DevOps Market Size, Share, Trends and Forecast by Type, Deployment Model, Organization Size, Tools, Industry Vertical, and Region, 2026-2034

DevOps Market Size, Share, Trends & Forecast (2026-2034)

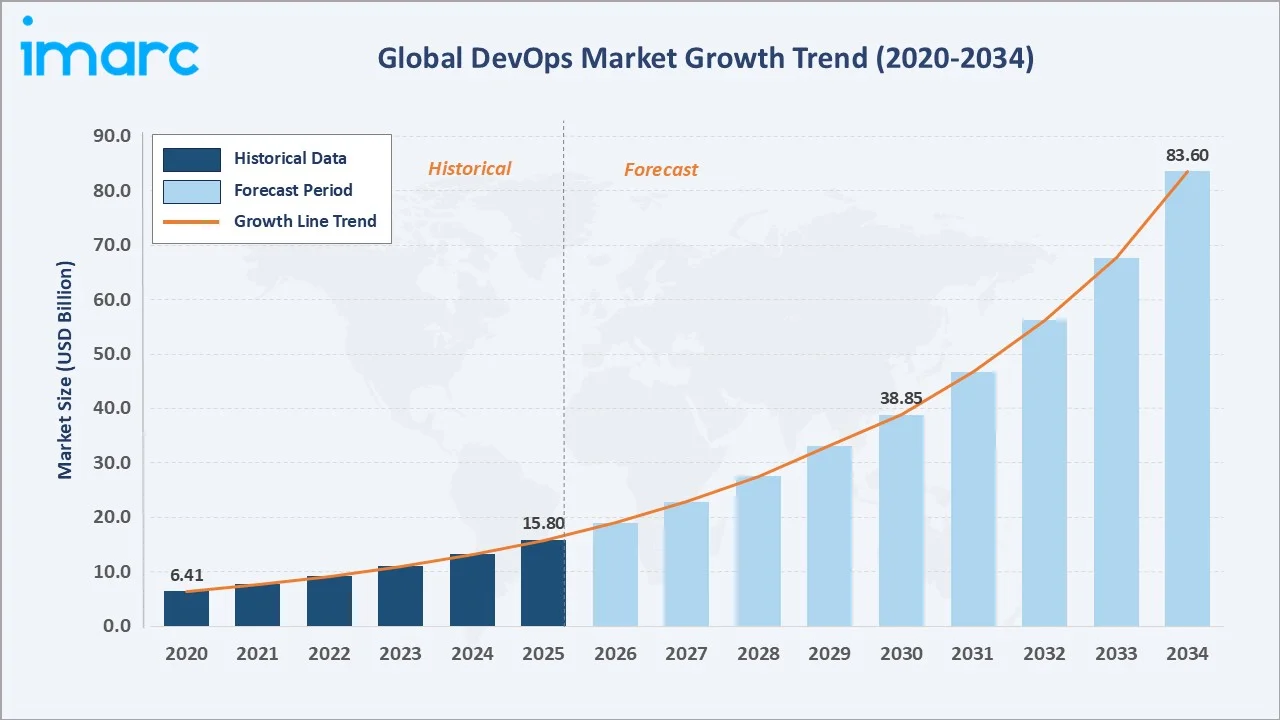

The global DevOps market reached USD 15.80 Billion in 2025 and is projected to reach USD 83.60 Billion by 2034, growing at a CAGR of 19.74% during 2026-2034. Accelerating digital transformation, widespread cloud adoption, and growing enterprise demand for faster, more reliable software delivery are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.80 Billion |

|

Forecast Market Size (2034) |

USD 83.60 Billion |

|

CAGR (2026-2034) |

19.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (43.4% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

To get more information on this market, Request Sample

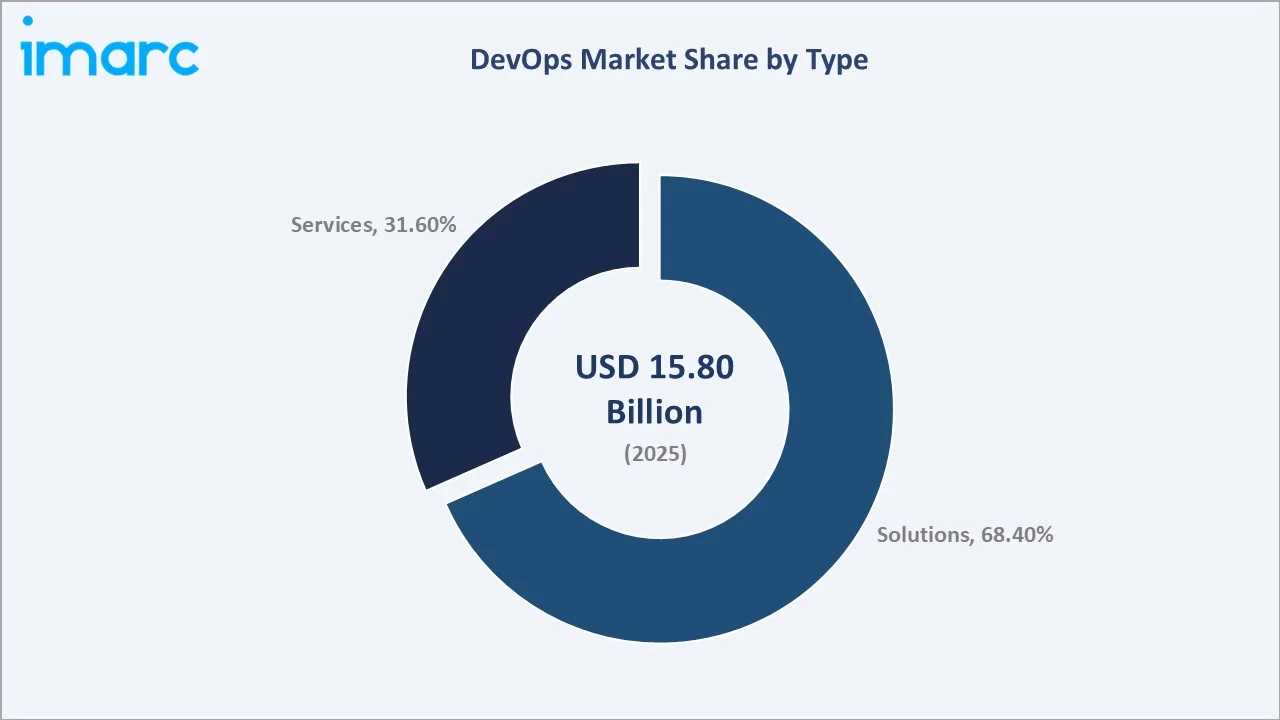

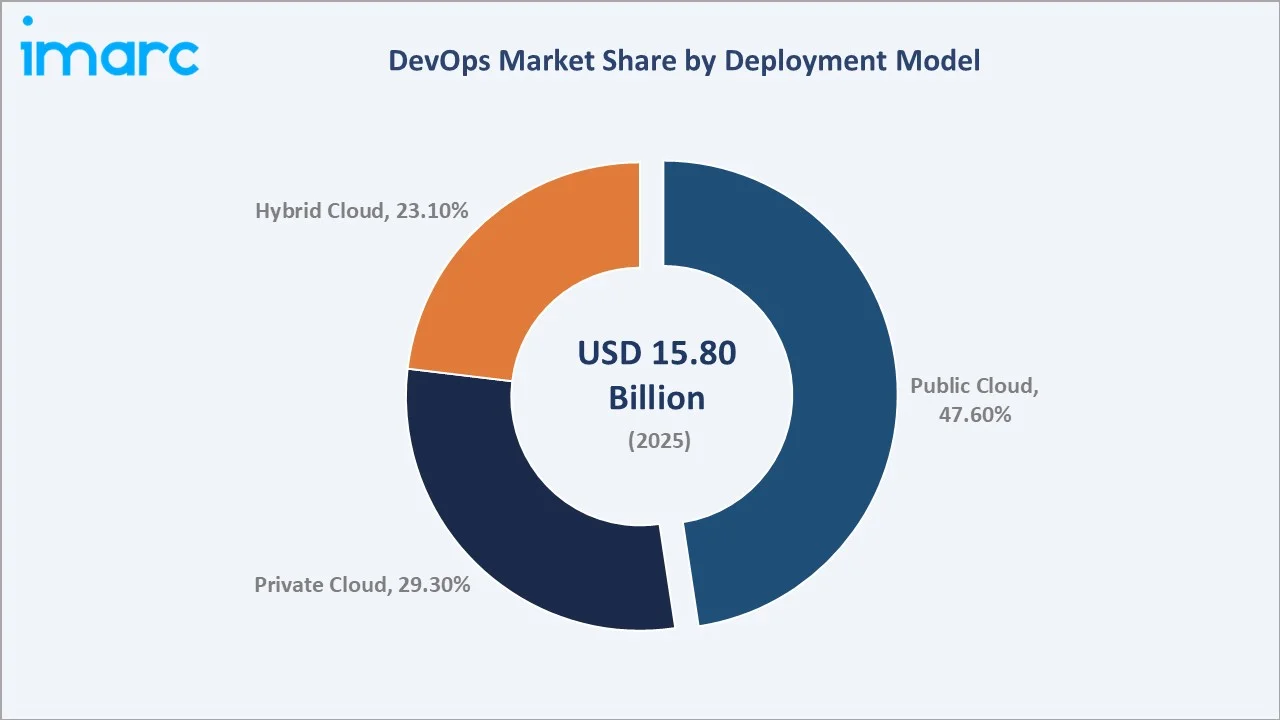

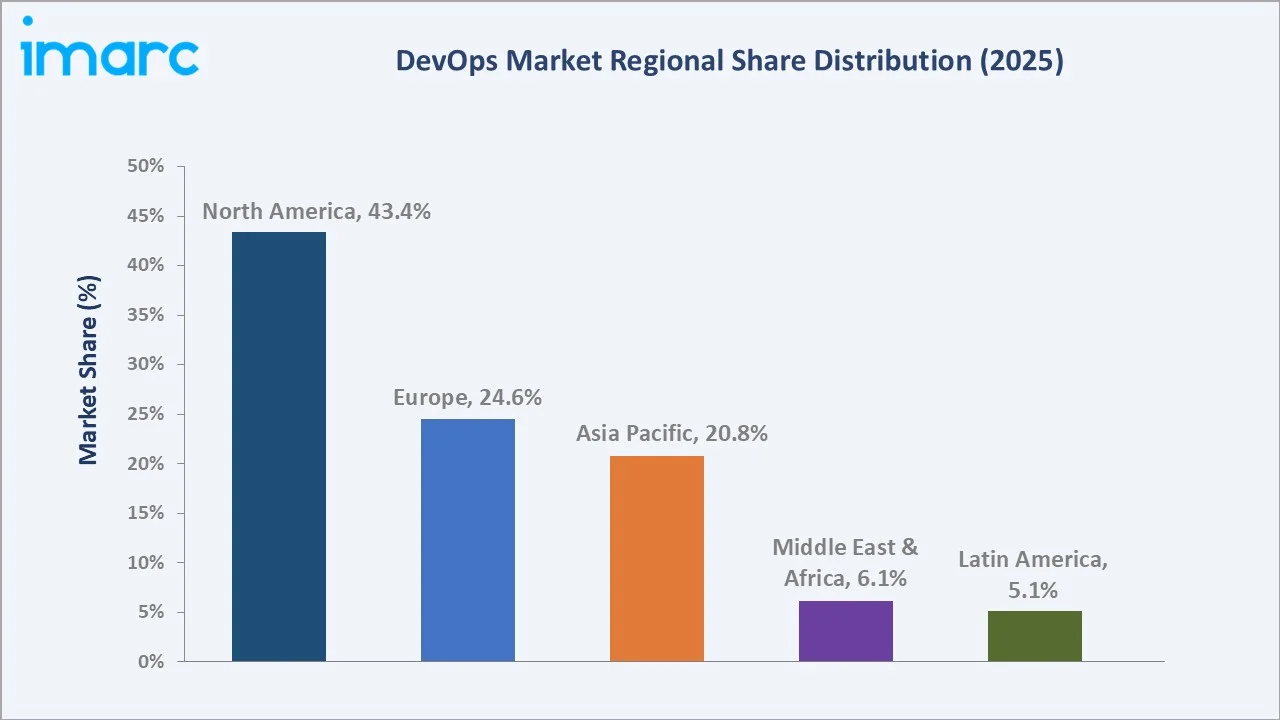

North America dominates, holding a 43.4% market share in 2025, while the solutions type segment leads with 68.4%. Public cloud remains the dominant deployment model with a 47.6% share. DevOps delivers accelerated release cycles, improved collaboration between development and operations teams, and enhanced software quality, making it an indispensable methodology for enterprises navigating the demands of digital-first business environments.

