Drone Package Delivery Market Size, Share, Trends and Forecast by Solution, Duration, Range, Long Range, Capacity, Type, End Use Industry, and Region 2026-2034

Drone Package Delivery Market Size, Share, Trends & Forecast (2026-2034)

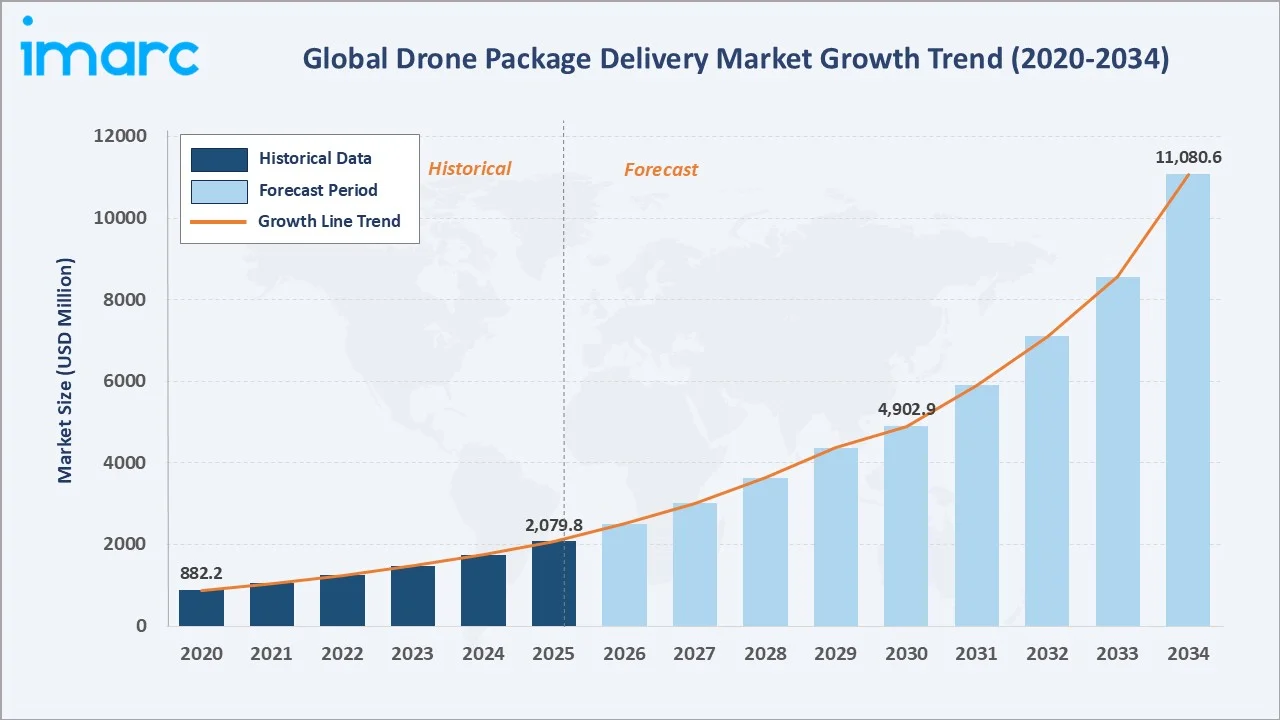

The global drone package delivery market reached USD 2,079.8 Million in 2025 and is projected to reach USD 11,080.6 Million by 2034, growing at a CAGR of 18.71% during 2026-2034. Surging e-commerce demand, last-mile delivery transformation, growing regulatory approvals for beyond visual line of sight (BVLOS) operations, and significant investments in UAV infrastructure are the primary growth catalysts driving the market forward.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2,079.8 Million |

|

Forecast Market Size (2034) |

USD 11,080.6 Million |

|

CAGR (2026-2034) |

18.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.8% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

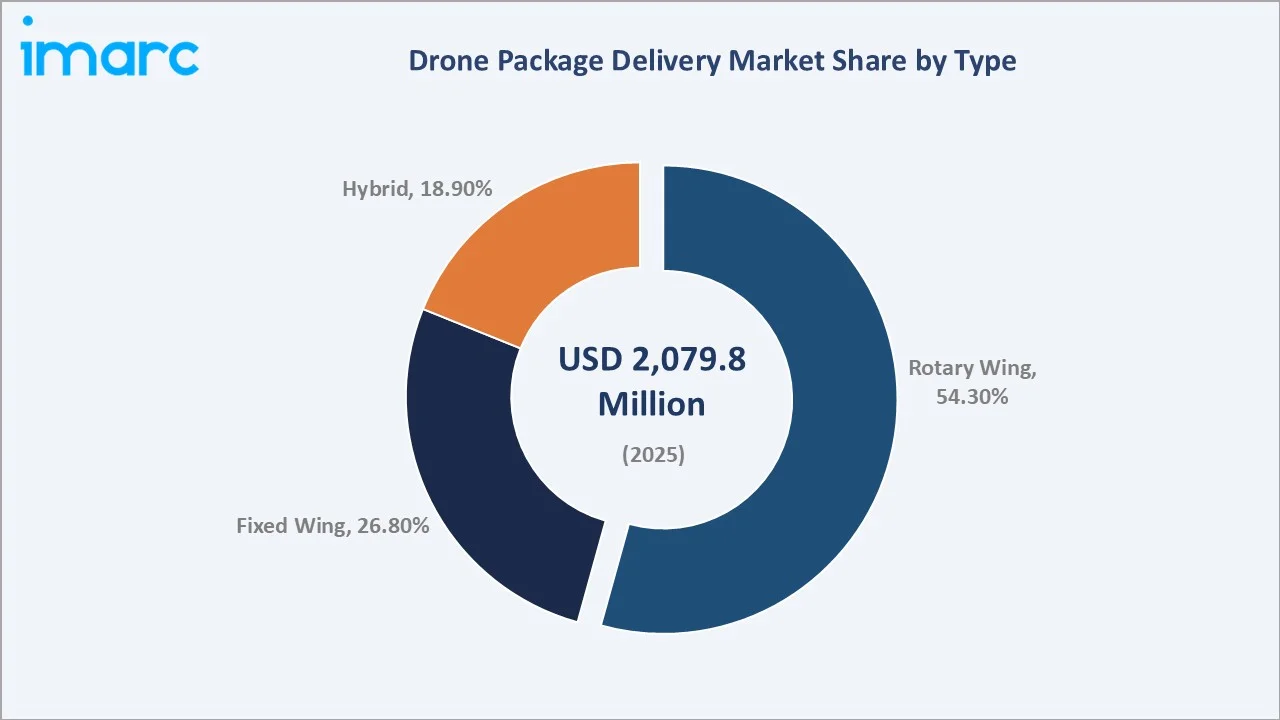

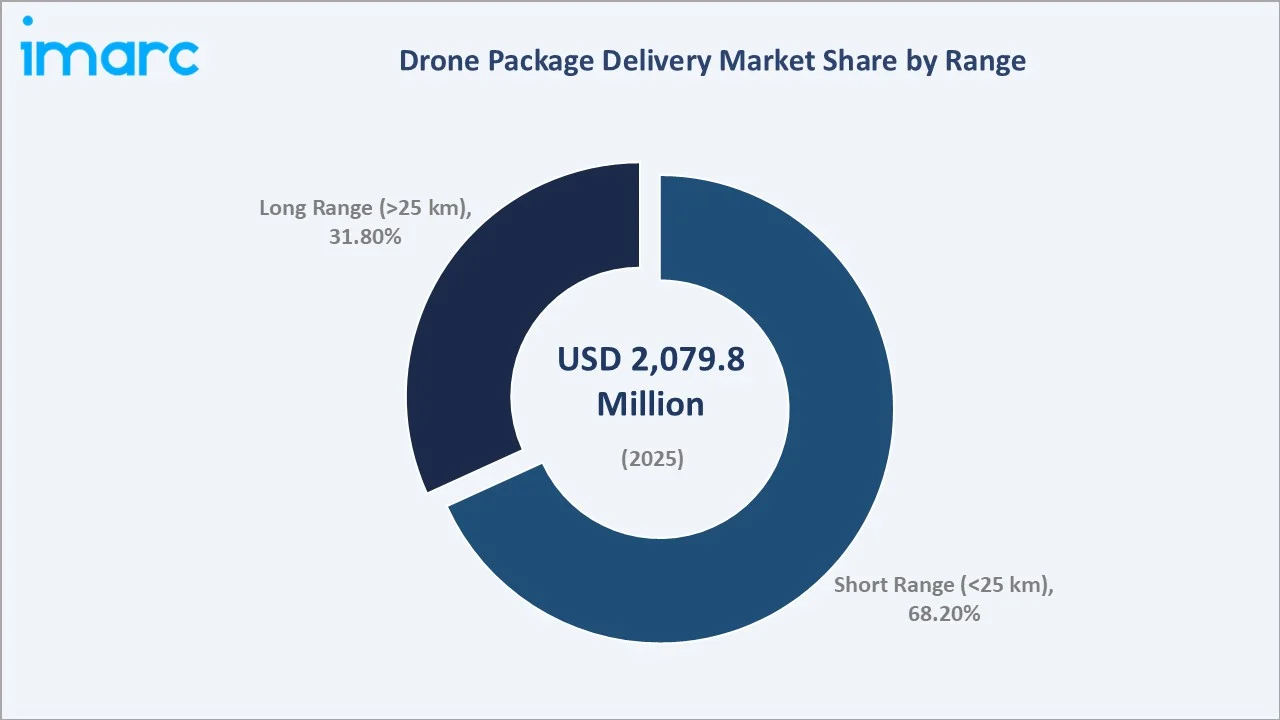

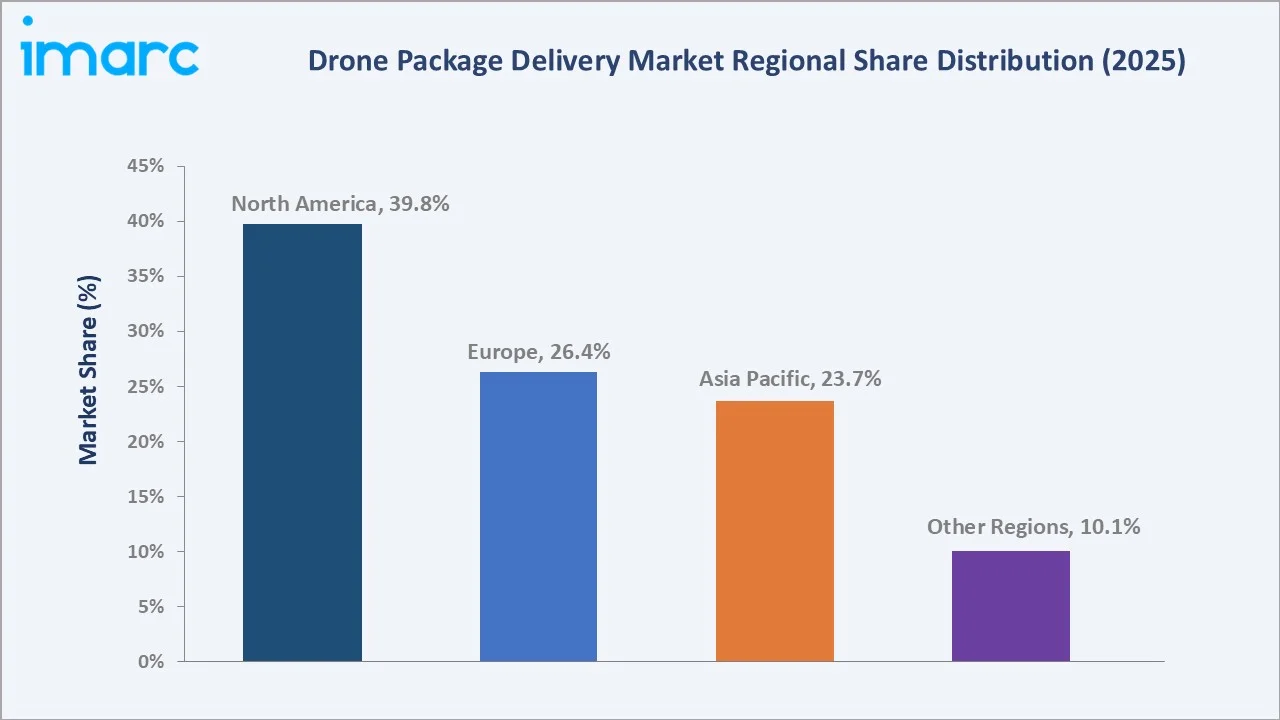

North America dominates, holding a 39.8% market share in 2025, while the rotary wing segment leads type demand at 54.3%. Short range delivery (<25 kilometers) maintains the largest range segment share at 68.2%. Drone package delivery offers significant advantages over conventional logistics, including faster last-mile fulfilment, reduced carbon emissions per delivery, access to geographically constrained areas, and significant cost reduction potential in urban and semi-urban delivery corridors.

To get more information on this market, Request Sample

With applications spanning e-commerce, healthcare, food and beverage, and postal services, the market is expected to continue expanding, supported by AI-integrated flight management systems, battery technology breakthroughs, and expanding regulatory frameworks enabling commercial drone operations at scale.

Executive Summary

The global drone package delivery market is on an accelerating growth trajectory, underpinned by rapid e-commerce expansion, increasing regulatory clarity for commercial UAV operations, and significant private and public investment in drone infrastructure. The market reached USD 2,079.8 Million in 2025 and is forecast to reach USD 11,080.6 Million by 2034, reflecting a robust CAGR of 18.71% over the forecast period.

North America leads globally with a 39.8% revenue share in 2025, driven by progressive FAA regulatory frameworks, high e-commerce penetration, and active deployment by Amazon Prime Air, Wing (Alphabet), and UPS Flight Forward. Asia Pacific, at 23.7%, represents the fastest-growing opportunity, with China, Japan, and South Korea investing heavily in drone corridor infrastructure and urban air mobility integration.

Rotary wing drones dominate type demand at 54.3% due to their vertical takeoff and landing (VTOL) capability, hover stability, and suitability for last-mile urban delivery. Short range delivery (<25 km) commands the largest range segment at 68.2%, aligned with the predominance of urban and suburban delivery use cases. Leading players, including Amazon.com Inc., Wing Aviation LLC, United Parcel Service of America, Inc., Zipline, Matternet Inc., and EHang. continue to invest in autonomous flight systems, safety redundancy, and regulatory compliance frameworks.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Rotary Wing – 54.3% share (2025) |

|

Largest Segment (Range) |

Short Range (<25 km) – 68.2% share (2025) |

|

Leading Region |

North America – 39.8% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (urbanization + regulatory expansion) |

|

Top Companies |

Amazon.com Inc., Wing Aviation LLC, United Parcel Service of America, Inc., Zipline, Matternet Inc., and EHang. |

|

Market Opportunity |

Healthcare drone delivery projected at USD 1.8 Billion by 2034 |

Key Analytical Observations Supporting The Above Data:

- Rotary wing drones account for 54.3% of the market in 2025, preferred for urban last-mile delivery due to VTOL capability, precision hovering for winch delivery systems, and superior maneuverability in constrained airspace.

- Short range delivery (<25 km) is the dominant range segment at 68.2% 2025, aligned with metropolitan delivery use cases where drone corridors are being actively designated by aviation authorities in the US, EU, and Asia.

- North America holds 39.8% of the global market in 2025, led by the U.S., where the FAA's BVLOS operational waivers have enabled commercial drone delivery networks in over 50 cities by 2025.

- Asia Pacific is emerging as the fastest-growing region, driven by China's national UAV commercialization policy framework, Japan's Level 4 drone flight authorization system implemented in 2022, and India's Drone Rules 2021, creating a structured pathway for commercial operations.

- Healthcare applications represent the highest-value per-delivery segment, with temperature-controlled medical supply chains, blood product delivery to remote clinics, and emergency defibrillator delivery programs driving premium pricing.

Global Drone Package Delivery Market Overview

Drone package delivery refers to the use of unmanned aerial vehicles (UAVs) to transport parcels, medical supplies, food, and other goods directly to consumers or facilities without requiring human vehicle operators. Originally pioneered for military logistics and surveillance, commercial drone delivery has matured into a rapidly scaling civilian logistics segment, enabled by advances in battery energy density, AI-powered autonomous navigation, computer vision obstacle avoidance, and compressed regulatory approval timelines.

The market ecosystem spans drone hardware manufacturers, software platform developers, flight management system providers, vertiport and ground infrastructure operators, regulatory technology providers, and end-user logistics operators. Integration across these layers is creating a vertically consolidating industry where leading operators seek to control hardware-to-delivery stack ownership for margin optimization and quality assurance.

Macroeconomic factors, including rapid e-commerce growth (global e-commerce sales are projected to increase from USD 6.42 trillion in 2025 to USD 7.89 trillion by 2028), urban congestion reducing conventional vehicle delivery efficiency, and sustainability mandates reducing the carbon intensity of logistics operations, are primary growth catalysts. In 2025, drone delivery is expected to offer cost savings of up to 70% for light packages compared to truck deliveries.

Market Dynamics

To evaluate market opportunities, Request Sample

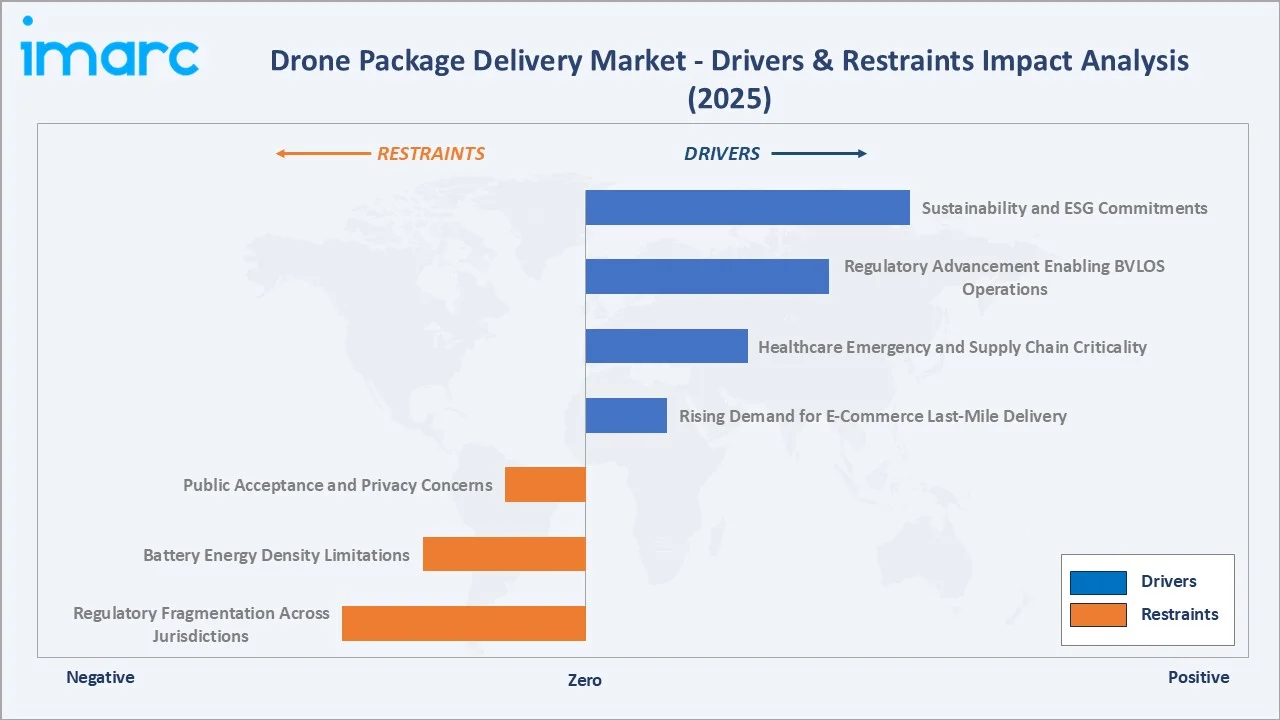

Market Drivers

- Rising Demand for E-Commerce Last-Mile Delivery: Global e-commerce GMV exceeded USD 6.3 Trillion in 2024, with last-mile delivery costs representing 53% of total logistics spend. Drone delivery reduces last-mile costs by up to 80% in eligible corridors, creating compelling economics for high-density urban areas and drone-serviceable suburban zones.

- Regulatory Advancement Enabling BVLOS Operations: The FAA's Part 135 Air Carrier certification program and the EU's U-Space framework have enabled commercial BVLOS operations in controlled corridors. Over 200 commercial drone delivery operator authorizations will have been issued globally, creating a structured operating environment that accelerates investment and deployment.

- Healthcare Emergency and Supply Chain Criticality: Drone delivery of blood products, vaccines, and emergency medications is reducing mortality rates in time-critical scenarios in documented deployments. Zipline’s drone delivery program in Rwanda has cut delivery times for blood products and helped reduce blood wastage by about 67%.

- Sustainability and ESG Commitments: Logistics operators face increasing pressure from ESG investors and corporate procurement policies to decarbonize last-mile operations. Electric drone delivery produces 84–94% fewer carbon emissions per delivery compared to diesel delivery vehicles, creating powerful incentives for adoption within corporate sustainability strategies.

These drivers reinforce a self-sustaining growth cycle, regulatory clarity drives capital deployment, which accelerates hardware cost reduction through scale, which in turn expands the economically viable delivery use cases into more geographies and applications.

Market Restraints

- Regulatory Fragmentation Across Jurisdictions: Diverging drone operating regulations across 190+ countries create compliance complexity for global operators. Inconsistent rules on BVLOS authorization, maximum payload limits, flight corridor designations, and noise standards increase per-market entry costs by 25–40% and delay commercialization timelines.

- Battery Energy Density Limitations: Conventional LiPo batteries offer ≤250 Wh/kg, limiting drones to a range of 25–40 km with a 2 kg payload. This constrains the addressable delivery geography and necessitates costly recharging/swapping infrastructure investment in hub-and-spoke deployment models.

- Public Acceptance and Privacy Concerns: Surveys across North America and Europe indicate that 34–41% of consumers express moderate-to-high privacy concerns about drone delivery flight paths over residential areas. Noise complaints from rotary-wing drones in urban neighborhoods have resulted in operational restrictions in several municipalities.

Market Opportunities

- Healthcare Logistics Modernization: The global pharmaceutical logistics market is projected to grow at a CAGR of 5.96% from 2025 to 2033, with cold chain and time-critical supply segments representing high-value drone-addressable opportunities. Governments in 45+ countries are actively funding drone delivery pilots for rural health facility resupply, representing an incremental USD 1.8 Billion opportunity by 2034.

- Suburban and Rural Market Expansion: While urban deployments dominate current revenue, suburban and rural markets represent significant untapped potential. Low population density areas where conventional delivery vehicles face long route times and high per-stop costs represent the most favorable economics for fixed-wing long-range drone delivery systems.

- Autonomous Urban Air Traffic Management (UTM): Investment in drone UTM software platforms, including NASA's UAS Traffic Management initiative and EASA's U-Space, creates a digital infrastructure layer enabling coordinated fleet operations at scale. UTM platform providers represent a high-margin software opportunity projected at USD 3.1 Billion by 2034.

Market Challenges

- Airspace Integration Complexity: Coordinating commercial drone delivery corridors with existing manned aviation, military restricted zones, and emerging urban air mobility (UAM) vehicle operations requires sophisticated airspace management. Conflicts between overlapping airspace users create safety and operational planning challenges that slow corridor authorization timelines

- Cybersecurity and Signal Jamming Vulnerability: Commercial delivery drones relying on GPS navigation and wireless command links are vulnerable to GPS spoofing, signal jamming, and cyberattack targeting flight management systems. The European Aviation Safety Agency (EASA) has mandated cybersecurity certification requirements for commercial drone operators from 2025, adding compliance cost burdens.

