Ethiopia Dairy Market Size, Share, Trends and Forecast by Product Type and Region, 2026-2034

Ethiopia Dairy Market Summary:

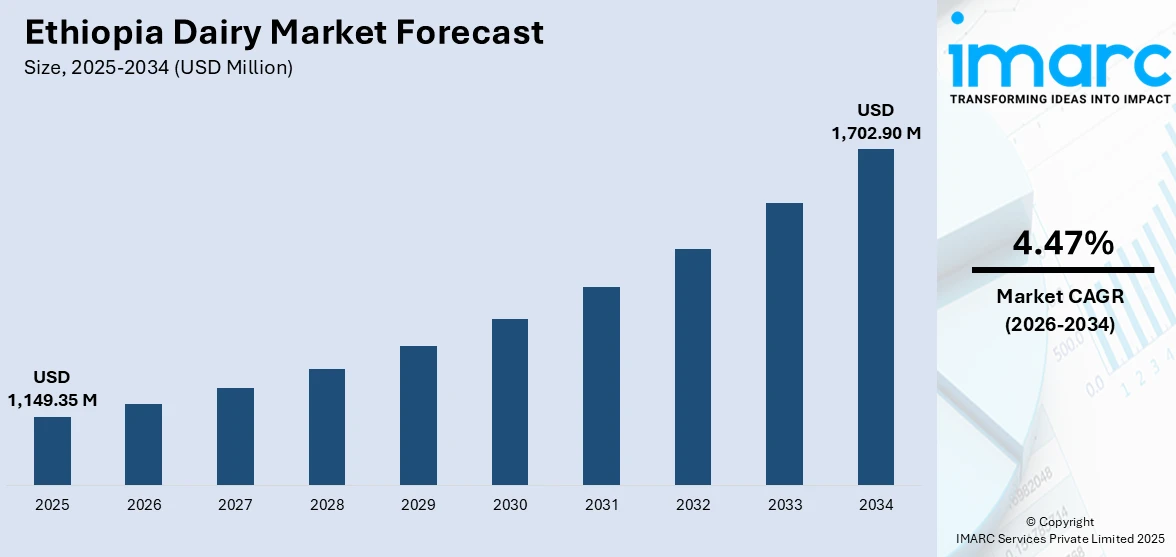

The Ethiopia dairy market size was valued at USD 1,149.35 Million in 2025 and is projected to reach USD 1,702.90 Million by 2034, growing at a compound annual growth rate of 4.47% from 2026-2034.

The Ethiopia dairy industry is witnessing a healthy growth pace with an increased pace of government endeavors, urbanization, and development in the processing sectors. Investments in cross-breeding and processing units are boosting production and bettering product quality. Health awareness and a rise in per-capita incomes are changing consumption behavior in the Ethiopia dairy market share. Developments in value chains, improvements in processing technology, and support from Farmer Cooperatives are simultaneously making Ethiopia a developing destination in the dairy industry in the Ethiopia dairy market share.

Key Takeaways and Insights:

- By Product Type: Liquid milk dominates the market with a share of 43.2% in 2025, driven by rising consumer preference for fresh pasteurized products and expanding urban retail networks.

- By Region: Oromia Region leads the market with a share of 43.5% in 2025, supported by favorable agro-climatic conditions and proximity to major processing facilities.

- Key Players: The Ethiopia dairy market features established processors and emerging cooperatives competing through product diversification, quality improvements, and distribution expansion. Companies are investing in processing capacity, strengthening farmer partnerships, expanding retail networks, and introducing value-added products to capture growing urban consumer demand.

To get more information on this market Request Sample

The Ethiopia dairy market continues to evolve as stakeholders embrace modernized production practices and commercial value chain approaches. The government’s Yelemat Tirufat initiative has catalyzed transformational changes, driving an eightfold increase in crossbred cattle populations and substantially boosting milk yields across major agricultural clusters. In May 2025, Holland Dairy, one of Ethiopia’s leading processors, unveiled a new premium cheese product made entirely from locally sourced milk using advanced Dutch technology, underscoring growing industry innovation and capacity expansion in value‑added dairy products. Urban dairy consumption patterns are shifting toward processed products, with pasteurized milk gaining market share as food safety awareness increases among consumers. Processing capacity has expanded significantly with the number of active dairy companies tripling over the past decade. Smallholder farmers remain integral to the supply chain, while larger commercial operations are increasingly contributing to formal market channels.

Ethiopia Dairy Market Trends:

Expansion of Commercial Dairy Processing Infrastructure

The Ethiopia dairy market is witnessing rapid expansion of commercial processing infrastructure as demand for pasteurized products accelerates. Processing facilities are investing in modern equipment to enhance production capacity and product quality. The number of active dairy processing companies has grown substantially, with major processors expanding their geographic reach beyond Addis Ababa to regional centers including Bahir Dar, Awassa, and Gondar. This decentralization is reducing transportation costs while improving product freshness and market accessibility for consumers in secondary cities and emerging urban centers.

Accelerated Genetic Improvement Through Crossbreeding Programs

Crossbreeding initiatives are transforming dairy productivity across Ethiopia, with the Yelemat Tirufat program driving significant advancements in cattle genetics. According to the Ethiopian Ministry of Agriculture, annual crossbreeding under the “Bounty of the Basket” (Yelemat Tirufat) initiative has expanded from about 500,000 animals to 1.2 million in the first year and 2.4 million in the second year, contributing to an eightfold rise in crossbred cattle and nearly doubling milk production to an estimated 12 billion liters in three year. Annual crossbreeding activities have expanded substantially, significantly growing the improved cattle population nationwide. The Ministry of Agriculture has invested in local liquid nitrogen production for artificial insemination services, ensuring consistent supply for nationwide breeding efforts. These genetic improvement programs are enhancing milk yields while supporting the Ethiopia dairy market growth trajectory toward self-sufficiency targets.

Rising Urban Consumption and Market Formalization

Urban dairy consumption patterns are shifting significantly as Ethiopia's middle class expands and dietary preferences evolve toward protein-rich foods. According to recent industry reporting, the number of dairy processing companies supplying liquid milk and other pasteurized products has more than tripled over the past decade, underscoring growing availability of quality‑assured dairy products for urban consumers. Dairy expenditures among urban households have increased notably, with liquid milk gaining prominence in consumer baskets compared to traditional butter-based products. The formal market channel is capturing greater share as consumers increasingly prefer quality-assured pasteurized products from established processors over informal raw milk sources. Modern retail channels including supermarkets and specialized dairy shops are expanding distribution reach across major cities.

Market Outlook 2026-2034:

The future prospects in the dairy industry in Ethiopia are bright as different factors are coming together to push developments in this industry in a positive way. The dedication of the government in making this country self-reliant in dairy products through the National Dairy Development Strategy is making this a reality from end to end in this industry. Foreign investment collaborations are bringing in modern technology and organizational skills that will boost productivity and product development in this industry. The factors of increased urbanization and a greater middle class with demands for healthy protein food are keeping demand growth steady in this industry. The market generated a revenue of USD 1,149.35 Million in 2025 and is projected to reach a revenue of USD 1,702.90 Million by 2034, growing at a compound annual growth rate of 4.47% from 2026-2034.

Ethiopia Dairy Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Liquid Milk |

43.2% |

|

Region |

Oromia Region |

43.5% |

Product Type Insights:

- Liquid Milk

- Flavored Milk

- Cream

- Butter

- Cheese

- Yoghurt

- Ice Cream

- Anhydrous Milk Fat (AMF)

- Skimmed Milk Powder (SMP)

- Whole Milk Powder (WMP)

- Whey Protein

- Lactose Powder

- Curd

- Paneer

The liquid milk dominates with a market share of 43.2% of the total Ethiopia dairy market in 2025.

The market for liquid milk is dominant in the Ethiopian dairy products market, given the rise in consumer preferences for fresh and pasteurized milk, along with convenience and nutritional advantages. The segment is also backed by improved processing capacities, mainly in the large plants based in and around the capital city, Addis Ababa. The key companies in the sector meet the major demand for pasteurized dairy products in the market, primarily due to strong consolidation and quality synchronization within the sector.

There has been a preference for liquid milk over traditional dairy products by urban households, with a rise in the importance of cow milk spending as a dairy product at the household level over the years. Enhanced awareness regarding food safety and health has led to increased demand for pasteurized milk from consumers through proper retail channels. Organizations involved in milk processing have improved their distribution channels to supermarkets, retail outlets, restaurants, and institutions while developing cold chain storage to enhance freshness.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Oromia Region exhibits a clear dominance with a 43.5% share of the total Ethiopia dairy market in 2025.

Oromia Region represents Ethiopia's largest dairy-producing area, benefiting from favorable agro-ecological conditions and strategic proximity to the capital city's substantial consumer market. The region hosts numerous dairy processing facilities including major industry players operating large-scale operations. Smallholder farmers in Oromia supply raw milk to processors located within accessible distance of Addis Ababa, forming the backbone of the commercial dairy value chain and supporting formal market development.

The World Bank's BioCarbon Fund Initiative has partnered with Solidaridad to implement climate-smart dairy business models in Oromia, demonstrating approaches that boost productivity while reducing greenhouse gas emissions. These pilot programs are establishing dairy service hubs that link farmers to processors through joint milking, collection, and cooling facilities near dairy villages. The region's dairy development trajectory is supported by investments in crossbreeding services, improved feed availability, and extension services enhancing farmer practices.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Dairy Market Growing?

Supportive Government Policies and Strategic Development Initiatives

The Ethiopian government has prioritized dairy sector development through comprehensive policy frameworks and targeted investment programs. In December 2023, Ethiopia officially unveiled its National Dairy Development Strategy 2022–2031, a road map developed by the Ministry of Agriculture in collaboration with the International Livestock Research Institute (ILRI) and other partners to quadruple milk production by 2031 and strengthen dairy value chains nationwide. The strategy launched by the Ministry of Agriculture in collaboration with the International Livestock Research Institute, establishes ambitious targets for increasing milk production and achieving self-sufficiency. The Livestock and Fisheries Sector Development Project operates with World Bank funding to increase productivity and commercialization of dairy producers.

Significant Foreign Direct Investment and Private Sector Participation

International investment flows are accelerating dairy sector modernization and capacity expansion in Ethiopia. In February 2025, Ethiopian Investment Holdings (EIH) and the Ethiopian Agricultural Business Corporation (EABC) signed a $600 million shareholders agreement with UK private‑equity firm Asset Green to develop an integrated dairy‑farming and processing project that will include large‑scale feed production and modern dairy operations, marking one of the largest foreign investments in the country’s agribusiness sector. Ethiopian Investment Holdings and the Ethiopian Agricultural Business Corporation have partnered with international private equity firms for integrated dairy farming and processing projects. These initiatives are establishing large-scale dairy farming operations with integrated feed production, introducing advanced agricultural technologies and best management practices. Such partnerships reflect growing international confidence in Ethiopia's dairy sector potential and provide templates for additional investment attraction across the entire value chain.

Rising Population, Urbanization, and Changing Consumption Patterns

Ethiopia's demographic trends are creating sustained demand growth for dairy products as the population expands and urbanizes rapidly. The country's strong economic growth has driven household income improvements that enable greater consumption of high-value protein sources including dairy products. In 2025, Holland Dairy launched a new line of flavored yoghurts and premium dairy products targeting urban consumers, reflecting rising demand for processed and value‑added dairy items in major cities. Urban dairy consumption has increased substantially, with major city residents exhibiting higher per capita consumption levels compared to rural areas. Rising health awareness and changing dietary preferences are shifting consumption toward processed dairy products, creating opportunities for value-added product development and market expansion.

Market Restraints:

What Challenges the Ethiopia Dairy Market is Facing?

Feed Shortage and High Input Costs

Limited availability and high costs of quality animal feed remain primary constraints affecting dairy productivity across Ethiopia. Smallholder farmers face significant challenges accessing improved forages, concentrate feeds, and agricultural by-products necessary for enhanced milk production. Feed resource limitations contribute to seasonal production variability and constrain the ability of producers to fully capitalize on genetic improvements achieved through crossbreeding programs.

Inadequate Infrastructure and Cold Chain Limitations

Underdeveloped market infrastructure, limited milk collection facilities, and insufficient cold chain networks impede dairy value chain efficiency. Many rural and semi-urban areas lack adequate cooling and storage facilities, resulting in significant post-harvest losses. Transportation constraints and poor road connectivity further challenge the timely movement of perishable dairy products from production areas to processing facilities and consumer markets.

Low Productivity of Indigenous Cattle Breeds

The predominance of indigenous cattle breeds constrains overall milk production potential across Ethiopia. Indigenous breeds produce significantly lower milk yields compared to crossbred animals. While crossbreeding programs are expanding improved cattle populations, the transformation of the national herd remains a gradual process requiring sustained investment in artificial insemination services, veterinary care, and comprehensive farmer training programs.

Competitive Landscape:

This is a relatively diversified market with established commercial processors and emerging dairy cooperatives that compete across product categories and geographic markets. The formal pasteurized milk segment is dominated by major processors supplying supermarkets, hotels, and institutional buyers in Addis Ababa and regional centers. Competition is growing tighter with companies increasing processing capacity, adding product portfolios such as yogurt, cheese, and butter, and advancing distribution networks to reach less-served markets. Dairy cooperatives are emerging to take more market share by aggregating smallholder production and making investments in processing capabilities. Strategic partnerships between domestic operators and international investors will introduce advanced technologies and management practices, further raising competitive standards across the industry.

Recent Developments:

-

In April 2025, Holland Dairy launches new banana yoghurt in Ethiopia, unveiling a Banana Yoghurt made with real Ethiopian bananas to blend local flavor and dairy innovation while supporting smallholder farmers. The product expands the company’s flavored range and boosts the domestic dairy sector’s value‑added offerings.

Ethiopia Dairy Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Liquid Milk, Flavored Milk, Cream, Butter, Cheese, Yoghurt, Ice Cream, Anhydrous Milk Fat (AMF), Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Whey Protein, Lactose Powder, Curd, Paneer |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Dairy Market Report

The Ethiopia dairy market size was valued at USD 1,149.35 Million in 2025.

The Ethiopia dairy market is expected to grow at a compound annual growth rate of 4.47% from 2026-2034 to reach USD 1,702.90 Million by 2034.

Liquid milk, holding the largest revenue share of 43.2%, remains the dominant segment in Ethiopia’s dairy market, driven by rising consumer preference for pasteurized products, expanding processing infrastructure, and growing urban consumption through formal retail channels.

Key factors driving the Ethiopia dairy market include supportive government policies and strategic initiatives, significant foreign direct investment inflows, rising population and urbanization, expanding processing infrastructure, and genetic improvement programs enhancing dairy productivity.

Major challenges include feed shortage and high input costs, inadequate infrastructure and cold chain limitations, low productivity of indigenous cattle breeds, limited access to veterinary services, and underdeveloped market linkages between producers and processors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)