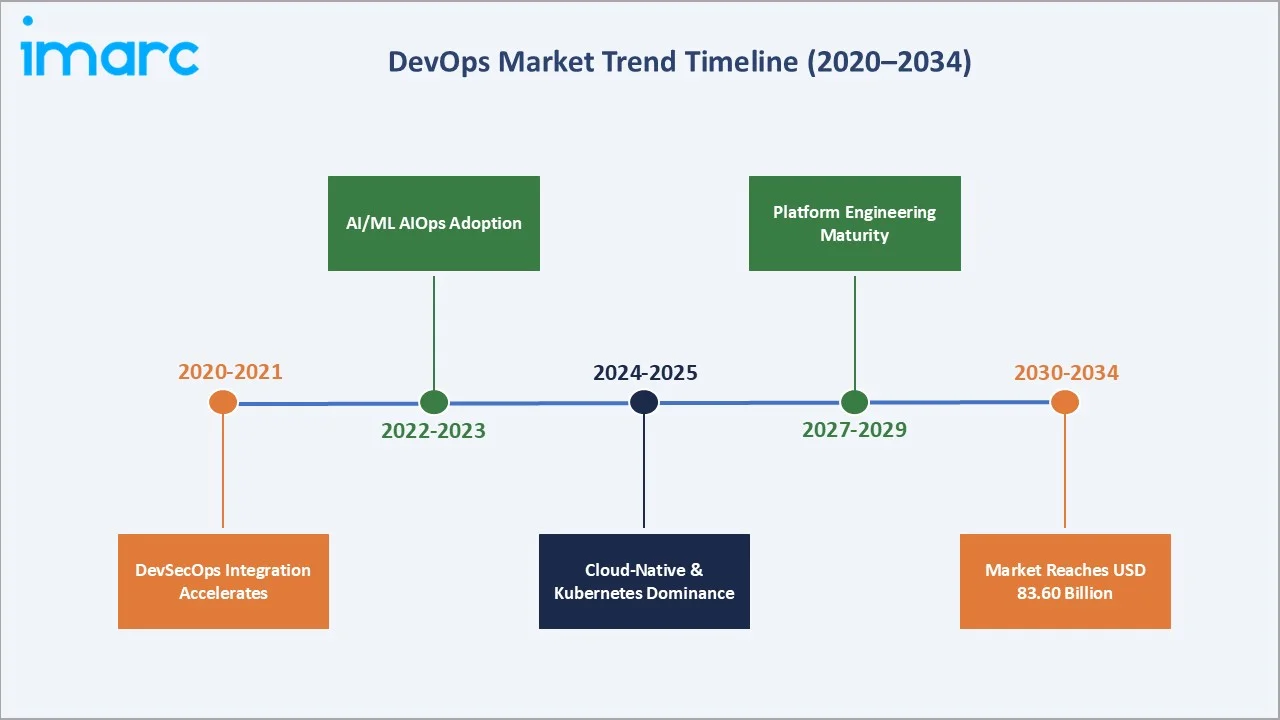

With adoption spanning BFSI, telecommunications, healthcare, retail, and government sectors, the market is expected to continue its high-growth trajectory, supported by advancements in AI-driven automation, DevSecOps integration, and the rapid maturation of cloud-native and containerized application architectures globally.

Executive Summary

The global DevOps market is on a sustained, high-velocity growth path, underpinned by accelerating enterprise digital transformation, the imperative for faster software delivery cycles, and the pervasive adoption of cloud-native architectures. The market reached USD 15.80 Billion in 2025 and is forecast to surpass USD 83.60 Billion by 2034, reflecting a robust CAGR of 19.74% over the forecast period.

North America leads globally with a 43.4% revenue share in 2025, driven by a mature technology ecosystem, high enterprise IT spending, and early adoption of CI/CD practices across cloud-native software development organizations. Asia Pacific, at 20.8%, represents the fastest-growing regional opportunity, with China, India, Japan, and South Korea investing heavily in digital infrastructure and agile software delivery platforms.

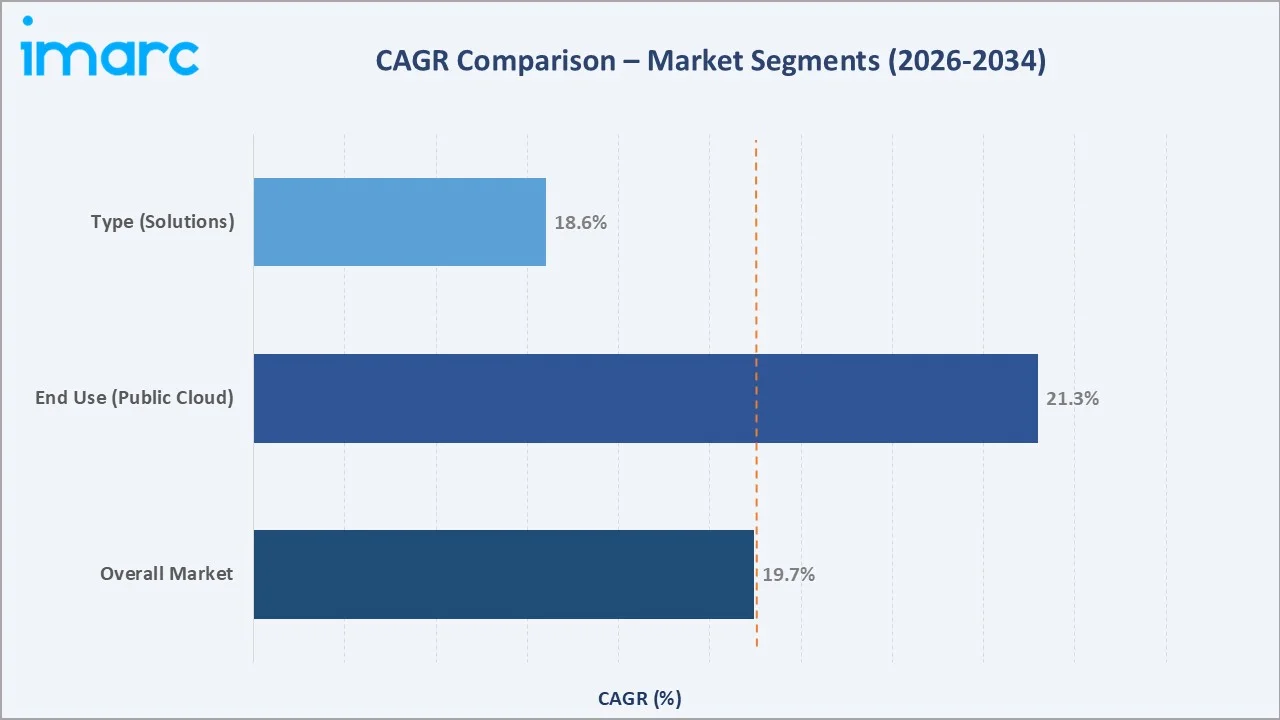

The solutions segment dominates with a 68.4% market share, reflecting enterprise preference for integrated DevOps toolchains over standalone professional services. Public cloud deployments command the largest share at 47.6%, enabled by the scalability and on-demand resource provisioning inherent to cloud platforms. Key players continue to invest in AI-augmented DevOps capabilities, platform engineering solutions, and geographic expansion to capture the expanding global enterprise demand.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Solutions – 68.4% share (2025) |

|

Largest Segment (Deployment Model) |

Public Cloud – 47.6% share (2025) |

|

Leading Region |

North America – 43.4% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (digital transformation + cloud adoption) |

|

Top Companies |

Microsoft Corporation, IBM Corporation, Amazon Web Services, Google LLC, GitLab, Inc. |

|

Market Opportunity |

AI-driven DevOps automation growing at ~26% CAGR through 2034 |

Key analytical observations supporting the above data:

- Solutions type account for 68.4% of the DevOps market in 2025, preferred by enterprises for comprehensive integrated platforms that consolidate CI/CD, monitoring, security scanning, and collaboration tooling into unified, vendor-supported ecosystems.

- Public cloud deployments lead with 47.6% share, driven by the scalability, cost efficiency, and resource agility that cloud environments provide for running containerized, microservices-based DevOps pipelines at enterprise scale.

- North America holds 43.4% of the global market in 2025, led by the U.S., which accounts for over 61% of DevOps tool deployments globally, driven by high IT spending and deep enterprise cloud maturity across BFSI, technology, and healthcare sectors.

- Asia Pacific is the fastest-growing region, with India, China, and Australia accelerating DevOps adoption through digital transformation mandates, government-backed technology initiatives, and a rapidly expanding base of cloud-native startups and enterprises.

- AI integration is becoming a core DevOps differentiator. The 2026 analysis by the Software Testing Journal reveals that teams utilizing AI-powered testing frameworks achieve 83% test coverage, compared to just 54% with traditional methods, while also reducing testing time by 56%.

Global DevOps Market Overview

DevOps is a transformative set of cultural philosophies, practices, and tools that unify software development (Dev) and IT operations (Ops) to shorten the systems development lifecycle and deliver features, fixes, and updates continuously in alignment with business objectives. DevOps has evolved into a comprehensive discipline encompassing continuous integration, continuous delivery, infrastructure as code, automated testing, real-time monitoring, and collaborative culture.

Macroeconomic factors, including the acceleration of enterprise digital transformation, competitive pressure to reduce time-to-market, and increasing software complexity driven by microservices and cloud-native architectures, are primary growth catalysts. DevOps practices enable organizations to deploy software significantly more frequently than traditional approaches, reduce change failure rates, and recover from incidents faster, delivering measurable improvements in both IT performance and business outcomes across industry verticals.

Market Dynamics

To evaluate market opportunities, Request Sample

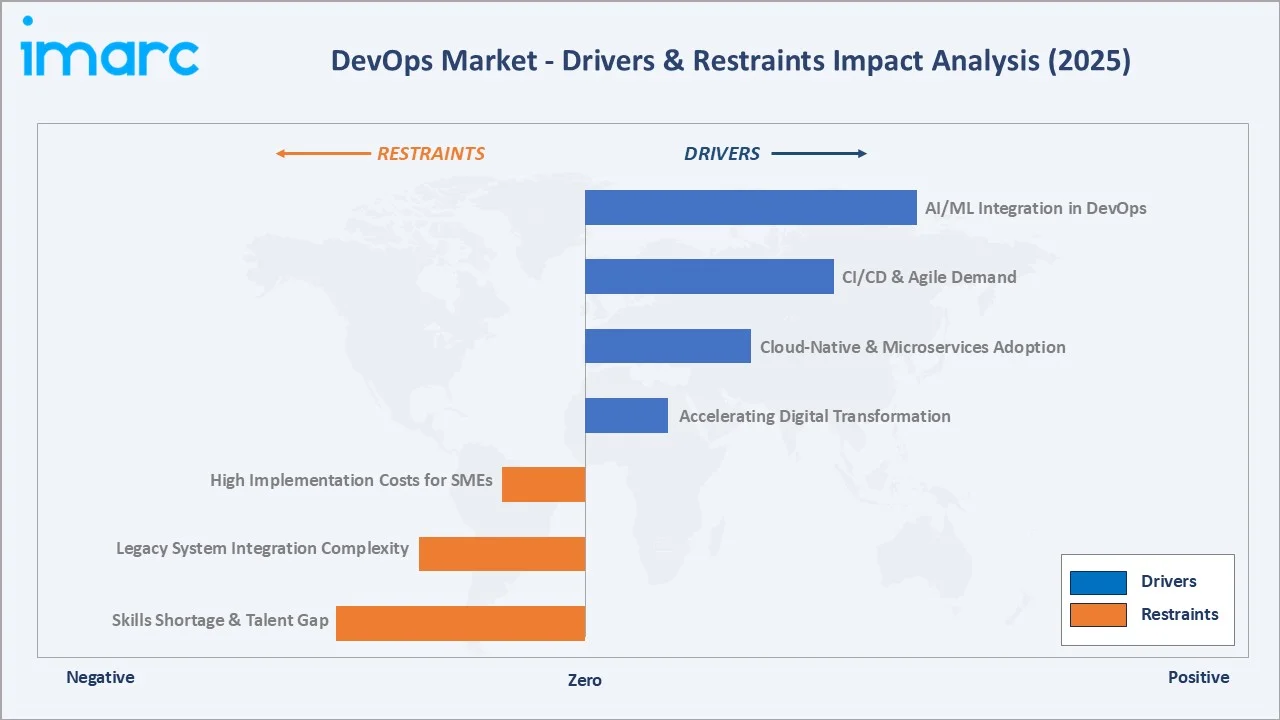

Market Drivers

- Accelerating Enterprise Digital Transformation: Around 80% of organizations worldwide now use DevOps in some form, reflecting the methodology's centrality to digital transformation strategies across BFSI, healthcare, retail, and government sectors seeking agile, resilient software delivery capabilities.

- Cloud-Native Architecture and Microservices Adoption: The widespread shift to containerized, microservices-based applications, with Docker maintaining over 32% of the containerization market, necessitates automated deployment pipelines and continuous delivery practices that are core competencies of the DevOps methodology.

- Demand for Faster, Higher-Quality Software Releases: Organizations implementing DevOps report 49% shorter time-to-market and a 61% improvement in deliverable quality, driving sustained enterprise investment in DevOps platforms, tooling, and upskilling programs to meet competitive software delivery demands.

- AI/ML Integration Transforming DevOps Automation: The global AIOps market reached USD 16.42 Billion in 2025, with AI-powered automation tools reducing DevOps release cycles by up to 67% and enabling predictive incident management, intelligent test case generation, and anomaly detection across CI/CD pipelines.

These drivers reinforce a self-sustaining growth cycle – digital transformation initiatives drive DevOps adoption, which accelerates release velocity, which improves competitive positioning, which mandates further DevOps investment and capability maturation across enterprise IT organizations.

Market Restraints

- Skills Shortage and Talent Gap: Skills shortages remain the most cited challenge for 33% of organizations implementing DevOps, as the demand for engineers proficient in CI/CD, Kubernetes, IaC, and DevSecOps substantially outpaces the available talent pool in most global markets.

- Legacy System Integration Complexity: For 29% of enterprises, legacy architecture presents a major adoption barrier, as integrating traditional monolithic applications and on-premises infrastructure with modern DevOps toolchains requires significant refactoring investment and organizational change management effort.

- High Implementation Costs for SMEs: Comprehensive DevOps platform licensing, infrastructure provisioning, and the professional services required for initial implementation represent a prohibitive upfront investment for small and medium-sized enterprises operating under constrained IT budgets.

Market Opportunities

- DevSecOps Becoming a Mandatory Enterprise Requirement: With cyber threats growing in sophistication, the integration of automated security scanning, vulnerability assessment, and compliance enforcement throughout the DevOps pipeline is becoming a procurement requirement, creating substantial expansion opportunities for security-embedded DevOps platforms.

- Emerging Market Digital Infrastructure Buildout: Southeast Asia, the Middle East, and Latin America are witnessing 40%+ growth in DevOps-focused investment portfolios as governments and enterprises accelerate digital infrastructure development and cloud migration programs, opening significant greenfield market opportunities.

- Platform Engineering as the Next DevOps Evolution: By 2027, Gartner estimates 80% of organizations will incorporate DevOps platforms into their toolchains, with Internal Developer Portals emerging as high-value commercial opportunities for vendors that can standardize developer workflows and accelerate platform adoption.

Market Challenges

- Tool Sprawl and Integration Complexity: The proliferation of DevOps tools across planning, coding, testing, deployment, monitoring, and security categories creates significant integration overhead and vendor management complexity for enterprise IT teams attempting to maintain coherent, end-to-end automated pipelines.

- Cultural Resistance to DevOps Transformation: Organizational change management remains a persistent challenge, as DevOps requires fundamental shifts in team structures, responsibilities, and workflows that frequently encounter resistance from entrenched development and operations organizational cultures.

Emerging Market Trends

1. AI-Augmented DevOps and AIOps Integration

In 2025, AI generates or assists in 41% of all code, highlighting its significant impact on global software workflows, significantly reducing development cycle times without compromising code quality. Automated testing accelerated by AI integration is reducing deployment cycle times by 63% in leading DevOps organizations, representing a fundamental productivity uplift that is driving accelerated enterprise platform adoption across the global technology landscape.

2. DevSecOps Becoming Standard Enterprise Practice

Over 63% of DevOps professionals now use AI as a copilot for secure code writing, reflecting the growing intersection of security automation and AI-augmented development workflows. Regulatory pressure across BFSI, healthcare, and government sectors is accelerating DevSecOps adoption, as organizations face increasing compliance obligations requiring demonstrable security controls throughout the software supply chain.

3. Cloud-Native Architectures and Kubernetes Dominance

Public cloud deployment leads the market with 47.6% share, as organizations leverage cloud-native CI/CD capabilities on AWS, Microsoft Azure, and Google Cloud to achieve elastic scalability and geographic deployment flexibility. GitOps, which applies version control and Git workflows to infrastructure automation, is becoming the industry standard for managing Kubernetes-based infrastructure, providing enhanced security, improved developer experience, and full audit trails for infrastructure changes.

4. Platform Engineering and Internal Developer Portals

By centralizing infrastructure access, CI/CD pipeline templates, and observability tooling within governed self-service platforms, platform engineering significantly reduces developer cognitive load and improves deployment consistency across complex multi-cloud environments. The platform engineering market is attracting substantial venture investment, with Qovery securing USD 13 million in October 2025 to expand its developer experience platform.

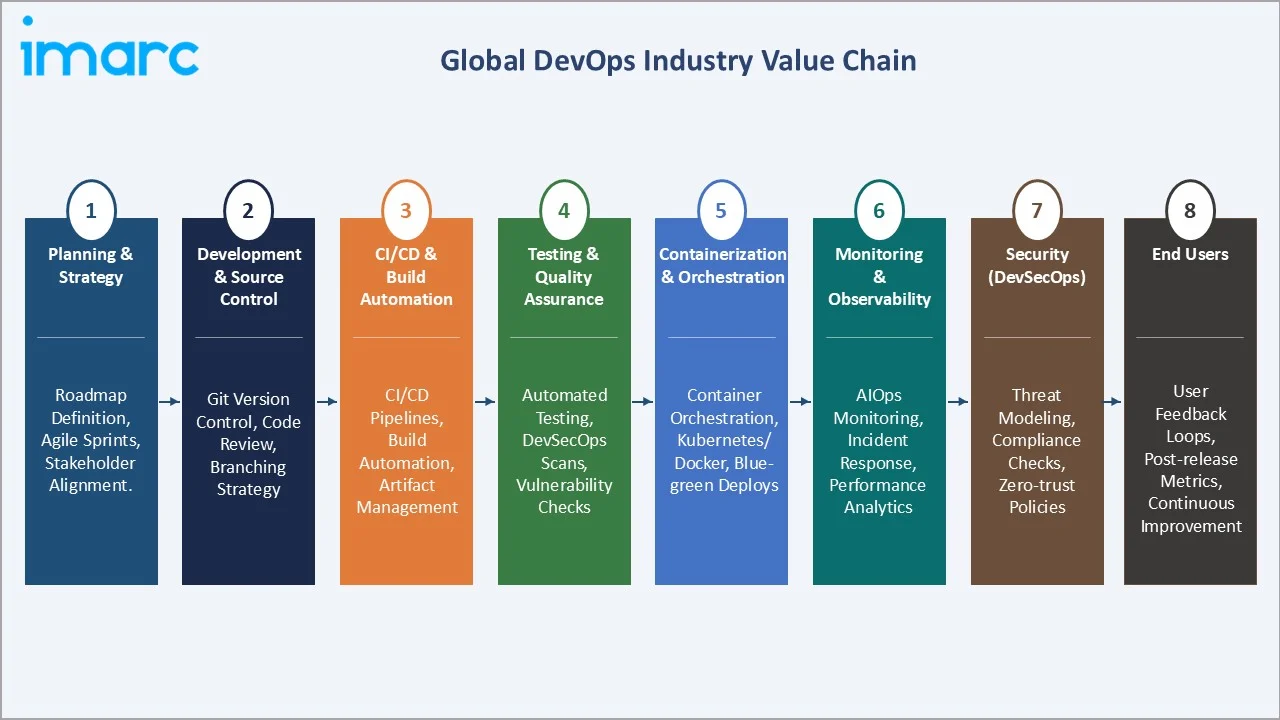

Industry Value Chain Analysis

The DevOps value chain spans strategic planning through continuous feedback, with each stage supported by specialized tooling vendors, platform providers, and professional services organizations whose performance directly influences software delivery speed, quality, and operational reliability.

|

Stage |

Key Players / Technologies |

|

Planning & Strategy |

Atlassian Jira, Azure Boards, GitLab, Rally (Broadcom) |

|

Development & Source Control |

GitHub (Microsoft), GitLab, Bitbucket (Atlassian) |

|

CI/CD & Build Automation |

Jenkins, GitHub Actions, Azure DevOps Pipelines, CircleCI, GitLab CI |

|

Testing & Quality Assurance |

Selenium, TestNG, JUnit, Tricentis Tosca |

|

Containerization & Orchestration |

Docker, Kubernetes, Red Hat OpenShift, AWS EKS, Google Kubernetes Engine (GKE), Microsoft Azure Kubernetes Service (AKS) |

|

Monitoring & Observability |

Datadog, Splunk, New Relic, Dynatrace, IBM Instana |

|

Security (DevSecOps) |

Snyk, Checkmarx, Aqua Security, Prisma Cloud (Palo Alto Networks) |

|

End Users |

BFSI, Telecom/ITES, Healthcare, Retail, Manufacturing, Government |

Technology Landscape in the DevOps Industry

AI-Powered CI/CD Pipeline Optimization

Platforms such as GitHub Copilot for PRs and Harness AI leverage large language models to generate code, summarize pull requests, and predict deployment risk scores before releases reach production. AI-driven predictive analytics analyze historical pipeline data to identify recurring failure patterns, enabling platform teams to proactively address bottlenecks before they impact release schedules.

Infrastructure as Code and GitOps Standardization

Infrastructure as Code tools, including Terraform, Pulumi, and AWS CloudFormation, have become foundational elements of enterprise DevOps practice, enabling version-controlled, reproducible infrastructure provisioning that eliminates configuration drift and supports audit compliance. GitOps extends these principles to runtime infrastructure management by using Git repositories as the single source of truth for desired cluster and application state.

Container Security and Supply Chain Protection

New tooling categories addressing software bill of materials (SBOM) generation, container image signing, and supply chain attestation are experiencing rapid adoption. In April 2025, Aqua Security highlights the launch of the industry’s first free Container Security Risk Assessment, which gives organizations real‑world visibility into runtime container risks, demonstrating the commercial impact of security-embedded DevOps tooling on enterprise risk posture improvement.

Observability and AIOps for Production Intelligence

AIOps capabilities embedded within platforms such as Datadog, Dynatrace, and IBM Instana enable automated anomaly detection, root cause analysis, and intelligent alert correlation that reduces alert fatigue for on-call engineering teams. The global AIOps market, valued at USD 16.42 Billion in 2025, is expected to reach USD 36.6 Billion by 2030, reflecting the scale of enterprise investment in AI-augmented operations intelligence as a core component of mature DevOps organizational capability.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Solutions | 68.4% | 2025 |

| Deployment Model | Public Cloud | 47.6% | 2025 |

| Organization Size | Large Enterprises | 49.4% | 2025 |

| Tools | Development Tools | 45.0% | 2025 |

| Industry Vertical | Telecommunications and Information Technology Enabled Services (ITES) | 35.7% | 2025 |

| Region | North America | 43.4% | 2025 |

By Type

To access detailed market analysis, Request Sample

Solutions dominate the type segment with a 68.4% share in 2025 (equivalent to approximately USD 10.81 Billion). Their dominance reflects enterprise preference for comprehensive integrated DevOps platforms that consolidate CI/CD automation, monitoring, security scanning, collaboration, and analytics capabilities into unified, vendor-supported toolchains that reduce integration complexity and total cost of ownership.

Services account for 31.6% of the market (approximately USD 4.99 Billion in 2025), encompassing consulting, implementation, training, managed DevOps, and support offerings. Professional services are particularly significant in large-scale enterprise DevOps transformation programs, where organizational change management, legacy system integration, and custom toolchain architecture require specialized expertise that supplements vendor-provided platform capabilities.

By Deployment Model

Public cloud deployments lead the market with a 47.6% share in 2025, driven by the scalability, geographic flexibility, and pay-as-you-go economics that cloud environments provide for CI/CD workloads. Major cloud providers, including AWS, Microsoft Azure, and Google Cloud Platform, have deeply integrated DevOps tooling into their native service offerings, creating compelling ecosystems that reduce friction for enterprises pursuing cloud-first DevOps strategies.

Private cloud deployments represent 29.3% of the market (approximately USD 4.63 Billion), favored by regulated industries including BFSI, healthcare, and government, where data sovereignty requirements, compliance mandates, and security policies restrict the use of public cloud infrastructure for sensitive application workloads.

Regional Market Insights

North America’s market leadership (43.4%, 2025) reflects the region’s mature cloud infrastructure, high enterprise IT investment levels, and early adoption of DevOps methodologies across technology, BFSI, and healthcare sectors. The U.S. accounts for over 61% of global DevOps tool deployments, with Azure DevOps maintaining a 13.62% share of the DevOps services market.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

North America |

43.4% |

High enterprise IT spend, cloud hyperscaler HQs, early CI/CD adoption, BFSI & healthcare digitization |

NIST cybersecurity frameworks; FedRAMP for govt DevSecOps; state data privacy laws |

|

Europe |

24.6% |

GDPR compliance driving DevSecOps, digital transformation mandates, strong BFSI and manufacturing sectors |

GDPR, EU Cyber Resilience Act; NIS2 Directive; DORA for BFSI |

|

Asia Pacific |

20.8% |

Digital India, China cloud build-out, Japan DX push, ASEAN startup ecosystem, rising IT services sector |

National cloud-first policies; sector-specific digital mandates; data localization laws |

|

Middle East & Africa |

6.1% |

Government Vision programs (Saudi Vision 2030, UAE Centennial), smart city initiatives, oil & gas digitization |

UAE cloud-first strategy; KSA national data regulations; NEOM digital infrastructure mandates |

|

Latin America |

5.1% |

Brazilian fintech boom, Mexico nearshoring growth, digital banking adoption, and agile software exports |

LGPD (Brazil data law); sector-specific fintech regulations; digital services tax frameworks |

Asia Pacific is the highest-growth region, with India targeting a USD 1 trillion internet economy by 2030, and China's cloud infrastructure buildout accelerating enterprise DevOps adoption across manufacturing, fintech, and government sectors. Southeast Asia's rapidly expanding base of cloud-native startups and technology services exporters further strengthens the region’s long-term DevOps market growth profile through 2034.

Competitive Landscape

The global DevOps market exhibits a moderately fragmented structure, dominated by large cloud and enterprise software conglomerates that offer integrated DevOps platforms alongside a broad ecosystem of specialized tooling vendors. Microsoft Corporation, IBM Corporation, Amazon Web Services, Google, LLC, and Oracle Corporation collectively command substantial market share through deeply integrated cloud-native DevOps offerings that benefit from existing enterprise customer relationships and bundled cloud service economics.

|

Company Name |

Key Platform |

Market Position |

Core Strength |

|

Microsoft Corporation |

Azure DevOps / GitHub |

Market Leader |

End-to-end DevOps ecosystem; GitHub Copilot AI integration; 13.62% DevOps services market share |

|

IBM Corporation |

IBM DevOps Deploy / Turbonomic |

Market Leader |

Enterprise hybrid cloud DevOps; AI-powered AIOps; decades of Fortune 500 IT relationships |

|

Amazon Web Services |

AWS CodePipeline / CodeBuild |

Market Leader |

Dominant cloud platform; 47% of organizations use AWS DevOps; native cloud-native integration |

|

Google LLC |

Google Cloud Build / Cloud Deploy |

Strong Challenger |

Kubernetes originator; GKE leadership; AI/ML-native DevOps capabilities via Vertex AI |

|

GitLab, Inc. |

GitLab DevSecOps Platform |

Strong Challenger |

Comprehensive single-platform DevSecOps; strong open-source community; rapid enterprise growth |

|

Oracle Corporation |

OCI DevOps |

Strong Challenger |

Deep enterprise database integration; OCI DevOps for cloud-native apps; large existing ERP customer base |

|

Cisco Systems |

Cisco AppDynamics/ Splunk |

Challenger |

Full-stack application performance monitoring and observability for DevOps teams |

|

Hewlett Packard Enterprise |

HPE GreenLake for Private Cloud Enterprise / OpsRamp |

Challenger |

Hybrid cloud DevOps for on-premises-heavy enterprises; edge computing integration |

Open-source-driven competitors, including GitLab, Red Hat, Docker, and Puppet, compete through developer-first community adoption strategies and commercial enterprise editions that monetize on top of widely adopted open platforms.

Key Company Profiles

Microsoft Corporation

Microsoft Corporation, headquartered in Redmond, Washington, is the global leader in integrated DevOps platforms through its Azure DevOps suite and GitHub platform, which together serve millions of developers and thousands of enterprise organizations worldwide.

- Product Portfolio: Azure DevOps (Boards, Repos, Pipelines, Test Plans, Artifacts), GitHub Enterprise, GitHub Copilot AI coding assistant, Azure Monitor, and Microsoft Defender for DevOps security integration.

- Recent Developments: Starting April 2025, Azure DevOps halted new registrations for OAuth apps as part of a planned phase-out in favour of more secure authentication mechanisms, and introduced pipeline-free dependency scanning within GitHub Advanced Security.

- Strategic Focus: Deep GitHub Copilot AI integration across the DevOps lifecycle; Azure cloud-native DevOps platform expansion; enterprise security through Microsoft Defender for DevOps; developer experience leadership through GitHub Codespaces.

IBM Corporation

IBM Corporation, headquartered in Armonk, New York, offers a comprehensive DevOps and hybrid cloud automation portfolio under its IBM DevOps brand, including IBM DevOps Deploy (formerly UrbanCode Deploy), IBM Turbonomic for AIOps-driven resource optimization, and IBM Instana for full-stack observability across containerized and traditional enterprise application environments.

- Product Portfolio: IBM DevOps Deploy, IBM DevOps Velocity, IBM Turbonomic Application Resource Management, IBM Instana Observability, and IBM AIOps Insights for intelligent IT operations automation.

- Recent Developments: IBM DevOps Deploy 2023.12 (version 8.0.0) introduced a unified DevOps Automation platform, rebranding from UrbanCode Deploy and significantly enhancing automation capabilities for enterprise application release orchestration across hybrid environments.

- Strategic Focus: Hybrid cloud DevOps for regulated industries; AI-augmented IT operations through IBM AIOps Insights; mainframe modernization DevOps integration; consulting-led enterprise DevOps transformation programs globally.

Amazon Web Services

Amazon Web Services (AWS), headquartered in Seattle, Washington, is the world’s largest cloud computing provider and a dominant force in cloud-native DevOps tooling, with around 47% of organizations globally leveraging AWS DevOps services. AWS provides an end-to-end suite of natively integrated DevOps tools covering source control, build automation, deployment orchestration, container management, and monitoring, all deeply integrated with its hyperscale cloud infrastructure platform.

- Product Portfolio: AWS CodePipeline, CodeBuild, CodeDeploy, Amazon EKS (Kubernetes), Amazon ECS, AWS Lambda (serverless), Amazon CloudWatch, AWS X-Ray, and AWS Systems Manager for DevOps automation.

- Recent Developments: AWS has been progressively expanding Amazon Q Developer, its AI-powered code generation and DevOps automation tool, with capabilities spanning code transformation, security vulnerability detection, and automated documentation generation for enterprise development teams.

- Strategic Focus: AI-native DevOps through Amazon Q; serverless and container-first deployment architectures; global infrastructure expansion; enterprise migration programs to AWS cloud-native DevOps pipelines.

GitLab, Inc.

GitLab, Inc., headquartered in San Francisco, California, provides a comprehensive single-platform DevSecOps solution that covers the entire software development lifecycle from planning and source control through CI/CD, security scanning, and observability. GitLab’s all-in-one approach reduces the integration complexity of multi-tool DevOps environments and is particularly well-suited to organizations seeking to consolidate fragmented toolchains into a unified, governed platform.

- Product Portfolio: GitLab DevSecOps Platform (Community and Enterprise Editions), GitLab CI/CD, GitLab Security (SAST, DAST, dependency scanning), GitLab Duo AI features, and GitLab Observability with distributed tracing.

- Recent Developments: GitLab has been rapidly expanding its GitLab Duo AI capabilities across code generation, automated code review, vulnerability explanation, and pipeline configuration assistance, positioning itself as an AI-first DevSecOps platform for enterprise customers.

- Strategic Focus: Single-platform DevSecOps consolidation; GitLab Duo AI differentiation; enterprise customer expansion from community base; public sector and regulated industry penetration through FedRAMP-authorized offerings.

Market Concentration Analysis

The DevOps market exhibits moderate-to-high concentration at the platform level, with Microsoft, AWS, IBM, Google, and GitLab collectively commanding approximately 45–50% of total platform revenue in 2025. However, a significant long tail of specialized tooling vendors spanning monitoring, security, testing, container management, and collaboration functions ensures substantial overall market fragmentation, with open-source tools dominating 68% of the tooling market by deployment volume.

