Deep Hole Drilling Machines Market Size, Share, Trends and Forecast by Type, Operation, Business Type, End-user Industry, and Region, 2026-2034

Deep Hole Drilling Machines Market Size, Share, Trends & Forecast (2026-2034)

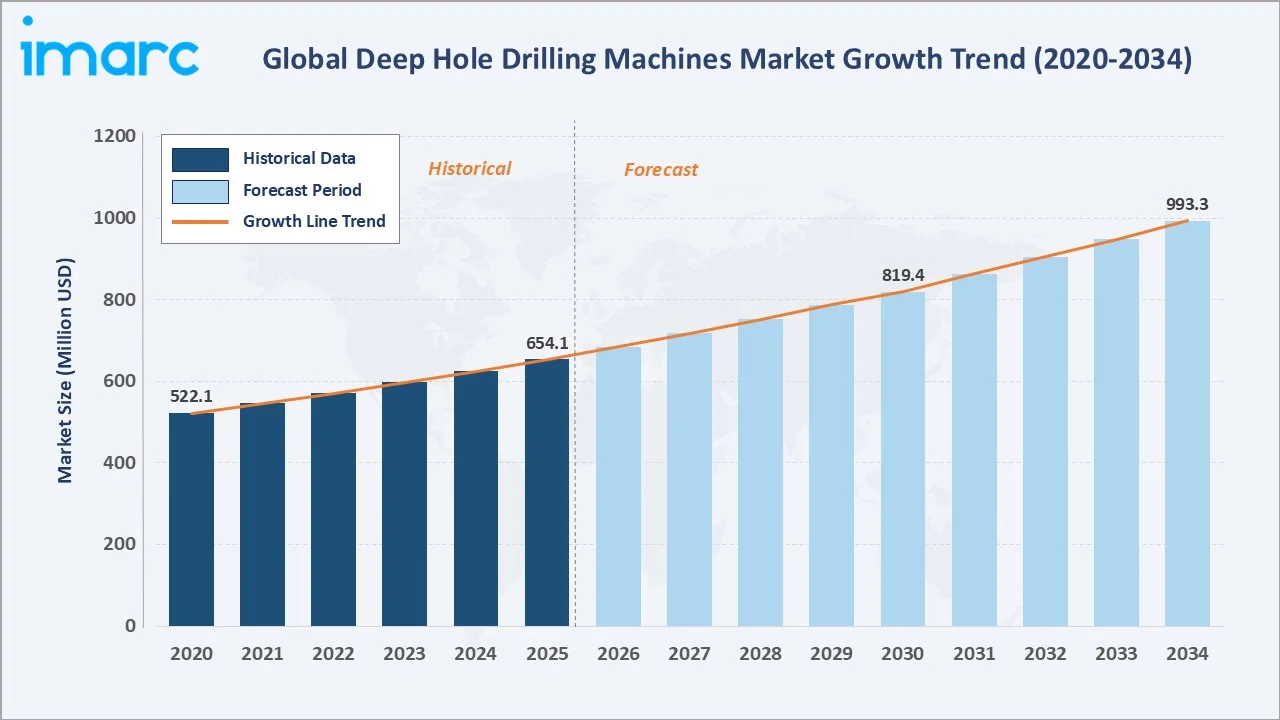

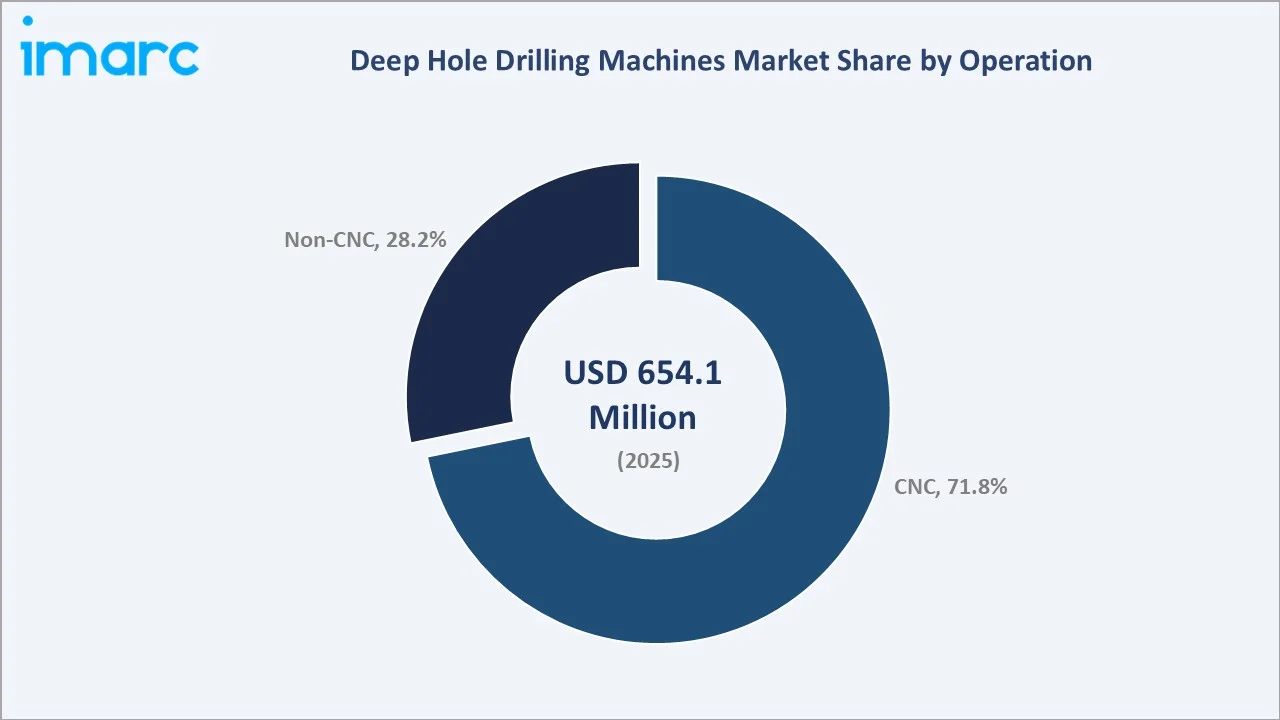

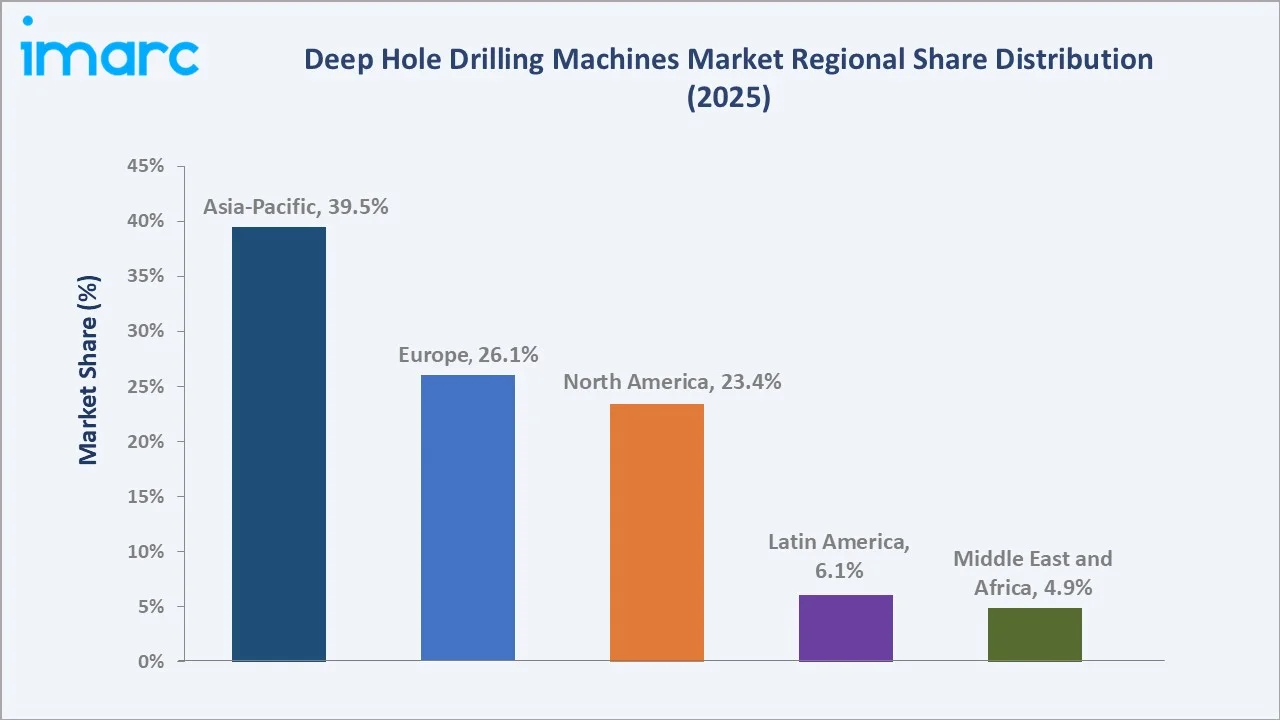

The global deep hole drilling machines market reached USD 654.1 Million in 2025 and is projected to reach USD 993.3 Million by 2034, growing at a CAGR of 4.61% during 2026-2034. Growth is further supported by automation, CNC integration, and the need to machine complex components with tight tolerances and improved productivity. AI is projected to raise productivity by around 40% by 2035. By integrating AI into CNC systems, machines can continuously analyze production data, identify process variations, and make real-time adjustments to improve speed, accuracy, and operating efficiency. AI-enabled deep hole drilling machines are especially valuable in aerospace, automotive, defense, and oil & gas applications, where high-precision deep-bore machining is critical. CNC leads the operation at 71.8%. Automotive leads end-user at 24.7%. Asia-Pacific leads regionally at 39.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 654.1 Million |

|

Forecast Market Size (2034) |

USD 993.3 Million |

|

CAGR (2026-2034) |

4.61% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Operation |

CNC (71.8%, 2025) |

|

Dominant End-user Industry |

Automotive (24.7%, 2025) |

|

Leading Region |

Asia-Pacific (39.5%, 2025) |

The global deep hole drilling machines market has shown steady growth, rising from USD 522.1 Million in 2020 to USD 654.1 Million in 2025, supported by demand from automotive, aerospace, defense, oil & gas, and heavy engineering sectors. By 2030, the market is expected to reach USD 819.4 Million, reflecting increasing adoption of CNC-based and automated drilling systems for precision machining. The market is projected to further expand to USD 993.3 Million by 2034, driven by the need for high-accuracy deep-bore drilling, improved productivity, and advanced manufacturing technologies.

To get more information on this market, Request Sample

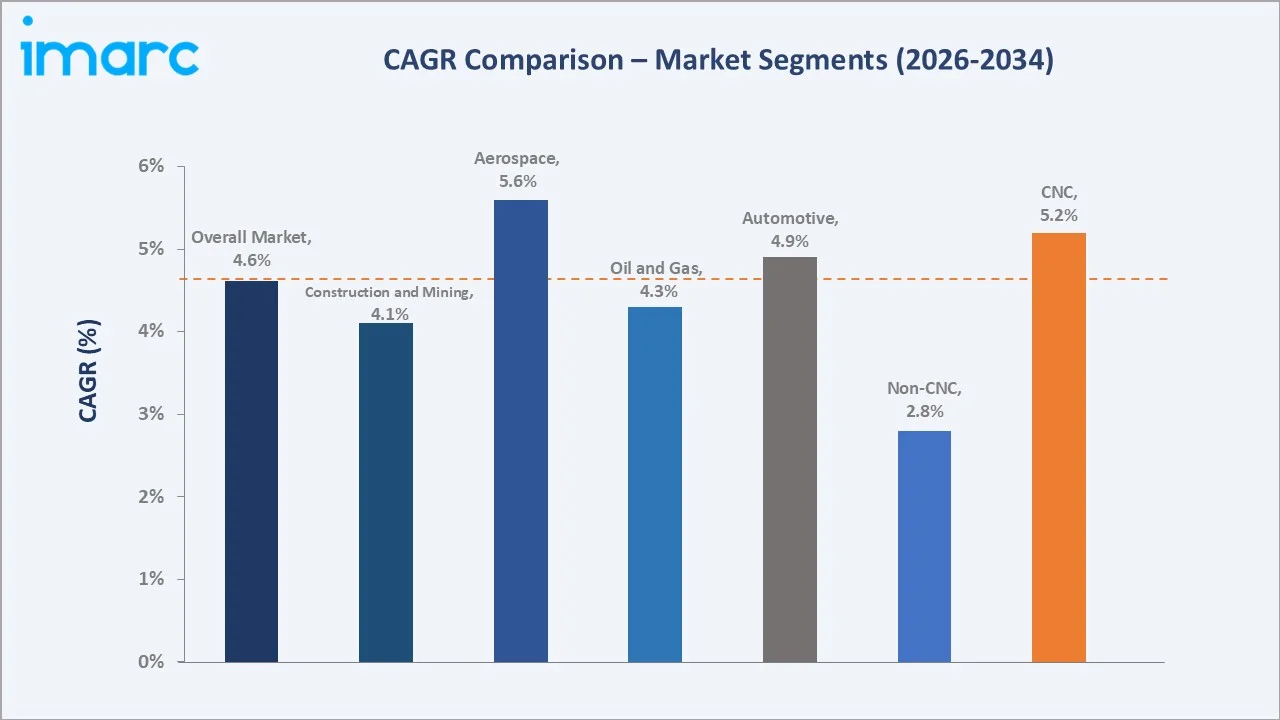

CNC operation grows fastest at ~5.2% CAGR through AI adaptive feed control, IIoT process monitoring, and digital twin simulation. The aerospace segment grows fastest at ~5.6% CAGR.

Executive Summary

The global deep hole drilling machines market reached USD 654.1 Million in 2025, driven by increasing demand for precision machining in aerospace, automotive, defense, energy, and industrial manufacturing applications. The adoption of CNC automation, AI-enabled process optimization, and Industry 4.0 technologies is enhancing drilling accuracy, productivity, and operational efficiency. Rising investments in advanced manufacturing facilities and the production of complex, high-performance components are further supporting market expansion. The market is projected to reach USD 993.3 Million by 2034.

CNC at 71.8% leads through multi-axis precision automation. Automotive at 24.7% leads end-user through engine block and EV motor housing. Asia-Pacific leads at 39.5% through China's automotive and Japan's precision engineering.

Key Market Insights

|

Insight |

Data |

|

Dominant Operation |

CNC - 71.8% share (2025) |

|

Dominant End-user Industry |

Automotive - 24.7% market share (2025) |

|

Leading Region |

Asia-Pacific - 39.5% share (2025) |

|

Market Opportunity |

Aerospace titanium turbine cooling hole BTA drilling; EV motor housing deep hole CNC; medical implant gun drill precision; oil & gas downhole tool drilling; defense gun barrel deep hole boring |

Key Analytical Observations Supporting the Above Data:

- CNC at 71.8%: The CNC segment dominates due to its high precision, repeatability, and ability to handle complex deep-hole drilling operations with minimal manual intervention. Its integration with automation, real-time monitoring, and advanced control systems further improves productivity and machining accuracy.

- Automotive at 24.7%: The automotive segment dominates due to high demand for deep-hole drilling in engine blocks, crankshafts, fuel injection systems, transmission components, and EV battery-related parts. Rising vehicle production and the need for precision-machined components further support its leading share.

- Asia-Pacific at 39.5%: Asia-Pacific dominates regionally due to its strong automotive, aerospace, heavy machinery, and industrial manufacturing base. Rising factory automation, CNC adoption, and large-scale component production further support regional demand for deep hole drilling machines.

Deep Hole Drilling Machines Market Overview

The global deep hole drilling machines market encompasses three primary deep hole drilling technologies: gun drilling, BTA/STS drilling, and ejector drilling. The uniqueness of the market lies in its ability to achieve extremely high depth-to-diameter ratios while maintaining exceptional precision, surface finish, and dimensional accuracy. Unlike conventional drilling equipment, these machines are specifically designed for complex deep-bore applications in critical industries such as aerospace, defense, automotive, and energy. The market is further differentiated by the growing integration of CNC automation, AI-driven process control, and real-time monitoring technologies that enhance productivity and machining reliability.

The deep hole drilling machines ecosystem integrates precision tool and spindle component supply, machine manufacturer and OEM, CNC control and software provider, distributor and system integrator, standards and certification bodies, and automotive, oil and gas, aerospace, and multi-industry end users. Macroeconomic factors include rising industrialization, expansion of automotive and aerospace manufacturing, and increased capital investment in precision engineering.

