Ethiopia Greenhouse Farming Market Size, Share, Trends and Forecast by Structure Type, Crop Type, Technology, and Region, 2026-2034

Ethiopia Greenhouse Farming Market Summary:

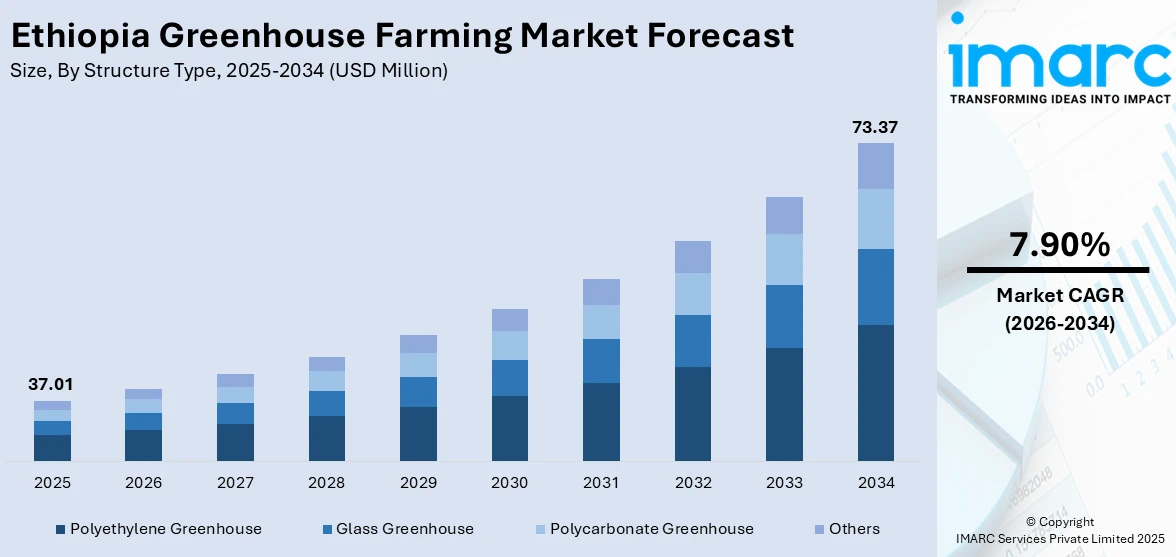

The Ethiopia greenhouse farming market size was valued at USD 37.01 Million in 2025 and is projected to reach USD 73.37 Million by 2034, growing at a compound annual growth rate of 7.90% from 2026-2034.

As Ethiopia speeds up its shift from conventional open-field production to controlled-environment agriculture, the market for greenhouse farming is expanding. Market development is being reinforced by growing government investment in protected agricultural infrastructure, growing use of soilless farming technology, and growing export aspirations. Improved irrigation infrastructure and greenhouse building techniques are revolutionizing horticultural practices, establishing Ethiopia as a growing hub for greenhouse-based agriculture, and increasing the market share of Ethiopian greenhouse farming.

Key Takeaways and Insights:

- By Structure Type: Polyethylene greenhouse dominates the market with a share of 49.2% in 2025, because of its low cost, lightweight design, and suitability for the semi-arid highland environment that prevails in Ethiopia's horticultural regions. The market is growing as a result of growing usage among commercial and smallholder producers.

