Diabetes Care Devices Market Report by Type (Blood Glucose Monitoring (BGM) Devices, Insulin Delivery Devices), Distribution Channel (Retail, Institutional), End User (Hospitals, Homecare, Diagnostic Centres, Ambulatory Surgery Centres), Region and Competitive Landscape (Market Share, Business Overview, Products Offered, Business Strategies, SWOT Analysis and Major News and Events) 2026-2034

Diabetes Care Devices Market Size:

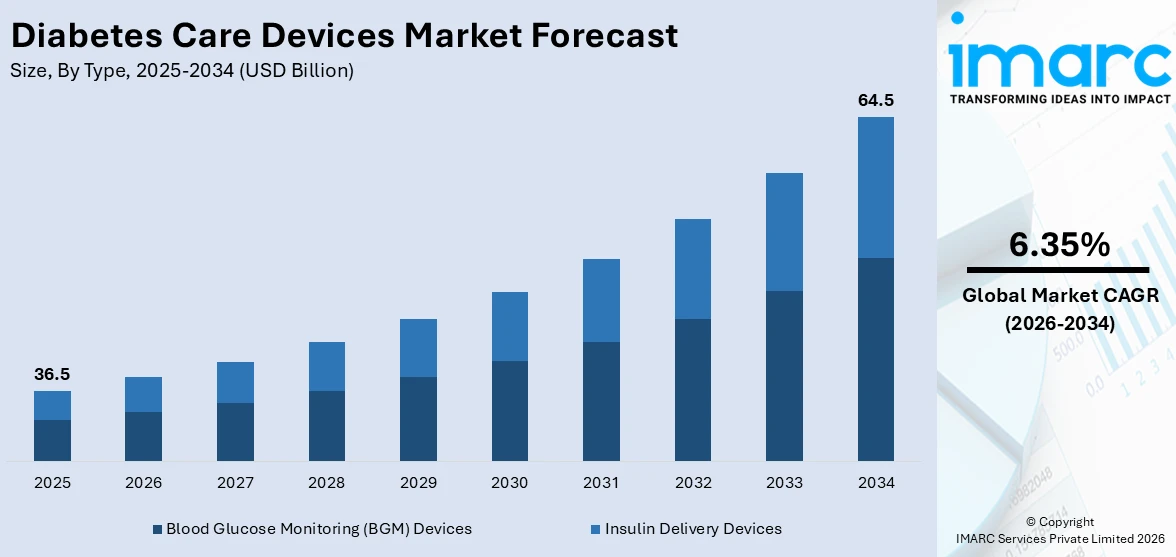

Diabetes care devices market size reached USD 36.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 64.5 Billion by 2034, exhibiting a growth rate (CAGR) of 6.35% during 2026-2034. The implementation of favorable government initiatives, the rising importance of regular monitoring and adherence to treatment regimens, the growing number of consumer-centric healthcare policies, and increasing disposable income levels of the masses are driving the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 36.5 Billion |

| Market Forecast in 2034 | USD 64.5 Billion |

| Market Growth Rate (2026-2034) | 6.35% |

Diabetes Care Devices Market Analysis:

- Major Market Drivers: Government initiatives and healthcare policies are major factors driving the market.

- Key Trends: The considerable growth in home healthcare services and the rise of digital health platforms and mobile health apps are key trends.

- Geographical Trends: North America is dominating the market due to high consumer purchasing power and availability of advanced medical facilities.

- Competitive Landscape: Some of the market players are Abbott Laboratories, ACON Laboratories Inc., Bionime Corporation, etc.

- Challenges and Opportunities: The high cost of diabetes care devices is a challenge and continual advancements in wearable sensors represents a lucrative opportunity for the market.

To get more information on this market Request Sample

Diabetes Care Devices Market Drivers:

Rising Prevalence of Diabetes

The increasing diabetic population is a significant factor that is driving the market. The need for diabetic care technologies, such as insulin pumps, is also high. The market players and patients are looking for devices to help monitor blood glucose levels and manage diabetes. As a result, companies are under pressure to create and provide solutions to satisfy the expanding market and adapt to the changing needs of diabetic patients. In 2021, Medtronic launched the Medtronic Extended infusion. This advancement doubles the time an infusion set can be worn. It allows users to safely continue on insulin pump therapy with fewer interruptions and insertions while adding feasibility and comfort to their diabetes management routine.

Growing Adoption of Self-Monitoring Devices

Nowadays, individuals are becoming more concerned about managing their health. Due to this, there is an increasing demand for devices to monitor and manage diabetes. The key players are introducing these devices to meet the increasing patient demand. In March 2022, Abbott introduced FreeStyle Libre 3, a device that switched from isCGM to rtCGM. It received FDA approval in May 2022. Wearable devices are bringing about a shift, as more companies adopt the technology. Hospitals and patients are counting on digitally based diabetes management systems and virtual care. The need for self-monitoring devices is further fueled by the increased incidence of diabetes worldwide, as medical professionals stress the value of routine monitoring and proactive treatment to avert complications and enhance patient quality of life. The WHO estimated that around 422 million people have diabetes across the globe.

Increasing Awareness and Education

A vital characteristic of the diabetes care devices market is the increased consciousness as well as education with respect to diabetes. Informed public about dangers and ways of managing diabetes persuades a higher number of patients for early diagnosis. The role played by healthcare professionals, patient advocacy groups, and government organizations in enlightening on how to avoid diabetes, its symptoms, and the treatment options provided cannot be underestimated. This situation leads to high demand in the market since people become more cautious about their blood sugar levels. Moreover, regular monitoring or adherence to treatment regimens becomes a known factor. Furthermore, enhanced training on the significance of using diabetes care devices results in better patient compliance and improved health outcomes. As such, manufacturers are compelled to keep researching new systems so that they can have user-friendly devices that are also accurate and technologically advanced hence meeting the ever-increasing need for them. In January, Medtronic received a CE mark for its MiniMed 780G automated insulin delivery system with the Simplera Sync sensor. Simplera Sync, a disposable continuous glucose monitor (CGM), eliminates the need for fingersticks and overtape.

Diabetes Care Devices Market Opportunities:

Continued Innovation in Diabetes Care Devices

The market is driven by continued innovations in diabetes care devices. The changing technology landscape has seen manufacturers continually come up with new and better machines to meet the ever-changing requirements of diabetic patients. The use of advanced features has improved the usability, accuracy, and convenience for users. Furthermore, the convergence of Artificial Intelligence (AI) and Machine Learning algorithms within diabetes care devices has the potential for customizable treatment approaches as well as predictive analytics thereby leading to healthcare providers being able to offer specific interventions that will be suitable for a particular patient thus preventing complications. The World Health Organization estimates that there are over 25 million people at risk of diabetes and 77 million adults over the age of 18 who have Type 2 diabetes, making the need for innovative solutions even more pressing.

Increasing Awareness of Diabetes in Emerging Markets

Individuals growing knowledge of diabetes is driving significant growth in the market for diabetic care devices. Diabetes is becoming a bigger issue as a result of lifestyle changes. However, NGOs and the healthcare sector, are consistently striving to increase awareness among individuals through community development programs and educational initiatives. Moreover, the Indian state government and the UTs have requested the central government to provide economic help under the National Programme for Prevention and Control of Non-Communicable Diseases. It focuses on investing in the infrastructure, educational awareness, and detecting, controlling, and preventing the disease. The market for diabetic care devices is on the rise and it provides various products like glucose monitor devices, glucose meters, etc. With a rapid expansion, manufacturers are investing more in marketing and educational campaigns to increase awareness in society.

Key Technological Trends & Development:

Continuous Glucose Monitoring (CGM) Technology

The ever-changing world of blood sugar measurement has been transformed by CGM technology with its novel abilities, thus, making the diabetes care devices market develop further. Unlike conventional glucose monitoring techniques, CGM provides real-time glucose level data, enabling timely adaptations in therapy schedules. In addition, it is a way more convenient and accurate method as it eliminates the need for frequent finger pricks that enhance the compliance of patients. Besides this, CGM systems help healthcare providers to understand different trends in glucose levels among patients which in turn facilitates customization of management plans. Thus, the increasing number of people with diabetes around the globe has led to an increased call for advanced monitoring options thereby promoting the growth of the market even further. As patients and healthcare providers find improvements in performance, cost-effectiveness, and user-friendliness within continuous glucose monitoring (CGM) technology, they are increasingly attracted toward them leading to a significant expansion in the market.

Emerging Technologies like AI and Machine Learning

The market has been driven by AI and machine learning technologies. Newer glucose monitoring devices have AI and ML algorithms that can analyze large amounts of data to make accurate predictions on sugar levels as well as provide recommendations for personalized treatment. They make it possible for healthcare providers to make data-based decisions leading to better patient outcomes and improved management of complications associated with diabetes mellitus. As the researchers continue to explore AI/ML, we should anticipate more innovative products in the field of diabetes care equipment that will stimulate market growth further, ensuring it revolutionizes diabetic management techniques. These innovations promote precision, active service delivery, and patient-focused approaches in diabetes care.

Remote Patient Monitoring (RPM) Technology

The introduction of remote patient monitoring technology is also driving the market. Those with diabetes can now perform real-time monitoring of their glucose and other vital parameters without leaving their houses. Such RPM gadgets as connected glucometers and wearable sensors transmit data in real-time to medical professionals, thus engendering a need to regularly adjust treatment plans or reduce in-person visits. This improves patient convenience, involvement, and adherence to therapy regimens for better health outcomes. In addition, RPM technology enables the remote monitoring of many patients by health workers which increases efficiency in resource allocation and reduces healthcare costs. With the rise in demand for remote care due to factors like the COVID-19 pandemic and the increased prevalence of diabetes, RPM technology will be largely responsible for significant growth within the diabetes care devices market soon enough.

Diabetes Care Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034 Our report has categorized the market based on type, distribution channel, and end user.

Breakup by Type:

- Blood Glucose Monitoring (BGM) Devices

- Insulin Delivery Devices

Blood glucose monitoring (BGM) devices account for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the type. This includes blood glucose monitoring (BGM) devices and insulin delivery devices. According to the report, blood glucose monitoring (BGM) devices represented the largest segment.

The demand for blood glucose monitoring (BGM) devices is being driven by the increasing occurrence of diabetes across the world. The practice of effective diabetes management requires regular blood glucose checks, therefore in keeping with that BGM devices enable patients to engage with their conditions and make well-informed choices on the matter of diet, medicine, and lifestyle. In addition, advancement in technology has seen improvements in BGM devices leading to more accurate methods of tracking blood sugar among others such as wearable sensors and continuous glucose monitors (CGMs) which have enhanced accuracy, convenience, and usability hence expanding the market further. Furthermore, diabetic patients and healthcare providers have been made aware of taking proactive steps toward managing the disease through early diagnosis which has led to a rise in the number of patients using BGMs. Consequently, there are various companies investing heavily in research development to enhance their products.

Breakup by Distribution Channel:

Access the comprehensive market breakdown Request Sample

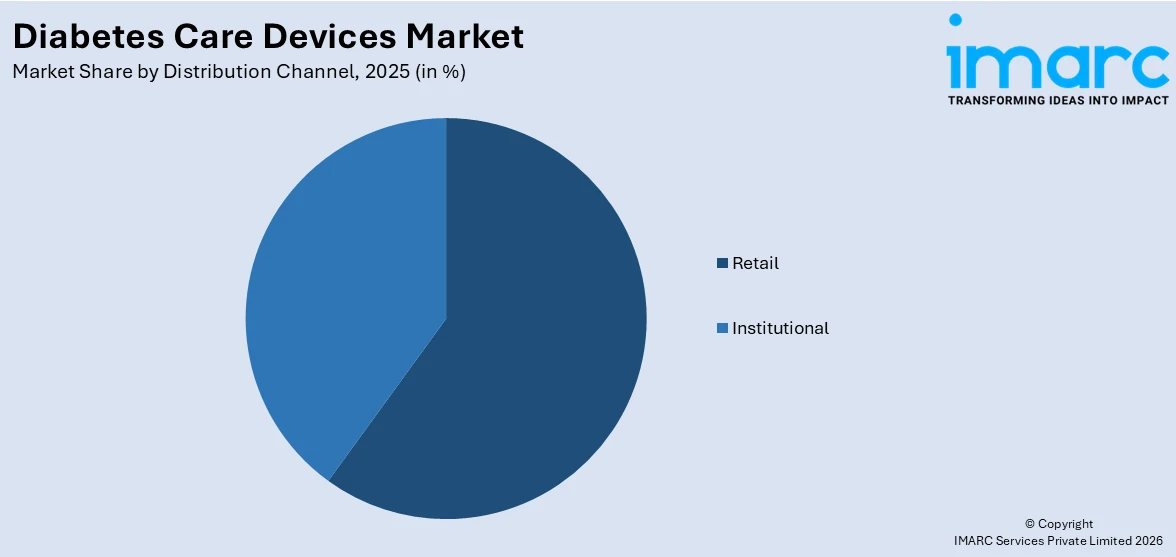

- Retail

- Institutional

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes retail and institutional.

Breakup by End User:

- Hospitals

- Homecare

- Diagnostic Centres

- Ambulatory Surgery Centres

Hospitals hold the largest share in the industry

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes hospitals, homecare, diagnostic centres, and ambulatory surgery centres. According to the report, hospitals accounted for the largest market share.

The diabetes care devices market has several ways of being driven by hospitals. They are the major healthcare providers for diabetes patients using these tools to diagnose, cure, and keep monitoring. Hospitals act as places where diabetes management and education programs are held so that people can be taught how to use and blend them in their treatment plans. They update their medical equipment including diabetes care devices regularly to ensure that they provide patients with quality services. Also, hospitals influence market trends through their buying decisions whereby they buy diabetes care devices in large quantities leading to market growth.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

North America leads the market, accounting for the largest diabetes care devices market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); the Middle East; and Africa. According to the report, North America accounted for the largest market share.

38.4 million people in America had diabetes in 2021. Out of which, 2 million had type 1 diabetes, including about 304,000 children and adults. This increasing prevalence across the region is driving the market. The region has many people suffering from diabetes, and this necessitates complexity and novelty in assisting diabetes patients. In addition, North America is blessed with well-developed hospitals equipped with good medical facilities as well as a strong regulatory framework that favors new trends in diabetes care. Finally, the presence of leading healthcare and tech firms and high spending on research promote this leadership in the sector. This is further boosted by a large amount of money spent on health care in the region as well as positive reimbursement policies for medical equipment. Furthermore, awareness about managing it as well as preventive initiatives towards diabetics increase the use of these objects there too.

Leading Key Players in the Diabetes Care Devices Industry:

A number of market drivers are responsible for enhancing the performance of major players in the diabetes care devices market. They undertake extensive research and development that encourages innovation and upgrading of existing products through the introduction of such advanced technologies as continuous glucose monitoring systems, insulin pumps, smart insulin pens, etc. There is a focus on the expansion of product portfolios through strategic acquisitions, collaborations, and partnerships with other healthcare organizations/technology firms. They have a top-priority strategy in relation to expanding markets by targeting those countries that experience high prevalence rates of diabetes mellitus alongside increasing healthcare expenditure. In addition to this point, these companies have marketing strategies as well as educational programs designed to make people aware of managing diabetes and using their products. These firms endeavor to provide user-friendly equipment as well as comprehensive customer care services while at the same time coming up with digital health platforms for remote monitoring and data management-related activities.

The market research report has provided a comprehensive analysis of the competitive landscape covering market structure, market share by key players, market player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, among others. Detailed profiles of all major companies have also been provided. This includes business overview, product offerings, business strategies, SWOT analysis, financials, and major news and events. Some of the key players in the market include:(PHC Holdings Corporation)

- Abbott Laboratories

- ACON Laboratories Inc.

- Ascensia Diabetes Care Holdings AG

- Becton Dickinson and Company

- Bionime Corporation

- Dexcom Inc.

- F. Hoffmann-La Roche AG

- Johnson & Johnson

- Medtronic plc

- Novo Nordisk A/S

- Sinocare Inc.

- Terumo Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Analysis Covered for Each Player:

- Market Share

- Business Overview

- Products Offered

- Business Strategies

- SWOT Analysis

- Major News and Events

Latest News:

- March 25, 2024: Abbott Laboratories, a global medical device company, announced that it has received CE Mark in Europe for its Assert-IQ insertable cardiac monitor (ICM). Assert-IQ ICM is a new addition to Abbott's growing portfolio of connected health devices. It can detect even hard-to-spot irregularities with heartbeats and help physicians determine the best treatment course.

- November 9, 2023: ACON Laboratories Inc., a global diagnostic and medical device company, received 510(k) marketing clearance for the Flowflex COVID-19 Antigen Home Test. The 510(k) version of the Flowflex COVID-19 Antigen Home Test will also be produced domestically, in ACON Laboratories’ new 97,000 square foot San Diego manufacturing facility.

- October 9, 2023: Ascensia Diabetes Care Holdings AG collaborated with Senseonics Holdings, Inc., a medical technology company, to launch a new U.S. advertising and marketing campaign for Eversense E3 CGM System. ‘The CGM for Real Life’ campaign is designed to significantly drive awareness of Eversense E3 as a unique CGM option that is ideally suited to supporting the everyday lives of people with diabetes.

Diabetes Care Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Blood Glucose Monitoring (BGM) Devices, Insulin Delivery Devices |

| Distribution Channels Covered | Retail, Institutional |

| End Users Covered | Hospitals, Homecare, Diagnostic Centres, Ambulatory Surgery Centres |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, ACON Laboratories Inc., Ascensia Diabetes Care Holdings AG (PHC Holdings Corporation), Becton Dickinson and Company, Bionime Corporation, Dexcom Inc., F. Hoffmann-La Roche AG, Johnson & Johnson, Medtronic plc, Novo Nordisk A/S, Sinocare Inc., Terumo Corporation. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global diabetes care devices market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global diabetes care devices market?

- What is the impact of each driver, restraint, and opportunity on the global diabetes care devices market?

- What are the key regional markets?

- Which countries represent the most attractive diabetes care devices market?

- What is the breakup of the market based on the type?

- Which is the most attractive type in the diabetes care devices market?

- What is the breakup of the market based on distribution channel?

- Which is the most attractive distribution channel in the diabetes care devices market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the diabetes care devices market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global diabetes care devices market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the diabetes care devices market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global diabetes care devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the diabetes care devices industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)