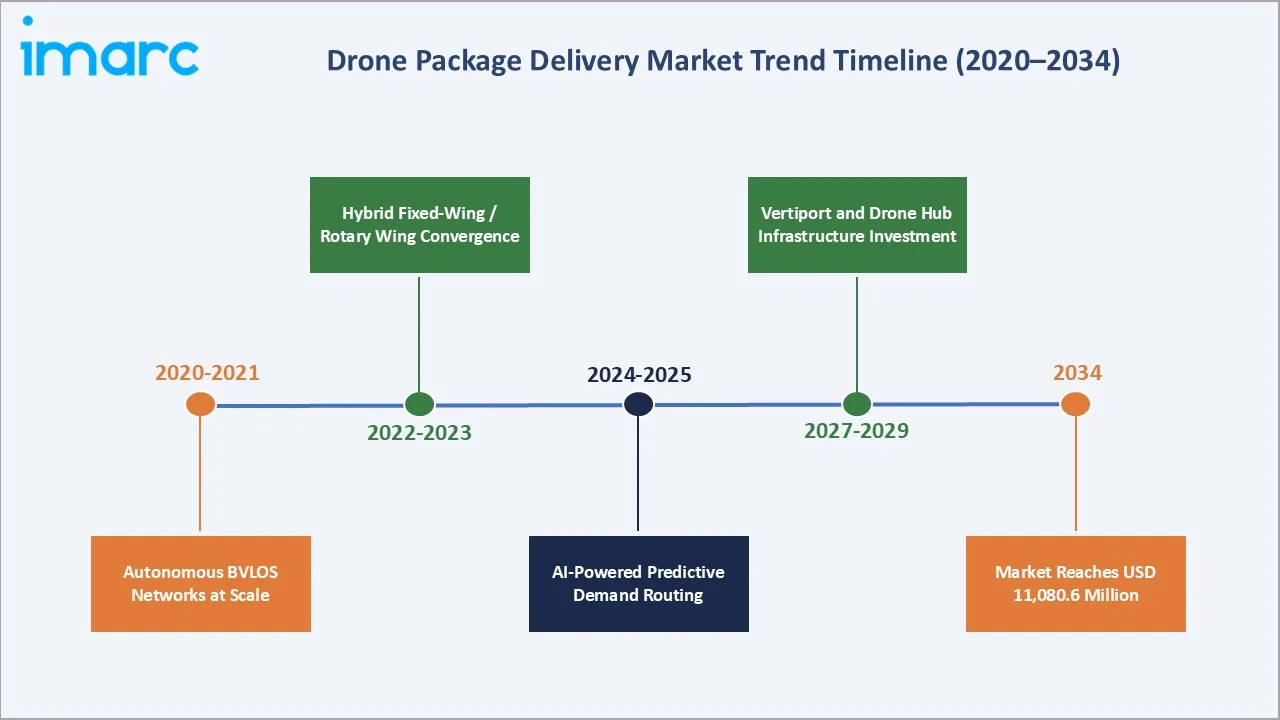

Emerging Market Trends

1. Autonomous BVLOS Networks at Scale

Commercial drone operators are transitioning from single-operator supervised flights to fully autonomous BVLOS networks managed by AI-powered fleet management platforms. In August 2024, DroneUp, an autonomous drone delivery company, reached a new industry milestone by completing 500 deliveries in a single day, showcasing significant improvements in delivery scale and efficiency.

2. Hybrid Fixed-Wing/Rotary Wing Convergence

Hybrid VTOL drones combining fixed-wing cruise efficiency with rotary wing landing precision are the fastest-growing hardware segment (20.8% CAGR). Companies including Joby Aviation and Archer Aviation are adapting urban air mobility technology for cargo delivery, while Volansi raised $50 million in Series B funding to expand its long‑range, VTOL drone delivery services for commercial and defense applications.

3. AI-Powered Predictive Demand Routing

Integration of machine learning demand forecasting with drone fleet management systems enables pre-positioning of goods at micro-fulfilment centers in anticipation of consumer orders. This reduces delivery time from order placement to doorstep to under 10 minutes for high-frequency consumer goods, creating a structural competitive advantage over conventional logistics in speed-sensitive categories.

4. Vertiport and Drone Hub Infrastructure Investment

Global investment in vertiport and drone hub infrastructure accounted for high investments, with major airports, logistics REITs, and urban real estate developers incorporating drone landing/charging infrastructure into new construction. This physical infrastructure investment is a leading indicator of sustained market expansion, creating operational capacity that anchors multi-year delivery contracts.

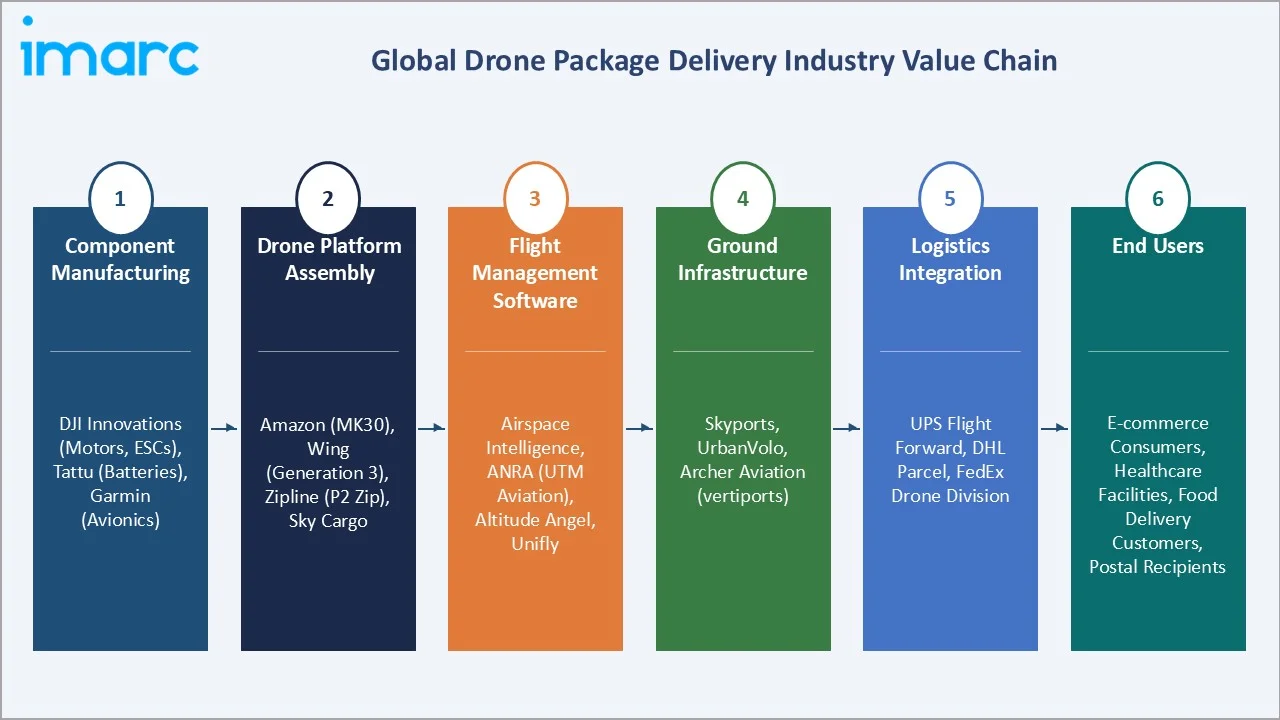

Industry Value Chain Analysis

The drone package delivery value chain spans raw material and component supply through end-consumer delivery execution, with each stage populated by specialized operators whose performance directly influences system reliability, delivery economics, and regulatory compliance.

|

Stage |

Key Players / Examples |

|

Component Manufacturing |

DJI (motors, ESCs), Tattu (batteries) |

|

Drone Platform Assembly |

Amazon.com Inc. (MK30), Wing Aviation LLC, Zipline (P2 Zip) |

|

Flight Management Software |

Unifly, ANRA Technologies |

|

Ground Infrastructure |

Amazon's PADDC model, Wing Nests, and Zipline |

|

Logistics Integration |

UPS Flight Forward, DHL Group, FedEx Express (Elroy Air partnership) |

|

End Users |

E-commerce consumers, healthcare facilities, food delivery customers, postal recipients |

Technology Landscape in the Drone Package Delivery Industry

Drone Airframe and Multi-Rotor Propulsion Technologies

Fixed-wing hybrid VTOL (Vertical Take-Off and Landing) airframes have emerged as the dominant platform architecture for mid-range package delivery. Wing (a subsidiary of Alphabet) and Zipline’s new commercial delivery drone, touted as the world’s fastest, can reach speeds up to 128 km/h (about 80 mph), dramatically accelerating autonomous delivery and ranges of 25–60 km per charge, significantly outperforming conventional octocopter platforms on energy efficiency per kilometer.

Autonomous Navigation, AI, and Computer Vision

Zipline's Platform 2 (P2 Zip), launched in 2023, incorporates simultaneous localization and mapping (SLAM) algorithms fused with real-time LiDAR point-cloud data to achieve precision hover accuracy of ±0.3 meters over designated drop zones. Wing’s detect-and-avoid (DAA) system uses stereo optical cameras combined with acoustic sensing to classify and avoid manned aircraft, birds, and power lines at ranges exceeding 200 meters, meeting FAA BVLOS (Beyond Visual Line of Sight) operational requirements.

Unmanned Traffic Management (UTM) and Connectivity Infrastructure

UTM platforms form the critical digital backbone enabling scalable commercial drone operations, providing real-time situational awareness, conflict detection, and dynamic re-routing across shared airspace. NASA’s UTM research program and the EU’s U-Space regulatory framework (enacted across all EU member states from January 2023) have established the standards architecture that commercial UTM providers have commercialized into software-as-a-service platforms.

Battery Technology, Hybrid Power, and Range Extension

Lithium-ion battery energy density, the principal constraint on drone range and payload capacity, has advanced from approximately 200 Wh/kg in 2019 to around 350 Wh/kg, with commercial cells deployed in delivery drones as of 2025, with solid-state lithium-ceramic prototypes from Toyota and QuantumScape targeting 400+ Wh/kg by 2027.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Solution | Service | 🔒 | 2025 |

| Duration | Short Duration (<30 minutes) | 🔒 | 2025 |

| Range | Short Range (<25 kilometres) | 68.2% | 2025 |

| Capacity | <2 kilograms | 🔒 | 2025 |

| Type | Rotary Wing | 54.3% | 2025 |

| End-Use Industry | E-Commerce | 🔒 | 2025 |

| Region | North America | 39.8% | 2025 |

By Type

To access detailed market analysis, Request Sample

Rotary wing drones dominate the global market due to their vertical takeoff and landing capability, which eliminates the need for dedicated runway infrastructure and enables precise urban delivery to doorsteps, rooftops, or designated landing pads. Multi-rotor configurations (quadcopters, hexacopters, octocopters) provide redundant propulsion systems that meet aviation safety standards for flight over populated areas.

Fixed wing drones offer substantially superior energy efficiency in cruise flight compared to rotary wing designs, enabling longer ranges (50–200 km) at higher speeds with heavier payloads. These characteristics make them ideal for rural healthcare supply chains, inter-island delivery networks, and extensive geographic coverage in regions with dispersed population centers.

By Range

Short range delivery dominates with a 68.2% market share, reflecting the concentration of commercial drone delivery deployments in urban and suburban environments where high order density justifies hub-and-spoke drone infrastructure investment. The majority of commercial drone delivery authorizations issued by the FAA, EASA, and CAAC target corridors of 5–20 km radius from micro-fulfilment centers.

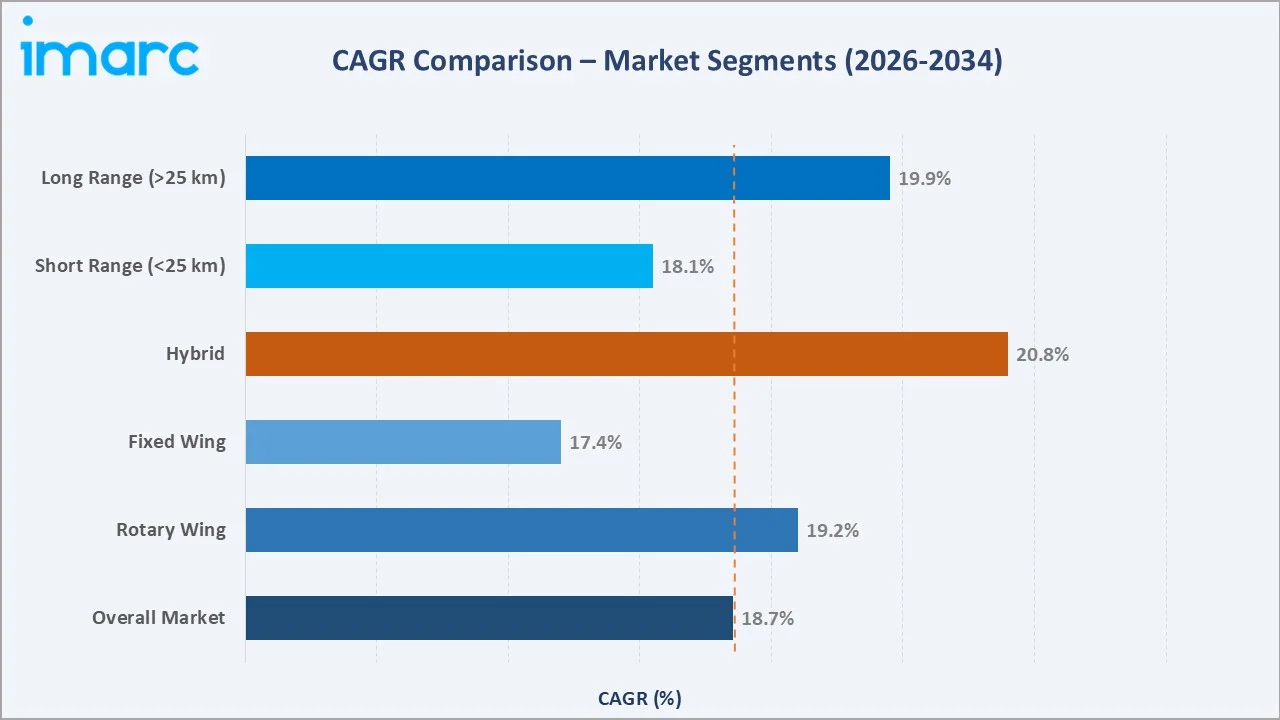

Long range delivery, while representing a smaller current share, is the higher-growth sub-segment driven by critical healthcare logistics applications and the economics of rural delivery, where conventional vehicle costs per stop are prohibitively high. The segment is expected to grow at 19.9% CAGR through 2034, with fixed-wing and hybrid VTOL platforms driving range capability expansion to 100+ km for commercial payloads.

Regional Insights

North America's market leadership is underpinned by the world's most commercially active drone delivery operators and the FAA's progressive waiver-based authorization framework that has enabled commercial operations ahead of other major jurisdictions. Amazon Prime Air's delivery service, Wing's suburban operations, and UPS Flight Forward's FAA Air Carrier certification collectively represent the world's most scaled commercial drone delivery infrastructure.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

North America |

39.8% |

E-commerce scale, FAA BVLOS waivers, Amazon/Wing deployments |

FAA Part 135 Air Carrier; LAANC corridor system |

|

Europe |

26.4% |

U-Space framework, healthcare pilots, and strong sustainability mandates |

EASA cybersecurity reqs; U-Space 2023 |

|

Asia Pacific |

23.7% |

China UAV policy, Japan Level 4, India Drone Rules 2021 |

CAAC national UAV corridors; JCAB Level 4 |

|

Other Regions |

10.1% |

Healthcare access gaps, rural infrastructure deficits, and NGO-funded pilots |

GCAA (UAE); Rwanda CAA; WHO partnerships |

Asia Pacific is the fastest-growing region, driven by China's comprehensive national UAV commercialization policy, Japan's Level 4 autonomous flight authorization system implemented in December 2022, and India's Drone Rules 2021, creating a structured pathway for commercial operations. EHang's autonomous aerial vehicle platform has received Chinese Civil Aviation Administration (CAAC) type certification, making China the first country to certify a fully autonomous cargo drone for commercial operations.

Competitive Landscape

The global drone package delivery market exhibits a moderately fragmented structure, characterized by the presence of large technology platform operators, specialized drone delivery pure-plays, and established logistics companies expanding into UAV delivery. The top five operators collectively hold approximately 42–48% of global market revenue in 2025, with a long tail of regional operators and technology providers accounting for the remainder.

|

Company Name |

Service Brand |

Market Position |

Core Strength |

|

Amazon.com Inc. |

Amazon Prime Air |

Market Leader |

Largest e-commerce ecosystem; MK30 drone; multi-city deployment; FAA Part 135 Air Carrier certification |

|

Wing Aviation LLC. |

Wing |

Market Leader |

Technology-first platform; autonomous multi-drone fleet; Gen 3 drone; global regulatory engagement |

|

United Parcel Service of America, Inc. |

UPS Flight Forward |

Strong Challenger |

First Standard Part 135 Air Carrier certification; hospital campus delivery; extensive logistics network integration |

|

Zipline |

Zipline |

Strong Challenger |

Global healthcare delivery pioneer; P2 Zip fixed-wing platform; 80 km radius operations; Rwanda, Ghana, US deployments |

|

Matternet Inc. |

Matternet |

Challenger |

Urban healthcare logistics specialist; Swiss hospital network operator; regulatory compliance expertise |

|

EHang |

EHang Cargo |

Challenger |

China market leader; CAAC type certification; autonomous aerial vehicle pioneer; logistics corridor expansion |

Key Company Profiles

Amazon.com Inc.

Amazon.com Inc., headquartered in Seattle, Washington, operates Amazon Prime Air, the commercially scaled drone delivery service. The company's MK30 drone delivers packages up to 5 pounds to customers in under 60 minutes. Amazon holds FAA Part 135 Air Carrier certification, enabling commercial BVLOS operations.

- Product Portfolio: Prime Air delivery service, MK30 drone platform, autonomous flight management system, and micro-fulfilment center integration.

- Recent Developments: Expanded Prime Air to 5+ US cities in 2024–2025; planning operations under Darlington for UK operations and received CAA approval; introduced MK30 with approx. 25% reduced noise signature versus predecessor.

- Strategic Focus: Urban density expansion; international regulatory market entry; integration of drone delivery with same-day fulfilment for Amazon Fresh and pharmacy categories. Zipline International Inc.

Zipline

Zipline, headquartered in South San Francisco, California, operates the world's largest commercial drone delivery network by delivery volume, with operations across Rwanda, Ghana, Nigeria, the Ivory Coast, Kenya, Japan, and the U.S.

- Product Portfolio: P2 Zip hybrid VTOL fixed-wing drone, platform dock delivery system, and cold chain-certified payload containment.

- Recent Developments: Launched US consumer delivery operations in Salt Lake City and expanded to 10 US markets by 2025; completed 1 millionth commercial delivery in 2024; introduced new Zip platform with silent propulsion and precision landing capability.:

- Strategic Focus: US consumer market scaling; healthcare system integration; platform dock deployment enabling 60-second delivery precision; international emerging market expansion.

Wing Aviation LLC.

Wing Aviation LLC. headquartered in Palo Alto, California, it operates commercial drone delivery services in Australia, Finland, Ireland, and the U.S.

- Product Portfolio: Wing Cloud flight management platform, autonomous BVLOS operations system.

- Recent Developments: Expanded to 5 Australian cities serving 250,000+ households; partnered with Walmart and DoorDash for a U.S. retail delivery network.

- Strategic Focus: Regulatory framework development; suburban density expansion; retail partner ecosystem growth; Wing Cloud UTM platform commercialization.

Market Concentration Analysis

The drone package delivery market exhibits moderate concentration at the operator level, with the top five commercial delivery platforms holding approximately 42–48% of total revenue in 2025. However, the hardware supply chain (drone component manufacturing, battery technology, flight management software) is significantly more fragmented, with 500+ active technology vendors competing across the ecosystem.

Consolidation activity is accelerating, driven by regulatory compliance costs (FAA/EASA certification processes), the capital intensity of building drone delivery infrastructure, and the advantages of scale in autonomous fleet management. Between 2021 and 2025, significant M&A and strategic partnership transactions reshaped the competitive landscape, including Walmart's partnership with Wing and UPS's integration of drone delivery into its healthcare logistics division.

Investment & Growth Opportunities

Fastest Growing Segments

Hybrid VTOL drone platforms (20.8% CAGR), healthcare-specific delivery networks (21.3% CAGR), and autonomous UTM software platforms (22% CAGR) represent the three highest-growth investment vectors through 2034. Together, these segments address a combined total addressable market of approximately USD 3.9 Billion by 2030.

Emerging Market Expansion

Sub-Saharan Africa, Southeast Asia, and South Asia collectively represent an incremental USD 1.2 Billion drone delivery opportunity by 2034. Entry via WHO-partnered healthcare delivery programs, alignment with national e-commerce digital economy initiatives, and joint ventures with local logistics operators are preferred investment modalities for international operators.

Venture and Institutional Investment Trends

- Key investment themes include vertiport infrastructure REITs, cold chain-certified payload systems, AI-powered autonomous conflict avoidance technology, and drone delivery insurance and liability management platforms.

- Institutional investors and sovereign wealth funds are increasingly targeting vertically integrated drone delivery platforms—combining hardware manufacturing, software development, regulatory certification, and logistics operations—seeking USD 500 Million–USD 2 Billion platform acquisitions.

Future Market Outlook (2026-2034)

The global drone package delivery market is positioned for sustained, high-compound growth through 2034. From a base of USD 2,079.8 Million in 2025, the market is projected to reach USD 11,080.6 Million by 2034, representing total incremental value creation of USD 9,000.8 Million over the forecast decade.

Regulatory evolution, particularly the FAA's anticipated rulemaking on BVLOS operations (expected 2026), EASA's U-Space full deployment across EU member states, and China's national UAV corridor network completion, will be the primary catalysts unlocking mass-market deployment. Markets that achieve regulatory clarity by 2027 are positioned to capture disproportionate first-mover market share through infrastructure investment and operator experience advantages.

Long-term, the market's trajectory is tied to three structural macro-themes: e-commerce penetration acceleration (creating relentless demand for faster, cheaper last-mile logistics), urbanization creating high-density delivery corridors that optimize drone economics, and technological convergence of AI, battery technology, and telecommunications infrastructure enabling reliable autonomous BVLOS operations at scale.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including drone delivery operators, aviation regulators, aerospace hardware manufacturers, logistics technology developers, healthcare procurement officers, and e-commerce supply chain executives across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, FAA/EASA/CAAC regulatory filings, drone industry association publications (AUVSI, GUTMA), industry databases (Drone Industry Insights, PitchBook), trade publications (Commercial UAV News, DroneLife), and publicly available financial data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators (e-commerce GMV growth, urbanization rates, healthcare expenditure), regulatory adoption timelines, drone hardware cost reduction curves (Wright's Law applied to UAV manufacturing), and historical market evolution data.

Drone Package Delivery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solutions Covered | Service, Platform, Infrastructure, Software |

| Durations Covered | Short Duration (<30 minutes), Long Duration (>30 minutes) |

| Ranges Covered | Short Range (<25 kilometers), Long Range (>25 kilometers) |

| Capacities Covered | <2 kilograms, 2-5 kilograms, >5 kilograms |

| Types Covered | Rotary Wing, Fixed Wing, Hybrid |

| End Use Industries Covered | E-Commerce, Healthcare, Food and Beverages, Postal Services, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Other Regions |

| Countries Covered | United States, Canada, United Kingdom, Germany, France, China, Australia, Japan |

| Companies Covered | Amazon.com Inc., Wing Aviation LLC., United Parcel Service of America, Inc., Zipline, Matternet Inc., EHang, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the drone package delivery market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global drone package delivery market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the drone package delivery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Drone Package Delivery Market Report

The global drone package delivery market reached USD 2,079.8 Million in 2025 and is projected to reach USD 11,080.6 Million by 2034.

The market is expected to grow at a CAGR of 18.71% during the forecast period from 2026 to 2034, supported by regulatory approvals, e-commerce expansion, and UAV technology advances.

North America leads with a 39.8% revenue share in 2025, driven by FAA regulatory leadership, Amazon Prime Air and Wing commercial deployments, and high e-commerce density creating viable drone delivery economics in urban corridors.

Rotary wing drones dominate the type segment with a 54.3% share in 2025. Their VTOL capability, precision delivery characteristics, and suitability for urban deployment environments make them the preferred platform for commercial last-mile delivery operations.

Short Range (<25 km) holds the largest share at 68.2% in 2025, driven by the concentration of commercial deployments in urban and suburban delivery corridors where high order density supports drone hub infrastructure investment.

Key players include Amazon.com Inc., Wing Aviation LLC., United Parcel Service of America, Inc., Zipline, Matternet Inc., and EHang.

Key growth drivers include rising e-commerce last-mile delivery demand, BVLOS regulatory approvals enabling commercial scaling, healthcare logistics efficiency requirements, and ESG mandates driving carbon reduction in logistics operations.

Key challenges include regulatory fragmentation across jurisdictions, battery energy density limitations constraining delivery range, public acceptance and privacy concerns, and cybersecurity vulnerabilities requiring investment in hardened communication and navigation systems.

Significant investment opportunities exist in hybrid VTOL drone platforms, autonomous UTM software, healthcare-specific delivery networks, vertiport infrastructure development, and emerging market expansion across Sub-Saharan Africa, Southeast Asia, and South Asia.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)