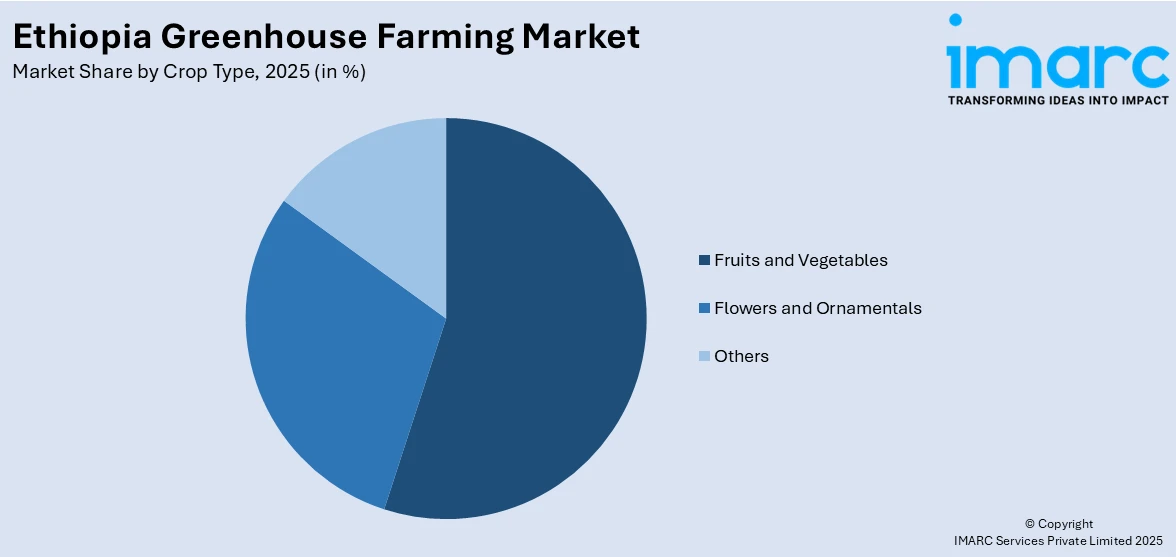

- By Crop Type: Fruits and vegetables lead the market with a share of 61.7% in 2025. Rising domestic food security demands, growing export demand from European and Gulf markets, and ideal agroclimatic conditions that allow for year-round greenhouse agriculture are the main drivers of this domination.

- By Technology: Hydroponics exhibits a clear dominance in the market with 43.6% share in 2025, demonstrating robust institutional and development partner support for soilless farming practices that enhance yields, save water, and allow crop production in areas of the nation with limited resources.

- By Region: Oromia Region is the largest region with 34.9% share in 2025, spurred by the concentration of commercial horticulture and flower farms, the abundance of fertile terrain, and the close proximity to the cold-chain and logistical facilities of Addis Ababa.

- Key Players: By investing in cutting-edge greenhouse structures, developing soilless agriculture methods, and forming alliances with global development organizations, major companies propel Ethiopia's greenhouse farming business. Their initiatives to increase production capacity, enhance post-harvest processing, and get export certifications hasten the use of greenhouses in a variety of producing locales.

To get more information on this market Request Sample

The Ethiopia greenhouse farming market is advancing as the government, development partners, and the private sector collaborate to modernize the country’s horticultural landscape through protected cultivation systems. Rising climate variability and recurrent droughts are increasing reliance on controlled-environment agriculture to ensure consistent crop production throughout the year. The Ethiopian Horticulture Producers and Exporters Association reported that horticulture exports generated USD 564.9 Million in the 2024/25 fiscal year, underscoring the sector’s growing economic significance and its role as a major foreign exchange earner. Due to growing demands for worldwide market access and local food security, greenhouse farming is shifting from its traditional floriculture concentration to the cultivation of fruits and vegetables. A favorable climate for protected production is being created by ongoing irrigation infrastructure expansion, government greenhouse structure subsidies, and conformity to international agricultural sustainability requirements. The productivity of greenhouses is being further increased by the integration of precision farming technology and digital agricultural tools. Furthermore, it is anticipated that the proposed Greenhouse Horticulture Investment Proclamation would provide a well-organized regulatory framework that will promote additional private investment in the industry.

Ethiopia Greenhouse Farming Market Trends:

Government-led strategic horticulture modernization

Through extensive national planning and policy involvement, the Ethiopian government is giving structural reform of the horticultural industry top priority. Enhancing food security, promoting export diversification, and encouraging infrastructure development throughout protected agricultural systems are the goals of recent strategic efforts. These policy frameworks, which reflect a revolutionary institutional commitment that directly supports greenhouse farming expansion and positions the industry for sustainable modernization and growth, set long-term roadmaps for boosting horticulture production and export competitiveness.

Integration of solar-powered and digital agriculture technologies

To increase crop productivity and lessen dependency on traditional energy sources, Ethiopian greenhouse operators are increasingly utilizing solar energy and computerized monitoring systems. Initiatives for digital agriculture supported by the government seek to improve greenhouse operations' efficiency and resource management by integrating precise instruments throughout agricultural value chains. Year-round crop production is made possible by the use of subsidized solar-powered irrigation, illustrating the usefulness of integrating renewable energy sources into protected farming throughout the nation's midland and highland agro-ecological zones.

Expansion of export-oriented greenhouse cultivation targeting Gulf markets

Ethiopia is using its geographic closeness to offer fresh food quickly, strategically placing its greenhouse industry to cater to the Gulf Cooperation Council's high-demand export markets. Investment in export-quality protected cultivation infrastructure is being driven by the government's increasing aspirations for horticulture export revenues. The nation's competitiveness as a dependable provider of high-quality fresh produce is bolstered by greenhouse-based production, which allows for supply stabilization, enhanced product homogeneity, and off-season cultivation capabilities that satisfy exacting international quality requirements.

Market Outlook 2026-2034:

The Ethiopia greenhouse farming market is poised for sustained expansion as the country intensifies its efforts to modernize horticultural production through protected cultivation systems. The convergence of government policy support, international development partnerships, and private sector investment is creating a favorable ecosystem for greenhouse adoption across key growing regions. The market generated a revenue of USD 37.01 Million in 2025 and is projected to reach a revenue of USD 73.37 Million by 2034, growing at a compound annual growth rate of 7.90% from 2026-2034. The transition from open-field farming to controlled-environment agriculture is being accelerated by the growing need for a year-round supply of fresh produce for both domestic food security and export markets in Europe and the Gulf area. Crop production and export competitiveness are anticipated to increase with further advancements in soilless growing techniques, irrigation technology, and greenhouse infrastructure quality. Increased investment and structural change in the industry are expected as a result of government efforts such as the planned Greenhouse Horticulture Investment Proclamation, the 10-Year National Horticulture Strategy, and subsidized solar-powered systems.

Ethiopia Greenhouse Farming Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Structure Type |

Polyethylene Greenhouse |

49.2% |

|

Crop Type |

Fruits and Vegetables |

61.7% |

|

Technology |

Hydroponics |

43.6% |

|

Region |

Oromia Region |

34.9% |

Structure Type Insights:

- Glass Greenhouse

- Polycarbonate Greenhouse

- Polyethylene Greenhouse

- Others

Polyethylene greenhouse dominates with a market share of 49.2% of the total Ethiopia greenhouse farming market in 2025.

Polyethylene greenhouses are the preferred structural choice across Ethiopia’s horticultural landscape due to their cost-effectiveness, ease of installation, and suitability for the country’s diverse agro-climatic conditions. The lightweight polyethylene film covering allows efficient light transmission while providing essential protection against extreme weather, pests, and temperature fluctuations. Smallholder farmers and commercial growers alike favor these structures because they require significantly lower capital investment compared to glass or polycarbonate alternatives, making protected cultivation accessible to a broader range of producers. The widespread availability of polyethylene materials through import channels further supports adoption rates.

The expansion of polyethylene greenhouse adoption is closely linked to government subsidy programs and development-partner initiatives promoting protected agriculture. Ethiopia maintains a growing number of active flower farms operating predominantly under polyethylene-covered structures, with industry associations reporting that vegetable farming operations are expected to increase significantly in the coming years across Oromia, Amhara, and Sidama regions. The affordability and adaptability of polyethylene structures enable rapid deployment in both highland and midland zones, supporting the country's strategic shift toward year-round greenhouse production for domestic food security and export diversification.

Crop Type Insights:

Access the comprehensive market breakdown Request Sample

- Fruits and Vegetables

- Flowers and Ornamentals

- Others

Fruits and vegetables lead with a share of 61.7% of the total Ethiopia greenhouse farming market in 2025.

Fruits and vegetables represent the dominant crop category in Ethiopia's greenhouse farming sector, driven by escalating domestic food security demands and growing export market opportunities. Ethiopia produces substantial volumes of fruits and vegetables annually, yet only a small fraction reaches international markets despite significant surplus availability, highlighting substantial untapped potential for greenhouse-based production to bridge quality and supply consistency gaps. Greenhouse cultivation enables year-round production of high-value crops that meet both local consumption needs and stringent international market standards.

The expanding export infrastructure for greenhouse-grown produce is strengthening the segment’s position. In November 2024, Ethio Vegfru launched Ethiopia’s first refrigerated vegetable shipment to Europe, transporting 12 Tons of sugar snap peas and mangetout from Koka to the Netherlands via the Ethio-Djibouti transport corridor using modern refrigeration containers. This milestone demonstrates the growing capacity for greenhouse-produced vegetables to access premium international markets. The government’s 10-Year National Horticulture Strategy prioritizes fruit and vegetable export diversification, and alignment with Gulf market standards is creating additional demand channels for controlled-environment produce.

