Digital Textile Printing Market Size, Share, Trends and Forecast by Printing Method, Substrate Type, Ink Type, Application, and Region, 2026-2034

Digital Textile Printing Market Size, Share, Trends & Forecast (2026-2034)

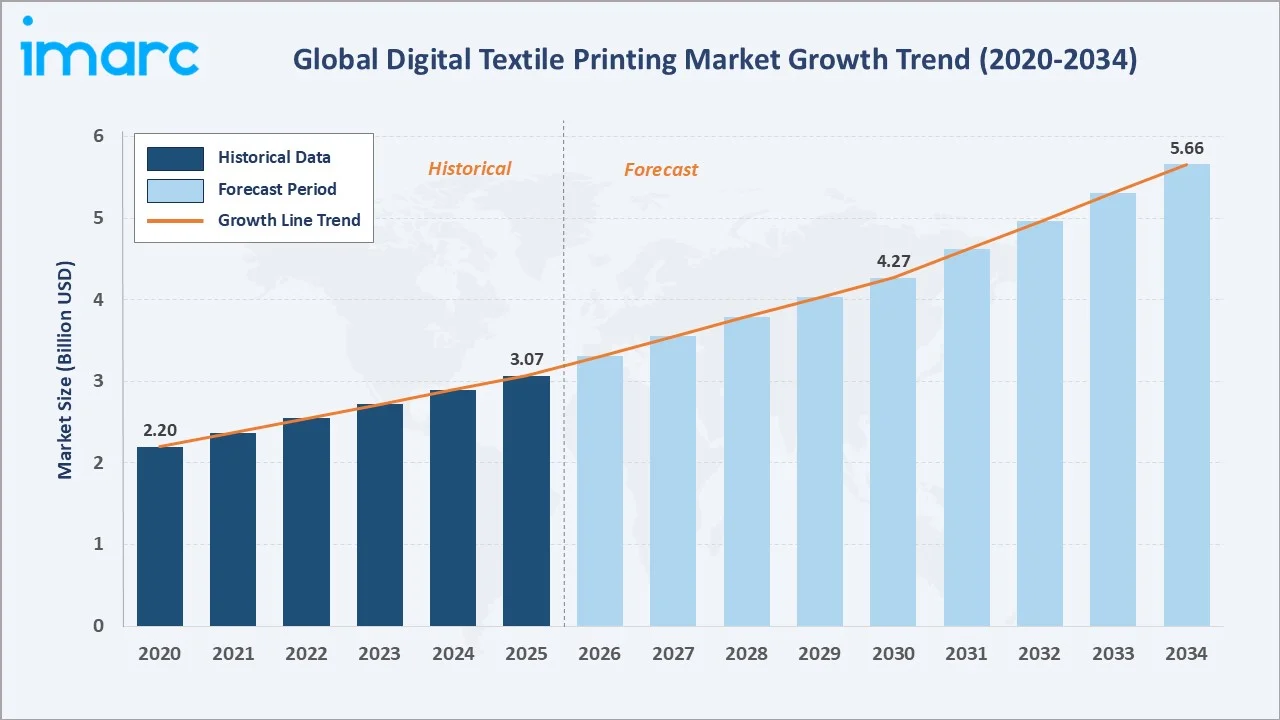

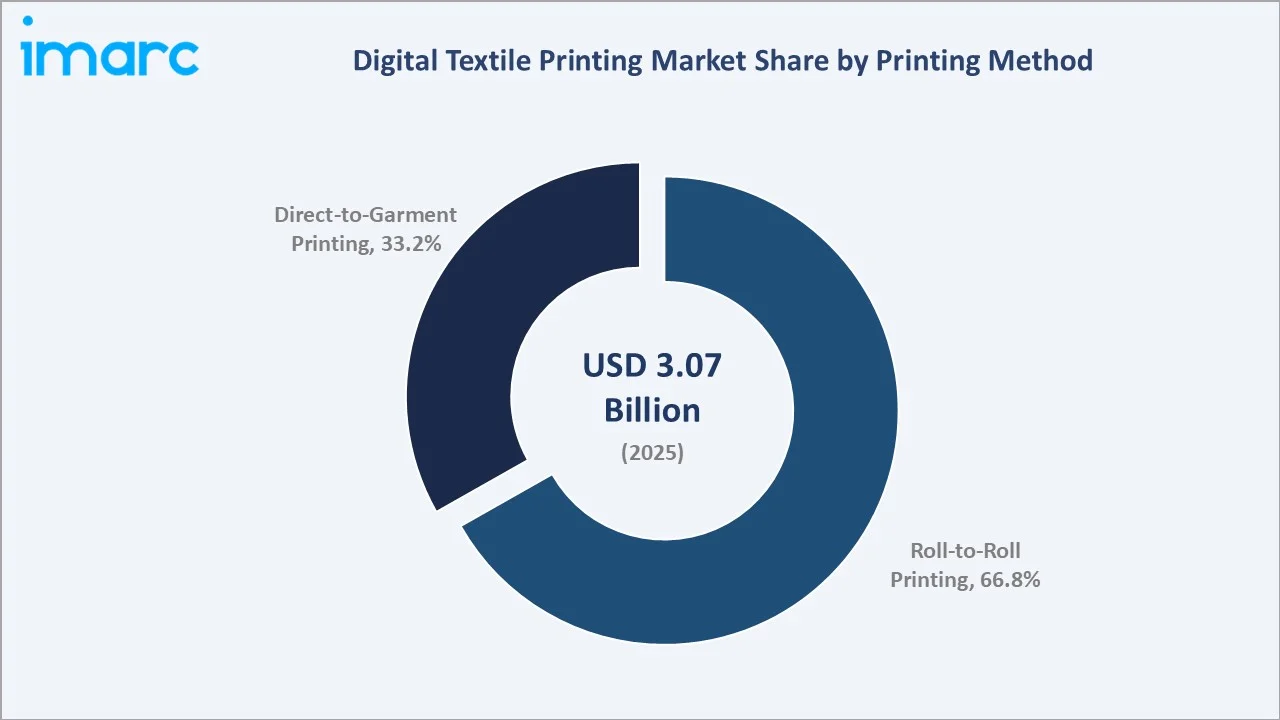

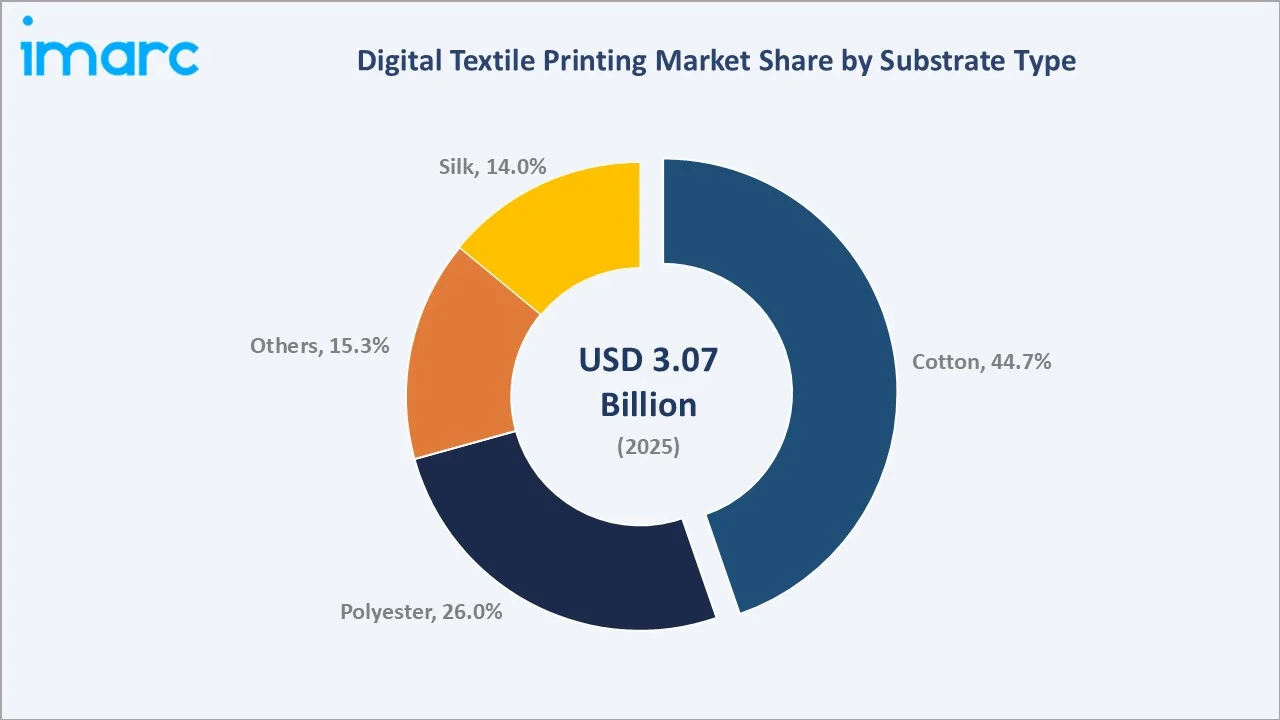

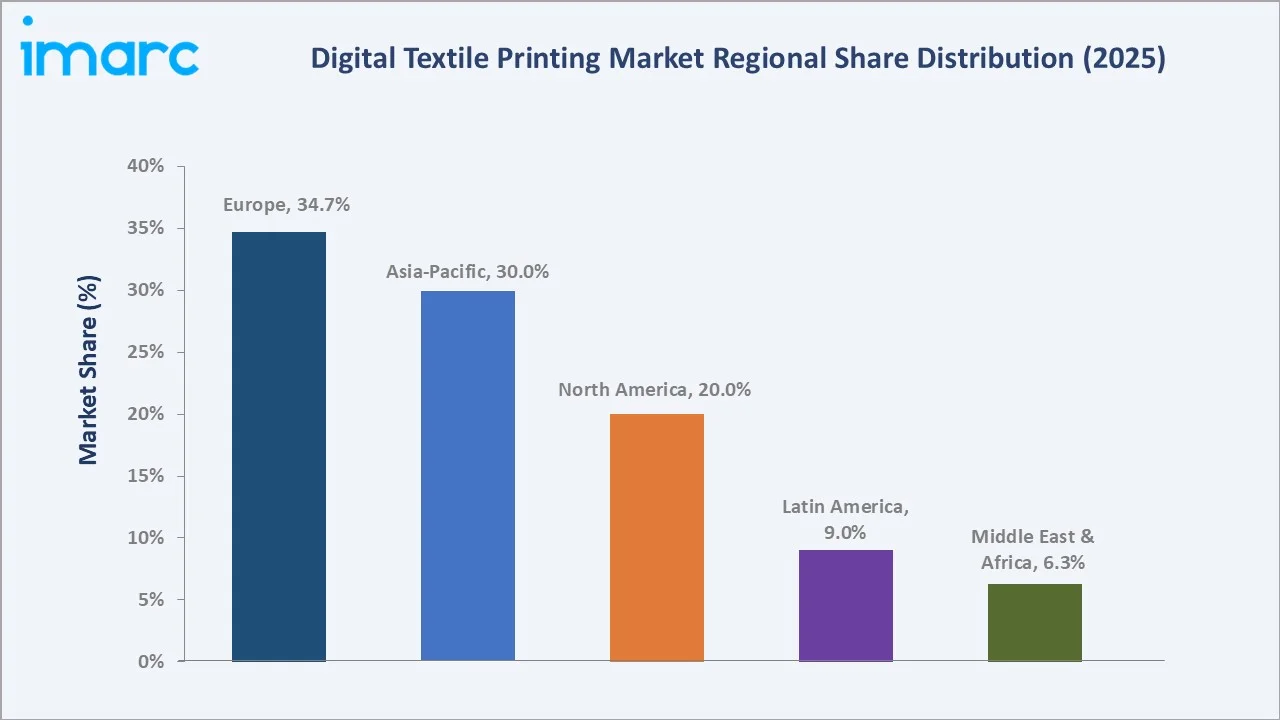

The global digital textile printing market reached USD 3.07 Billion in 2025 and is projected to reach USD 5.66 Billion by 2034, growing at a CAGR of 6.84% during 2026-2034. The global population is projected to grow to 8.6 billion by 2030, 9.8 billion by 2050, and 11.2 billion by 2100. This rising population is driving growth in the digital textile printing market by increasing demand for apparel, home textiles, and customized fabrics. As the number of consumers grows, manufacturers are adopting digital printing technologies to efficiently produce personalized, on-demand, and high-volume textile designs, supporting faster turnaround times and reduced waste. Roll-to-roll printing method dominates at 66.8%. Cotton leads the substrate at 44.7%. Europe commands 34.7% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 3.07 Billion |

| Forecast Market Size (2034) | USD 5.66 Billion |

| CAGR (2026-2034) | 6.84% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Printing Method | Roll-to-Roll Printing (66.8% share, 2025) |

| Dominant Substrate Type | Cotton (44.7% share, 2025) |

| Leading Region | Europe (34.7% share, 2025) |

The global digital textile printing market expanded from USD 2.20 Billion in 2020 to USD 3.07 Billion in 2025, anchored at USD 4.27 Billion in 2030, and forecast to reach USD 5.66 Billion by 2034. Digital textile printing, encompassing all inkjet-based printing on fabric, using reactive, acid, disperse (sublimation), and pigment inks applied through piezoelectric or thermal inkjet printheads to produce colored patterns on textile substrates, represents the most commercially consequential technology disruption in the global textile printing industry since rotary screen printing displaced flatbed printing.

To get more information on this market, Request Sample

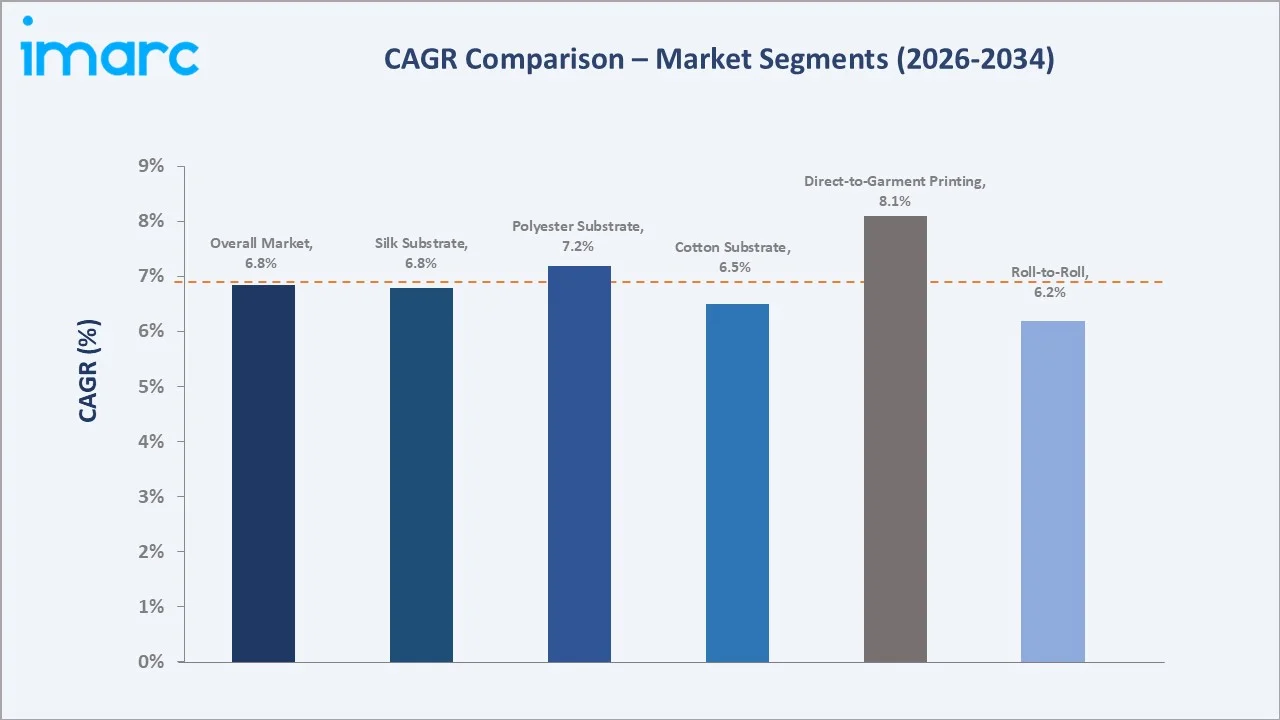

Direct-to-garment printing grows fastest at ~8.1% CAGR through the global print-on-demand market's above-market expansion. Polyester substrate grows at ~7.2% CAGR through disperse/sublimation digital printing's above-market expansion in sportswear, athleisure, and polyester home décor applications.

Executive Summary

The global digital textile printing market at USD 3.07 Billion in 2025 represents the most commercially dynamic technology platform in the global textile printing industry, growing at above-industry-average rates through the structural convergence of fashion's on-demand production transformation, sustainability regulation driving water reduction in textile processing, and e-commerce's creation of economically viable single-piece custom apparel production. Digital textile printing's commercial definition encompasses all inkjet-based printing on fabric substrates, including direct-to-garment, roll-to-roll, and dye-sublimation, creating a technology platform that serves applications from luxury silk fashion fabric through commodity custom t-shirt printing on a single unified inkjet technology foundation. The market is projected to reach USD 5.66 Billion by 2034.

Roll-to-roll printing method at 66.8% leads through industrial fabric yardage production for apparel, home textile, and soft signage applications. Cotton at 44.7% leads the substrate through the dominance of reactive inkjet in apparel and home textiles. Europe leads regionally at 34.7% as a global technology pioneer.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Printing Method | Roll-to-Roll – 66.8% share (2025) |

| Dominant Substrate Type | Cotton – 44.7% market share (2025) |

| Leading Region | Europe – 34.7% share (2025) |

| Market Opportunity | On-demand apparel fulfilment through e-commerce; sustainable waterless digital printing vs conventional; customized home textile printing; technical and medical textile digital print applications |

Key Analytical Observations Supporting The Above Data:

- Roll-to-roll printing method at 66.8%: The roll-to-roll printing method dominates due to its high-speed continuous production, cost-efficiency, and suitability for large-volume fabric processing, making it ideal for apparel, home textiles, and industrial applications.

- Cotton substrate at 44.7%: Cotton is the dominant substrate due to its excellent absorbency, smooth surface, and compatibility with various ink types, making it ideal for vibrant, high-quality prints in apparel and home textiles.

- Europe at 34.7%: Europe dominates regionally due to its well-established textile manufacturing infrastructure, early adoption of advanced printing technologies, and strong focus on high-quality, sustainable, and customized textile production for fashion and home textiles.

Digital Textile Printing Market Overview

The global digital textile printing market operates at the intersection of the textile industry's most commercially consequential technology transition, with rotary screen printing progressively giving way to inkjet digital textile printing through the economic crossover where digital's zero setup cost, unlimited design complexity capability, and single-piece production viability create commercial advantages above screen printing's superior throughput and lower variable cost in long production runs. The digital textile printing market is commercially differentiated from the broader digital printing market by the unique substrate challenges.

The market ecosystem integrates specialty textile inkjet hardware, specialty textile inks, RIP software and workflow, pre-treatment chemistry, and post-process infrastructure. Macroeconomic factors include rising disposable incomes, urbanization, and growing global demand for customized and fashion-forward textiles.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

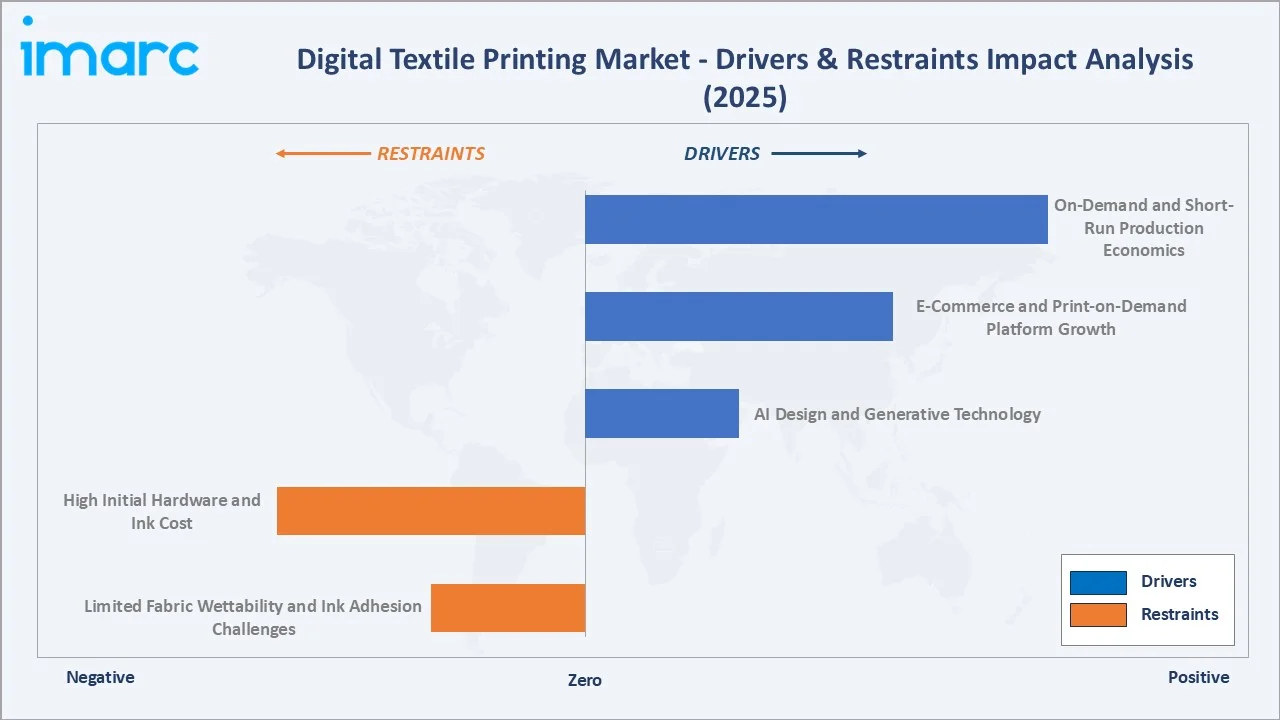

- On-Demand and Short-Run Production Economics: On-demand and short-run production economics enable manufacturers to produce small batches or customized designs quickly and cost-effectively, reducing inventory costs and minimizing waste. Most of the print-on-demand products have an average 20% profit margin. This allows brands to respond to changing fashion trends, seasonal demands, and personalized customer preferences. The ability to run short production cycles efficiently enhances profitability and encourages the adoption of digital printing technologies over traditional screen printing methods, supporting market growth across apparel, home textiles, and specialty fabrics.

- E-Commerce and Print-on-Demand Platform Growth: The growth of e-commerce and print-on-demand platforms enable brands and individual designers to offer customized and personalized textile products directly to consumers. These platforms reduce the need for large inventories and allow for rapid fulfillment of small orders, making digital printing ideal for short-run and one-off designs. Increasing online shopping penetration and consumer preference for unique, on-demand products are accelerating the adoption of digital textile printing technologies across apparel, home textiles, and promotional fabrics.

- AI Design and Generative Technology: AI design and generative technologies enabling rapid creation of unique, complex, and customizable patterns without extensive manual effort. These technologies allow designers to quickly generate new prints, optimize color palettes, and simulate fabric visuals, reducing time-to-market and production costs. By integrating AI into digital printing workflows, manufacturers can efficiently meet growing consumer demand for personalized, on-demand, and trend-responsive textiles in apparel, home décor, and promotional products, enhancing market adoption and innovation. In August 2025, Zimmer Austria advanced textile production by integrating Artificial Intelligence (AI) into its advanced printing technologies. This innovation enhances production efficiency, improves quality control, and expands creative possibilities, providing manufacturers worldwide with greater precision and flexibility in design.

Market Restraints

- High Initial Hardware and Ink Cost: High initial hardware and ink costs create a significant financial barrier for small and medium-sized textile manufacturers. Advanced digital printers and specialized textile inks require substantial upfront investment, limiting adoption despite the technology’s benefits in customization and efficiency. Additionally, ongoing ink and maintenance expenses can increase operational costs, making traditional screen printing or roll-to-roll methods more attractive for price-sensitive producers. This cost challenge slows market penetration, particularly in emerging regions and smaller textile businesses.

- Limited Fabric Wettability and Ink Adhesion Challenges: Limited fabric wettability and ink adhesion challenges reduce print quality, color vibrancy, and durability on certain fabrics, especially synthetics and blends. Inadequate absorption or bonding of inks can lead to smudging, uneven prints, and frequent reprints, increasing waste and production costs. Manufacturers must invest in pre-treatment processes, specialized inks, or surface modification techniques, which add complexity and cost. These technical limitations slow the adoption of digital textile printing, particularly for diverse fabric types and high-volume applications.

Market Opportunities

- Sustainable and Waterless Digital Textile Printing: Sustainable and waterless digital textile printing reduces water usage, chemical waste, and environmental impact compared to conventional textile printing methods. These eco-friendly technologies appeal to environmentally conscious brands and consumers, supporting corporate sustainability goals and regulatory compliance. By enabling energy-efficient, cost-effective, and resource-saving production, manufacturers can expand the adoption of digital printing solutions across apparel, home textiles, and specialty fabrics. This trend positions digital textile printing as a preferred method for sustainable and responsible textile manufacturing.

- Technical and Industrial Textile Digital Printing: Technical and industrial textile digital printing enables customized, high-precision printing on specialized fabrics used in automotive, medical, protective, and industrial applications. Digital printing allows complex patterns, functional coatings, and variable designs that traditional methods cannot achieve efficiently. Adoption in these sectors drives higher-value applications, reduces production time, and supports innovation in performance textiles. As industrial and technical textile demand grows, digital printing provides a scalable, flexible, and sustainable solution, expanding market potential beyond conventional apparel and home textiles.

Market Challenges

- Competition from Traditional Printing: Competition from traditional printing methods, such as screen printing and roll-to-roll printing, offering lower costs for large-volume production and established workflows. Many manufacturers continue to rely on these conventional methods for bulk orders due to familiarity, scalability, and reduced per-unit expenses. This makes it difficult for digital printing to penetrate price-sensitive segments and limits adoption, especially in regions where cost efficiency outweighs customization or sustainability benefits.

- Color Consistency and Pantone Matching Challenges: Color consistency and Pantone matching make it difficult to achieve uniform colors across different production runs and fabric types. Variations in ink behavior, fabric absorbency, and printer calibration can lead to discrepancies in shade and vibrancy. These inconsistencies affect brand quality standards and customer satisfaction, requiring additional testing, pre-treatment, or color correction processes.

Emerging Market Trends

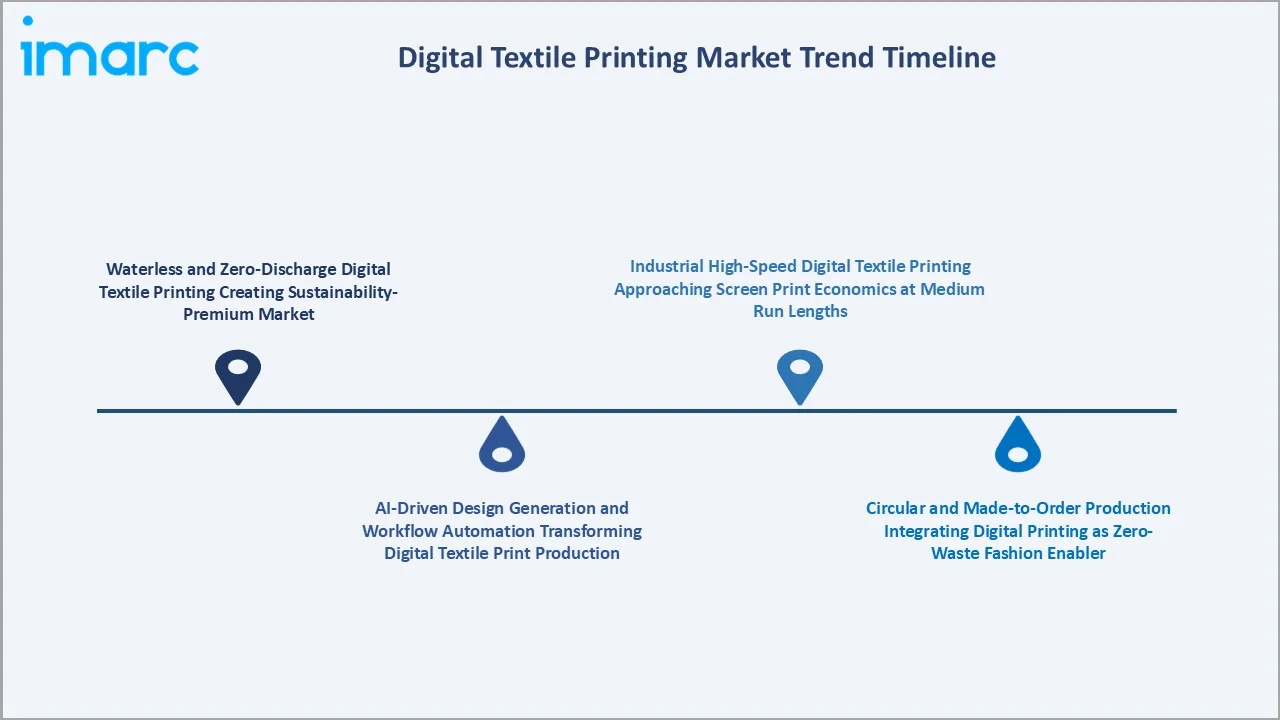

1. Waterless and Zero-Discharge Digital Textile Printing Creating Sustainability-Premium Market

Waterless and zero-discharge digital textile printing is emerging as a key trend by creating a sustainability-premium segment in the market. These technologies minimize water usage, eliminate harmful effluents, and reduce chemical waste, appealing to eco-conscious brands and consumers willing to pay a premium for sustainable textiles. In April 2025, Mimaki Engineering Co., Ltd. launched its “Tx330-1800” and “Tx330-1800B” direct textile inkjet printers for the textile and apparel industry. These printers can print on various fabrics while using extremely low amounts of water. This launch supports the waterless digital textile printing by providing an eco-friendly, sustainability-focused option that minimizes water consumption and chemical waste.

2. AI-Driven Design Generation and Workflow Automation Transforming Digital Textile Print Production

AI-driven design generation and workflow automation enable the rapid creation of complex, customized patterns and streamlining production processes. These technologies reduce design-to-production time, minimize errors, and optimize resource use, enhancing efficiency and consistency. Integration of AI allows predictive design, automated color management, and adaptive printing, supporting on-demand and short-run manufacturing. As a result, manufacturers can deliver personalized, high-quality textile products at scale, driving innovation and adoption in the digital textile printing market.

3. Industrial High-Speed Digital Textile Printing Approaching Screen Print Economics at Medium Run Lengths

Industrial high-speed digital textile printing is bridging the cost gap with traditional screen printing for medium run lengths. Advanced high-speed printers enable faster production without sacrificing print quality, making digital printing economically viable for larger batches. This development allows manufacturers to achieve flexibility, customization, and shorter lead times while approaching the cost efficiency of conventional methods. As a result, adoption expands beyond short-run, niche applications into broader apparel, home textiles, and industrial textile segments, driving market growth.

4. Circular and Made-to-Order Production Integrating Digital Printing as Zero-Waste Fashion Enabler

Circular and made-to-order production enabling zero-waste fashion models. Digital printing allows brands to produce textiles only as orders are received, minimizing overproduction and inventory waste. This approach supports sustainability initiatives, promotes on-demand customization, and integrates seamlessly with circular fashion strategies where materials are reused or recycled. By reducing environmental impact while maintaining design flexibility, digital textile printing becomes a crucial enabler of eco-friendly, made-to-order, and circular fashion practices.

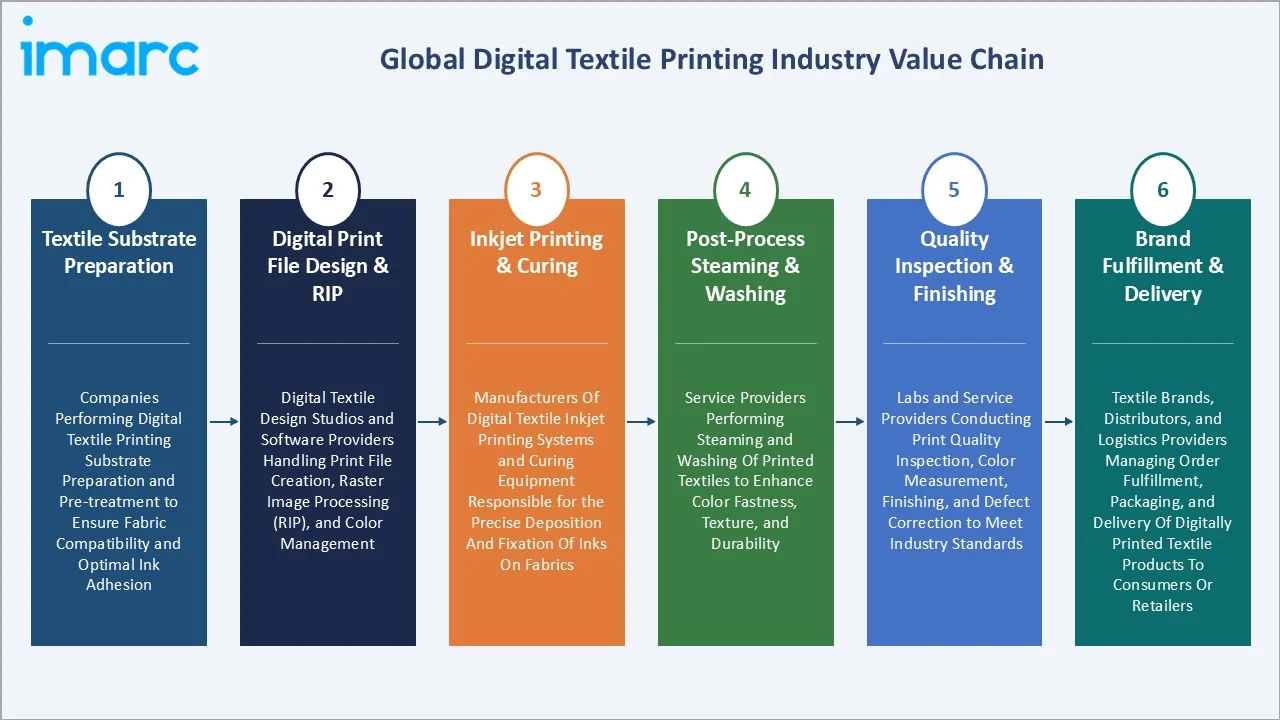

Industry Value Chain Analysis

The digital textile printing value chain is the most technology-intensive value chain in the global textile industry, from specialty ink chemistry through precision inkjet hardware through substrate pre-treatment through the print event through post-process fixation to the finished printed textile product.

| Stage | Key Participants |

|---|---|

| Textile Substrate Preparation | Companies performing digital textile printing substrate preparation and pre-treatment to ensure fabric compatibility and optimal ink adhesion. |

| Digital Print File Design & RIP | Digital textile design studios and software providers handling print file creation, raster image processing (RIP), and color management. |

| Inkjet Printing & Curing | Manufacturers of digital textile inkjet printing systems and curing equipment responsible for the precise deposition and fixation of inks on fabrics. |

| Post-Process Steaming & Washing | Service providers performing steaming and washing of printed textiles to enhance color fastness, texture, and durability. |

| Quality Inspection & Finishing | Labs and service providers conducting print quality inspection, color measurement, finishing, and defect correction to meet industry standards. |

| Brand Fulfillment & Delivery | Textile brands, distributors, and logistics providers managing order fulfillment, packaging, and delivery of digitally printed textile products to consumers or retailers. |

The post-process fixation stage is the digital textile printing value chain's most commercially important quality determinant, reactive inkjet print on cotton requiring precise steam fixation conditions, creating the covalent dye-fiber bond that determines wash fastness performance and commercial quality standard. Inadequate fixation, creating below-standard wash fastness, is the most commercially consequential quality failure in digital reactive cotton printing, requiring correct fixation equipment investment and process control above the hardware and ink investment, receiving disproportionate market attention.

Technology Landscape in the Digital Textile Printing Industry

Printhead Technology

Printhead technology enables high-resolution, precise ink deposition on diverse textile substrates. Innovations in piezoelectric and thermal print heads improve droplet control, speed, and accuracy, allowing complex and detailed designs with consistent color quality. Advanced printhead systems also enhance ink efficiency, reduce waste, and support a wider range of fabric types. By improving print speed, durability, and customization capabilities, printhead advancements drive greater adoption of digital textile printing across apparel, home textiles, and technical fabrics.

Inkjet Printing Technology

Inkjet printing technology enables direct, precise, and high-resolution ink application on a wide variety of fabrics. It supports complex, multi-color designs with minimal waste and faster production cycles compared to traditional methods. Advances in ink formulations, droplet control, and printing speed allow consistent color quality and improved durability across different textile substrates. In January 2026, Konica Minolta, Inc. introduced the O’ROBE inline pretreatment ink for reactive dyes to its Nassenger series of inkjet textile printers. This new ink is designed to shorten the inkjet printing process and reduce energy consumption, enhancing the efficiency of textile printing workflows. This development supports inkjet printing technology by improving process efficiency, enabling faster production cycles, and maintaining high-quality, precise prints.

Sustainable and Waterless Printing Technology

Sustainable and waterless printing technology reduces water usage, chemical discharge, and environmental impact in textile production. These technologies allow manufacturers to produce high-quality prints on various fabrics while meeting strict sustainability standards. By minimizing resource consumption and waste, they support eco-friendly and zero-discharge practices, appealing to environmentally conscious brands and consumers. This innovation enhances the adoption of digital textile printing in premium, sustainable, and made-to-order fashion segments, strengthening the market’s growth and differentiation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Printing Method |

Roll-to-Roll Printing |

66.8% |

2025 |

|

Substrate Type |

Cotton |

44.7% |

2025 |

|

Ink Type |

Sublimation |

48.4% |

2025 |

|

Application |

Garments and Apparels |

41.5% |

2025 |

|

Region |

Europe |

34.7% |

2025 |

By Printing Method

Roll-to-roll printing leads at 66.8% (2025). The roll-to-roll segment serves industrial fabric yardage production across all major end-use applications, apparel fabric, home textile, soft signage, and technical textile, through continuous web inkjet printing at speeds of 50-1,500 sqm/hour, depending on printer generation and model. The segment grows at ~6.2% CAGR through industrial adoption in medium-run fabric printing and home textile digital market expansion.

To access detailed market analysis, Request Sample

Direct-to-garment printing at 33.2% grows fastest at ~8.1% CAGR through the print-on-demand e-commerce revolution and custom apparel market expansion. Direct-to-garment commercial expansion is being driven by declining hardware cost and fashion customization's above-standard consumer demand growth through social media's creator economy.

By Substrate Type

Cotton leads at 44.7% (2025). Cotton's dominance reflects reactive ink digital printing's established commercial deployment for the most widely consumed apparel and home textile fiber, reactive digital print on cotton creating wash-fast, color-brilliant results that sustain cotton's commercial dominance in fashion and home textile digital print applications.

Polyester at 26.0% grows fastest at ~7.2% CAGR through sublimation digital printing's above-market expansion in sportswear and home décor. Silk at 14.0% represents the most commercially premium per-sqm digital textile print application through luxury fashion fabric high-end silk printing. Others at 15.3% encompass nylon, linen, and blended substrates.

Regional Market Insights

| Region | Share (2025) | Key Digital Textile Printing Market Drivers & Characteristics |

|---|---|---|

| Europe | 34.7% | Driven by advanced textile manufacturing infrastructure, early adoption of digital printing technologies, and a strong focus on sustainable, high-quality, and customized textile production. |

| Asia-Pacific | 30.0% | Supported by extensive production capacity, abundant raw material availability, and increasing adoption of digital textile printing for apparel and home textiles. |

| North America | 20.0% | Dominated by the USA’s large and commercially sophisticated textile printing industry, with significant demand for high-quality, customized, and sustainable digital textile products. |

| Latin America | 9.0% | Anchored by Brazil, the region’s most commercially significant digital textile printing hub, supporting both regional consumption and export-oriented textile production. |

| Middle East & Africa | 6.3% | Combining emerging textile manufacturing hubs with growing adoption of digital printing technologies and increasing demand for customized and sustainable textiles. |

Europe's 34.7% market leadership reflects the region's unique combination of digital textile print technology innovation and sophisticated premium fabric printing end-use demand. Asia-Pacific's 30.0% reflects China's and India's rapidly growing digital print adoption above conventional screen printing for short-run fabric and DTG garment production.

North America's 20.0% reflects the most commercially advanced digital textile print ecosystem. Latin America's 9.0% is growing at above-market CAGR through Brazil's textile sector's progressive digital adoption, and the region's growing e-commerce apparel market, creating local digital print service demand. The Middle East and Africa's 6.3% represents the most commercially frontier digital textile print geography with sophisticated print market, premium event and fashion print demand, and emerging adoption collectively creating above-overall-market growth through the region's low base effect and rising commercial adoption rate.

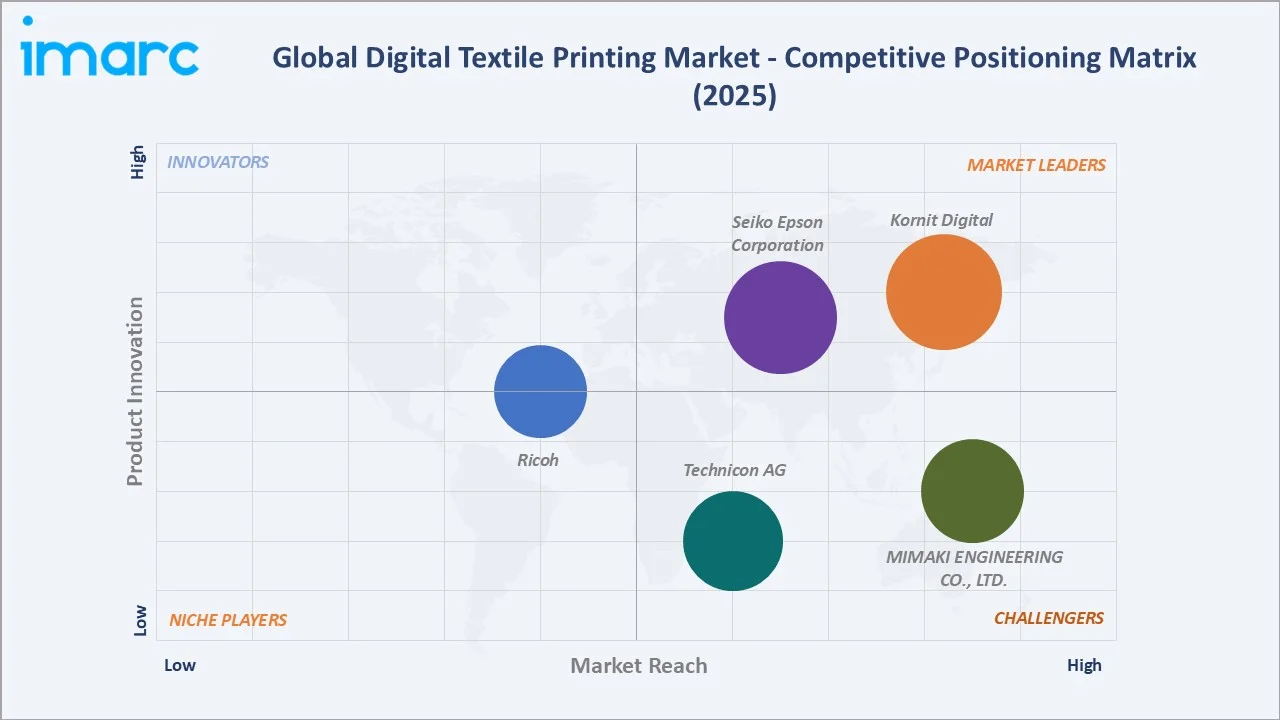

Competitive Landscape

The global digital textile printing competitive landscape is structured across three commercially distinct value chain positions: hardware OEMs, ink and chemistry companies, and software and workflow providers.

| Company Name | Key Brands | Market Position | Core Strength |

|---|---|---|---|

| Kornit Digital | Kornit Presto MAX PLUS, Kornit Atlas MATRIX | Market Leader | Kornit Digital is a leader in sustainable, on-demand digital textile printing, specializing in Direct-to-Garment (DTG) technologies. |

| Seiko Epson Corporation | Monna Lisa Direct-to-Fabric Printers, Epson Direct-to-Garment Printers, Epson Direct-to-Film (DTFilm) Printers | Market Leader | Seiko Epson Corporation is a leader in digital textile printing, driving the industry transition from analog to digital with its high-precision printhead technology and the industrial Monna Lisa printer series. |

| MIMAKI ENGINEERING CO., LTD. | TS330-1800, TS200-1600, Tx330-1800B, TRAPIS | Strong Challenger | MIMAKI ENGINEERING CO., LTD. plays a leading role in digital textile printing by providing comprehensive, high-speed, and cost-effective industrial inkjet printing solutions. |

| Technicon AG | Alpha 330 Textile Edition, Alpha 190 Textile Edition, Alpha DyeSub Edition, P5 350 TEX iSUB, P5 500 TEX iSUB | Strong Challenger | Technicon AG is the holding company and strategic parent entity for the Durst Group, a global leader in high-end industrial inkjet printing technology. Through its subsidiaries, particularly Durst Group AG, Technicon AG plays a critical role in developing and manufacturing industrial digital textile printing systems. |

| Ricoh | Ri 100, Ri 1000X, Ri 2000, Ri 4000 | Established Player | Ricoh plays a major role in digital textile printing by providing advanced, high-speed inkjet printheads and direct-to-garment (DTG) / direct-to-film (DTF) printers. |

The competitive landscape's most commercially consequential disruption is the emerging low-cost Chinese digital textile printer manufacturers. While Chinese systems have not yet achieved the quality, reliability, and software ecosystem of premium OEMs, their progressive technology improvement and price competitiveness are creating commercial pressure on premium OEM pricing power above the historically premium-market-protected Western OEM competitive position.

Key Company Profiles

Kornit Digital

Kornit Digital is a leading global provider of innovative digital textile printing solutions, specializing in direct‑to‑garment (DTG) printing systems. The company’s technologies enable high‑quality, on‑demand, and environmentally conscious textile production by eliminating the need for screens and reducing water and chemical usage compared with traditional printing methods.

- Key Products: Kornit Presto MAX PLUS, Kornit Atlas MATRIX.

- Recent Developments: In May 2026, Kornit Digital announced that its Atlas MATRIX platform is commercially available, following a global beta program conducted in production facilities across Europe and North America. The Atlas MATRIX platform builds on Kornit’s Atlas MAX PLUS capabilities, extending support to polyester, blended, and sublimated fabrics. It allows manufacturers to print across multiple fabric types on a single system while maintaining industrial-scale productivity and delivering retail-quality output.

- Strategic Focus: Expanding versatile, industrial‑scale printing platforms that support multiple fabric types while delivering high productivity and retail‑grade quality for sustainable, on‑demand textile production.

Seiko Epson Corporation

Seiko Epson Corporation is a major Japanese technology company with a strong presence in the digital textile printing industry through its advanced precision inkjet printing solutions.

- Key Products: Monna Lisa Direct-to-Fabric Printers, Epson Direct-to-Garment Printers, Epson Direct-to-Film (DTFilm) Printers.

- Recent Developments: In January 2026, Epson launched the SureColor G9000, a new high-production Direct-To-Film (DTFilm) printer designed to meet the increasing global demand for versatile and efficient textile transfer printing. Building on Epson’s existing DTFilm lineup alongside the SC-G6000, the SC-G9000 offers improved speed, reliability, and easier maintenance, catering to commercial garment decorators and textile manufacturers.

- Strategic Focus: Advancing high‑precision, energy‑efficient inkjet printing technologies and expanding versatile production solutions like DTFilm printers to meet growing demand for quality, flexible, and sustainable textile printing.

Market Concentration Analysis

The global digital textile printing market is moderately concentrated in the hardware segment and fragmented in the ink market. Market concentration is evolving through two opposing forces: premium market concentration and mid-market fragmentation. However, the presence of regional and niche players in specific segments (e.g., direct‑to‑film, textile transfer printing) keeps competitive dynamics diverse, with innovation and specialization shaping market shares.

Investment & Growth Opportunities

Highest Growth Segments

Direct-to-garment printing (~8.1% CAGR through POD e-commerce and custom apparel), polyester sublimation substrate (~7.2% CAGR through sportswear and home décor), AI-driven design-to-print automation platform (~20-25% CAGR from small base), sustainable waterless digital textile print technology (~10-12% CAGR through sustainability regulation), South and Southeast Asia regional adoption (~10-12% CAGR through China and India industrial transition from screen to digital), and technical textile digital printing (~9-12% CAGR through automotive and medical specialty applications) represent the highest-growth digital textile printing investment vectors through 2034.

Emerging Investment Opportunities

The AI design generation integration market for digital textile printing, connecting generative AI design platforms directly to digital textile print production workflows through API integration that allows e-commerce sellers, POD platform users, and fashion brands to generate, approve, and automatically dispatch custom digital textile print orders without human design or production intervention, represents the most commercially novel digital textile printing adjacency investment opportunity above traditional hardware and ink market participation.

Investment Themes

- Waterless and sustainable digital textile print certification program investment for European fashion brand premium sourcing market: The European fashion brand sustainable sourcing premium creates a commercially accessible sustainable print premium that digital print service bureaux can capture through relatively modest certification investment above expensive hardware replacement.

- RIP software and AI design integration platform investment targeting the global POD market's design creation workflow: The print-on-demand market's most commercially underserved technology need is the design-to-production automation layer, connecting generative AI design creation through automatic file optimization, substrate-specific color management, and automatic print dispatch through direct API connection to POD fulfilment infrastructure.

Future Market Outlook (2026-2034)

The global digital textile printing market is projected to grow from USD 3.07 Billion in 2025 to USD 5.66 Billion by 2034, delivering a 6.84% CAGR over the forecast period. The market's anchor value of USD 4.27 Billion in 2030 represents the digital textile printing industry at its most commercially consequential structural inflection, the point at which digital textile printing transitions from a specialty niche and premium market technology toward a mainstream production alternative competitive with rotary screen printing at medium run lengths through the combination of continued speed improvement, ink cost reduction, and sustainability regulatory preference that collectively create digital print's commercial viability above screen printing across progressively longer production runs through 2030.

Three structural forces define digital textile printing's growth through 2034: the print-on-demand market's permanent commercial establishment as the primary custom apparel production model, EU textile sustainability regulation's commercial mandate for reduced-water-consumption printing, and AI design generation's commercial scale-up, creating the textile design content supply that enables the POD market's unlimited SKU catalogue economics.

Research Methodology

Primary Research

Primary research comprised structured interviews with global digital textile printing industry stakeholders, including technology directors, product managers, ink chemistry directors, production directors, pod platform technology managers, and market participant surveys from commercial and industrial digital textile printers across Europe, Asia Pacific, and North America.

Secondary Research

Secondary research encompassed digital textile printing market data, company annual reports, product documentation and market communications, digital textile printing market analysis, market development data, and digital textile ink certification database. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a digital textile print production volume model: estimated global digital textile print yardage production by region multiplied by average digital print price per sqm, creating revenue by application. POD market modelled separately through global POD order volume growth multiplied by average DTG print revenue per order. Equipment sales and service revenue are modelled through production capacity expansion demand.

Digital Textile Printing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Printing Methods Covered | Roll-to-Roll Printing, Direct-to-Garment Printing |

| Substrate Types Covered | Cotton, Silk, Polyester, Others |

| Ink Types Covered | Reactive, Acid, Direct Disperse, Sublimation, Pigments, Others |

| Applications Covered | Garment and Apparels, Home Furnishing Textiles, Technical Textiles, Display and Signage, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Kornit Digital, Seiko Epson Corporation, MIMAKI ENGINEERING CO. LTD., Technicon AG, Ricoh, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the digital textile printing market from 2020-2034.

- The digital textile printing market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the digital textile printing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Digital Textile Printing Market Report

The global digital textile printing market reached USD 3.07 Billion in 2025, driven by growing demand for customized, on-demand, and sustainable textile products, rapid adoption of advanced inkjet and waterless printing technologies, and expansion of e-commerce and print-on-demand platforms that support personalized apparel, home textiles, and technical fabrics.

The global digital textile printing market grows at 6.84% CAGR during 2026-2034, reaching USD 5.66 Billion by 2034. The overall growth is sustained by POD e-commerce platform growth, textile sustainability regulations creating demand for waterless digital printing above conventional wet processing, and AI design generation enabling unlimited custom textile print content creation at a commercial scale.

Roll-to-roll printing leads at 66.8% through industrial fabric yardage production for apparel, home textile, and soft signage at throughput rates of 200-1,500 sqm/hour.

Cotton leads at 44.7% through reactive inkjet digital printing's established commercial deployment for the most widely consumed apparel and home textile fiber, reactive dye's covalent bonding to cellulose, creating wash-fast, color-brilliant results in fashion apparel and home textile digital print.

Europe leads at 34.7% through Italy's luxury silk and fashion fabric digital printing market, Germany's technical textile digital print sector, and industrial volume digital textile adoption for fast fashion fabric.

Leading companies include Kornit Digital, Seiko Epson Corporation, MIMAKI ENGINEERING CO., LTD., Technicon AG, and Ricoh, among others.

The global digital textile printing market is projected to reach approximately USD 4.27 Billion by 2030, with ultra-high-speed industrial R2R digital printing growth creating commercial viability, competing with rotary screen printing for medium-run fabric production for the first time commercially. The Asia Pacific POD market is growing as China and India develop domestic on-demand custom apparel fulfilment infrastructure, and waterless digital printing achieves mainstream certification.

Three priority investment opportunities: Direct-to-garment industrial system investment for Asia Pacific POD market development, waterless and sustainable digital textile print service certification investment for European fashion brand premium sourcing, and AI design-to-print SaaS platform targeting the POD market's design creation workflow automation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)