Electrolyte and Vitamin Water Market Size, Share, Trends and Forecast by Fortification, Variants, Type, Packaging, Distribution Channel, and Region, 2026-2034

Electrolyte and Vitamin Water Market Size and Share:

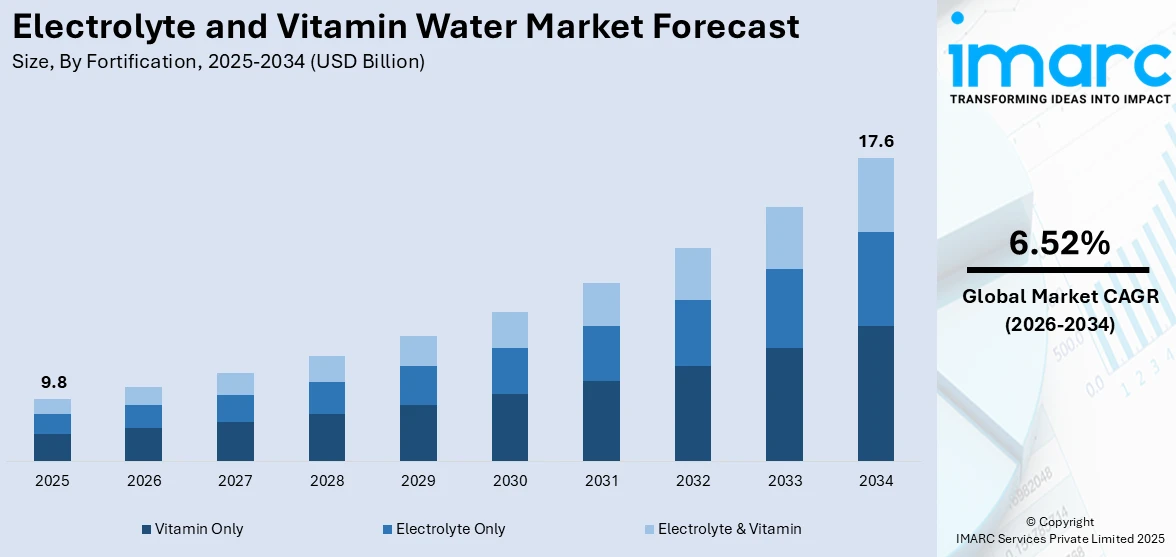

The global electrolyte and vitamin water market size was valued at USD 9.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 17.6 Billion by 2034, exhibiting a CAGR of 6.52% from 2026-2034. North America currently dominates the market, holding a market share of 37% in 2025. The region benefits from a well-established retail infrastructure, high consumer spending on health and wellness beverages, increasing preference for functional hydration products among fitness-oriented demographics, and growing distribution networks across supermarkets, convenience stores, and e-commerce platforms, all expanding to the electrolyte and vitamin water market share.

The international electrolyte and vitamin water market is undergoing substantial growth due to increased consumer awareness about the need for proper hydration and vitamin intake. The increasing number of lifestyle diseases, such as dehydration, electrolyte disorders, and vitamin deficiencies, is pushing consumers to opt for vitamin-enriched drinks as a part of their regular health and wellness regimens. Furthermore, the increasing trend of fitness activities, sports, and gym culture across the globe is fueling the demand for hydration drinks that provide functional benefits beyond mere hydration. Additionally, the increasing innovation in product development, such as the introduction of natural flavors, organic, and low-calorie electrolyte and vitamin water, is attracting health-conscious consumers who value clean-label and transparent product offerings, thus contributing to the electrolyte and vitamin water market growth.

The United States of America has turned out to be a prominent region in the electrolyte and vitamin water market due to a number of reasons. The well-developed health and wellness culture in the United States has led to a significant demand for functional beverages that not only quench thirst but also offer essential vitamins and electrolytes. The rising engagement levels in fitness activities, sports, and outdoor games among people of all age groups have led to a consistent demand for electrolyte-enhanced beverages. For example, the Health & Fitness Association (HFA) revealed in 2024 that more than 77 million Americans have gym memberships, indicating a widespread engagement in fitness activities that contributes to the demand for performance-driven hydration products. In addition, the well-developed retail infrastructure with prominent supermarket chains, health stores, and rapidly expanding e-commerce platforms ensures easy product accessibility. The focus on preventive healthcare and the rising demand for beverages with added nutritional value over carbonated drinks are further boosting demand in the country.

To get more information on this market Request Sample

Electrolyte and Vitamin Water Market Trends:

Rising Clean Label Consumer Preferences

The rising demand for clean-label beverages is having a major impact on the electrolyte and vitamin water market. Today’s consumer is increasingly examining the ingredient deck and seeking out beverages that use natural, recognizable, and minimally processed ingredients. This is forcing manufacturers to reformulate their offerings by removing artificial colors, sweeteners, and preservatives in favor of plant extracts, natural fruit flavors, and organic vitamin blends. The focus on transparency in labeling is forcing brands to be more open about their labeling and nutritional claims on packaging. Furthermore, the trend towards cleaner labels is being reinforced by regulatory changes in various markets that are forcing brands to improve labeling standards and ingredient disclosure. Retailers are also devoting more shelf space to clean-label beverages in response to consumer demand for healthier beverage options. In 2025, in a move to further strengthen its presence in the functional beverage and hydration category, Coca-Cola has launched Powerade Power Water, a zero-sugar electrolyte beverage designed for the growing health, wellness, and fitness-oriented consumer base.

Functional Hydration Beyond Sports Applications

The emerging trend of functional hydration products in non-sporting domains is having a major impact on the electrolyte and vitamin water market outlook. Electrolyte and vitamin water products are being positioned for their general wellness benefits, such as boosting the immune system, improving mental performance, enhancing skin health, and serving as a recovery drink after illness or exhaustion. This has led to a wider appeal of electrolyte and vitamin water products to a broader customer base, including working professionals, students, seniors, and health-conscious families, in addition to sports enthusiasts. Micronutrient deficiencies, particularly folate (vitamin B9) and vitamin B12, are extremely prevalent in India. A meta-analysis conducted recently (2015-2020) showed that 37% of the Indian population is deficient in folate, and 53% have inadequate vitamin B12 levels. Companies are developing niche products with functional ingredients such as adaptogens, collagen, B-vitamins, zinc, and magnesium to meet the varied functional needs. The trend of premiumization in general hydration beverages, along with targeted marketing communications that highlight the general wellness benefits, is helping to position electrolyte and vitamin water as a necessary daily drink category.

Sustainable Packaging Innovation Trends

The growing need for environmental sustainability is also fueling innovation in packaging in the electrolyte and vitamin water industry, thereby adding to the electrolyte and vitamin water market forecast. Consumers and governments are also pushing the industry to adopt environmentally sustainable packaging solutions that have minimal plastic waste and carbon footprints. This is also fueling the use of recycled PET bottles, plant-based packaging materials, biodegradable packaging materials, and light-weight aluminum packaging alternatives. Major players in the industry are also investing heavily in closed-loop recycling systems and environmentally sustainable supply chain management to meet global environmental commitments. For example, the European Commission announced in February 2025 that the European Union's single-use plastics directive had led to a decrease in plastic waste from beverage bottles in the European Union member countries since the directive came into effect. The need for sustainable packaging is also fueling competitive differentiation, as environmentally conscious consumers are also willing to pay a higher price for products that have globally verified environmental credentials.

Electrolyte and Vitamin Water Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global electrolyte and vitamin water market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on fortification, variants, type, packaging, and distribution channel.

Analysis by Fortification:

- Vitamin Only

- Electrolyte Only

- Electrolyte & Vitamin

Vitamin only captures 38% of the market share. Vitamin-enriched water products have received considerable consumer acceptance as a means to provide a daily dose of micronutrients without the calorie intake that is associated with vitamin supplements and vitamin-fortified juices. These products usually contain vital vitamins like B-complex vitamins, vitamin C, vitamin D, and vitamin E, which are known to fulfill nutritional deficiencies in contemporary diets characterized by the consumption of processed foods and irregular eating habits. The increasing consumer interest in preventive health care and boosting the immune system has further fueled the demand for vitamin-enriched hydration products across various consumer segments. For example, the National Institutes of Health in the United States revealed in 2024 that a significant section of the American population was at risk of at least one vitamin deficiency, thus identifying the nutritional supplementation opportunity that is fulfilled by vitamin water products. Additionally, the convenience of acquiring vital vitamins through ready-to-drink products is especially attractive to busy urban consumers and the younger generation of consumers who are increasingly looking for convenient means to manage their health and wellness.

