Data Center Generator Market Size, Share, Trends and Forecast by Product, Capacity, Tier, and Region, 2026-2034

Global Data Center Generator Market Size, Share, Trends & Forecast (2026-2034)

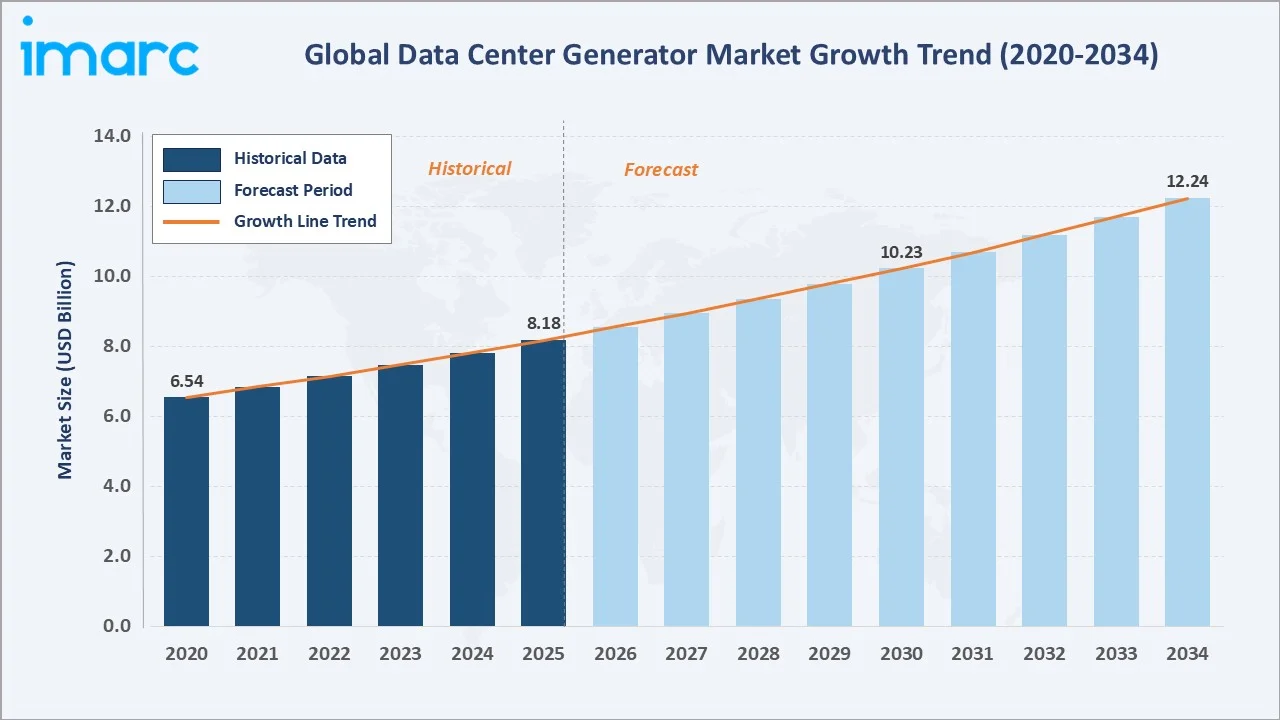

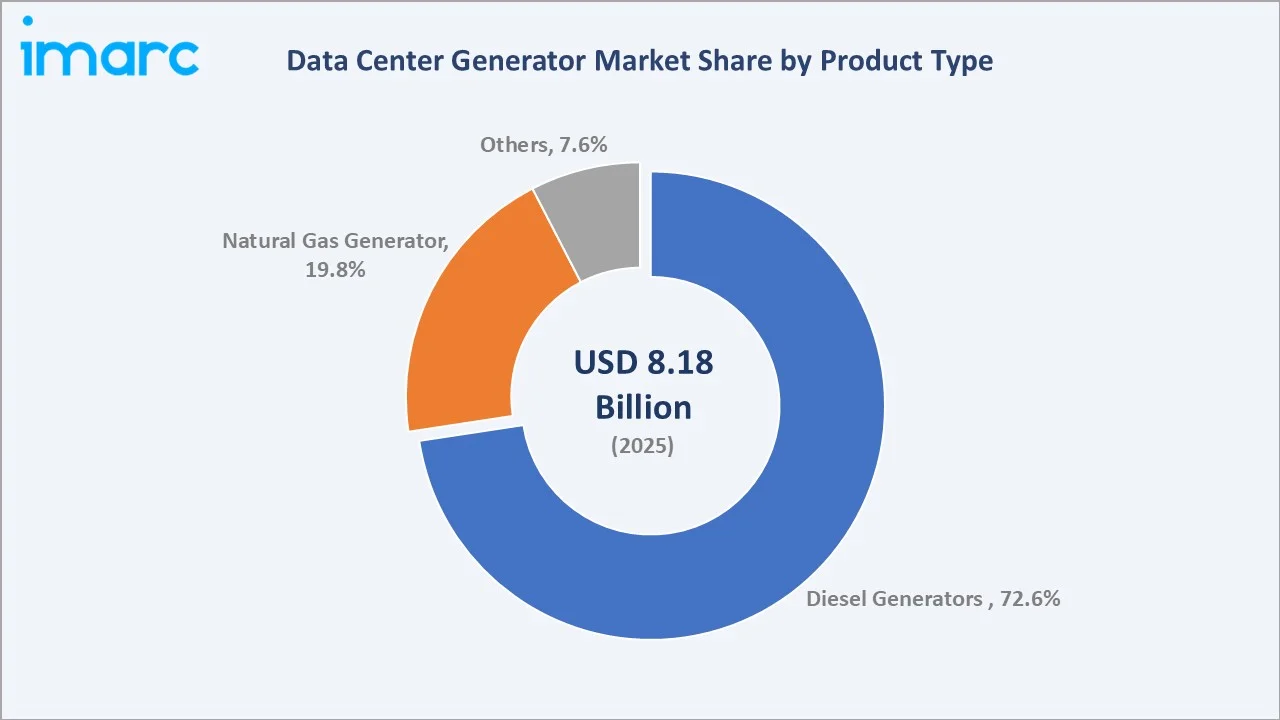

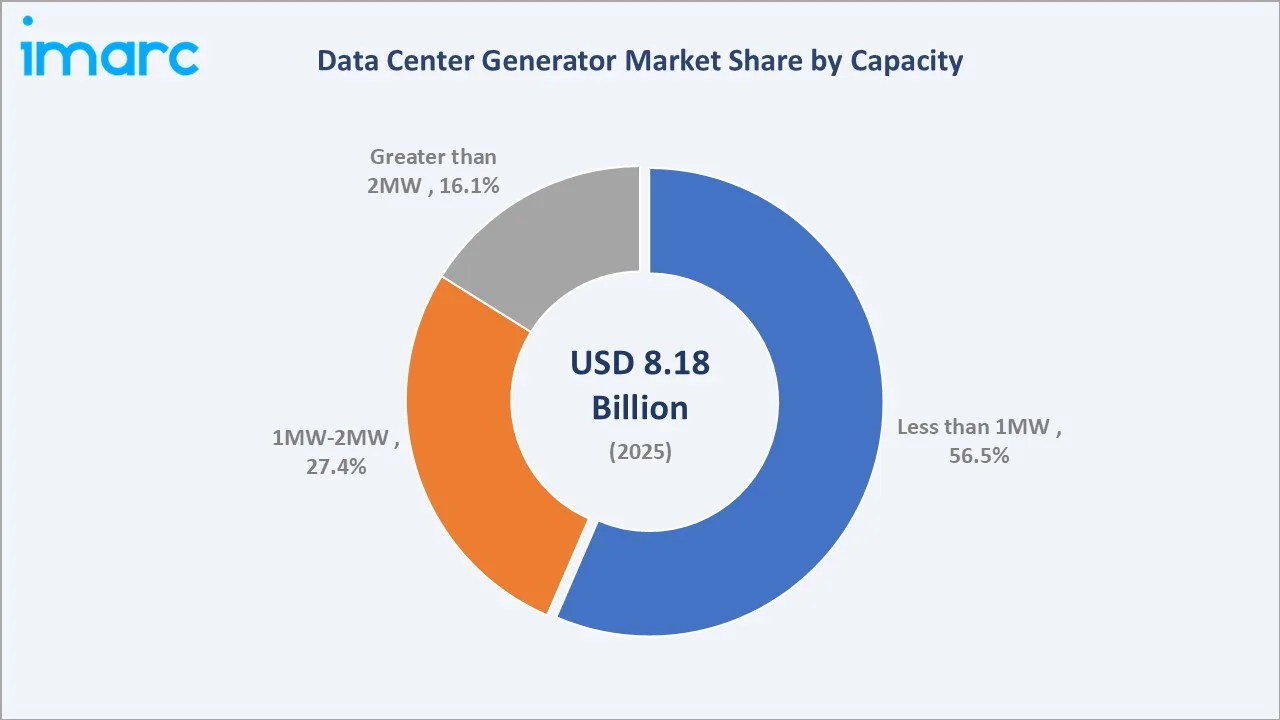

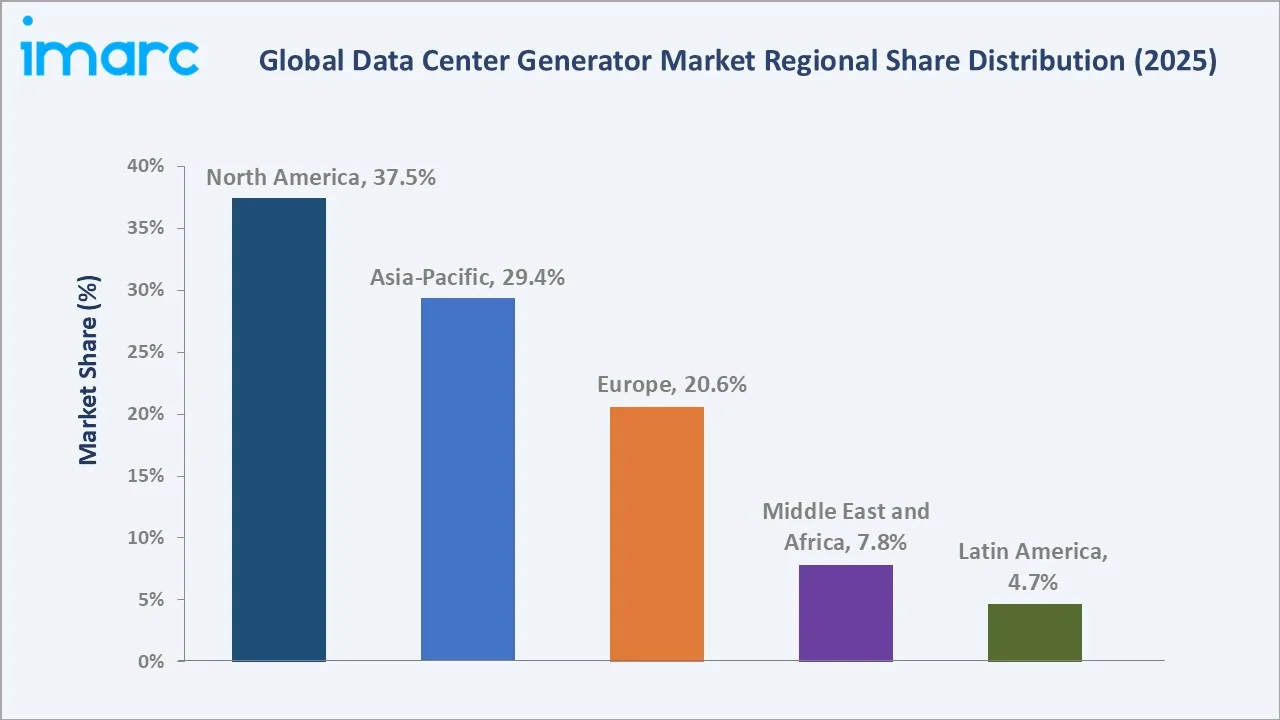

The global data center generator market size was valued at USD 8.18 Billion in 2025 and is projected to reach USD 12.24 Billion by 2034, exhibiting a CAGR of 4.58% during the forecast period 2026-2034. Surging demand for uninterruptible power supply across cloud and hyperscale infrastructure, rapid expansion of AI training data centers by Amazon, Google, Microsoft, and Meta, growing reliance on edge computing, and stringent government regulations mandating data center uptime and resilience are the primary factors driving the data center generator market growth. Diesel generators lead by product at 72.6% share in 2025, while the Less than 1MW capacity segment commands 56.5% of the market. North America accounts for 37.5% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.18 Billion |

|

Forecast Market Size (2034) |

USD 12.24 Billion |

|

CAGR (2026-2034) |

4.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Product Segment |

Diesel (72.6%, 2025) |

|

Leading Capacity Segment |

Less than 1MW (56.5%, 2025) |

The global data center generator market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by cloud infrastructure investments, AI workload surges, and edge computing deployments.

To get more information on this market, Request Sample

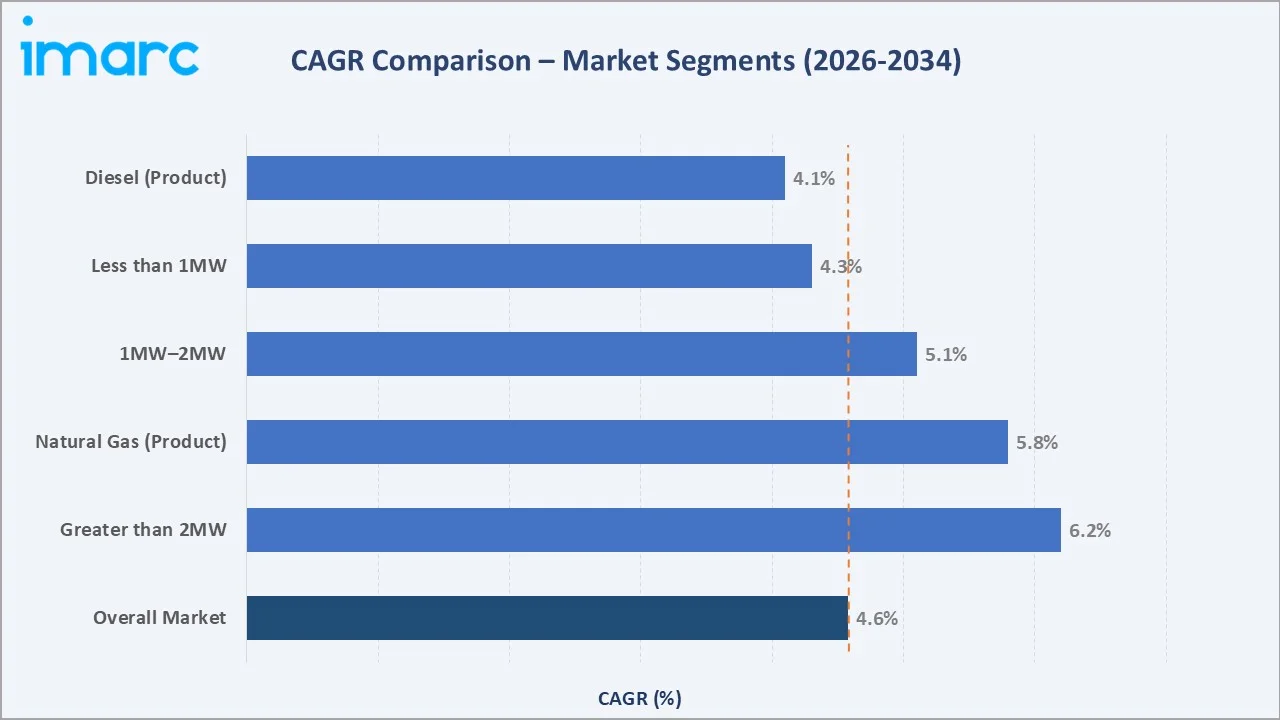

Segment-level CAGR comparisons highlighting natural gas generators and the greater than 2MW capacity tier as the two fastest-growing sub-categories within the global data center generator industry analysis through 2034.

Executive Summary

The global data center generator market is experiencing steady growth driven by rapid digitalization, AI-intensive workloads, and increasing demand for uninterrupted power supply. The market is projected to expand from USD 8.18 billion in 2025 to USD 12.24 billion by 2034, registering a CAGR of 4.58%. Diesel generators continue to dominate with a 72.6% share due to their reliability, quick start-up capability, and extended backup duration, making them essential for mission-critical operations. By capacity, systems below 1MW lead with 56.5% share, supported by the rise of edge computing and distributed data centers, while the above 2MW segment is the fastest-growing, driven by hyperscale facilities and large AI training clusters. Regionally, North America holds the largest share at 37.5%, led by the United States and increasing cybersecurity-driven uptime requirements, whereas Asia-Pacific (29.4%) is the fastest-growing region, fueled by strong capacity expansion in India, China’s cloud investments, and Southeast Asia’s digital economy growth. Overall, the market outlook remains positive, supported by continued AI investments, hyperscale infrastructure expansion, and the shift toward hybrid and lower-emission power solutions.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Diesel - 72.6% share (2025) |

|

Fastest Growing Product |

Natural Gas - ~5.8% CAGR (2026-2034) |

|

Largest Capacity Segment |

Less than 1MW - 56.5% share (2025) |

|

Fastest Growing Capacity |

Greater than 2MW - ~6.2% CAGR (2026-2034) |

|

Leading Region |

North America - 37.5% revenue share (2025) |

|

Top Companies |

Caterpillar, Cummins, Generac, Kohler, Rolls-Royce (MTU), Himoinsa (Yanmar), Mitsubishi Heavy Industries, Wärtsilä |

|

Market Opportunity |

AI-driven hyperscale build-outs and edge computing expansion |

Key Analytical Observations Supporting The Above Data:

- Diesel generators' 72.6% dominance in 2025 reflects their industry-standard role in critical-uptime environments such as Tier III and Tier IV data centers, where start-up within 10-15 seconds is a baseline requirement per Uptime Institute specifications. Caterpillar and Cummins together account for the majority of global diesel genset deployments in data centers above 1MW.

- Natural gas generators at ~19.8% share (2025) are gaining traction through lower emissions profiles, cost efficiency in regions with piped gas infrastructure, and alignment with corporate ESG commitments by hyperscale operators such as Microsoft and Google.

- Less than 1MW segment commands 56.5% due to the proliferation of edge micro-data centers, enterprise co-location requirements, and rapid deployment of 5G-enabled small cell data infrastructure across North America, Europe, and Asia-Pacific.

- North America's 37.5% leadership is anchored by stringent NFPA 110, ASHRAE, and Uptime Institute standards mandating redundant power infrastructure, supported by the Northern Virginia corridor hosting over 27 million square feet of data center space.

Global Data Center Generator Market Overview

Data center generators are essential backup systems that ensure uninterrupted operations during grid failures, supporting critical infrastructure across banking, healthcare, e-commerce, government, and communications. The market includes diesel, natural gas, and hybrid generators ranging from sub-100 kW portable units to large-scale systems exceeding 3 MW. Demand spans hyperscale cloud providers like Amazon Web Services, Google, and Microsoft Azure, as well as colocation leaders such as Equinix and Digital Realty, alongside enterprise and edge deployments.

Growth is driven by expanding cloud infrastructure spending, rapid proliferation of connected devices, increasing investment in data center capacity, and accelerating demand for AI computing. These factors are collectively strengthening the need for reliable backup power, supporting sustained demand for data center generators across all capacity segments through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

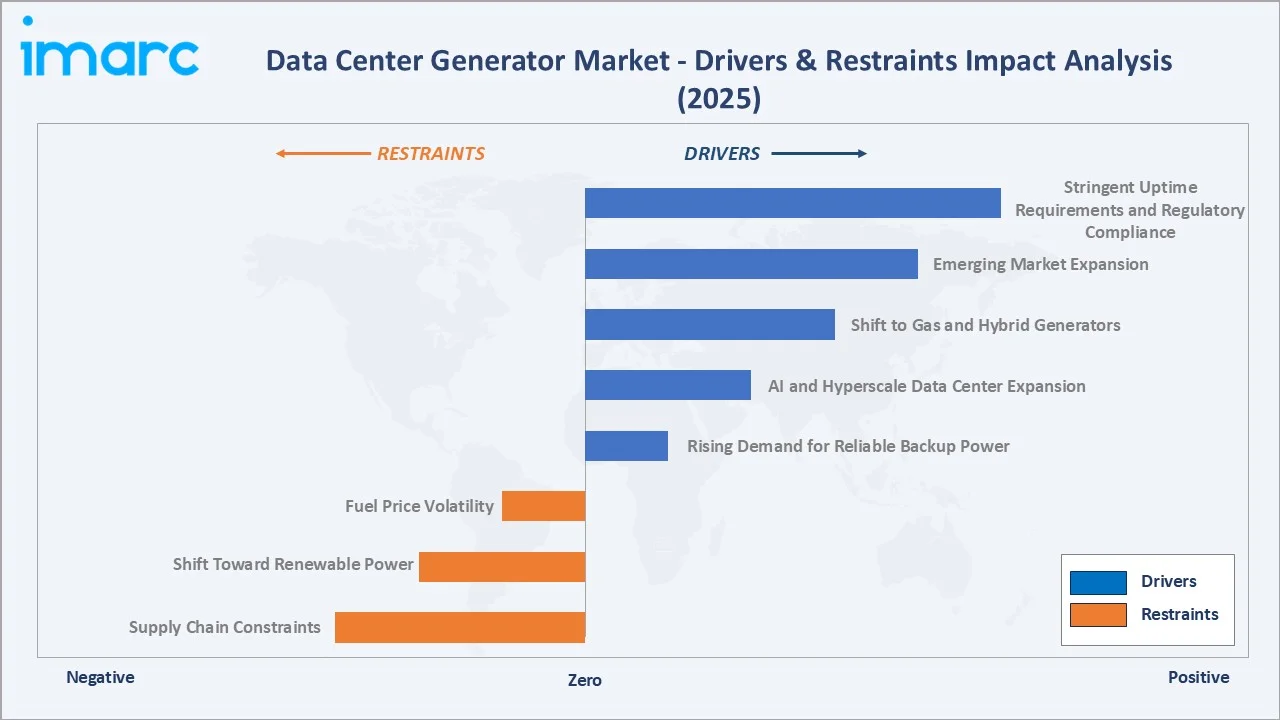

Market Drivers

- Rising Demand for Reliable Backup Power: As critical operations increasingly shift to digital platforms, continuous power availability has become essential. Industry standards such as the Uptime Institute Tier Classification System require high levels of redundancy and fault tolerance, making generator-backed power systems a core requirement for achieving stringent uptime targets in modern data centers.

- AI and Hyperscale Data Center Expansion: The rapid growth of AI workloads and cloud computing is accelerating hyperscale data center investments by leading technology companies. These large-scale facilities require multi-megawatt backup power infrastructure, significantly increasing demand for high-capacity generator systems to ensure operational continuity.

Market Restraints

- Fuel Price Volatility: Fluctuating diesel prices, driven by geopolitical factors, increase total cost uncertainty for operators managing large, multi-location generator fleets.

- Stringent Emission Regulations: Tightening standards such as EPA Tier 4 Final and Euro Stage V are raising compliance and procurement costs, particularly in regions with strict carbon reduction mandates like Europe.

Market Opportunities

- Shift to Gas and Hybrid Generators: Adoption of lower-emission gas and hybrid systems is rising, especially in regions with strong gas infrastructure, as operators align with ESG goals and reduce direct emissions.

- Emerging Market Expansion: Africa, Southeast Asia, and the Middle East are seeing rapid data center growth, creating new opportunities for generator suppliers amid limited competition and unreliable grid infrastructure.

Market Challenges

- Supply Chain Constraints: Semiconductor shortages have significantly extended lead times for generator components, while concentrated chip supply and geopolitical risks continue to pose structural challenges.

- Shift Toward Renewable Power: Growing adoption of renewable energy in data centers may reduce long-term reliance on diesel generators, pushing manufacturers toward low-emission alternatives like hydrogen and biofuels.

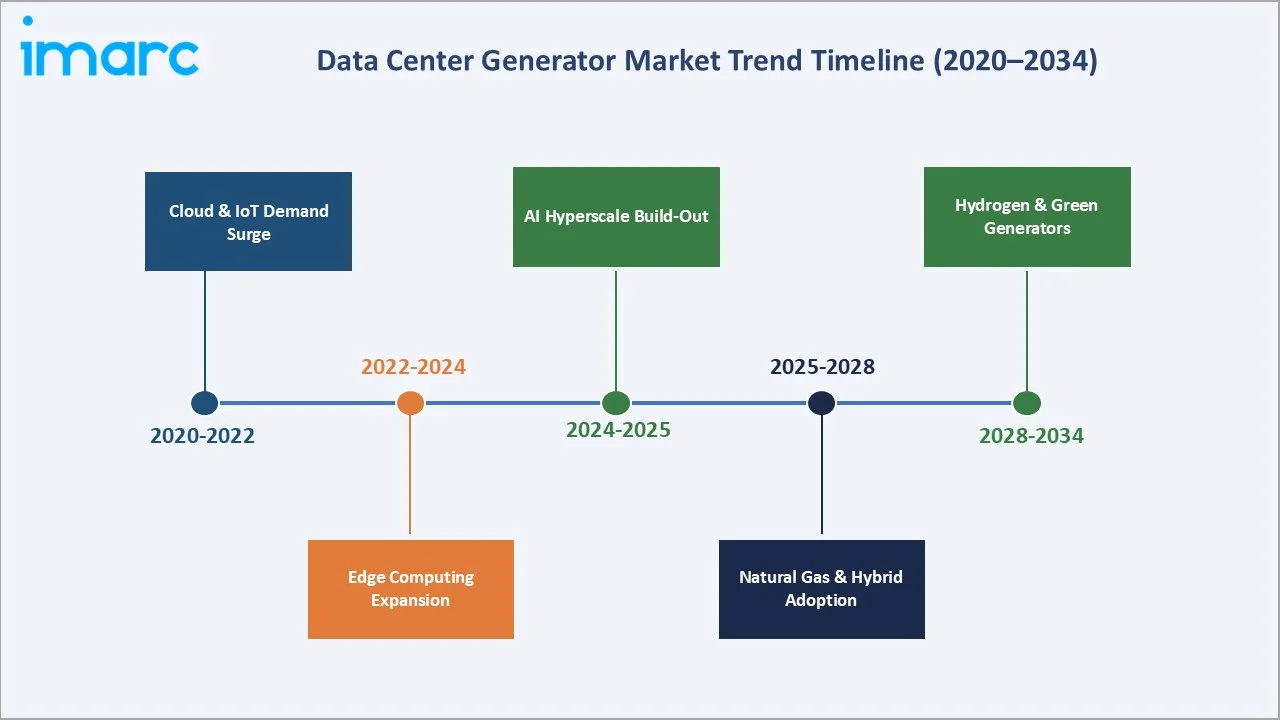

Emerging Market Trends

1. AI-Driven Hyperscale Power Demand Surge

The rapid expansion of AI workloads is significantly increasing data center power requirements, with hyperscale facilities growing from ~30 MW a decade ago to 200 MW+ today. This surge is driven by large-scale model training and high-density compute infrastructure deployed by cloud providers like Microsoft, Google, and AWS.

2. Hybrid Generator-BESS-Solar Microgrid Deployments

AI-driven load variability is accelerating adoption of hybrid power systems combining generators with battery energy storage systems (BESS). Batteries are increasingly used to stabilize sudden power spikes and complement traditional backup systems, improving efficiency and reducing reliance on continuous generator usage.

3. Natural Gas and Alternative Fuel Generator Transition

Data center operators are actively exploring alternative energy solutions, including hydrogen fuel cells and integrated power generation. These technologies are emerging as long-term solutions to meet both reliability and decarbonization goals as energy demands rise with AI expansion.

4. Modular and Containerized Generator Deployments

The expansion of hyperscale and edge data centers is driving demand for flexible, rapidly deployable infrastructure solutions. Reliable backup systems, including modular generator configurations, are critical to maintaining uptime and supporting fast capacity scaling in distributed environments.

5. Digital Monitoring and Predictive Maintenance Platforms

Advancements in digital power management, including real-time monitoring and predictive maintenance, are improving operational reliability. These technologies are becoming essential as data centers handle increasingly dynamic and high-density workloads driven by AI.

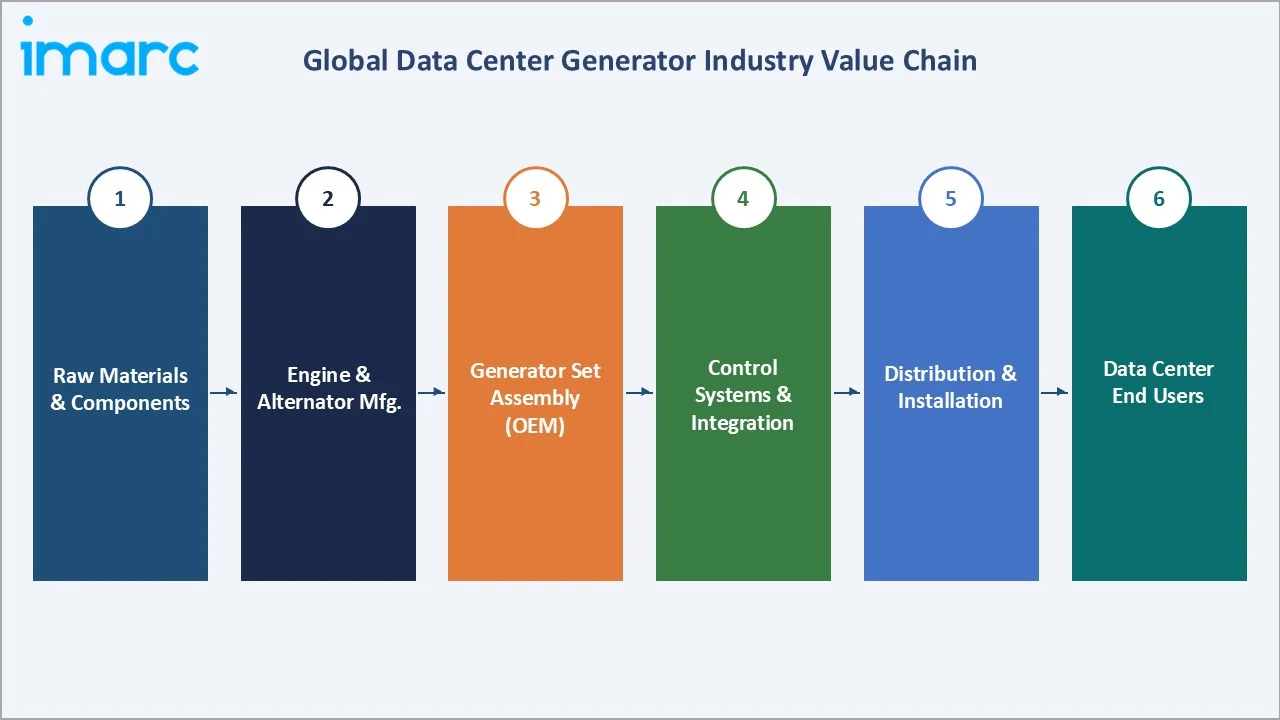

Industry Value Chain Analysis

The data center generator value chain spans six integrated stages from raw material supply through end-user facility management. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements that shape the competitive structure of the global data center generator industry.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Steel, copper, alternator cores, fuel injection components - Bosch, Delphi Technologies, Parker Hannifin |

|

Engine & Alternator Manufacturing |

Perkins Engines (Caterpillar), Cummins Engine Business, MTU Friedrichshafen, Kohler Engine Division |

|

Generator Set Assembly (OEM) |

Caterpillar (Cat Electric Power), Cummins Power Generation, Generac Industrial, Kohler Power Systems, Rolls-Royce (MTU), Himoinsa (Yanmar), Mitsubishi Heavy Industries, Wärtsilä |

|

Control Systems & Integration |

ABB, Schneider Electric, Vertiv, Eaton - providing switchgear, ATS, digital monitoring, and DCIM platforms |

|

Distribution & Installation |

Authorized dealer networks, MEP contractors, EPC firms - Turner Construction, AECOM, Jacobs Engineering |

|

Data Center End Users |

AWS, Google, Microsoft Azure, Meta, Equinix, Digital Realty, enterprise IT, and co-location facility operators |

Generator OEMs hold the highest strategic value in the data center market, integrating engines, alternators, and controls into turnkey sets. Caterpillar, Cummins, and Rolls-Royce (MTU) lead high-capacity installations, while Himoinsa (Yanmar), Mitsubishi Heavy Industries, and Wärtsilä grow in niche and emerging markets.

Technology Landscape in the Data Center Generator Industry

Diesel Engine Technology: Tier 4 Final and Emission Compliance

Modern data center generators use advanced diesel platforms with SCR and DPF systems to meet stringent emission norms like EPA Tier 4 Final. High-capacity engines such as Caterpillar 3516E and Cummins QSK95 deliver multi-megawatt output and fast start-up, aligned with International Organization for Standardization (ISO 8528) and Uptime Institute requirements.

Natural Gas and Dual-Fuel Systems

Gas and dual-fuel generators offer lower emissions and fuel flexibility, gaining traction in regions with strong gas infrastructure. Solutions like GE Jenbacher engines and Caterpillar CG170 series are increasingly used for cleaner and space-efficient operations.

Advanced Control Systems and Remote Monitoring

Digital control platforms such as Cummins PowerCommand 3300 and Caterpillar EMCP 4 enable load sharing, automation, and real-time monitoring, improving reliability and reducing downtime.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Diesel |

72.6% |

2025 |

|

Capacity |

Less than 1MW |

56.5% |

2025 |

|

Tier |

Tier I & II |

52.3% |

2025 |

|

Region |

North America |

37.5% |

2025 |

By Product

Diesel generators lead the data center generator market with a commanding 72.6% share in 2025. Their dominance reflects mission-critical performance requirements of data center operators - specifically the industry-standard 10-second load pick-up specification required by Uptime Institute Tier III and Tier IV classifications. Diesel's energy density, fuel storage viability for 72+ hour run autonomy, and established maintenance infrastructure across global geographies make it the preferred choice for primary backup power at hyperscale and co-location facilities.

To access detailed market analysis, Request Sample

Natural gas generators hold a 19.8% share in 2025and represent the fastest-growing product segment at approximately 5.8% CAGR through 2034. The shift is driven by corporate sustainability targets from hyperscale operators, regulatory tailwinds in Europe favouring lower-emission fuels, and operational cost advantages in regions with well-developed gas infrastructure. Others - including hydrogen fuel cells, HVO biofuel-compatible units, and dual-fuel hybrid systems - represent 7.6% in 2025 but are projected to gain meaningful share through 2034 as hydrogen infrastructure matures and green fuel mandates expand.

By Capacity

The Less than 1MW capacity segment dominates at 56.5% in 2025, reflecting the large installed base of enterprise data centers, co-location facilities, and edge computing nodes that require cost-effective, space-efficient generator solutions. This segment is driven by the global proliferation of small and mid-scale data infrastructure - from hospital server rooms to retail fulfilment centers and telecommunications edge nodes. Generac and Kohler are prominent suppliers in this sub-1MW tier, offering standardized packaged genset solutions with rapid deployment capabilities.

The 1MW-2MW capacity segment captures 27.4% in 2025, serving mid-tier co-location campuses and regional enterprise data centers, favoured for N+1 generator configurations in facilities with 5-20MW total IT load. The Greater than 2MW segment, at 16.1% in 2025, is the fastest-growing capacity tier at approximately 6.2% CAGR through 2034 - driven exclusively by hyperscale campus developments in Northern Virginia, Dublin, Singapore, and Tokyo, where individual generator sets of 2-4MW are deployed in banks of 10-20 units to serve 100MW+ campus power requirements.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.5% |

US hyperscale cloud campuses, NFPA 110 compliance, AI data center build-outs, cyber threat resilience |

|

Asia-Pacific |

29.4% |

India 500+ MW pipeline, China state cloud investment, Singapore/Tokyo hyperscale, SEA digital economy |

|

Europe |

20.6% |

EU data sovereignty rules, GDPR compliance, UK resilience mandates, Nordic green data center growth |

|

Middle East and Africa |

7.8% |

Saudi Vision 2030, UAE/Qatar mega-data centers, sub-Saharan digital infrastructure, grid instability |

|

Latin America |

4.7% |

Brazil/Mexico data localization laws, growing cloud adoption, FinTech, and e-commerce expansion |

Asia-Pacific commands a 29.4% global revenue share in 2025 and is the fastest-growing region. China is the single most important national market within Asia-Pacific, combining rapid expansion of state-backed cloud computing parks with the world's most aggressive AI infrastructure build-out programs.

North America, with 37.5% in 2025, is anchored by the United States, which hosts the world’s largest hyperscale capacity, particularly in Northern Virginia. Strong demand from cloud and AI workloads, combined with established standards such as NFPA 110 and Uptime Institute Tier requirements, ensures structured deployment of reliable backup power infrastructure.

Europe, at 20.6%, is driven by regulatory frameworks including GDPR and data sovereignty mandates, with growth concentrated in FLAP-D markets and emerging Nordic hubs. However, expansion is increasingly constrained by power availability and environmental regulations despite sustained demand.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Caterpillar Inc. |

Cat Electric Power / EMCP 4 |

Leader |

Largest global dealer network, high-capacity diesel gensets, Cat Connect IoT monitoring |

|

Cummins Inc. |

Cummins Power Generation / PowerCommand |

Leader |

Engine technology depth, dual-fuel capability, 190-country service network |

|

Generac Holdings Inc. |

Generac Industrial / Mobile Link |

Leader |

Sub-1MW segment dominance, North American market depth, and modular rapid deployment |

|

Kohler Co. |

Kohler Power Systems |

Challenger |

Full-range gensets, premium reliability, utility-grade industrial solutions |

|

Rolls-Royce (MTU) |

MTU Series 4000 / Master Control System |

Challenger |

High-performance large gensets, European market leadership, gas engine technology |

|

Himoinsa (Yanmar) |

Himoinsa HYW / HFW Series |

Challenger |

Wide capacity range, global distribution, hybrid, and gas generator expertise |

|

Mitsubishi Heavy Industries |

MHI Turbocharger / MGS Series |

Challenger |

Heavy-duty industrial gensets, Asia-Pacific market strength, engineering reliability |

|

Wärtsilä |

Wärtsilä 34DF / Energy Storage |

Emerging |

Flexible fuel engines, hybrid power solutions, energy management integration |

The global data center generator competitive landscape is characterized by a core group of established OEMs - Caterpillar, Cummins, and Generac - commanding a combined estimated market share of 40-50% in 2025, followed by Kohler and Rolls-Royce (MTU) as the leading challengers. Himoinsa (Yanmar), Mitsubishi Heavy Industries, and Wärtsilä represent significant players expanding their data center generator presence across Asia-Pacific, Europe, and emerging markets through hybrid and flexible-fuel product strategies.

Key Company Profiles

Caterpillar Inc.

Caterpillar leads the global data center generator market, with Cat Electric Power serving all capacity tiers (6 kW–4 MW+) and a global dealer network of 190+ countries, supported by its Cat Connect digital monitoring platform for advanced service and performance management.

- Product & Platform Portfolio: Cat 3516E series (2MW+), Cat XQC1600, containerized modular gensets, Cat EMCP 4 digital control platform, Cat Connect remote monitoring and predictive maintenance platform, HVO-compatible generator configurations.

- Recent Developments: In August 2025, Caterpillar entered a strategic partnership with Hunt Energy (Aug 2025) to deliver scalable, off-grid, and hybrid power solutions for data centers, targeting ~1 GW capacity deployments in North America.

- Strategic Focus: Caterpillar is investing in hydrogen-ready engine platforms and alternative fuel generator sets, aligning with hyperscale operator sustainability roadmaps. The company's strategy centers on Cat Connect digital services expansion, modular containerized generator systems for edge computing deployments, and large-capacity multi-megawatt solutions for AI training campus build-outs.

Cummins Inc.

Cummins Power Generation is the world’s second-largest data center generator supplier, strong in 500 kW–3 MW and dual-fuel diesel/natural gas solutions, with integrated engine and alternator manufacturing, and its PowerCommand system enabling advanced multi-unit hyperscale management.

- Product & Platform Portfolio: QSK95 series (3.8MW), C3500D6, PowerCommand 3300 controller, C-Gas gensets (natural gas), Cummins transfer switches and paralleling switchgear, New Power hydrogen and fuel cell platforms.

- Recent Developments: In June 2025, Cummins launched a new Centum Series (S17) generator platform, supporting higher power density and compatibility with low-carbon fuels such as HVO.

- Strategic Focus: Multi-fuel flexibility across diesel, natural gas, hydrogen, and HVO, supported by a global service network in 190 countries with 24/7 technical support capabilities. Cummins is positioning PowerCommand as a cloud-connected generator fleet management platform to capture recurring digital services revenue alongside traditional hardware sales.

Rolls-Royce (MTU)

Rolls-Royce Power Systems’ MTU brand is a leading European supplier of high-performance generators, with the MTU Series 4000 serving as a benchmark for large-capacity diesel generators in Tier III and IV data centers across Europe, the Middle East, and Asia-Pacific.

- Product & Platform Portfolio: MTU Series 4000 (up to 3.3MW per unit), MTU Series 2000, MTU Master Control System (MCS), dual-fuel, and gas engine variants, MTU OnCall 24/7 remote monitoring and diagnostics platform.

- Recent Developments: In October 2025, Rolls-Royce (MTU) introduced next-gen mtu Series 4000 gas generators (2025) with fast-start capability (as low as 45 seconds), specifically designed for AI-driven data center loads.

- Strategic Focus: MTU's data center strategy focuses on high-power-density generator systems for hyperscale and Tier IV facilities, with premium reliability positioning in the European market. The company is investing in remote diagnostics, predictive maintenance software, and dual-fuel flexibility to address both performance and sustainability requirements of major cloud operators.

Market Concentration Analysis

The global data center generator market exhibits moderate concentration among the top-tier OEMs, with Caterpillar, Cummins, and Generac collectively accounting for an estimated 40-50% of global revenue in 2025. The top eight players - adding Kohler, Rolls-Royce (MTU), Himoinsa (Yanmar), Mitsubishi Heavy Industries, and Wärtsilä - represent 65-75% of market value, reflecting a market where engineering complexity, global service network scale, and certification requirements create meaningful barriers to entry.

Market fragmentation is highest in the sub-500 kW segment, where regional and Asian manufacturers compete aggressively on price. Himoinsa and Mitsubishi Heavy Industries are gaining share across Asia-Pacific and emerging markets, while Wärtsilä is strengthening its position in hybrid and flexible-fuel, large-capacity systems.

