Egypt Aquaculture Market Size, Share, Trends and Forecast by Fish Type, Environment, Distribution Channel, and Region, 2026-2034

Egypt Aquaculture Market Summary:

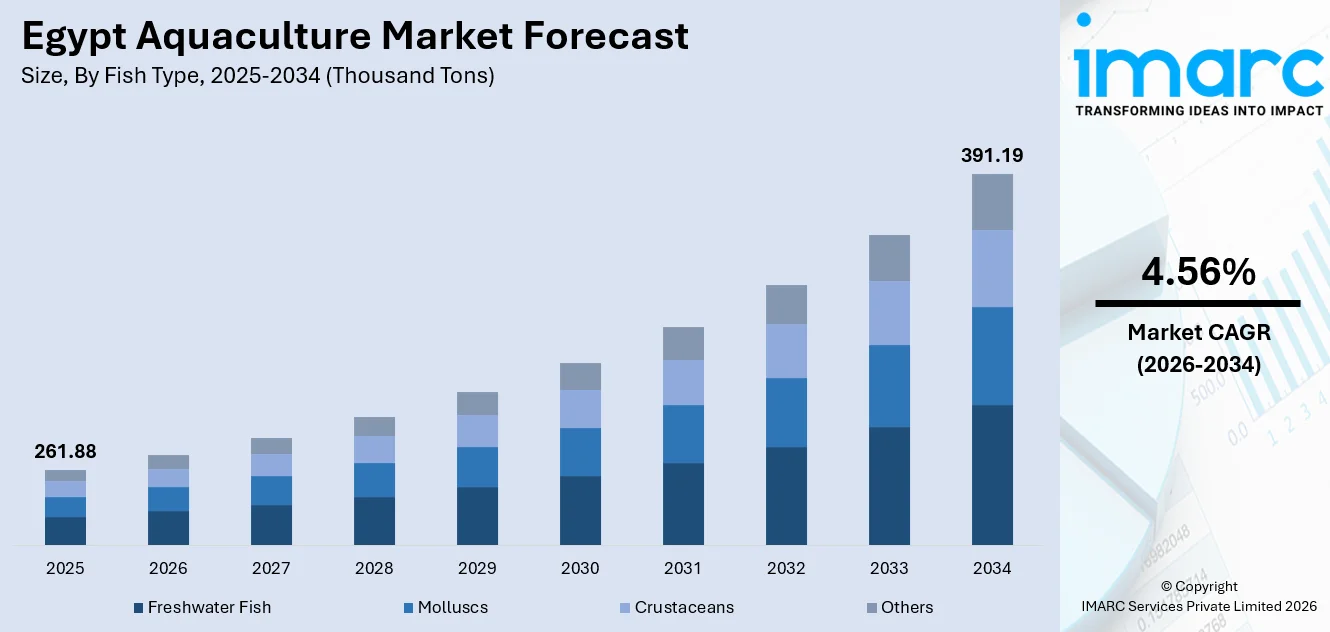

The Egypt aquaculture market size reached 261.88 Thousand Tons in 2025 and is projected to reach 391.19 Thousand Tons by 2034, growing at a compound annual growth rate of 4.56% from 2026-2034.

The Egypt aquaculture market is propelled by growing domestic demand for affordable animal protein, the expansion of freshwater farming, and government initiatives to enhance national food security. Population growth, rising per capita fish consumption, and the adoption of advanced aquaculture practices across major production regions are driving sector growth. Additionally, improvements in feed technology and selective breeding programs are boosting production efficiency, further strengthening the market’s overall share and long-term potential.

Key Takeaways and Insights:

- By Fish Type: Freshwater fish dominates the market with a share of 46.2% in 2025, driven by widespread Nile Tilapia farming, consumer demand for affordable freshwater fish, and well-established pond aquaculture infrastructure in Delta governorates.

- By Environment: Fresh water leads the market with a share of 46.18% in 2025, owing to the extensive network of earthen ponds and irrigation canal systems concentrated in the Nile Delta and favorable climatic conditions for year-round freshwater farming.

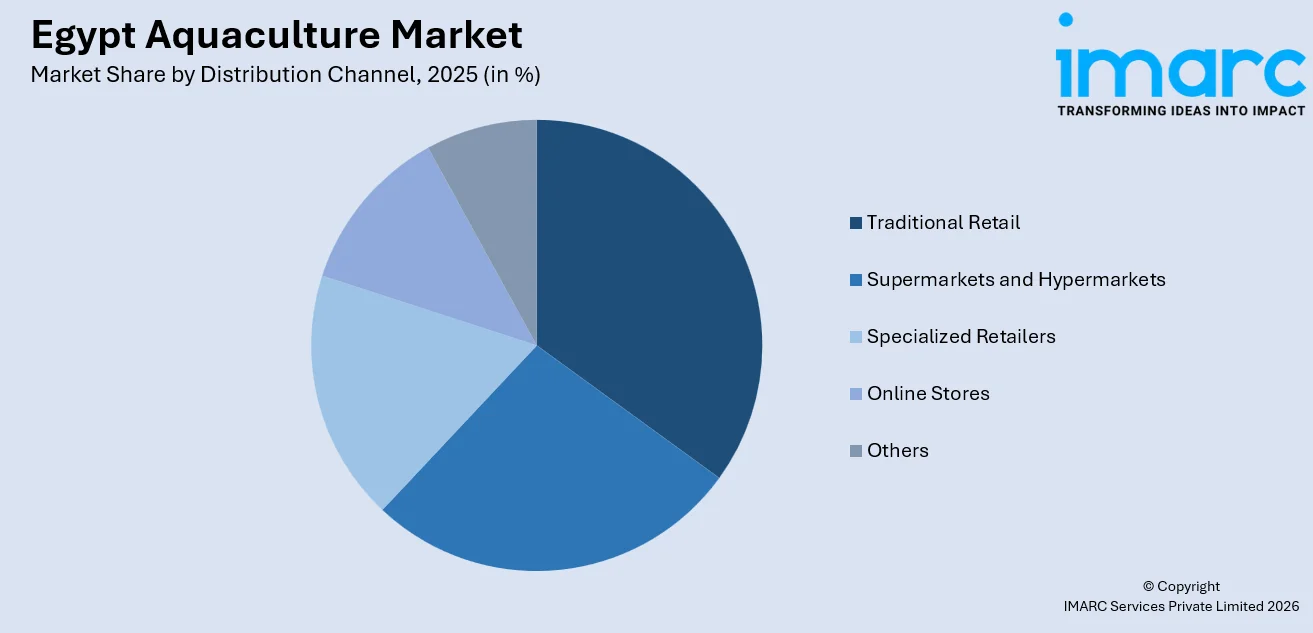

- By Distribution Channel: Traditional retail represents the largest segment with a market share of 32.05% in 2025, driven by deeply entrenched consumer habits of purchasing live and fresh fish from open-air markets, independent fishmongers, and strong cultural preferences for whole unprocessed fish.

- Key Players: The Egypt aquaculture market exhibits a fragmented competitive landscape, characterized by numerous small and medium-scale fish farming enterprises operating alongside vertically integrated operations spanning freshwater pond operators, cage-based producers, and hatchery providers.

To get more information on this market Request Sample

The Egypt aquaculture market is experiencing sustained growth propelled by a convergence of demographic, nutritional, and policy-driven factors. The country's rapidly expanding population has intensified demand for affordable animal protein, positioning farmed fish as a critical component of national food security strategies. As per sources, Egypt’s Suez Canal Aquaculture Company produced 1.7 million MT of farmed fish, with partnerships like Tejedor Lázaro’s MoU aiming to boost national fish output and improve operations. Moreover, rising per capita fish consumption, fueled by increasing health awareness and dietary diversification trends, continues to drive production volumes upward. Government initiatives aimed at expanding aquaculture zones, modernizing farm infrastructure, and supporting hatchery development have created a conducive environment for sector growth. Furthermore, the adoption of advanced feed technologies, including extruded feed formulations, has significantly improved feed conversion ratios and production yields.

Egypt Aquaculture Market Trends:

Expansion of Intensive and Semi-Intensive Farming Systems

A significant trend shaping the Egypt aquaculture market is the progressive transition from traditional extensive farming practices to intensive and semi-intensive production systems. Farmers across key aquaculture regions are increasingly adopting controlled pond environments with enhanced water management capabilities. In October 2024, the Tilapia Welfare Egypt Project improved the welfare of over 120 million Nile tilapia, trained 150 welfare educators, and reached more than 1,000 farms across Egypt. Furthermore, this shift is enabling higher stocking densities, improved feed utilization, and more predictable harvest cycles.

Adoption of Climate-Smart and Renewable Energy Solutions

The integration of climate-smart aquaculture practices and renewable energy technologies represents an emerging trend across the Egyptian aquaculture sector. Solar-powered aeration and water pumping systems are being deployed across fish farms to reduce operational energy costs while maintaining optimal growing conditions. In 2024, WorldFish and the Royal Norwegian Embassy launched a solar‑powered aquaponics greenhouse in Abbassa that uses renewable energy to jointly produce fish and vegetables, showcasing a scalable climate‑smart model for integrated aquaculture‑agriculture systems. Integrated aquaculture-agriculture systems are gaining popularity, enabling farmers to utilize water resources more efficiently by combining fish production with crop cultivation.

Growing Focus on Genetic Improvement and Hatchery Development

An important trend gaining momentum in the Egypt aquaculture market is the increased emphasis on genetic improvement programs and the expansion of specialized hatchery infrastructure. Research institutions are actively developing improved fish strains with enhanced growth rates, disease resistance, and tolerance to varying environmental conditions. In December 2025, Egypt renewed its hosting of WorldFish’s Abbassa Research Centre, where an enhanced Nile tilapia strain grows 28 % faster and lowers environmental impact by 36 %, with a goal of adoption across 35 % of local farms. Moreover, the expansion of advanced hatchery technologies for producing high-quality fingerlings is improving farm productivity by ensuring uniform growth patterns and higher yields.

Market Outlook 2026-2034:

The Egypt aquaculture market is projected to witness steady revenue growth over the forecast period, supported by sustained domestic demand for farmed fish products and ongoing modernization of production infrastructure. Rising per capita fish consumption driven by population expansion and urbanization is expected to remain the primary revenue driver. Government investments in mega aquaculture projects, development of advanced hatchery facilities, and promotion of sustainable farming technologies are anticipated to unlock additional revenue streams. The market size was estimated at 261.88 Thousand Tons in 2025 and is expected to reach 391.19 Thousand Tons by 2034, reflecting a compound annual growth rate of 4.56% over the forecast period 2026-2034.

Egypt Aquaculture Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Fish Type |

Freshwater Fish |

46.2% |

|

Environment |

Fresh Water |

46.18% |

|

Distribution Channel |

Traditional Retail |

32.05% |

Fish Type Insights:

- Freshwater Fish

- Molluscs

- Crustaceans

- Others

Freshwater fish dominates with a market share of 46.2% of the total Egypt aquaculture market in 2025.

The freshwater fish commands the leading position in the Egypt aquaculture market, driven predominantly by the extensive cultivation of Nile tilapia across the major aquaculture governorates. Tilapia remains the cornerstone of Egyptian fish farming owing to its adaptability to diverse freshwater environments, rapid growth rates, and strong consumer demand as an affordable protein source. The well-established network of earthen ponds provides ideal conditions for freshwater fish cultivation, supported by readily accessible irrigation water resources and favorable climatic conditions.

Additional freshwater fish including mullet, carp, and catfish contribute to the diversity of this segment, catering to varied regional taste preferences across Egyptian markets. The ongoing development of improved tilapia strains through selective breeding programs continues to enhance production efficiency within the freshwater segment. Investment in modern hatchery infrastructure is expanding the availability of high-quality fingerlings, strengthening the supply chain foundation for freshwater aquaculture. The segment benefits from the established downstream distribution infrastructure that efficiently channels fresh fish from farm to consumer across both urban and rural markets.

Environment Insights:

- Fresh Water

- Marine Water

- Brackish Water

Fresh water leads with a share of 46.18% of the total Egypt aquaculture market in 2025.

The fresh water holds the largest share in the Egypt aquaculture market, reflecting the country's geographic and hydrological advantages centered around the Nile River system. The extensive network of freshwater ponds, canals, and irrigation channels across the Delta region provides the primary production base for Egyptian aquaculture. Freshwater farming operations dominate due to lower capital requirements compared to marine and brackish water systems, making them accessible to small and medium-scale producers who form the backbone of the sector.

The fresh water enables the rearing of several economically valuable species, with the production of tilapia being the overwhelming majority. Semi-intensive pond farming is still the most common farming practice in this sector, although the use of intensive farming practices with water recirculation technology is gradually gaining popularity. Water utilization policies that favor efficiency and the establishment of integrated aquaculture-agriculture systems are improving the productivity of freshwater farming. The concentration of aquaculture knowledge and infrastructure in freshwater areas further cements the dominance of this sector.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Traditional Retail

- Supermarkets and Hypermarkets

- Specialized Retailers

- Online Stores

- Others

Traditional retail exhibits a clear dominance with a 32.05% share of the total Egypt aquaculture market in 2025.

The traditional retail leads the distribution channel category in the Egypt aquaculture market, underpinned by deeply rooted consumer purchasing habits and the extensive reach of informal fish markets throughout the country. As per sources, in February 2025, Egypt’s three largest aquaculture hubs—Kafr El Sheikh, Sharkia, and Behera—were studied, confirming high freshwater fish safety and traceability standards, supporting traditional market distribution for local and export consumption. Moreover, open-air fish markets, independent fishmongers, and street vendors constitute the primary touchpoints where Egyptian consumers purchase fresh and live fish.

This channel has an advantage due to their close proximity to both the wholesale distribution centers and consumers, thus allowing for quick turnaround of perishable goods without the need for elaborate cold chain distribution. The widespread existence of daily fish markets in the urban and weekly fish markets in the rural areas ensures that the geographic reach is comprehensive and accessible to all segments of consumers. The price competitiveness in traditional retailing channels, which is a result of low operating costs and direct sourcing from farms and wholesale markets, further cements consumer loyalty to this distribution channel.

Regional Insights:

- Greater Cairo

- Alexandria

- Suez Canal

- Delta

- Others

Greater Cairo serves as the largest consumption hub for aquaculture products, driven by its massive urban population and concentrated demand for affordable protein. The region benefits from proximity to major wholesale fish markets, extensive traditional retail networks, and growing supermarket channels that distribute farmed fish sourced primarily from nearby Delta production zones.

Alexandria represents a significant aquaculture market driven by its coastal location, strong seafood consumption culture, and established fishing heritage. The region supports both freshwater and marine aquaculture activities, with consumers demonstrating preference for diverse fish species. Its well-developed port infrastructure and wholesale markets facilitate efficient distribution of farmed fish across the northern Mediterranean coastal belt.

Suez Canal is emerging as a strategic aquaculture zone, supported by access to both marine and brackish water environments suitable for diverse species cultivation. Government-led mega aquaculture projects in the region are expanding production capacity, leveraging the unique geographic positioning that provides access to Red Sea and Mediterranean water resources for mariculture development.

Delta dominates Egypt's aquaculture production landscape, housing the majority of freshwater fish farming operations concentrated across key governorates. Its extensive network of earthen ponds, irrigation canals, and favorable agricultural water access makes it the primary tilapia and mullet production base, supported by established hatcheries, feed suppliers, and well-developed farm-to-market distribution infrastructure.

Others collectively contribute to the Egypt aquaculture market through scattered farming operations in Upper Egypt and emerging aquaculture zones. These areas are witnessing gradual development supported by government initiatives to decentralize fish production, expand desert aquaculture projects, and promote integrated farming systems that combine fish cultivation with traditional agricultural activities.

Market Dynamics:

Growth Drivers:

Why is the Egypt Aquaculture Market Growing?

Rising Population and Increasing Per Capita Fish Consumption

Egypt's rapidly growing population is creating sustained upward pressure on demand for affordable animal protein, directly benefiting the aquaculture sector. As per sources, Egypt’s per capita fish consumption has risen from around 15 kg to about 20 kg annually, largely driven by increased availability of farmed fish like tilapia and shifts toward healthier diets. Furthermore, as the population continues to expand, the need for domestically produced protein sources that can be scaled efficiently becomes increasingly critical. Fish, particularly farmed tilapia, occupies a unique position in the Egyptian dietary landscape as an accessible and nutritious protein source for both middle-class and lower-income households.

Government Support and National Aquaculture Development Programs

The Egyptian government has demonstrated strong commitment to expanding the aquaculture sector through dedicated development programs, infrastructure investments, and strategic national projects. Large-scale mega aquaculture initiatives are expanding production capacity in designated zones, creating new farming areas equipped with modern infrastructure. Policy frameworks supporting hatchery development, farm licensing, and access to credit for small-scale producers are lowering barriers to entry and encouraging broader participation. The government's focus on achieving greater food self-sufficiency has elevated aquaculture to a national strategic priority.

Advancements in Feed Technology and Farm Management Practices

Continuous improvements in aquaculture feed formulations and farm management methodologies are driving productivity gains across the Egypt aquaculture market. The transition from traditional sinking feed to advanced extruded feed products has significantly enhanced feed conversion ratios, enabling producers to achieve higher yields with optimized input costs. According to sources, Kafrelsheikh University developed the Smart Feed Estimation Device, optimizing tilapia feed based on fish numbers and water temperature, improving productivity and water quality across Egyptian farms. Extruded feed technology allows farmers to better manage feeding schedules and monitor consumption patterns, reducing waste and improving overall farm economics.

Market Restraints:

What Challenges the Egypt Aquaculture Market is Facing?

Water Scarcity and Competition for Freshwater Resources

The Egypt aquaculture market faces significant constraints from increasing competition for limited freshwater resources. Large-scale national infrastructure and irrigation projects are redirecting water flows, creating scarcity in traditional aquaculture zones. Climate change-induced reductions in river discharge and rising evaporation rates are compounding water availability challenges. The prioritization of agricultural and municipal water needs over aquaculture allocations restricts expansion potential for freshwater farming operations.

Rising Feed Input Costs and Supply Chain Vulnerabilities

Escalating costs of key feed ingredients, particularly soybean meal and fishmeal, represent a major restraining factor for Egyptian aquaculture producers. Feed constitutes the single largest operational expense for fish farmers, and price volatility in global commodity markets directly impacts production economics. Competition between the aquaculture, poultry, and dairy sectors for limited processed feed ingredients further intensifies cost pressures and squeezes profit margins.

Limited Processing Infrastructure and Value Addition Capabilities

The underdeveloped state of fish processing and value-addition infrastructure constrains market growth potential in the Egypt aquaculture sector. The overwhelming majority of farmed fish is sold in whole, unprocessed form as a bulk commodity, limiting revenue generation opportunities along the value chain. Insufficient cold chain facilities and processing plants prevent producers from accessing higher-value market segments such as filleted and frozen products.

Competitive Landscape:

The Egypt aquaculture market is characterized by a highly fragmented competitive structure, with a vast number of small and medium-scale fish farming operations distributed across the Nile Delta governorates. The market features a broad spectrum of participants ranging from traditional extensive pond operators to modern intensive farming enterprises utilizing advanced production technologies. Competition is primarily driven by production volume, species diversity, geographic proximity to major consumption centers, and the ability to achieve consistent product quality. Vertically integrated operations that control multiple stages of the value chain, from hatchery and feed production to distribution, hold competitive advantages through cost optimization and supply chain reliability.

Egypt Aquaculture Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fish Types Covered | Freshwater Fish, Molluscs, Crustaceans, Others |

| Environments Covered | Fresh Water, Marine Water, Brackish Water |

| Distribution Channels Covered | Traditional Retail, Supermarkets and Hypermarkets, Specialized Retailers, Online Stores, Others |

| Regions Covered | Greater Cairo, Alexandria, Suez Canal, Delta, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Egypt Aquaculture Market Report

The Egypt aquaculture market reached a volume of 261.88 Thousand Tons in 2025.

The Egypt aquaculture market is expected to grow at a compound annual growth rate of 4.56% from 2026-2034 to reach 391.19 Thousand Tons by 2034.

Freshwater fish held the largest market share, driven by the overwhelming dominance of Nile tilapia farming across key governorates, strong consumer preference for affordable and locally produced freshwater species, and the well-established pond-based aquaculture production infrastructure throughout the country.

Key factors driving the Egypt aquaculture market include rising population growth and increasing per capita fish consumption, government-led national aquaculture development programs and mega-project investments, and continuous advancements in feed technology and farm management practices.

Major challenges include water scarcity and increasing competition for limited freshwater resources, rising feed input costs driven by global commodity price volatility, limited processing and cold chain infrastructure, dependence on wild-caught fry for certain species, and climate change impacts affecting production conditions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)