Drones Market Size, Share, Trends and Forecast by Type, Component, Payload, Point of Sale, End-Use Industry, and Region, 2026-2034

Drones Market Size, Share, Trends & Forecast (2026-2034)

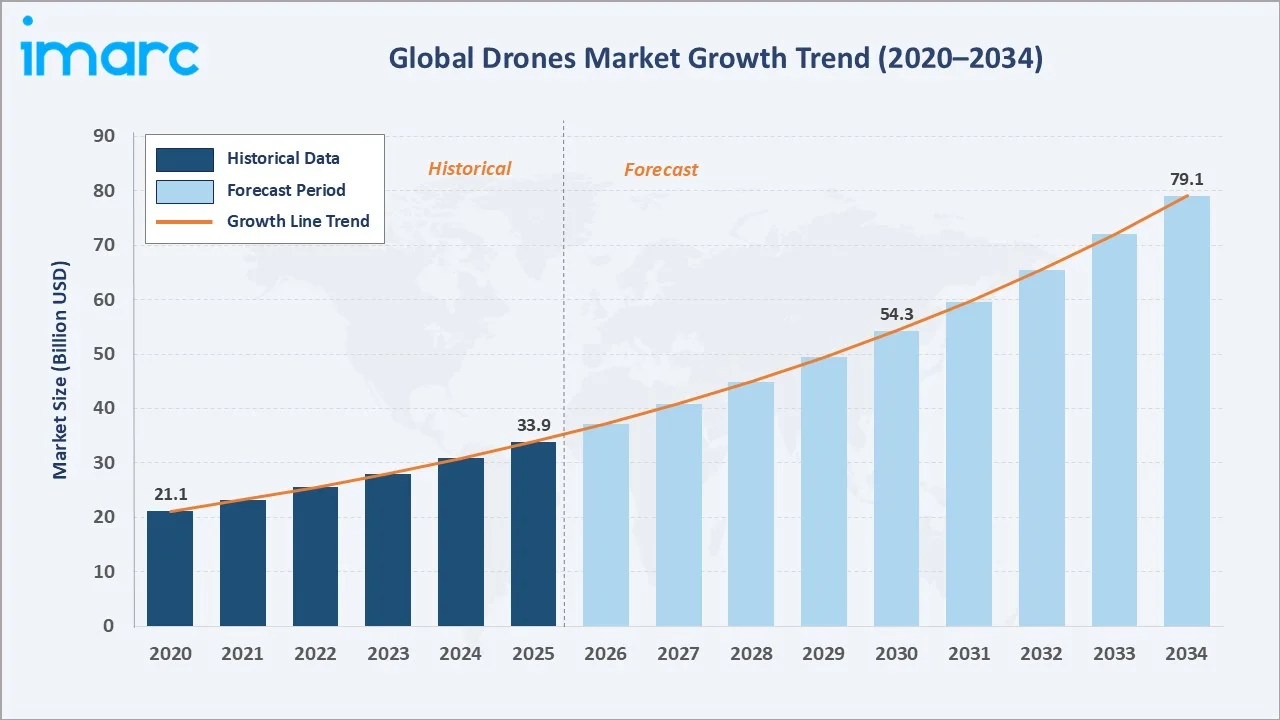

The global drones market reached USD 33.9 Billion in 2025 and is projected to reach USD 79.1 Billion by 2034, growing at a CAGR of 9.89% during 2026-2034. Increasing AI adoption for autonomous navigation, rising defense and commercial sector demand, and accelerating integration of drones across logistics, agriculture, infrastructure inspection, and smart city applications are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 33.9 Billion |

|

Forecast Market Size (2034) |

USD 79.1 Billion |

|

CAGR (2026-2034) |

9.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (48.4% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

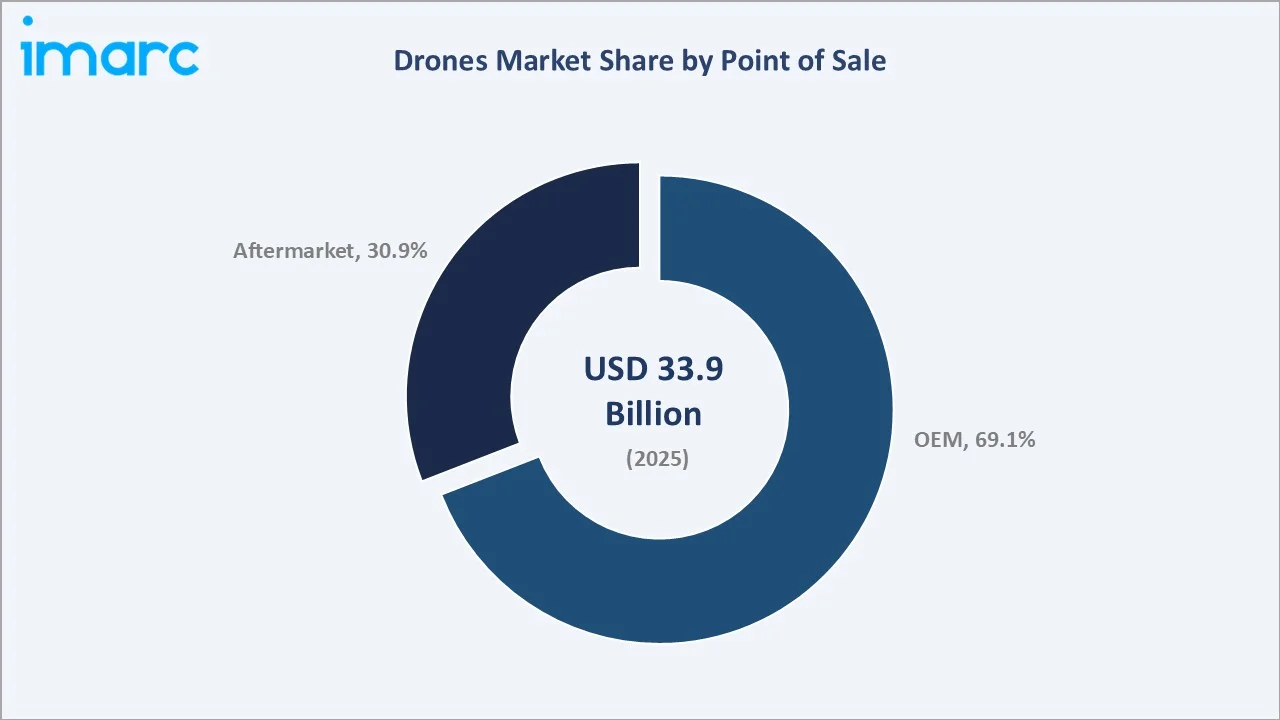

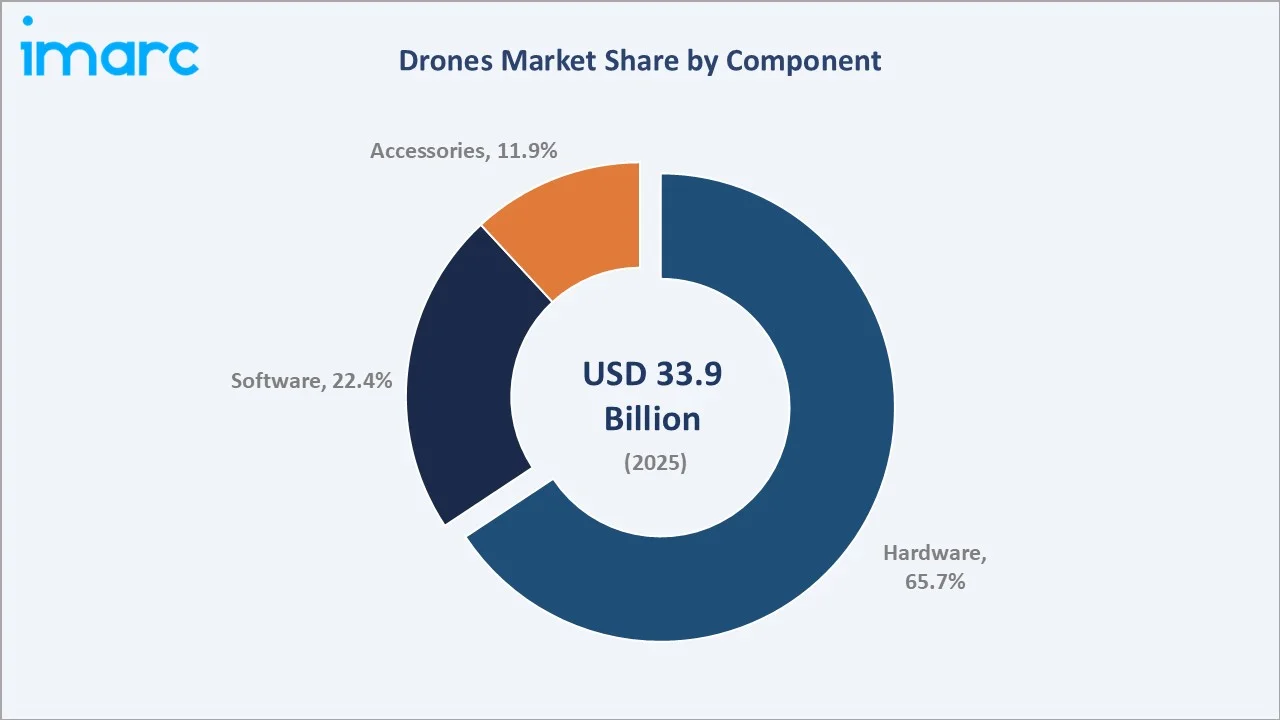

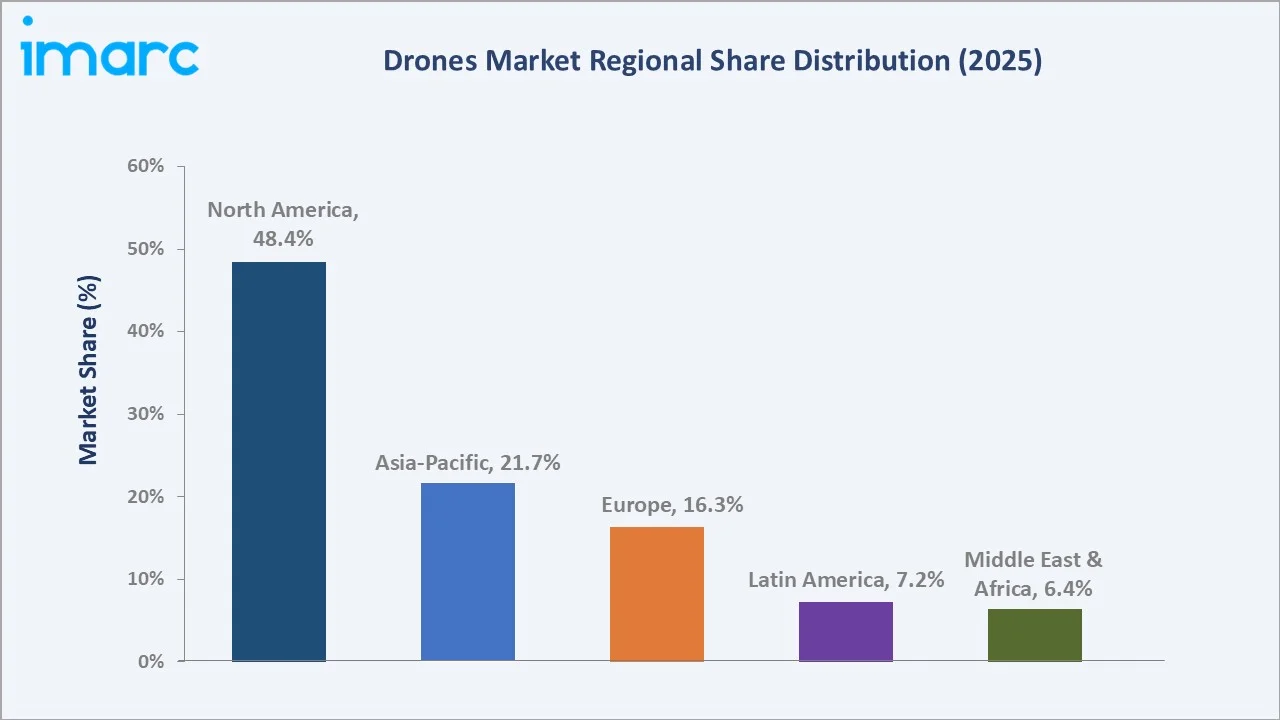

North America dominates, holding a 48.4% market share in 2025, while OEM sales channels lead with a 69.1% share. Hardware remains the dominant component at 65.7%. Drones offer compelling operational advantages over traditional methods, including real-time aerial data capture, cost reduction in large-area monitoring, and access to hazardous or remote environments.

To get more information on this market, Request Sample

With applications spanning defense and military, commercial logistics, agricultural monitoring, infrastructure inspection, and consumer recreational use, the market is expected to continue expanding, supported by innovations in AI-powered autonomous flight, beyond visual line of sight (BVLOS) regulatory frameworks, and increasing adoption in regions investing aggressively in digital infrastructure.

Executive Summary

The global drones market is on a sustained growth path, underpinned by escalating defense modernization programs, rapid commercial adoption across industries, and the progressive regulatory liberalization of airspace frameworks that are enabling BVLOS operations at scale. The market reached USD 33.9 Billion in 2025 and is forecast to surpass USD 79.1 Billion by 2034, reflecting a healthy CAGR of 9.89% over the forecast period.

North America leads globally with a 48.4% share in 2025, driven by the U.S. defense procurement pipeline, FAA's evolving BVLOS regulatory framework, and widespread commercial adoption across agriculture, construction, energy inspection, and last-mile logistics. Asia-Pacific, at 21.7%, is the fastest-growing region, with China's dominant manufacturing position through DJI, combined with India's rapidly expanding civilian drone ecosystem and government-backed smart city programs, generating compelling growth momentum.

OEM channels command a 69.1% share, reflecting the dominance of direct procurement in defense, enterprise, and agricultural applications. Hardware retains a 65.7% component share, anchored by airframe, propulsion, and sensor hardware manufacturing, while software at 22.4% is the fastest-growing component, driven by AI-powered autonomy platforms, fleet management software, and data analytics applications.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Point of Sale) |

OEM – 69.1% share (2025) |

|

Second Largest (Point of Sale) |

Aftermarket – 30.9% share (2025) |

|

Dominant Component |

Hardware – 65.7% share (2025) |

|

Leading Region |

North America – 48.4% share (2025) |

|

Fastest Growing Region |

Asia-Pacific (rapid urbanization + defense investment) |

|

Top Companies |

DJI, Boeing, Parrot Drones SAS, Skydio, and Delair |

Key Analytical Observations Supporting The Above Data:

- OEM channels account for 69.1% of the drones market in 2025, driven by structured procurement processes for defense UAV systems, enterprise agricultural drone fleets, and commercial inspection platforms where direct manufacturer relationships ensure technical support, customization, and regulatory compliance.

- Aftermarket channels represent 30.9% (2025), growing at approximately 10.8% CAGR as drone-as-a-service (DaaS) models, software subscription upgrades, and replacement component markets expand with the growing installed base of commercial and consumer drones globally.

- Hardware dominates with 65.7% of the market in 2025, reflecting the capital-intensive nature of drone airframe, propulsion, and sensor manufacturing. However, software at 22.4% is growing fastest, driven by AI autonomy platforms, route planning software, and cloud-based fleet analytics, generating high-margin recurring revenue.

- North America holds 48.4% of global market revenue in 2025, with the U.S. Department of Defense remaining the world's largest single drone procurer. The FAA's expanding BVLOS authorization framework is accelerating commercial adoption, particularly in logistics, energy inspection, and public safety applications.

Global Drones Market Overview

The global drones market encompasses unmanned aerial vehicles (UAVs) across all categories, from sub-250g consumer drones to large military MALE (Medium Altitude Long Endurance) and HALE (High Altitude Long Endurance) systems, including the hardware platforms, onboard and ground-based software, payload systems, and associated aftermarket services. The ecosystem spans drone manufacturers, component suppliers, software developers, regulatory bodies, service operators, and end-user industries, including defense, agriculture, construction, logistics, energy, and public safety.

Macroeconomic factors, including rising global defense budgets, accelerating digital transformation across industrial sectors, and the growing economic case for drone-based operational cost reduction, are primary growth catalysts. Drones deliver significant advantages over traditional alternatives, replacing helicopter patrols, manual crop surveys, cable inspections, and ground vehicle deliveries with systems that reduce operational cost, eliminate personnel safety risks, and generate superior data quality at lower cost per mission, creating structural demand that is largely independent of economic cyclicality.

Market Dynamics

To evaluate market opportunities, Request Sample

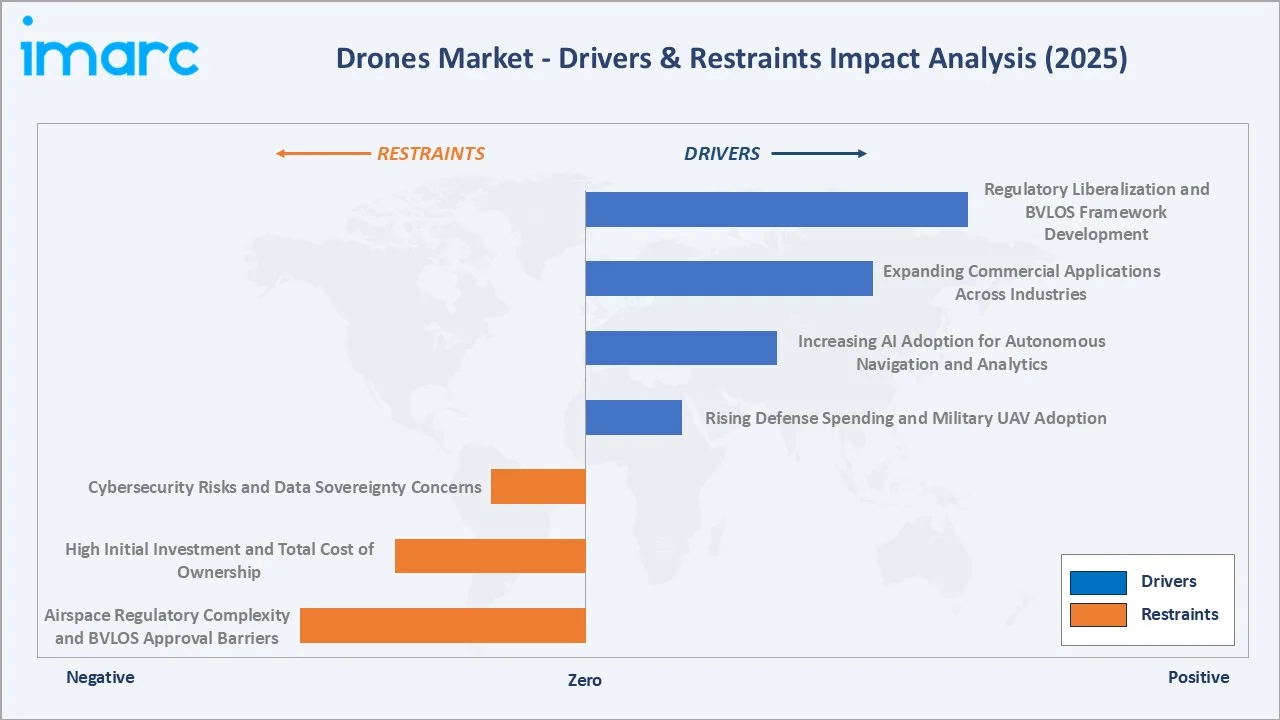

Market Drivers

- Rising Defense Spending and Military UAV Adoption: Global defense budgets have increased in response to geopolitical tensions, with NATO Allies committed to dedicating 5% of their Gross Domestic Product (GDP) annually to core defense needs and defense- and security-related expenditures by 2035.

- Increasing AI Adoption for Autonomous Navigation and Analytics: AI-powered autonomy capabilities, including AI obstacle avoidance, path planning, swarm coordination, and real-time aerial analytics, have transformed drones from remotely piloted vehicles into fully autonomous systems. Skydio's AI autonomy stack, deployed across U.S. military and enterprise inspection clients, exemplifies the premium value generated by AI-differentiated platforms that operate safely without real-time human oversight.

- Expanding Commercial Applications Across Industries: Agriculture, construction, energy, telecommunications, and logistics collectively represent a multi-billion-dollar commercial drone opportunity. According to the FAA, the U.S. commercial drone fleet is projected to reach 112 million units by 2028.

- Regulatory Liberalization and BVLOS Framework Development: Progressive regulatory reform by the FAA (U.S.), EASA (Europe), CASA (Australia), and DGCA (India) is enabling BVLOS operations, the prerequisite for scalable commercial delivery, infrastructure inspection at range, and large-area agricultural monitoring.

Market Restraints

- Airspace Regulatory Complexity and BVLOS Approval Barriers: Despite progressive liberalization, obtaining BVLOS operational approvals remains time-consuming and jurisdiction-specific. Diverging standards across the FAA, EASA, and national aviation authorities create compliance cost burdens for operators seeking to scale across geographies.

- High Initial Investment and Total Cost of Ownership: Enterprise and defense-grade drone platforms carry significant upfront acquisition costs, from USD 50,000 for commercial inspection drones to hundreds of millions for advanced military systems. Hidden ongoing costs, including software subscriptions, maintenance, pilot training, insurance, and regulatory compliance, create total cost of ownership barriers for small and mid-market commercial operators.

- Cybersecurity Risks and Data Sovereignty Concerns: The integration of drones with cloud-based data platforms raises significant cybersecurity and data sovereignty concerns, particularly for government and critical infrastructure applications. The U.S. NDAA's restrictions on the procurement of Chinese-manufactured drones reflect the growing geopolitical dimension of drone supply chain security, reshaping procurement patterns globally.

Market Opportunities

- Drone Delivery and Last-Mile Logistics: E-commerce and pharmaceutical delivery applications represent the highest near-term commercial opportunity, with Amazon Prime Air, UPS Flight Forward, and Wing (Alphabet) having received FAA approval for commercial drone delivery operations.

- Smart City Infrastructure and Urban Air Mobility (UAM): Governments worldwide are integrating drone operations into smart city frameworks for traffic monitoring, emergency response, infrastructure inspection, and environmental monitoring. The convergence of drone corridors, UTM (Unmanned Traffic Management) systems, and 5G connectivity is enabling scalable urban drone operations.

- Emerging Market Agricultural and Infrastructure Adoption: Asia-Pacific and Latin America collectively represent an incremental USD 8 billion drone opportunity by 2030 through agricultural modernization, infrastructure inspection in remote regions, and expanding digital economy investments. Government subsidy programs for drone-assisted precision agriculture in India, China, and Brazil are driving accelerated adoption among commercial farming operators.

Market Challenges

- Counter-Drone Technologies and Restricted Airspace Management: The proliferation of commercial drones is driving investment in counter-UAV (C-UAV) technologies by governments and critical infrastructure operators, creating complex airspace management challenges. Drone operators must navigate increasingly dense restricted airspace zones around airports, military installations, and urban critical infrastructure, limiting operational flexibility and increasing flight planning complexity.

- Supply Chain Disruptions and Component Geopolitical Risk: Drone manufacturing is highly dependent on advanced semiconductors, rare earth materials, and precision sensors concentrated in specific geographies. NDAA restrictions on Chinese-sourced components create procurement risk and cost pressure for non-Chinese manufacturers seeking to scale production of NDAA-compliant platforms for U.S. government procurement.

Emerging Market Trends

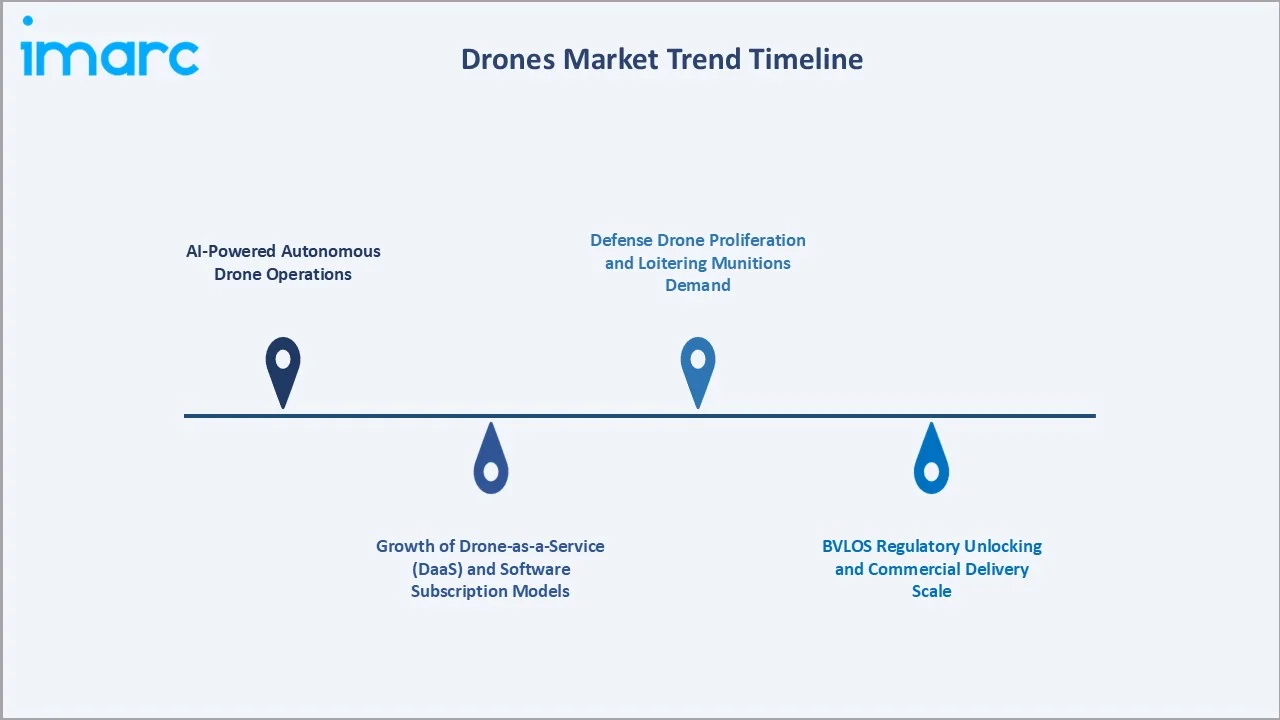

1. AI-Powered Autonomous Drone Operations

The market is transitioning from remotely piloted to fully autonomous drone operations enabled by AI. Skydio's AI autonomy stack, deployed across U.S. Army reconnaissance programs and enterprise infrastructure inspection clients, demonstrates AI's capacity to enable collision-free flight in GPS-denied, complex environments without real-time pilot input. Machine learning models trained on billions of flight data points are enabling predictive maintenance, dynamic route optimization, and real-time anomaly detection during inspection missions.

2. Growth of Drone-as-a-Service (DaaS) and Software Subscription Models

The aftermarket segment (30.9% share, growing at 10.8% CAGR) is being reshaped by the emergence of drone-as-a-service models where operators access drone capabilities, hardware, software, pilots, and data analytics as a bundled subscription rather than outright hardware purchase. Terra Drone Corp.'s industrial DaaS platform and Delair's analytics-as-a-service offering exemplify this transition.

3. BVLOS Regulatory Unlocking and Commercial Delivery Scale

FAA's Pathfinder and BEYOND programs have established operational precedents for commercial BVLOS delivery, infrastructure inspection, and emergency response applications. EASA's U-space regulation creates a structured European BVLOS framework from 2025 onward. As BVLOS approvals standardize, commercial delivery and large-area inspection applications will see exponential adoption growth, materially accelerating the overall market expansion trajectory.

4. Defense Drone Proliferation and Loitering Munitions Demand

Ukraine produced over 2 million drones domestically in 2024 and demonstrated the strategic value of drone swarms in contested airspace. AeroVironment's Switchblade 300 and 600 loitering munitions have gained international prominence, while NATO countries are dramatically increasing tactical UAV budget allocations.

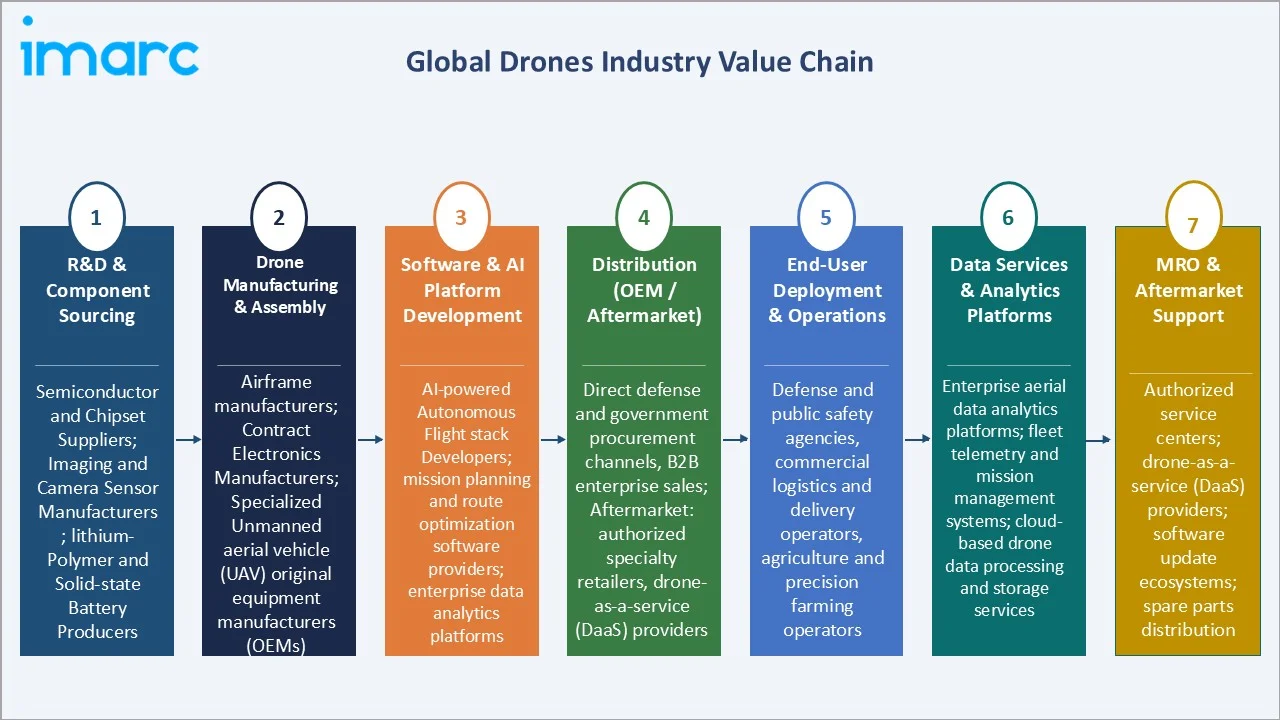

Industry Value Chain Analysis

The drones' value chain spans raw component sourcing through aftermarket service delivery, with each stage populated by specialized operators whose performance directly influences platform capability, cost competitiveness, regulatory compliance, and end-user operational outcomes.

|

Stage |

Key Players / Examples |

|

R&D & Component Sourcing |

Semiconductor and chipset suppliers; imaging and camera sensor manufacturers; lithium-polymer and solid-state battery producers |

|

Drone Manufacturing & Assembly |

Airframe manufacturers; contract electronics manufacturers; specialized unmanned aerial vehicle (UAV) original equipment manufacturers (OEMs) |

|

Software & AI Platform Development |

AI-powered autonomous flight stack developers; mission planning and route optimization software providers; enterprise data analytics platforms |

|

Distribution (OEM / Aftermarket) |

Direct defense and government procurement channels, B2B enterprise sales; Aftermarket: authorized specialty retailers, drone-as-a-service (DaaS) providers |

|

End-User Deployment & Operations |

Defense and public safety agencies, commercial logistics and delivery operators, agriculture and precision farming operators |

|

Data Services & Analytics Platforms |

Enterprise aerial data analytics platforms; fleet telemetry and mission management systems; cloud-based drone data processing and storage services |

|

MRO & Aftermarket Support |

Authorized service centers; drone-as-a-service (DaaS) providers; software update ecosystems; spare parts distribution |

Technology Landscape in the Drones Industry

AI and Machine Learning for Autonomous Navigation

Skydio’s Autonomy system uses advanced AI‑powered onboard software and multiple navigation cameras to enable drones to see, understand, and navigate complex environments in real time without manual control. Moreover, Qualcomm Technologies introduced the Qualcomm Flight RB5 5G Platform, the world’s first drone platform integrating 5G connectivity and on‑device AI, enabling real‑time data processing, low‑latency communication, and advanced edge computing for autonomous operations.

Advanced Propulsion, Battery, and Hydrogen Fuel Cell Technology

Battery energy density improvements, driven by lithium-silicon and solid-state battery development, are progressively extending drone endurance from the 30-minute limitations of current lithium-polymer systems to 90-minute+ flight times for commercial multi-rotor platforms. Hydrogen fuel cell propulsion is gaining traction for long-endurance fixed-wing applications, with platforms like H3 Dynamics' HY-series demonstrating 4-hour+ flight endurance for infrastructure inspection.

5G Connectivity and UTM Platform Integration

5G network-connected drones enable real-time HD video streaming, telemetry data upload, and command-and-control communications at low latency across extended ranges without spectrum congestion. UTM (Unmanned Traffic Management) platforms, including NASA's UTM research ecosystem and the U-space European framework, provide the digital air traffic control infrastructure required to safely coordinate thousands of simultaneous drone operations in shared airspace.

Advanced Sensor and Payload Technology

Teledyne’s FLIR OEM business unit is advancing the state of the art in infrared imaging by vertically integrating the design and mass production of IR sensors and thermal modules, delivering tens of thousands of units weekly for defense, automotive, uncrewed, industrial, and professional applications. These sensor advances are enabling precision agriculture yield forecasting, building facade crack detection, and wildfire perimeter tracking through thermal imaging.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Fixed Wing |

52.5% |

2025 |

|

Component |

Hardware |

65.7% |

2025 |

|

Payload |

<25 Kilograms |

53.8% |

2025 |

|

Point of Sale |

Original Equipment Manufacturers (OEM) |

69.1% |

2025 |

| End-Use Industry | Military and Defense | 30.5% | 2025 |

|

Region |

North America |

48.4% |

2025 |

By Point of Sale

OEM channels dominate the point-of-sale segment with a 69.1% share in 2025. OEM dominance reflects the structured procurement processes for defense and military drone systems, direct enterprise contracts for commercial drone fleet deployment in agriculture, energy, and construction, and the preference of large institutional buyers to procure directly from manufacturers for technical support, customization, and warranty coverage.

To access detailed market analysis, Request Sample

Aftermarket channels represent 30.9% of the market, growing at approximately 10.8% CAGR as the installed base of commercial and consumer drones expands globally. The aftermarket encompasses replacement components, software upgrades, drone-as-a-service subscriptions, maintenance and repair services, payload accessory add-ons, and operator training.

By Component

Hardware dominates the component segment with a 65.7% share in 2025. Hardware dominance reflects the material cost of drone airframes, propulsion systems, flight controllers, GPS modules, and onboard sensors. Defense drone hardware carries the highest per-unit values, with individual platform costs ranging from hundreds of thousands to tens of millions of dollars, sustaining hardware segment revenue concentration at the premium end.

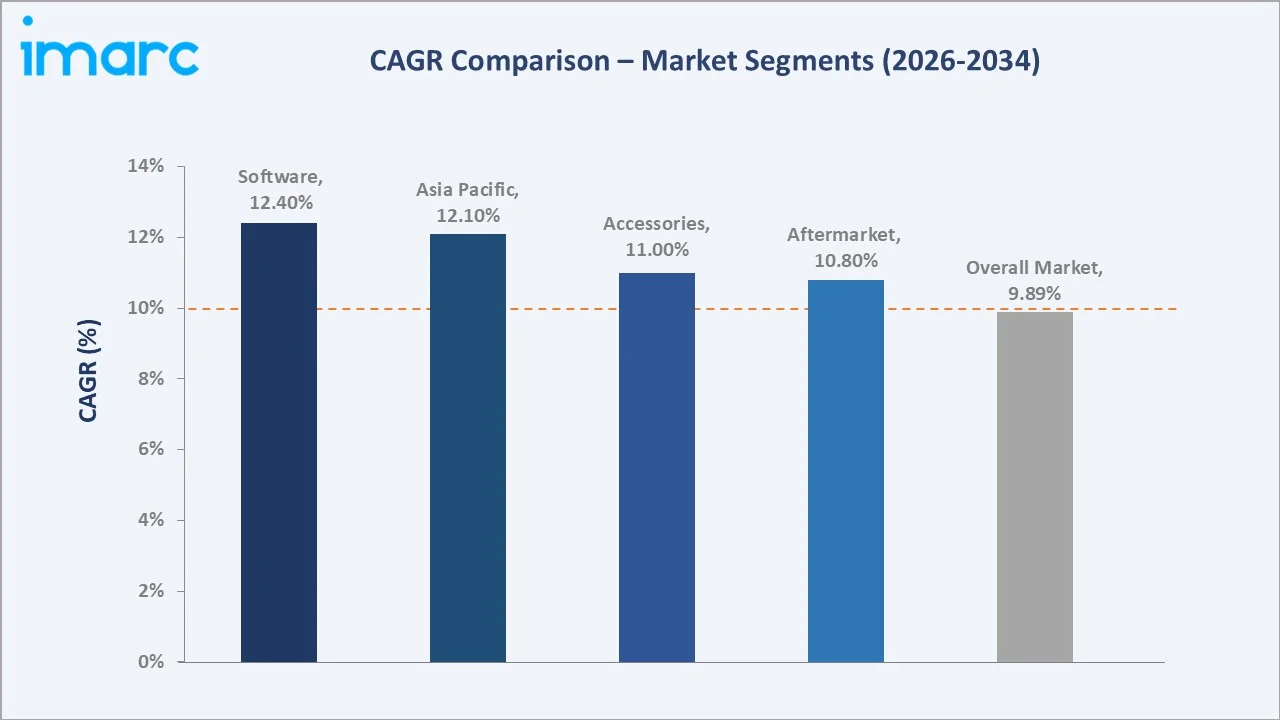

Software accounts for 22.4% of the market, growing at the highest segment CAGR of approximately 12.4% through 2034. The software segment encompasses mission planning software, autonomous flight stacks, fleet management platforms, data analytics applications, and cloud-based data storage and processing services. Accessories account for 11.9%, including replacement batteries, payload cameras, protective cases, ground control systems, and simulation training tools.

Regional Market Insights

North America's market leadership is anchored by the United States' position as the world's largest single drone procurement market. The U.S. Department of Defense, Federal Aviation Administration-authorized commercial operators, and a mature ecosystem of manufacturers, including Boeing, drive both volume and value at the premium end of the global market.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

48.4% |

Rising defense and public safety UAV procurement, progressive BVLOS regulatory frameworks, commercial delivery adoption, and smart city infrastructure investment |

|

Asia-Pacific |

21.7% |

Rapid urbanization, established drone manufacturing ecosystems, government-backed smart city and digital infrastructure programs, and agricultural modernization initiatives. |

|

Europe |

16.3% |

Sustainable logistics demand, regional drone corridor development, precision agriculture expansion, and growing infrastructure inspection applications |

|

Latin America |

7.2% |

Agricultural monitoring and crop management, oil and gas pipeline inspection, expanding e-commerce delivery networks, and improving digital infrastructure |

|

Middle East & Africa |

6.4% |

Smart city development initiatives, oil and gas asset inspection, humanitarian and emergency delivery programs, and tourism and urban infrastructure investment |

Asia-Pacific is the highest-growth region, projected at approximately 12.1% CAGR through 2034. DJI's manufacturing dominance provides China with unmatched scale economics in commercial drone production. As of February 2026, India has established a regulated drone ecosystem with over 38,500 registered drones (UIN), 39,890 DGCA-certified remote pilots, and 244 approved training organizations.

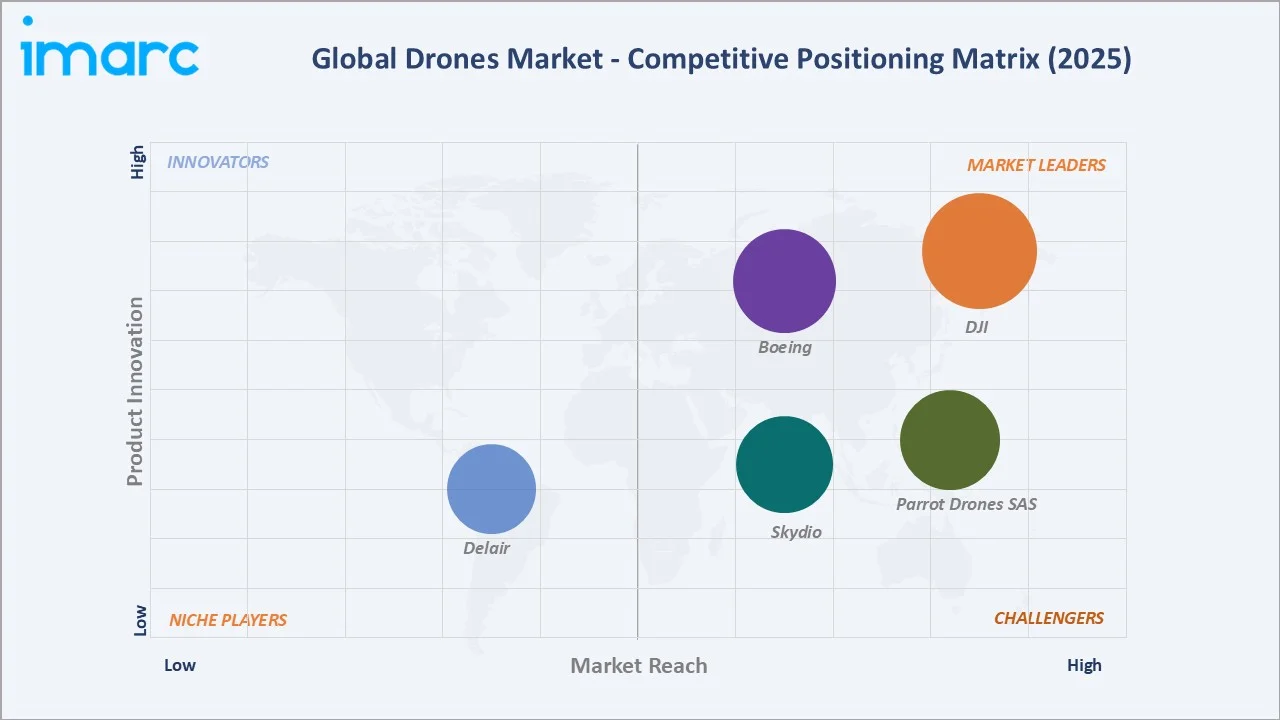

Competitive Landscape

The global drones market exhibits a moderately fragmented structure with significant concentration at the top tier. DJI holds an estimated 70%+ share of the global consumer and commercial multi-rotor drone market, representing unprecedented concentration at the platform manufacturer level.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

DJI |

DJI Mavic, DJI Air, DJI Mini, DJI Flip, DJI Avata, DJI Neo, DJI Inspire, Enterprise, Education |

Market Leader |

World's largest drone manufacturer; 70%+ consumer share; diverse commercial portfolio |

|

Boeing |

MQ-25 Stingray, MQ-28 Ghost Bat |

Market Leader |

Defense-grade UAV systems; autonomous refueling drones |

|

Parrot Drones SAS |

ANAFI USA, ANAFI Ai, ANAFI UKR |

Strong Challenger |

NDAA-compliant; European defense contracts; enterprise mapping & inspection |

|

Skydio |

Skydio R10, Skydio X10 |

Strong Challenger |

AI-powered autonomous obstacle avoidance; U.S. military contracts; infrastructure inspection |

|

Delair |

UX11, DT26 LINE, DT46 line, DT61 |

Niche Player |

Fixed-wing enterprise analytics; BVLOS operations; agriculture & energy inspection. |

The defense UAV segment is dominated by Western OEMs, including Boeing, Northrop Grumman, and AeroVironment, creating a structurally bifurcated competitive landscape divided by regulatory and geopolitical procurement barriers.

Key Company Profiles

DJI

DJI, headquartered in Shenzhen, China, is the world's largest drone manufacturer by revenue and unit volume, commanding an estimated 70%+ share of the global consumer and commercial multi-rotor drone market.

- Product Portfolio: DJI Mavic, DJI Air, DJI Mini, DJI Flip, DJI Avata, DJI Neo, DJI Inspire, Enterprise, and Education.

- Recent Developments: In December 2025, DJI launched the DJI FlyCart 100, a heavy‑payload delivery drone capable of carrying up to 100 kg, designed to support logistics, emergency response, and industrial applications.

- Strategic Focus: Vertical integration across hardware and software; enterprise market expansion; agricultural drone adoption in emerging markets; navigating NDAA compliance headwinds in the U.S. market through platform differentiation.

Boeing

Boeing, headquartered in Arlington, Virginia, USA, is a leading developer and manufacturer of advanced unmanned aerial systems for military and commercial applications. Boeing's drone portfolio spans carrier-based refueling drones, high-altitude surveillance UAVs, and autonomous delivery systems.

- Product Portfolio: MQ-25 Stingray and MQ-28 Ghost Bat.

- Recent Developments: In October 2025, Boeing unveiled a new autonomous tiltrotor concept that combines vertical takeoff and landing (VTOL) capability with long‑range cruise efficiency, aimed at future reconnaissance, attack, and logistics missions.

- Strategic Focus: Defense-focused autonomous systems development; collaborative combat aircraft (CCA) program positioning; integration of AI autonomy across naval and air force UAV platforms; BVLOS commercial delivery infrastructure investment.

Parrot Drones SAS

Parrot Drones SAS, headquartered in Paris, France, is one of Europe's leading drone manufacturers for enterprise, commercial, and defense applications. Following a strategic pivot from consumer drones to professional platforms.

- Product Portfolio: ANAFI USA, ANAFI Ai, and ANAFI UKR.

- Recent Developments: In December 2025, Parrot Drones SAS expanded its global distribution network by partnering with five new distributors across Europe and Asia, strengthening its reach in key regional markets for drones and related products.

- Strategic Focus: NDAA-compliant enterprise and defense market penetration; European defense contract expansion; precision agriculture data solutions; U.S. government procurement positioning as primary NDAA-compliant European drone manufacturer.

Market Concentration Analysis

The global drones market exhibits a complex dual concentration structure. In commercial and consumer segments, DJI holds an estimated 70%+ share of multi-rotor drone manufacturing by unit volume, representing extraordinary concentration at the platform level. However, the defense UAV segment, which represents the largest share of market value, is distributed among Western defense OEMs, including The Boeing Company, Northrop Grumman, General Atomics, and AeroVironment, where procurement is governed by national security regulations that structurally exclude Chinese manufacturers.

Consolidation activity is accelerating in the commercial drone software and services segment. Terra Drone Corp. has pursued an aggressive global acquisition strategy, establishing operational entities across 25+ countries to build the world's first truly global industrial drone services platform. Private equity interest remains strong in NDAA-compliant drone manufacturers, autonomous software platform developers, and drone-as-a-service operators with demonstrated enterprise customer bases and recurring revenue profiles.

Investment & Growth Opportunities

Fastest Growing Segments

Drone delivery and logistics platforms (estimated CAGR 20%+), AI-powered autonomous inspection software (12% CAGR), and defense loitering munitions and tactical UAVs (15% CAGR) represent the three highest-growth investment vectors through 2034. Together, these segments address a total addressable market of approximately USD 35 Billion by 2030, with software and autonomous services commanding the highest margin profiles within the broader drones ecosystem.

Emerging Market Expansion

Asia-Pacific and Latin America collectively represent an incremental USD 15 billion drone opportunity by 2030. India's government-backed PLI drone manufacturing scheme, Brazil's agricultural drone adoption program, and Southeast Asia's smart city infrastructure investment are creating highly accessible entry points for drone service operators and platform providers capable of localizing support, training, and compliance to regional regulatory frameworks. Agricultural drone services represent the highest near-term volume opportunity in these markets.

Venture and Institutional Investment Trends

- Key investment themes include AI autonomy software platforms commanding multiple premiums to hardware peers, UTM (Unmanned Traffic Management) infrastructure enabling scalable commercial operations, counter-drone (C-UAV) technology for critical infrastructure protection, and hydrogen fuel cell endurance platforms unlocking long-duration commercial inspection and delivery applications.

- Defense-focused PE and strategic investors are targeting NDAA-compliant drone manufacturers with certified product portfolios and active government contracts. The combination of regulatory certification, existing procurement relationships, and demonstrated operational performance creates significant barriers to competition and predictable revenue visibility that commands premium acquisition multiples from defense prime contractors.

Future Market Outlook (2026-2034)

The global drones market is positioned for sustained, broad-based growth through 2034. From a base of USD 33.9 Billion in 2025, the market is projected to reach USD 79.1 Billion by 2034, representing total incremental value creation of USD 45.2 Billion over the forecast decade. The drones market forecast remains consistently positive, underpinned by structural demand tailwinds from defense modernization, commercial digitization, and regulatory liberalization.

Platform evolution, particularly the transition from manually piloted to fully autonomous multi-mission platforms capable of operating in swarms under AI orchestration, will redefine how value is captured across defense, logistics, and industrial inspection applications. OEMs that successfully integrate hardware, AI autonomy software, data analytics, and service delivery into complete solutions will command sustainable competitive advantages over pure hardware manufacturers competing on specification and price alone.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 180 industry participants in 2024–2025, including drone manufacturers, defense procurement officers, commercial UAV operators, regulatory authority representatives, software platform developers, and institutional investors with drone sector exposure across North America, Europe, Asia-Pacific, and the Middle East.

Secondary Research

Secondary research encompassed a systematic review of company annual reports and investor filings, FAA and EASA regulatory documentation, defense budget appropriations documents, industry databases (Drone Industry Insights, Drone Analyst, Teal Group), trade publications (Drone Life, AUVSI's Unmanned Systems), and publicly available government procurement data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating global defense budget trajectories, commercial drone fleet growth rates, software penetration rate modelling, and regional economic development indices. A base-case CAGR of 9.89% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates,

Drones Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fixed Wing, Rotary Wing, Hybrid |

| Components Covered | Hardware, Software, Accessories |

| Payloads Covered | 25 Kilograms, 25-170 Kilograms, >170 Kilograms |

| Point of Sales Covered | Original Equipment Manufacturers (OEM), Aftermarket |

| End-Use Industries Covered | Construction, Agriculture, Military and Defense, Law Enforcement, Logistics, Media and Entertainment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | DJI, Boeing, Parrot Drones SAS, Skydio, Delair, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the drones market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global drones market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the drones industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Drones Market Report

The global drones market reached USD 33.9 Billion in 2025. It is projected to reach USD 79.1 Billion by 2034.

The drones market is expected to grow at a CAGR of 9.89% during the forecast period from 2026-2034, supported by consistent demand from defense procurement, commercial UAV adoption, and expanding software and data service revenues.

North America leads the market with a 48.4% share in 2025, driven by the U.S. Department of Defense's global leadership in drone procurement, the FAA's progressive commercial drone regulatory framework, and widespread adoption across agriculture, construction, energy inspection, and logistics.

OEM channels dominate with a 69.1% share in 2025, valued at approximately USD 23.4 Billion. OEM dominance reflects structured defense and enterprise procurement processes where buyers prefer direct manufacturer relationships for technical support, customization, and warranty coverage.

Hardware holds the largest component share at 65.7% in 2025 (approx. USD 22.3 Billion), driven by the capital-intensive manufacture of drone airframes, propulsion systems, flight controllers, and onboard sensors. However, Software at 22.4% is growing fastest at approximately 12.4% CAGR.

Key players include DJI, Boeing, Parrot Drones SAS, Skydio, and Delair, among others.

Government regulations are a critical growth enabler. The FAA's BVLOS authorization framework, EASA's U-space regulation, and CASA's BVLOS approvals in Australia are unlocking commercial delivery and large-area inspection applications that are economically unviable under VLOS constraints.

Key challenges include airspace regulatory complexity limiting BVLOS operations, high total cost of ownership for enterprise and defense platforms, counter-drone technology deployment limiting operational flexibility in certain airspace zones, and semiconductor supply chain geopolitical risks affecting non-Chinese manufacturers.

Significant opportunities exist in drone delivery and logistics platforms (20%+ CAGR), AI-powered autonomous inspection software, defense loitering munitions and tactical UAVs, UTM infrastructure development, and NDAA-compliant Western drone manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)