Egypt Insurtech Market Size, Share, Trends and Forecast by Type, Service, Technology, and Region, 2026-2034

Egypt Insurtech Market Summary:

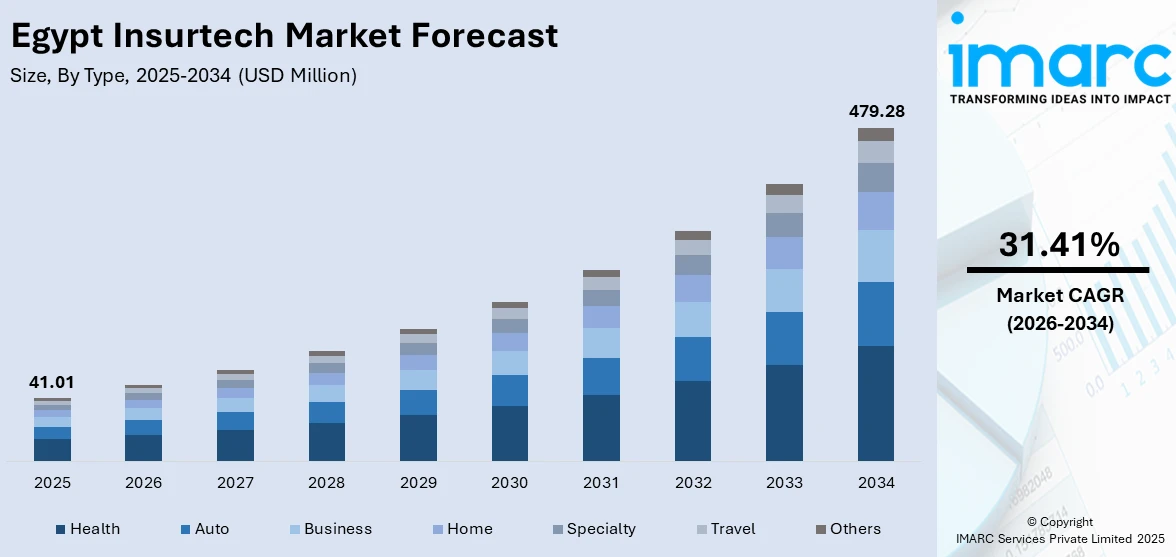

The Egypt insurtech market size was valued at USD 41.01 Million in 2025 and is projected to reach USD 479.28 Million by 2034, growing at a compound annual growth rate of 31.41% from 2026-2034.

The market is driven by increasing smartphone penetration, rising digital literacy among the population, and growing demand for seamless insurance purchasing experiences. Government initiatives supporting financial inclusion and digital transformation are accelerating insurtech adoption. Traditional insurers are embracing technological partnerships to modernize their offerings. Young demographics seeking convenient insurance solutions are fueling innovation. Expanding internet connectivity across urban and rural areas is enabling wider market reach, contributing to Egypt insurtech market share expansion.

Key Takeaways and Insights:

- By Type: Health dominates the market with a share of 25.72% in 2025, driven by increasing healthcare awareness, rising medical costs, expanding corporate coverage requirements, and growing consumer preference for digital policy management.

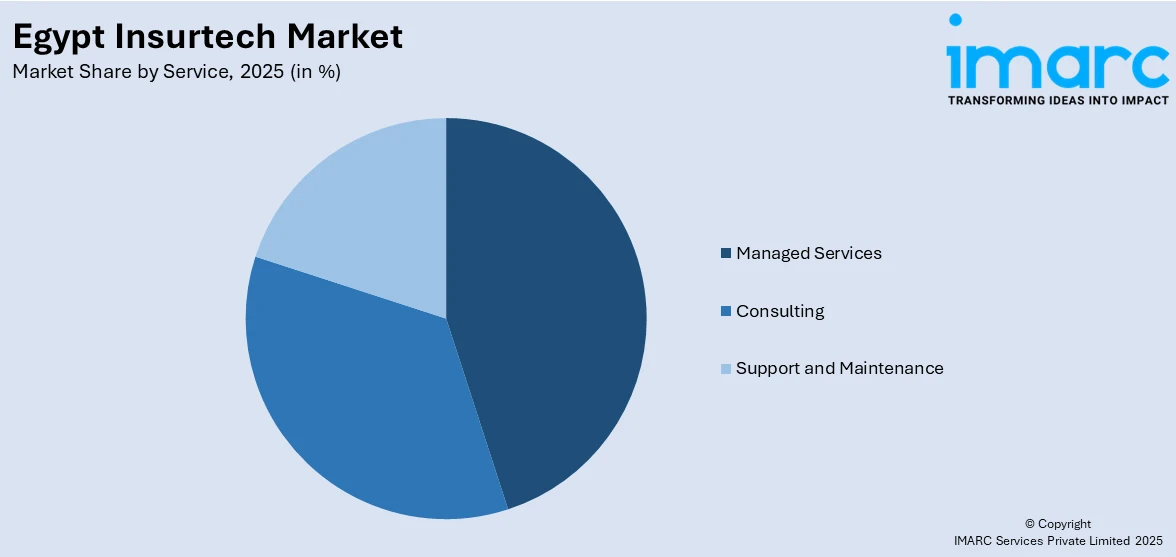

- By Service: Managed services lead the market with a share of 44.55% in 2025, owing to insurers' preference for outsourcing technology operations, cost optimization benefits, access to specialized expertise, and seamless system integration.

- By Technology: Cloud computing represents the largest segment with a market share of 26.84% in 2025, driven by scalability advantages, reduced infrastructure investments, enhanced data accessibility, and accelerated deployment timelines for insurance solutions.

- Key Players: The Egypt insurtech market exhibits a developing competitive landscape, with established insurance providers partnering alongside emerging technology startups, differentiating through innovative offerings, superior customer experience, and strategic digital transformation initiatives.

To get more information on this market Request Sample

The Egypt insurtech market is experiencing robust growth driven by the country's ambitious digital transformation agenda and supportive regulatory environment encouraging financial technology innovation. Rising smartphone adoption and expanding internet infrastructure are enabling insurers to reach previously underserved populations through digital channels. Increasing awareness about insurance benefits among the young, tech-savvy population is driving demand for convenient digital insurance solutions. Traditional insurers are actively seeking technological partnerships to modernize legacy systems and enhance customer engagement. In October 2025, Egyptian insurtech startup SehaTech raised $1.1 Million in a seed funding round led by Ingressive Capital to expand its AI‑powered health insurance platform across Egypt and the MENA region, highlighting investor confidence in digital insurance infrastructure. Moreover, the government's focus on financial inclusion and cashless transactions is creating favorable conditions for insurtech expansion. Additionally, growing middle-class populations with rising disposable incomes are seeking comprehensive insurance coverage through accessible digital platforms. Strategic collaborations between banks and insurtech providers are further accelerating market penetration.

Egypt Insurtech Market Trends:

Rising Integration of Artificial Intelligence in Policy Underwriting

The Egypt insurtech market is witnessing accelerated adoption of artificial intelligence (AI) technologies for streamlined underwriting processes. Insurers are leveraging machine learning algorithms to analyze customer data, assess risk profiles, and deliver personalized policy recommendations. In October 2025, Egyptian insurtech Amenli was recognized as the only African startup on the global top 50 insurtech list, highlighting its growing role in simplifying digital insurance experiences and adoption of advanced technologies across the region’s insurance ecosystem. This technological shift is enabling faster policy issuance while maintaining accuracy in risk evaluation. AI-powered chatbots and virtual assistants are enhancing customer interactions throughout the insurance journey.

Expansion of Usage-Based Insurance Models

Egypt insurtech providers are increasingly offering usage-based insurance products that calculate premiums based on actual customer behavior and consumption patterns. This trend is particularly prominent in auto insurance segments where telematics devices monitor driving patterns. In July 2025, the Insurers Federation of Egypt (IFE) announced it is studying the introduction of pay‑as‑you‑drive (PAYD) and smart car insurance products, signaling industry support for UBI models that tie pricing to driver behavior. Furthermore, consumers are attracted to these models due to potential cost savings and perceived fairness in pricing. Insurers benefit from improved risk assessment and customer engagement through continuous data collection.

Growing Emphasis on Embedded Insurance Solutions

The market is experiencing significant growth in embedded insurance offerings integrated within non-insurance digital platforms and customer journeys. E-commerce platforms, travel booking sites, and financial applications are partnering with insurtech providers to offer contextual insurance products at point of sale. In January 2026, Egyptian fintech leader Fawry partnered with Talabat Egypt to offer “Sehetak Fawry” digital medical coverage for more than 800 delivery riders, exemplifying embedded insurance tied directly into digital economy platforms. Moreover, this distribution model enhances convenience for customers while expanding market reach for insurers. The seamless integration eliminates traditional friction in insurance purchasing processes.

Market Outlook 2026-2034:

The Egypt insurtech market revenue is projected to experience substantial growth during the forecast period, supported by continued digital transformation initiatives across the insurance sector. Regulatory reforms promoting innovation and consumer protection are expected to strengthen market foundations. Increasing foreign investments in Egypt's fintech ecosystem will accelerate technological advancements and market expansion. The growing adoption of mobile-first insurance solutions will drive revenue growth, particularly among younger demographics. Strategic collaborations between traditional insurers and technology providers will enhance service delivery capabilities. The market generated a revenue of USD 41.01 Million in 2025 and is projected to reach a revenue of USD 479.28 Million by 2034, growing at a compound annual growth rate of 31.41% from 2026-2034.

Egypt Insurtech Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Health |

25.72% |

|

Service |

Managed Services |

44.55% |

|

Technology |

Cloud Computing |

26.84% |

Type Insights:

- Auto

- Business

- Health

- Home

- Specialty

- Travel

- Others

Health dominates with a market share of 25.72% of the total Egypt insurtech market in 2025.

The health commands the largest market share within the Egypt insurtech landscape, driven by increasing healthcare costs and growing awareness about medical coverage benefits among the population. Digital health insurance platforms are enabling convenient policy comparison, purchase, and claims management, attracting tech-savvy consumers seeking hassle-free experiences. In October 2025, SEKEM extended health insurance coverage to 40,000 farmers through the Nice Deer InsurTech platform, demonstrating how embedded digital health solutions can expand access to insurance for underserved communities.

Insurtech innovations including telemedicine integration, wellness program linkages, and simplified claims processing are enhancing the value proposition for health insurance customers across demographic segments. Mobile applications enabling instant policy issuance, real-time claims tracking, and cashless hospitalization services are driving consumer preference for digital health coverage. Partnerships between insurtech providers and healthcare networks are expanding service accessibility while reducing administrative burdens. The integration of wearable device data for personalized premium calculations and preventive healthcare recommendations is further strengthening the segment's market position and consumer engagement levels.

Service Insights:

Access the comprehensive market breakdown Request Sample

- Consulting

- Support and Maintenance

- Managed Services

Managed services lead with a share of 44.55% of the total Egypt insurtech market in 2025.

The managed services dominate as insurance providers increasingly outsource technology operations to specialized service providers for operational efficiency. This approach enables insurers to access cutting-edge technological capabilities without significant capital investments while focusing resources on core business activities and customer relationships. As per sources, Egypt’s KAF Insurance partnered with global tech services provider DXC Technology for a long‑term managed services agreement that includes core policy administration, data analytics, digital application development, and real‑time platform support to boost operational excellence.

Managed services offer comprehensive solutions encompassing system maintenance, security management, data analytics, and continuous platform optimization for insurance clients. The scalability and flexibility of managed services arrangements allow insurers to adapt quickly to changing market demands and evolving regulatory requirements while maintaining operational efficiency. These providers bring industry best practices and technological innovations from global markets, accelerating digital transformation journeys for Egyptian insurers. Cost predictability through subscription-based pricing models enables better financial planning while reducing technology-related risks and ensuring consistent service quality levels.

Technology Insights:

- Block Chain

- Cloud Computing

- IoT

- Machine Learning

- Robo Advisory

- Others

Cloud computing exhibits a clear dominance with a 26.84% share of the total Egypt insurtech market in 2025.

Cloud computing leads the market by enabling insurers to deploy scalable, cost-effective infrastructure supporting comprehensive digital transformation initiatives across operations. The technology eliminates significant upfront capital expenditures while providing flexibility to adjust computing resources based on business demands and seasonal fluctuations. In 2025, Huawei Cloud Egypt partnered with Nice Deer to host its entire digital ecosystem, accelerating AI-driven health insurance services and digital transformation across Egypt’s healthcare and InsurTech sectors. Cloud platforms facilitate rapid deployment of new insurance products and services, reducing time-to-market significantly compared to traditional infrastructure approaches.

Cloud platforms facilitate enhanced data accessibility, improved stakeholder collaboration, and accelerated development cycles for innovative insurance products and customer-facing services. The technology supports advanced analytics capabilities, enabling insurers to derive actionable insights from customer data while maintaining robust security and compliance standards. Integration capabilities allow seamless connectivity with third-party services, payment gateways, and partner ecosystems essential for modern insurtech operations. The pay-as-you-go pricing model aligns technology costs with business growth, making cloud computing attractive for emerging startups and established insurers pursuing digital transformation.

Regional Insights:

- Greater Cairo

- Alexandria

- Suez Canal

- Delta

- Others

Greater Cairo represents the primary hub for Egypt's insurtech market, benefiting from concentrated corporate headquarters, robust digital infrastructure, and highest smartphone penetration rates. The region's large population base and established financial services ecosystem create favorable conditions for insurtech adoption and innovation, attracting significant investment, technological talent, and strategic partnerships driving market expansion.

Alexandria serves as a significant secondary market for insurtech services, driven by substantial population, thriving commercial activities, and growing digital adoption rates. The city's strategic Mediterranean location and industrial base support demand for various insurance products, while improving connectivity enables expanded digital insurance distribution channels reaching diverse consumer segments.

Suez Canal presents unique insurtech opportunities driven by maritime, logistics, and trade-related insurance requirements. The economic zone's strategic importance and ongoing development initiatives foster demand for specialized commercial insurance solutions, with digital platforms enabling efficient coverage for complex international trade operations and shipping-related risk management needs.

Delta represents an emerging market for insurtech services, with agricultural insurance and micro-insurance products gaining traction among farming communities. Expanding mobile connectivity enables insurtech providers to reach previously underserved rural populations, offering accessible coverage solutions through digital channels, simplified product designs, and affordable premium structures.

Others across Egypt witness gradual insurtech adoption as digital infrastructure expands beyond major urban centers. Government initiatives promoting financial inclusion support market development in these areas. Mobile-first insurance solutions prove particularly effective in reaching dispersed populations seeking convenient access to essential coverage products through accessible digital platforms.

Market Dynamics:

Growth Drivers:

Why is the Egypt Insurtech Market Growing?

Accelerating Digital Transformation and Government Support

The Egyptian government's comprehensive digital transformation strategy is creating favorable conditions for insurtech market expansion. National initiatives promoting digitization across financial services are encouraging innovation and investment in insurance technology solutions. Regulatory bodies are implementing supportive frameworks that balance consumer protection with market development objectives. As per sources, Egypt’s Financial Regulatory Authority launched the first regulatory sandbox for non‑banking financial services, enabling fintech and insurtech innovators to test new solutions in a controlled environment, accelerating digital finance innovation. Public-private partnerships are facilitating knowledge transfer and capability building within the insurance sector. The establishment of regulatory sandboxes allows insurtech startups to test innovative solutions in controlled environments before full market deployment.

Rising Financial Inclusion Initiatives Expanding Market Reach

Egypt's commitment to financial inclusion is driving insurtech adoption among previously unbanked and underinsured population segments. Digital insurance platforms are enabling providers to reach customers in remote areas without traditional branch infrastructure. In December 2025, POST for Investment and AXA Egypt received FRA approval to establish “Sawa,” Egypt’s first licensed microinsurance company, expanding affordable insurance access to low-income populations nationwide. Microinsurance products designed for low-income households are gaining traction through mobile distribution channels. Simplified product designs and affordable premium structures are making insurance accessible to broader demographics.

Growing Young Population Demanding Digital Insurance Solutions

Egypt's young, increasingly tech-savvy population is driving demand for digital-first insurance experiences. Millennials and younger generations expect seamless online purchasing, instant policy issuance, and efficient claims processing through mobile applications. This demographic shift is compelling insurers to invest in digital capabilities and user experience improvements. Social media and digital marketing channels are proving effective in reaching younger insurance consumers. The preference for transparent pricing and personalized products is encouraging insurtech innovation across various insurance categories.

Market Restraints:

What Challenges the Egypt Insurtech Market is Facing?

Limited Digital Infrastructure in Rural Regions

Despite progress in urban areas, inadequate digital infrastructure in rural Egypt presents significant challenges for insurtech expansion. Inconsistent internet connectivity and limited smartphone penetration in remote regions restrict market reach for digital insurance platforms. The digital divide between urban and rural populations creates uneven market development patterns, limiting growth potential in underserved areas across the country.

Low Insurance Awareness Among General Population

Traditional low insurance penetration in Egypt reflects limited awareness about insurance benefits among significant population segments. Cultural factors and historical distrust of insurance products create substantial barriers to market expansion. Educating consumers about digital insurance solutions requires considerable investment in awareness campaigns and trust-building initiatives across diverse demographic groups throughout urban and rural communities.

Cybersecurity Concerns and Data Privacy Issues

Growing cybersecurity threats and data privacy concerns present considerable challenges for insurtech providers handling sensitive customer information. Building consumer trust in digital platforms requires significant investments in security infrastructure and compliance measures. Regulatory requirements for data protection add complexity and cost to insurtech operations, potentially slowing innovation, market entry, and overall industry development.

Competitive Landscape:

The Egypt insurtech market features a dynamic competitive environment characterized by collaboration and competition between established insurance providers and emerging technology-focused startups. Traditional insurers are investing significantly in digital transformation initiatives and forming strategic partnerships with technology providers to modernize operations and enhance customer engagement. Startups are differentiating through innovative product designs, superior user experiences, and agile development capabilities. Market participants are competing across multiple dimensions including technological sophistication, product breadth, pricing competitiveness, and customer service quality. Strategic alliances between local players and international insurtech firms are facilitating knowledge transfer and market development.

Recent Developments:

- In June 2024, Egyptian insurtech Mal Bazaar secured an insurance brokerage license from the Financial Regulatory Authority and launched its “My Policy” digital platform, digitizing corporate insurance management for over 60,000 employees across sectors, enhancing access to medical, motor, property, and cargo coverage.

Egypt Insurtech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Auto, Business, Health, Home, Specialty, Travel, Others |

| Services Covered | Consulting, Support and Maintenance, Managed Services |

| Technologies Covered | Block Chain, Cloud Computing, IoT, Machine Learning, Robo Advisory, Others |

| Regions Covered | Greater Cairo, Alexandria, Suez Canal, Delta, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Egypt Insurtech Market Report

The Egypt insurtech market size was valued at USD 41.01 Million in 2025.

The Egypt insurtech market is expected to grow at a compound annual growth rate of 31.41% from 2026-2034 to reach USD 479.28 Million by 2034.

Health held the largest Egypt insurtech market share, driven by increasing healthcare awareness, rising medical costs, expanding corporate health coverage requirements, and growing consumer preference for digital health policy management solutions.

Key factors driving the Egypt insurtech market include government digital transformation initiatives, rising smartphone penetration, growing financial inclusion efforts, and increasing demand from young demographics for convenient digital insurance solutions.

Major challenges include limited digital infrastructure in rural areas, low insurance awareness among the general population, cybersecurity concerns, regulatory complexity, data privacy requirements, and building consumer trust in digital insurance platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)