Electric Insulator Market Size, Share, Trends and Forecast by Material, Voltage, Category, Installation, Product, Rating, Application, End Use Industry, and Region, 2026-2034

Global Electric Insulator Market Size, Share, Trends & Forecast (2026-2034)

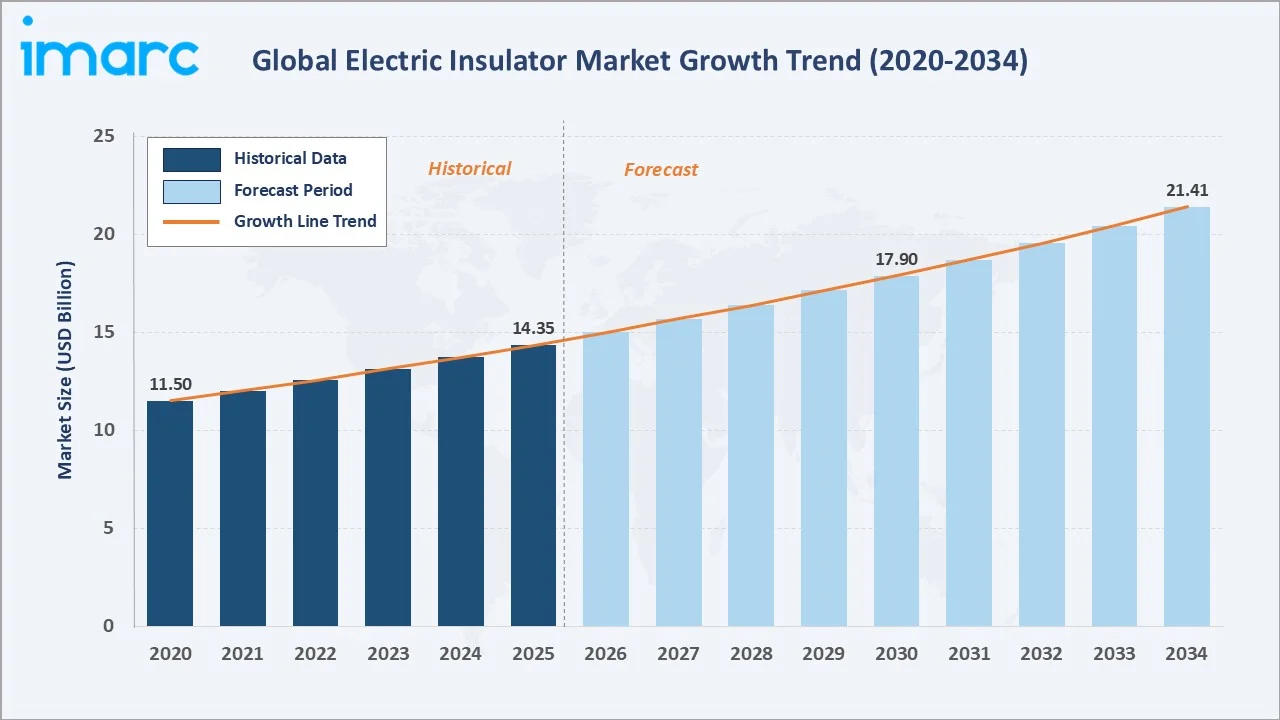

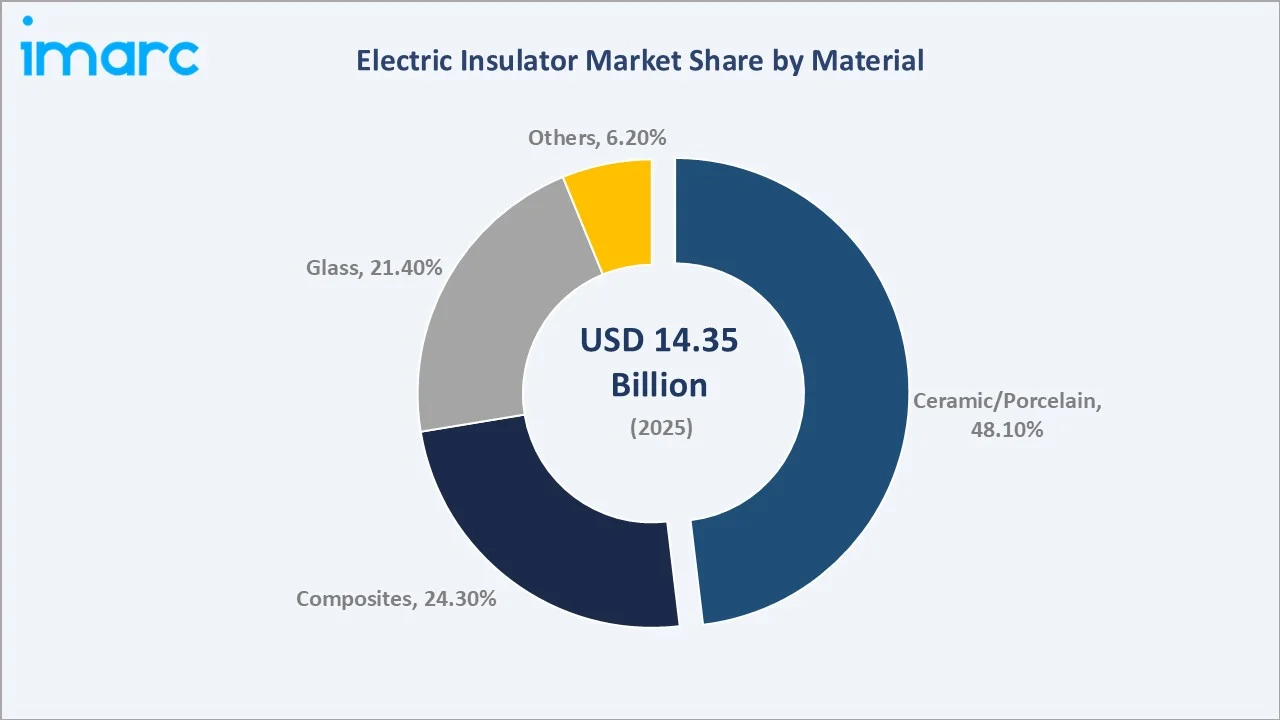

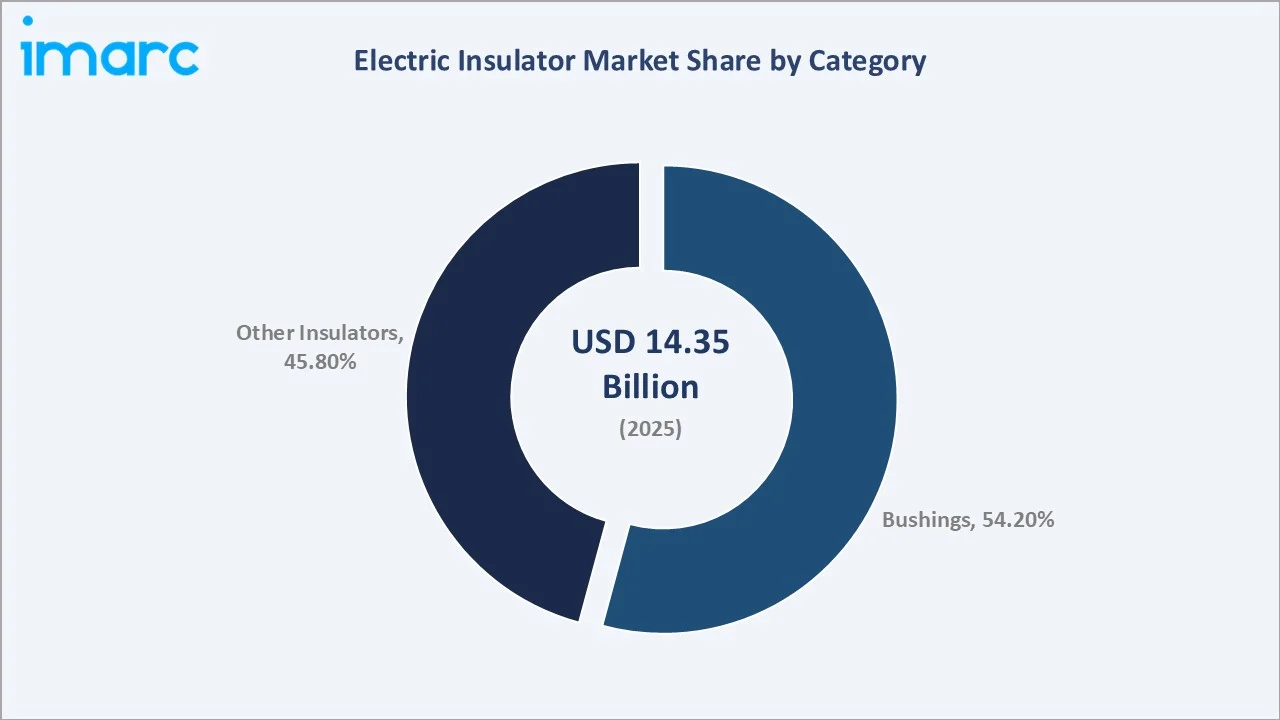

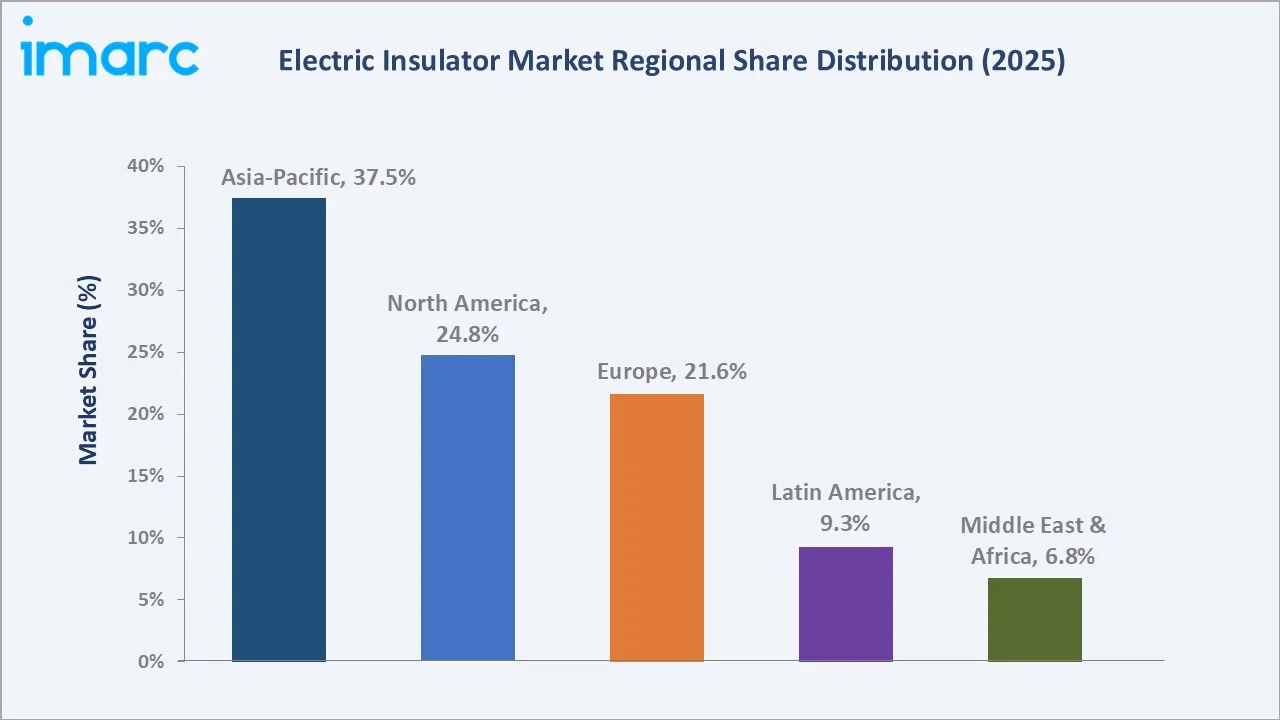

The global electric insulator market size was valued at USD 14.35 Billion in 2025 and is projected to reach USD 21.41 Billion by 2034, exhibiting a CAGR of 4.55% during the forecast period 2026-2034. Escalating electricity demand driven by rapid urbanization, large-scale renewable energy deployment, and smart grid modernization programs is powering the electric insulator market growth. Ceramic/Porcelain leads the material segment at 48.1% in 2025, while Bushings dominate the category segment at 54.2%. Asia-Pacific accounts for 37.5% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.35 Billion |

|

Forecast Market Size (2034) |

USD 21.41 Billion |

|

CAGR (2026-2034) |

4.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (37.5% share, 2025) |

|

Leading Material Segment |

Ceramic/Porcelain (48.1%, 2025) |

|

Leading Category Segment |

Bushings (54.2%, 2025) |

The global electric insulator market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base with a sustained forecast curve powered by grid modernization, offshore wind integration, and rising electricity demand across emerging economies.

To get more information on this market, Request Sample

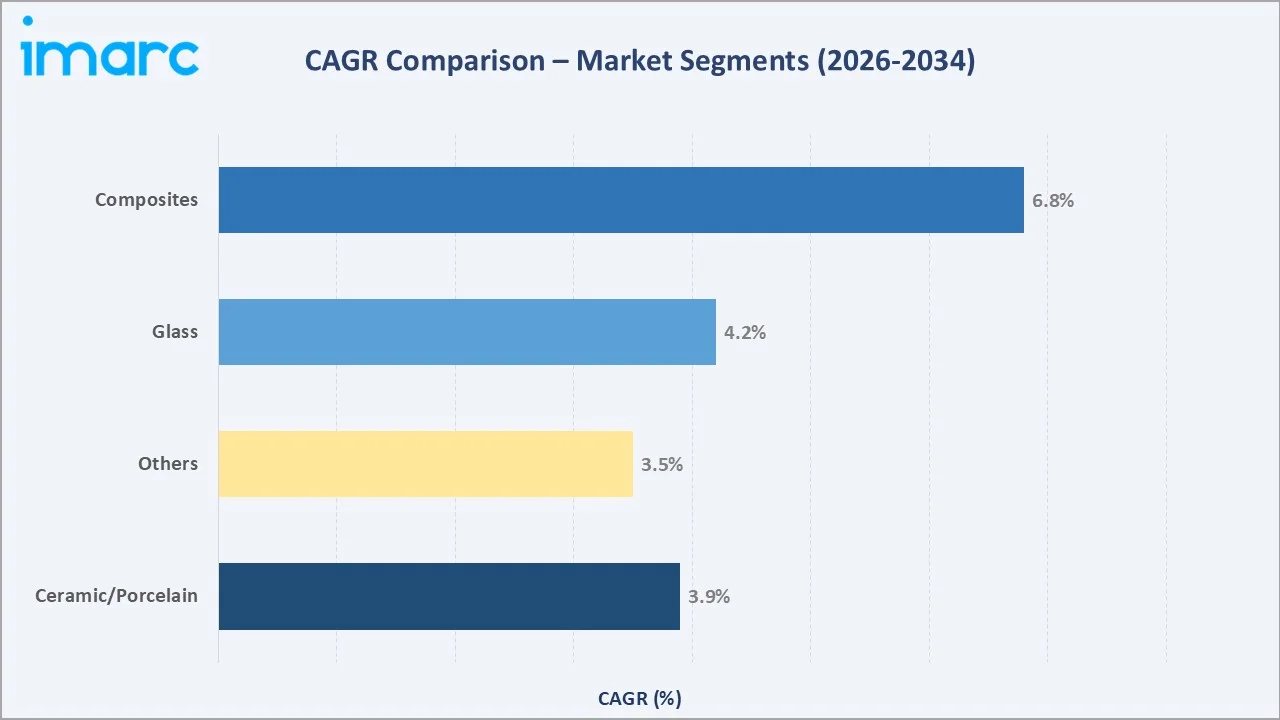

Segment-level CAGR comparisons highlighting composite insulators as the fastest-growing material sub-category within the global electric insulator industry analysis through 2034, driven by polymer adoption in offshore wind and HVDC applications.

Executive Summary

The global electric insulator market is at a structural inflection point, propelled by the convergence of grid modernization, accelerating renewable energy integration, and the broad electrification of transport and industry. Valued at USD 14.35 Billion in 2025, the market is forecast to reach USD 21.41 Billion by 2034 at a CAGR of 4.55%. The United Nations projects that 68% of the global population will reside in urban areas by 2050, translating into sustained demand for high-capacity transmission and distribution infrastructure that relies fundamentally on high-performance insulation.

Ceramic/Porcelain maintains the largest material share at 48.1% in 2025, underpinned by proven dielectric reliability in high-voltage substations and outdoor transmission lines. However, composite and polymer insulators are gaining rapid traction due to lighter weight, superior pollution resistance, and suitability for offshore wind and remote microgrid deployments. The composite insulators sub-segment, valued at approximately USD 2.4 Billion in 2023, is forecast to reach approximately USD 4.4 Billion by 2033. Bushings dominate the category segment at 54.2%, reflecting the growing density of transformer and switchgear installations across utility substations worldwide.

Asia-Pacific commands the leading regional position at 37.5% in 2025, anchored by China's ultra-high-voltage grid expansion and India's large-scale electrification programs. North America follows at 24.8%, driven by aging infrastructure replacement and EV charging network build-outs. In September 2025, the U.S. Department of Energy launched the Speed to Power initiative to accelerate multi-gigawatt transmission projects, directly increasing insulator procurement across new corridors. Europe holds 21.6%, with cross-border HVDC interconnectors and offshore wind integration underpinning sustained insulator demand.

Key Market Insights

|

Insight |

Data |

|

Largest Material Segment |

Ceramic/Porcelain – 48.1% share (2025) |

|

Fastest-Growing Material |

Composites – ~6.8% CAGR (2026–2034) |

|

Leading Category |

Bushings – 54.2% share (2025) |

|

Leading Region |

Asia-Pacific – 37.5% revenue share (2025) |

|

Second Region |

North America – 24.8% revenue share (2025) |

|

Top Companies |

Hitachi Energy, Siemens AG, NGK Insulators, Hubbell, GE, BHEL, MacLean-Fogg, Seves Group |

Key Analytical Observations Supporting The Above Data:

- Ceramic/Porcelain's 48.1% dominance in 2025 reflects decades of proven reliability in high-voltage transmission lines and substations, where consistent dielectric properties and mechanical durability are paramount across diverse operating environments.

- Composite insulators are the fastest-growing material at ~6.8% CAGR through 2034, driven by their superior hydrophobicity, pollution resistance, and lighter weight in offshore wind farm connections, coastal substations, and HVDC transmission corridors.

- Bushings account for 54.2% of the category segment in 2025, driven by the global expansion of transformer and switchgear installations in utility-scale substations and renewable energy generation facilities requiring high-grade isolation components.

- Asia-Pacific's 37.5% regional leadership is anchored by China's ultra-high-voltage grid expansion and India's PM Surya Ghar program, with India's T&D sector adding 35,760 MVA of transformation capacity in 2024 alone.

- North America's 24.8% share reflects U.S. new utility-scale generation additions estimated at approximately 62.8 GW in 2024, a 55% increase over 2023 levels, which indirectly but materially boosts insulator demand across interconnecting transmission infrastructure.

Global Electric Insulator Market Overview

Electric insulators are passive electrical components manufactured from dielectric materials, including ceramic/porcelain, glass, and composite polymers, designed to prevent unintended current flow between conductors and support structures in power transmission, distribution, and industrial electrical systems. They serve as critical safety and performance components across overhead transmission lines, substations, distribution networks, railways, and industrial facilities operating across a wide range of voltage ratings from low-voltage distribution to ultra-high-voltage HVDC transmission corridors above 800 kV.

Applications span the full power sector ecosystem: utility-scale transmission and distribution infrastructure, renewable energy generation facilities including wind and solar farms, railway electrification systems, industrial power plants, and increasingly, EV charging network infrastructure. The market is also intersecting with smart grid and digital substation trends, where insulator condition monitoring through embedded sensors and IoT connectivity is creating a new premium product category.

Macroeconomic enablers include the global commitment to net-zero emissions requiring massive renewable energy buildout, the United Nations projection that 68% of the world population will live in urban areas by 2050 necessitating expanded grid capacity, and the IEA's estimate that the global power sector will require approximately USD 16.4 Trillion in cumulative investment over the next three decades with T&D infrastructure representing the largest sub-sector share.

Market Dynamics

To evaluate market opportunities, Request Sample

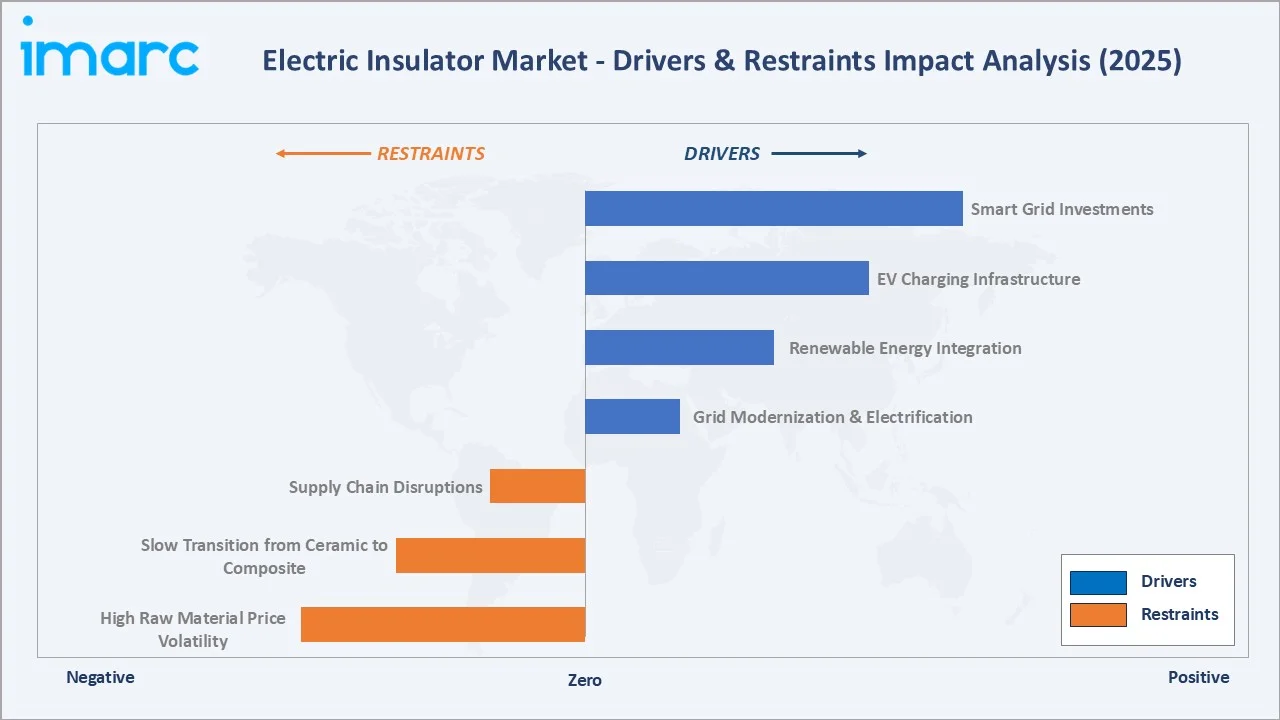

Market Drivers

- Grid Modernization and T&D Infrastructure Expansion: Governments worldwide are investing heavily in upgrading aging transmission networks and expanding grid capacity to manage intermittent renewable energy sources. Africa's target to achieve universal electricity access requires 160 GW of new generation capacity and 130 million new on-grid connections, creating sustained insulator procurement demand.

- Renewable Energy Integration: The global shift to wind and solar power requires extensive new transmission and substation infrastructure. Offshore wind installations in particular demand marine-grade composite and polymer insulators capable of withstanding salt spray, humidity, and high UV exposure across long operational lifetimes, driving both volume and value growth.

- EV Charging Infrastructure Expansion: The rapid buildout of electric vehicle charging networks, particularly high-power DC fast-chargers operating at 150–350 kW, is increasing demand for quality electrical insulation at the distribution level. With the global EV fleet expected to grow significantly through 2034, distribution network upgrades are creating a growing insulator demand channel.

- Smart Grid and HVDC Deployment: HVDC transmission systems require specialized insulators engineered for sustained DC voltage stress, and their growing adoption for long-distance bulk power delivery and offshore wind farm connections is creating a structurally distinct premium market segment for advanced insulation solutions.

Market Restraints

- Raw Material Price Volatility: Ceramic insulators depend on alumina and silica, while composite insulators use silicone rubber and fiberglass, all of which are subject to commodity price fluctuations and supply chain disruptions that can compress manufacturer margins and delay project timelines.

- Utility Conservatism Toward New Materials: Many utility operators remain cautious about transitioning from proven ceramic and glass insulators to composite alternatives due to higher upfront costs and mixed field performance data in certain contamination environments, slowing the pace of composite adoption below its technical potential.

Market Opportunities

- Smart Insulators and Condition Monitoring: The integration of sensors, IoT connectivity, and AI-based analytics into insulator designs enables real-time leakage current monitoring, contamination detection, and predictive maintenance. This technology-embedded segment commands significant price premiums and is growing at an accelerating pace.

- Rural and Remote Electrification Programs: Off-grid and microgrid deployments across Sub-Saharan Africa, Southeast Asia, and Latin America represent a fast-growing demand channel for compact, low-maintenance insulators suited to challenging environmental conditions and limited service infrastructure.

Market Challenges

- Stringent Certification and Testing Requirements: IEC 60305, ANSI C29, and CIGRE standards impose rigorous type testing and quality verification requirements that extend development timelines and increase compliance costs, particularly for new composite insulator entrants seeking utility qualification.

- Skilled Workforce Shortage: Advanced composite insulator manufacturing and high-voltage field installation require specialized technical expertise that is in short supply across many growth markets, constraining both production scale-up and deployment velocity.

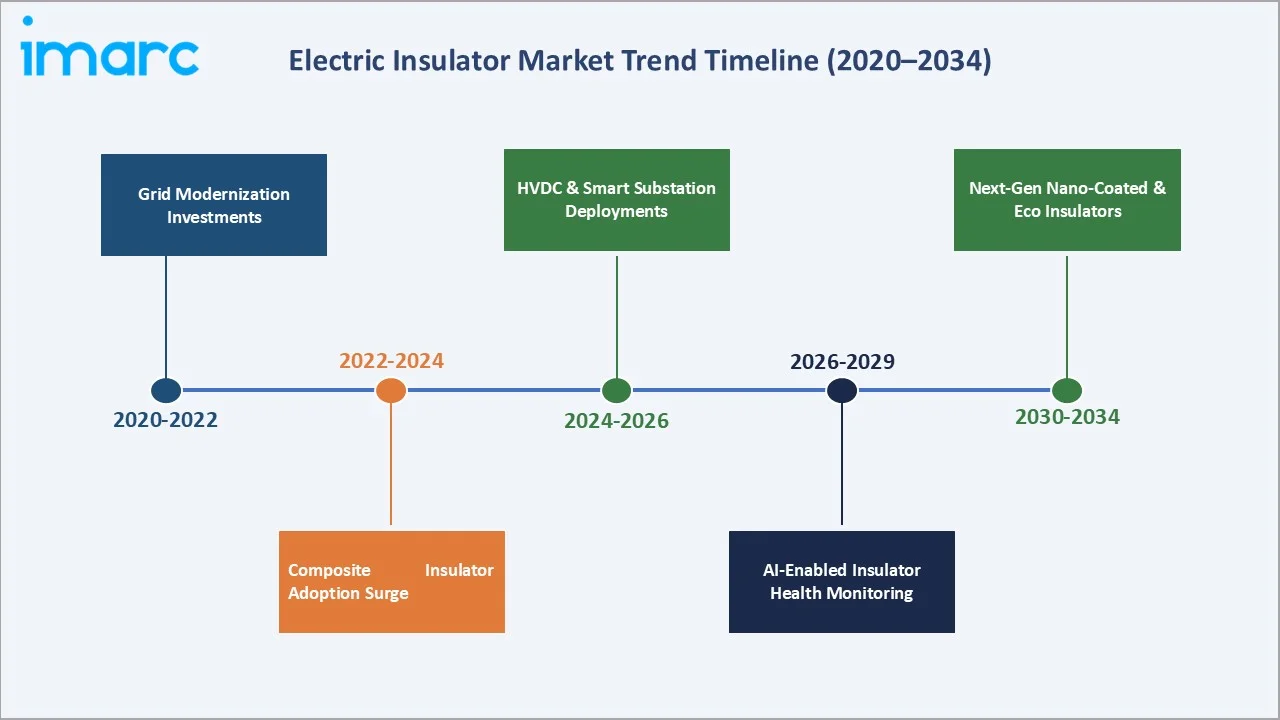

Emerging Market Trends

1. Rapid Expansion of Power Transmission and Distribution Infrastructure

The escalating global demand for electricity is driving widespread upgrades of power transmission and distribution networks. In February 2024, India's PM Surya Ghar: Muft Bijli Yojana scheme targeted one crore households for rooftop solar, offering subsidies of up to 40% of panel costs, generating material new grid connectivity requirements.

2. Shift Toward Composite and Polymer Insulators in Advanced Applications

The global transition from traditional ceramic and glass insulators to composite polymer variants is gaining momentum, particularly in demanding environments such as offshore wind installations, high-altitude transmission networks, and coastal substations where durability and performance are critical.

3. Smart Grid and HVDC Transmission System Expansion

High-voltage direct current transmission systems require specialized insulators engineered for sustained DC voltage stress. The U.S. Department of Energy launched the Speed to Power initiative on September 18, 2025, through its Grid Deployment Office to accelerate the development of large-scale transmission and generation infrastructure projects. The program explicitly targets multi-gigawatt grid capacity expansion to meet rapidly rising electricity demand—particularly from AI data centers, advanced manufacturing, and broader electrification trends.

4. AI-Enabled Insulator Health Monitoring and Predictive Maintenance

Utilities are adopting sensor-equipped insulators and drone-based inspections for real-time leakage, pollution, and failure monitoring. This enables condition-based maintenance, reduces outages, extends asset life, and leverages machine learning analytics as a key market differentiator.

5. Nano-Coated Insulators and Eco-Friendly Material Innovation

Manufacturers are developing nano-coated insulators for better hydrophobicity and pollution resistance, while recyclable composites and low-impact ceramics address regulatory sustainability requirements in Europe and North America.

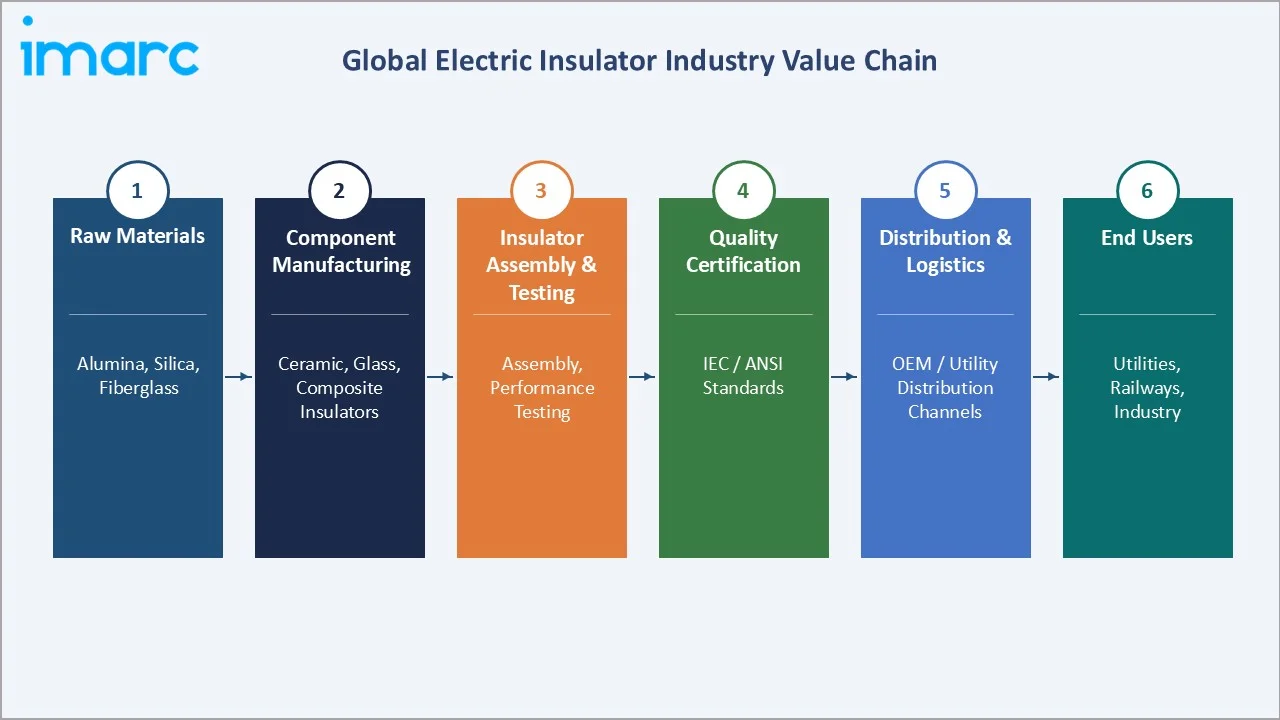

Industry Value Chain Analysis

The electric insulator value chain spans five integrated stages from raw material supply through end-user deployment, each presenting distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials (Alumina, Silica, Fiberglass, Silicone Rubber) |

Global commodity suppliers, specialty chemical manufacturers (Dow Corning, Wacker Chemie) |

|

Component Manufacturing (Ceramic, Glass, Composite Forming) |

NGK Insulators, Seves Group, Aditya Birla Insulators, Lapp Insulators, and regional producers |

|

Insulator Assembly, Testing & Certification |

Hitachi Energy, Siemens AG, Hubbell, BHEL, MacLean-Fogg, PFISTERER – IEC/ANSI certified facilities |

|

Distribution & Project Supply (Utility Tenders, EPC Contracts) |

Global distributors, national electrical equipment wholesalers, OEM direct procurement |

|

End Users (Installation & Maintenance) |

Electric utilities, grid operators, railway networks, industrial facility operators, EPC contractors |

Insulator manufacturers at the assembly, testing, and certification stage hold the highest strategic value by combining material science, precision manufacturing, and regulatory compliance. Yet, raw material volatility and ongoing certification costs Favor global-scale players over regional ones.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Ceramic/Porcelain |

48.1% |

2025 |

|

Voltage |

Low |

40.6% |

2025 |

|

Category |

Bushings |

54.2% |

2025 |

|

Installation |

Distribution Networks |

39.8% |

2025 |

| Product | Pin Insulator | 45.9% | 2025 |

| Rating | 22 kV | 15.5% | 2025 |

| Application | Cable | 28.8% | 2025 |

| End Use Industry | 🔒 | 🔒 | 2025 |

|

Region |

Asia Pacific |

37.5% |

2025 |

By Material

Ceramic/Porcelain dominates the material segment with 48.1% of the global electric insulator market share in 2025, reflecting its proven dielectric reliability and mechanical strength across high-voltage outdoor applications. Glass holds 21.4%, remaining the preferred choice for suspension insulator strings on overhead transmission lines due to its transparent self-cleaning properties and ease of visual fault detection. Composites account for 24.3%, the fastest-growing sub-segment. Others represent 6.2%, encompassing hybrid and specialty dielectric materials for niche industrial and railway applications.

To access detailed market analysis, Request Sample

Ceramic/Porcelain's 48.1% leadership reflects the material's high dielectric constant, stable performance across temperature ranges, and strong mechanical load-bearing properties essential for overhead transmission applications. The expanding T&D network in emerging markets, where cost-effective proven solutions are prioritized, continues driving ceramic insulator procurement. Glass insulators at 21.4% maintain a strong position in suspension string applications on high-voltage overhead lines, valued for their self-monitoring transparency property – cracked discs are visually identifiable during routine aerial inspection, reducing maintenance costs. Composite insulators at 24.3% are the fastest-growing material, driven by offshore wind, HVDC, and remote electrification applications where their hydrophobicity, lightweight properties, and superior pollution resistance provide compelling advantages over legacy materials.

By Category

Bushings account for 54.2% of the global electric insulator market share by category in 2025, driven by the proliferation of transformer, circuit breaker, and switchgear installations in utility substations and industrial facilities. Other Insulators represent 45.8%, encompassing pin insulators, suspension insulators, shackle insulators, and strain insulators across distribution and transmission line applications.

Bushings' 54.2% category dominance is underpinned by the growing density of power transformer installations globally, where each large power transformer requires multiple high-voltage bushings to connect internal windings to the external network. As grid operators expand transformer capacity to accommodate renewable energy intermittency and rising load demand, bushing procurement volumes increase proportionally. The demand for bushings rated above 145 kV is specifically accelerating with HVDC corridor expansion. In August 2025, Hitachi Energy India announced a USD 36 million investment at its Mysuru facility to double EHV-class transformer insulation production capacity, directly reflecting the volume trajectory of this segment.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

37.5% |

China UHV grid expansion, India PM Surya Ghar, ASEAN rural electrification, offshore wind buildout |

|

North America |

24.8% |

DOE Speed to Power initiative, aging grid replacement, EV charging infrastructure, and renewable integration |

|

Europe |

21.6% |

Cross-border HVDC interconnectors, offshore wind, GreenSwitch modernization, EU net-zero mandates |

|

Latin America |

9.3% |

Brazil and Mexico grid expansion, rural electrification, and renewable energy project buildout |

|

Middle East & Africa |

6.8% |

Saudi Vision 2030 infrastructure, UAE smart grid projects, Sub-Saharan Africa electrification programs |

Asia-Pacific commands 37.5% global revenue share in 2025, the most dominant regional position in the electric insulator market. China is the single largest national market, combining the world's most extensive ultra-high-voltage grid network with massive annual transmission infrastructure expansion. Japan and South Korea contribute advanced composite and specialty insulator manufacturing capabilities, while Southeast Asian nations are expanding grid access in rapidly urbanizing markets.

North America, with 24.8% in 2025, is anchored by the United States, where the DOE's Speed to Power initiative launched in September 2025, targeting multi-gigawatt transmission project acceleration to support AI data centre power demand and clean energy integration. Aging transmission networks in the U.S. and Canada require replacement of key components, including insulators, and government initiatives promoting renewable energy integration are further increasing demand for high-performance composite and polymer insulator solutions. Canada's grid interconnection expansion and Mexico's growing power infrastructure add further North American market breadth.

Europe's 21.6% share reflects the region's cross-border interconnector ambitions and offshore wind leadership. The EU‑backed GreenSwitch project is modernizing grid infrastructure across Austria, Slovenia, and Croatia. With EUR 73 million in CEF Energy funding (total value EUR 146 million, 2023–2028), it strengthens transmission and distribution networks, enhances reliability, and boosts renewable energy integration through smart grid technologies. Latin America, at 9.3%, is led by Brazil and Mexico. The Middle East and Africa, at 6.8%, are driven by Saudi Arabia's Vision 2030 infrastructure investments and Sub-Saharan Africa's electrification programs.

Competitive Landscape

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Hitachi Energy |

Composite insulators, Bushings |

Leader |

12–15% global HV category share; full product range; HVDC expertise |

|

Siemens AG |

Composite, Ceramic, Switchgear Insulators |

Leader |

~10–12% transmission-level share; integrated grid equipment |

|

NGK Insulators Ltd. |

Porcelain, Composite, Specialty |

Leader |

Global ceramic insulator technology benchmark: Japan ecosystem |

|

Hubbell Incorporated |

Porcelain, Polymer, Composite |

Challenger |

Strong North America position; distribution and transmission focus |

|

BHEL |

Porcelain, Glass, Composite |

Challenger |

Dominant India position; government utility supply programs |

|

MacLean-Fogg Company |

Composite, Polymer |

Challenger |

North America composite strength; smart grid compatibility |

|

Seves Group |

Glass Insulators |

Niche Leader |

Global glass insulator specialist; Sediver brand; overhead line focus |

|

PFISTERER |

Composite, Cable Interface |

Niche Player |

Cable end insulation and composite specialization; European focus |

The global electric insulator market is moderately consolidated, led by a few multinational conglomerates and specialized regional players. Competition focuses on material technology, voltage range, certifications, distribution, and lifecycle services. Leading firms are accelerating R&D in composite, nano-coated, and smart insulators, while capacity expansions in India, Sweden, and Asia-Pacific enhance supply resilience and reduce lead times.

Key Company Profiles

Hitachi Energy

Hitachi Energy is a major force in transformer insulation and composite insulator manufacturing, with a strategic focus on enabling the energy transition through advanced transmission and substation solutions.

- Product & Platform Portfolio: Composite insulators for transformers, circuit breakers, and power electronics; EHV-class pressboard; laminated board for transformer insulation; power transmission equipment components.

- Recent Developments: In January 2025, Hitachi Energy announced the expansion of its composite component factory in Piteå, Sweden, increasing its workforce by 50% and investing in new machinery to meet rising global demand.

- Strategic Focus: Hitachi Energy is positioning its insulator capabilities as integral components of its end-to-end grid solution offering, including HVDC systems, transformers, and digital substations. Its dual investment strategy in Sweden and India reflects both developed-market quality leadership and emerging-market capacity growth priorities.

NGK Insulators Ltd.

NGK Insulators is the global technology benchmark for ceramic/porcelain insulator manufacturing, with manufacturing expertise built over more than a century and deep relationships with Japanese and international utility customers. The company occupies the leading position in specialty ceramic insulators for transmission and railway applications.

- Product & Platform Portfolio: Porcelain suspension and pin insulators, ceramic disc insulators, composite long-rod insulators, railway insulators, and ultra-high-voltage ceramic designs.

- Recent Developments: In January 2026, CNN International Commercial and NGK Insulators launched a global cross‑platform campaign highlighting NGK’s advanced ceramic technologies and sustainability focus, reinforcing NGK’s premium positioning amid competition from composite materials.

- Strategic Focus: NGK's strategy focuses on defending its ceramic quality leadership while expanding its composite portfolio for markets where polymer performance advantages are decisive. The company leverages its deep utility relationships in Japan, the U.S., and Europe to sustain specification-level positioning in major grid upgrade projects.

Siemens AG

Siemens AG (via Siemens Energy) is a key player in the global electric insulator market, with a significant share in high-value applications. It focuses on integrated insulation systems within transmission equipment rather than standalone insulators.

- Product & Platform Portfolio: HV/EHV bushings, GIS insulation systems, station post insulators, HVDC wall bushings, and surge arresters.

- Recent Developments: In February 2026, Siemens Energy approved an investment of approximately ₹20.6 billion (~$226.33 million) through internal accruals to set up a 30,000 MVA power transformer factory.

- Strategic Focus: System-level integration (GIS, transformers, HVDC), digital monitoring, sustainability (eco-friendly insulation), and turnkey grid projects—targeting premium, high-spec applications.

Investment & Growth Opportunities

Fastest-Growing Segments

Composite insulators are the highest-growth material sub-segment at approximately 6.8% CAGR through 2034, driven by offshore wind farm connections requiring marine-grade polymer insulators, HVDC transmission corridors demanding specialized DC-rated composite designs, and the replacement cycle of aging ceramic insulators in high-pollution coastal and industrial environments. Smart insulators with embedded IoT sensors represent the highest value-addition opportunity, commanding significant premiums over conventional designs.

Emerging Market Expansion

Sub-Saharan Africa represents the most structurally underpenetrated insulator market globally, with universal electricity access targets requiring 160 GW of new generation capacity and 130 million new grid connections through 2030. Southeast Asia's rapidly urbanizing grid expansion programs and India's continued electrification push offer large-volume procurement opportunities for mid-range insulator manufacturers with competitive pricing and regional manufacturing capabilities. HVDC sub-station insulators represent a premium emerging niche as long-distance renewable energy corridors are commissioned.

Capital and M&A Trends

Strategic capacity investments have been notable across leading manufacturers, with Hitachi Energy committing USD 36 million to its India facility in August 2025 and expanding its Sweden composite factory in January 2025. Private equity interest in regional insulator manufacturers in India and Southeast Asia is growing on the back of structural power system growth, while collaboration between composite insulator suppliers and offshore wind developers is creating multi‑year supply commitments that enhance revenue visibility.

Future Market Outlook (2026-2034)

The global electric insulator market forecast projects steady value expansion from USD 14.35 Billion in 2025 to USD 21.41 Billion by 2034 at a CAGR of 4.55%, representing cumulative value creation of USD 7.06 Billion underpinned by renewable energy infrastructure buildout, grid modernization investment cycles, and the ongoing material transition toward composite and polymer insulator technologies across premium application segments.

Three key trends will reshape the electric insulator market through 2034: accelerating ceramic-to-composite adoption, mainstreaming of smart insulators with condition-based monitoring, and growth of HVDC-specific insulators with higher value-per-unit economics. By 2034, the industry will shift from a materials-focused commodity to a solutions-oriented market emphasizing sensors, warranties, lifecycle services, and digital monitoring. Asia-Pacific will remain dominant in volume, while North America and Europe capture outsized value from premium HVDC and composite demand..

Research Methodology

Primary Research

Primary research encompassed structured interviews with electric insulator industry stakeholders, including product directors at leading insulator manufacturers, utility procurement managers, grid operator engineers, renewable energy project developers, and independent electrical engineering consultants. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments across major regional markets.

Secondary Research

Secondary sources include IEA World Energy Outlook, IRENA renewable capacity statistics, World Bank electrification data, IEC and ANSI standards documentation, European Commission energy infrastructure program publications, national energy ministry reports from India, China, and the U.S., company annual reports and investor presentations, and trade publications including Transmission & Distribution World, Power Technology, and IEEE Electrical Insulation Magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, electricity demand projections, T&D capital expenditure estimates, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty, raw material price volatility, and policy risk factors.

Electric Insulator Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Ceramic/Porcelain, Glass, Composites, Others |

| Voltages Covered | Low, Medium, High |

| Categories Covered | Bushings, Other Insulators |

| Installations Covered | Distribution Networks, Transmission Lines, Substations, Railways, Others |

| Products Covered | Pin Insulator, Suspension Insulator, Shackle Insulator, Others |

| Ratings Covered | <11 kV, 11 kV, 22 kV, 33 kV, 72.5 kV, 145 kV, Others |

| Applications Covered | Transformer, Cable, Switchgear, Busbar, Surge Protection Device, Others |

| End Use Industries Covered | Utilities, Industries, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Hitachi Energy, Siemens AG, NGK Insulators Ltd., Hubbell Incorporated, BHEL, MacLean-Fogg Company, Seves Group, PFISTERER, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electric insulator market from 2020-2034.

- The electric insulator market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electric insulator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Electric Insulator Market Report

The global electric insulator market was valued at USD 14.35 Billion in 2025, driven by grid modernization, renewable energy integration, and expanding electrification programs globally.

The market is projected to reach USD 21.41 Billion by 2034, growing at a CAGR of 4.55% during 2026-2034, driven by offshore wind integration, HVDC expansion, composite material adoption, and smart grid investments.

Ceramic/Porcelain leads with a 48.1% share in 2025, driven by its proven dielectric reliability and mechanical strength in high-voltage transmission and distribution infrastructure globally.

Bushings dominate with a 54.2% share in 2025, driven by the global proliferation of transformer, circuit breaker, and switchgear installations in utility substations and renewable energy generation facilities.

Asia-Pacific leads with a 37.5% share in 2025, driven by China's ultra-high-voltage grid expansion, India's large-scale electrification programs, and growing grid investment across Southeast Asian emerging economies.

Key drivers include grid modernization investments, renewable energy infrastructure buildout requiring new transmission lines, EV charging network expansion, HVDC transmission deployment, and rural electrification programs across Africa and Asia targeting universal energy access.

Composite insulators are the fastest-growing material segment at approximately 6.8% CAGR through 2034, driven by offshore wind applications, HVDC transmission, and their superior performance in high-pollution and extreme-weather environments.

Leading companies include Hitachi Energy, Siemens AG, NGK Insulators Ltd., Hubbell Incorporated, BHEL, MacLean-Fogg Company, Seves Group, PFISTERER, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)