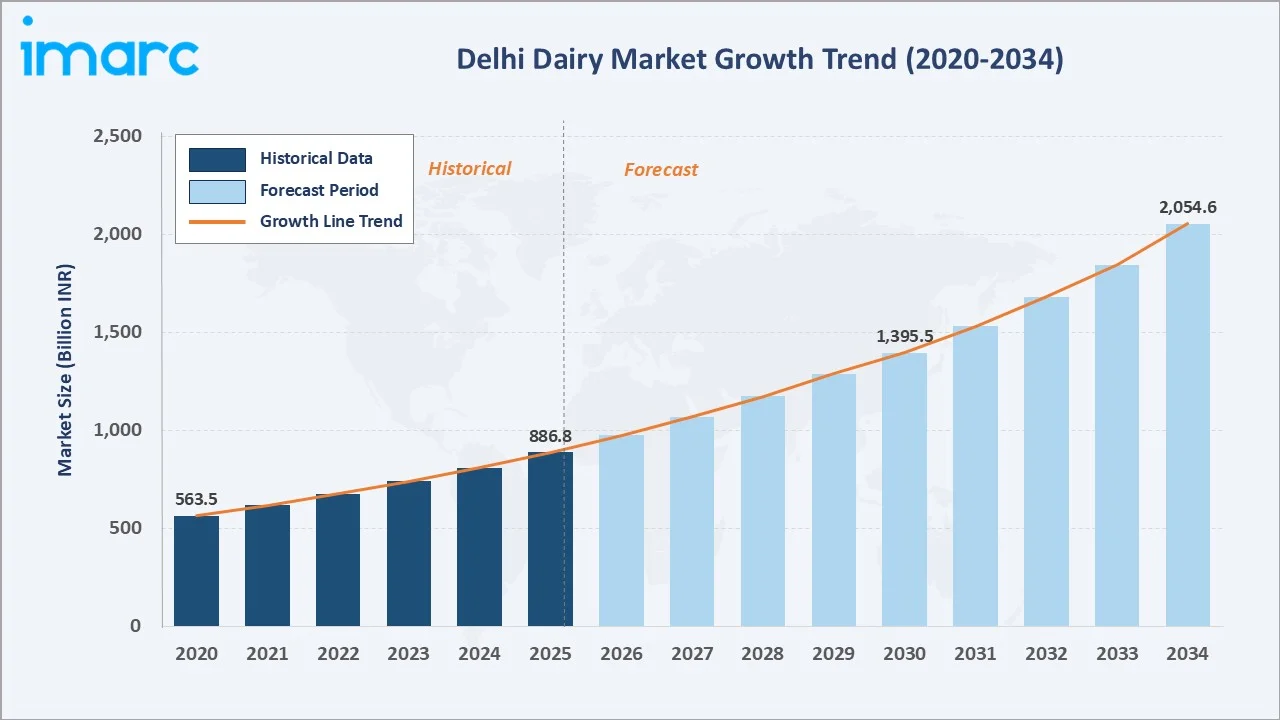

The dairy industry in Delhi reached INR 886.8 Billion in 2025 and is projected to reach INR 2,054.6 Billion by 2034, growing at a CAGR of 9.49% from 2026 to 2034. The market is driven by rising urbanisation, growing health awareness, increasing disposable incomes, and the expansion of organised dairy cooperatives.

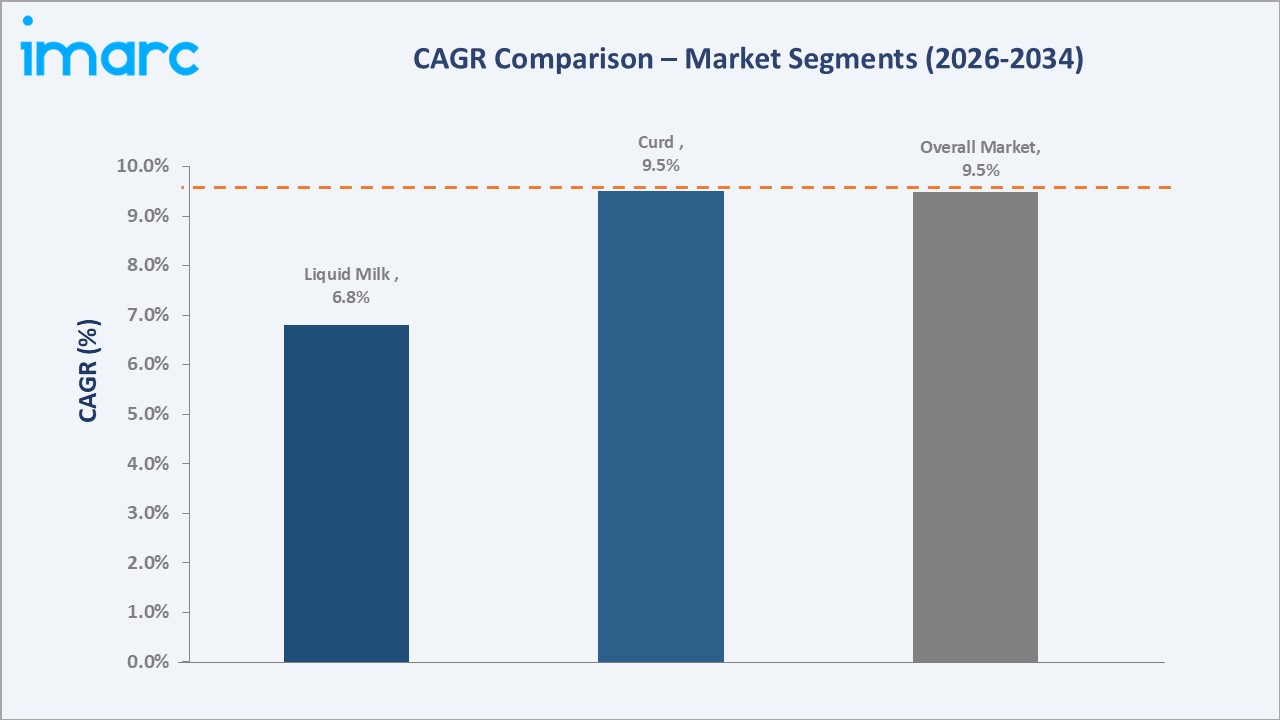

Liquid milk, at 42.0%, dominates the product-type share through cooperative booth infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 886.8 Billion |

|

Forecast Market Size (2034) |

INR 2,054.6 Billion |

|

CAGR (2026-2034) |

9.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Liquid Milk (42.0%, 2025) |

The market expanded from INR 563.5 Billion in 2020 to INR 886.8 Billion in 2025, anchored at INR 1,395.5 Billion in 2030, and forecast to reach INR 2,054.6 Billion by 2034. Rising per-capita dairy expenditure, Delhi's large urban population, and cooperative dairy infrastructure underpin this trajectory.

To get more information on this market, Request Sample

Liquid milk continues to anchor the market while value-added products, including paneer, ghee, flavoured milk, and probiotic curd, are gaining share at above-market growth rates, progressively reshaping the product mix toward higher-margin categories through 2034.

Executive Summary

The dairy industry in Delhi represents one of India's largest urban dairy consumption markets, underpinned by a growing population and demand for both commodity and value-added dairy products. The market reached INR 886.8 Billion in 2025 and is projected to reach INR 2,054.6 Billion by 2034, growing at a 9.49% CAGR.

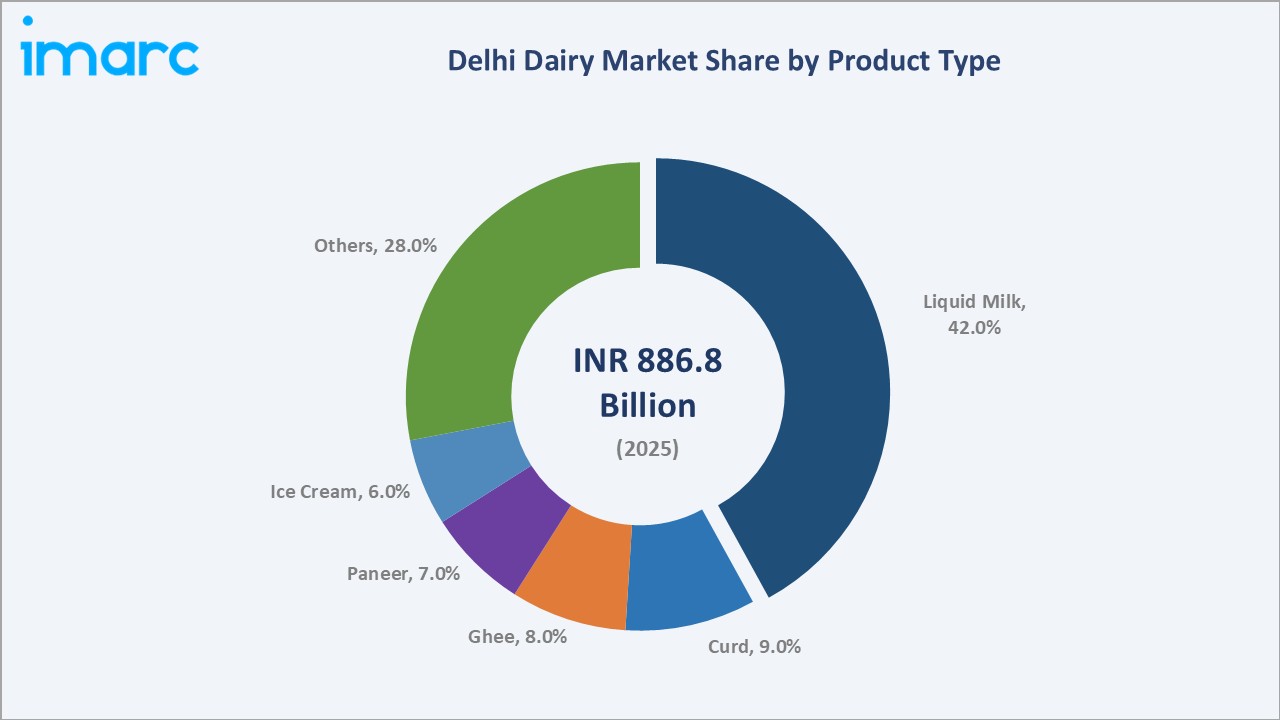

Liquid milk at 42.0% dominates through daily household consumption, cooperative booth distribution, and strong brand loyalty. Curd at 9.0% and ghee at 8.0% are the next largest categories. Paneer at 7.0% is gaining rapid traction, driven by food service and restaurant demand across all Delhi zones.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Liquid Milk - 42.0% share (2025) |

|

Second Largest Product |

Curd - 9.0% market share (2025) |

|

Third Largest Product |

Ghee - 8.0% market share (2025) |

|

Market Opportunity |

Value-added dairy: paneer, flavoured milk, UHT milk, probiotic curd, premium ghee |

Key Analytical Observations Supporting the Above Data:

- Liquid Milk at 42.0%: Daily household staple with deep cooperative penetration via various outlets across all Delhi zones. Consistent daily demand anchors market volume.

- Curd at 9.0%: Growing probiotic awareness and convenience packaging are driving organised market expansion.

- Ghee at 8.0%: Premium ghee segment growing at above-market CAGR as consumers trade up from loose ghee to branded packaged ghee driven by quality assurance and health narratives.

Dairy Industry in Delhi - Market Overview

The dairy industry in Delhi encompasses the procurement, processing, packaging, and distribution of all milk and milk-derived products consumed within the national capital territory, integrating cooperative dairies, private processors, informal vendors, cold-chain logistics providers, and modern retail formats.

The market structure is shaped by private players, including VRS Foods, and others. Macroeconomic drivers include rising disposable incomes, health awareness, growing dual-income households, and organised retail expansion.

Market Dynamics

Market Drivers

- Rising Urbanisation and Population Density Driving Liquid Milk Demand: Delhi's growing urban population, exceeding 32 million, generates sustained daily liquid milk demand. Concentrated residential density reduces per-litre distribution cost, enabling cooperative and private dairies to profitably serve micro-market clusters across all city zones.

- Expanding Organised Retail and Modern Trade Boosting Value-Added Dairy Sales: Rapid expansion of supermarkets, modern trade formats, and e-grocery platforms accelerates value-added dairy product adoption. Refrigerated shelving supports paneer, flavoured milk, UHT milk, and fresh cream sales, enabling branded players to capture premium margins.

- Health and Wellness Trends Accelerating Probiotic and Functional Dairy Demand: Growing consumer health awareness drives demand for probiotic curd, fortified milk, and low-fat dairy variants. This trend supports above-market CAGR for curd, flavoured milk, and yoghurt sub-categories across Delhi's urban consumer base.

- Cold-Chain Infrastructure Expansion Enabling Premium Perishable Category Growth: Investment in refrigerated logistics, last-mile cold storage, and temperature-controlled retail extends the reach of premium dairy products, enabling paneer, fresh cream, and UHT milk to penetrate deeper into Delhi's residential clusters.

Market Restraints

- Raw Milk Procurement Constraints Due to Limited Local Livestock Base: Delhi's limited agricultural hinterland constrains local milk procurement, creating supply dependence on distant milk sheds in Haryana, Uttar Pradesh, and Rajasthan. Seasonal fluctuations compress processor margins and introduce supply reliability risks.

- Intense Price Competition from Informal and Unorganised Dairy Vendors: Unorganised loose milk vendors retain significant market share through competitive pricing, operating below organised sector cost structures and compressing branded player pricing power in lower-income residential zones.

- Stringent Food Safety Regulations Increasing Compliance Costs for Processors: FSSAI regulations governing dairy processing, packaging, labelling, and distribution impose significant compliance costs. Small and mid-sized dairy operators face a disproportionate burden, restricting the pace of market formalisation.

Market Opportunities

- UHT Milk and Aseptic Packaging Reducing Cold-Chain Dependency: UHT processed milk in aseptic Tetra Pak formats reduces refrigeration dependency, enabling distribution in areas with limited cold-chain infrastructure. UHT milk at 3.0% segment share offers above-market growth potential.

- Premium Ghee and Artisanal Dairy Product Premiumisation: Rising consumer spending on premium A2-milk-derived ghee and artisanal dairy products creates high-margin growth opportunities. Branded premium ghee commands 2-3x price premium over commodity ghee.

Market Challenges

- Seasonal Demand Fluctuation for Ice Cream and Frozen Dairy Categories: Ice cream and frozen dairy categories exhibit significant seasonal demand variation, creating production planning and inventory management challenges that strain cold storage capacity and increase fixed cost per unit.

- Adulteration and Quality Consistency Issues Impacting Consumer Trust: Milk adulteration remains a persistent challenge in Delhi's dairy market, undermining consumer trust and accelerating preference for established branded cooperative suppliers over unorganised informal channels.

Emerging Market Trends

1. Direct-to-Consumer and Subscription Milk Delivery Models Gaining Traction

Startups and established players are deploying app-based subscription models for daily doorstep delivery of fresh and value-added dairy products. Various platforms are disrupting the traditional cooperative booth model in Delhi's tech-savvy consumer segments, commanding premium pricing.

2. A2 Milk Premium Category Creating New Consumer Segmentation

A2 milk derived from indigenous Indian cattle breeds is gaining recognition among health-conscious Delhi consumers. Premium pricing of 2-3x conventional milk creates attractive margin opportunities for niche dairy brands targeting wellness-oriented urban households in South Delhi and NCR zones.

3. Plant-Based Dairy Alternatives Entering Delhi's Urban Consumer Market

Plant-based milk alternatives including oat, almond, and soy are entering Delhi's premium retail and food service channels. While still below 1% of total dairy market volume, the category is growing rapidly among lactose-intolerant, vegan, and health-conscious consumers.

4. Cooperative Modernisation and Digital Procurement Platforms

Delhi's cooperative dairy sector is investing in digital milk procurement platforms, GPS-enabled milk tanker tracking, real-time quality testing, and farmer-facing mobile apps, improving procurement efficiency, reducing adulteration risk, and strengthening farmer-processor relationships.

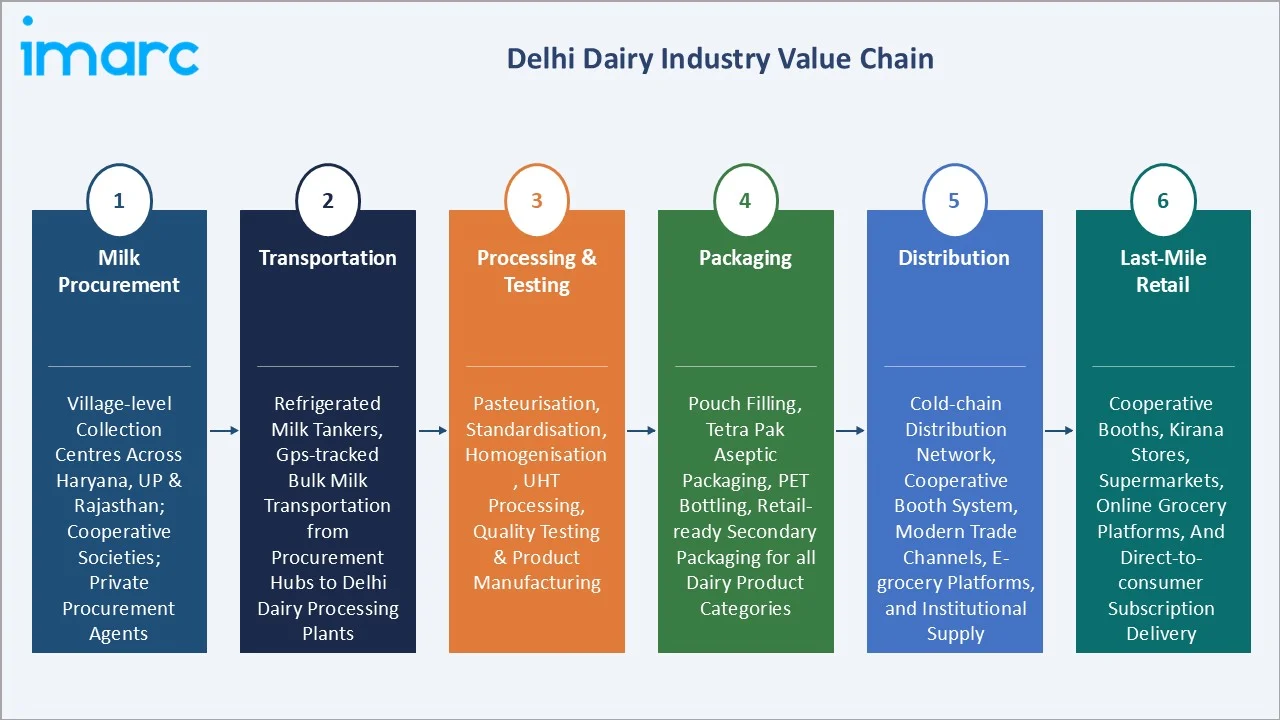

Industry Value Chain Analysis

The Delhi dairy value chain integrates milk procurement from Haryana, UP, and Rajasthan milk sheds, transportation to Delhi processing plants, pasteurisation, product manufacturing, packaging, cold-chain distribution, and last-mile delivery through cooperative booths, modern retail, and e-commerce platforms.

|

Stage |

Key Participants & Activities |

|

Milk Procurement |

Village-level milk collection centres across Haryana, UP, and Rajasthan milk sheds; cooperative societies; private procurement agents |

|

Transportation |

Refrigerated milk tankers, GPS-tracked bulk milk transportation from procurement hubs to Delhi dairy processing plants |

|

Processing & Testing |

Pasteurisation, standardisation, homogenisation, UHT processing, quality testing, and product manufacturing |

|

Packaging |

Pouch filling, Tetra Pak aseptic packaging, PET bottling, retail-ready secondary packaging for all dairy product categories |

|

Distribution |

Cold-chain distribution network, cooperative booth system, modern trade channels, e-grocery platforms, and institutional supply |

|

Last-Mile Retail |

Cooperative booths, kirana stores, supermarkets, online grocery platforms, and direct-to-consumer subscription delivery |

Technology Landscape in the Dairy Industry in Delhi

1. Cold Chain and Refrigeration Technology

Advanced cold chain and refrigeration technology is central to Delhi dairy market efficiency, enabling extended shelf life, reduced spoilage, and wider distribution of perishable dairy products. Investments in insulated milk tankers, refrigerated last-mile vehicles, and retail cold storage are expanding organised dairy reach across all Delhi zones, supporting premium perishable category growth.

2. UHT (Ultra-High Temperature) Processing Technology

UHT processing technology pasteurises milk at temperatures above 135°C for a brief period, achieving commercial sterility and enabling ambient storage of dairy products for up to six months without refrigeration. In Delhi, UHT technology is accelerating liquid milk and flavoured milk distribution beyond traditional cold-chain-dependent channels, supporting modern trade and e-grocery penetration.

3. Digital Milk Procurement and Quality Testing Platforms

Digital milk procurement platforms integrating GPS-enabled tanker tracking, electronic milk testing at collection points, farmer-facing mobile payment apps, and real-time quality dashboards are modernising Delhi's cooperative dairy supply chain. These technologies reduce adulteration risk, improve procurement transparency, and strengthen farmer-processor relationships, underpinning organised sector quality assurance.

4. Probiotic and Functional Dairy Formulation Technology

Advanced probiotic strain formulation and microencapsulation technology enables dairy processors to produce shelf-stable probiotic curd, fortified milk, and functional dairy beverages with clinically validated health benefits. In Delhi, this technology supports the fast-growing functional dairy sub-category, allowing branded players to differentiate products targeting health-conscious urban consumers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product type |

Liquid Milk |

42.0% |

2025 |

By Product Type

Liquid milk dominates at 42.0% of the Delhi dairy market in 2025, anchored by daily household consumption patterns, cooperative booth infrastructure, and strong brand loyalty toward established brands. The segment's sheer volume sustains market scale and cross-subsidises value-added category investment.

To access detailed market analysis, Request Sample

Curd at 9.0% and ghee at 8.0% represent the next most significant categories. Paneer at 7.0% gains rapid traction, particularly in food service. Ice cream at 6.0% demonstrates strong seasonal demand, while cheese at 5.0% and flavoured milk at 4.0% reflect growing Western dietary influence and health beverage trends.

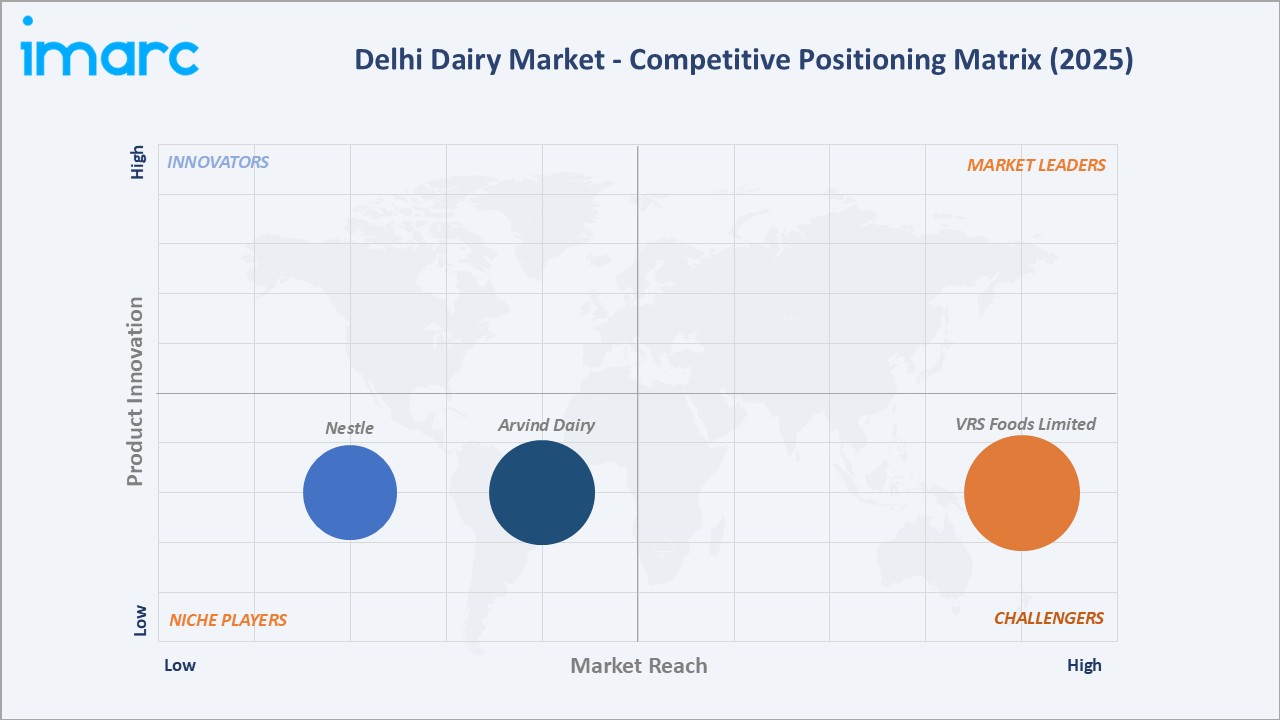

Competitive Landscape

The Delhi dairy market's competitive landscape is moderately concentrated, anchored by 2-3 dominant cooperative players alongside private players, the public sector Delhi Milk Scheme, and regional entrants.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

VRS Foods Limited |

Paras milk, ghee, butter, flavoured milk, paneer, curd, buttermilk |

Strong Challenger |

Private dairy in Delhi; strong village procurement |

|

Nestlé |

Nestlé a+ Dahi, Nestlé a+ Nourish milk |

Niche Player |

Premium and children's dairy segments; strong modern trade and supermarket distribution |

|

Arvind Dairy |

Butter, Dahi, Ghee, Paneer, Tofu |

Niche Player |

Delhi-based specialty dairy player; focus on fresh and vegetarian dairy products for local retail and institutional buyers |

Key players include VRS Foods Limited, Nestlé, Arvind Dairy, and others.

Key Company Profiles

VRS Foods Limited

VRS Foods Limited, operating the Paras Dairy brand, is a leading private dairy company headquartered in New Delhi with a strong and established presence in the Delhi dairy market. The company maintains an extensive village-level milk procurement network across multiple states and processes large volumes of milk daily for supply across the Delhi Metro.

- Key Products: Paras milk, Ghee, Butter, Flavoured Milk, Paneer, Curd, Buttermilk, and others.

- Strategic Focus: Expanding beyond liquid milk into high-margin value-added categories, including premium cheese, flavoured milk, and protein dairy products; strengthening modern trade and e-grocery distribution in Delhi NCR; and leveraging its large-scale village procurement network to sustain quality and cost competitiveness.

Arvind Dairy

Arvind Dairy Pvt. Ltd. is a Delhi-based dairy manufacturer and retailer headquartered at Karol Bagh, New Delhi, with processing operations sourcing milk primarily from the Brajbhoomi region of Uttar Pradesh.

- Key Products: Butter, Dahi, Ghee, Paneer, Tofu

- Strategic Focus: Strengthening the Arlys retail brand in Delhi's premium and health-conscious consumer segments through e-commerce and direct-to-consumer delivery; expanding the speciality dairy range including tofu, flavoured butter, and artisanal sweets; and positioning Brajbhoomi milk sourcing as a quality and provenance differentiator in Delhi's premium fresh dairy and desi ghee category.

Market Concentration Analysis

The Delhi dairy market is moderately concentrated at the liquid milk supply level. Top 3-4 players collectively account for an estimated 55-65% of organised liquid milk supply in Delhi. The organised sector accounts for approximately 60-65% of total Delhi dairy consumption, with the remainder served by unorganised informal vendors.

Market concentration is expected to increase gradually over the forecast period as FSSAI food safety enforcement, consumer preference for branded quality-assured products, and cooperative modernisation investments progressively displace unorganised supply channels across all Delhi zones.

Investment & Growth Opportunities

Highest Growth Segments

Paneer (very high growth), UHT milk (very high growth), flavoured milk (~10-12% CAGR), probiotic curd (~11-13% CAGR), premium ghee (~9-11% CAGR), cheese (~10-12% CAGR), and A2 milk premium category (~25%+ CAGR from small base) represent the highest investment return potential through 2034.

Emerging Investment Opportunities

Direct-to-consumer dairy subscription services represent the highest-margin emerging opportunity in Delhi's urban dairy market. Technology-enabled doorstep delivery at premium pricing creates 15-25% higher per-litre revenue versus cooperative booth supply, with a rapidly growing urban subscriber base.

- Cold-chain infrastructure investment: Expanding refrigerated last-mile logistics enables premium perishable product growth across all Delhi zones, unlocking value-added dairy category revenues that cannot be captured without reliable cold-chain reach.

- A2 milk and premium dairy brand building: Delhi's high-income South Delhi and NCR extension consumer base represents a receptive market for premium A2 and organic dairy brand positioning at 2-3x conventional milk price premiums.

Future Market Outlook (2026-2034)

The dairy industry in Delhi is projected to grow from INR 886.8 Billion in 2025 to INR 2,054.6 Billion by 2034, at a 9.49% CAGR. The market's anchor value of INR 1,395.5 Billion in 2030 represents the industry at a key commercial inflection as value-added categories begin to meaningfully shift the product mix.

Value-added product categories will progressively increase their revenue share as consumers trade up from liquid milk toward ghee, paneer, cheese, flavoured milk, and probiotic dairy. Organised sector share is expected to expand from 60-65% to 72-78% by 2034, driven by quality preference and modern trade growth.

Three structural forces define Delhi dairy market growth through 2034: urban household income growth sustaining per-capita dairy expenditure increases, dietary diversification toward value-added products expanding average revenue per kilogram of milk equivalent, and distribution modernisation enabling organised players to displace unorganised supply.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders including dairy cooperative managers, processing plant directors, cold-chain logistics providers, modern trade category managers, institutional dairy procurement officers, and Delhi food safety regulatory officials.

Secondary Research

Secondary research encompassed IMARC Group internal dairy market database, NDDB annual reports, FSSAI inspection and registration data, Delhi government dairy industry records, company annual reports, trade association publications, and consumer survey data. Over 50 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a bottom-up demand model: (i) Delhi household count multiplied by per-household dairy expenditure by product category; (ii) food service and institutional dairy demand overlay; (iii) organised versus unorganised sector share migration model; (iv) price inflation adjustment.

Dairy Industry in Delhi Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Liquid Milk, Ghee, Curd, Paneer, Ice-Cream, Table Butter, Skimmed Milk Powder, Frozen/Flavoured Yoghurt, Fresh Cream, Lassi, Butter Milk, Cheese, Flavoured Milk, UHT Milk, Dairy Whitener, Sweet Condensed Milk, Infant Food, Malt Based Beverages |

| Companies Covered | VRS Foods Limited, Nestlé, Arvind Dairy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Dairy Industry in Delhi Report

The dairy industry in Delhi reached INR 886.8 Billion in 2025, anchored by liquid milk at 42.0% of product-type share. The market is driven by Delhi's large urban population, cooperative dairy infrastructure, and growing demand for value-added dairy products including curd, ghee, paneer, and flavoured milk.

The Delhi dairy market grows at 9.49% CAGR during 2026-2034, reaching INR 2,054.6 Billion by 2034. Growth is driven by income-led per-capita dairy expenditure increases, value-added product category expansion, and organised sector share gains from informal supply channels.

Liquid milk leads at 42.0% share in 2025, reflecting daily household consumption patterns and cooperative booth distribution infrastructure. Curd (9.0%) and ghee (8.0%) are the second and third largest categories, with value-added segments growing at above-market rates through 2034.

Leading companies include VRS Foods Limited, Nestlé, Arvind Dairy, and others.

The Delhi dairy market is projected to reach INR 1,395.5 Billion by 2030, with significant growth contributions from paneer, ghee, flavoured milk, UHT milk, and probiotic curd categories, alongside continued liquid milk volume growth driven by population increase and rising per-capita income.

Priority investment opportunities include direct-to-consumer dairy subscription delivery platforms, A2 milk and premium dairy brand positioning, cold-chain infrastructure development for perishable value-added product distribution, and UHT milk capacity expansion targeting modern trade and e-grocery channels.

Liquid milk's 42.0% dominance is driven by daily household consumption necessity, extensive cooperative booth network across all Delhi zones, affordable cooperative pricing, and consistent supply reliability through organised cooperative procurement chains.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)