E-Fuel Market Size, Share, Trends and Forecast by Product, State, Production Method, Technology, End Use, and Region, 2026-2034

E-Fuel Market Size and Share:

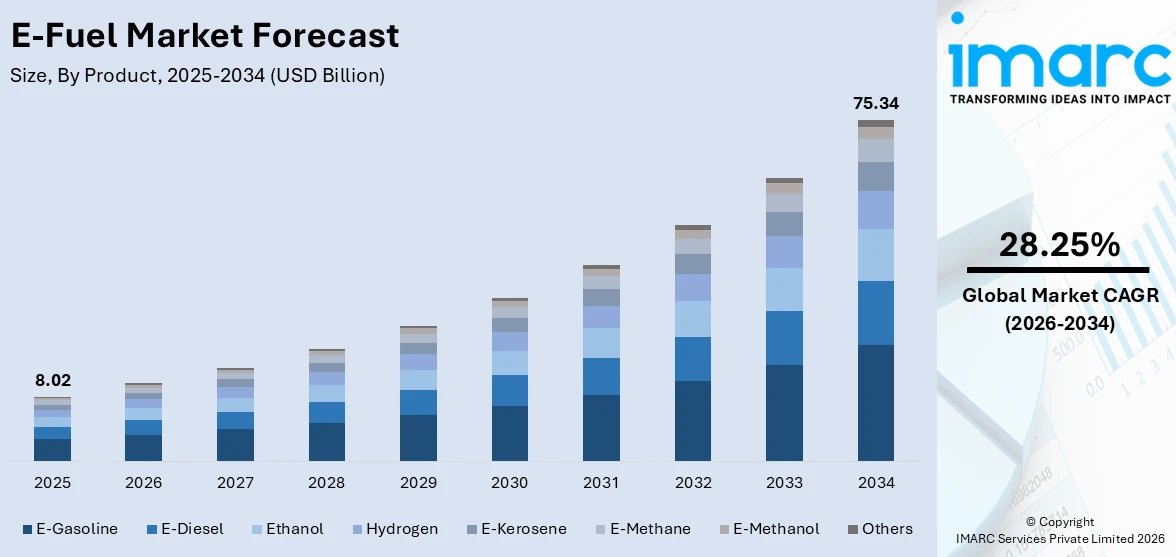

The global e-fuel market size was valued at USD 8.02 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 75.34 Billion by 2034, exhibiting a CAGR of 28.25% from 2026-2034. North America currently dominates the market, holding a market share of 32% in 2025. The region benefits from favorable regulatory frameworks, substantial federal investments in clean energy infrastructure, and the growing demand for sustainable aviation fuel across the transportation sector, all contributing to expansion of the e-fuel market share.

The global e-fuel market is experiencing growth, driven by the intensifying urgency to decarbonize hard-to-abate sectors, such as aviation, maritime shipping, and heavy-duty transportation. Governments worldwide are implementing stringent carbon emission reduction targets and renewable fuel mandates that are accelerating the adoption of synthetic fuels produced through power-to-liquid and power-to-gas pathways. The rising availability of low-cost renewable electricity from wind and solar installations is improving the economic viability of e-fuel production, while advancements in electrolyzer technologies are enhancing the efficiency and scalability of green hydrogen generation. Furthermore, corporate sustainability commitments and environmental, social, and governance mandates are encouraging major transportation and logistics companies to procure carbon-neutral fuel alternatives.

The United States is emerging as a key region in the e-fuel market, driven by supportive regulatory frameworks, increasing investment in sustainable fuel production, and strong demand for low-carbon alternatives across transportation and industrial sectors. These factors are enhancing the commercial viability of large-scale e-fuel projects, encouraging innovation, and accelerating adoption of sustainable fuels in aviation, industrial, and transport applications. Regulatory support, combined with expanding production capacity, positions the US as a leading market for e-fuels globally, fostering long-term growth and strengthening the low-carbon energy transition. This trend was exemplified in 2025, when HIF Global received the first US approval for an e-fuels design pathway under California’s Low Carbon Fuel Standard, enabling production of e-SAF, e-Naphtha, and e-Diesel, and supporting its 1.4 mtpa Texas project, demonstrating the practical advancement of large-scale e-fuel commercialization in the country.

To get more information on this market Request Sample

E-Fuel Market Trends:

Growing Investment and Funding

Strategic investments and funding initiatives are significantly influencing the e-fuel market by enabling large-scale deployment of low-carbon fuel production facilities and accelerating technological innovation. Capital inflows allow companies to expand infrastructure, scale operations, and commercialize sustainable fuel solutions, supporting decarbonization across transportation and industrial sectors. For example, in 2024, Swedish Liquid Wind secured €44 million in Series C funding to accelerate the development of ten Power-to-Liquid e-fuel facilities by 2027, converting biogenic CO₂ and renewable electricity into e-methanol for maritime and industrial applications. The investment, led by Uniper, HYCAP Fund I, and Samsung Ventures, supported scalable, modular plant designs projected to reduce approximately 200,000 tons of CO₂ per facility annually. This funding positions Liquid Wind to rapidly expand e-fuel production, strengthen supply chain capabilities, and advance Europe’s low-carbon energy objectives. Such financial backing underscores the critical role of strategic investments in enabling market growth and facilitating the broader adoption of sustainable e-fuels globally.

Technological Advancements in E-Fuel Production

Technological innovations in production are bolstering the e-fuel market growth by improving efficiency, yield, and scalability of sustainable fuels, particularly in the aviation sector. Advanced catalysts and optimized chemical processes enable higher conversion rates and greater output of low-carbon fuels, addressing supply constraints and supporting large-scale deployment. In 2025, Sasol Chemicals signed a Letter of Intent with INERATEC to supply its next-generation Fischer-Tropsch catalyst for e-SAF production. The upgraded catalyst, expected to be operational in 2026, was projected to increase plant capacity and enhance e-kerosene yields by 15% at INERATEC’s ERA ONE Power-to-Liquid facility in Frankfurt. This collaboration strengthened the commercialization potential of sustainable aviation fuel, allowing producers to maximize efficiency despite limited green hydrogen availability. By facilitating higher production volumes and improving process reliability, such technological advancements accelerate the adoption of e-fuels, reduce carbon intensity in aviation, and contribute to the broader decarbonization objectives of the global transportation sector.

Adoption of Low-Carbon E-Fuels in Maritime Transport

The adoption of low-carbon e-fuels in the maritime sector is emerging as a key factor offering a favorable e-fuel market outlook, as shipping companies seek to reduce greenhouse gas emissions and comply with increasingly stringent environmental regulations. E-fuels, such as hydrogen-derived e-methanol and e-ammonia offer significant lifecycle emission reductions, providing viable alternatives to conventional fossil-based marine fuels. For instance, in 2025, the Zero Emission Maritime Buyers Alliance (ZEMBA) announced Hapag-Lloyd and North Sea Container Line as winners of its second e-fuel tender, enabling the deployment of these sustainable fuels in container shipping. By achieving over 90% reductions in lifecycle emissions, this initiative demonstrates the scalability and practical applicability of e-fuels in large-scale maritime operations. The project not only supports participating shipping companies in their decarbonization goals but also establishes industry benchmarks for low-carbon fuel adoption, fostering broader acceptance of e-fuels and driving long-term market growth.

E-Fuel Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global e-fuel market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, state, production method, technology, and end use.

Analysis by Product:

- E-Diesel

- E-Gasoline

- Ethanol

- Hydrogen

- E-Kerosene

- E-Methane

- E-Methanol

- Others

E-gasoline accounts for 20% of the e-fuel market share, reflecting its growing adoption as a sustainable alternative to conventional gasoline. Also known as synthetic gasoline, e-gasoline is produced by combining green hydrogen with captured carbon dioxide through advanced catalytic processes, creating a drop-in fuel that is chemically identical to petroleum-based gasoline. Its primary advantage lies in its full compatibility with existing internal combustion engine vehicles and the established fuel distribution network, eliminating the need for costly modifications to engines or refueling infrastructure. This seamless integration allows consumers and industries to transition toward lower-carbon fuel solutions without significant investment in new technologies. Additionally, the production of e-gasoline supports decarbonization efforts by reducing lifecycle greenhouse gas emissions while maintaining energy density and performance standards comparable to conventional fuels. The e-fuel market forecast indicates strong growth, driven by rising adoption of e-gasoline and its compatibility with existing engines and infrastructure.

Analysis by State:

- Liquid

- Gas

Liquid dominates the market with a share of 69%, driven by its versatility, high energy density, and compatibility with existing transportation infrastructure and internal combustion engines. This category includes synthetic gasoline, e-diesel, e-kerosene, and e-methanol, all of which can be integrated seamlessly into current fuel supply chains without requiring costly modifications or new storage and distribution systems. The liquid state of these fuels simplifies handling, transport, and logistics, enabling immediate deployment across various sectors. Strong demand is particularly evident in aviation and maritime transport, where long-distance operations and high energy requirements limit the feasibility of battery-electric or direct hydrogen alternatives. By offering scalable, drop-in solutions that reduce carbon intensity while maintaining performance standards, liquid e-fuel addresses the decarbonization needs of hard-to-electrify sectors. These developments reflect key e-fuel market trends, highlighting the increasing adoption of liquid e-fuels as scalable, low-carbon solutions across transportation sectors.

Analysis by Production Method:

- Power-to-Liquid

- Power-to-Gas

- Gas-to-Liquid

- Biologically Derived Fuels

Power-to-liquid dominates the market, with a share of 38%, due to its ability to convert renewable electricity into green hydrogen via electrolysis, which is then combined with captured carbon dioxide through Fischer-Tropsch synthesis or methanol pathways to produce high-quality liquid synthetic fuels. This method is particularly suitable for generating sustainable aviation fuel, e-diesel, and e-gasoline, offering drop-in solutions fully compatible with existing engines and fuel infrastructure. The approach supports large-scale decarbonization by enabling consistent, scalable fuel production with minimal disruption to current logistics and refueling systems. In 2026, Nordic Norsk e-Fuel and Finnish stainless steel leader Outokumpu signed a Memorandum of Understanding to develop a CO-to-SAF Power-to-Liquid facility in Tornio, Finland, targeting 80,000–100,000 tons of sustainable aviation fuel annually. By utilizing Outokumpu’s carbon monoxide side streams, the project is expected to reduce approximately 200,000 tons of CO₂ emissions, advancing EU aviation decarbonization objectives while reinforcing the practical viability of power-to-liquid technologies in the e-fuel market.

Analysis by Technology:

- Hydrogen Technology (Electrolysis)

- Fischer-Tropsch

- Reverse-Water-Gas-Shift (RWGS)

Hydrogen technology (electrolysis) represents the leading segment, with a market share of 35%. Electrolysis forms the foundational step in e-fuel production by splitting water molecules into hydrogen and oxygen using renewable electricity. The resulting green hydrogen serves as the essential building block for all downstream e-fuel synthesis processes, including power-to-liquid and power-to-gas pathways. Advancements in proton exchange membrane, alkaline, and solid oxide electrolyzer technologies are improving conversion efficiency while reducing capital and operational costs, making large-scale green hydrogen production increasingly viable. The growing government support through subsidies, tax credits, and innovation funding is accelerating electrolyzer deployment worldwide. For example, in 2025, Electric Hydrogen was selected by Synergen Green Energy to supply 240 megawatts of electrolyzer capacity for a green ammonia project in the United States, highlighting the expanding scale of electrolyzer installations supporting the broader e-fuel and clean fuels ecosystem.

Analysis by End Use:

Access the comprehensive market breakdown Request Sample

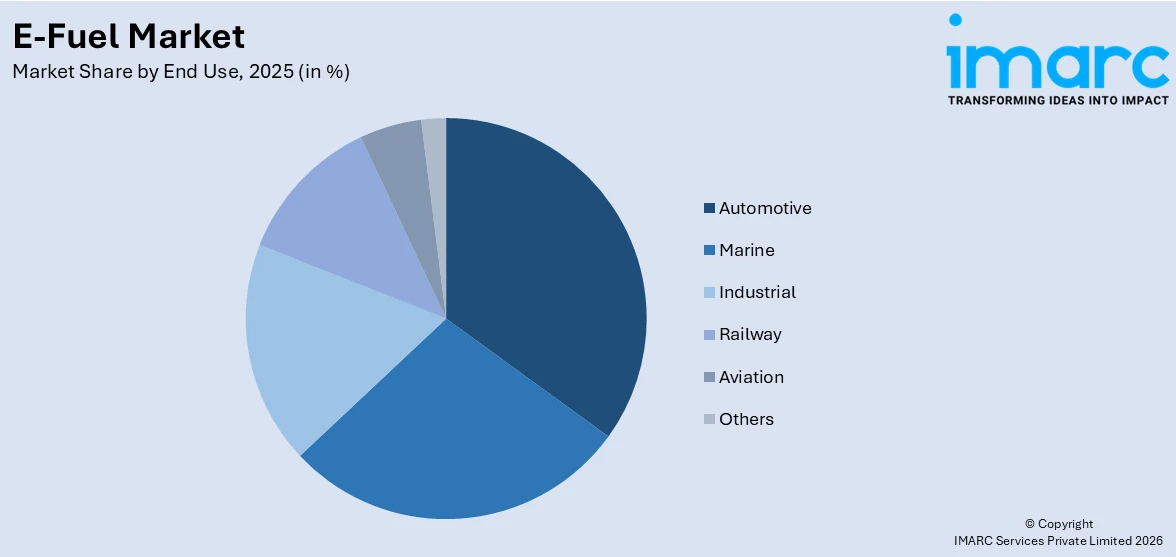

- Automotive

- Marine

- Industrial

- Railway

- Aviation

- Others

Automotive holds 30% of the market share. The automotive sector represents the largest segment because of the growing need to decarbonize conventional internal combustion engines while utilizing existing fuel infrastructure. E-fuels, including e-diesel, e-gasoline, and e-naphtha, provide high energy density and seamless compatibility with current vehicles, enabling fleet operators and individual consumers to transition to low-carbon mobility without significant modifications. This capability supports broader sustainability and emission reduction goals across the transportation sector. Industrial-scale deployment further strengthens market adoption. For instance, in 2024, Sacramento-based Infinium successfully commenced production at its Corpus Christi facility, generating approximately 8,300 litres of e-fuel daily from water and CO₂ using renewable energy-powered electrolysis. The facility produced e-diesel, e-kerosene, and e-naphtha, offering near-net-zero carbon alternatives for hard-to-decarbonize sectors such as trucking and aviation. This example underscores how practical production initiatives are driving adoption, reinforcing the automotive sector as a critical growth segment within the market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Other

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Other

- Latin America

- Brazil

- Mexico

- Other

- Middle East and Africa

North America, holding 32% share of the market, maintains a leading position attributed to strong federal policy support, abundant renewable energy resources, and substantial private sector investments in commercial-scale production facilities. The region benefits from an established technological ecosystem, access to capital, and regulatory frameworks that encourage sustainable fuel adoption across aviation, automotive, and industrial sectors. Strategic funding initiatives are accelerating market growth by enabling large-scale deployment of low-carbon fuels and commercialization of innovative technologies. For example, in 2025, US-based e-fuel start-up Twelve secured a strategic investment from United Airlines, adding to USD 728 Million raised since September 2024. The company aimed to produce e-SAF from green hydrogen and captured CO₂ at its AirPlant One facility in Washington, supporting large-scale adoption of sustainable aviation fuel. This investment underscores the region’s capacity to drive e-fuel commercialization, strengthen supply chains, and advance global decarbonization objectives, reinforcing North America’s dominant role in the market.

Key Regional Takeaways:

United States E-Fuel Market Analysis

The United States e-fuel market is witnessing growth, fueled by favorable policy incentives, abundant renewable energy resources, and substantial private investment in large-scale production infrastructure. These factors collectively enhance the commercial viability of synthetic fuels, enabling sustainable alternatives for aviation, industrial, and transportation sectors. Technological innovation, combined with financial backing, supports scalable production while addressing lifecycle carbon reduction targets, positioning e-fuels as a practical solution for hard-to-decarbonize applications. In 2025, Infinium’s affiliate, Roadrunner One, LLC, secured project financing from HSBC Holdings plc for its Roadrunner Project in Pecos, Texas. The facility was set to produce 23,000 tons per year of e-SAF and low-carbon e-fuels using renewable electricity and captured CO₂ and established long-term offtake agreements with American Airlines and IAG. With construction underway, the project exemplifies the growing financial and operational feasibility of commercial-scale e-fuel production in the US, reinforcing the country’s leading role in advancing sustainable aviation fuels and supporting global decarbonization objectives.

Europe E-Fuel Market Analysis

The Europe e-fuel market is progressing rapidly, driven by a robust regulatory framework, significant public and private investment, and expanding commercial-scale production capabilities. These factors collectively facilitate the large-scale adoption of low-carbon fuels across aviation, maritime, and industrial sectors, supporting the continent’s decarbonization and sustainability objectives. Technological innovation in renewable hydrogen production and carbon capture further enhances the efficiency, scalability, and economic viability of synthetic fuels. In 2025, Europe’s largest green hydrogen-based e-fuels plant, operated by INERATEC GmbH in Frankfurt, Germany, commenced commercial operations. The facility produces synthetic crude oil using biogenic CO₂ and by-product hydrogen from chlor-alkali processes, representing a significant advancement in sustainable fuel production. This milestone highlights Europe’s commitment to deploying renewable e-fuels at scale, promoting clean hydrogen technologies, and strengthening energy transition strategies. By combining regulatory support, technological expertise, and operational capacity, Europe is establishing itself as a global leader in the sustainable e-fuel sector, accelerating the adoption of low-carbon alternatives across multiple industries.

Asia-Pacific E-Fuel Market Analysis

The Asia-Pacific e-fuel market is gaining momentum, driven by substantial investments in hydrogen infrastructure, synthetic fuel technologies, and strategic partnerships aimed at supporting regional decarbonization targets. These efforts are enabling the development and deployment of scalable, low-carbon fuel solutions across transportation and industrial sectors. At Expo 2025 in Osaka, Japan, Toyota Motor Corporation, along with partners including Eneos Corporation, Mazda, Suzuki, Subaru, and Daihatsu, showcased vehicles powered by e-fuels produced from renewable hydrogen and captured CO₂. These synthetic fuels, fully compatible with existing engines and distribution networks, were used to power transport around the Expo, demonstrating practical low-emission applications in real-world scenarios. The initiative highlights the region’s commitment to transitioning from conventional fuels toward sustainable alternatives, reinforcing Japan’s clean mobility agenda and broader decarbonization objectives. Such demonstrations provide both technical validation and market visibility, accelerating adoption and supporting the sustained growth of the Asia-Pacific e-fuel market.

Latin America E-Fuel Market Analysis

The Latin American e-fuel market is witnessing growth, owing to abundant renewable energy resources and increasing international investment in synthetic fuel projects. Favorable geographic conditions and supportive infrastructure enable the region to develop scalable low-carbon fuel production, advancing decarbonization across transport and industrial sectors. In 2024, HIF Global announced its first Brazilian e-fuels initiative by signing a land reservation agreement with the Port of Açu to develop an e-methanol facility. The planned plant, located in Rio de Janeiro state, was expected to produce up to 800,000 tons per year of e-methanol, utilizing port infrastructure and Brazil’s renewable energy potential. This project strengthens Brazil’s position in the energy transition, supports sustainable fuel supply for shipping and other transportation sectors, and promotes regional economic development.

Middle East and Africa E-Fuel Market Analysis

The Middle East and Africa e-fuel market is evolving as traditional energy producers diversify into synthetic fuel production, aiming to maintain long-term relevance in the global energy landscape. Leveraging existing hydrocarbon infrastructure, financial resources, and the growing renewable energy capacity, regional players are investing in scalable e-fuel technologies to support sustainable transport and industrial decarbonization. In 2024, Nordic Electrofuel announced plans to expand its renewable hydrogen-based e-SAF production into Saudi Arabia and Oman, securing preliminary agreements for major plant developments. The proposed facility in Jubail, Saudi Arabia, was expected to produce approximately 300,000 tons per year by 2029, utilizing government-approved land and low-cost renewable power at around $20/MWh.

Competitive Landscape:

The competitive landscape of the global e-fuel market is characterized by a dynamic mix of established energy corporations, innovative cleantech startups, and strategic cross-industry partnerships driving the commercialization of synthetic fuel technologies. Major energy companies are leveraging their existing infrastructure, capital resources, and distribution networks to invest in power-to-liquid and power-to-gas production facilities, while technology-focused firms are pioneering advancements in electrolyzer efficiency, Fischer-Tropsch synthesis, and carbon capture integration. Strategic alliances between aerospace manufacturers, airline operators, and fuel producers are establishing bankable offtake agreements that de-risk investment and accelerate project development. Government-backed funding mechanisms, including venture debt facilities from the banks and grants are supporting early-stage commercial operations and enabling startups to scale production capacity to meet growing regulatory demand for sustainable fuels.

The report provides a comprehensive analysis of the competitive landscape in the e-fuel market with detailed profiles of all major companies, including:

- Ceres Power Holdings plc

- eFuel Pacific Limited

- Exxon Mobil Corporation

- Liquid Wind

- Norsk e-Fuel AS

- Saudi Arabian Oil Co.

- Siemens Energy AG

Latest News and Developments:

- In February 2026, HIF Global and German eFuel One GmbH signed a Heads of Agreement to supply 100,000 tons annually of certified e-Methanol, supporting long-term decarbonization goals. The fuel will be sourced from HIF’s planned Paysandú, Uruguay facility and comply with international sustainability standards, including EU RED III RFNBO requirements. The partnership strengthens Europe’s green fuel import ecosystem, positioning Germany as a key hub for scalable, low-carbon e-fuels in transport and industry.

- In November 2025, Greenlyte Carbon Technologies launched the world’s first LiquidSolar™ SNG plant in Duisburg, Germany, marking a major milestone toward industrial-scale synthetic fuel production. Backed by EU and North Rhine-Westphalia funding, Greenlyte planned to scale to e-methanol production by 2027 and expand internationally by 2030, strengthening Germany’s role in the emerging e-fuel market.

E-Fuel Market Report Scope:

| Report Features | Details |

|---|---|

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment

|

| Products Covered | E-Diesel, E-Gasoline, Ethanol, Hydrogen, E-Kerosene, E-Methane, E-Methanol, Others |

| States Covered | Liquid, Gas |

| Production Methods Covered | Power-to-Liquid, Power-to-Gas, Gas-to-Liquid, Biologically Derived Fuels |

| Technologies Covered | Hydrogen Technology (Electrolysis), Fischer-Tropsch, Reverse-Water-Gas-Shift (RWGS) |

| End Uses Covered | Automotive, Marine, Industrial, Railway, Aviation, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Ceres Power Holdings plc, eFuel Pacific Limited, Exxon Mobil Corporation, Liquid Wind, Norsk e-Fuel AS, Saudi Arabian Oil Co., Siemens Energy AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the e-fuel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global e-fuel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the e-fuel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the E-fuel Market Report

The e-fuel market was valued at USD 8.02 Billion in 2025.

The e-fuel market is projected to exhibit a CAGR of 28.25% during 2026-2034, reaching a value of USD 75.34 Billion by 2034.

The e-fuel market is driven by strategic investments, technological advancements, and adoption in hard-to-decarbonize sectors. Funding expands production capacity, innovations improve efficiency and yield, and deployment in maritime and industrial transport reduces emissions, collectively supporting broader acceptance, scalability, and long-term growth of sustainable e-fuels.

North America currently dominates the e-fuel market, accounting for a share of 32%. The region benefits from robust federal policy incentives, abundant renewable energy resources, and significant private sector investment in commercial-scale e-fuel production facilities that support sustainable aviation fuel supply chains.

Some of the major players in the e-fuel market include Ceres Power Holdings plc, eFuel Pacific Limited, Exxon Mobil Corporation, Liquid Wind, Norsk e-Fuel AS, Saudi Arabian Oil Co., Siemens Energy AG, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)