Dairy Industry in India Size, Share, Trends and Forecast by Product and Region, 2026-2034

Dairy Industry in India Size, Share, Trends & Forecast (2026-2034)

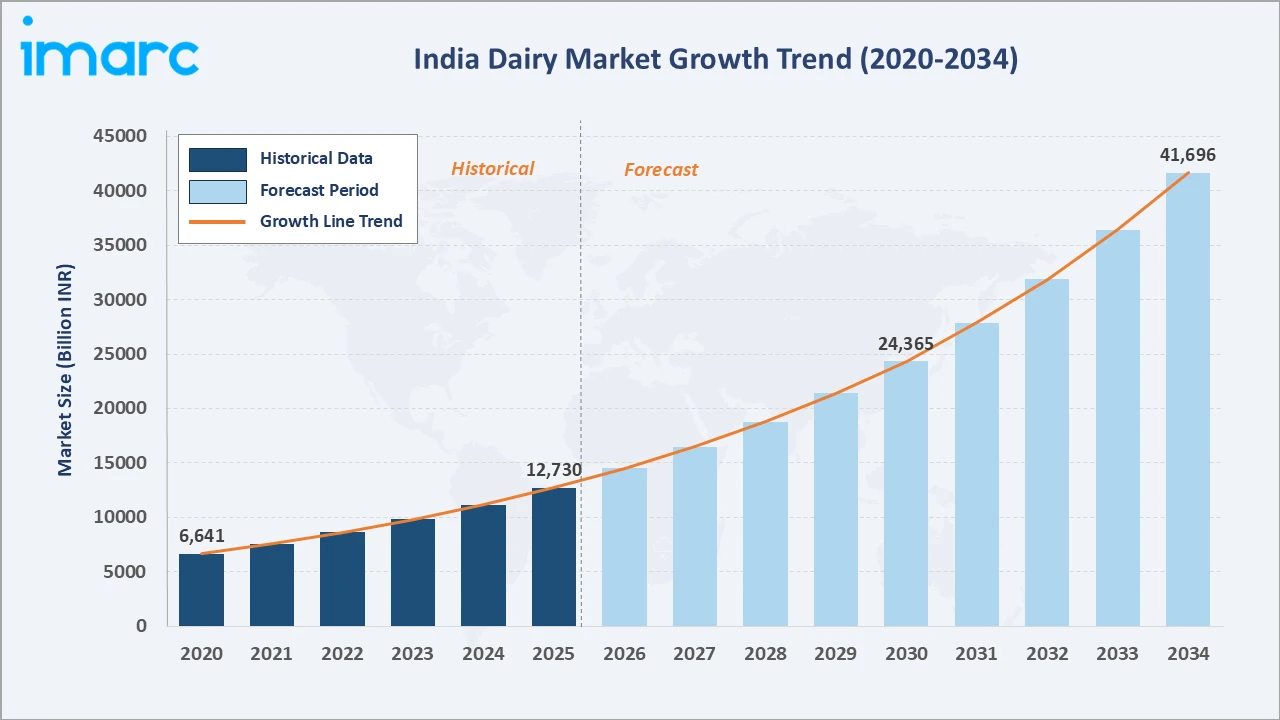

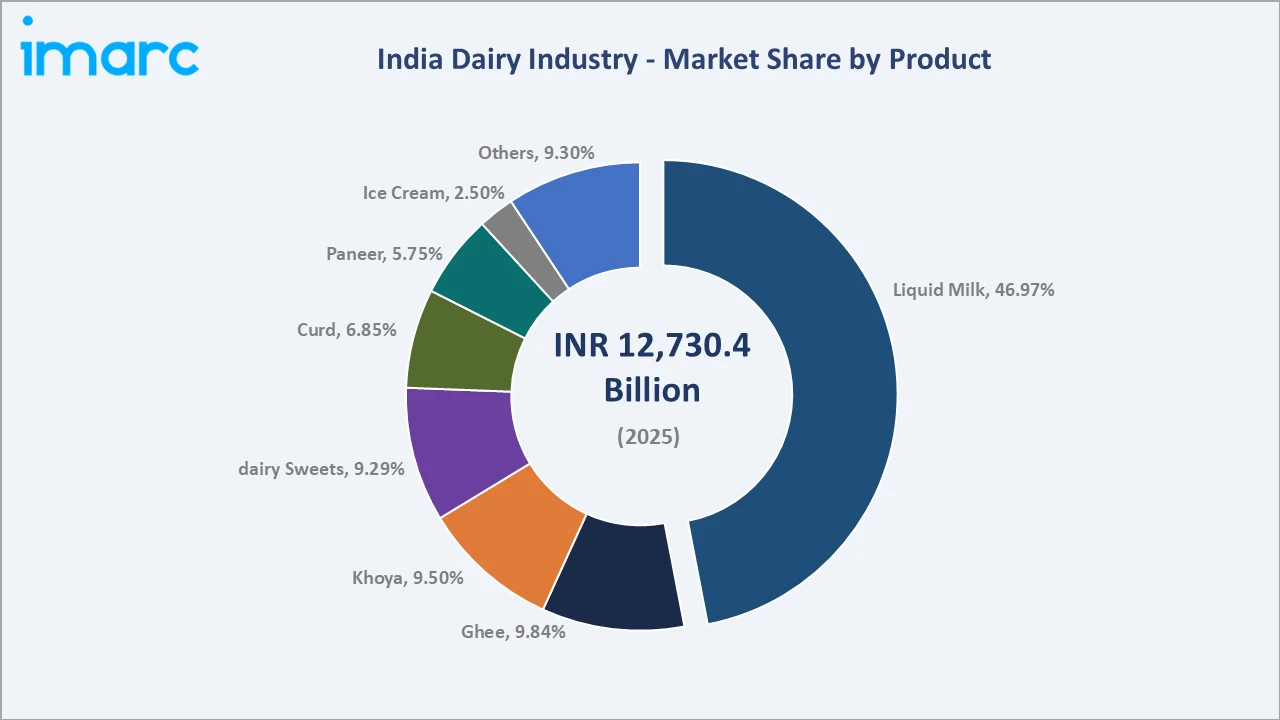

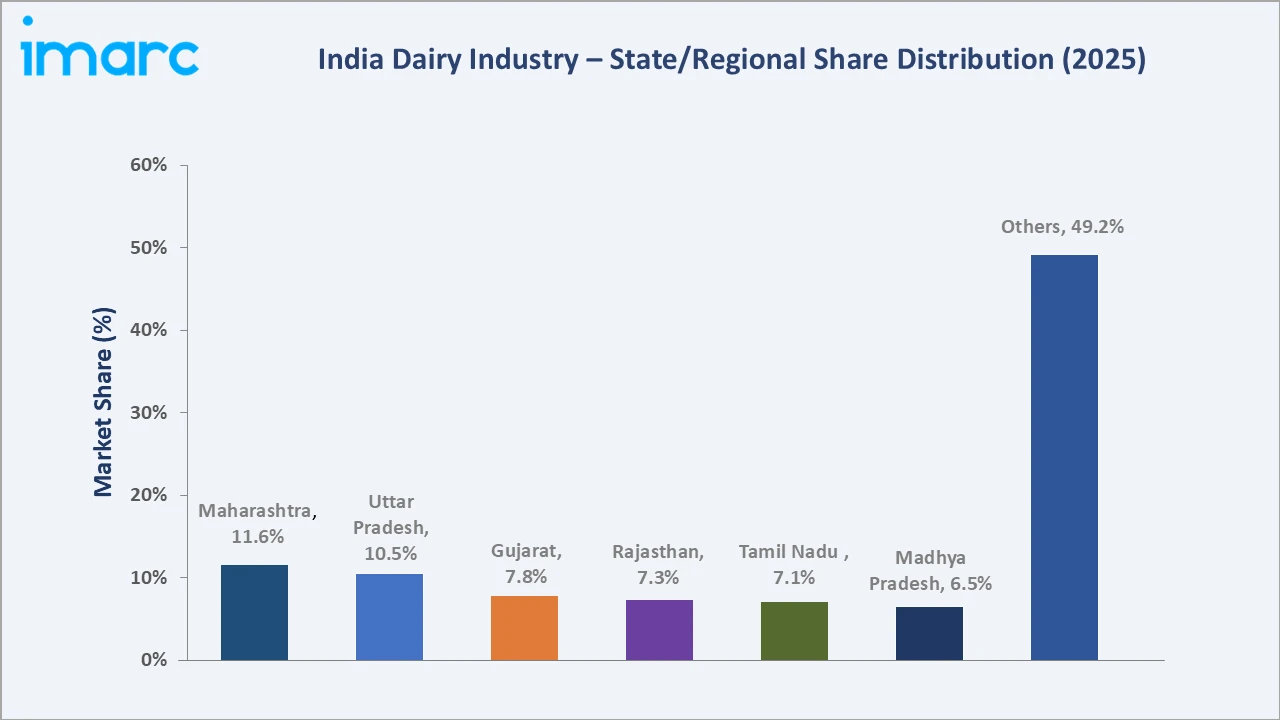

The dairy industry in India reached INR 12,730.4 Billion in 2025 and is projected to reach INR 41,696.39 Billion by 2034, growing at a CAGR of 14.14% during 2026-2034. India remains the world's largest producer and consumer of milk, with dairy forming a cornerstone of rural livelihoods, nutrition security, and agricultural GDP. The market is driven by rising per-capita consumption, urbanization, higher disposable incomes, and a decisive shift toward branded, packaged, and value-added products. The global surge in demand for hygienic, protein-rich dairy is accelerating investment in organized procurement, cold-chain modernization, and processing capacity. Liquid milk dominates the product mix at 46.97% in 2025, while ghee, khoya, dairy sweets, and curd anchor value-added demand. Maharashtra leads regionally at 11.60%, followed by Uttar Pradesh at 10.50%, as cooperative and private networks continue to formalize the sector.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 12,730.4 Billion |

|

Forecast Market Size (2034) |

INR 41,696.39 Billion |

|

CAGR (2026-2034) |

14.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Liquid Milk (46.97%, 2025) |

|

Fastest-Growing Product |

Paneer (highest CAGR 16.3%, 2025) |

|

Leading Region |

Maharashtra (11.60%, 2025) |

The Indian dairy market expanded from INR 6,641.1 Billion in 2020 to INR 12,730.4 Billion in 2025, anchored at INR 24,365.0 Billion in 2030, and forecast to reach INR 41,696.39 Billion by 2034. Rising incomes, urbanization, and heightened nutrition awareness sustained above-trend growth through 2020-2025. Steady volume expansion, premiumization, and organized-sector formalization continue to lift realizations, translating into a near-3.3x expansion over the forecast horizon and reinforcing India's position as the world's largest dairy economy.

To get more information on this market, Request Sample

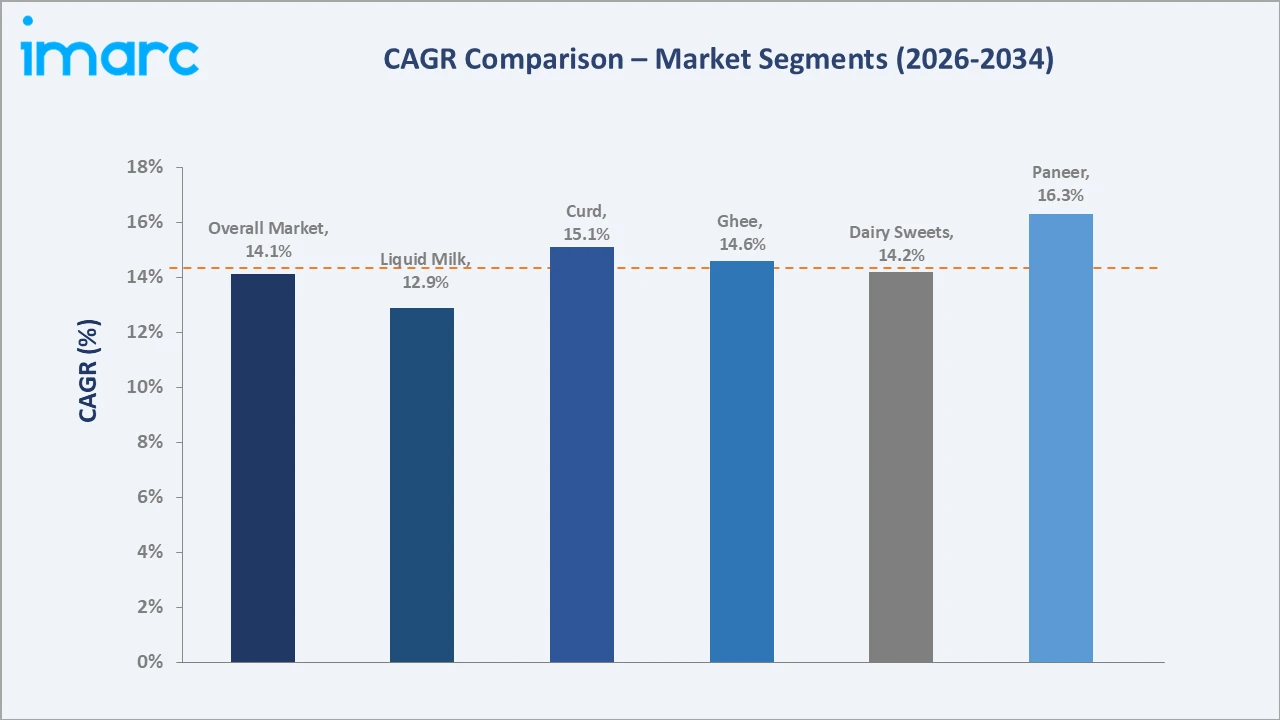

Value-added categories are growing faster than commodity liquid milk. Paneer, ice cream, and curd record above-market CAGRs through 2034 on the back of health-led premiumization, cold-chain reach, and rising branded demand, while liquid milk retains its dominant share through daily-staple consumption across urban and rural households.

Executive Summary

The dairy industry in India reached INR 12,730.4 Billion in 2025, representing one of the most dynamic intersections of agriculture, nutrition, and consumer goods in the country. The market spans milk production, procurement and chilling, processing and packaging, value-added manufacturing, cold-chain distribution, and retail. A vast unorganized base coexists with a fast-scaling organized segment led by cooperative federations and private dairies that continue to consolidate procurement and processing capacity across high-output states.

Liquid milk at 46.97% dominates through daily-staple demand, followed by ghee (9.84%), khoya (9.50%), and dairy sweets (9.29%). Maharashtra, at 11.60%, leads the regional landscape through strong cooperative and private processing networks, ahead of Uttar Pradesh at 10.50%, which anchors the nation's largest milk-producing base. Rising incomes, urbanization, premiumization, and digital distribution collectively drive branded penetration and higher-margin value-added growth through the forecast period.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Liquid Milk - 46.97% share (2025) |

|

Fastest-Growing Product |

Paneer & value-added dairy - highest CAGR (2025) |

|

Leading Region |

Maharashtra - 11.60% market share (2025) |

|

Market Opportunity |

Premium & functional dairy; A2/organic milk; cold-chain expansion; direct-to-consumer & quick commerce; export-oriented processing; value-added product innovation |

Key Analytical Observations Supporting The Above Data:

- Liquid Milk at 46.97%: Liquid milk dominates as a daily nutritional staple consumed across all income tiers. Rising urban demand for packaged, hygienic, and branded milk, along with expanding cold-chain and doorstep delivery, continues to sustain its leading share while supporting steady volume growth across rural and urban India.

- Value-Added Dairy Momentum: Paneer, curd, ice cream, ghee, and dairy sweets are gaining share as consumers premiumize. Health awareness, protein-rich diets, and organized branding are shifting demand toward higher-margin products, driving above-market growth across value-added categories nationwide.

- Maharashtra at 11.60%: Maharashtra leads through dense cooperative and private processing networks, strong urban demand, and well-developed distribution infrastructure. Uttar Pradesh follows closely, supported by the country's largest milk-producing base and expanding organized-sector participation across the state.

Dairy Industry in India Market Overview

The Indian dairy market encompasses the production, procurement, processing, packaging, and distribution of milk and milk-based products across cooperative, private, and unorganized channels. It links millions of smallholder dairy farmers to consumers through an extensive network of village-level collection centers, chilling plants, processing facilities, and retail outlets, balancing large-scale aggregation with structural fragmentation.

Macroeconomic drivers include rising disposable incomes, population growth, rapid urbanization, and increasing protein and nutrition awareness. Government support for the dairy sector, cooperative-led procurement, expanding cold-chain infrastructure, and modern retail and digital distribution are accelerating the shift from unorganized to organized and branded dairy, reshaping quality standards, pricing, and category growth nationwide.

Market Dynamics

To evaluate market opportunities, Request Sample

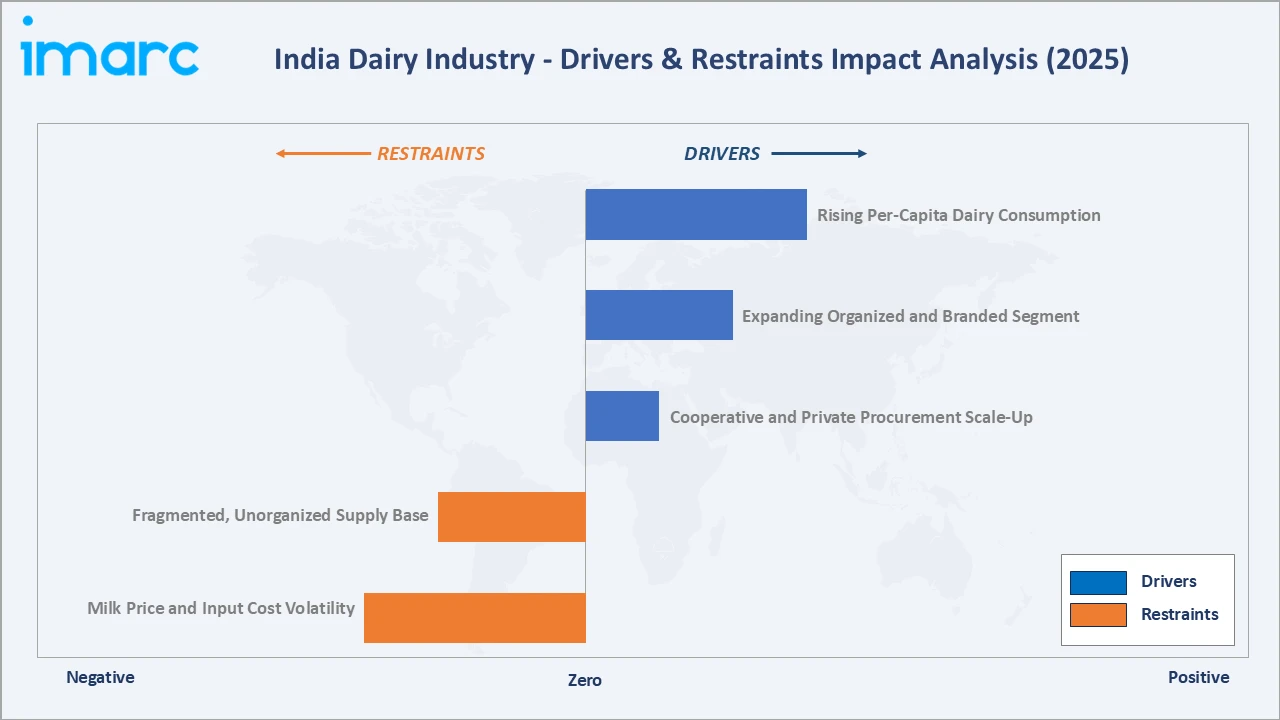

Market Drivers

- Rising Per-Capita Dairy Consumption: Growing incomes, urbanization, and heightened protein and nutrition awareness are lifting per-capita dairy consumption across income groups. Demand is broadening from basic liquid milk toward value-added products such as curd, paneer, cheese, and ghee. This structural rise in consumption sustains steady, above-trend volume growth and underpins long-term market expansion across both rural and urban India, reinforcing dairy's central role in the country's food economy.

- Expanding Organized and Branded Segment: Modern retail, packaging, food-safety standards, and consumer trust in branded products are steadily shifting share from the unorganized to the organized dairy segment. Cooperatives and private players are investing in branded portfolios, cold chains, and quality assurance. This formalization improves realizations, product consistency, and traceability, accelerating the market's transition toward higher-value, packaged dairy offerings across categories.

- Cooperative and Private Procurement Scale-Up: Sustained investment by cooperative federations and private dairies in milk procurement, chilling infrastructure, and processing capacity is strengthening supply reliability and quality. Deeper rural procurement networks and expanded plant capacity enable higher throughput, reduced wastage, and consistent supply of value-added products, supporting both volume growth and geographic expansion into underserved and emerging dairy markets.

- Cold-Chain and Technology Modernization: Modernization of cold chains, automation in processing, and digital distribution are reducing spoilage and widening branded reach. IoT-enabled monitoring, improved logistics, and analytics-driven demand planning enhance efficiency across the value chain. These upgrades enable reliable delivery of perishable and premium dairy, unlocking growth in high-margin categories and new consumption geographies.

Market Restraints

- Fragmented, Unorganized Supply Base: A large informal base of small dairy farmers and local vendors limits standardization, traceability, and consistent quality. Fragmented procurement raises collection costs and complicates food-safety compliance. This structural fragmentation slows organized-sector penetration and constrains the scale advantages needed for efficient, high-quality, branded dairy production across several regions of the country.

- Milk Price and Input Cost Volatility: Fluctuations in feed, fodder, and milk procurement prices pressure margins for both farmers and processors. Seasonal supply variations and rising input costs create pricing instability across the value chain. This volatility can squeeze profitability, discourage investment among smaller players, and complicate long-term planning for branded dairy operators and cooperatives alike.

- Cold-Chain and Quality Infrastructure Gaps: Inadequate cold-chain and quality infrastructure in certain regions constrains the distribution of perishable and premium dairy. Gaps in refrigeration, transport, and testing lead to spoilage and quality inconsistency. These shortfalls limit branded reach in interior markets and raise operational costs, restraining growth in value-added and high-margin categories.

Market Opportunities

- Premium, Functional, and A2/Organic Dairy: Rising health consciousness is creating strong demand for high-protein, low-fat, fortified, A2, and organic dairy products. These premium categories command higher margins and brand loyalty. Companies investing in functional dairy innovation and clean-label positioning are well placed to capture affluent, health-focused urban consumers seeking differentiated, value-added offerings.

- Direct-to-Consumer and Quick Commerce Expansion: D2C models, subscription milk delivery, and quick-commerce platforms are compressing delivery timelines and expanding branded reach in urban and semi-urban markets. These channels improve freshness, consumer data, and repeat purchase. Investment in digital distribution and last-mile cold chain offers a scalable route to higher-margin, direct consumer relationships.

Market Challenges

- Supply-Demand and Seasonality Management: Balancing seasonal milk supply with year-round demand remains a persistent challenge. Flush-and-lean production cycles create surpluses and shortages that strain procurement, storage, and pricing. Managing this variability requires investment in drying, storage, and flexible processing to maintain consistent product availability and stable farmer incomes throughout the year.