Competition is shifting toward integrated solutions, with OEMs investing in digital monitoring, remote diagnostics, and energy management platforms. As a result, differentiation is moving beyond hardware to software-driven, recurring revenue models, while DCIM and building management software players are increasingly entering the power infrastructure layer.

Investment & Growth Opportunities

Fastest-Growing Segments

Greater than 2MW generators are the highest-growth capacity sub-segment at approximately 6.2% CAGR through 2034, driven by hyperscale AI campus build-outs where single-campus power loads exceed 100MW. Natural gas generators at 5.8% CAGR represent the fastest-growing product category, enabled by expanding gas infrastructure, corporate decarbonization commitments, and EU regulatory pressure on diesel emissions. Modular containerized generator solutions for edge deployments are growing fastest in volume unit terms, aligned with the 5G edge computing build-out across Asia-Pacific, North America, and Europe.

Emerging Market Expansion

Sub-Saharan Africa, Southeast Asia, and the GCC present high-growth frontier opportunities where grid instability elevates generators from backup to primary power, significantly expanding the addressable market per MW of installed IT capacity. Nigeria, Kenya, and South Africa are seeing their first hyperscale data center campuses, while Saudi Arabia's NEOM project and Vision 2030 smart city investments are attracting significant data center capital. Indonesia and Vietnam represent rapidly emerging Southeast Asian markets with growing cloud adoption and limited existing generator infrastructure.

Venture & Private Investment Trends

Private equity investment in data centers has been significant, with firms such as KKR and Blackstone leading major acquisitions and platform builds — for example, KKR’s ~$15 billion acquisition of CyrusOne in H1 2022. These activities illustrate sustained infrastructure investment appetite, but specific aggregated deal value totals (such as “USD 24 billion in H1 2022” or precise totals through 2024–2025) are not explicitly reported in publicly available market overviews.

Future Market Outlook (2026-2034)

The global data center generator market forecast projects steady value expansion from USD 8.18 Billion in 2025 to USD 12.24 Billion by 2034 at a CAGR of 4.58%, representing a near 50% increase in market value underpinned by AI workload-driven hyperscale growth, rising edge computing infrastructure investment, and ongoing digital transformation across emerging economies in Asia-Pacific, the Middle East, and Africa.

Three key forces will shape the data center generator market through 2034. Rapid AI growth will drive multi-megawatt installations at hyperscale campuses, while the fuel mix shifts toward natural gas, hydrogen, and hybrid systems, reducing diesel’s share from 72.6% in 2025 to 60–65% by 2034. Digital generator platforms with predictive maintenance and remote monitoring will become standard, creating recurring software and service revenue. By 2034, the market will split into two battlegrounds: hyperscale campuses dominated by Caterpillar, Cummins, and Rolls-Royce (MTU), and edge/enterprise sub-1MW deployments led by Generac, Kohler, and Himoinsa (Yanmar), with Wärtsilä and Mitsubishi Heavy Industries expanding through flexible-fuel and hybrid solutions.

Research Methodology

Primary Research

Primary research included interviews with data center operations directors, hyperscale procurement managers, generator OEMs, electrical contractors, and infrastructure investors, providing insights to validate market size, capacity splits, regional demand, technology adoption, and competitive positioning across the global data center generator market.

Secondary Research

Secondary sources include IMARC Group proprietary databases, Uptime Institute Global Data Center Survey (2024), IEA Global Energy Outlook,, company annual reports (Caterpillar, Cummins, Generac), Cushman & Wakefield Data Center Market Outlook, CBRE Data Center Trends, UK Government Data Infrastructure Consultation (2023), EPA Tier 4 emission regulation publications, NFPA 110 standards documentation, and trade publications including Data Center Dynamics, DCD Magazine, and Power Engineering International.

Forecasting Models

Market size estimations used a combination of bottom-up capacity-based models - estimating generator requirements per MW of data center IT load by region and facility type - and top-down macroeconomic correlations with cloud spend, digital economy GDP contribution, and infrastructure investment indices. Scenario analysis across base, optimistic, and conservative cases was applied to account for AI workload growth uncertainty, green transition pace, and emerging market expansion rate variability.

Data Center Generator Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Diesel, Natural Gas, Others |

| Capacities Covered | Less than 1MW, 1MW–2MW, Greater than 2MW |

| Tiers Covered | Tier I and II, Tier III, Tier IV |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Germany, France, United Kingdom, Italy, Spain, Russia, Indonesia, Brazil, Mexico |

| Companies Covered | Caterpillar Inc., Cummins Inc., Generac Holdings Inc., Kohler Co., Rolls-Royce (MTU), Himoinsa (Yanmar), Mitsubishi Heavy Industries, Wärtsilä, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the data center generator market from 2020-2034.

- The data center generator market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the data center generator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Data Center Generator Market Report

The global data center generator market was valued at USD 8.18 Billion in 2025, driven by uninterruptible power supply demand, cloud computing expansion, and AI data center infrastructure investments globally.

The market is projected to reach USD 12.24 Billion by 2034, growing at a CAGR of 4.58% during 2026-2034, driven by AI hyperscale build-outs, edge computing proliferation, and regulatory compliance mandates.

Diesel generators lead with a 72.6% share in 2025, driven by rapid 10-second load pick-up, 72+ hour fuel autonomy, and Uptime Institute Tier III and Tier IV compliance requirements for mission-critical data center applications.

Natural gas generators are the fastest-growing product segment at approximately 5.8% CAGR through 2034, fuelled by corporate ESG commitments, lower emissions versus diesel, and cost advantages in regions with pipeline infrastructure.

The Less than 1MW segment leads at 56.5% in 2025, driven by the large installed base of enterprise data centers, co-location facilities, and edge computing nodes requiring compact and cost-effective generator solutions.

North America leads with a 37.5% share in 2025, anchored by US hyperscale data center density, NFPA 110 compliance mandates, and AI infrastructure investments.

Key drivers include a rise in cloud spending, AI training workload proliferation, IoT connected devices, and increasing cyber-threat resilience requirements.

Leading companies include Caterpillar, Cummins, Generac, Kohler, Rolls-Royce (MTU), Himoinsa (Yanmar), Mitsubishi Heavy Industries, and Wärtsilä.

Key trends include AI-driven hyperscale power surges, natural gas and hybrid generator adoption, modular containerized deployments for edge computing, and IoT-connected predictive maintenance platforms reducing downtime by up to 35%.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)