Technology Insights:

- Hydroponics

- Aquaponics

- Aeroponics

- Others

Hydroponics exhibits a clear dominance with 43.6% share of the total Ethiopia greenhouse farming market in 2025.

Hydroponics has emerged as the leading greenhouse technology in Ethiopia, driven by its superior water efficiency, higher crop yields compared to soil-based methods, and compatibility with resource-constrained environments. The soilless cultivation approach reduces water consumption significantly when compared to traditional irrigation, a critical advantage in a country where recurrent droughts and water scarcity pose persistent agricultural challenges. Hydroponic systems enable year-round production of leafy greens, herbs, and high-value vegetables in controlled environments, supporting both urban and peri-urban food security initiatives and reducing dependency on seasonal rainfall patterns across the nation.

Institutional support has been instrumental in accelerating hydroponic adoption. International development organizations have launched pilot hydroponic vegetable farming programs in partnership with local agricultural companies to address child malnutrition while enhancing food system resilience across vulnerable regions. These initiatives have demonstrated that hydroponic farming enables year-round production regardless of weather or seasonal conditions, with significant improvements in crop performance compared to soil-based cultivation. The technical simplicity and scalability of hydroponic systems are positioning the technology as the foundational approach for indoor and greenhouse agriculture development in Ethiopia.

Region Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Oromia Region represents the leading segment with 34.9% share of the total Ethiopia greenhouse farming market in 2025.

Oromia Region holds the dominant position in Ethiopia's greenhouse farming market, benefiting from its vast fertile agricultural land, favorable agro-climatic conditions, and strong concentration of commercial horticultural operations. The region accounts for the largest share of national agricultural output and coffee exports, reflecting its established role as the country's primary agricultural production hub. Oromia's proximity to Addis Ababa provides critical logistical advantages, including access to international airport cargo facilities, cold-chain storage infrastructure, and major transport corridors for export shipments.

The region's greenhouse sector is further strengthened by significant flower farm investments and expanding vegetable production operations. Leading horticultural companies based in Oromia are undertaking major greenhouse expansions driven by growing demand from international wholesale markets, particularly in Europe. Additionally, new companies are emerging to invest in vegetable farming across the region, supported by the expansion of irrigation infrastructure and government-backed cluster farming initiatives. Ongoing agricultural development programs, aided by the distribution of fertilizers and improved seeds, are further consolidating the region's leadership in protected cultivation and greenhouse-based production.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Greenhouse Farming Market Growing?

Rising food security concerns and climate variability driving protected cultivation

Ethiopia faces persistent food security challenges exacerbated by recurrent droughts, erratic rainfall patterns, and climate variability affecting traditional open-field agriculture. With over 85 percent of the population depending on agriculture for livelihood, the vulnerability of rain-fed farming systems has intensified the need for controlled-environment agriculture that ensures consistent crop production regardless of weather conditions. Greenhouse farming provides critical climate resilience by enabling year-round cultivation, protecting crops from extreme temperatures, and optimizing water usage through advanced irrigation systems. In December 2024, the Climate Investment Funds approved a USD 500 Million financial plan to restore degraded landscapes, conserve forests, and enhance food security across Ethiopia, reflecting the scale of investment being mobilized to build agricultural resilience. The growing recognition that traditional farming methods alone cannot sustain the country’s rapidly expanding population is accelerating the adoption of greenhouse technologies across highland, midland, and lowland agro-ecological zones.

Government subsidies, policy support, and strategic national planning

The Ethiopian government has implemented a comprehensive policy framework to promote greenhouse farming through direct subsidies, tax incentives, and strategic planning initiatives. Export-oriented greenhouse investments benefit from income tax exemptions, duty-free importation of greenhouse equipment, irrigation systems, and building materials, and easy access to agricultural land at competitive rental rates. The Ministry of Agriculture has launched a long-term national horticulture strategy that prioritizes food security, export diversification, infrastructure development, and sustainable job creation across the greenhouse and broader horticulture sector. The strategy aims to substantially increase horticulture export earnings over the coming decade through targeted interventions and institutional support. Complementary initiatives including a comprehensive digital agriculture roadmap and the proposed Greenhouse Horticulture Investment Proclamation are establishing a structured regulatory and investment environment that directly encourages greenhouse adoption and modernization across diverse growing regions.

Growing export demand from European and Gulf markets

International market access is emerging as a powerful growth catalyst for Ethiopia's greenhouse farming sector, with rising demand from European Union and Gulf Cooperation Council countries driving investment in export-quality protected cultivation. Ethiopia's geographic proximity to Gulf markets provides a competitive advantage, enabling the delivery of fresh greenhouse-grown produce within hours compared to competitors from Asia or South America. The country's horticultural export volumes continue to expand, with destinations spanning the Middle East, East Africa, and European markets demonstrating growing appetite for Ethiopian produce. The requirement for compliance with international quality standards is encouraging growers to transition from open-field to greenhouse production systems that offer superior product uniformity, traceability, and supply reliability. Expanding cold-chain logistics, improved refrigerated transport corridors, and growing airline cargo capacity are creating the infrastructure necessary to sustain and grow export volumes of greenhouse-produced commodities.

Market Restraints:

What Challenges the Ethiopia Greenhouse Farming Market is Facing?

High construction costs and dependence on imported materials

The absence of local greenhouse manufacturing capacity forces Ethiopian growers to depend entirely on imported steel structures, polyethylene films, climate control equipment, and irrigation components, substantially increasing initial investment costs. This import dependency creates financial barriers particularly for smallholder farmers and small-scale commercial operators seeking to transition from open-field to protected cultivation, slowing broader market penetration across rural agricultural communities.

Limited cold-chain and post-harvest infrastructure

Despite improvements in export logistics, Ethiopia’s cold-chain infrastructure remains insufficient to support the growing volume of perishable greenhouse-produced crops. Inadequate refrigerated storage facilities, limited transport connectivity between rural growing areas and export hubs, and high post-harvest losses undermine the economic viability of greenhouse investments. These infrastructure gaps restrict the ability of growers to access premium domestic and international markets consistently.

Inadequate technical expertise and skilled workforce availability

The successful operation of greenhouse farming systems requires specialized knowledge in climate control management, soilless cultivation techniques, fertigation, and integrated pest management that remains scarce across Ethiopia’s agricultural workforce. Limited access to structured training programs, insufficient extension services focused on protected agriculture, and the absence of local technical support for greenhouse equipment maintenance constrain productivity optimization and discourage broader adoption among potential growers.

Competitive Landscape:

The Ethiopia greenhouse farming market is characterized by a mix of established international horticultural companies and emerging domestic operators competing across floriculture, vegetable, and fruit production segments. Key market participants are differentiating through investments in modern greenhouse structures, advanced cultivation technologies, and international quality certifications to strengthen export competitiveness. Strategic partnerships with development organizations, technology providers, and logistics companies are enabling market players to expand production capacity and improve supply chain efficiency. The competitive environment is further shaped by government incentive programs that attract new entrants, while ongoing sector consolidation through farm expansions and technology upgrades is raising operational standards across the industry.

Ethiopia Greenhouse Farming Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Structure Types Covered |

Glass Greenhouse, Polycarbonate Greenhouse, Polyethylene Greenhouse, Others |

|

Crop Types Covered |

Fruits and Vegetables, Flowers and Ornamentals, Others |

|

Technologies Covered |

Hydroponics, Aquaponics, Aeroponics, Others |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Greenhouse Farming Market Report

The Ethiopia greenhouse farming market size was valued at USD 37.01 Million in 2025.

The Ethiopia greenhouse farming market is expected to grow at a compound annual growth rate of 7.90% from 2026-2034 to reach USD 73.37 Million by 2034.

Polyethylene greenhouse dominated the market with a share of 49.2%, driven by its affordability, lightweight construction, ease of installation, and compatibility with Ethiopia’s diverse agro-climatic conditions favoring low-cost protected cultivation.

Key factors driving the Ethiopia greenhouse farming market include rising food security concerns, government policy support and subsidies, growing export demand from European and Gulf markets, expanding irrigation infrastructure, and increasing adoption of soilless cultivation technologies.

Major challenges include high construction costs due to dependence on imported materials, limited cold-chain and post-harvest infrastructure, inadequate technical expertise for greenhouse operations, climate variability, and insufficient local manufacturing capacity for greenhouse components.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade