Ethiopia BNPL (Buy Now Pay Later) Market Size, Share, Trends and Forecast by Channel, Enterprise Size, End Use, and Region, 2026-2034

Ethiopia BNPL (Buy Now Pay Later) Market Summary:

The Ethiopia BNPL (buy now pay later) market size was valued at USD 11.58 Million in 2025 and is projected to reach USD 58.84 Million by 2034, growing at a compound annual growth rate of 19.8% from 2026-2034.

The Ethiopia BNPL market is gaining meaningful traction as the country accelerates its digital transformation and financial inclusion agenda. The rapid proliferation of mobile wallets, expanding e-commerce platforms, and rising consumer demand for flexible short-term financing are encouraging adoption across urban centers. Government-led digitization programs, regulatory reforms supporting fintech innovation, and increasing collaboration between technology firms and financial institutions are further driving interest in deferred payment models, positioning the country for sustained expansion in Ethiopia BNPL (buy now pay later) market share.

Key Takeaways and Insights:

- By Channel: Online holds the largest market share at 58.7% in 2025, reflecting the growing integration of BNPL solutions into Ethiopia's expanding e-commerce and digital retail platforms.

- By Enterprise Size: Large enterprises dominate the market with a 62.4% share in 2025, leveraging superior digital infrastructure and merchant partnerships to embed BNPL options across their retail ecosystems.

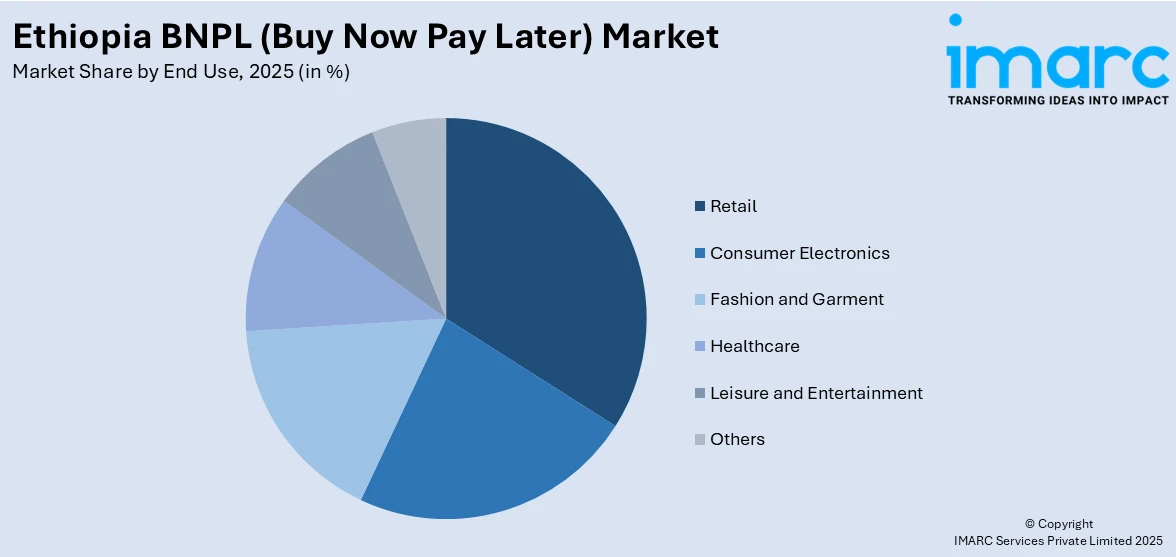

- By End Use: Retail leads the market with a 34.9% share in 2025, driven by increasing consumer preference for installment-based purchasing of everyday goods and fashion products.

- By Region: Addis Ababa accounts for the market share of 41.6% in 2025, owing to its concentrated urban population, advanced digital payment infrastructure, and higher smartphone penetration rates.

- Key Players: The Ethiopia BNPL market features emerging local fintech firms and technology companies that are partnering with banks and international payment providers to develop innovative deferred payment solutions, expand merchant networks, and accelerate digital financial services adoption across the country.

To get more information on this market Request Sample

The Ethiopia BNPL market is advancing as digital payment adoption accelerates and consumer expectations shift toward flexible, accessible financing options. Apart from this, the country's mobile money ecosystem has expanded dramatically, with accounts growing from under 1 million in 2020 to over 128.5 million by December 2024, according to the National Bank of Ethiopia. This surge in digital transaction infrastructure is creating a foundation for BNPL services to integrate seamlessly with mobile wallets and e-commerce platforms. For example, EagleLion System Technology launched DubePay, a buy-now-pay-later platform developed in partnership with Dashen Bank, offering installment-based payment solutions to salaried customers in Ethiopia. Rising fintech investment, expanding internet access, and supportive regulatory frameworks are contributing to a more favorable environment for BNPL adoption.

Ethiopia BNPL (Buy Now Pay Later) Market Trends:

Rapid Expansion of Mobile Money and Digital Wallet Ecosystems

Ethiopia's mobile money landscape has undergone a transformative shift, creating a robust foundation for BNPL adoption. Digital financial transactions surpassed cash transactions for the first time during the 2023/24 fiscal year, with the National Bank of Ethiopia recording 9.7 trillion Birr in digital transaction value. Mobile money accounts expanded from under 1 million in 2020 to over 128.5 million by December 2024. This digital momentum is enabling BNPL providers to integrate deferred payment options directly into widely used mobile wallets, supporting Ethiopia BNPL (buy now pay later) market growth.

Integration of BNPL with E-Commerce and Merchant Platforms

BNPL services are increasingly being embedded into Ethiopia's growing e-commerce and merchant payment ecosystems. Local fintech firms are developing installment payment solutions tailored to online and point-of-sale channels. For instance, EagleLion System Technology introduced DubePay in alliance with Dashen Bank, offering a buy-now-pay-later consumer financing platform where salaried customers can pay on an installment basis on their payday. These partnerships between technology companies and banking institutions are helping formalize deferred payments and expand consumer access to short-term credit. In 2025, Ethiopia has officially unveiled its National Digital Payment Strategy (NDPS 2026–2030) and the Instant Payment System today during the 2nd Ethiopian Digital Payment Conference in Addis Ababa. The five-year plan outlines a course for interoperability, trust, and innovation in the nation's digital finance industry. The conference convened high-ranking government officials, such as Deputy Prime Minister Temesgen Truneh, along with policymakers, regulators, banks, tech innovators, and development partners to expedite Ethiopia’s transition to a digital, inclusive, and cashless economy.

Government-Driven Digital Financial Inclusion Initiatives

Ethiopia's regulatory environment is evolving to support innovative financial services, including BNPL. In March 2025, the National Bank of Ethiopia launched Phase Two of its National Digital Payments Strategy for 2025–2029, focusing on deepening digital payment usage, ensuring full interoperability, and expanding digital ID integration across the financial ecosystem. Phase Two of the Strategy (2025–2029) will emphasize enhancing the use of digital payments, achieving complete interoperability, broadening digital ID integration, establishing an inclusive and responsible digital financial environment, and speeding up merchant acceptance, especially among small and medium-sized enterprises, women, and rural communities. These policy-level initiatives are creating an enabling framework for BNPL services to scale alongside mobile banking, digital wallets, and merchant payment acceptance networks.

Market Outlook 2026-2034:

Ethiopia's BNPL market is positioned for steady growth, supported by ongoing digital transformation efforts, expanding fintech innovation, and increasing consumer demand for flexible payment options. The market generated a revenue of USD 11.58 Million in 2025 and is projected to reach a revenue of USD 58.84 Million by 2034, growing at a compound annual growth rate of 19.8% from 2026-2034. Continued regulatory modernization, deeper mobile wallet penetration, and growing e-commerce activity are expected to drive higher adoption rates across both urban and emerging markets. Strategic collaborations between domestic fintech companies, international payment networks, and banking institutions are anticipated to strengthen merchant acceptance and product innovation. As digital ID systems mature and interoperability frameworks expand, the BNPL ecosystem is expected to become more competitive, accessible, and inclusive, establishing Ethiopia as a notable market for deferred payment solutions in East Africa.

Ethiopia BNPL (Buy Now Pay Later) Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Channel |

Online |

58.7% |

|

Enterprise Size |

Large Enterprises |

62.4% |

|

End Use |

Retail |

34.9% |

|

Region |

Addis Ababa |

41.6% |

Channel Insights:

- Online

- Point of Sale (POS)

Online dominates with a market share of 58.7% of the total Ethiopia BNPL (buy now pay later) market in 2025.

The online channel has emerged as the largest segment due to its reach, convenience, and ability to influence purchase decisions before a transaction is completed. Consumers increasingly begin their buying journey on digital platforms, using search engines, brand websites, and e-commerce marketplaces to compare features, prices, and reviews. The availability of detailed product information, customer ratings, video demonstrations, and promotional offers strengthens buyer confidence and shortens the decision cycle. Online platforms also enable brands to target specific customer groups through personalized recommendations, social media advertising, and retargeting campaigns, which improves conversion rates.

Subscription models, direct-to-consumer websites, and app-based purchasing further expand accessibility and encourage repeat purchases. In addition, online channels reduce geographic barriers, allowing brands to penetrate tier II and tier III cities without investing heavily in physical infrastructure. Flexible payment options, including digital wallets, buy-now-pay-later services, and easy returns, contribute to higher adoption. The ability to track user behavior in real time provides companies with actionable data, helping them optimize pricing, promotions, and inventory planning. These advantages collectively position online platforms as the dominant revenue contributor within the overall distribution mix.

Enterprise Size Insights:

- Large Enterprises

- Small and Medium Enterprises

Large enterprises lead with a share of 62.4% of the total Ethiopia BNPL (buy now pay later) market in 2025.

Large enterprises represent the dominant segment due to their extensive operational scale and higher spending capacity. These organizations typically manage complex structures across multiple locations, business units, or even countries, which increases the need for integrated and high-performance solutions. Their budgets allow them to invest in advanced systems, customized deployments, and long-term vendor partnerships. Procurement decisions in large enterprises often prioritize reliability, data security, regulatory compliance, and seamless integration with existing infrastructure. With dedicated IT teams and structured implementation processes, they are better positioned to deploy enterprise-grade solutions efficiently and extract full value from their investments.

In addition, large enterprises tend to lead in technology adoption as part of broader digital transformation strategies aimed at improving efficiency, productivity, and competitive positioning. The scale of their workforce and customer base amplifies the benefits of automation, analytics, and centralized management tools. Ongoing upgrades, maintenance contracts, and expansion projects further contribute to consistent revenue generation from this segment. Their ability to commit to multi-year agreements and large-volume deployments strengthens vendor relationships and drives higher average contract values. These factors collectively ensure that large enterprises remain the largest contributor within the enterprise size segmentation.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Consumer Electronics

- Fashion and Garment

- Healthcare

- Leisure and Entertainment

- Retail

- Others

Retail exhibits a clear dominance with a 34.9% share of the total Ethiopia BNPL (buy now pay later) market in 2025.

Retail represents the largest end-use segment, driven by its high transaction volume, broad customer base, and constant need for operational efficiency. Retail businesses operate in a fast-paced environment where consumer preferences change quickly, making it essential to adopt solutions that enhance customer engagement, optimize inventory management, and improve sales performance. The sector’s reliance on both physical stores and e-commerce platforms has increased demand for integrated technologies that support omnichannel experiences. Retailers use advanced tools for real-time stock tracking, personalized marketing, dynamic pricing, and customer relationship management, all of which contribute to stronger competitiveness.

Large retail chains, supermarkets, and specialty stores invest heavily in digital systems to streamline supply chain operations and reduce costs. Additionally, the rise of online shopping and mobile commerce has expanded the need for seamless payment systems, efficient delivery logistics, and data-driven decision-making. These factors have positioned retail as the most prominent contributor to market demand, with continuous innovation and high adoption rates across both developed and emerging economies.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Addis Ababa leads with a share of 41.6% of the total Ethiopia BNPL (buy now pay later) market in 2025.

Addis Ababa leads the Ethiopia BNPL market as the country's commercial, financial, and technological hub. The capital city benefits from the highest concentration of digital payment infrastructure, internet connectivity, and smartphone penetration in the country. With over 28.6 million internet users nationwide and the majority of digital commerce activity centered in urban areas, Addis Ababa serves as the primary market for BNPL service providers. The city hosts the headquarters of leading fintech firms alongside major banking institutions that are actively partnering with technology providers to offer deferred payment solutions.

Addis Ababa's advanced merchant acceptance ecosystem, supported by growing POS terminal deployment and mobile QR payment capabilities, creates favorable conditions for both online and offline BNPL integration. The capital also benefits from a higher concentration of salaried workers and young professionals who represent the core demographic for installment-based purchasing. As digital ID verification through the Fayda national program matures and interoperability across mobile wallets and bank accounts strengthens, Addis Ababa is expected to continue serving as the primary growth engine for Ethiopia's expanding BNPL market.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia BNPL (Buy Now Pay Later) Market Growing?

Expanding Digital Payments Infrastructure and Mobile Money Adoption

The rapid expansion of Ethiopia's digital payments ecosystem is creating a strong foundation for BNPL services. Mobile money accounts surged from under 1 million in 2020 to over 128.5 million by December 2024, driven by the entry of non-bank mobile money service providers and regulatory liberalization. Platforms are reshaping how consumers access financial services. In May 2024, Mastercard partnered with EagleLion System Technology to empower Ethiopian businesses and consumers with secure digital payment acceptance solutions via Mastercard Gateway's advanced payment technology. This collaboration is enhancing the digital payments infrastructure that supports BNPL integration at the merchant level.

Young, Tech-Savvy Population and Rising E-Commerce Activity

Ethiopia's large, young population is a key driver of BNPL market growth. A large number of people in the country are under the age of 30, representing a demographic that is mobile-first, digitally connected, and increasingly comfortable with online purchasing. Internet penetration surpassed 34% in 2024, and smartphone ownership continues to rise due to more affordable devices from Chinese and African brands. This digital-first demographic is driving demand for flexible payment options that align with their consumption patterns. Social commerce through platforms is expanding rapidly, and integrated payment solutions from providers are enabling seamless online transactions that can be paired with BNPL offerings to increase purchasing power among young consumers.

Regulatory Modernization and Fintech-Friendly Policy Environment

Ethiopia's evolving regulatory framework is actively encouraging innovation in digital financial services, including BNPL. Ethiopia has introduced its National Digital Payment Strategy (NDPS 2026–2030) along with the Instant Payment System (IPS). The Instant Payment System and the National Digital Payment Strategy 2030, outlining a five-year plan for interoperability, trust, and innovation in Ethiopia's digital finance environment, were unveiled at the second Ethiopia Digital Payment Conference held in Addis Ababa. The introduction of regulatory sandboxes and improved licensing frameworks is lowering entry barriers for innovative payment solutions while ensuring consumer protection standards are maintained.

Market Restraints:

What Challenges the Ethiopia BNPL (Buy Now Pay Later) Market is Facing?

Low Digital Literacy and Consumer Trust Deficit

Despite significant progress in digital payment adoption, low digital literacy remains a notable barrier to BNPL expansion. Many consumers, particularly in rural and semi-urban areas, remain unfamiliar with digital credit concepts and hesitant to adopt installment-based payment models. A culture of cash dependence, limited exposure to formal credit products, and concerns about cybersecurity and data privacy continue to slow broader BNPL adoption.

Infrastructure and Connectivity Gaps in Rural Areas

Limited internet connectivity, unreliable power supply, and insufficient digital payment infrastructure outside major urban centers constrain the geographic reach of BNPL services. While Addis Ababa and other cities benefit from advancing digital ecosystems, rural areas, where a major portion of the population resides, face significant gaps in network coverage, POS terminal availability, and merchant acceptance of digital payments.

Nascent Regulatory Framework for BNPL-Specific Services

While Ethiopia has made substantial progress in fintech regulation broadly, specific regulatory frameworks governing BNPL services remain underdeveloped. The absence of dedicated BNPL licensing requirements, clear consumer protection guidelines for deferred payment products, and standardized credit assessment protocols creates uncertainty for providers and may expose consumers to over-indebtedness risks as the market grows.

Competitive Landscape:

The Ethiopia BNPL market is in an early development phase, with a competitive landscape shaped by domestic fintech firms, technology solution providers, and banking institutions forming strategic partnerships to introduce deferred payment solutions. Companies are focused on building digital infrastructure, expanding merchant acceptance networks, and integrating BNPL options with mobile wallets and e-commerce platforms. Collaboration with international payment networks and technology providers is accelerating innovation and market development. As regulatory clarity improves and digital payment adoption deepens, competition is expected to intensify, with providers differentiating through product features, user experience, and merchant partnerships.

Ethiopia BNPL (Buy Now Pay Later) Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Channels Covered |

Online, Point of Sale (POS) |

|

Enterprise Sizes Covered |

Large Enterprises, Small and Medium Enterprises |

|

End Uses Covered |

Consumer Electronics, Fashion and Garment, Healthcare, Leisure and Entertainment, Retail, Others |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The Ethiopia BNPL (buy now pay later) market size was valued at USD 11.58 Million in 2025.

The market is expected to grow at a compound annual growth rate of 19.8% from 2026-2034 to reach USD 58.84 Million by 2034.

Online, holding the largest revenue share of 58.7%, remains pivotal for Ethiopia's BNPL adoption, driven by expanding e-commerce integration, growing digital payment platforms, and increasing consumer preference for online installment-based purchasing.

Key factors driving the Ethiopia BNPL market include expanding digital payments infrastructure, rapid mobile money adoption, a young and tech-savvy population, growing e-commerce activity, and supportive government-led digital transformation and financial inclusion initiatives.

Major challenges include low digital literacy and consumer trust deficits, limited infrastructure and connectivity in rural areas, a nascent BNPL-specific regulatory framework, and high dependence on cash-based transactions outside urban centers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)