Analysis by Variants:

- Flavored

- Non-flavored

Flavored leads the market with a share of 70%. Flavored electrolyte and vitamin water products dominate consumer preferences owing to their ability to combine functional health benefits with appealing taste profiles that encourage regular consumption. Manufacturers offer an extensive range of flavor options, including citrus blends, tropical fruit combinations, berry infusions, and botanical extracts such as cucumber-mint and lavender-lemon, catering to diverse palate preferences across different regional markets. The palatability advantage of flavored variants is particularly significant in driving adoption among younger consumers and children who may otherwise resist plain or unflavored functional beverages. Apart from this, continuous flavor innovation, seasonal limited editions, and collaborations with popular lifestyle brands are sustaining consumer interest and encouraging repeat purchases within the flavored segment.

Analysis by Type:

- Sweetened

- Non-sweetened

Sweetened dominates the market, with a share of 65%. Sweetened electrolyte and vitamin water products maintain strong consumer demand due to their palatable taste profiles that encourage consistent hydration habits across broad population segments. These products utilize various sweetening agents, including natural sweeteners such as stevia, monk fruit extract, and agave, alongside traditional cane sugar and high-fructose corn syrup, providing options across different caloric preference ranges. The widespread consumer preference for beverages that deliver both functional nutrition and enjoyable flavor experiences positions sweetened variants as the dominant category in retail channels worldwide. For instance, the World Health Organization published findings in 2025 indicating that reformulated beverages using natural sweeteners experienced a higher consumer acceptance rates compared to artificially sweetened alternatives in global taste preference surveys. The ongoing reformulation efforts by manufacturers to reduce added sugar content while maintaining desirable sweetness levels are addressing evolving regulatory requirements and health-conscious consumer expectations.

Analysis by Packaging:

- PET

- Glass

- Aluminum

PET represents the leading segment, with a market share of 52%. PET bottles dominate the electrolyte and vitamin water market packaging landscape owing to their lightweight, durable, shatterproof, and cost-effective characteristics that make them ideal for both manufacturing and consumer convenience. Apart from this, the excellent clarity and versatility of PET packaging allows for attractive product presentation, customizable bottle shapes, and effective brand differentiation on retail shelves. PET bottles are favored across distribution channels, from supermarkets and convenience stores to vending machines and online delivery, owing to their portability and resealable functionality. Furthermore, advances in recycled PET technology and increasing incorporation of post-consumer recycled content are addressing environmental concerns while maintaining the functional advantages that make PET the preferred packaging material.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Supermarkets