Market Dynamics

To evaluate market opportunities, Request Sample

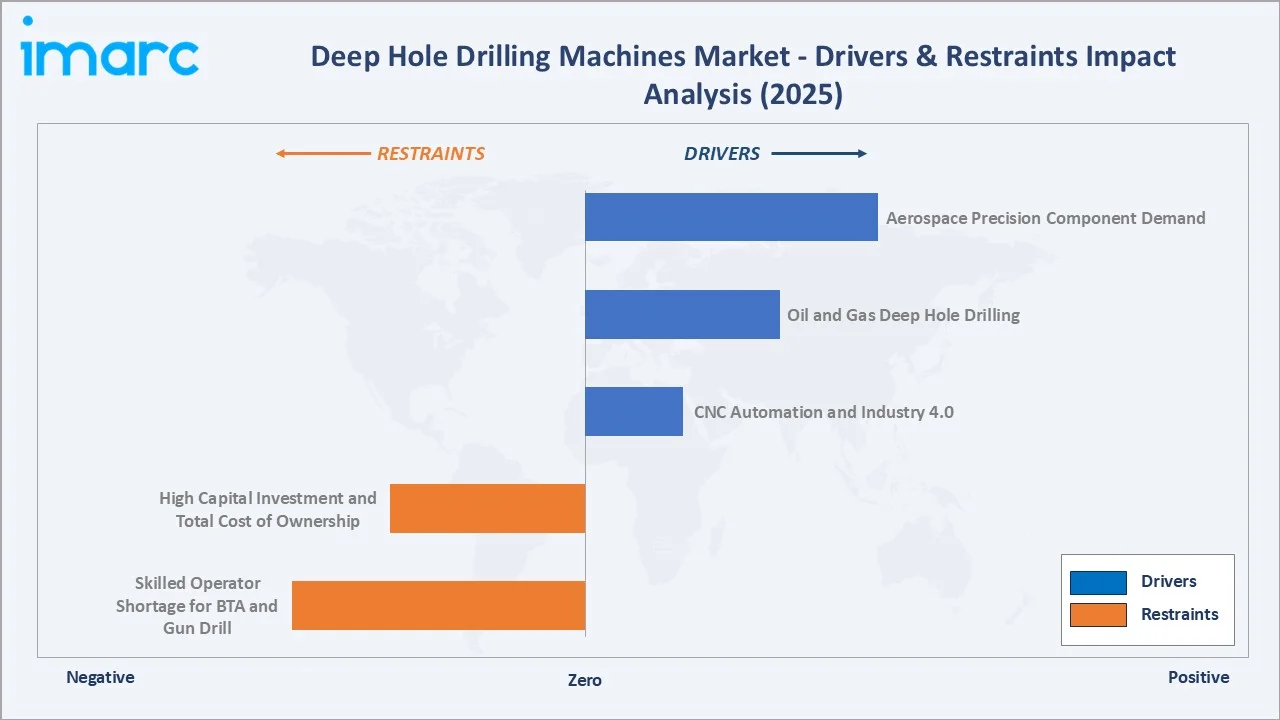

Market Drivers

- Aerospace Precision Component Demand: Aerospace precision component demand is driving the market, as aircraft engines, landing gear systems, hydraulic components, and structural parts require highly accurate deep-hole machining. These components often involve complex geometries and tight tolerances that conventional drilling methods cannot consistently achieve. Growing commercial aircraft production, defense aviation programs, and demand for fuel-efficient aircraft are increasing the need for precision-manufactured aerospace parts. As a result, manufacturers are investing in advanced deep hole drilling machines to ensure superior quality, reliability, and compliance with stringent aerospace standards.

- Oil and Gas Deep Hole Drilling: The oil and gas sector requires precision-machined components such as drill collars, mud motors, valves, pumps, and downhole tools. In June 2026, a large-scale drilling project in Russia aims to test a debated Soviet-era theory that oil can originate deep within the Earth without organic material. Geologists at Saint Petersburg Mining University have started drilling boreholes up to 8 kilometers deep in Russia’s Arctic Komi region. The project will test Russian-made drilling technologies while also searching for evidence that oil deposits can form through purely geological processes, potentially supporting the idea that oil could be a renewable or virtually limitless resource. Such projects stimulate demand for technologically advanced deep hole drilling machines, drilling tools, and related services.

- CNC Automation and Industry 4.0: CNC Automation and Industry 4.0 enabling higher precision, repeatability, and process control in complex drilling operations. Smart CNC systems allow real-time monitoring of tool wear, coolant flow, vibration, and drilling accuracy, reducing defects and machine downtime. Integration with AI, sensors, and data analytics helps manufacturers optimize cycle times, improve productivity, and maintain consistent quality. This is increasing the adoption of advanced deep hole drilling machines across automotive, aerospace, defense, energy, and heavy engineering industries.

Market Restraints

- High Capital Investment and Total Cost of Ownership: High capital investment and total cost of ownership are limiting the market, as advanced CNC, BTA, and gun drilling systems require substantial upfront spending. Beyond machine purchase, users must bear costs for tooling, coolant systems, fixtures, installation, maintenance, software, and skilled labor. These expenses make adoption difficult for small and medium-sized manufacturers. As a result, many companies delay upgrades or continue using conventional drilling methods, slowing market expansion.

- Skilled Operator Shortage for BTA and Gun Drill: The shortage of skilled operators for BTA and gun drilling is hampering the market because these processes require specialized knowledge of tool alignment, coolant pressure, chip evacuation, feed rates, and bore accuracy. Improper machine handling can lead to tool breakage, poor surface finish, dimensional errors, and higher scrap rates. Many manufacturers struggle to find trained personnel who can operate advanced CNC deep-hole drilling systems efficiently. This limits adoption among smaller workshops and increases reliance on external machining service providers, slowing overall market growth.

Market Opportunities

- Medical Implant Precision Gun Drill: Medical implant precision gun drilling is creating opportunities as implants and surgical instruments require extremely accurate micro-holes, smooth internal finishes, and tight dimensional tolerances. Demand is rising for orthopedic implants, dental implants, trauma devices, and minimally invasive surgical tools. In May 2025, Resonetics acquired the nitinol gun drilling operations and related assets of Medical Component Specialists’ New Boston, NH facility, strengthening its U.S.-based nitinol manufacturing capabilities. The acquisition supports Resonetics’ broader strategy to improve the availability and supply of nitinol, a key material used in advanced next-generation medical devices. As medical device makers expand production of implants, guidewires, stents, and minimally invasive surgical tools, demand for advanced deep hole drilling machines is expected to increase.

- Defense Gun Barrel and Missile Component Deep Hole: Defense gun barrel and missile component deep-hole machining is creating opportunities, as these applications require long, straight, high-precision bores with excellent surface finish and dimensional accuracy. Rising defense modernization, ammunition production, and missile system development are increasing demand for specialized gun drilling and BTA machines. These systems help manufacture barrels, launcher parts, hydraulic components, and guidance-related structures with consistent quality. As defense manufacturers prioritize reliability, safety, and performance, the adoption of advanced deep hole drilling machines is expected to grow.

Market Challenges

- Complex Machine Setup and Longer Training Requirements: Complex machine setup and longer training requirements present a significant challenge as achieving accurate deep-hole machining requires precise alignment, tooling selection, coolant management, and process parameter optimization. Operators must be trained to handle specialized techniques such as gun drilling and BTA drilling to avoid bore deviation, tool failure, and quality issues.

- Risk of Tool Breakage, Bore Deviation, and Quality Defects: Deep-hole machining involves long drilling depths, high cutting forces, and strict tolerance requirements. Any misalignment, poor chip evacuation, coolant failure, or incorrect feed speed can damage tools and compromise bore accuracy. These issues lead to higher scrap rates, machine downtime, rework costs, and production delays. As a result, manufacturers may hesitate to adopt deep hole drilling systems unless they have strong process control, skilled operators, and reliable maintenance support.

Emerging Market Trends

.webp)

1. AI-Adaptive CNC Deep Hole Drilling

AI-adaptive CNC deep hole drilling is emerging as manufacturers seek higher precision, productivity, and process automation. AI-enabled systems can analyze real-time machining data, including vibration, temperature, tool wear, and cutting performance, to automatically adjust drilling parameters. This improves bore accuracy, reduces tool breakage, minimizes downtime, and extends tool life. As Industry 4.0 adoption accelerates across aerospace, automotive, defense, and energy sectors, demand for AI-driven deep hole drilling solutions is expected to grow significantly.

2. Multi-Spindle and Pallet-Automated CNC Deep Hole Cell

Multi-spindle and pallet-automated CNC deep hole cells are emerging as manufacturers seek higher throughput and greater production efficiency. Multi-spindle configurations enable multiple holes to be drilled simultaneously, reducing cycle times and increasing output. Meanwhile, pallet automation allows automatic loading and unloading of workpieces, minimizing downtime and labor requirements. These systems support continuous, high-volume production while maintaining precision and consistency, making them increasingly attractive for automotive, aerospace, defense, and industrial manufacturing applications.

3. Rare Earth Exploration Deep Drilling Expansion

Rare earth exploration deep drilling expansion are emerging as demand for critical minerals and rare earth elements rises across EVs, wind turbines, electronics, and defense applications. Exploration companies are increasingly using deep drilling programs to test high-priority mineral targets at greater depths. In June 2026, Appia Rare Earths and Uranium CEO Tom Drivas announced the mobilization of a 3,300-metre diamond drilling program at the company’s fully owned Alces Lake Rare Earth Elements project in northern Saskatchewan. This is creating demand for reliable drilling machines capable of operating in complex geological conditions with high accuracy and durability.

4. EV Motor and Battery Component Deep Hole Growth

EV motor and battery component deep hole growth is emerging as electric vehicle production continues to accelerate worldwide. EV motors, battery housings, cooling plates, rotor shafts, and powertrain components require precise deep-hole machining for thermal management, structural integrity, and performance optimization. Manufacturers are increasingly adopting advanced CNC deep hole drilling systems to achieve tighter tolerances, higher productivity, and superior component quality. The rapid expansion of the EV industry is therefore creating new demand for specialized deep hole drilling solutions across automotive supply chains.

Industry Value Chain Analysis

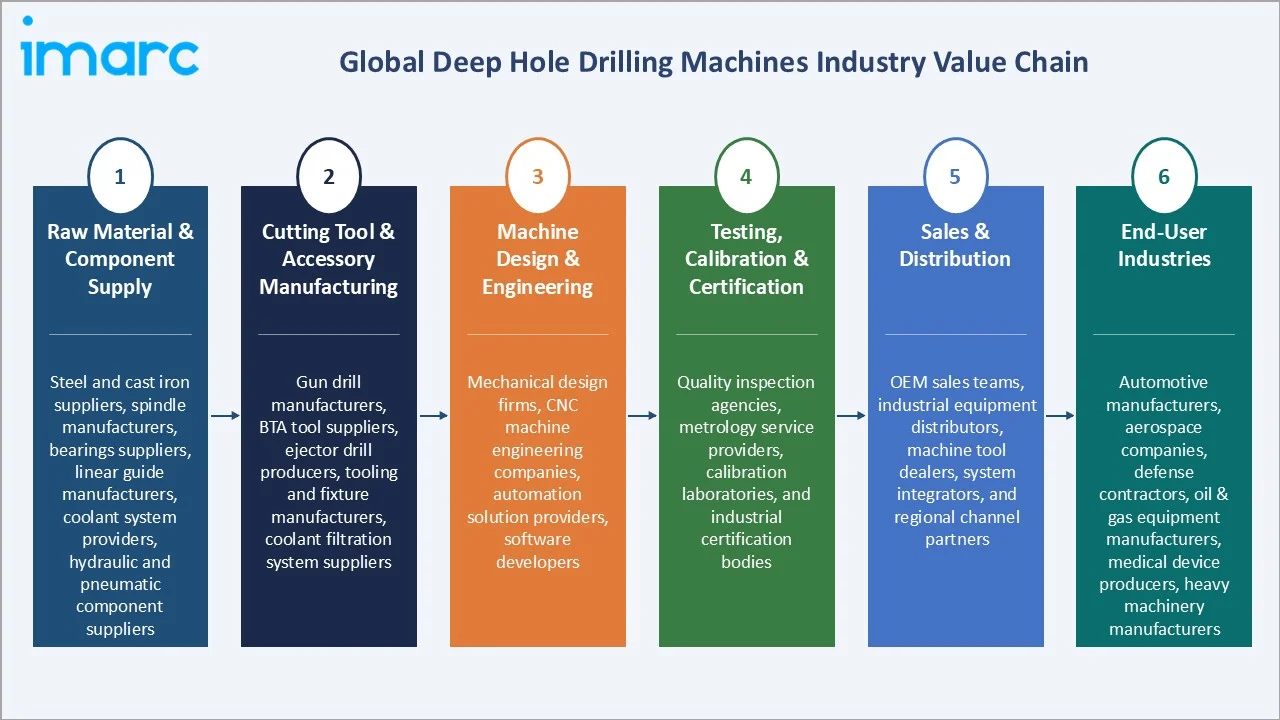

The deep hole drilling machines value chain integrates raw material & component supply, cutting tool & accessory manufacturing, machine design & engineering, testing, calibration & certification, sales & distribution, and end-user industries.

|

Stage |

Key Participants |

|

Raw Material & Component Supply |

Steel and cast iron suppliers, spindle manufacturers, bearings suppliers, linear guide manufacturers, coolant system providers, hydraulic and pneumatic component suppliers |

|

Cutting Tool & Accessory Manufacturing |

Gun drill manufacturers, BTA tool suppliers, ejector drill producers, tooling and fixture manufacturers, coolant filtration system suppliers |

|

Machine Design & Engineering |

Mechanical design firms, CNC machine engineering companies, automation solution providers, software developers |

|

Testing, Calibration & Certification |

Quality inspection agencies, metrology service providers, calibration laboratories, and industrial certification bodies |

|

Sales & Distribution |

OEM sales teams, industrial equipment distributors, machine tool dealers, system integrators, and regional channel partners |

|

End-User Industries |

Automotive manufacturers, aerospace companies, defense contractors, oil & gas equipment manufacturers, medical device producers, heavy machinery manufacturers |

The machine manufacturing & assembly stage is typically the most value-added stage in the deep hole drilling machines value chain. This phase combines precision mechanical engineering, CNC control systems, automation technologies, spindle integration, and application-specific customization to create the final high-performance machine. A significant portion of the product's intellectual property, technological differentiation, and profit margins is generated at this stage. Manufacturers that offer advanced CNC capabilities, automation features, and turnkey solutions generally capture the highest value within the industry.

Technology Landscape in the Deep Hole Drilling Machines Industry

Gun Drilling Technology

Gun drilling technology forms a foundational element due to its ability to produce highly accurate, straight, and smooth deep holes with superior surface finishes. The technology utilizes specialized single-lip drill tools and high-pressure coolant systems to ensure efficient chip removal and dimensional precision. Continuous advancements in CNC integration, tool materials, and process monitoring are enhancing drilling speed, accuracy, and reliability. As a result, gun drilling remains widely adopted across aerospace, automotive, medical device, defense, and precision engineering applications.

BTA/STS Drilling Technology

BTA/STS (boring and trepanning association / single tube system) drilling technology enables the efficient machining of large-diameter and ultra-deep holes with high productivity. The technology uses internal coolant delivery and optimized chip evacuation to maintain drilling stability and accuracy over extended depths. Advances in CNC controls, monitoring systems, and cutting tool designs are further improving performance, reducing cycle times, and extending tool life. As a result, BTA/STS drilling is increasingly used in oil & gas, aerospace, defense, heavy machinery, and energy applications where precision deep-hole machining is critical.

Down-the-Hole (DTH) Surface Drilling Technology

Down-the-hole (DTH) surface drilling technology enables efficient drilling of deep, straight holes in hard rock and challenging geological formations. The technology places the hammer directly behind the drill bit, improving energy transfer, penetration rates, and drilling accuracy. Advances in DTH systems, including automated controls, enhanced hammer designs, and real-time monitoring, are improving operational efficiency and reducing drilling costs. In February 2026, Sandvik launched the Leopard DI610i, a high-performance down-the-hole (DTH) surface drill rig built for open-pit mining, large quarry operations, and drilling contractors. As mining, quarrying, infrastructure, and mineral exploration activities expand, demand for advanced DTH drilling solutions continues to grow.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

BTA Machines |

🔒 |

2025 |

|

Operation |

CNC |

71.8% |

2025 |

|

Business Type |

Original Equipment Manufacturer (OEM) |

🔒 |

2025 |

|

End-user Industry |

Automotive |

24.7% |

2025 |

|

Region |

Asia-Pacific |

39.5% |

2025 |

By Operation

CNC leads at 71.8% (2025), due to its superior precision, automation capability, and ability to perform complex deep-hole drilling with consistent repeatability. Its integration with real-time monitoring, advanced controls, and multi-axis machining improves productivity, reduces errors, and supports high-volume industrial applications.

To access detailed market analysis, Request Sample

Non-CNC at 28.2% driven by demand from cost-sensitive manufacturers, small workshops, and maintenance operations that require simpler drilling solutions with lower upfront investment. They remain preferred for low-volume production, basic deep-hole machining tasks, and applications where full automation and advanced programming capabilities are not essential.

By End-user Industry

Automotive leads at 24.7% (2025), through engine block, crankshaft, camshaft, hydraulic valve body, and EV motor housing deep hole drilling.

.webp)

Oil and gas at 19.8% reflects drill collar, drill pipe, MWD tool, and downhole component BTA deep hole boring. Aerospace at 14.2% grows fastest at ~5.6% CAGR through turbine blade cooling hole, titanium structural, and composite fastener deep hole. Construction and mining at 12.6% reflects rock drill steel, mining equipment, and hydraulic hammer for deep holes. Energy at 10.8% reflects the wind turbine shaft, nuclear reactor component, and hydraulic cylinder deep hole. Military and defense at 8.1% reflects gun barrel, missile body, and MIL-SPEC component deep hole. Medical at 5.4% reflects cannulated implant, surgical instrument, and catheter deep hole. Others at 4.4% includes heavy machinery, industrial equipment, shipbuilding, railways, tooling and mold manufacturing, hydraulics and pneumatics, precision engineering, and general manufacturing applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Deep Hole Drilling Machines Market Drivers & Characteristics |

|

Asia-Pacific |

39.5% |

Driven by its strong automotive, aerospace, heavy machinery, and industrial manufacturing base. |

|

Europe |

26.1% |

Benefits from high adoption of automated CNC machining technologies, stringent quality standards, and continuous investments in precision manufacturing and Industry 4.0 initiatives. |

|

North America |

23.4% |

Supported by strong demand from aerospace, defense, oil & gas, medical device, and energy industries. |

|

Latin America |

6.1% |

Driven by mining, oil & gas, industrial equipment, and infrastructure development activities. |

|

Middle East and Africa |

4.9% |

Supported by oil & gas, mining, energy, and infrastructure sectors. |

Asia-Pacific's 39.5% supported by its large automotive, aerospace, industrial machinery, and precision manufacturing sectors, particularly in China, Japan, South Korea, and India. Europe's 26.1% due to its advanced engineering capabilities, aerospace production, and widespread adoption of Industry 4.0 technologies.

North America's 23.4% benefits from substantial demand from aerospace, defense, medical device, and oil & gas industries that require high-precision deep-hole machining. Latin America's 6.1% and Middle East & Africa’s 4.9% are witnessing gradual growth driven by mining, energy, infrastructure, and industrial development projects.

