Data Center Server Market Size, Share, Trends and Forecast by Product, Application, and Region 2026-2034

Global Data Center Server Market Size, Share, Trends & Forecast (2026-2034)

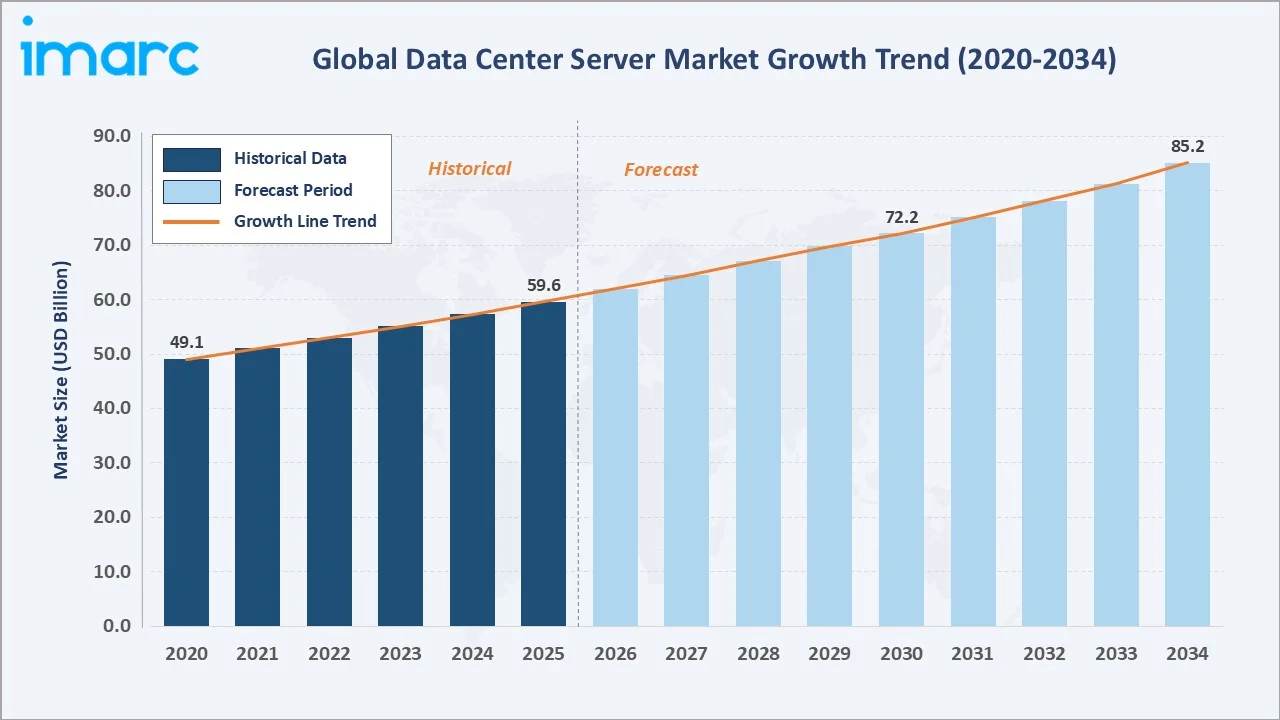

The global data center server market size reached USD 59.6 Billion in 2025 and is projected to reach USD 85.2 Billion by 2034, exhibiting a CAGR of 3.94% during 2026-2034. Accelerating AI and machine learning workload deployments by hyperscalers and enterprises, rapid cloud-native application proliferation, and escalating global digital transformation programs are the primary forces driving data center server market growth.

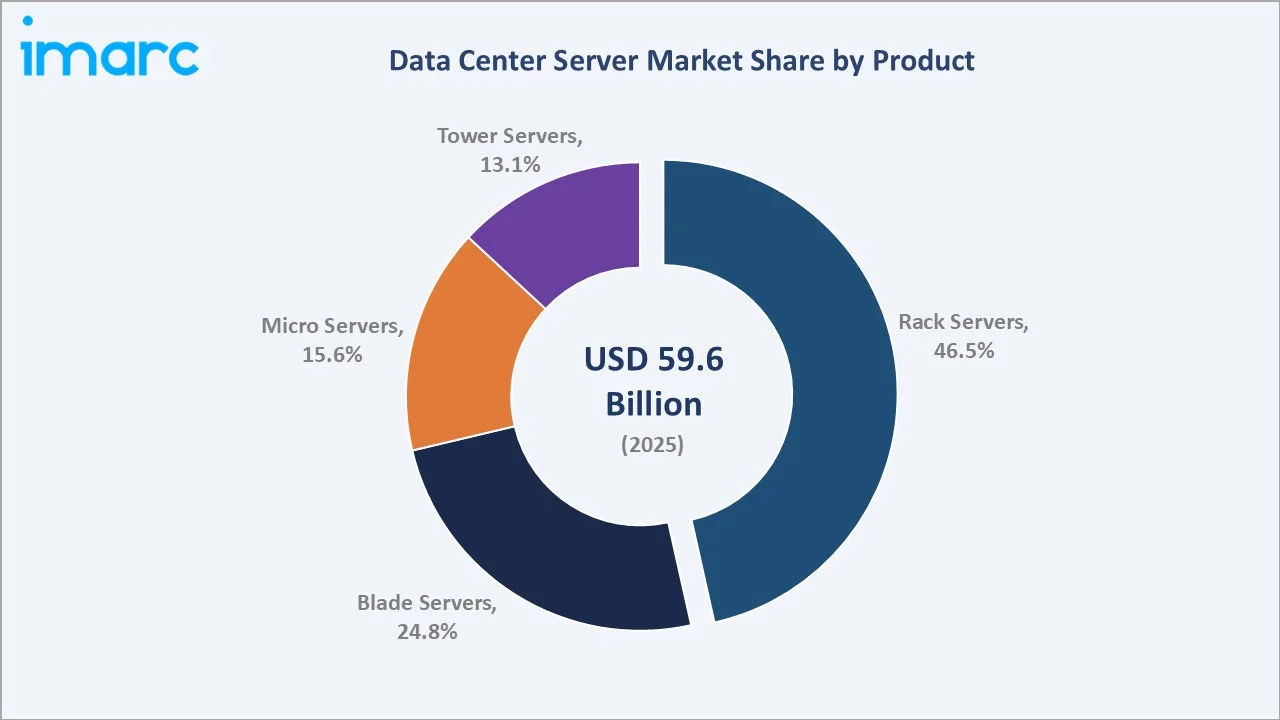

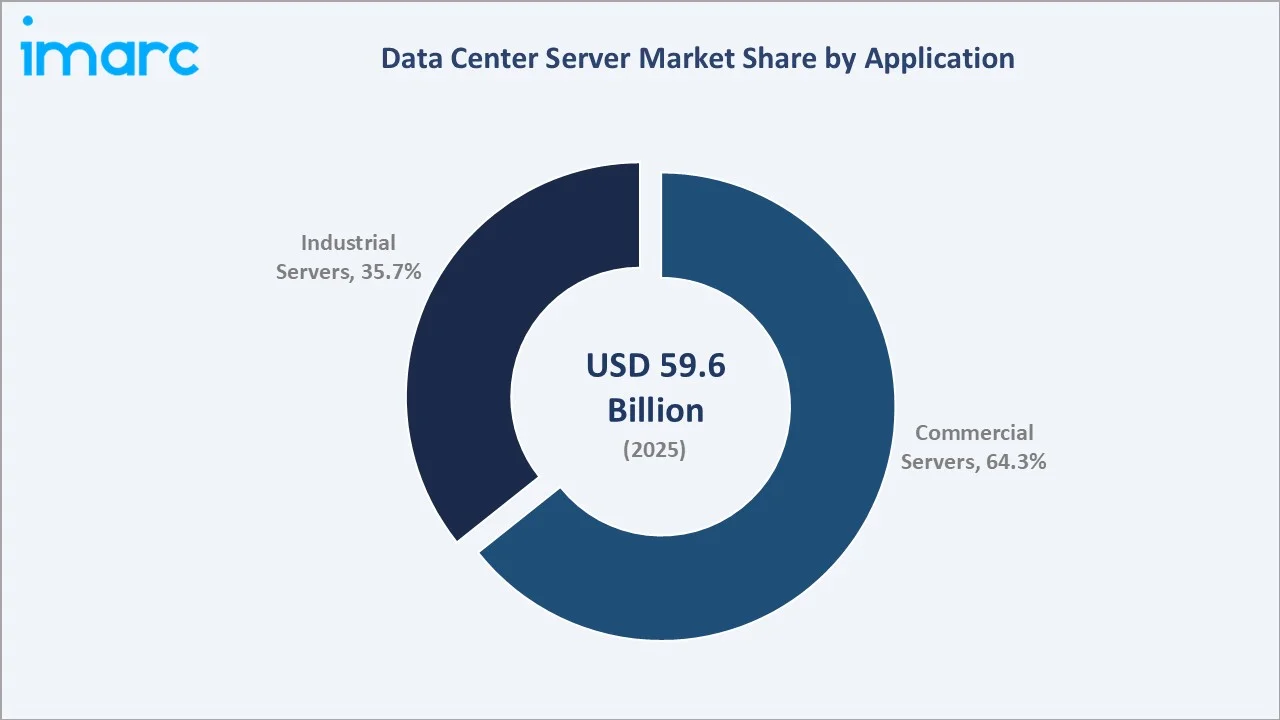

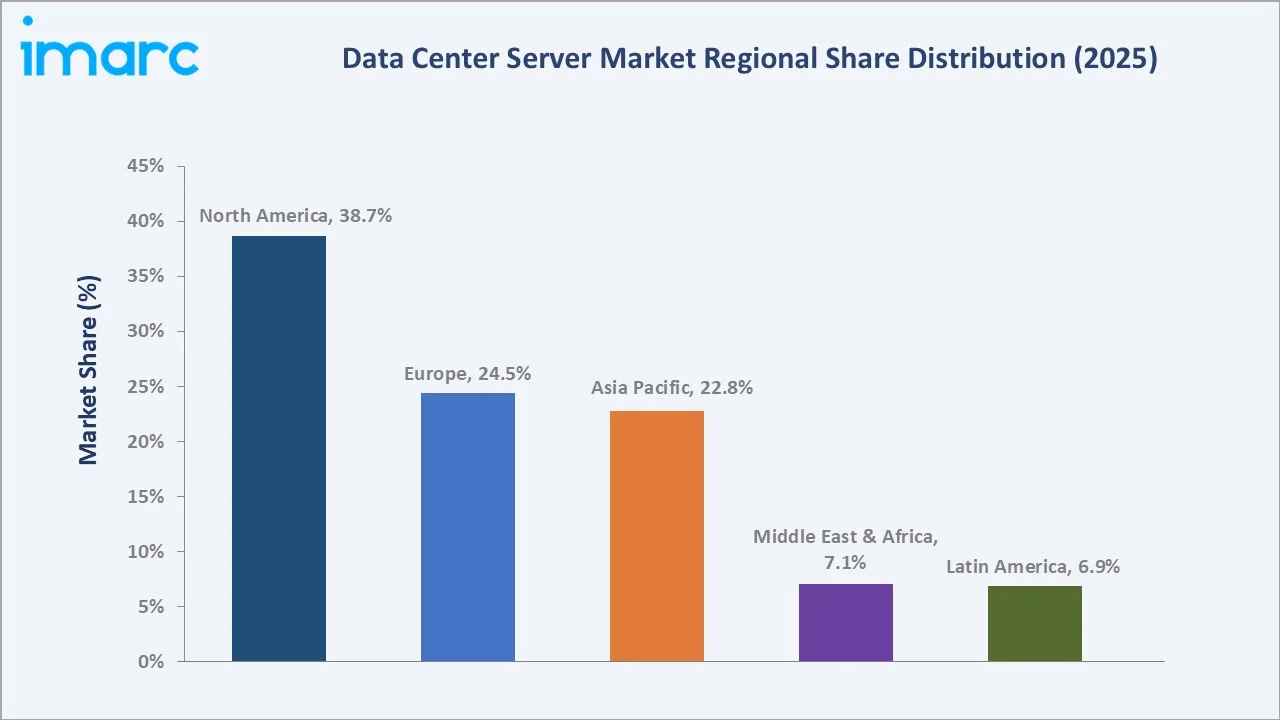

Rack servers dominate the product mix at 46.5% in 2025, while commercial servers lead the application segment at 64.3%. North America commands a dominant 38.7% regional share in 2025, reflecting unparalleled hyperscaler concentration and sustained enterprise IT investment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 59.6 Billion |

|

Forecast Market Size (2034) |

USD 85.2 Billion |

|

CAGR (2026-2034) |

3.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.7% share, 2025) |

|

Leading Product |

Rack Servers (46.5%, 2025) |

|

Leading Application |

Commercial Servers (64.3%, 2025) |

The global data center server market growth trajectory from 2020 through 2034, with the historical expansion to USD 59.6 Billion in 2025, reflects consistent infrastructure-driven demand, while the forecast to USD 85.2 Billion captures accelerating AI investment, hyperscale cloud expansion, and Asia-Pacific digitalization-led demand through 2034.

To get more information on this market, Request Sample

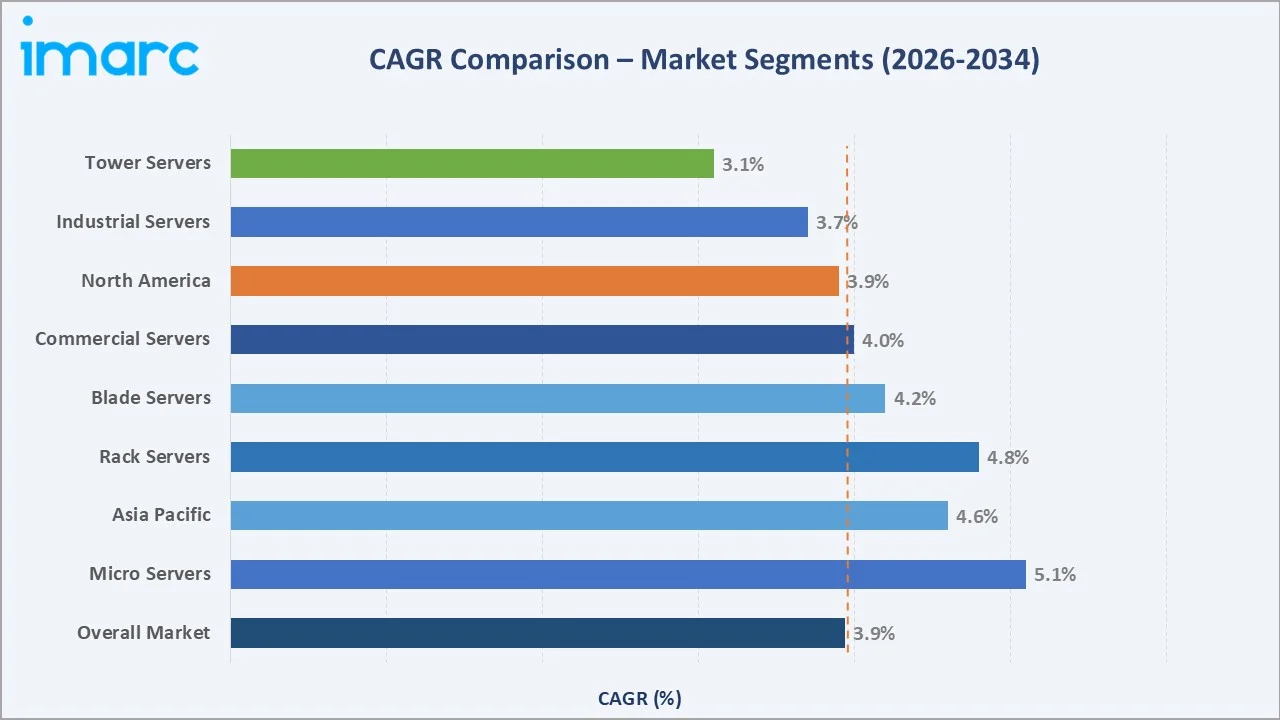

The CAGR trajectories across key product and application sub-segments, with micro servers at ~5.1% CAGR and commercial servers at ~4.0% CAGR, are the fastest-growing categories within the global data center server industry through 2034.

Executive Summary

The global data center server market is on a sustained growth trajectory from USD 59.6 Billion in 2025 to USD 85.2 Billion by 2034. Data center servers, the critical compute infrastructure underpinning cloud services, AI model training, enterprise applications, and digital content delivery, benefit from the non-discretionary nature of digital infrastructure investment globally.

Rack servers dominate product at 46.5% in 2025, owing to their unmatched density and versatility across hyperscale and enterprise deployments. Blade servers at 24.8% offer superior resource consolidation for virtualized enterprise environments. Micro servers at 15.6% are the fastest-growing segment driven by edge computing and distributed AI inference adoption.

North America dominates at 38.7% in 2025, reflecting the US concentration of hyperscale cloud operators and sustained enterprise IT modernization. Europe at 24.5% and Asia Pacific at 22.8% follow, driven by sovereign cloud mandates, AI infrastructure investment supercycles, and rapid cloud adoption across emerging economies.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Rack Servers – 46.5% share (2025) |

|

Fastest-Growing Product |

Micro Servers – ~5.1% CAGR (2026-2034) |

|

Leading Application |

Commercial Servers – 64.3% share (2025) |

|

Leading Region |

North America – 38.7% revenue share (2025) |

|

Second Region |

Europe – 24.5% revenue share (2025) |

|

Top Companies |

Hewlett Packard Enterprise, Dell Inc., Cisco Systems Inc., Lenovo Group Ltd. |

Key Analytical Observations expanding On The Above Data:

- Rack servers, with 46.5% in 2025, dominate because of their unmatched compute density and universal compatibility with GPU accelerators. For hyperscalers executing AI infrastructure buildouts, rack servers deliver the highest workload density per square foot of data center floor space, making them the default specification across cloud and AI factory deployments.

- Commercial servers, with 64.3% in 2025, lead application share because the explosive growth of cloud-native SaaS, AI-as-a-Service, and digital media streaming platforms creates continuous server procurement from hyperscale operators including AWS, Microsoft Azure, Google Cloud, and Others, each committing record capital expenditures in 2025 and 2026.

- North America's 38.7% dominance in 2025 reflects multiple structural forces including the headquarters concentration of the world's five largest hyperscalers, the highest enterprise IT modernization investment globally, and the US government's CHIPS and Science Act driving semiconductor fab construction that requires dense server deployments.

- Asia Pacific, with 22.8% in 2025, is the fastest-growing region driven by China's hyperscale buildout, India's USD 15 billion digital infrastructure investment program for 2026-2030, and ASEAN cloud adoption acceleration that is creating new demand centers beyond established North American and European hyperscale campuses.

Global Data Center Server Market Overview

A data center server is a high-performance computing system designed and optimized for continuous operation within controlled data center environments, providing compute, storage, and network processing capabilities for enterprise applications, cloud services, AI workloads, and digital infrastructure. Server configurations are defined by form factor, processor architecture, memory capacity, storage density, GPU acceleration capability, and thermal management approach.

The global ecosystem integrates semiconductor manufacturers producing CPUs, GPUs, and custom ASICs; server OEMs and ODMs designing and assembling complete systems; hyperscale cloud operators and co-location providers deploying infrastructure at scale; enterprise IT departments procuring for on-premises workloads; and a broad ecosystem of software, networking, and storage vendors that define server platform requirements.

Market Dynamics

To evaluate market opportunities, Request Sample

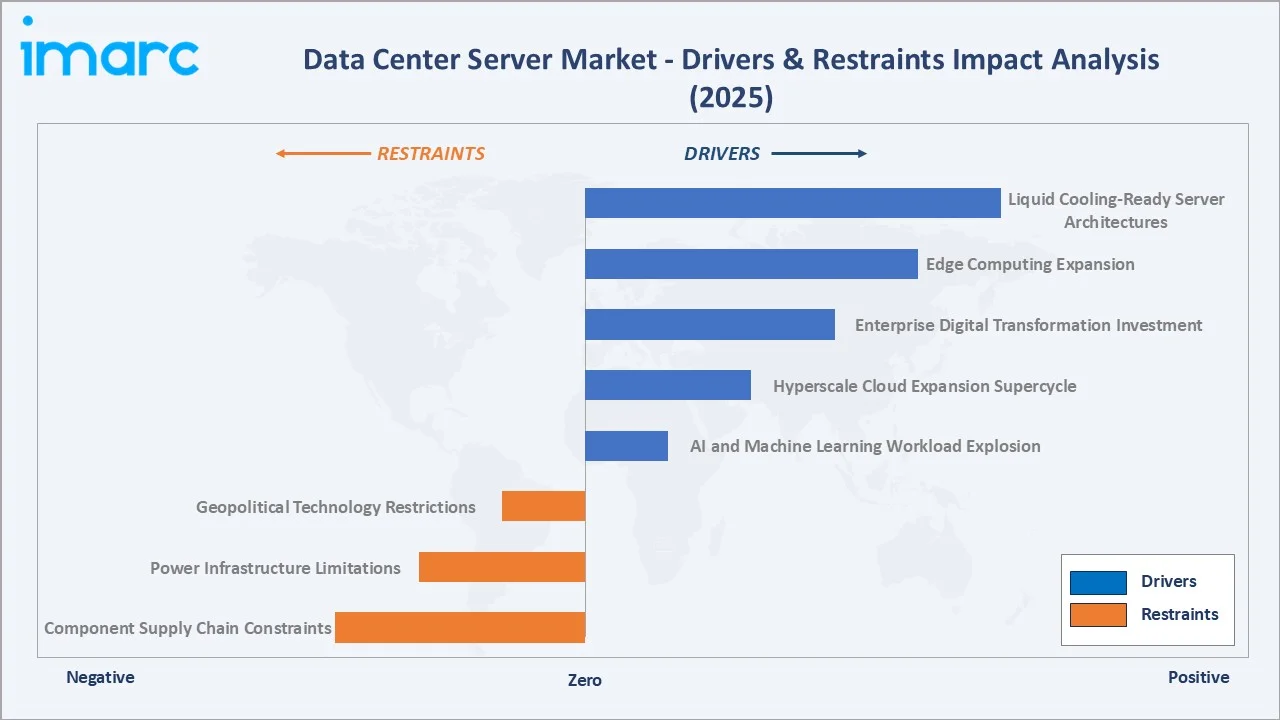

Market Drivers

- AI and Machine Learning Workload Explosion: According to Dell's Oro Group, worldwide data center capital expenditures increased 57% in 2025, with the top four US cloud service providers expanding capex by 76%, driven almost entirely by AI infrastructure investment that requires GPU-dense rack and blade server deployments at unprecedented scale.

- Hyperscale Cloud Expansion Supercycle: JLL's 2026 Global Data Center Outlook projects nearly 100 GW of new data center capacity to be added globally between 2026 and 2030, effectively doubling total capacity, with each gigawatt of new capacity requiring thousands of server units across all product categories.

- Enterprise Digital Transformation Investment: Gartner estimates worldwide datacenter systems spending rose 46.8% to USD 489.5 Billion in 2025, reflecting broad enterprise adoption of hybrid cloud, real-time analytics, and AI-powered automation that requires sustained server refresh cycles across financial services, healthcare, manufacturing, and public sector verticals.

Market Restraints

- Component Supply Chain Constraints: The AI boom has created unprecedented DRAM and high-bandwidth memory shortages, with Dell, Lenovo, HPE, and other OEMs announcing server price increases of 10-20% in late 2025 and early 2026 driven by memory cost escalation, constraining procurement budgets for price-sensitive enterprise customers.

- Power Infrastructure Limitations: JLL's 2026 Global Data Center Outlook identifies grid-connection wait times exceeding four years in primary data center markets, creating bottlenecks that delay new facility commissioning and associated server deployment timelines across North America and Europe.

Market Opportunities

- Edge Computing Expansion: The global active data center IT capacity will grow sixfold from 24 GW in 2025 to 147 GW by 2035, with a growing proportion destined for distributed edge deployments requiring micro and compact server configurations in telecommunications, retail, and industrial environments.

- Liquid Cooling-Ready Server Architectures: Modern AI racks drawing 100 kW or more per rack require direct liquid cooling that is incompatible with legacy air-cooled server designs, creating a large server replacement opportunity as operators upgrade facilities to support next-generation GPU-dense deployments.

Market Challenges

- Geopolitical Technology Restrictions: US export controls on advanced semiconductors are fragmenting the global server supply chain, compelling Chinese hyperscalers to develop domestic server platforms while restricting access to leading-edge GPU architectures, creating divergent product ecosystems that complicate global vendor strategies.

- Cybersecurity and Firmware Integrity: The proliferation of AI-connected server infrastructure increases the attack surface for firmware-level vulnerabilities, requiring OEMs to invest heavily in secure supply chain verification, hardware root-of-trust implementations, and real-time security monitoring integration that adds development cost and complexity.

Emerging Market Trends

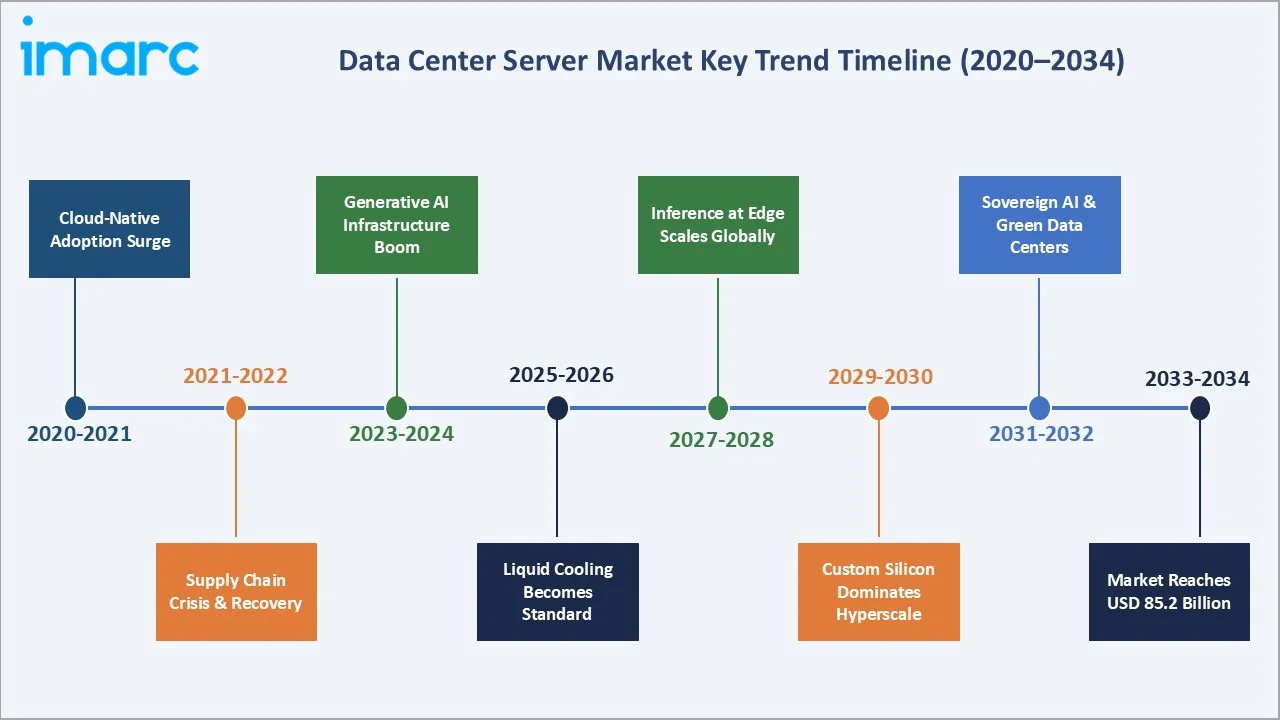

1. AI-Optimized Server Architectures Displacing General-Purpose Compute

The transition from general-purpose CPU-centric server configurations to AI-optimized platforms featuring NVIDIA Blackwell, AMD Instinct MI300X, and Intel Gaudi3 accelerators is reshaping the entire server OEM competitive landscape. According to IDC, revenue from servers with embedded GPUs grew 49.4% year-over-year in Q3 2025 and accounted for over half of total server market revenue, demonstrating that AI-driven demand has become the primary growth engine within the global data center server market.

2. Hyperscale Investment Supercycle Creating Sustained Server Demand

The capital expenditure commitments of leading hyperscale operators have reached levels that create durable, multi-year server procurement visibility. Each gigawatt of new capacity requires thousands of rack, blade, and micro-server units, creating a direct demand multiplier that underpins data center server market forecast momentum through 2034.

3. Edge Computing Proliferation Diversifying Server Deployment Geography

The latency requirements of real-time AI inference, autonomous vehicles, smart manufacturing, and 5G-connected IoT systems are driving server deployment beyond centralized hyperscale campuses to distributed edge locations including telecommunications facilities, factory floors, and retail environments. Micro servers and compact rack configurations optimized for power-constrained and space-limited edge deployments are gaining specification preference.

4. Liquid Cooling Integration Driving Next-Generation Server Design

Rising compute densities driven by AI GPU clusters, with modern AI racks drawing 100 kW or more per rack versus 5-15 kW for general-purpose CPU racks, are making direct liquid cooling architectures a standard design requirement rather than a premium option.

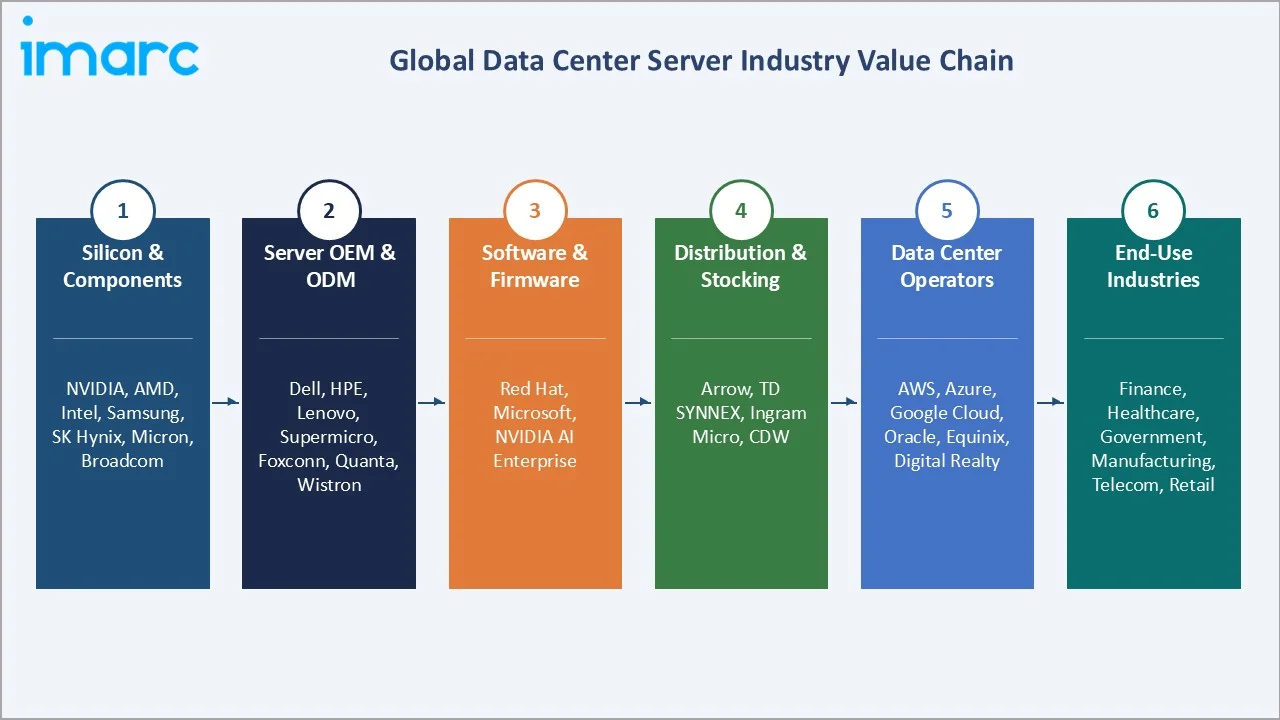

Industry Value Chain Analysis

The data center server value chain spans six stages from silicon production through end-use deployment and lifecycle management. Server OEM assembly and system integration capture the highest value-add margins, while hyperscale direct procurement and ODM white-box sourcing increasingly compress margins for traditional branded OEMs in commodity compute segments.

|

Stage |

Key Players / Examples |

|

Silicon & Components |

NVIDIA, AMD, Intel, Samsung Electronics Co., Ltd., SK Hynix Inc., Micron, Broadcom |

|

Server OEM / ODM Assembly |

Dell Inc., HPE, Lenovo, Supermicro, Hon Hai Precision Industry Co., Ltd., Quanta Computer Inc., Wistron |

|

Software & Firmware |

Microsoft, Red Hat, NVIDIA AI Enterprise |

|

Logistics & Distribution |

Arrow Electronics, Ingram Micro, CDW |

|

Data Center Operators |

AWS, Microsoft Azure, Google Cloud, Equinix, Digital Realty |

|

End Users / Enterprises |

Financial services, healthcare, government, manufacturing, telecom |

Vertically integrated hyperscalers such as Amazon, Google, and Microsoft increasingly design proprietary server architectures and source directly from ODMs, bypassing traditional OEM channels in commodity compute segments. This vertical integration creates a meaningful competitive advantage in total cost of ownership for hyperscale AI and cloud workloads while pressuring traditional OEM market share in the high-volume segment.

Technology Landscape in the Data Center Server Industry

Processor Architecture: CPU, GPU, and Custom Accelerators

The dominant processing paradigm is shifting from CPU-centric architectures to heterogeneous compute platforms combining CPUs for general workloads with GPUs, DPUs, and custom ASICs for AI inference and training. NVIDIA's Blackwell architecture, now shipping across enterprise servers from Dell, HPE, Lenovo, Cisco, and Supermicro, delivers unprecedented inference performance with built-in Confidential Computing.

Memory and Storage: HBM and High-Density NVMe Integration

AI training and inference workloads demand High-Bandwidth Memory (HBM3/HBM3E) integrated with GPU accelerators to minimize data transfer latency, creating a structural shortage of HBM capacity that constrains AI server production.

Networking: High-Speed Interconnects and SmartNIC Integration

High-performance data center networking is transitioning from 100G to 400G and 800G Ethernet and InfiniBand interconnects to support the data-intensive requirements of distributed AI training across GPU clusters.

Cooling Technology: Direct Liquid and Immersion Cooling Adoption

Modern AI racks drawing 100 kW or more per rack are incompatible with traditional air-cooling architectures, driving adoption of direct liquid cooling (DLC), rear-door heat exchangers, and full immersion cooling systems. HPE's ProLiant Compute XD685, introduced in December 2025, features direct-liquid cooling for Blackwell Ultra GPU configurations. ABB and NVIDIA announced collaboration in October 2025 to develop gigawatt-scale AI data centers with advanced 800 VDC power architectures and high-efficiency power distribution systems optimized for high-density liquid-cooled server deployments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Rack Servers |

46.5% |

2025 |

|

Application |

Commercial Servers |

64.3% |

2025 |

|

Region |

North America |

38.7% |

2025 |

By Product

To access detailed market analysis, Request Sample

Rack servers command a dominant 46.5% share of the data center server market in 2025, reflecting their unmatched compute density, GPU compatibility, and universal applicability across hyperscale cloud and enterprise data center architectures. Their standardized 1U-4U form factors maximize space utilization in high-density deployments, making them the preferred platform for AI training and inference workloads where GPU accelerator density per rack unit is the primary optimization metric.

Blade servers at 24.8% offer superior resource sharing through centralized chassis-level power and cooling, preferred in enterprise environments consolidating virtualization workloads.

By Application

Commercial servers account for 64.3% of the data center server market in 2025, underscoring the dominant role of hyperscale cloud operators, financial services, e-commerce platforms, and SaaS providers in driving global server procurement.

The explosive growth of AI-as-a-Service, generative AI platforms, and cloud-native applications creates continuous server deployment demand.

Industrial servers at 35.7% serve manufacturing automation systems, process control infrastructure, energy grid management, transportation networks, and smart city applications.

These deployments specify rugged, temperature-tolerant, vibration-resistant, and extended-lifecycle server platforms that differ significantly from hyperscale commodity designs. Industrial server procurement is driven by Industry 4.0 adoption, predictive maintenance AI deployment, and the digitalization of operational technology environments across automotive, energy, and utilities sectors globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.7% |

Hyperscaler capex supercycle; AI infrastructure build-out; CHIPS Act fab investment; enterprise IT modernization |

|

Europe |

24.5% |

Sovereign cloud mandates; EU AI Act compliance infrastructure; Industry 4.0 digitalization; green data center investment |

|

Asia Pacific |

22.8% |

China hyperscale buildout; India digital infrastructure program; Japan semiconductor reinvestment; ASEAN cloud adoption |

|

Middle East & Africa |

7.1% |

GCC Vision 2030 smart infrastructure; NEOM digital platform; sovereign AI cloud strategies; African digital economy |

|

Latin America |

6.9% |

Brazil AI data center platform; Mexico nearshoring enterprise IT; Chile colocation hub development; regional cloud growth |

North America's 38.7% market dominance in 2025 is driven by the most structurally exceptional combination of hyperscale infrastructure concentration, enterprise IT investment, and AI-driven server procurement in any global market.

Europe, with 24.5% in 2025, is experiencing pronounced growth driven by EU digital sovereignty regulations, the EU AI Act compliance requirements creating demand for locally hosted AI-ready server infrastructure, and Germany's automotive and manufacturing sectors investing heavily in edge computing deployments for Industry 4.0 applications.

