Ethiopia Leather and Tannery Market Size, Share, Trends and Forecast by Leather Type, Animal Source, Tanning Process, Finish Type, Application, Distribution Channel, and Region, 2026-2034

Ethiopia Leather and Tannery Market Summary:

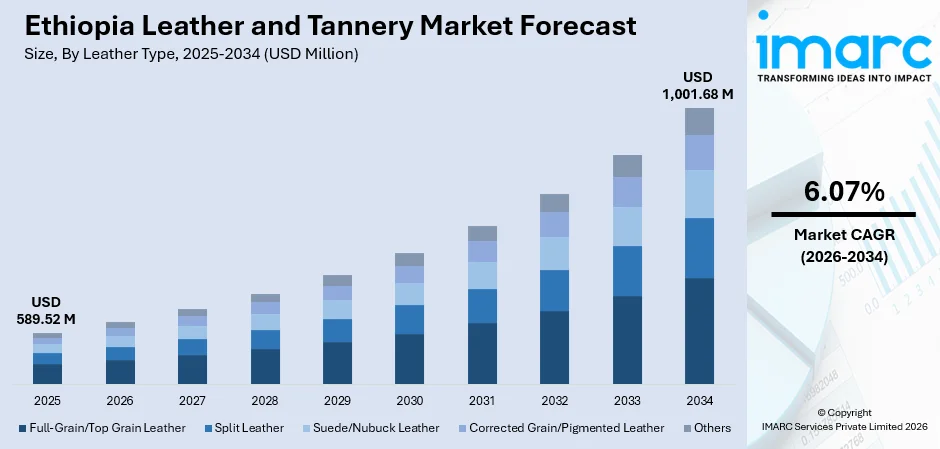

The Ethiopia leather and tannery market size was valued at USD 589.52 Million in 2025 and is projected to reach USD 1,001.68 Million by 2034, growing at a compound annual growth rate of 6.07% from 2026-2034.

As Ethiopia uses its status as Africa's largest cattle holder to bolster its industrial leather processing capabilities, the country's leather and tannery business is growing gradually. Sector expansion is being driven by the government's increased focus on value addition, the rising demand for finished leather goods both domestically and internationally, and the continuous infrastructural development throughout tannery clusters. Ethiopia's leather and tannery market share is being supported by increased investments in sophisticated tanning facilities, worker development initiatives, and sustainable production methods, all of which are improving competitiveness.

Key Takeaways and Insights:

- By Leather Type: Full-grain/top grain leather dominates the market with a share of 36.7% in 2025, owing to its superior durability, natural grain clarity, and strong demand from premium footwear and accessories manufacturers seeking high-quality Ethiopian highland leather.

- By Animal Source: Bovine cattle lead the market with a share of 49.4% in 2025, due to the nation’s massive livestock numbers, which ensure a plentiful and steady availability of raw hides. This consistent internal resource supports local tanning operations and sustains large-scale industrial production cycles.

- By Tanning Process: Chrome tanning dominates the market with a share of 58.1% in 2025, owing to its faster processing time, cost-effectiveness, and ability to produce versatile, soft leather suitable for diverse industrial and consumer applications.

- By Finish Type: Finished leather leads the market with a share of 44.6% in 2025, reflecting the government’s push toward value addition and the growing capacity of Ethiopian tanneries to process hides beyond semi-finished stages for export markets.

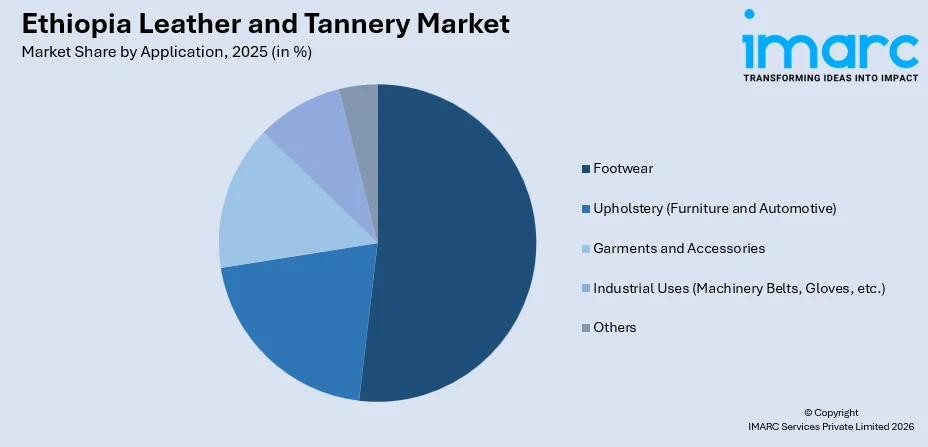

- By Application: Footwear represents the biggest segment with a market share of 52.8% in 2025, reflecting Ethiopia’s strong tradition of leather shoemaking and rising domestic consumption alongside growing export-oriented footwear manufacturing.

- By Distribution Channel: Direct sales exhibit a clear dominance in the market with 46.9% share in 2025, driven by established business-to-business relationships between tanneries, footwear manufacturers, and leather goods producers operating within Ethiopia’s industrial clusters.

- By Region: Addis Ababa is the largest region with 31.7% share in 2025, driven by the concentration of leather product manufacturers, major marketplaces like Merkato, established distribution networks, and proximity to government institutions and export logistics infrastructure.

- Key Players: Key players drive the Ethiopia leather and tannery market by investing in modern processing technologies, pursuing international sustainability certifications, and expanding finished leather production. Their focus on workforce training, quality assurance, and strengthening supply chain linkages with livestock producers enhances competitiveness across both domestic and export markets.

To get more information on this market Request Sample

As Ethiopia promotes the conversion of its vast livestock resources into high-value finished commodities, the country's leather and tannery business is growing. The nation provides a vast and reliable supply of raw materials that support the tanning industry as a whole since it is home to the greatest animal population on the continent. The creation of specialized industrial zones and the encouragement of sophisticated manufacturing to go beyond raw exports are the main government measures driving this change. A dedication to updating industrial centers and simplifying regional logistics is demonstrated by the recent approvals of significant infrastructure projects. Significant investments in tanning technology, an expanding local customer base, and growing foreign demand are all driving this strategic change. These elements, when combined with extensive workforce development initiatives, are creating a strong basis for long-term growth, boosting the industry's general level of global competitiveness, and guaranteeing a place in the global economy for the future.

Ethiopia Leather and Tannery Market Trends:

Growing adoption of sustainable and green tanning practices

In order to meet the demands of global consumers for sustainably produced goods, Ethiopia's leather sector is transitioning toward environmentally conscious production. To reduce their reliance on chemicals and industrial pollutants, tanneries are incorporating cleaner technology, enzyme-based techniques, and sophisticated waste management systems. These programs concentrate on substituting biological materials for dangerous ones throughout the processing phases. The industry is in line with international compliance requirements by placing a high priority on ecological care. Through better environmental governance, these sustainability initiatives help the nation's standing in the global economy and, eventually, the long-term growth and modernization of the local leather and tannery industry.

Expansion of industrial park infrastructure for leather manufacturing

Ethiopia is rapidly developing dedicated leather industrial zones to consolidate tanning operations and improve production efficiency. The government is investing in purpose-built facilities equipped with shared utilities, waste treatment systems, and logistics infrastructure. For instance, in October 2024, Gelila Manufacturing PLC inaugurated its export-standard shoe factory at Bole Lemi Industrial Park with a Birr 2.1 Billion investment, producing 4,000 shoe pairs daily. Such investments are strengthening Ethiopia’s position as a leather manufacturing hub.

Rising focus on international quality certifications and market access

Ethiopian tanneries are aggressively working to get international certifications in order to gain competitive positioning and access to high-end international markets. Manufacturers show their dedication to strict environmental and operational excellence by coordinating their production with the framework established by the Leather Working Group. Numerous domestic companies have already attained high-level memberships, such as gold and silver ratings, which make exporting easier and meet the exacting standards of foreign purchasers. This shift is a calculated turn toward an industrial paradigm that is focused on quality. The industry is improving its traceability and transparency through these certification-backed initiatives, guaranteeing long-term sustainability and a more robust integration into the global leather supply chain.

Market Outlook 2026-2034:

The Ethiopia leather and tannery market is positioned for sustained expansion over the forecast period, driven by the government’s industrialization agenda, growing domestic manufacturing capacity, and strengthening export competitiveness. The market generated a revenue of USD 589.52 Million in 2025 and is projected to reach a revenue of USD 1,001.68 Million by 2034, growing at a compound annual growth rate of 6.07% from 2026-2034. Ongoing development of the Modjo Leather City project, combined with increasing adoption of sustainable tanning technologies and rising investments in finished leather and footwear manufacturing, is expected to create significant value-addition opportunities. Workforce development programs, including vocational training supported by international partners, are building the skilled labor base needed to support industrial scaling. As Ethiopian manufacturers secure more international quality certifications and expand their product portfolios beyond semi-finished leather, the country is well placed to capture a larger share of the global leather trade, driving higher revenue streams and fostering a more competitive and diversified leather industry.

Ethiopia Leather and Tannery Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Leather Type |

Full-Grain/Top Grain Leather |

36.7% |

|

Animal Source |

Bovine Cattle |

49.4% |

|

Tanning Process |

Chrome Tanning |

58.1% |

|

Finish Type |

Finished Leather |

44.6% |

|

Application |

Footwear |

52.8% |

|

Distribution Channel |

Direct Sales |

46.9% |

|

Region |

Addis Ababa |

31.7% |

Leather Type Insights:

- Full-Grain/Top Grain Leather

- Split Leather

- Suede/Nubuck Leather

- Corrected Grain/Pigmented Leather

- Others

Full-grain/top grain leather dominates with a market share of 36.7% of the total Ethiopia leather and tannery market in 2025.

Full-grain/top grain leather holds the leading position in Ethiopia’s leather and tannery market, driven by the country’s reputation for producing high-quality hides with natural clarity, fine grain patterns, and superior fiber structure. Ethiopian cattle hides are internationally recognized for their suitability in premium footwear, garments, and accessories, creating strong demand from domestic manufacturers and global buyers. The growing emphasis on value addition and finished leather exports is reinforcing the dominance of this premium leather category across the country’s tanning operations.

The expansion of modern tannery infrastructure is supporting higher volumes of full-grain leather processing in Ethiopia. For instance, in the first five months of Ethiopia’s fiscal year 2025, leather exports rose by 37% compared with the same period the previous year, reaching USD 14.7 Million, reflecting growing international demand for quality Ethiopian leather. Investments in quality control, compliance with international grading standards, and workforce training in finishing techniques are enabling tanneries to produce export-grade full-grain leather that meets the specifications of premium global footwear and fashion brands.

Animal Source Insights:

- Bovine (Cattle)

- Ovine (Sheep)

- Caprine (Goat)

- Camel

- Others

Bovine cattle lead with a share of 49.4% of the total Ethiopia leather and tannery market in 2025.

Bovine cattle represent the primary animal source within the regional leather market, supported by the nation’s status as a major global livestock holder. This massive population provides an expansive raw material base for producing hides used in footwear, upholstery, and fashion. Bovine hides are favored for their significant surface area, thickness, and versatility across various industrial applications. Consequently, this segment forms the essential foundation of the domestic tanning industry and serves as a critical component of the country’s diverse international export portfolio.

Continuous efforts to enhance hide quality through improved livestock management and modernized slaughtering practices are strengthening the segment’s global competitiveness. By studying international traceability models and sustainable livestock systems, the industry aims to implement higher standards for hide collection and processing. National development institutes are also facilitating capacity-building programs across the entire value chain, from abattoirs to final processors. These initiatives focus on improving efficiency and traceability, ensuring that bovine products meet the rigorous quality demands of the premium global marketplace.

Tanning Process Insights:

- Vegetable Tanning

- Chrome Tanning

- Aldehyde Tanning

- Synthetic Tanning

- Others

Chrome tanning is the largest segment, accounting for 58.1% of the total Ethiopia leather and tannery market in 2025.

Chrome tanning serves as the primary processing method within the regional landscape due to its rapid turnaround time and overall cost efficiency. This technique produces soft, uniform leather that is highly adaptable for diverse applications, ranging from footwear to high-end garments. Because it facilitates high-volume production, most domestic tanneries utilize this approach to satisfy both internal manufacturing needs and international export requirements. The method ensures consistent coloring and physical properties, which remain vital for meeting the rigorous quality specifications demanded by global purchasers.

Simultaneously, the industry is investigating innovative alternatives to mitigate the environmental footprint associated with traditional processing operations. Recent trials of biological unhairing methods have shown that sustainable techniques can achieve results comparable to conventional chemical treatments. These advancements, paired with the development of centralized waste management infrastructure, aim to enhance ecological sustainability without compromising industrial throughput. By integrating modern treatment systems, the sector seeks to maintain its competitive efficiency while evolving toward a more responsible and environmentally conscious production model.

Finish Type Insights:

- Finished Leather

- Semi-Finished Leather (Crust, Wet Blue)

- Raw Hides and Skins

Finished leather holds the largest share at 44.6% of the total Ethiopia leather and tannery market in 2025.

Finished leather leads the segment, reflecting a longstanding policy emphasis on moving the industry up the value chain. Tanneries are increasingly investing in advanced finishing lines, dyeing capabilities, and surface treatment technologies to produce export-ready materials. The growing capacity of domestic manufacturers to absorb these processed hides for footwear and accessories is strengthening demand across industrial clusters. By shifting away from raw materials, the sector is enhancing its economic impact and fostering a more sophisticated manufacturing environment that supports diverse downstream leather applications.

Government policies restricting the export of raw hides have been instrumental in driving this shift toward finished production. Strategic national plans prioritize value addition and finished goods manufacturing as central pillars of sectoral reform. Additionally, support for international environmental accreditations is enabling tanneries to access premium global markets where demand for responsibly produced leather is high. These efforts reflect a broader commitment to quality and compliance, ensuring that domestic products meet the rigorous standards of international buyers while promoting sustainable industrial growth.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Footwear

- Upholstery (Furniture and Automotive)

- Garments and Accessories

- Industrial Uses (Machinery Belts, Gloves, etc.)

- Others

Footwear accounts for the highest share of 52.8% of the total Ethiopia leather and tannery market in 2025.

Footwear is the dominant application segment, driven by a deep-rooted tradition of shoemaking and expanding export-oriented manufacturing capabilities. The country hosts numerous large-scale manufacturers alongside a vibrant community of small-scale artisans producing for domestic and international markets. Growing urbanization and increasing fashion consciousness are sustaining strong demand for leather in this sector. This expansion is supported by a robust internal supply chain that connects tanneries directly to shoe producers, ensuring a steady flow of high-quality material for various consumer footwear styles.

Major investments in manufacturing facilities are accelerating the growth of this segment within dedicated industrial parks. National campaigns and industrial incentives are attracting both domestic and foreign investors to scale up production for global export. These initiatives often include duty exemptions on capital goods and specialized infrastructure designed to streamline output. By fostering a competitive manufacturing environment, the government aims to position the nation as a regional hub for high-quality leather footwear, leveraging its vast livestock resources to gain a global advantage.

Distribution Channel Insights:

- Direct Sales

- Wholesalers/Distributors

- Online Retail

- Others

Direct sales represent the leading segment with 46.9% share of the total Ethiopia leather and tannery market in 2025.

Direct sales dominate the distribution landscape, reflecting established business-to-business procurement structures. Tanneries typically supply finished leather directly to footwear and garment factories through long-term contractual relationships. This channel minimizes intermediary costs, ensures supply chain reliability, and enables customized order fulfillment that meets the specific quality and volume requirements of downstream manufacturers. Such direct interactions foster strong partnerships between suppliers and producers, allowing for better synchronization of production schedules and technical specifications across the diverse leather goods manufacturing sector.

The concentration of industry operations within specific industrial clusters facilitates these direct procurement relationships. These zones host a significant portion of the country's tanneries, creating a dense network of supplier-buyer interactions. Export-oriented transactions also predominantly follow direct sales channels, with international buyers placing orders directly with certified tanneries for specific grades and finishes. This streamlined approach to distribution enhances transparency and traceability, which are increasingly vital for meeting international trade standards and maintaining the trust of global brands and large-scale retailers.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Addis Ababa dominates the Ethiopia leather and tannery market with 31.7% share in 2025.

Addis Ababa holds the leading position in the market, serving as the primary commercial hub for leather product manufacturing, distribution, and trade. The capital is home to the largest concentration of footwear factories and retail marketplaces, providing an extensive ecosystem for wholesale operations. Proximity to international transport hubs and regulatory institutions provides manufacturers with superior logistics and export connectivity. This central location allows for the efficient movement of goods and provides businesses with ready access to both domestic consumers and international shipping routes.

The capital’s importance is reinforced by ongoing industrial investments and targeted policy support. Dedicated industrial parks in the area host multiple leather factories, benefiting from infrastructure designed to support large-scale production and value addition. National initiatives continue to channel resources toward industrial development, strengthening the city's role as the nerve center for leather operations. By integrating manufacturing, commerce, and logistics, the capital serves as a critical driver for the sector's modernization, facilitating the transition from traditional craftsmanship to a globally competitive industrial model.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Leather and Tannery Market Growing?

Abundant livestock resources providing a strong raw material base

Ethiopia’s unparalleled livestock wealth forms the foundational driver of its leather and tannery market expansion, providing an extensive and renewable supply of hides and skins for tanning operations. The country’s diverse animal population yields raw materials internationally renowned for their unique quality, thickness, and flexibility, which are highly suitable for premium garments, fashion accessories, and upholstery. This consistent availability of resources ensures a continuous production cycle for the industry while underscoring the broader economic significance of animal husbandry. Furthermore, ongoing efforts to modernize veterinary services and livestock management aim to enhance the quality and volume of materials by reducing natural defects. By focusing on improved husbandry practices, the sector is strengthening its raw material base to support higher-value processing, ensuring that the inherent characteristics of the hides meet the rigorous standards required for global competitiveness and sustained industrial growth.

Government-led industrialization and infrastructure development

The Ethiopian government has designated the leather sector as a strategic priority, deploying policy instruments to accelerate industrial transformation and attract diverse investment. Key measures include the development of dedicated industrial parks, tax incentives, and direct support for value addition to move the industry toward finished goods rather than raw exports. The centerpiece of this strategy is the development of specialized leather cities designed as eco-friendly, innovation-driven zones. These hubs consolidate tanning operations with shared infrastructure for waste treatment and resource recovery, centralizing essential services to improve operational efficiency. By fostering an integrated manufacturing environment, these initiatives aim to modernize production standards, enhance environmental sustainability, and solidify the nation's position as a regional leader in leather manufacturing and global trade.

Rising international demand for sustainably produced leather

Global markets are increasingly favoring leather products that meet stringent environmental, social, and governance standards, creating a significant opportunity for manufacturers who invest in sustainable production. International brands now require suppliers to demonstrate compliance with sustainability frameworks, driving tanneries to adopt cleaner technologies and pursue recognized certifications that validate responsible manufacturing. This trend is supported by international partnerships and capacity-building programs that help firms secure memberships in global certification bodies. These accreditations evaluate producers against rigorous environmental and operational criteria, significantly strengthening compliance and improving access to premium export markets. As global sustainability requirements continue to tighten, proactive investments in green tanning technologies and certification readiness are positioning the sector to capture growing demand from environmentally conscious buyers worldwide.

Market Restraints:

What Challenges the Ethiopia Leather and Tannery Market is Facing?

Raw material quality and supply chain inefficiencies

Despite possessing vast livestock resources, Ethiopia's leather industry faces persistent challenges in securing high-quality raw hides and skins. The absence of modern husbandry and veterinary systems results in significant hide damage from parasites, diseases, and injuries. Traditional backyard slaughtering practices, which remain the predominant method of animal processing, further degrade hide quality through knife cuts and improper handling. Additionally, rising external demand from West African markets for Ethiopian raw hides for food consumption is diverting supply away from domestic tanneries, compounding input shortages.

Dependence on imported production inputs

Ethiopian tanneries depend heavily on imported chemicals, dyes, machinery, and accessories for leather processing, creating vulnerability to supply chain disruptions and foreign exchange constraints. The country lacks domestic chemical manufacturing capacity, requiring nearly all tanning chemicals to be sourced from international suppliers across Europe and other regions. Chronic foreign currency shortages and lengthy import procedures frequently delay chemical deliveries, forcing tanneries to operate below capacity. These recurring shortages have previously compelled numerous leather factories and tanneries to halt production entirely, while others continued operating at minimal capacity.

Limited environmental compliance infrastructure

The tanning process generates substantial quantities of wastewater, solid waste, and chemical effluent, posing significant environmental challenges for the industry. Processing raw hides produces considerable volumes of liquid and solid waste, requiring specialized treatment infrastructure that many Ethiopian tanneries currently lack. Most tanneries do not operate their wastewater treatment plants efficiently due to high energy costs and insufficient trained personnel. The absence of centralized effluent treatment systems increases operational costs, limits environmental compliance, and restricts access to sustainability-conscious international markets.

Competitive Landscape:

The Ethiopia leather and tannery market features a mix of established domestic tanneries, foreign direct investment enterprises, and small-to-medium scale leather product manufacturers operating across the value chain. Competition is driven by investments in processing technology, capacity expansion, product diversification, and pursuit of international quality certifications. Companies are focusing on upgrading from semi-finished to finished leather production to capture higher margins and meet rising export standards. Strategic partnerships with international organizations and technology providers are enabling knowledge transfer and operational improvements. The presence of numerous companies within the Ethiopian Leather Industries Association reflects a dynamic competitive environment. Market players are also leveraging industrial park infrastructure to reduce costs, access shared services, and strengthen supply chain linkages, positioning themselves for greater competitiveness in both domestic and global leather markets.

Ethiopia Leather and Tannery Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Leather Types Covered |

Full-grain/Top Grain Leather, Split Leather, Suede/Nubuck Leather, Corrected Grain/Pigmented Leather, Others |

|

Animal Sources Covered |

Bovine (Cattle), Ovine (Sheep), Caprine (Goat), Camel, Others |

|

Tanning Processes Covered |

Vegetable Tanning, Chrome Tanning, Aldehyde Tanning, Synthetic Tanning, Others |

|

Finish Types Covered |

Finished Leather, Semi-Finished Leather (Crust, Wet Blue), Raw Hides and Skins |

|

Applications Covered |

Footwear, Upholstery (Furniture and Automotive), Garments and Accessories, Industrial Uses (Machinery Belts, Gloves, etc.), Others |

|

Distribution Channels Covered |

Direct Sales, Wholesalers/Distributors, Online Retail, Others |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Leather and Tannery Market Report

The Ethiopia leather and tannery market size was valued at USD 589.52 Million in 2025.

The Ethiopia leather and tannery market is expected to grow at a compound annual growth rate of 6.07% from 2026-2034 to reach USD 1,001.68 Million by 2034.

Full-grain/top grain leather dominated the market with a share of 36.7%, driven by Ethiopia’s internationally recognized high-quality hides with natural grain clarity and strong demand from premium footwear and accessories manufacturers.

Key factors driving the Ethiopia leather and tannery market include abundant livestock resources, government-led industrialization through industrial parks and policy incentives, rising international demand for sustainably produced leather, and expanding domestic manufacturing capacity.

Major challenges include raw material quality degradation from poor livestock management and traditional slaughtering practices, heavy dependence on imported chemicals and production inputs, foreign currency constraints, limited environmental compliance infrastructure, and supply chain fragmentation across the leather value chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)