- Convenience Stores

- Online Stores

- Specialty Stores

- Others

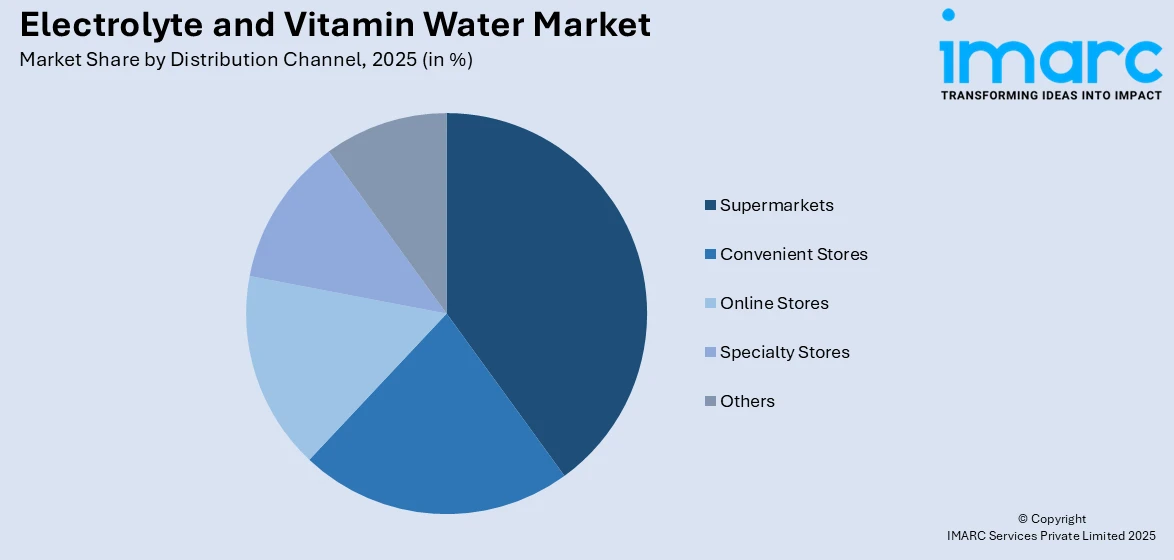

Supermarket holds 30% of the market share. Supermarkets serve as the primary retail channel for electrolyte and vitamin water products owing to their extensive product assortments, competitive pricing strategies, and the convenience of one-stop shopping experiences they offer to consumers. These retail formats provide dedicated beverage aisles and health-focused sections that facilitate product discovery and encourage impulse purchases of functional hydration products. The availability of multiple brands, pack sizes, and promotional offerings in supermarkets enables consumers to compare options and make informed purchasing decisions. Additionally, strategic shelf placement, end-cap displays, and in-store sampling programs employed by leading supermarket chains are effectively increasing product visibility and consumer trial rates for electrolyte and vitamin water brands.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 37% of the share, enjoys the leading position in the market. The region's dominance is underpinned by a highly developed health and wellness culture, strong consumer purchasing power, and extensive retail distribution infrastructure that ensures widespread product availability. The presence of established beverage manufacturers and a robust innovation ecosystem drives continuous product development, including new formulations with added functional ingredients targeting specific health outcomes. Increasing consumer awareness about electrolyte balance, hydration optimization, and daily vitamin requirements, supported by widespread digital health content and fitness influencer endorsements, sustains demand across diverse demographic segments. Additionally, the expanding direct-to-consumer and subscription-based delivery models are creating new revenue streams for brands operating in the region.

Key Regional Takeaways:

United States Electrolyte and Vitamin Water Market Analysis

The United States represents a critical growth driver within the electrolyte and vitamin water market, supported by a combination of high health awareness, significant disposable income levels, and a deeply entrenched fitness culture that spans all age demographics. The country's consumers are increasingly prioritizing functional beverages that deliver tangible health benefits, including enhanced hydration, immune support, and energy optimization, over conventional sugary soft drinks and carbonated beverages. The rapid proliferation of specialty health food retailers, wellness-focused grocery chains, and direct-to-consumer e-commerce platforms has expanded the accessibility of electrolyte and vitamin water products to both urban and suburban populations. Strategic marketing initiatives by major and emerging brands, leveraging social media influencers, sports sponsorships, and celebrity endorsements, are effectively driving brand recognition and consumer loyalty. The Council for Responsible Nutrition (CRN), the foremost trade association for the dietary supplement and functional food sector, announced today key results from its 2024 Consumer Survey, carried out by Ipsos, indicating that three-quarters of Americans still utilize dietary supplements. The reported 75% usage rate for this year is consistent with last year's figures, highlighting the continued importance of supplements in promoting health and wellness. The ongoing shift toward preventive healthcare approaches and the increasing adoption of personalized nutrition strategies are further strengthening the market position of functional hydration products across the nation, with particular growth observed in metropolitan areas.

Europe Electrolyte and Vitamin Water Market Analysis

The European electrolyte and vitamin water market is witnessing steady expansion driven by increasing health consciousness, stringent food safety regulations, and growing consumer demand for natural and organic functional beverages. European consumers demonstrate strong preferences for products with clean ingredient profiles, low sugar content, and transparent sourcing practices, encouraging manufacturers to develop premium formulations that comply with rigorous European Union food labeling standards. The region's established wellness culture, particularly in Western European nations such as Germany, France, and the United Kingdom, fosters consistent demand for hydration products enriched with vitamins and electrolytes. Government-led public health campaigns promoting adequate hydration and balanced nutrition are further supporting consumer adoption. Additionally, the growing influence of fitness trends, including running events, cycling communities, and yoga culture across European markets, continues to drive demand for functional hydration solutions among active lifestyle consumers.

Asia-Pacific Electrolyte and Vitamin Water Market Analysis

The Asia-Pacific electrolyte and vitamin water market is experiencing rapid growth fueled by rising disposable incomes, accelerating urbanization, and expanding health awareness among growing middle-class populations across the region. The increasing adoption of Western dietary habits and fitness culture, particularly in countries such as China, Japan, India, and Australia, is driving demand for functional hydration products. The hot and humid climatic conditions prevalent in many Asia-Pacific nations further amplify the need for electrolyte replenishment solutions. For instance, the Asian Development Bank reported that the developing economies of Asia and the Pacific are expected to expand by 5.0% this year due to robust domestic demand and significant export increases, representing a massive and growing market for premium health-oriented beverages. Expanding modern retail infrastructure, including hypermarkets, convenience store chains, and e-commerce platforms, is improving product accessibility across both urban centers and emerging tier-two cities throughout the region.

Latin America Electrolyte and Vitamin Water Market Analysis

The Latin American electrolyte and vitamin water market is expanding steadily, supported by increasing urbanization, growing health awareness, and rising consumer interest in functional beverages across the region. The tropical and subtropical climate conditions prevalent in major markets such as Brazil, Mexico, and Argentina drive natural demand for hydration-oriented products. Apart from this, the growing penetration of modern retail formats and e-commerce platforms is enhancing product availability and enabling brands to reach previously underserved consumer segments.

Middle East and Africa Electrolyte and Vitamin Water Market Analysis

The Middle East and Africa electrolyte and vitamin water market is witnessing gradual growth driven by extreme climatic conditions that necessitate regular hydration, increasing urbanization, and rising disposable incomes in key economies. The hot and arid climate across much of the region creates a fundamental need for electrolyte replenishment and hydration solutions. The expansion of modern retail infrastructure, growing health consciousness among younger demographics, and increasing availability of international beverage brands are supporting market development.

Competitive Landscape:

The competitive landscape of the electrolyte and vitamin water market is characterized by the presence of established multinational beverage corporations alongside a growing number of agile, health-focused startup brands competing for consumer attention. Major industry participants are deploying multi-faceted strategies encompassing product portfolio diversification, aggressive marketing campaigns leveraging digital and social media channels, strategic partnerships with fitness organizations and sports teams, and continuous investment in research and development to introduce innovative formulations. The market is witnessing increasing merger and acquisition activity as larger corporations seek to acquire niche brands with strong consumer followings in the functional beverage space. Companies are also investing significantly in sustainable packaging solutions and clean-label reformulations to align with evolving consumer preferences and regulatory requirements. The intensifying competition is driving price optimization strategies, premium product positioning, and geographic expansion initiatives as brands seek to establish or consolidate their positions across both developed and emerging markets worldwide.

The report provides a comprehensive analysis of the competitive landscape in the electrolyte and vitamin water market with detailed profiles of all major companies, including:

- Danone S.A.

- Essentia Water LLC (Nestlé USA)

- Frucor Suntory (Suntory Holdings Limited)

- Karma Culture LLC

- Keurig Dr Pepper Inc.

- PepsiCo Inc.

- Talking Rain Beverage Company

- The Alkaline Water Company Inc.

- The Coca-Cola Company

- Vitamin Well

- VOSS of Norway AS

Electrolyte and Vitamin Water Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fortifications Covered | Vitamin Only, Electrolyte Only, Vitamin and Electrolyte |

| Variants Covered | Flavored, Non-flavored |

| Types Covered | Sweetened, Non-sweetened |

| Packagings Covered | PET, Glass, Aluminum |

| Distribution Channels Covered | Supermarkets, Convenience Stores, Online Stores, Specialty Stores, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Danone S.A., Essentia Water LLC (Nestlé USA), Frucor Suntory (Suntory Holdings Limited), Karma Culture LLC, Keurig Dr Pepper Inc., PepsiCo Inc., Talking Rain Beverage Company, The Alkaline Water Company Inc., The Coca-Cola Company, Vitamin Well, VOSS of Norway AS, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electrolyte and vitamin water market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global electrolyte and vitamin water market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electrolyte and vitamin water industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Electrolyte and Vitamin Water Market Report

The electrolyte and vitamin water market was valued at USD 9.8 Billion in 2025.

The electrolyte and vitamin water market is projected to exhibit a CAGR of 6.52% during 2026-2034, reaching a value of USD 17.6 Billion by 2034.

The electrolyte and vitamin water market is primarily driven by increasing consumer health awareness, rising demand for functional hydration solutions, growing fitness culture globally, expansion of organized retail and e-commerce channels, and continuous product innovation in natural flavors, clean-label formulations, and sustainable packaging solutions that attract health-conscious consumers.

North America currently dominates the electrolyte and vitamin water market, accounting for a share of 37% in 2025. The region's leadership is supported by high consumer spending on health and wellness products, a well-established retail and e-commerce infrastructure, and strong fitness culture driving consistent demand.

Some of the major players in the electrolyte and vitamin water market include Danone S.A., Essentia Water LLC (Nestlé USA), Frucor Suntory (Suntory Holdings Limited), Karma Culture LLC, Keurig Dr Pepper Inc., PepsiCo Inc., Talking Rain Beverage Company, The Alkaline Water Company Inc., The Coca-Cola Company, Vitamin Well, VOSS of Norway AS, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)