Competitive Landscape

The global data center server market is moderately concentrated, with established technology OEMs competing aggressively across rack, blade, micro, and tower server segments. Dell Technologies leads all OEMs in AI-optimized server revenue in 2025 with 8.3% revenue share in Q3 2025 per IDC, benefiting from strong NVIDIA Blackwell shipments.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Hewlett Packard Enterprise Development LP |

ProLiant Gen11, ProLiant Gen12, ProLiant XD685 |

Leader |

AI Factory strategy; GreenLake hybrid cloud; liquid-cooled Blackwell platforms |

|

Dell, Inc. |

PowerEdge Servers |

Leader |

AI-optimized server leader; NVIDIA Blackwell; PowerStore integration |

|

Cisco Systems, Inc. |

UCS C-Series, X-Series |

Challenger |

Converged server-network platform; secure AI factory architecture |

|

Lenovo |

ThinkSystem SR, ThinkAgile HX, Neptune liquid-cooled |

Leader |

Fastest-growing top-5 vendor; Asia-Pacific strength; Neptune DLC |

|

Super Micro Computer, Inc. |

X14 Series, X13 Series, Data Center Building Block Solutions (DCBBS) |

Challenger |

GPU server specialist; hyperscale direct; Blackwell Ultra deployments |

|

Huawei Technologies Co., Ltd. |

FusionServer Pro, TaiShan 200 series |

Leader (China) |

China domestic leader; ARM-based ecosystem; domestic GPU alternatives |

|

Fujitsu Ltd. |

PRIMERGY M7, PRIMEQUEST, PRIMEHPC FX |

Challenger |

Japan and EU markets; HPC strength; Fugaku successor platforms |

Key players include Hewlett Packard Enterprise Development LP, Dell, Inc., Cisco Systems, Inc., Lenovo, Super Micro Computer, Inc., Huawei Technologies Co., Ltd., Fujitsu Ltd., and others.

Key Company Profiles

Hewlett Packard Enterprise Development LP

Hewlett Packard Enterprise Development LP is a global technology company headquartered in Houston, Texas, providing server, storage, networking, and hybrid cloud infrastructure. HPE's flagship AI platform co-developed with NVIDIA bundles ProLiant servers, high-speed Ethernet, GreenLake storage, and NVIDIA AI Enterprise software under the HPE GreenLake cloud-managed platform.

- Product Portfolio: ProLiant Gen11, ProLiant Gen12, ProLiant XD685.

- Recent Developments: In December 2025, Hewlett Packard Enterprise (HPE) expanded its collaboration with NVIDIA to accelerate AI adoption across government and enterprise sectors by introducing secure AI factory solutions. These innovations provide integrated, scalable infrastructure that simplifies the deployment of AI while ensuring strong data security, compliance, and operational control, enabling organizations to develop and run AI workloads more efficiently in regulated and data-sensitive environments.

- Strategic Focus: HPE's strategy centers on the AI Factory platform concept, integrating compute, networking, and storage under GreenLake cloud management, targeting enterprises transitioning from on-premises to hybrid cloud AI deployments where integrated stack management and software-defined infrastructure reduce operational complexity.

Dell, Inc.

Dell Technologies is the global leader in AI-optimized server revenue in 2025, headquartered in Round Rock, Texas. Dell's PowerEdge AI server line and XE series GPU servers lead the market in NVIDIA Blackwell shipment volumes, supported by a comprehensive enterprise services and support ecosystem spanning 180 countries.

- Product Portfolio: PowerEdge Servers.

- Recent Developments: In late 2025, Dell announced server price increases of 10-20% driven by DRAM and HBM cost escalation while simultaneously expanding its AI Factory with NVIDIA as a complete enterprise AI platform integrating compute, networking, and storage.

- Strategic Focus: Dell's strategy leverages its vertically integrated supply chain and enterprise sales relationships to compete on AI server total delivered cost, while expanding toward higher-value AI platform solutions where integration expertise and rapid deployment capabilities command premium positioning over commodity ODM alternatives.

Lenovo

Lenovo's Data Center Group (DCG) is rapidly rising in global server market share, with revenue growth of 70% year-over-year in Q4 2024 per IDC. Headquartered in Hong Kong with manufacturing across Asia, Lenovo's Neptune direct water-cooling technology is a key competitive differentiator for high-density AI server deployments.

- Product Portfolio: ThinkSystem SR, ThinkAgile HX, Neptune liquid cooled.

- Recent Developments: In February 2026, Lenovo has reorganized its data center (Infrastructure Solutions Group) business to improve profitability as strong demand for AI products drives rapid growth. The company reported record quarterly revenue, with all major divisions achieving double-digit gains, largely fueled by AI across devices, infrastructure, and services.

- Strategic Focus: Lenovo's DCG strategy focuses on Neptune liquid cooling leadership for AI-dense deployments, aggressive expansion in Asia-Pacific cloud markets where it holds strong relationships, and Nutanix hybrid cloud partnership to penetrate enterprise accounts transitioning from legacy on-premises to hybrid AI infrastructure.

Super Micro Computer, Inc.

Super Micro Computer, headquartered in San Jose, California, is a GPU server specialist with deep hyperscale direct relationships and the fastest product development cycles among major OEMs. Supermicro's modular architecture enables rapid integration of new GPU platforms, allowing it to ship NVIDIA Blackwell systems ahead of most competitors.

- Product Portfolio: X14 Series, X13 Series, Data Center Building Block Solutions (DCBBS)

- Recent Developments: In March 2026, Supermicro launched seven AI data platform solutions in partnership with NVIDIA and ecosystem partners, reinforcing its GPU-dense rack server positioning for hyperscale AI training and expanding its product range for inference at the edge.

- Strategic Focus: Supermicro's strategy differentiates on time-to-market for new GPU architectures, total cost of ownership through modular component reuse across server generations, and direct hyperscaler relationships that provide early access to next-generation AI workload requirements informing platform design decisions.

Market Concentration Analysis

The global data center server market is moderately concentrated at the global level, with Dell Technologies leading at 8.3% revenue share in Q3 2025 and no single company holding more than 10% of total annual market revenue. The competitive structure differs significantly across customer segments: hyperscale cloud operators increasingly source from ODM white-box vendors and proprietary designs, while enterprise and co-location markets are primarily served by branded OEMs including HPE, Dell, Lenovo, and Cisco.

Consolidation at the segment level is advancing through AI platform partnerships. Dell's AI Factory with NVIDIA, HPE's Private Cloud AI, Cisco's Nexus HyperFabric, and Lenovo's Neptune AI infrastructure are creating integrated platform ecosystems that bundle server hardware with software management and AI acceleration libraries, raising switching costs and differentiating from commodity ODM alternatives in enterprise procurement decisions.

Investment & Growth Opportunities

Fastest-Growing Segments

Micro servers are the fastest-growing product segment at ~5.1% CAGR through 2034, driven by edge computing proliferation, distributed AI inference requirements, and 5G-connected IoT infrastructure deployments that require dense, low-power compute at locations outside traditional data center environments. The Middle East and Africa at ~4.5% CAGR is the fastest-growing region, driven by GCC Vision 2030 smart infrastructure investment and sovereign AI cloud development.

Emerging Markets

India represents the most significant emerging server market through 2034, supported by a USD 15 billion digital infrastructure investment program for 2026-2030 that is expected to drive significant growth in AI data center infrastructure. In January 2026, RT-One and Hitachi Energy signed an agreement to develop electrification infrastructure for Latin America's largest AI data center platform in Brazil, signaling that the region is entering a high-growth infrastructure build phase that will require substantial server procurement.

Venture & Investment Trends

Private equity and institutional investor appetite for data center infrastructure continues to intensify, with the landmark USD 30 billion joint venture between Blue Owl and Meta in 2025 highlighting both the scale and sophistication of hyperscale financing. Data centers have evolved into a mature, highly institutionalized asset class with record-low vacancy rates and strong rent growth. Investors are deploying complex capital structures including forward sales, joint ventures, and preferred equity, all of which underpin sustained server procurement pipelines that benefit OEMs with hyperscaler supply relationships through 2034.

Future Market Outlook (2026-2034)

The global data center server market is forecast to expand from USD 59.6 Billion in 2025 to USD 85.2 Billion by 2034 at a CAGR of 3.94%, adding USD 25.6 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's AI-infrastructure-linked, non-discretionary demand characteristics across hyperscale, enterprise, and industrial customer segments globally.

Three technological forces will most significantly shape the data center server industry landscape through 2034. AI inference at scale will transition from centralized hyperscale clusters to distributed inference networks requiring micro and edge server deployments. Liquid cooling will become standard across all rack server product categories as GPU densities exceed 100 kW per rack. Custom silicon from hyperscalers including AWS Graviton, Google Axion, and Microsoft Maia will capture an increasing share of hyperscale compute, pressuring traditional CPU-based OEM server revenue while creating opportunities for ODM-style custom platform assembly.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews in 2025-2026 with data center server industry stakeholders, including senior commercial managers at OEMs, hyperscale infrastructure procurement specialists, enterprise IT directors, semiconductor technology executives, and data center construction project managers. Primary data validated market sizing, product segment shares, regional demand estimates, and technology adoption timelines across all major geographies.

Secondary Research

Key secondary sources include IDC Worldwide Quarterly Server Tracker (2020-2025), Dell's Oro Group Data Center IT Capex Reports, JLL Global Data Center Outlook 2026, BloombergNEF AI Data Center Build reports, ABI Research Data Center Capacity forecasts, Gartner IT spending surveys, IEEE publications on server architecture standards, and trade publications including Data Center Dynamics, DCD, and SDxCentral.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating AI workload growth rates, hyperscaler capex trajectories, enterprise IT refresh cycle data, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for geopolitical, supply chain, and macroeconomic uncertainty factors.

Data Center Server Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Rack Servers, Blade Servers, Micro servers, Tower Servers |

| Applications Covered | Industrial Servers, Commercial Servers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Hewlett Packard Enterprise Development LP, Dell, Inc., Cisco Systems, Inc., Lenovo, Super Micro Computer, Inc., Huawei Technologies Co., Ltd., Fujitsu Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the data center server market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global data center server market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the data center server industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Data Center Server Market Report

The global data center server market reached USD 59.6 Billion in 2025, reflecting consistent demand from AI infrastructure investment, hyperscale cloud expansion, and broad enterprise digital transformation programs across all major global regions.

The market is projected to reach USD 85.2 Billion by 2034, growing at a CAGR of 3.94% during 2026-2034, driven by sustained AI workload proliferation, hyperscale cloud capex supercycle, edge computing expansion, and enterprise IT modernization across financial services, healthcare, and manufacturing sectors.

Rack servers lead with a 46.5% product share in 2025, valued for their superior compute density, GPU accelerator compatibility, and universal applicability across hyperscale and enterprise data center deployments globally, making them the default specification for AI training and cloud infrastructure.

Commercial servers lead at 64.3% in 2025, driven by the explosive growth of cloud-native SaaS platforms, generative AI services, digital media streaming, and financial services applications that require continuous high-performance server procurement from hyperscale operators and enterprise IT organizations.

North America commands a dominant 38.7% market share in 2025, driven by the unparalleled concentration of hyperscale cloud operators including AWS, Microsoft, Google, Meta, and others, combined with the highest enterprise IT modernization investment and sustained AI infrastructure build-out in any global region.

Micro servers are the fastest-growing product segment at ~5.1% CAGR through 2034, driven by the proliferation of edge computing architectures, distributed AI inference requirements, and 5G-connected IoT deployments that require compact, power-efficient compute at locations outside traditional centralized data centers.

Leading companies include Hewlett Packard Enterprise Development LP, Dell, Inc., Cisco Systems, Inc., Lenovo, Super Micro Computer, Inc., Huawei Technologies Co., Ltd., Fujitsu Ltd., and others.

AI server demand is driven by the explosive growth of large language model training, generative AI inference, and real-time AI application deployment by hyperscalers. Dell's Oro Group reports data center capex increased 57% in 2025 with the top four US cloud providers expanding AI-related capex by 76%, requiring GPU-dense rack server deployments at unprecedented scale.

Edge computing is expanding the server deployment geography beyond centralized hyperscale campuses to distributed locations including telecommunications facilities, factory floors, and retail environments.

Modern AI GPU racks drawing 100 kW or more per rack require direct liquid cooling systems incompatible with legacy air-cooled designs. This is driving a mandatory server platform refresh across hyperscale and enterprise operators, with HPE, Dell, Lenovo, and Supermicro all introducing liquid-cooled AI server platforms in 2025-2026 to support NVIDIA Blackwell and future GPU architectures.

North America holds 42% of total global electrical data center capacity as of 2026 per ABI Research, hosting the world's largest hyperscaler infrastructure concentration. Over 35 GW of data center capacity is currently under construction in North America per JLL, 60% of which is fully pre-leased, underpinning durable server procurement demand from hyperscale operators and enterprise co-location tenants through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)