Dental 3D Scanners Market Report by Product (Desktop Or Laboratory 3D Dental Scanners, Intraoral 3D Dental Scanners, Cone Beam Computerized Tomography (CBCT)), End User (Hospitals, Dental Clinics), and Region 2026-2034

Market Overview:

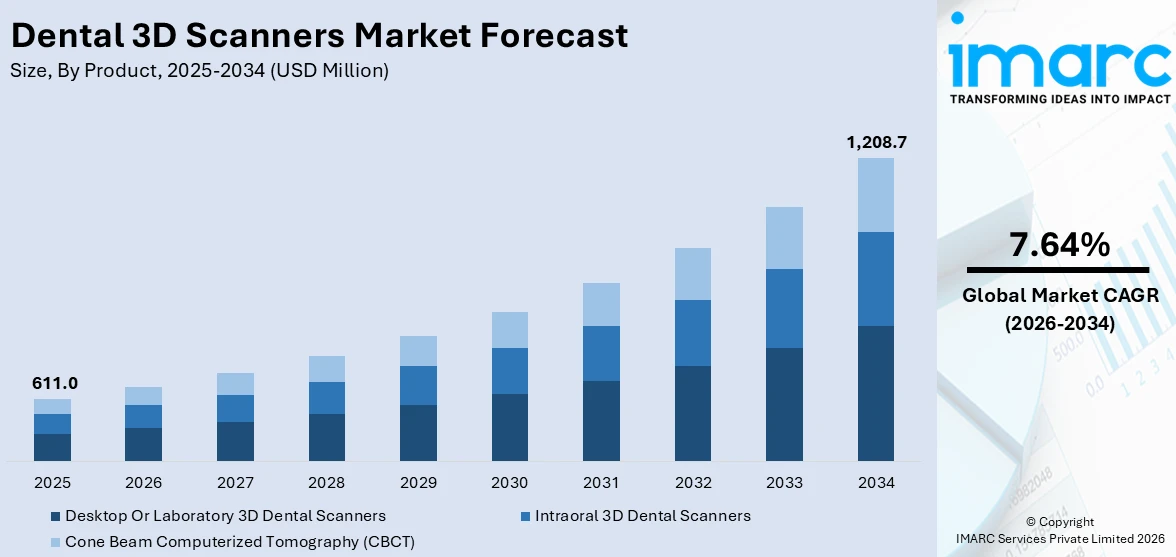

The global dental 3D scanners market size reached USD 611.0 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,208.7 Million by 2034, exhibiting a growth rate (CAGR) of 7.64% during 2026-2034. Rapid advancements in digital dentistry, rising prevalence of dental disorders, increasing demand for cosmetic dentistry procedures, shift to digital workflows, continuous technological advancements, rising geriatric population, growing disposable income, favorable government initiatives and subsidies, are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 611.0 Million |

| Market Forecast in 2034 | USD 1,208.7 Million |

| Market Growth Rate (2026-2034) | 7.64% |

Dental 3D scanners Market Analysis:

- Major Market Drivers: Increased demand for digital dental diagnostics, growing incidence of dental disorders, and expansion in the geriatric population drive the market. Better patient outcomes and more efficient workflow also promote the adoption of dental 3D scanners in clinics and laboratories.

- Key Market Trends: One of the key trends consists of the mass shift from analog impressions to computer-aided design workflows. Growing cosmetic dental treatments and CAD/CAM system integration are also transforming the market, coupled with technological developments providing quicker, more precise, and easier-to-use 3D scanning technology.

- Competitive Landscape: The market is somewhat consolidated with international and regional firms competing on innovation, precision, and integration of software. The companies emphasize strategic alliances, R&D, and broadening product offerings to reinforce their presence in dental clinics, laboratories, and universities worldwide.

- Challenges and Opportunities: High investment costs of equipment and low digital literacy in certain geographies are challenges, but rising awareness, chairside scanning demand, and the uptake of digital dentistry among emerging economies are powerful opportunities for market growth and greater access to 3D scanning technology.

To get more information on this market Request Sample

Dental 3D scanners are advanced medical devices used in the field of dentistry to capture highly detailed and precise three-dimensional (3D) images of a patient's oral structures, including teeth, gums, and jawbone. These scanners employ cutting-edge technology, such as lasers or structured light, to create digital models of the patient's dental anatomy. Dental professionals use these digital models for a wide range of applications, including treatment planning for restorative procedures, orthodontic assessments, and the creation of custom dental prosthetics like crowns and bridges. Moreover, dental 3D scanners also contribute to improved diagnostics, treatment outcomes, and overall patient care in the dental industry.

The increasing awareness among both dental professionals and patients about the benefits of digital dentistry is fostering greater adoption of these advanced scanning technologies. In addition to this, the growing prevalence of dental disorders and the need for precise diagnostics and treatment planning are further driving the demand. Moreover, the rising demand for cosmetic dentistry procedures, such as dental implants and orthodontics, relies heavily on 3D scanning for accurate customization and aesthetics. Furthermore, technological advancements, such as faster scanning speeds and improved accuracy, are enhancing the appeal of dental 3D scanners. The ongoing trend of dental clinics and laboratories transitioning to digital workflows to streamline processes and reduce manual errors is another contributing factor. Besides this, the increasing geriatric population, which often requires extensive dental care, is bolstering market growth.

Dental 3D Scanners Market Trends/Drivers:

Increasing awareness of digital dentistry

The growing awareness and acceptance of digital dentistry practices among dental professionals and patients are significantly driving the demand for dental 3D scanners. Moreover, dental practitioners are increasingly recognizing the advantages of digital workflows in terms of accuracy, efficiency, and patient comfort. Patients, on the other hand, are becoming more inclined towards treatments that incorporate advanced technology due to the perception of better outcomes and reduced discomfort. This awareness has led to a shift from traditional analog methods to digital solutions, with dental 3D scanners at the forefront of this transformation.

Rising prevalence of dental disorders

The global increase in the prevalence of dental disorders, such as tooth decay, gum diseases, and malocclusions, is another factor facilitating the demand for dental 3D scanners. As these conditions become more common, the need for precise and efficient diagnostic tools is paramount. Dental 3D scanners offer unparalleled accuracy in capturing the intricate details of oral structures, enabling early detection and comprehensive treatment planning. Consequently, dental professionals are increasingly relying on these scanners to provide optimal care to their patients.

Growing demand for cosmetic dentistry procedures

The growing demand for cosmetic dentistry procedures, including dental implants, veneers, and orthodontics, is fueling the adoption of dental 3D scanners. Dental 3D scanners excel in this regard, allowing for the creation of highly accurate digital models that serve as the foundation for crafting custom restorations and aligners. As more individuals seek cosmetic dental enhancements to improve their smiles, the use of 3D scanners becomes indispensable in achieving natural-looking and long-lasting results, driving market growth in this segment. Furthermore, the widespread adoption of dental 3D scanners as it enables dentists to communicate and collaborate more effectively with dental laboratories and other specialists involved in the cosmetic dental treatment process, is supporting the market growth.

Dental 3D Scanners Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global dental 3D scanners market report, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product and end user.

Breakup by Product:

- Desktop Or Laboratory 3D Dental Scanners

- Intraoral 3D Dental Scanners

- Cone Beam Computerized Tomography (CBCT)

Desktop or laboratory 3D dental scanners dominate the market

The report has provided a detailed breakup and analysis of the market based on the product. This includes desktop or laboratory 3D dental scanners, intraoral 3D dental scanners, and cone beam computerized tomography (CBCT). According to the report, desktop or laboratory 3D dental scanners represented the largest segment.

Desktop or laboratory 3D dental scanners are leading the product type segment in the dental 3D scanners market primarily due to their advanced capabilities, high precision, and versatility. These scanners are generally more reliable and offer better image quality compared to their portable counterparts. Additionally, they are designed to handle a larger volume of scanning tasks, making them well-suited for high-throughput dental laboratories and clinics. The desktop variants also usually have better software integration, offering a more comprehensive range of options for dental modeling and analysis. Moreover, economies of scale often make desktop or laboratory 3D dental scanners more cost-effective in the long run for dental practices with a high volume of cases. Their robustness and durability also mean less frequent replacements and lower maintenance costs. The above-mentioned factors contribute to the prominence of the desktop or laboratory 3D dental scanners among the professionals in the dental field, thereby dominating this market segment.

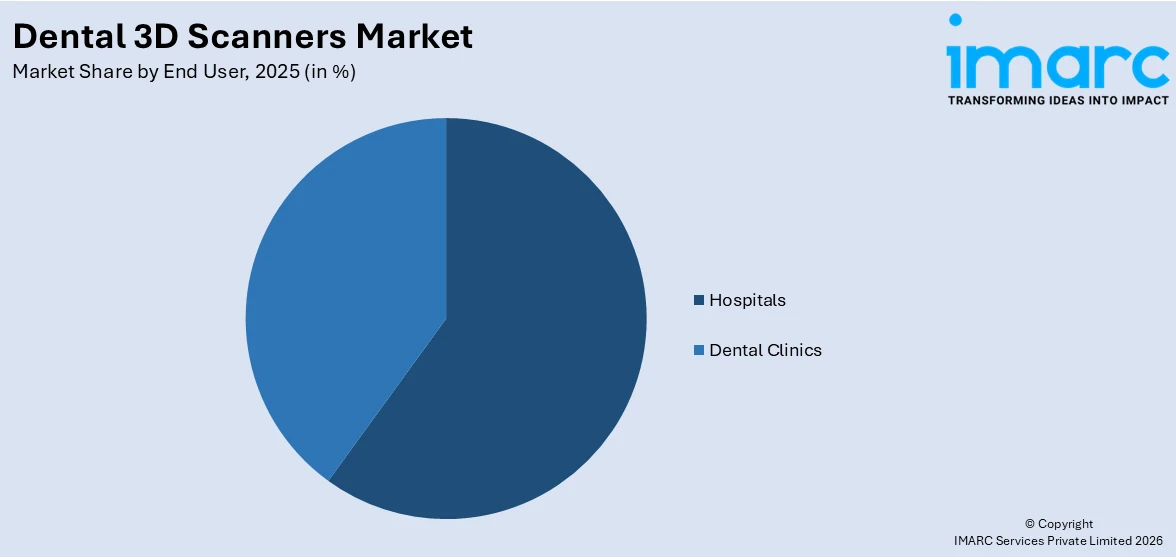

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Dental Clinics

Hospitals hold the largest share in the market

A detailed breakup and analysis of the market based on the end user has also been provided in the report. This includes up to hospitals and dental clinics. According to the report, hospitals accounted for the largest market share.

Hospitals are taking a leading role in the end user segment of the dental 3D scanners market for several key reasons. Hospitals have greater access to financial resources, which enables them to invest in advanced technologies such as dental 3D scanners. This technology facilitates more accurate diagnoses and planning, contributing to improved patient outcomes in oral health care. Moreover, hospitals generally handle a higher volume of patients compared to private dental practices, making the efficiency and speed offered by 3D scanning technology especially valuable. This high patient turnover requires robust technology to ensure quick and accurate results. Additionally, the multidisciplinary nature of hospitals often necessitates a higher standard of care and equipment. Dental 3D scanners fit into this requirement by offering versatile functionalities that can be utilized in various aspects of dental medicine, from orthodontics to oral surgery. For these reasons, hospitals are increasingly dominating the end user segment of the dental 3D scanners market.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest dental 3D scanners market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America holds a leading position in the dental 3D scanners market primarily due to advanced healthcare infrastructure, increased investment in dental technologies, and a high level of awareness among patients and practitioners about the benefits of 3D scanning in dental procedures. The region is also home to several key market players who actively invest in research and development, thereby driving technological advancements in dental 3D scanners. Additionally, insurance coverage and reimbursement policies in North America tend to be more favorable towards new and sophisticated medical technologies, which further promotes adoption. Moreover, educational programs and workshops contribute to better skills and knowledge among dental professionals, augmenting the uptake of 3D scanners in dental diagnostics and treatments. These factors collectively contribute to North America's dominant role in the dental 3D scanners market.

Key Regional Takeaways:

North America Dental 3D Scanners Market Analysis

North America is a leader in the dental 3D scanners market with its highly developed healthcare infrastructure, early demand for digital dentistry, and high per capita dental expenditure. The United States has the largest share, fueled by a developed network of dental clinics, good insurance coverage, and demand for cosmetic and restorative dental procedures. The presence of high awareness levels among dental professionals and patients sustains the adoption of intraoral and laboratory scanners. Furthermore, North American academic institutions and research facilities are also investing significantly in the advancement of advanced scanning technologies, further consolidating regional leadership. Support in terms of regulations for digital dental devices and coordination among dental clinics and manufacturers of scanners further boost market expansion. The accelerating geriatric population with high prevalence of dental conditions along with the increasing digitalization of the healthcare industry is further keeping North America at the forefront as a key player in the global dental 3D scanners market.

Europe Dental 3D Scanners Market Analysis

Europe accounts for a major share in the dental 3D scanners market owing to the increasing adoption of digital workflows and favorable pool of trained dental professionals. Regions like Germany, the UK, France, and Italy dominate the regional market, with well-entrenched dental education frameworks and positive reimbursement mechanisms for oral care. Increasing popularity for cosmetic and implant dentistry among the populace further fuels the adoption of precision diagnostic tools such as 3D scanners. Dental labs throughout Europe are also progressively adopting CAD/CAM technologies, where desktop 3D scanners play a central role. The concentration of some leading scanner brands based in Europe enhances the competitive edge. Additionally, public campaigns towards oral health and healthcare digitalization continue to fuel market growth. Despite some cost-related issues in rural settings, the region's emphasis on high-quality dental results and patient-focused services continues to underpin demand for dental 3D scanning technology among private and institutional practices.

Asia Pacific Dental 3D Scanners Market Analysis

The Asia Pacific region is emerging as one of the rapidly growing dental 3D scanners markets, as the region is influenced by increasing disposable incomes, an increasing awareness of oral care, and access to modern dental services. Countries such as China, Japan, South Korea, and India are witnessing swift adoption of digital dentistry tools that have been prompted by urbanization and demand for high-quality cosmetic dental procedures. Governments in the region are promoting healthcare infrastructure development, including digital diagnostic machines in both private and public dental clinics. Production of affordable 3D scanners locally is also enhancing market penetration in price-conscious markets. In addition, the boosting geriatric population in nations like Japan, combined with high rates of dental disorders, drive scanner adoption. As dental labs and clinics in the region increasingly invest in chairside scanning solutions and workflow automation, Asia Pacific will emerge as a key region for market growth in the next few years with robust prospects in urban as well as semi-urban regions.

Latin America Dental 3D Scanners Market Analysis

In Latin America, the market for dental 3D scanners is slowly growing with improving dental healthcare infrastructure and heightened focus on aesthetic dentistry. Brazil and Mexico are leading contributors to regional demand, sustained by a relatively extensive base of dentists and growing awareness of new dental technologies. Expansion of private dental chains and growing popularity of aesthetic procedures like veneers and aligners are driving demand for precision scanning instruments. Although cost is a hindrance to mass use in public settings, dental clinics and high-end city centers are at the forefront of adopting 3D scanning systems. Training sessions and dental conventions also aid in narrowing the gap of information around digital technology. As increasingly educated patients are learning about technology-based treatments, and manufacturers are providing cost-effective scanner models, the Latin American market will see consistent growth, especially in urban areas and medical tourism destinations for high-quality dental care.

Middle East and Africa Dental 3D Scanners Market Analysis

The Middle East and African market for dental 3D scanners is recording encouraging growth potential, driven by high-income nations in the Gulf region like Saudi Arabia and the UAE. The nations are pursuing significant investments in healthcare modernization and quality dental treatment, with private clinics embracing digital scanners to provide upscale cosmetic and restorative treatments. Dental tourism in the Middle East is further sustaining scanner demand. Conversely, scanner penetration in certain areas of Africa is lower because of inadequate healthcare financing and shortage of trained professionals. Yet, government reforms, foreign-aid programs, and partnerships with international dental technology providers are increasingly enhancing access to state-of-the-art equipment. As there is more emphasis on quality dental outcomes, urbanization, and the growing dental disease burden, the region presents long-term growth prospects. Market participants with portable and low-cost scanner solutions designed for low-resource environments have the potential to unlock untapped markets in underserved regions of Africa.

Competitive Landscape:

The leading players in the global dental 3D scanners market are actively engaged in several strategic initiatives to maintain and expand their market presence. They are consistently investing in research and development (R&D) to enhance the capabilities of their scanner technologies. This includes improving scanning speed, accuracy, and software integration to streamline workflows for dental practitioners. Additionally, market leaders are focusing on expanding their product portfolios to cater to a wider range of dental applications, from restorative dentistry to orthodontics. They are also emphasizing user-friendly interfaces to ensure that dental professionals of varying expertise levels can efficiently utilize their equipment. Moreover, these companies are forging partnerships and collaborations with dental clinics, laboratories, and educational institutions to promote the adoption of their 3D scanning solutions.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- 3Shape A/S

- AGE Solutions S.r.l.

- Align Technology, Inc.

- Amann Girrbach AG

- Carestream Dental LLC

- Condor Technologies NV

- Densys Ltd.

- Dentsply Sirona Inc.

- Envista Holdings Corporation

- Kulzer GmbH (Mitsui Chemicals Group)

- Planmeca Oy

- Shining 3D Tech Co., Ltd.

- Straumann Holding AG

Latest News and Developments:

- In July 2025, Medit will introduce the Medit i900 Mobility intraoral scanner, engineered to improve chairside procedures and facilitate mobile care. Based on a mobility-first design, the device is aimed at addressing the changing needs of multi-chair clinics and contemporary dental practices, simplifying intraoral scanning processes.

- In March 2025, 3Shape introduced the TRIOS 6 intraoral scanner at IDS 2025 with hyperspectral imaging to detect caries and gingival recession. Introduced along with it were the TRIOS Dx Plus diagnostic software and DentalHealth app, allowing patients to view scans and oral care advice on their smartphone directly.

- In September 2024, SHINING 3D released the Aoralscan Elite, the world's first intraoral scanner that combines photogrammetry through IPG technology. This innovation improves precision and productivity in full-mouth implant cases, particularly edentulous and All-on-X cases, and represents a significant development in digital dentistry workflows.

Dental 3D Scanners Market Report Scope:

| Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Desktop Or Laboratory 3D Dental Scanners, Intraoral 3D Dental Scanners, Cone Beam Computerized Tomography (CBCT) |

| End Users Covered | Hospitals, Dental Clinics |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, and Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3Shape A/S, AGE Solutions S.r.l., Align Technology, Inc., Amann Girrbach AG, Carestream Dental LLC, Condor Technologies NV, Densys Ltd., Dentsply Sirona Inc., Envista Holdings Corporation, Kulzer GmbH (Mitsui Chemicals Group), Planmeca Oy, Shining 3D Tech Co., Ltd., Straumann Holding AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the dental 3D scanners market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global dental 3D scanners market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the dental 3D scanners industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Dental 3D Scanners Market Report

The dental 3D scanners market was valued at USD 611.0 Million in 2025.

The dental 3D scanners market is projected to exhibit a (CAGR) of 7.64% during 2026-2034, reaching a value of USD 1,208.7 Million by 2034.

Major drivers are the increasing demand for digital dentistry, rising awareness about precise diagnostic equipment, rising dental disorders cases, and growing demand for cosmetic dentistry. Technological innovation and enhanced patient comfort also spur adoption in dental clinics and laboratories globally.

North America currently dominates the dental 3D scanners market, spurred by advanced healthcare infrastructure, early-stage technology adoption, and rising awareness among dental professionals. The region is favored by high incidences of dental ailments, rising cosmetic dental procedures, and strong investments in the integration of digital workflow among dental practices.

Some of the major players in the dental 3D scanners market include 3Shape A/S, AGE Solutions S.r.l., Align Technology, Inc., Amann Girrbach AG, Carestream Dental LLC, Condor Technologies NV, Densys Ltd., Dentsply Sirona Inc., Envista Holdings Corporation, Kulzer GmbH (Mitsui Chemicals Group), Planmeca Oy, Shining 3D Tech Co., Ltd., Straumann Holding AG, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)