Drone Data Services Market Report by Service Type (Mapping and Surveying, Photogrammetry, 3D Modeling and Digital Elevation Model (DEM), and Others), Platform (Cloud-based, Operator Software), End User (Real Estate and Construction, Agriculture, Security and Law Enforcement, Mining, and Others), and Region 2026-2034

Drone Data Services Market Size:

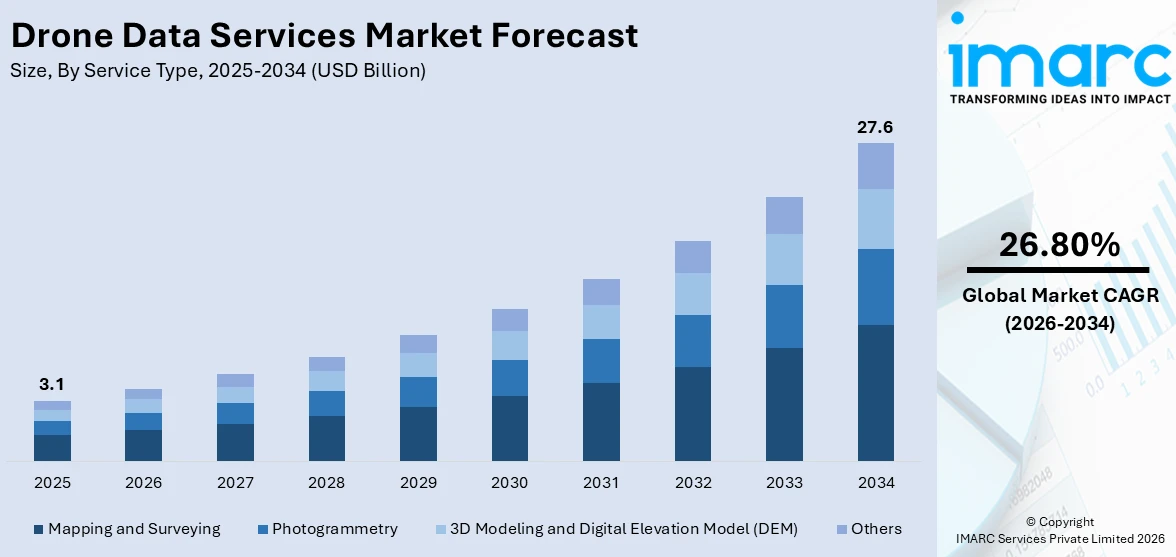

The global drone data services market size reached USD 3.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 27.6 Billion by 2034, exhibiting a growth rate (CAGR) of 26.80% during 2026-2034. The market is being driven by the widespread adoption of drones in commercial sectors, advancements in drone technology, and a growing need for efficient data collection and analysis in industries such as agriculture, construction, and real estate, enhancing decision-making and operational efficiencies.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 3.1 Billion |

|

Market Forecast in 2034

|

USD 27.6 Billion |

| Market Growth Rate 2026-2034 | 26.80% |

Drone Data Services Market Analysis:

- Major Market Drivers: Some of the major factors driving the drone data services market growth include increased commercial applications, rapid technological advancements, and regulatory support for safe and expanded use of drones.

- Key Market Trends: The development of autonomous drone operations, integration with artificial intelligence (AI) and analytics, the expansion of drone services in public safety, the development of regulatory frameworks, and customization for industry-specific applications are the major key trends for the drone data services market.

- Geographical Trends: North America dominates the drone data services market due to region’s innovative ecosystem fostering continuous advancements, favorable regulatory support, and increasing applications in agriculture and construction sectors.

- Competitive Landscape: Some of the major market players in the drone data services industry include Aerialair, Agribotix.com, Autodesk Inc, Cyberhawk, Deveron, DJI, Dronecloud, DroneDeploy, Ninox Robotics Pty Ltd, Pix4D SA, Sentera, Skycatch, Inc, and Terra Drone Corporation, among many others.

- Challenges and Opportunities: Compatibility and interoperability issues, counterfeit and substandard solutions, environmental concerns and sustainability, and standardization and regulatory compliance are some of the challenges. Nonetheless, there are few opportunities that key market players can use to their advantage, and they include developing enhanced analytics capabilities, expanding into emerging markets, and exploring applications in niche sectors like public safety, environmental monitoring, and delivery services.

To get more information on this market Request Sample

Drone Data Services Market Trends:

The Advent of Commercial Drones

The drone data services market is being driven by the increasing use of commercial drones. These drones are lightweight and are designed to provide efficient, cost-effective data collection for applications, such as training and simulation, along with repair, maintenance, and overhaul services. As per the data published by the Federal Aviation Administration, by February 2024, there were 781,781 drones registered in the US, with 375,226 specifically registered for commercial use.

The advent of commercial drones thereby is a significant factor for the drones data services market outlook.

Increasing Product Usage in Agriculture

The agriculture sector is increasingly adopting drone services to enhance efficiency, productivity, and precision. Drone services include various unmanned aerial vehicles (UAVs) and drone-related solutions equipped with advanced sensors that can monitor crop health, irrigation needs, and soil conditions. As a result, they are extensively utilized in crop monitoring and precision agriculture practices, enabling farmers make informed decisions. For instance, data sourced from the State of Food and Agriculture states that in 2021, close to 14% of agriculture retailers in the US adopted drone input application services, with an expected rise to 29% by 2024.

Rapid Technological Advancements and Product Innovations

Technological advancements and innovations have propelled the drone data services market by introducing features that improve sensor technology, flight and data processing capabilities, and extend battery life. These new products are equipped with high-resolution cameras, LiDAR systems, and multispectral sensors that offer higher resolution, detailed images and data, and improved stability, enabling businesses to take advantage of aerial data collection and analysis for diverse applications. Additionally, the integration of artificial intelligence (AI) and machine learning (ML) have allowed sophisticated data analysis, making drones a pivotal tool in industries requiring 3D mapping and geospatial information. For example, in April 2022, Wing Aviation LLC, a US-based company prominent in designing, manufacturing, and deploying delivery drones, launched a novel drone delivery service in Dallas. The company’s quadcopters will deliver health and wellness products that require immediate delivery.

Drone Data Services Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on service type, platform, and end user.

Breakup by Service Type:

- Mapping and Surveying

- Photogrammetry

- 3D Modeling and Digital Elevation Model (DEM)

- Others

Mapping and Surveying accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the service type. This includes mapping and surveying, photogrammetry, 3D modeling and digital elevation model (DEM), and others. According to the report, mapping and surveying represented the largest segment.

Mapping and surveying represents the dominating service type in the drone data services market share due to their high efficiency and accuracy in capturing detailed geographical data across inaccessible areas. Due to these characteristics, they are highly adopted in areas like construction, urban planning, and mining that require precise topographical information. As compared to traditional surveying methods, drones offer safer, quicker, and more cost-effective real-time data collection solutions as they are integrated with advanced imaging technologies and GPS. As a result, drones form an indispensable part of mapping and surveying in modern infrastructure development and land management.

Breakup by Platform:

- Cloud-based

- Operator Software

Operator software is the predominant market segment

A detailed breakup and analysis of the market based on the platform have also been provided in the report. This includes cloud-based and operator software. According to the report, operator software accounted for the largest market share.

Operator software holds a considerable share in the drone data services market size due to their increasing adoption in agriculture, infrastructure, construction, and public safety sectors. Operator software enables the efficient collection, organization, and analysis of vast amounts of data captured by drones, further providing actionable insights and informed decision making. For instance, in January 2024, UAVOS Inc. launched its next-generation flight control system Medium Altitude Long Endurance (MALE) UAV featuring AI software, sensors, powerful processing upgrades, and leading edge control algorithms. The use of such high-end technology promises the autonomous collection and analysis of data, enabling processing on big data platforms.

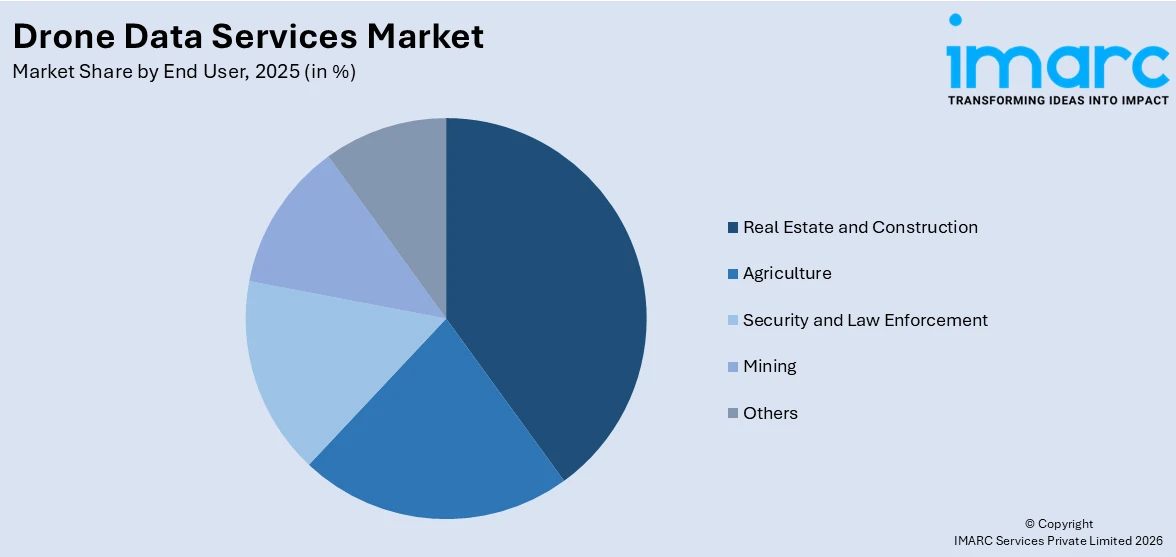

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Real Estate and Construction

- Agriculture

- Security and Law Enforcement

- Mining

- Others

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes real estate and construction, agriculture, security and law enforcement, mining, and others.

In real estate and construction, drones are extensively used for aerial photography, site inspection, and progress monitoring. They provide developers and contractors with high-resolution imagery that helps in marketing properties effectively, planning construction projects more accurately, and ensuring that development adheres to timelines and safety regulations.

Drones in agriculture help farmers enhance crop yields and reduce waste through precision farming techniques. They can monitor crop health, analyze soil conditions, and manage resources, such as water and fertilizers, with high precision. By providing data on crop vigor and pest infestations, drones allow for targeted intervention, ultimately leading to more efficient farm management and increased productivity.

For security and law enforcement, drones offer substantial capabilities in surveillance, crowd monitoring, and tactical operations. They can be deployed to gather real-time video during emergency responses, search and rescue missions, and at large public events, enhancing situational awareness and public safety. Drones also play a role in border surveillance and infrastructure security, providing a cost-effective alternative to manned patrols.

In the mining sector, drones are revolutionizing the way geological surveys and site inspections are conducted. They provide a safe means to explore and monitor mine sites, especially those that are hazardous and difficult for humans to access. Drones help in mapping and analyzing terrain, planning blasting activities, and monitoring environmental compliance, which improves operational efficiencies and safety in mining operations.

Other industries, such as environmental monitoring, energy, and utilities, also drive demand for drone data services. Drones monitor wildlife, track environmental pollution, inspect power lines and pipelines, and assess damage after natural disasters.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest drone data services market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for drone data services.

North America dominates the global drone data services market due to region’s innovative ecosystem fostering continuous advancements, favorable regulatory support, and increasing applications in agriculture and construction sectors. Also, their increasing adoption in civil aerospace, supported by the growing need for commercial drones are propelling the market. Moreover, the region houses leading drone manufacturers and tech companies that are continuously innovating drone capabilities and applications. Moreover, the need for advanced aerial mobility solutions is acting as another factor facilitating the leadership of North America in the drone data services market outlook. For instance, in October 2023, Michigan Central and the Michigan Department of Transportation (MDOT) launched Detroit's Advanced Aerial Innovation Region in Detroit to accelerate commercial drone development by attracting startups, catalyzing new data and service high-skill jobs, advancing policy, and driving commercialization and adoption of drone technology.

Competitive Landscape:

The competitive landscape of the drone data services market is characterized by rapid technological advancements, strategic collaborations, and a focus on expanding application areas to include emerging industries and new geographical markets. Companies compete on innovation, pricing, and quality of service, with key players often forming partnerships to leverage mutual technological and market advantages. The race to develop differentiated offerings and secure a dominant position is intensified by the entry of new startups, which continually challenge established firms with disruptive technologies and business models. The market players are also focusing on introducing image quality and optimal productivity drone data services solutions that further bolster the market growth. For instance, in September 2023, Phase One and Boston partnered for a strong Drone Imaging collaboration in the Nordics to enhance the market's access to drone payload solutions, offering customers unparalleled image quality, optimal productivity, and seamless data acquisition without any compromises.

The report provides a comprehensive analysis of the competitive landscape in the global drone data services market with detailed profiles of all major companies, including:

- Aerialair

- Agribotix.com

- Autodesk Inc

- Cyberhawk

- Deveron

- DJI

- Dronecloud

- DroneDeploy

- Ninox Robotics Pty Ltd

- Pix4D SA

- Sentera

- Skycatch, Inc

- Terra Drone Corporation

Drone Data Services Market News:

- In November 2022, Strayos partnered with Delta Drone to expand their reach into Australia and Africa.

- In December 2023, ReadyMonitor, a company based in the US that offers drone services, launched the 'Beyond Visual Line of Sight (BVLOS)' drone dock service to enable drone flight operations across the US through remotely operated drones.

- In September 2022, Safe Pro Group acquired mission-critical drone solutions company Airborne Response to grow its security and safety portfolio by leveraging drone-based technology for diverse applications.

Drone Data Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Types Covered | Mapping and Surveying, Photogrammetry, 3D Modeling and Digital Elevation Model (DEM), Others |

| Platforms Covered | Cloud-based, Operator Software |

| End Users Covered | Real Estate and Construction, Agriculture, Security and Law Enforcement, Mining, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Aerialair, Agribotix.com, Autodesk Inc, Cyberhawk, Deveron, DJI, Dronecloud, DroneDeploy, Ninox Robotics Pty Ltd, Pix4D SA, Sentera, Skycatch, Inc, Terra Drone Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the drone data services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global drone data services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the drone data services industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Drone Data Services Market Report

The global drone data services market was valued at USD 3.1 Billion in 2025.

We expect the global drone data services market to exhibit a CAGR of 26.80% during 2026-2034.

The rising integration of drone data services with advance technologies, such as the Internet of Things (IoT), Artificial Intelligence (AI), and cloud-based storage, to upload, share, store, and process aerial images is primarily driving the global drone data services market.

The sudden outbreak of the COVID-19 pandemic has led to the widespread adoption of drone data services across numerous counties to track the red alerted zones via aerial route.

Based on the service type, the global drone data services market has been segregated into mapping and surveying, photogrammetry, 3d modeling and Digital Elevation Model (DEM), and others. Among these, mapping and surveying currently holds the largest market share.

Based on the platform, the global drone data services market can be bifurcated into cloud-based and operator software. Currently, operator software exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global drone data services market include Aerialair, Agribotix.com, Autodesk Inc, Cyberhawk, Deveron, DJI, Dronecloud, DroneDeploy, Ninox Robotics Pty Ltd, Pix4D SA, Sentera, Skycatch, Inc, and Terra Drone Corporation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)