Ethiopia Avocado Market Size, Share, Trends and Forecast by Form, Distribution Channel, and Region, 2026-2034

Ethiopia Avocado Market Summary:

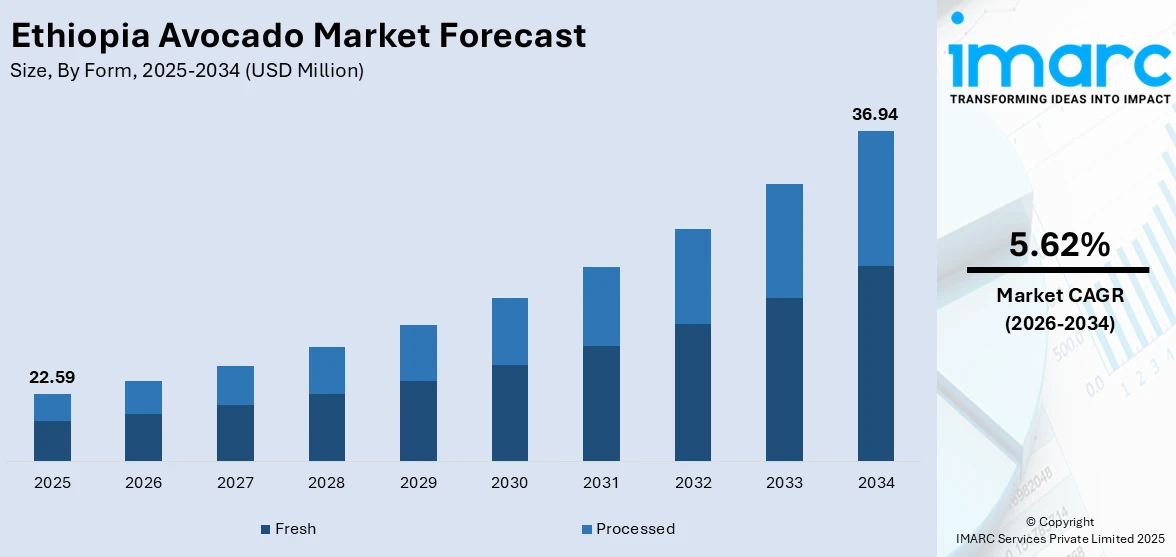

The Ethiopia avocado market size was valued at USD 22.59 Million in 2025 and is projected to reach USD 36.94 Million by 2034, growing at a compound annual growth rate of 5.62% from 2026-2034.

The Ethiopia avocado market is supported by favorable growing conditions, increasing local consumption, and rising export demand from international markets. Government-backed horticulture initiatives, collaboration with global partners, and the expansion of cultivation across key producing areas are encouraging steady market growth. At the same time, greater investment in processing facilities and improved cold chain infrastructure is strengthening supply chain efficiency. These developments are enhancing product quality, reducing post-harvest losses, and contributing to sustained expansion of Ethiopia’s avocado market share.

Key Takeaways and Insights:

- By Form: Fresh dominated the market with a share of 63.4% in 2025, driven by strong consumer preference for whole avocados in domestic markets and growing demand for fresh Hass variety exports to Europe and the Gulf region.

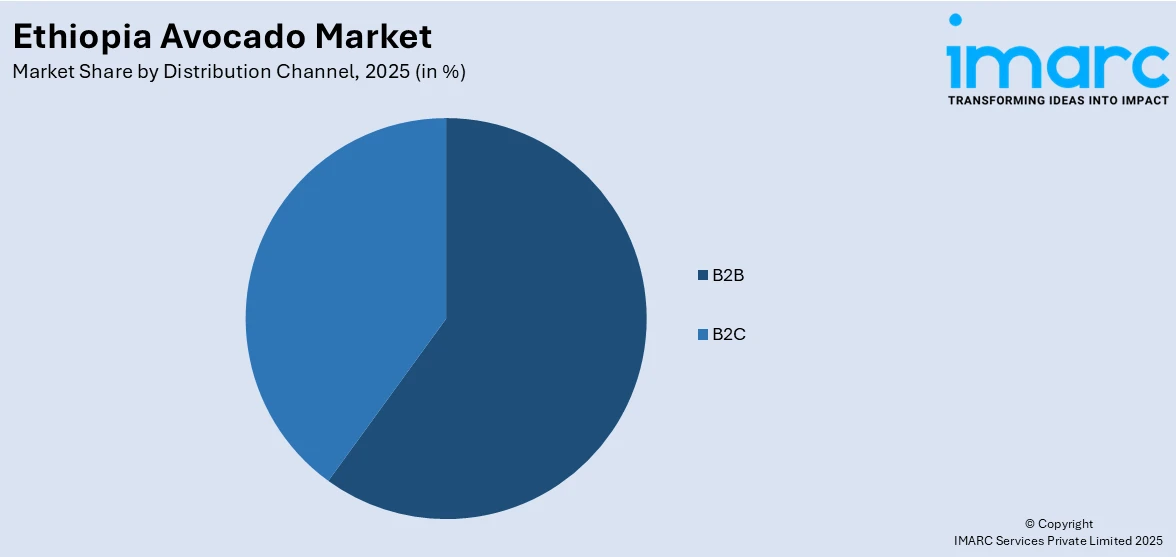

- By Distribution Channel: B2B leads the market with a share of 57.8% in 2025, owing to the dominance of bulk procurement by exporters, institutional buyers, and processing facilities sourcing directly from smallholder farmer cooperatives across major growing zones.

- By Region: Oromia Region represents the largest segment with a market share of 36.5% in 2025, supported by its vast cultivation area, favorable highland climate, and government-backed sapling distribution programs engaging thousands of smallholder farmers.

- Key Players: The Ethiopia avocado market features a fragmented competitive landscape with a mix of domestic agribusinesses, smallholder cooperatives, international development partners, and private investors. Market participants compete across the value chain, from seedling production and cultivation through processing and export logistics.

To get more information on this market Request Sample

The Ethiopia avocado market is experiencing a significant transformation driven by government-led expansion strategies and international development support. The Ethiopian government’s plan to increase avocado cultivation from approximately 30,000 hectares to 150,000 hectares by 2030 reflects the strategic importance of this sector to the nation’s agricultural diversification agenda. Under the Green Legacy Initiative, authorities have targeted the production and distribution of 1.8 million high-yield avocado seedlings in 2025, reinforcing their commitment to scaling production capacity. International partnerships, particularly with the Netherlands through the Centre for the Promotion of Imports from Developing Countries and the To SEA project, are facilitating the transition from costly air freight to sustainable sea freight for avocado exports. The regional agriculture authorities have established ambitious export goals and launched large-scale avocado planting initiatives across key cultivation areas, reflecting significant ongoing efforts to expand production capacity and strengthen the country’s avocado market, supporting both domestic growth and international trade opportunities.

Ethiopia Avocado Market Trends:

Transition from Air Freight to Sea Freight for Avocado Exports

Ethiopia is undertaking a strategic logistics overhaul, shifting avocado exports from expensive air cargo to cost-effective and sustainable sea freight. The Ethiopian Agriculture Authority and the Ethiopian Horticulture Producers and Exporters Association, supported by the Netherlands’ Development Partnership, have released an Avocado Export Guide to standardize maritime export procedures for domestic enterprises. The Cool Port Addis project, a dedicated cold-storage and logistics facility under construction at the Modjo Dry Port with an estimated investment of USD 50 million, will integrate directly with the Addis Ababa-Djibouti railway line to enable competitive perishable exports via the Port of Djibouti.

Growth of Avocado Oil Processing Infrastructure

Ethiopia’s avocado value chain is expanding beyond fresh fruit into processed products, with avocado oil emerging as a key segment. Industrial parks in southern and western regions have become major hubs for oil production, sourcing from thousands of smallholder farmers. At the Yirgalem Industrial Park in the Sidama region, avocado oil processing generates around 200 tons of pits and pulp each season, highlighting the scale of operations. The development of additional facilities is increasing extraction capacity, creating new income opportunities for farmers, and strengthening the overall avocado market while supporting value addition across the supply chain.

Expansion of Hass Avocado Cultivation for Export Markets

Ethiopian agriculture is increasingly focusing on cultivating high-value Hass avocado varieties tailored for international export markets. Government-led initiatives and collaborative horticulture programs have supported the distribution of improved avocado seedlings to thousands of smallholder farmers across key producing regions, enhancing both yield and quality. Rising global demand, particularly from Europe and the Middle East, is encouraging producers to adopt export-oriented practices and expand production capacity. These efforts are strengthening Ethiopia’s position in the international avocado market, boosting value addition, and supporting sustainable growth for smallholder farmers within the sector.

Market Outlook 2026-2034:

The Ethiopia avocado market is poised for sustained expansion over the forecast period, supported by government strategies to quintuple avocado farmland, improving cold chain infrastructure, and rising international demand for both fresh fruit and processed avocado products. The anticipated operationalization of Cool Port Addis will significantly enhance export competitiveness by enabling sea freight access via the Port of Djibouti, reducing logistics costs and expanding market reach to Europe and the Gulf states. The market generated a revenue of USD 22.59 Million in 2025 and is projected to reach a revenue of USD 36.94 Million by 2034, growing at a compound annual growth rate of 5.62% from 2026-2034.

Ethiopia Avocado Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Form |

Fresh |

63.4% |

|

Distribution Channel |

B2B |

57.8% |

|

Region |

Oromia Region |

36.5% |

Form Insights:

- Fresh

- Processed

- Pulp

- Guacamole

- Others

Fresh dominates with a market share of 63.4% of the total Ethiopia avocado market in 2025.

Fresh avocados form the backbone of Ethiopia’s avocado sector, reflecting strong local preferences for whole fruit consumption. The country’s highland regions provide favorable growing conditions that promote slower maturation and longer shelf life compared to lowland varieties. Domestically, avocados are sold through open-air markets, retail outlets, and institutional channels in urban centers, meeting consistent consumer demand. The combination of suitable agro-climatic conditions and well-established distribution networks supports year-round availability, ensuring that fresh avocados remain a staple in local diets while sustaining the domestic market’s growth.

Ethiopia’s fresh avocado exports are gaining traction, driven by growing demand in international markets. Counter-seasonal production relative to other major suppliers enhances the country’s appeal to buyers seeking a consistent supply. Expansion of avocado cultivation across key producing regions is strengthening export readiness, while improvements in temperature-controlled logistics are facilitating longer transit and reducing reliance on high-cost air shipments. These developments are enhancing Ethiopia’s competitiveness in the global fresh avocado market, supporting sustainable trade growth, and creating new opportunities for smallholder farmers and commercial producers alike.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- B2B

- B2C

- Processing Industry

- Food Service Industry

B2B leads with a share of 57.8% of the total Ethiopia avocado market in 2025.

The business-to-business distribution channel plays a central role in Ethiopia’s avocado market, connecting smallholder farmers with processors, exporters, and institutional buyers. Farmer cooperatives act as key aggregation points, enabling efficient sourcing for avocado oil processing facilities. This cooperative-based model ensures a reliable supply of raw materials while providing farmers with stable market access, fair pricing, and opportunities to participate in value-added production, strengthening the overall efficiency and resilience of the domestic avocado value chain.

Ethiopia’s B2B export channel is supported by growing logistics infrastructure and formal trade partnerships with international buyers. Standardized export guidelines help local producers navigate maritime shipping processes, enhancing the reliability and competitiveness of avocado exports. Strong B2B trade links are expanding access to regional and global markets, boosting Ethiopia’s presence in the international avocado sector and creating sustainable opportunities for smallholder farmers and commercial enterprises alike.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Oromia Region represents the largest share with 36.5% of the total Ethiopia avocado market in 2025.

Oromia Region plays a leading role in Ethiopia’s avocado market due to its extensive cultivation areas, favorable highland climate, and strong development initiatives. Large-scale planting programs across key zones have significantly expanded production capacity, supplying both domestic and international markets. Institutional support has facilitated coordinated efforts with farming clusters, improving access to improved seedlings and promoting consistent yields. The combination of suitable agro-climatic conditions, organized farming networks, and proactive cultivation strategies ensures Oromia remains a central hub for avocado production and a cornerstone of the country’s overall avocado supply.

Oromia’s importance extends to processing and logistics, with industrial parks hosting avocado oil facilities and cold chain infrastructure enhancing export readiness. Development of temperature-controlled logistics hubs with direct transport links to ports is strengthening the region’s supply chain efficiency. These investments support smooth domestic and international distribution, enabling the region to meet growing demand while maintaining quality standards. Oromia’s coordinated approach to production, processing, and logistics positions it as a strategic center for avocado exports and value-added products, reinforcing Ethiopia’s competitiveness in global avocado markets.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Avocado Market Growing?

Government-Led Cultivation Expansion and Agricultural Policy Support

The Ethiopian government has prioritized avocado cultivation as a key element of its broader agricultural diversification strategy, emphasizing high-value fruit crops over traditional horticulture. Large-scale planting initiatives are being rolled out across major producing regions, with improved seedlings distributed to smallholder farmers through coordinated regional programs. This integrated policy approach combines national directives with local implementation, creating a supportive framework that encourages widespread adoption of avocado farming. By fostering organized cultivation and enhancing access to quality planting material, the government is establishing the foundation for sustained production growth and positioning avocados as a strategic crop within Ethiopia’s agricultural landscape.

Development of Export-Oriented Cold Chain and Logistics Infrastructure

Investments in cold chain and logistics infrastructure are transforming Ethiopia’s avocado export capabilities by addressing long-standing supply chain challenges. Modern facilities are being developed to integrate with rail and road networks, providing end-to-end temperature-controlled handling for both sea and air shipments. Expansion of perishable cargo terminals further supports immediate export needs, while enabling more efficient transport of fresh avocados and processed products. These infrastructure improvements enhance market accessibility, reduce post-harvest losses, and strengthen the competitiveness of Ethiopian avocados in international markets.

Rising International Demand and Value-Added Processing Growth

The international market for avocados and its products presents opportunities to Ethiopian producers, especially given that the production cycle of this country supplements that of other major producers. The industry is also moving away from fresh fruit into value-added items like avocado oil, with the backing of industrial parks and processing plants that tap into the smallholder farmers. The growth of oil extraction and processing plants is diversifying the value chain, producing more value-added goods, and enhancing the prominence of Ethiopia in the global markets. This trend is increasing income opportunities for the producers and sustainable growth in the avocado industry.

Market Restraints:

What Challenges the Ethiopia Avocado Market is Facing?

Inadequate Post-Harvest Infrastructure and Cold Storage Limitations

There is a serious problem of post-harvest losses to the Ethiopian avocado industry because of a lack of adequate cold storage systems, especially in rural producing regions where most of the farms are located. The lack of access to refrigerated transportation and storage implies that a significant percentage of the harvested avocados are spoiled before they reach markets or processing plants. This infrastructure gap lowers the value that is realized in the markets in general and limits the capacity of smallholder farmers to engage effectively in the provision of higher-value export chains.

Limited Access to Quality Planting Materials and Technical Knowledge

Smallholder farmers in the Ethiopian avocado production zones are limited to accessing certified and disease-resistant avocado seedlings and up-to-date agronomic technologies. Unstable yields due to the usage of the old varieties and the lack of technical extension services lower productivity and product quality, diminishing the competitiveness of Ethiopian avocados on the global markets, requiring the presence of a uniform grade and the Global G.A.P. certification.

Weak Market Linkages and Price Information Asymmetry

Lack of access to real-time information about prices and fragmented market chains poses a major challenge to the Ethiopian producers of avocados. Farmers in smallholder situations do not have direct links with export buyers and processing plants; therefore, they are left at the mercy of intermediaries who end up taking a disproportionate value. Lack of centralized market facilities in the expanding communities limits price transparency and bargaining power of farmers with potentials to maximize income and reduce reinvestment in production advancement.

Competitive Landscape:

The Ethiopia avocado market is characterized by a fragmented competitive structure comprising smallholder farmer cooperatives, domestic agribusinesses, international development organizations, and private investors operating across the production, processing, and export segments. The market does not exhibit dominance by any single entity, reflecting the decentralized nature of avocado cultivation driven primarily by smallholder farming communities organized through cooperative structures. Competition is intensifying in the processing segment, where multiple avocado oil extraction facilities have commenced operations at agro-industrial parks in southern and western Ethiopia. Export market participation is being shaped by compliance capabilities, with players investing in Global G.A.P. certification and international quality standards to access premium European and Middle Eastern markets.

Recent Developments:

- December 2025: The Centre for the Promotion of Imports from Developing Countries (CBI) has introduced an Export Guide for Avocado via Sea Freight in Addis Ababa, aimed at helping Ethiopian growers and agribusinesses improve access to global avocado markets. The initiative focuses on strengthening export readiness by supporting the transition to maritime logistics and enhancing competitiveness in international trade.

- August 2025: The Sidama Regional Industrial Parks Development Corporation reported over USD 3.3 million in revenue from avocado oil exports for the fiscal year ending March 31, highlighting the region’s growing role in value-added avocado production and international trade.

- December 2024: The Oromia State Agriculture Bureau announced an export target of 1,200 tons of avocados for the 2024/25 fiscal year, having already shipped 61 tons to Europe. The Bureau initiated planting of 20 million avocado saplings, with 12.5 million already in the ground across 185 woredas.

Ethiopia Avocado Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Forms Covered |

|

|

Distribution Channels Covered |

|

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Avocado Market Report

The Ethiopia avocado market size was valued at USD 22.59 Million in 2025.

The Ethiopia avocado market is expected to grow at a compound annual growth rate of 5.62% from 2026-2034 to reach USD 36.94 Million by 2034.

Fresh represents the largest market share of 63.4% in 2025, driven by strong domestic consumer preference for whole avocado consumption and expanding export demand for Hass variety avocados in European and Middle Eastern markets.

Key factors driving the Ethiopia avocado market include government-led cultivation expansion through the Green Legacy Initiative, development of export-oriented cold chain infrastructure such as Cool Port Addis, rising international demand for fresh avocados and processed avocado oil, and expanding international partnerships supporting the horticulture sector.

Major challenges include inadequate post-harvest cold storage infrastructure in rural producing areas, limited access to certified planting materials and modern agronomic practices, weak market linkages and price information asymmetry for smallholder farmers, insufficient Global G.A.P. certification among producers, and logistical bottlenecks constraining export competitiveness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)