Consolidation activity remains elevated, driven by platform vendors seeking to close capability gaps and expand their total addressable market within existing enterprise customer relationships. Private equity interest in mid-tier DevOps platform operators has surged, with merger and acquisition activity accelerating across the container security, observability, and developer experience platform categories.

Investment & Growth Opportunities

Fastest Growing Segments

AI-augmented DevOps automation (estimated CAGR 26%), DevSecOps platform consolidation (approximately 24% CAGR), and Platform Engineering / Internal Developer Portal solutions represent the three highest-growth investment vectors through 2034. Together, these categories address a combined total addressable market exceeding USD 15 Billion in incremental annual revenue by 2030, representing a substantial opportunity for both strategic platform vendors and financial investors targeting software delivery infrastructure.

Emerging Market Expansion

Southeast Asia, Latin America, and the Middle East collectively represent significant DevOps greenfield opportunities through 2034. Preferred entry strategies include cloud-native SaaS platform launches in major technology hubs, partnerships with local system integrators and cloud resellers, alignment with government digital transformation procurement programs, and open-source community development that builds developer adoption ahead of commercial monetization.

Venture and Institutional Investment Trends

- Key investment themes include AI-native CI/CD pipeline optimization, developer experience platforms that improve engineering productivity, supply chain security and SBOM tooling, and multi-cloud DevOps governance frameworks that address regulatory compliance across hybrid enterprise environments.

- Family offices and private equity firms are increasingly targeting platform consolidation plays – aggregating CI/CD, monitoring, security, and collaboration tooling into integrated platform companies that can serve enterprise customers with a reduced vendor footprint and simplified procurement experience.

Future Market Outlook (2026-2034)

The global DevOps market is positioned for sustained, broad-based high growth through 2034. From a base of USD 15.80 Billion in 2025, the market is projected to reach USD 83.60 Billion by 2034, representing total incremental value creation of approximately USD 67.80 Billion over the forecast decade at a CAGR of 19.74%.

The regulatory environment, particularly the EU Cyber Resilience Act, US Executive Order 14028 on software supply chain security, and sector-specific digital compliance mandates in BFSI and healthcare, will drive significant DevSecOps platform investment through 2028. Platform vendors that achieve comprehensive security-embedded DevOps capabilities by 2026 are positioned to capture disproportionate enterprise budget share as organizations consolidate fragmented DevOps toolchains onto fewer, more capable integrated platforms.

Long-term, the market trajectory is anchored to three structural macro-themes: the continued acceleration of software-driven business model transformation across every industry vertical, the regulatory imperative for demonstrable software security and supply chain integrity, and the AI-driven productivity revolution that is making DevOps automation accessible to organizations of all sizes.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 130 industry participants in 2024–2025, including DevOps platform executives, enterprise IT decision-makers, software engineering leaders, DevSecOps practitioners, and technology investors across North America, Europe, and Asia Pacific. Key informants provided granular insights into toolchain procurement decisions, DevOps maturity assessment frameworks, and platform evaluation criteria across industry verticals.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, product release documentation, regulatory filings, industry databases (Gartner, IDC, Forrester), trade publications (DevOps.com, InfoQ, The New Stack), open-source foundation reports (CNCF Annual Survey, DORA State of DevOps Report), and publicly available financial data from major DevOps platform vendors and investors. Over 260 secondary sources were reviewed and triangulated to ensure comprehensive coverage and data accuracy.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, enterprise IT spending trajectories, cloud adoption rates, developer headcount growth, and historical DevOps platform revenue data. A base-case CAGR of 19.74% reflects consensus analyst estimates validated against reported vendor revenue growth rates and enterprise IT budget allocation trends across the forecast period 2026–2034.

DevOps Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Solutions, Services |

| Deployment Models Covered | Public Cloud, Private Cloud, Hybrid Cloud |

| Organization Sizes Covered | Large Enterprises, Medium-Sized Enterprises, Small-Sized Enterprises |

| Tools Covered | Development Tools, Testing Tools, Operation Tools |

| Industrial Verticals Covered | Telecommunications and Information Technology Enabled Services (ITES), Banking, Financial Services, and Insurance (BFSI), Retail, Manufacturing, Healthcare, Government and Public Sector, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Microsoft Corporation, IBM Corporation, Amazon Web Services, Google LLC, GitLab, Inc., Oracle Corporation, Cisco Systems, Hewlett Packard Enterprise, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the DevOps market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global DevOps market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the DevOps industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the DevOps Market Report

The global DevOps market reached USD 15.80 Billion in 2025. It is projected to reach USD 83.60 Billion by 2034, growing at a CAGR of 19.74% over the forecast period 2026-2034.

The DevOps market is expected to grow at a CAGR of 19.74% during the forecast period from 2026 to 2034, supported by accelerating enterprise digital transformation, cloud-native adoption, and the growing integration of AI/ML automation across CI/CD pipelines and IT operations.

North America leads the market with a 43.4% revenue share in 2025, driven by high enterprise IT spending, early DevOps adoption across BFSI, technology, and healthcare sectors, and the headquarters concentration of leading DevOps platform providers, including Microsoft, AWS, Google, and GitLab.

Solutions dominate the type segment with a 68.4% share in 2025, valued at approximately USD 10.81 Billion. Their dominance reflects enterprise preference for integrated platforms that consolidate CI/CD, monitoring, security, and collaboration capabilities, reducing toolchain complexity and total cost of ownership.

The public cloud deployment model holds the largest share at 47.6% in 2025 (approximately USD 7.52 Billion), driven by scalability, geographic flexibility, and the deep native DevOps tooling integration offered by leading cloud providers, including AWS, Microsoft Azure, and Google Cloud Platform.

Key players include Microsoft Corporation, IBM Corporation, Amazon Web Services, Google LLC, GitLab, Inc., Oracle Corporation, Cisco Systems, and Hewlett Packard Enterprise.

AI integration is fundamentally transforming DevOps by automating code generation, test case creation, vulnerability detection, and incident management. AI-powered tools are reducing DevOps release cycles by up to 67%, with coding assistants automating approximately 40% of routine development tasks, significantly accelerating software delivery velocity and reducing engineering resource requirements.

Key challenges include skills shortages (cited by 33% of organizations as the top barrier), legacy system integration complexity (blocking 29% of enterprises), high implementation costs for SMEs, tool sprawl and integration overhead, and organizational cultural resistance to the cross-functional collaboration that effective DevOps transformation requires.

Significant opportunities include AI-augmented DevOps automation platforms, DevSecOps security tooling, platform engineering and Internal Developer Portal solutions, emerging market expansion in Asia Pacific and Latin America, and multi-cloud DevOps governance frameworks, with the overall market projected to reach USD 83.60 Billion by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)