- Quality Assurance and Adulteration Control: Ensuring consistent quality and preventing adulteration across a fragmented supply base is operationally complex. Maintaining hygiene, testing, and traceability standards from farm to retail demands significant investment. Lapses can erode consumer trust and brand value, making robust quality assurance systems essential for sustained organized-sector growth.

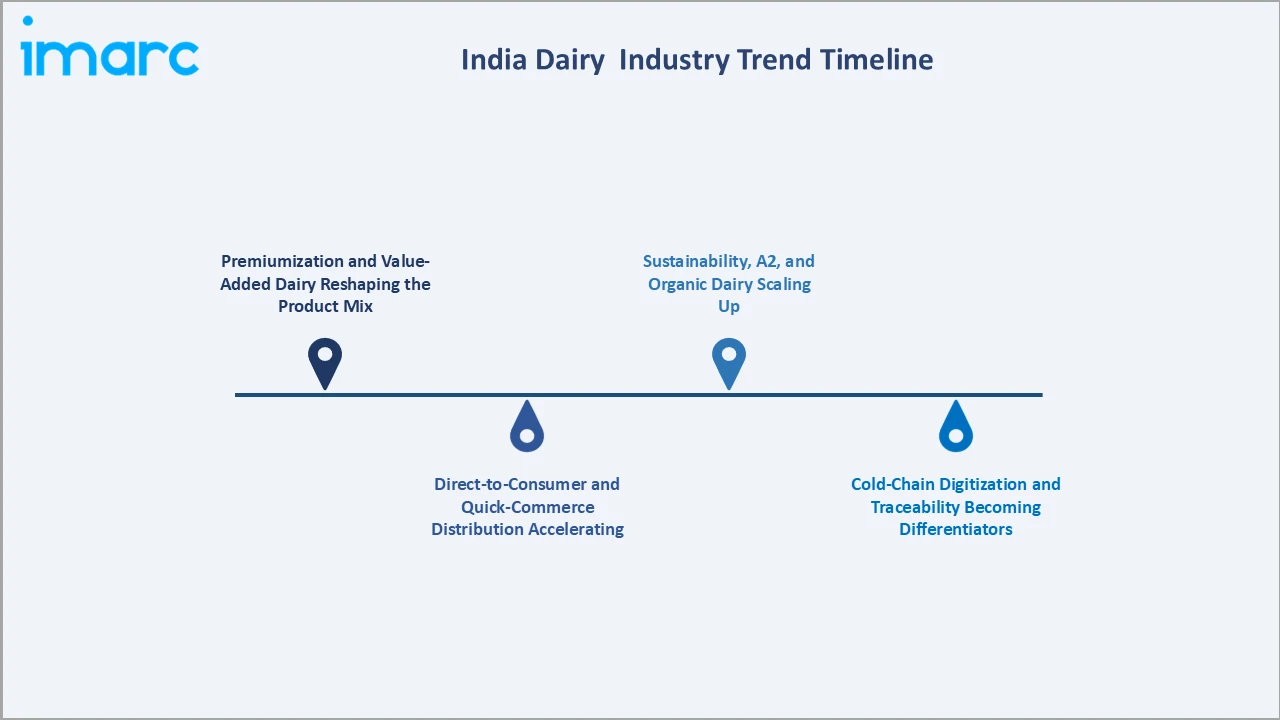

Emerging Market Trends

1. Premiumization and Value-Added Dairy Reshaping the Product Mix

Consumers are increasingly favoring premium, health-positioned, and value-added dairy over commodity milk. Demand for paneer, cheese, flavored and functional yogurt, ghee, and high-protein products is rising fast, particularly in urban markets. Brands are expanding premium portfolios with fortified, low-fat, and clean-label variants, capturing higher margins and driving a structural shift in the product mix toward differentiated, value-added categories through the forecast period.

2. Direct-to-Consumer and Quick-Commerce Distribution Accelerating

D2C dairy brands, subscription milk delivery, and quick-commerce platforms are transforming distribution. These channels enable fresh, doorstep delivery within minutes to hours, richer consumer data, and stronger repeat-purchase behavior. As urban consumers prioritize convenience and freshness, dairy players are investing in app-based ordering and last-mile cold chain, broadening branded reach well beyond traditional retail networks.

3. Cold-Chain Digitization and Traceability Becoming Differentiators

Cold-chain digitization, IoT-enabled monitoring, and farm-to-fork traceability are emerging as competitive differentiators. Real-time temperature tracking, digital procurement, and quality analytics reduce wastage and reinforce consumer trust. As food-safety expectations rise, dairy companies deploying traceability and smart cold-chain technologies gain advantages in premium, export-ready, and organized-retail segments across high-value dairy categories.

4. Sustainability, A2, and Organic Dairy Scaling Up

Sustainability, A2 milk, and organic dairy are moving from niche to mainstream. Consumers seek ethically sourced, chemical-free, and easily digestible products, while producers pursue lower-emission and resource-efficient operations. Growing demand for A2, organic, and clean-label dairy is encouraging investment in specialized sourcing, certification, and branding, creating durable, higher-margin growth pockets through the forecast period.

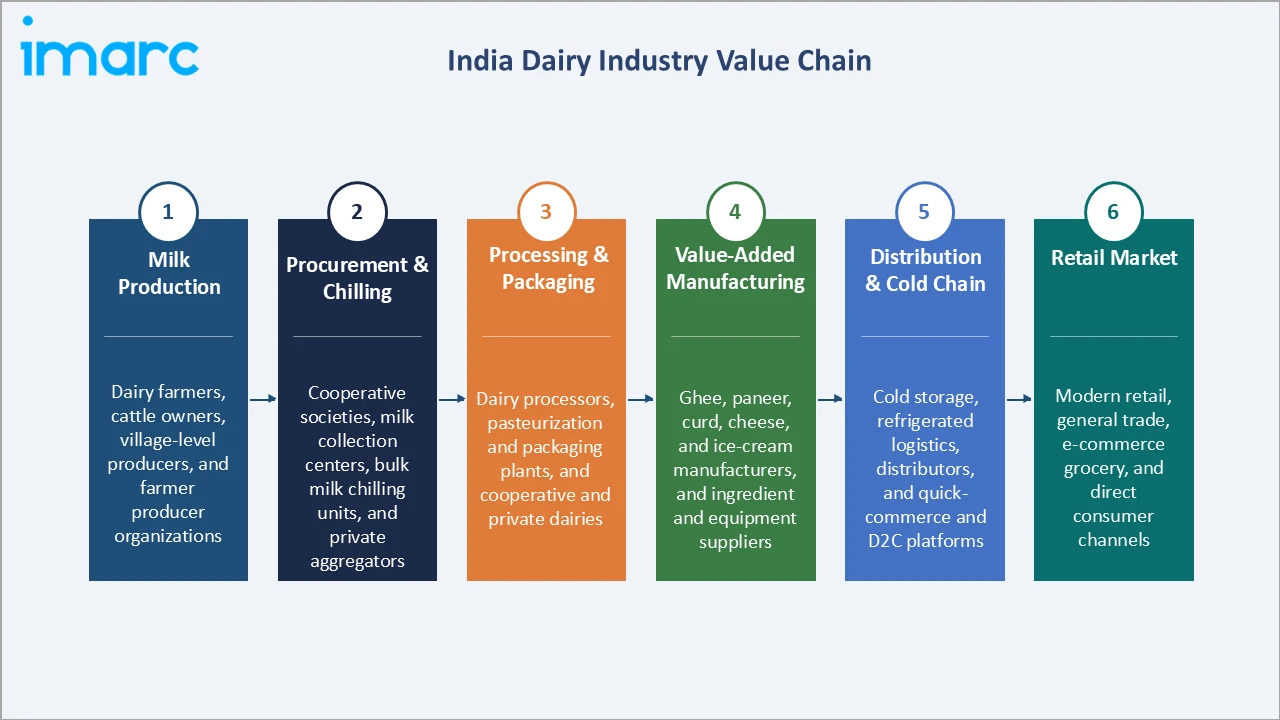

Industry Value Chain Analysis

The Indian dairy value chain integrates milk production, procurement and chilling, processing and packaging, value-added manufacturing, cold-chain distribution, and retail market supply. Each stage adds value through aggregation, preservation, transformation, and branding before products reach the end consumer.

|

Stage |

Key Participants |

|

Milk Production |

Dairy farmers, cattle owners, village-level producers, and farmer producer organizations |

|

Procurement & Chilling |

Cooperative societies, milk collection centers, bulk milk chilling units, and private aggregators |

|

Processing & Packaging |

Dairy processors, pasteurization and packaging plants, and cooperative and private dairies |

|

Value-Added Manufacturing |

Ghee, paneer, curd, cheese, and ice-cream manufacturers, and ingredient and equipment suppliers |

|

Distribution & Cold Chain |

Cold storage, refrigerated logistics, distributors, and quick-commerce and D2C platforms |

|

Retail Market |

Modern retail, general trade, e-commerce grocery, and direct consumer channels |

The procurement and chilling stage is among the value chain's most critical phases, determining milk quality and supply reliability from a fragmented farmer base. Processing and value-added manufacturing create the branding and margin advantages that organized players command, while cold-chain distribution sustains the freshness and quality premium that packaged dairy earns at retail.

Technology Landscape in the Dairy Industry

Automated Processing and Packaging Technology

Automated pasteurization, homogenization, and aseptic packaging enable large-scale, hygienic, and consistent dairy production. UHT and advanced packaging extend shelf life and support premium, export-ready portfolios. As demand for packaged and branded dairy grows, automation reduces labor dependence, improves quality control, and strengthens the organized sector's structural advantage over informal supply.

IoT-Enabled Cold Chain and Quality Monitoring

IoT sensors, real-time temperature tracking, and quality-analytics tools are transforming cold-chain management. These technologies minimize spoilage, ensure food safety, and enable traceability from farm to retail. As perishable and premium dairy distribution expands, connected cold-chain systems help operators maintain consistency, reduce wastage, and build consumer trust across value-added categories.

Digital Procurement and AI-Driven Demand Planning

Digital procurement platforms, automated farmer payments, and AI-based demand forecasting are streamlining upstream and downstream operations. Data-driven planning optimizes milk collection, inventory, and distribution, reducing costs and improving supply reliability. These tools support efficient scaling of procurement networks and enable dairy companies to respond quickly to shifting consumer demand.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Liquid Milk |

46.97% |

2025 |

|

Region |

Maharashtra |

11.60% |

2025 |

By Product Type

Liquid milk leads at 46.97% (2025). The liquid milk segment encompasses packaged, loose, toned, full-cream, and skimmed milk consumed as a daily staple across households. Its dominance is anchored by universal consumption, expanding cold-chain and doorstep delivery, and rising demand for hygienic, branded packaged milk in urban markets.

To access detailed market analysis, Request Sample

Value-added products collectively drive the next tier of demand. Ghee (9.84%), khoya (9.50%), and dairy sweets (9.29%) benefit from festive and traditional consumption, while curd (6.85%), paneer (5.75%), ice cream (2.50%), and buttermilk (1.91%) gain share on health-led and premium demand. The remaining products are grouped under others at 7.39%, reflecting a diversified and expanding value-added portfolio.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Maharashtra |

11.60% |

Led by dense cooperative and private processing networks, strong urban demand, and well-developed dairy distribution infrastructure. |

|

Uttar Pradesh |

10.50% |

Supported by the country's largest milk-producing base, rising organized-sector participation, and expanding processing capacity. |

|

Gujarat |

7.80% |

Anchored by strong cooperative federations, high milk output, and advanced value-added dairy manufacturing. |

|

Rajasthan |

7.30% |

Driven by large cattle populations, growing procurement networks, and rising demand for packaged dairy products. |

|

Tamil Nadu |

7.10% |

Backed by a strong Southern dairy base, cooperative and private processing, and steady urban consumption across the state. |

|

Madhya Pradesh |

6.50% |

Growing on the back of expanding milk production, procurement scale-up, and increasing organized-sector reach across districts. |

|

Karnataka |

6.20% |

Anchored by the strong Nandini cooperative network, high milk procurement, and rising demand for branded and value-added dairy. |

|

Delhi |

4.70% |

Driven by dense urban demand, high per-capita consumption, and a strong presence of branded packaged milk and value-added products. |

|

West Bengal |

4.50% |

Supported by large rural milk production, growing cooperative participation, and rising demand for traditional and packaged dairy. |

|

Andhra Pradesh |

4.20% |

Backed by strong private and cooperative dairies, high buffalo-milk output, and expanding value-added product manufacturing. |

|

Bihar |

3.80% |

Growing on the back of a large milch-animal population, expanding cooperative procurement, and rising rural and urban demand. |

|

Haryana |

3.40% |

Driven by high per-animal productivity, strong milk output, and growing organized procurement and processing capacity. |

|

Kerala |

3.20% |

Supported by cooperative-led procurement, high per-capita consumption, and steady demand for packaged milk and dairy products. |

|

Punjab |

3.20% |

Anchored by high milk yields, a strong dairy-farming base, and expanding branded and value-added dairy production. |

|

Telangana |

3.10% |

Backed by growing private and cooperative dairies, rising urban demand, and expanding cold-chain and processing infrastructure. |

|

Orissa |

2.60% |

Growing on the back of expanding cooperative networks, increasing milk production, and rising demand for packaged dairy. |

|

Others |

10.30% |

A diversified base of other states and union territories contributing through regional cooperatives, private dairies, and steady local consumption. |

Maharashtra's 11.60% leadership is anchored by mature cooperative and private processing clusters and strong urban demand, while Uttar Pradesh's 10.50% reflects the nation's largest milk-producing base. Gujarat's cooperative strength and value-added manufacturing further reinforce the concentration of dairy activity in western and northern India.

Southern states led by Tamil Nadu contribute strong cooperative and private dairy output, while the broad base of other states collectively accounts for 49.20% of the market. Rising procurement scale-up and organized-sector penetration across emerging regions are expected to gradually diversify India's regional dairy landscape through the forecast period.

Competitive Landscape

The Indian dairy competitive landscape spans large cooperative federations, private dairy companies, and multinational players. Competition centers on procurement scale, brand strength, product breadth, and distribution reach, with leading players expanding value-added portfolios and cold-chain networks to consolidate share.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

Gujarat Cooperative Milk Marketing Federation Ltd. |

Amul |

Market Leader |

Unmatched procurement scale, cooperative network, and nationwide brand equity across milk and value-added dairy categories. |

|

Mother Dairy Fruits & Vegetables Pvt. Ltd. |

Mother Dairy |

Market Leader |

Integrated supply chain, strong North India presence, and a trusted branded milk and value-added portfolio. |

|

Nestlé S.A. (Nestlé India Ltd.) |

Nestlé, a+ |

Established Player |

Strong R&D, premium branded nutrition products, and wide urban distribution reach across the dairy portfolio. |

|

Parag Milk Foods Ltd. |

Gowardhan, Go |

Established Player |

Focused value-added portfolio spanning ghee, cheese, and paneer with a growing branded presence. |

|

Heritage Foods Ltd. |

Heritage |

Established Player |

Strong South and West India footprint with integrated procurement and value-added dairy. |

|

Hatsun Agro Product Ltd. |

Arokya, Hatsun |

Established Player |

India's largest private dairy, with deep Southern reach across milk and ice cream. |

|

Karnataka Co-operative Milk Producers Federation Ltd. |

Nandini |

Regional Leader |

Dominant Southern cooperative with strong procurement and a trusted branded milk portfolio. |

Cooperative federations retain structural advantages through vast rural procurement networks and brand trust, while private and multinational players compete on premiumization, innovation, and value-added categories. Consolidation reflects the growing preference for integrated, quality-assured, and branded dairy suppliers as the organized sector expands.

Key Company Profiles

Gujarat Cooperative Milk Marketing Federation Ltd.

Gujarat Cooperative Milk Marketing Federation Ltd., which markets the Amul brand, is India's largest dairy organization and the country's leading marketer of milk and value-added dairy products. Backed by a vast cooperative procurement network, it operates across liquid milk, ghee, butter, cheese, ice cream, and beverages nationwide.

- Key Brands: Amul milk, Amul Butter, Amul Ghee, Amul Ice Cream, and Amul Cheese.

- Recent Developments: Continued expansion of processing capacity, value-added portfolios, and deeper rural procurement to strengthen nationwide market leadership.

- Strategic Focus: Portfolio diversification, capacity additions, cold-chain expansion, and premium and health-positioned dairy innovation.

Mother Dairy Fruits & Vegetables Pvt. Ltd.

Mother Dairy Fruits & Vegetables Pvt. Ltd. is a leading branded dairy company with a strong presence in North India across milk, curd, cultured products, and edible oils. It operates an integrated supply chain and a trusted brand spanning token milk, packaged milk, and value-added dairy.

- Key Brands: Mother Dairy milk, Mother Dairy Dahi, Nutrifit, and Classic products.

- Recent Developments: Expansion of packaged and premium value-added categories alongside modern retail, D2C, and quick-commerce distribution.

- Strategic Focus: Growth in value-added dairy, cold-chain strengthening, and deeper urban and digital consumer reach.

Market Concentration Analysis

The Indian dairy market is moderately fragmented, with a large unorganized base of small farmers and local vendors coexisting alongside a consolidating organized segment. At the branded tier, a handful of cooperative federations and top private dairies command significant share, while numerous regional players retain strong local strongholds. Market concentration is gradually increasing in the organized segment through capacity expansion, brand consolidation, and value-added portfolio growth, even as the broader supply base remains highly distributed across states.

Investment & Growth Opportunities

Highest Growth Segments

Value-added and premium categories represent the highest-growth investment vectors through 2034. Paneer, cheese, functional and Greek yogurt, ice cream, A2 and organic milk, and fortified dairy record above-market CAGRs on the back of premiumization and health-led demand. Cold-chain infrastructure, processing capacity, and direct-to-consumer distribution are complementary high-potential investment areas across urban and semi-urban markets.

Emerging Investment Opportunities

Value-added dairy manufacturing and cold-chain build-out represent the largest near-term opportunities. Companies establishing scaled processing capacity, traceable procurement, and last-mile cold chains are positioned for above-market growth as branded and premium demand accelerates. Export-ready processing and clean-label sourcing offer additional long-term, differentiated revenue potential.

Investment Themes

- Premium and functional dairy platforms: Investment in A2, organic, high-protein, and fortified dairy captures affluent, health-focused consumers at higher margins. Companies building specialized sourcing, certification, and branded portfolios by 2026-2027 are positioned to lead the premiumization wave across urban markets and modern retail channels.

- Digital distribution and cold-chain infrastructure: D2C platforms, quick-commerce partnerships, and IoT-enabled cold chains create scalable, high-margin, direct consumer relationships. Investment in last-mile refrigeration, traceability, and app-based ordering builds durable competitive advantage as branded dairy demand expands beyond traditional retail networks.

Future Market Outlook (2026-2034)

The dairy industry in India is projected to grow from INR 12,730.4 Billion in 2025 to INR 41,696.39 Billion by 2034, delivering a 14.14% CAGR over the forecast period. The market's anchor value of INR 24,365.0 Billion in 2030 marks a phase of accelerated formalization, in which organized and branded dairy progressively displaces unorganized supply, value-added categories mainstream across urban and semi-urban markets, and cold-chain and digital distribution reshape how dairy reaches consumers nationwide.

Three structural forces define market growth through 2034. Rising incomes and urbanization sustain durable demand growth in both liquid milk and premium value-added dairy. Health and nutrition awareness accelerates the shift toward functional, A2, organic, and protein-rich products. Continued investment in procurement, cold chain, technology, and sustainability strengthens supply reliability and organized-sector advantage, positioning India's dairy industry for sustained, above-trend expansion.

Research Methodology

Primary Research

Primary research comprised structured interviews with industry stakeholders (2025), including dairy processing executives, cooperative federation leaders, procurement and supply-chain heads, distribution and retail specialists, and regional dairy market experts across India.

Secondary Research

Secondary research encompassed dairy industry publications; cooperative and company annual reports; government and agricultural statistics; trade data; and market databases. Multiple secondary sources were reviewed and triangulated to ensure accuracy across product and regional segments.

Forecasting Models

Market revenue forecasts were developed using a combination of top-down and bottom-up models across (i) liquid milk, (ii) value-added products, and (iii) regional demand components, triangulated for consistency and accuracy.

Dairy Industry in India Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion INR |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

|

|

Regions Covered |

Karnataka, Maharashtra, Tamil Nadu, Delhi, Gujarat, Andhra Pradesh and Telangana, Uttar Pradesh, West Bengal, Kerala, Haryana, Punjab, Rajasthan, Madhya Pradesh, Bihar, Orissa |

|

Companies Covered |

Gujarat Cooperative Milk Marketing Federation Ltd., Mother Dairy Fruits & Vegetables Pvt. Ltd., Nestle S.A. (Nestle India Ltd.), Parag Milk Foods Ltd., Heritage Foods Ltd., Hatsun Agro Product Ltd., Karnataka Co-operative Milk Producers' Federation Ltd., etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Dairy Industry in India Report

The dairy industry in India reached INR 12,730.4 Billion in 2025. Growth is driven by rising per-capita consumption, urbanization, higher disposable incomes, and a decisive shift toward branded and value-added dairy products. Expanding cooperative and private procurement, cold-chain modernization, and the rapid rise of D2C and quick-commerce channels further support market growth.

The market is projected to grow at a 14.14% CAGR during 2026-2034, reaching INR 41,696.39 Billion by 2034. Value-added categories such as paneer, ice cream, and curd grow fastest, driven by premiumization, health-led demand, and expanding cold-chain and branded reach across urban and semi-urban markets.

Liquid milk leads at 46.97% in 2025 as a daily nutritional staple consumed across all income tiers. Value-added products such as ghee, khoya, dairy sweets, curd, and paneer form the next tier of demand and are gaining share on premiumization, health awareness, and expanding organized branding.

Maharashtra leads with an 11.60% share in 2025, supported by strong cooperative and private processing networks and robust urban demand. Uttar Pradesh follows at 10.50%, anchored by the country's largest milk-producing base and expanding organized-sector participation across high-output districts.

Leading players include Gujarat Cooperative Milk Marketing Federation Ltd. (Amul), Mother Dairy Fruits & Vegetables Pvt. Ltd., Nestle S.A. (Nestle India Ltd.), Parag Milk Foods Ltd., Heritage Foods Ltd., Hatsun Agro Product Ltd., and Karnataka Co-operative Milk Producers' Federation Ltd. (Nandini). Competition centers on procurement scale, brand strength, and value-added portfolios.

Key drivers include rising per-capita consumption, the expanding organized and branded segment, cooperative and private procurement scale-up, and cold-chain and technology modernization, supported by premiumization and digital distribution.

The market is projected to reach approximately INR 24,365.0 Billion by 2030, supported by rising branded penetration, value-added premiumization, and continued cold-chain and procurement investment across high-output states such as Maharashtra, Uttar Pradesh, and Gujarat.

The organized dairy segment is expanding steadily as cooperatives and private players invest in branded portfolios, cold chains, and quality assurance. Modern retail, packaging, and direct-to-consumer distribution are shifting share from unorganized supply, improving realizations, traceability, and product consistency across dairy categories.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade