Electric Vehicle Motor Market Size, Share, Trends and Forecast by Power Rating, Application, and Region, 2026-2034

Electric Vehicle Motor Market Size, Share, Trends & Forecast (2026-2034)

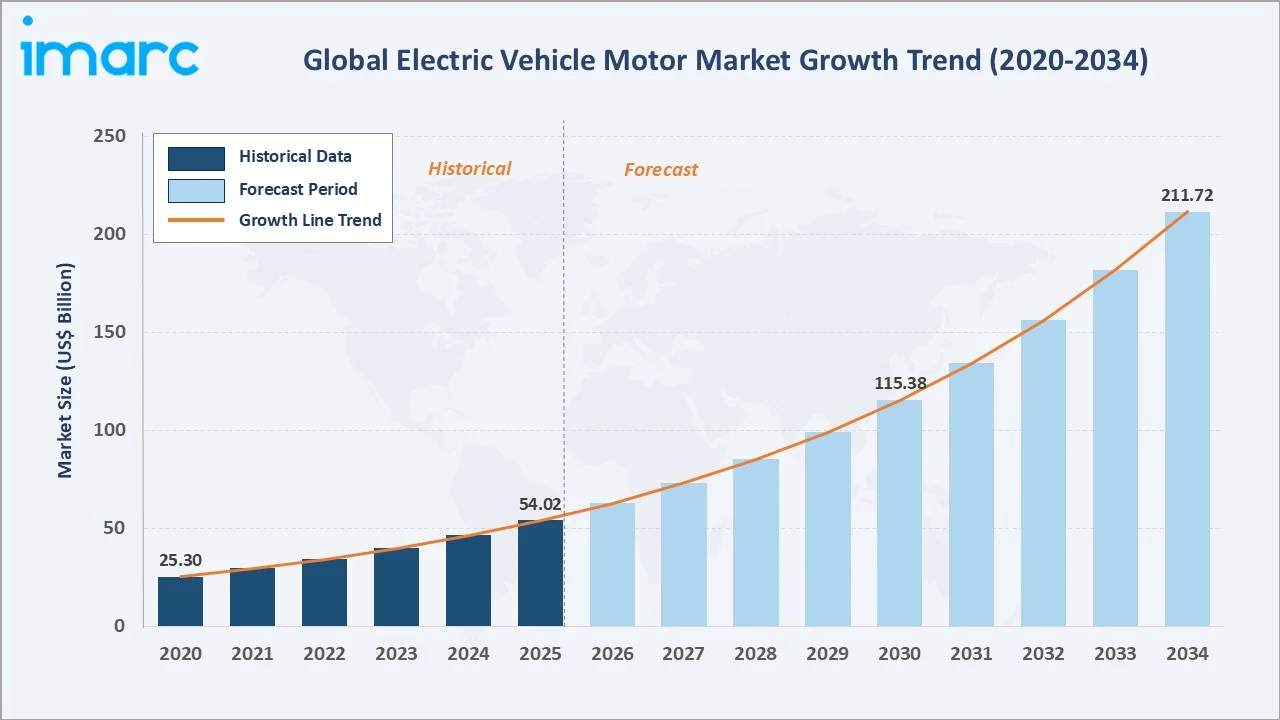

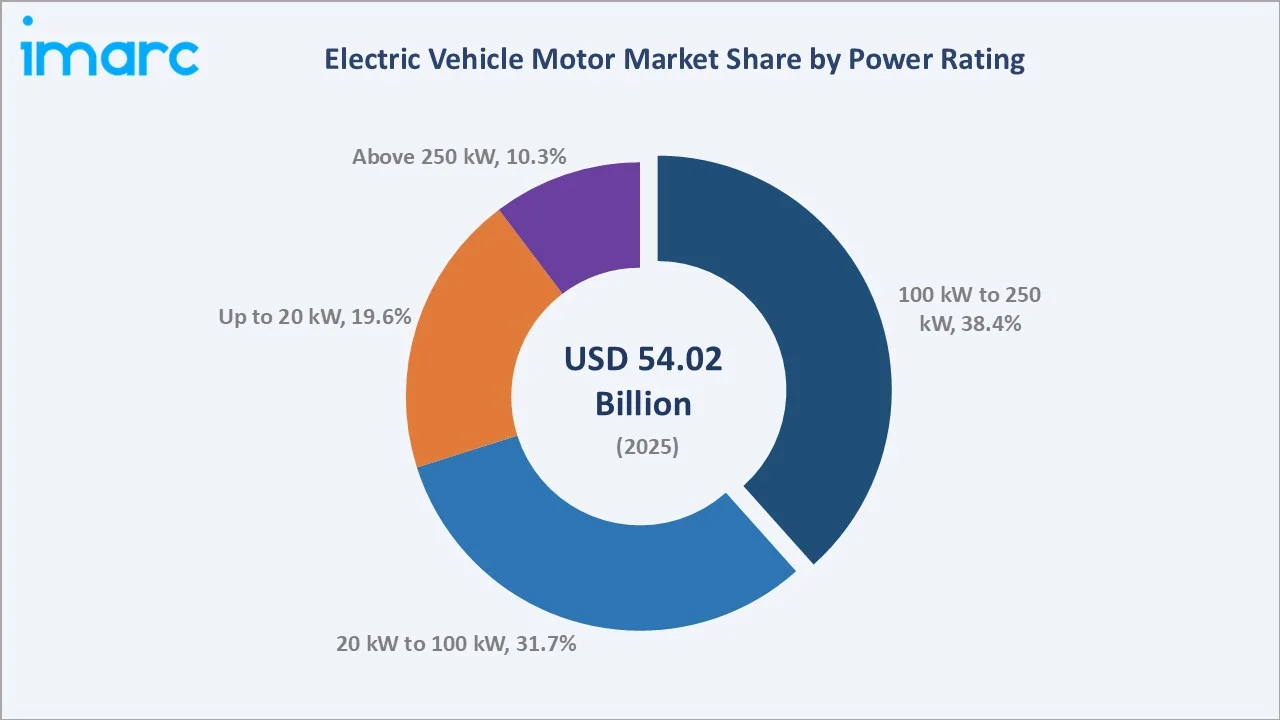

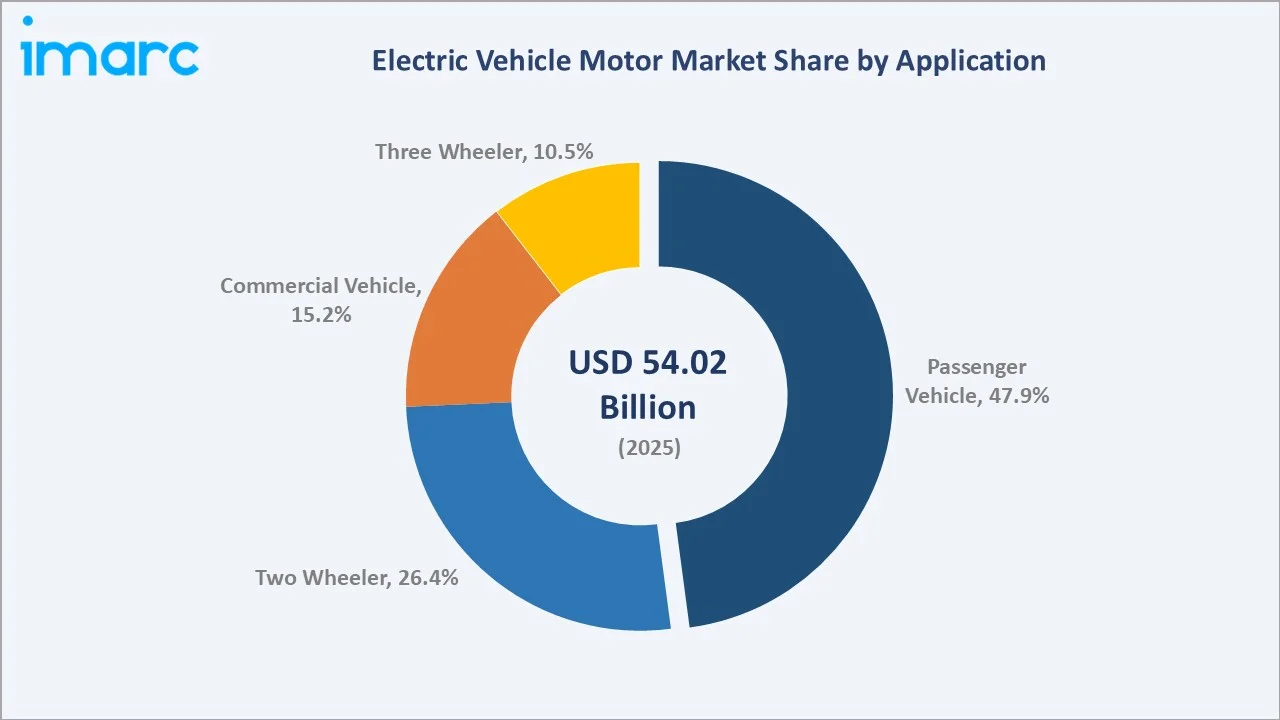

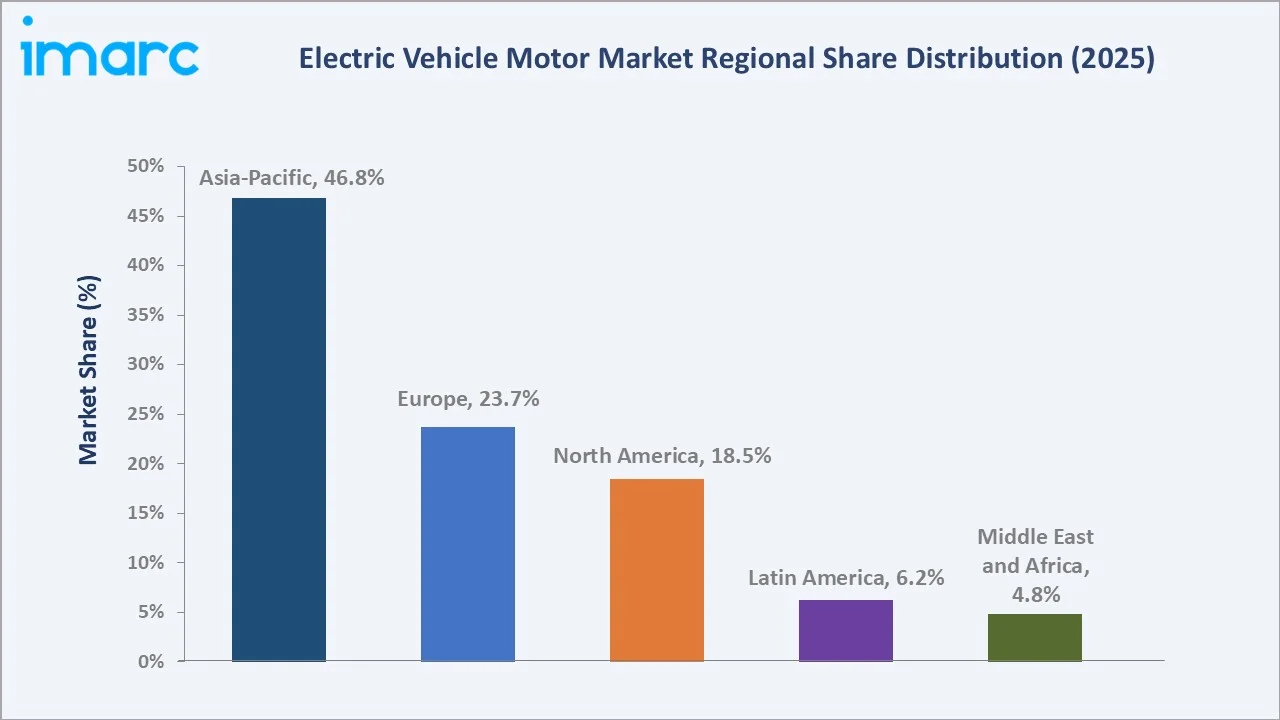

The global electric vehicle motor market reached USD 54.02 Billion in 2025 and is projected to reach USD 211.72 Billion by 2034, growing at a CAGR of 16.39% during 2026-2034. The market is driven by rising EV adoption, stricter emission regulations, government incentives, and automakers’ transition toward electrified powertrains. Electric car sales surpassed 20 million units in 2025, registering a 20% year-on-year increase, with China contributing more than 13 million sales and nearly 60% of global demand. This rapid expansion in EV production and sales is directly accelerating demand for electric vehicle motors, as automakers require greater volumes of efficient, high-performance traction motors to support growing vehicle output. The 100 kW to 250 kW from the power rating segment dominates at 38.4%. Passenger vehicles lead applications at 47.9%. Asia-Pacific commands 46.8% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 54.02 Billion |

| Forecast Market Size (2034) | USD 211.72 Billion |

| CAGR (2026-2034) | 16.39% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Leading Power Rating | 100 kW to 250 kW (38.4% share, 2025) |

| Leading Application | Passenger Vehicle (47.9% share, 2025) |

| Leading Region | Asia-Pacific (46.8% share, 2025) |

The market expanded from USD 25.30 Billion in 2020 to USD 54.02 Billion in 2025 - more than doubling in five years - anchored at USD 115.38 Billion in 2030 and forecast to reach USD 211.72 Billion by 2034. The semiconductor shortage created EV motor production constraints through inverter chip unavailability, but did not reverse the structural demand trajectory, which recovered sharply through 2023-2024 as chip supply normalized and OEM BEV production targets intensified.

To get more information on this market, Request Sample

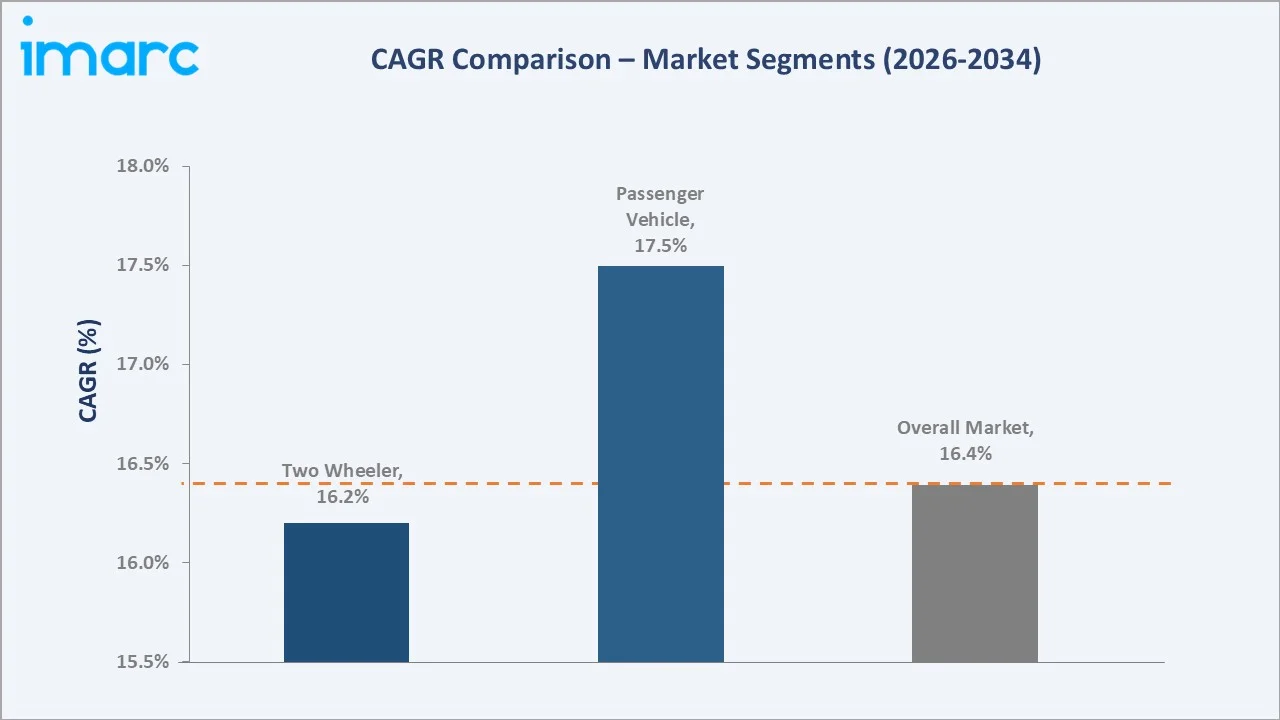

Passenger vehicle application grows fastest at ~17.5% CAGR as multi-motor BEV platforms (dual and quad-motor configurations) multiply motor units per vehicle, and the global BEV fleet continues compounding above overall vehicle production growth. The 100-250 kW power band grows at ~17.2% CAGR as the mainstream BEV passenger car (70-220 kW per motor) represents the world's highest-volume EV motor procurement category.

Executive Summary

The global electric vehicle motor market reached USD 54.02 Billion in 2025, representing one of the automotive industry's highest-growth technology component markets driven by the fundamental electrification transformation of global road transport. The EV traction motor is the defining powertrain component of the BEV, performing the function that the internal combustion engine, transmission, and driveshaft combined performed in conventional vehicles. The market is projected to reach USD 211.72 Billion by 2034.

The 100 kW to 250 kW power rating at 38.4% dominates by capturing the mainstream BEV passenger car market. Passenger vehicle application at 47.9% leads through the global BEV fleet's compounding demand and the highest per-unit motor value among all applications. Asia-Pacific at 46.8% leads globally through China's BEV production scale, Japan's motor manufacturing dominance, India's two-wheeler electrification, and the region's combined EV production and motor manufacturing concentration.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Power Rating | 100 kW to 250 kW – 38.4% revenue share (2025) |

| Dominant Application | Passenger Vehicle – 47.9% market share (2025) |

| Leading Region | Asia-Pacific – 46.8% market share (2025) |

| Market Opportunity | Axial flux PMSM; rare-earth-free wound-rotor motors; in-wheel hub systems; India two-wheeler BLDC scale-up; commercial EV motors |

Key Analytical Observations Supporting The Above Data:

- 100 kW to 250 kW at 38.4%: The 100 kW to 250 kW segment dominates as it provides an optimal balance of power, efficiency, driving range, and cost for high-volume passenger EVs, particularly sedans and SUVs. Its widespread adoption in electric passenger cars and medium-duty commercial vehicles by major OEMs such as Tesla and BYD further strengthens segment demand.

- Passenger Vehicle at 47.9%: The passenger vehicle segment dominates due to the high volume of electric cars sold worldwide, supported by expanding model availability, government incentives, and growing consumer adoption. With global electric car sales exceeding 20 million units in 2025, passenger EV production generates substantial demand for traction motors used in cars and SUVs.

- Asia-Pacific at 46.8%: The Asia-Pacific region dominates the electric vehicle motor market due to its large-scale EV production base and strong consumer demand, led primarily by China. In 2025, China alone accounted for over 13 million electric car sales, thereby generating substantial demand for EV traction motors.

Electric Vehicle Motor Market Overview

The global electric vehicle motor market encompasses the design, manufacture, and supply of all electric traction motors used to propel electric vehicles across all vehicle categories, such as passenger cars, electric two-wheelers, electric three-wheelers, electric commercial vehicles, construction equipment EVs, and defence EVs.

The ecosystem integrates EV motor and e-axle system manufacturers, permanent magnet suppliers, electrical steel producers for motor core laminations, power semiconductor manufacturers for inverters, inverter manufacturers, EV OEM vehicle manufacturers, and regulatory bodies setting EV motor efficiency standards. Macroeconomic factors include rising fuel prices, government incentives, stricter emission policies, growing urbanization, and investments in EV infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

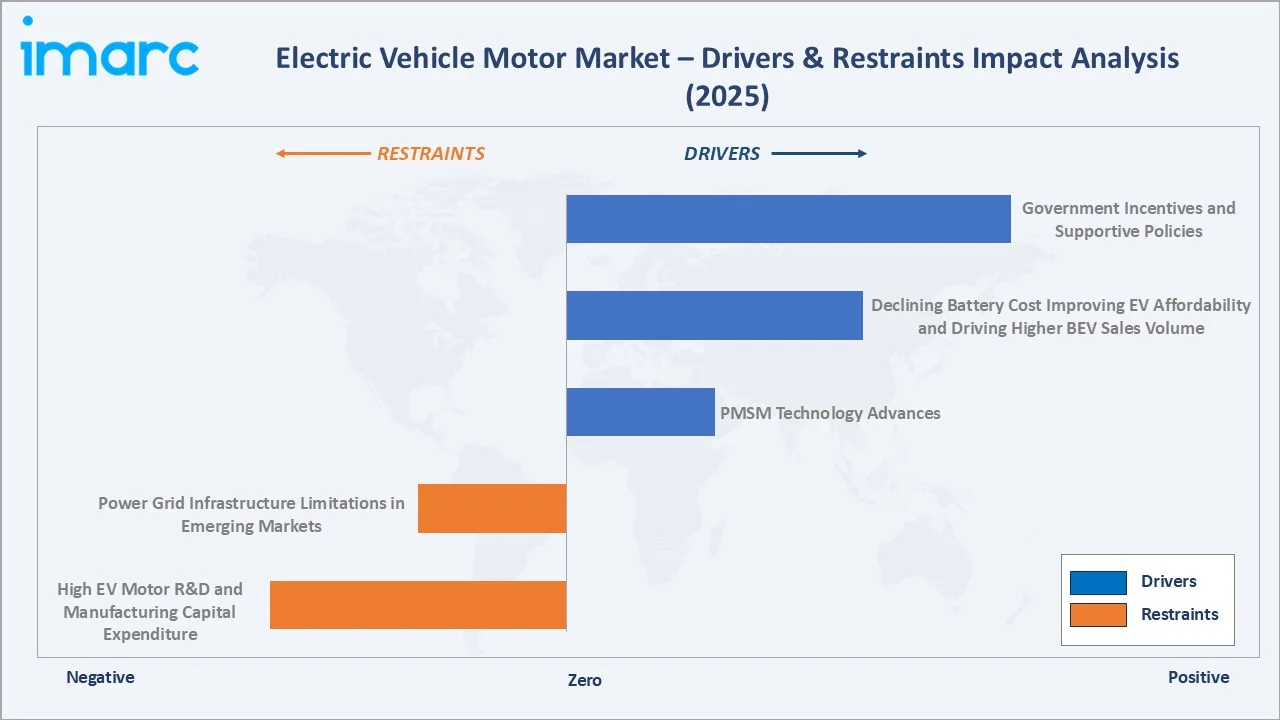

- PMSM Technology Advances: Permanent magnet synchronous motor (PMSM) technology advances improve motor efficiency, power density, and torque performance, enabling longer driving ranges and better vehicle acceleration. Advanced PMSMs also offer compact designs, lower energy losses, and enhanced thermal management, making them suitable for modern EV platforms. Their widespread adoption by automakers in passenger EVs and high-performance electric vehicles is increasing demand for advanced electric vehicle motors. PMSM motors are up to 15% more efficient than induction motors and are the most power-dense type of traction motors.

- Declining Battery Cost Improving EV Affordability and Driving Higher BEV Sales Volume: Declining battery costs are improving EV affordability by reducing overall vehicle prices, making battery electric vehicles (BEVs) more accessible to a broader consumer base. Lower costs are accelerating BEV adoption and increasing global sales volumes, leading automakers to expand EV production capacity. As every BEV requires one or more traction motors, rising BEV output directly boosts demand for electric vehicle motors and related motor technologies.

- Government Incentives and Supportive Policies: Government incentives and supportive policies are accelerating EV adoption through subsidies, tax credits, purchase incentives, and reduced registration fees. Many governments are also implementing stricter emission regulations and electrification targets, encouraging automakers to expand EV production. As of June 30, 2025, in India, the government incentivized more than 16.29 lakh EVs under the FAME II scheme, including electric two-wheelers, three-wheelers, four-wheelers, and buses. This highlights how policy support, subsidies, and public funding are accelerating EV adoption, increasing vehicle production, and directly boosting demand for electric vehicle motors across multiple segments.

Market Restraints

- High EV Motor R&D and Manufacturing Capital Expenditure: High EV motor R&D and manufacturing capital expenditure increases upfront costs for technology development, testing, tooling, and production facilities. Advanced motors require precision engineering, rare-earth materials, thermal management systems, and specialized manufacturing equipment, raising overall production costs. This can limit entry for smaller players, slow capacity expansion, and increase EV motor prices, affecting mass adoption.

- Power Grid Infrastructure Limitations in Emerging Markets: Power grid infrastructure limitations in emerging markets are restricting the expansion of EV charging networks and slowing EV adoption. Inadequate grid capacity, unstable electricity supply, and limited charging infrastructure reduce consumer confidence and delay large-scale electrification. Lower EV deployment consequently limits vehicle production volumes and reduces demand for electric vehicle motors.

Market Opportunities

- Axial Flux Motor Commercialization: Axial flux motor commercialization, enabling lighter, more compact, and higher power-density motor designs. These motors can improve vehicle efficiency, acceleration, and driving range, making them attractive for next-generation EV platforms. As automakers seek space-saving and performance-oriented motor solutions, wider adoption of axial flux technology can open new growth avenues for EV motor manufacturers.

- Rare-Earth-Free Wound Rotor Synchronous Motor: Rare-earth-free wound rotor synchronous motors reduce dependence on costly and supply-constrained rare-earth magnets. These motors can help automakers lower material risk, improve supply chain security, and meet sustainability goals. As EV production scales globally, demand for magnet-free motor designs is expected to rise, creating growth opportunities for advanced motor manufacturers.

Market Challenges

- Chinese Domestic EV Motor Supplier Development Creating Competitive Pressure on International Tier-1 Market Share in China: Chinese domestic EV motor supplier development is increasing competitive pressure on international Tier-1 suppliers operating in China. Local suppliers often offer cost-competitive motors, faster customization, and closer partnerships with Chinese EV OEMs. This can reduce market share, pricing power, and profit margins for global motor manufacturers in the world’s largest EV market.

- EV Motor NVH Whine Requiring Advanced Design Solutions as EV Powertrain Noise Becomes Primary Passenger Experience Differentiator: EV motor NVH (noise, vibration, and harshness) whine is becoming a key challenge as powertrain noise increasingly influences passenger comfort and vehicle perception. High-frequency motor noise and vibrations require advanced motor designs, precision engineering, acoustic insulation, and improved control systems. Addressing these issues increases R&D complexity and development costs for manufacturers while becoming a critical differentiator in EV performance and user experience.

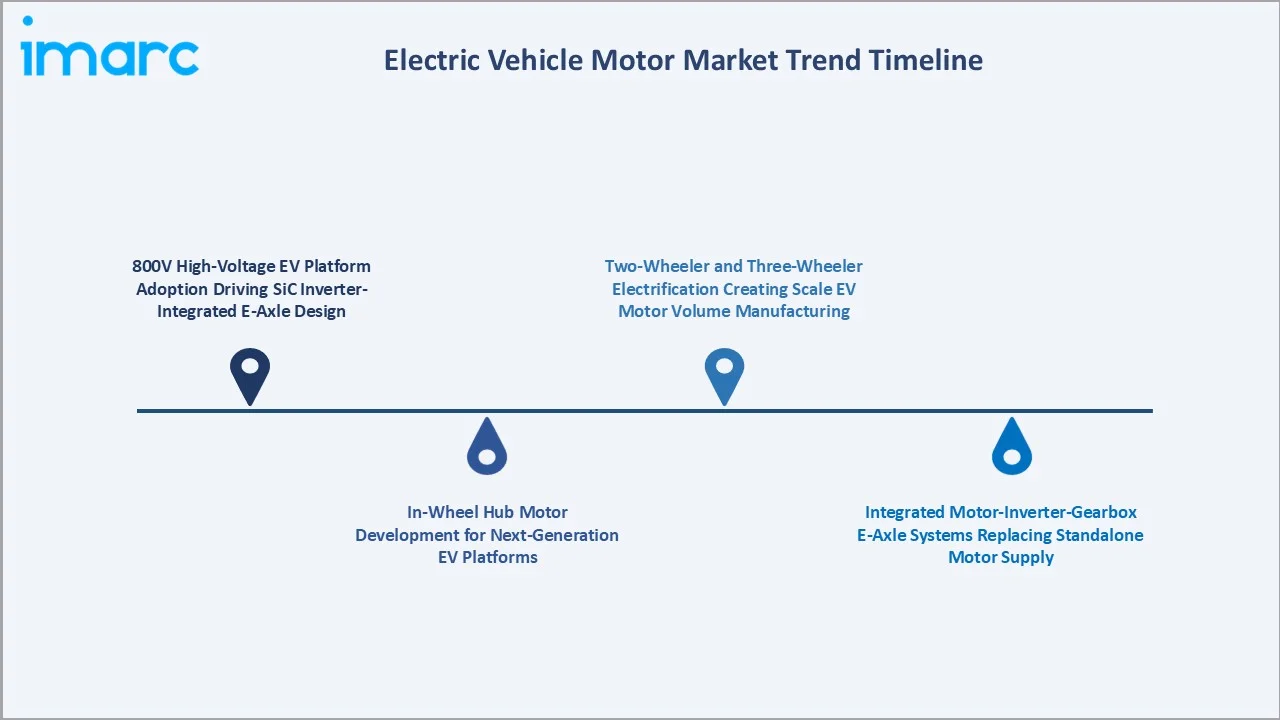

Emerging Market Trends

1. 800V High-Voltage EV Platform Adoption Driving SiC Inverter-Integrated E-Axle Design

Adoption of 800V high-voltage EV platforms enables faster charging, higher efficiency, and improved power delivery. This is driving the integration of SiC (silicon carbide) inverter-based e-axle systems, which reduce energy losses and improve motor performance. Compact e-axle designs also support vehicle lightweighting and extended driving range, increasing demand for advanced EV motor technologies. In July 2025, Sensata Technologies launched its High Efficiency Contactor (HEC), an advanced solution designed to ease the shift from 400V to 800V EV architectures. The HEC supports both existing and next-generation charging infrastructure while improving safety, efficiency, and system integration. This shift toward 800V systems is also accelerating the adoption of SiC inverter-integrated e-axle designs, which improve motor efficiency, reduce energy losses, and enhance overall EV powertrain performance.

2. In-Wheel Hub Motor Development for Next-Generation EV Platforms

In-wheel hub motor development integrates motors directly into the wheels, reducing drivetrain complexity and improving space utilization. This design can enhance vehicle efficiency, torque control, and handling performance. As next-generation EV platforms focus on lightweight, modular, and high-performance architectures, hub motors are gaining attention for future passenger cars, commercial EVs, and autonomous mobility solutions.

3. Integrated Motor-Inverter-Gearbox E-Axle Systems Replacing Standalone Motor Supply

Integrated motor-inverter-gearbox e-axle systems are emerging as OEMs shift from standalone motor procurement to compact, ready-to-install drivetrain modules. These systems improve powertrain efficiency, reduce weight, save space, and simplify EV assembly. As automakers seek cost-effective and high-performance EV platforms, demand is rising for suppliers offering complete integrated e-drive solutions.

4.Two-Wheeler and Three-Wheeler Electrification Creating Scale EV Motor Volume Manufacturing

Two-wheeler and three-wheeler electrification is emerging as these vehicle categories generate high-volume EV demand, especially in Asia-Pacific markets. Their rapid adoption creates large-scale production opportunities for compact, cost-efficient electric motors. As manufacturers expand volume manufacturing, motor suppliers benefit from economies of scale, lower unit costs, and wider market penetration.

Industry Value Chain Analysis

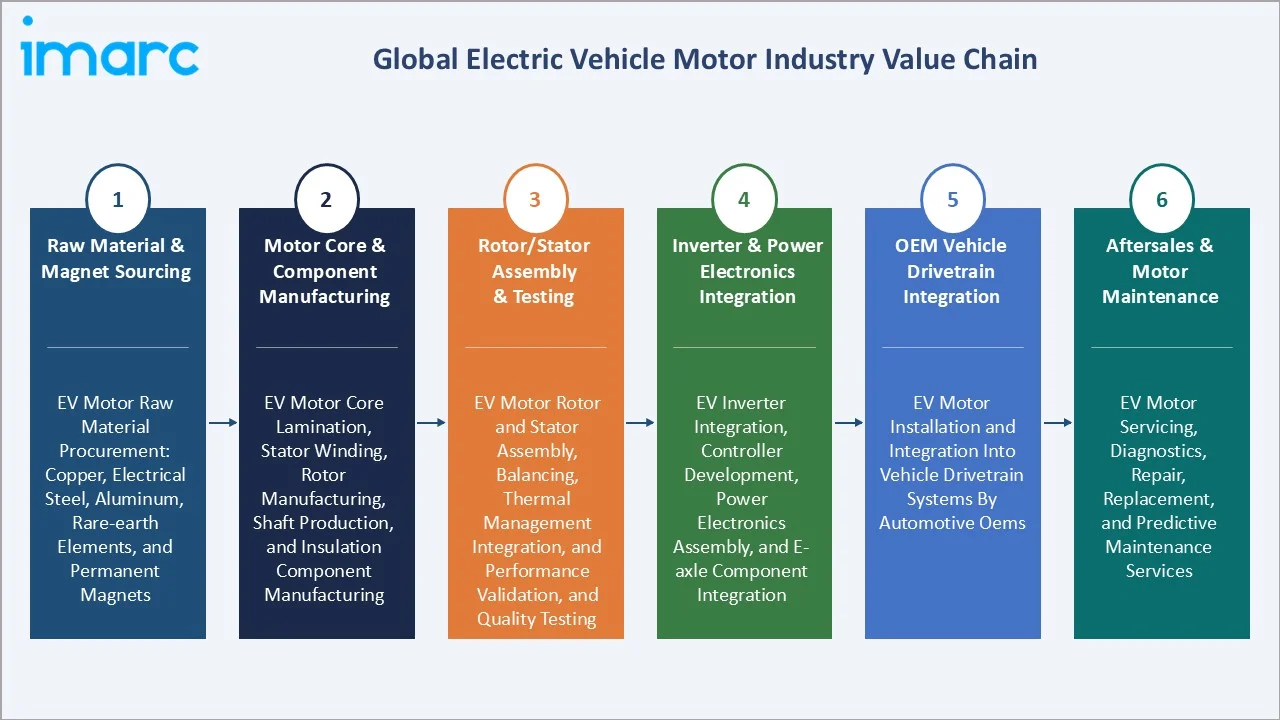

The EV motor value chain integrates raw material and magnet sourcing, motor core and component manufacturing, rotor/stator assembly and performance testing, inverter and power electronics integration, OEM vehicle drivetrain integration, and after-sales motor maintenance. The value chain's commercial architecture has been progressively consolidating toward integrated e-axle assembly as the primary commercial format, replacing the former upstream-downstream separation between motor manufacturer, inverter manufacturer, and gearbox manufacturer.

| Stage | Key Participants |

|---|---|

| Raw Material & Magnet Sourcing | EV motor raw materials procurement, including copper, electrical steel, aluminum, rare-earth elements, and permanent magnets |

| Motor Core & Component Manufacturing | EV motor core lamination, stator winding, rotor manufacturing, shaft production, and insulation component manufacturing |

| Rotor/Stator Assembly & Testing | EV motor rotor and stator assembly, balancing, thermal management integration, performance validation, and quality testing |

| Inverter & Power Electronics Integration | EV inverter integration, controller development, power electronics assembly, and e-axle component integration |

| OEM Vehicle Drivetrain Integration | EV motor installation and integration into vehicle drivetrain systems by automotive OEMs |

| Aftersales & Motor Maintenance | EV motor servicing, diagnostics, repair, replacement, and predictive maintenance services |

The raw material and magnet sourcing tier is the EV motor value chain's most commercially critical and geopolitically sensitive stage. The inverter and power electronics integration tier is experiencing the EV motor value chain's most rapid technology transition as silicon inverters are progressively displaced by silicon carbide SiC inverters for EV platforms.

Technology Landscape in the Electric Vehicle Motor Industry

Permanent Magnet Synchronous Motor (PMSM) Technology

Permanent magnet synchronous motor (PMSM) technology offers high efficiency, superior power density, and strong torque performance. PMSMs enable longer driving ranges, compact motor designs, and improved energy utilization, making them the preferred choice for modern EV platforms. Their compatibility with high-performance and premium EV applications is accelerating technological innovation and adoption across the industry.

Brushless DC Motor (BLDC) Technology

Brushless DC Motor (BLDC) technology offers high efficiency, low maintenance, compact size, and reliable performance. BLDC motors provide precise speed control and strong torque response, making them suitable for electric two-wheelers, three-wheelers, and compact EVs. Their cost-effectiveness and durability support wider adoption in mass-market electric mobility applications.

Silicon Carbide SiC Inverter Technology

In November 2025, Wolfspeed introduced its new 1200V SiC six-pack power modules, designed to enhance performance in high-power inverter applications. Using advanced Gen 4 SiC MOSFET technology and improved packaging, the modules offer significantly higher power cycling capability and deliver 15% greater inverter current capacity within a standard industry footprint. This supports silicon carbide (SiC) inverter technology by enabling more efficient, compact, and high-power EV inverter designs. Improved inverter performance enhances motor efficiency, power delivery, and thermal reliability, supporting next-generation EV motor and e-axle systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Power Rating |

100 kW to 250 kW |

38.4% |

2025 |

|

Application |

Passenger Vehicle |

47.9% |

2025 |

|

Region |

Asia-Pacific |

46.8% |

2025 |

By Power Rating

The 100 kW to 250 kW segment leads at 38.4% in 2025, encompassing the mainstream passenger BEV traction motor range, the most commercially competitive and highest-revenue product category in the EV motor market.

To access detailed market analysis, Request Sample

The 20 kW to 100 kW segment at 31.7% captures small passenger BEVs and performance electric motorcycles. Up to 20 kW at 19.6% represents the highest-unit-count segment, driven by India and China's electric two-wheeler and three-wheeler volume. Above 250 kW at 10.3% serves performance BEVs and electric commercial vehicles at premium per-unit motor values.

By Application

Passenger vehicles lead at 47.9% through the highest per-unit motor value and compounding BEV fleet volume growth. The passenger vehicle segment's above-market CAGR (~17.5%) reflects dual-motor platform proliferation that multiplies motor units per vehicle above simple fleet volume growth. Two-wheelers at 26.4% capture the world's highest-unit-count EV motor application, led by China's high annual electric bicycle production and India's high annual electric scooter sales.

Commercial vehicles at 15.2% are experiencing the fastest absolute revenue growth as electric buses and electric delivery vans create high-value motor procurement. Three-wheelers at 10.5% reflect India's and China's electric autorickshaw and cargo three-wheeler market volumes at above-market CAGR as India's high annual electric three-wheeler sales continue expanding.

Regional Market Insights

| Region | Share (2025) | Key EV Motor Market Drivers & Characteristics |

|---|---|---|

| Asia-Pacific | 46.8% | Driven by its strong EV production capacity, expanding battery manufacturing, supportive government policies, and high EV adoption across major economies |

| Europe | 23.7% | Driven by stringent emission regulations, vehicle electrification targets, investments in EV manufacturing, and increasing demand for sustainable mobility solutions |

| North America | 18.5% | Supported by EV production expansion, government incentives, charging infrastructure investments, and localization of EV supply chains |

| Latin America | 6.2% | Driven by increasing electrification initiatives, fleet electrification, and rising investments in electric mobility |

| Middle East & Africa | 4.8% | Emerging with growing EV adoption, infrastructure development initiatives, and increasing interest in sustainable transportation solutions |

Asia-Pacific, at 46.8%, leads through China's electric vehicle dominance, Japan's manufacturing scale, and India's two-wheeler electrification. Europe, at 23.7%, reflects EU CO2 mandate-driven BEV production growth and European EV motor technology leadership.

North America, at 18.5%, reflects EV manufacturing investment and US BEV adoption. Latin America, at 6.2%, and MEA, at 4.8%, represent early-stage but growing EV motor markets primarily driven by Brazil's electric bus fleet and GCC premium EV imports, respectively.

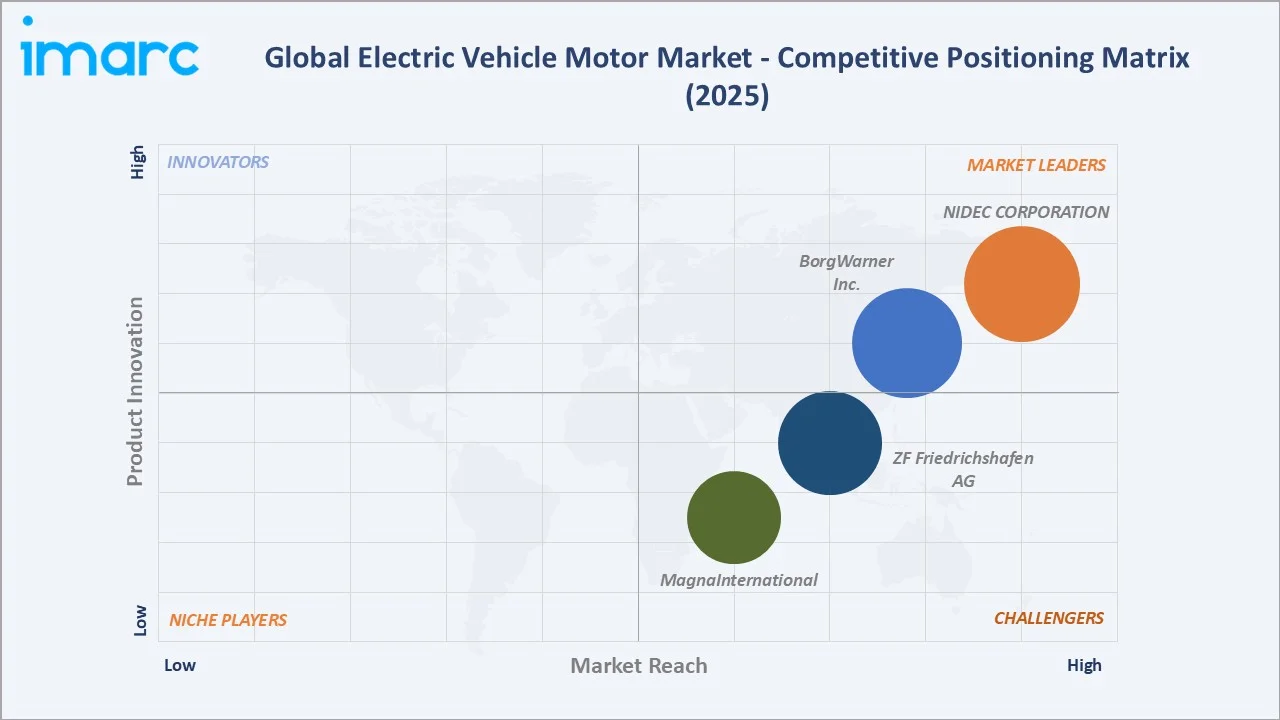

Competitive Landscape

The global electric vehicle motor market competitive landscape is moderately concentrated with three distinct competitive tiers: global full-system e-axle Tier-1s, speciality technology companies, and emerging domestic Chinese motor manufacturers competing primarily in the Chinese domestic OEM supply.

| Company Name | Key Products | Market Position | Core Strength |

|---|---|---|---|

| NIDEC CORPORATION | E-Axle Motor System | Market Leader | Nidec Corporation specializes in the development and mass production of E-Axle traction motor systems. |

| BorgWarner Inc. | 152 PMSM Drive Motor, 155 PMSM Drive Motor, 240 PMSM Drive Motor, HVH Series Electric Motors | Market Leader | BorgWarner Inc. is a leading Tier 1 automotive supplier transitioning from a combustion-focused company to a dominant player in the electric vehicle (EV) motor market. |

| ZF Friedrichshafen AG | em:SELECT | Strong Challenger | ZF Friedrichshafen AG specializes in the development and production of integrated, high-efficiency e-drives, electric motors, and power electronics for passenger cars and commercial vehicles. |

| Magna International Inc. | EtelligentDrive (Low/Mid/High) | Strong Challenger | Magna International Inc. specializes in the design, engineering, and manufacturing of electric powertrains (e-drives), gearboxes, and related power electronics. |

The competitive landscape is being actively reshaped by OEM vertical integration decisions. Each OEM captive motor manufacturing investment reduces the addressable external EV motor supply market for Tier-1s, but the scale of global BEV production growth creates more total market growth than any realistic level of OEM captive integration can absorb, sustaining growth for external EV motor Tier-1 suppliers through the forecast period.

Key Company Profiles

NIDEC CORPORATION

NIDEC CORPORATION is a Japan-based manufacturer of electric motors and automotive systems with a strong presence in the electric vehicle motor market through its E-Axle traction motor systems and integrated e-drive technologies.

- Key Products: E-Axle Motor System.

- Recent Developments: In November 2025, Nidec Corporation started full-scale production at its new Orchard Hub campus in Hubli-Dharwad, Karnataka. Built with an investment of USD 55 million, the 50-acre facility is Nidec’s largest and most advanced manufacturing site in India and produces key energy-transition products, including EV motors, EV chargers, wind turbine generators, BESS, and high-efficiency drives.

- Strategic Focus: Expanding integrated EV traction motor and E-Axle systems, combining motors, inverters, and reducers for efficient electric drivetrains.

BorgWarner Inc.

BorgWarner Inc. is a global automotive technology company with a strong presence in the electric vehicle motor market through its electrified propulsion portfolio.

- Key Products: 152 Permanent Magnet Synchronous Drive Motor, 155 Permanent Magnet Synchronous Drive Motor, 240 Permanent Magnet Synchronous Drive Motor, HVH Series Electric Motors.

- Recent Developments: In April 2026, BorgWarner secured three new e-motor programs in China and South Korea, covering BEV and hybrid vehicle applications. The contracts include stator assemblies, S-winding P2 motors, and generator units, with production expected to begin between mid-2026 and late 2027.

- Strategic Focus: Expanding its e-motor, integrated drive module, and power electronics portfolio for BEV and hybrid applications. The company is also strengthening its EV motor programs across key Asian markets, including China and South Korea.

Market Concentration Analysis

The EV motor market is moderately concentrated at the full-system e-axle Tier-1 level, with NIDEC CORPORATION, BorgWarner Inc., ZF Friedrichshafen AG, and Magna International Inc. collectively accounting for approximately 40-50% of global passenger car and light commercial EV traction motor revenue. OEM captive motor manufacturing accounts for an estimated 25-35% of global passenger BEV motor supply, with Chinese domestic motor manufacturers accounting for 10-15% of the global market volume. Market concentration is declining over the forecast period as Chinese domestic motor suppliers gain quality certification for mainstream BEV applications and new entrants create new competitive segments at the premium tier.

Investment & Growth Opportunities

Highest Growth Segments

Passenger vehicle application (~17.5% CAGR), 100-250 kW power band (~17.2% CAGR), commercial vehicle EV motor (~18-20% CAGR from smaller base), axial flux PMSM premium market (~25-30% CAGR from USD 200-300M base), India two-wheeler BLDC motor scale (~30%+ CAGR), SiC inverter-integrated e-axle (~20% CAGR), and rare-earth-free WRSM motor development (~15% CAGR from near-zero commercial base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Commercial vehicle EV motor systems represent the EV motor market's highest per-unit-value emerging opportunity, electric bus and electric truck traction motors at USD 3,000-20,000 per unit generate 3-10x the per-unit revenue of passenger car EV motors at equivalent power ratings, with European commercial vehicle electrification mandates creating a structurally growing demand pool through 2034.

Investment Themes

- SiC vertical integration for EV motor inverter manufacturing as a structural cost advantage through 2034: The silicon carbide value chain represents a USD 5-10 Billion investment programme for any EV motor Tier-1 seeking full SiC vertical integration. EV motor Tier-1s that achieve below-market SiC device cost through vertical integration create a sustainable EV motor inverter cost advantage that cannot be replicated by competitor’s dependent on external SiC procurement in a supply-constrained market.

- India's two-wheeler and three-wheeler EV motor manufacturing investment, capturing the world's fastest-growing unit volume EV motor market: India's electric two-wheeler market growth trajectory creates a 9x unit volume increase requiring a corresponding scale-up of BLDC hub motor supply, a market currently served primarily by domestic suppliers alongside some Chinese BLDC motor imports.

Future Market Outlook (2026-2034)

The global electric vehicle motor market is projected to grow from USD 54.02 Billion in 2025 to USD 211.72 Billion by 2034, delivering a 16.39% CAGR over the forecast period. The market's anchor value of USD 115.38 Billion in 2030 represents an EV motor industry at its most transformative commercial inflection. The 100-250 kW PMSM e-axle will have displaced standalone motor supply as the dominant commercial format, SiC inverters are expected to achieve wider adoption, particularly in higher-voltage and performance-oriented BEV platforms, India's electric two-wheeler market growth, creating a dedicated high-volume BLDC motor manufacturing ecosystem, and axial flux PMSM will have achieved its first mainstream OEM deployment.

Three structural forces define EV motor market growth through 2034 with exceptional confidence. The BEV fleet compounding growth creates a self-reinforcing demand cycle where EV motor investment begets BEV adoption, which begets further motor demand. The multi-motor platform proliferation trend multiplies the motor units per vehicle demanded above simple fleet volume growth, creating an additional 15-20% demand multiplier beyond headline BEV sales growth rates. The two-wheeler and commercial vehicle EV market convergence creates an additive EV motor market demand above the already rapid passenger BEV motor market growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Chief Technology Officers; OEM EV powertrain leads; two-wheeler EV motor specialists; SiC power electronics engineers; and commercial vehicle EV motor programme leads.

Secondary Research

Secondary research encompassed company annual reports; IEA Global EV Outlook and production projections; Electric Vehicle Outlook 2025 battery cost and BEV adoption forecasts; Society of Automotive Engineers EV motor technology conference papers 2024; China Association of Automobile Manufacturers; India Ministry of Road Transport and Highways EV registration data; EV motor and drivetrain market forecast 2025; EV drivetrain technology study 2024. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using EV production-based bottom-up model: (i) global BEV production forecast by vehicle type (passenger car, two-wheeler, three-wheeler, commercial vehicle); (ii) average motor unit count per vehicle by type; (iii) average motor revenue per vehicle by power rating and application multiplied by annual production volume; (iv) technology premium adjustment for e-axle integrated system versus standalone motor pricing.

Electric Vehicle Motor Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Power Ratings Covered | Up to 20 kW, 20 kW to 100 kW, 100 kW to 250 kW, Above 250 kW |

| Applications Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | NIDEC CORPORATION, BorgWarner Inc., ZF Friedrichshafen AG, Magna International Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electric vehicle motor market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global electric vehicle motor market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electric vehicle motor industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Electric Vehicle Motor Market Report

The global EV motor market reached USD 54.02 Billion in 2025, driven by the 100-250 kW PMSM traction motor segment dominant at 38.4%, passenger vehicle application leading at 47.9%, China's high annual BEV sales requiring EV traction motors, Asia-Pacific commanding 46.8% market share through China and Japan's combined EV production and motor manufacturing scale, and India's electric two-wheeler market contributing the world's fastest-growing EV motor unit volume pool.

The EV motor market grows at 16.39% CAGR during 2026-2034, reaching USD 211.72 Billion by 2034. This growth reflects global BEV fleet compounding demand, multi-motor platform proliferation creating 1.5-2.0 motor units per BEV vehicle average, India's two-wheeler electrification, commercial vehicle EV market emerging as a high-value new segment, and premium e-axle integrated system pricing growth.

The 100 kW to 250 kW segment leads at 38.4%, capturing the mainstream BEV passenger car traction motor specification. This segment grows at ~17.2% CAGR through multi-motor platform proliferation and BEV passenger car production expansion.

Passenger vehicle leads at 47.9% through the highest per-unit motor value and compounding BEV fleet growth, creating sustained procurement expansion. Passenger Vehicle grows fastest at ~17.5% CAGR through dual-motor platform proliferation, multiplying motor units per vehicle above simple BEV sales growth.

Asia-Pacific leads at 46.8% through China's high annual BEV sales, Japan's largest EV motor manufacturers, and India's electric two-wheeler rapid growth.

Leading companies include NIDEC CORPORATION, BorgWarner Inc., ZF Friedrichshafen AG, and Magna International Inc., among others.

The EV motor market is projected to reach approximately USD 115.38 Billion by 2030, with 800V SiC e-axle becoming a standard specification for new premium passenger BEV platforms, India's electric two-wheeler BLDC motor market growth, commercial vehicle EV motor growth, and axial flux PMSM motors beginning mainstream OEM adoption.

Three priority investment opportunities: SiC vertical integration for EV motor inverter manufacturing, India BLDC hub motor manufacturing for two-wheeler and three-wheeler electrification, and axial flux PMSM technology commercialization partnership.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)