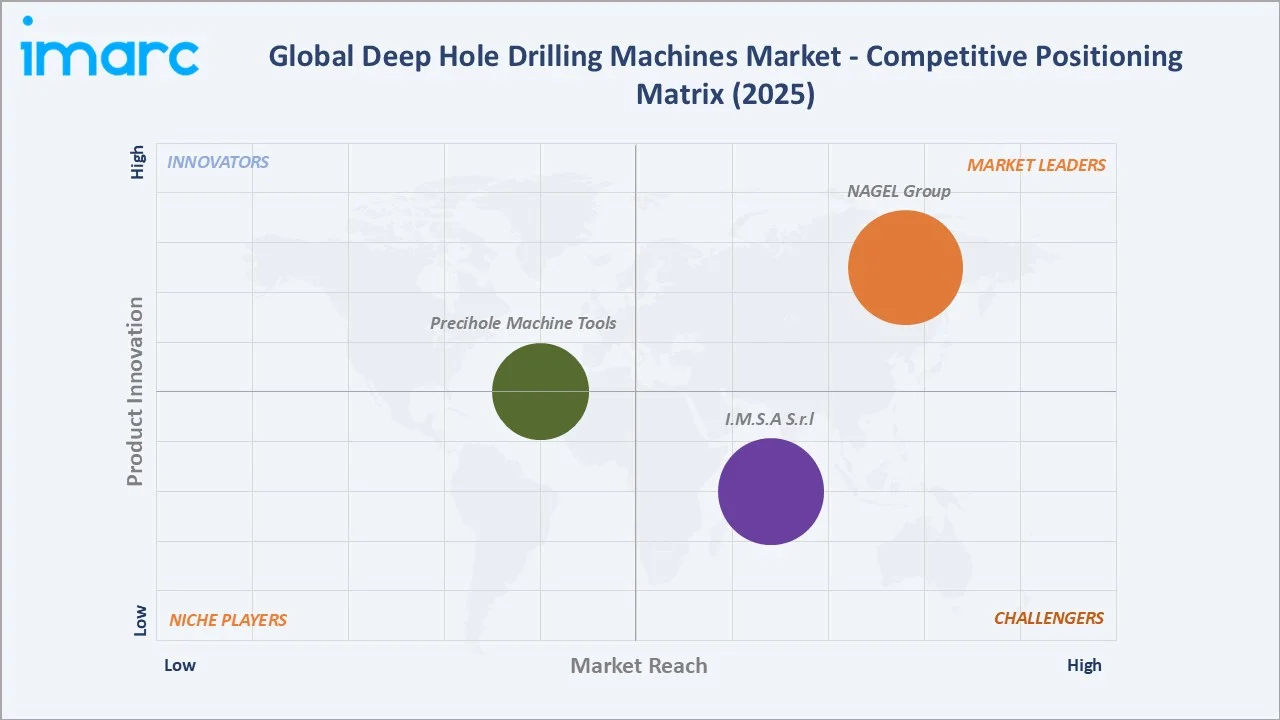

Competitive Landscape

The global deep hole drilling machines market is moderately consolidated, with competition centered on technological innovation, machining precision, automation capabilities, and aftermarket service support. Leading manufacturers focus on developing advanced CNC systems, multi-axis machining platforms, AI-enabled process monitoring, and automated production cells to enhance productivity and accuracy.

|

Company |

Key Products |

Market Position |

Core Strength |

|

NAGEL Group |

ML series, B series, BW series |

Market Leader |

The NAGEL Group plays a major role in deep hole drilling through its wholly-owned German subsidiary, TBT Tiefbohrtechnik GmbH + Co. |

|

I.M.S.A S.r.l |

MF800C, MF1200 D, MF1000 /2C, MF1000/2F with Rotary Table, MF1750 EVO, MFT 600 /12 EVO, MFT 1000EVO |

Strong Challenger |

I.M.S.A. S.r.l. is an Italian manufacturer that specializes in custom-tailored deep hole drilling machines. Recognized as an industry pioneer, the company focuses heavily on gundrilling and BTA (Boring and Trepanning Association) drilling technologies for mold-making, aerospace, and precision mechanical engineering. |

|

Precihole Machine Tools |

GVN06M micro gun drilling machine, GVN Series Gun Drilling Machines, XYGVN Series Knee Type Multi Axis Gun Drilling Machines, XYGVNCL Series Column Type Multi-Axis Gun Drilling Machines, BVN Series BTA (STS) Deep Hole Drilling Machines |

Established Player |

Precihole Machine Tools is a leading manufacturer and global provider of deep hole drilling and hole finishing solutions. For over decades, the company has engineered standard, custom, and Special Purpose Machines (SPMs) that provide high precision, straightness, and surface finish for complex components across various industries. |

Companies are also investing in specialized solutions for aerospace, automotive, defense, medical, and energy applications that require high-precision deep-hole machining. Strategic initiatives such as product launches, technology partnerships, capacity expansions, and acquisitions are common as players seek to strengthen their market positions. Growing demand for Industry 4.0-compatible equipment and customized drilling solutions is further intensifying competition across global markets.

Key Company Profiles

NAGEL Group

NAGEL Group is a Germany-based manufacturer specializing in precision machining, honing, superfinishing, deep hole drilling, and turnkey production systems for automotive and industrial applications. The company, through its subsidiary TBT Tiefbohrtechnik GmbH + Co., offers advanced deep hole drilling solutions integrated with CNC controls, automation systems, and customized production cells designed to achieve high accuracy, superior surface quality, and efficient machining of complex components.

- Key Products: ML series, B series, BW series.

- Strategic Focus: Delivering high-precision machining solutions through advanced CNC technology, automation, and integrated production systems.

I.M.S.A S.r.l

I.M.S.A. S.r.l. is an Italy-based manufacturer specializing in deep hole drilling and boring machines for precision machining applications. The company is recognized for its expertise in gun drilling, BTA drilling, trepanning, and multifunction machining solutions capable of handling complex deep-hole operations.

- Key Products: MF800C, MF1200 D, MF1000 /2C, MF1000/2F with Rotary Table, MF1750 EVO, MFT 600 /12 EVO, MFT 1000EVO.

- Strategic Focus: Providing high-precision deep hole drilling solutions through advanced CNC technology, multi-functional machining centers, and customized manufacturing systems.

Market Concentration Analysis

The global deep hole drilling machines market exhibits a moderately concentrated competitive structure, with a mix of established machine tool manufacturers and specialized deep-hole drilling technology providers. Leading players such as NAGEL Group, I.M.S.A S.r.l, and Precihole Machine Tools hold strong positions through advanced CNC capabilities, application expertise, and global service networks. Competition is primarily based on machining precision, automation, customization, and aftermarket support rather than price alone. Market leaders continue to invest in Industry 4.0 integration, AI-enabled process monitoring, and multi-functional machining platforms to strengthen differentiation. Meanwhile, regional manufacturers compete by offering cost-effective solutions and customized systems tailored to specific end-user requirements.

Investment & Growth Opportunities

Highest Growth Segments

CNC operation (~5.2% CAGR), aerospace end-user (~5.6% CAGR), EV motor housing deep hole (~8-10% CAGR from smaller base), medical cannulated implant (~6-8% CAGR), defense gun barrel (~4-5% CAGR), and Asia-Pacific CNC upgrade (~5.5% CAGR) represent deep hole drilling highest-growth investment vectors through 2034.

Investment Themes

- Aerospace titanium and nickel superalloy CNC BTA: The increasing use of titanium and nickel superalloys in aircraft engines, landing gear, and structural components is driving demand for advanced CNC BTA drilling systems. These materials are difficult to machine, creating opportunities for high-performance deep hole drilling solutions that offer superior precision, tool life, and productivity.

- EV motor housing and battery cooling deep hole CNC: The rapid growth of electric vehicles is increasing demand for precision-drilled motor housings, rotor shafts, battery cooling plates, and thermal management systems. CNC deep hole drilling machines are becoming essential for producing complex EV components with tight tolerances and improved heat dissipation performance.

- Medical precision gun drill for cannulated implant and surgical instrument: Growing demand for orthopedic implants, dental implants, and minimally invasive surgical instruments is creating opportunities for precision gun drilling technologies. These applications require ultra-accurate micro-holes, excellent surface finishes, and strict dimensional control, supporting investment in advanced medical-grade deep hole drilling systems.

Future Market Outlook (2026-2034)

The global deep hole drilling machines market is projected to grow from USD 654.1 Million in 2025 to USD 993.3 Million by 2034, delivering a 4.61% CAGR over the forecast period through aerospace precision component demand, EV automotive electrification adding deep hole applications, oil and gas drill collar BTA demand, medical precision expanding, and the CNC Industry 4.0 upgrading. The market's anchor value of USD 819.4 Million in 2030 represents deep hole drilling at Industry 4.0 inflection.

Three structural forces define the deep hole drilling machines market growth through 2034. First, the rising demand for precision-machined components in aerospace, automotive, defense, medical, and energy industries is increasing the need for advanced deep-hole drilling capabilities. Second, the adoption of CNC automation, AI-driven process optimization, and Industry 4.0 technologies is improving productivity, accuracy, and operational efficiency. Third, growing investments in EV manufacturing, critical mineral exploration, and high-performance industrial equipment are expanding applications for deep hole drilling machines across both established and emerging end-use sectors.

Research Methodology

Primary Research

Primary research comprised in-depth interviews and discussions with deep hole drilling machine manufacturers, CNC system providers, tooling suppliers, distributors, and industry experts. Insights were also gathered from production managers, machining specialists, and procurement executives across aerospace, automotive, defense, energy, and medical sectors.

Secondary Research

Secondary research encompassed company websites, annual reports, investor presentations, product brochures, trade publications, and industry databases. It also included reviewing machine tool associations, import-export data, technical papers, and government manufacturing statistics.

Forecasting Models

Forecasting models combined historical market performance, end-use industry demand trends, and macroeconomic indicators to estimate future market growth. Quantitative techniques such as CAGR analysis, trend extrapolation, and demand-side modeling were used alongside qualitative assessments of technology adoption, automation trends, and industrial investment patterns. Scenario analysis and expert validation were applied to ensure the robustness and reliability of long-term market projections through 2034.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Coverage | BTA Machines, Gun Drilling Machines, Skiving and Burnishing Machines |

| Operations Coverage | CNC, Non-CNC |

| Business Types Coverage | Original Equipment Manufacturer (OEM), Aftermarket |

| End-user Industries Coverage | Oil and Gas, Medical, Automotive, Construction and Mining, Energy, Aerospace, Military and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | NAGEL Group, I.M.S.A S.r.l, Precihole Machine Tools, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the deep hole drilling machines market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global deep hole drilling machines market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the deep hole drilling machines industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Deep Hole Drilling Machines Market Report

The global deep hole drilling machines market reached USD 654.1 Million in 2025, driven by rising demand for high-precision machining across automotive, aerospace, defense, oil & gas, medical, and energy sectors. Growth is supported by increasing adoption of CNC automation, AI-enabled monitoring, and Industry 4.0 manufacturing systems. Expanding EV production, critical mineral exploration, and advanced component manufacturing are further creating demand for efficient and accurate deep-hole drilling solutions.

The global deep hole drilling machines market grows at 4.61% CAGR during 2026-2034, reaching USD 993.3 Million by 2034. The CAGR reflects aerospace precision demand, EV adding motor housing deep hole, oil and gas drill collar BTA, CNC Industry 4.0 upgrade, and medical cannulated implants.

CNC leads at 71.8% due to their ability to deliver superior precision, repeatability, and process control in complex deep-hole machining operations. They enable automated parameter adjustments, real-time monitoring, and consistent drilling quality, reducing human error and production downtime.

Automotive leads at 24.7% due to strong demand for precision deep-hole machining in engine blocks, crankshafts, camshafts, transmission shafts, fuel injection systems, and hydraulic components. The segment benefits from high-volume production requirements and the need for consistent dimensional accuracy across complex parts.

Asia-Pacific leads at 39.5% due to its strong automotive, aerospace, heavy machinery, and industrial manufacturing base across China, India, Japan, and South Korea. Rising CNC adoption, factory automation, and large-scale component production are increasing demand for precision deep-hole drilling machines.

Leading companies include NAGEL Group, I.M.S.A S.r.l, and Precihole Machine Tools, among others.

The market is projected to reach approximately USD 819.4 Million by 2030, reflecting steady demand from automotive, aerospace, oil & gas, defense, and medical manufacturing. Growth will be supported by CNC automation, precision machining requirements, and wider adoption of advanced deep-hole drilling technologies.

Three priority investment opportunities include aerospace titanium and nickel superalloy CNC BTA drilling, driven by increasing aircraft production and demand for precision machining of advanced materials. EV motor housing and battery cooling deep-hole CNC solutions offer strong growth potential as electric vehicle manufacturing expands globally. Additionally, medical precision gun drilling for cannulated implants and surgical instruments presents an attractive opportunity due to rising healthcare demand and the need for ultra-precise, high-value medical components.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade