Ethiopia Packaged Meat Products Market Size, Share, Trends and Forecast by Product Type, Source, Packaging Type, Distribution Channel, End User, and Region, 2026-2034

Ethiopia Packaged Meat Products Market Summary:

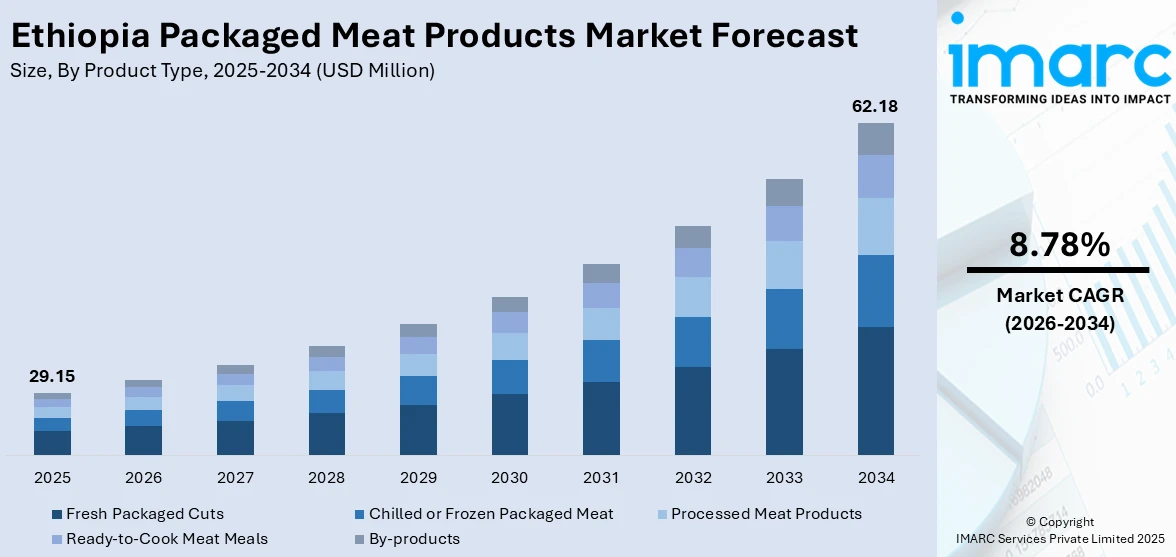

The Ethiopia packaged meat products market size was valued at USD 29.15 Million in 2025 and is projected to reach USD 62.18 Million by 2034, growing at a compound annual growth rate of 8.78% from 2026-2034.

The Ethiopia packaged meat products market is witnessing positive growth in the country due to rapid urbanization, rising income levels, and the changing food landscape. This has led to an increase in demand for packaged meat products. The increase in modern trade facilities, the rise of cold chain networks, and the shift in food safety awareness are creating new demand scenarios. The rising capabilities of livestock farming, as well as the rising interest in hygienic food varieties, are giving scope for the growth of the Ethiopia packaged meat products market share.

Key Takeaways and Insights:

-

By Product Type: Fresh packaged cuts dominate the market with a share of 33.8% in 2025, driven by strong consumer preference for minimally processed meat that aligns with traditional Ethiopian cooking practices and freshness expectations.

-

By Source: Cattle/beef leads the market with a share of 37.6% in 2025, reflecting the cultural significance of beef in Ethiopian cuisine and its widespread use across household and food service applications.

-

By Packaging Type: Plastic films and wraps hold the largest share of 29.4% in 2025, due to their cost-effectiveness, versatility, and ability to maintain meat freshness during short-term storage and retail display.

-

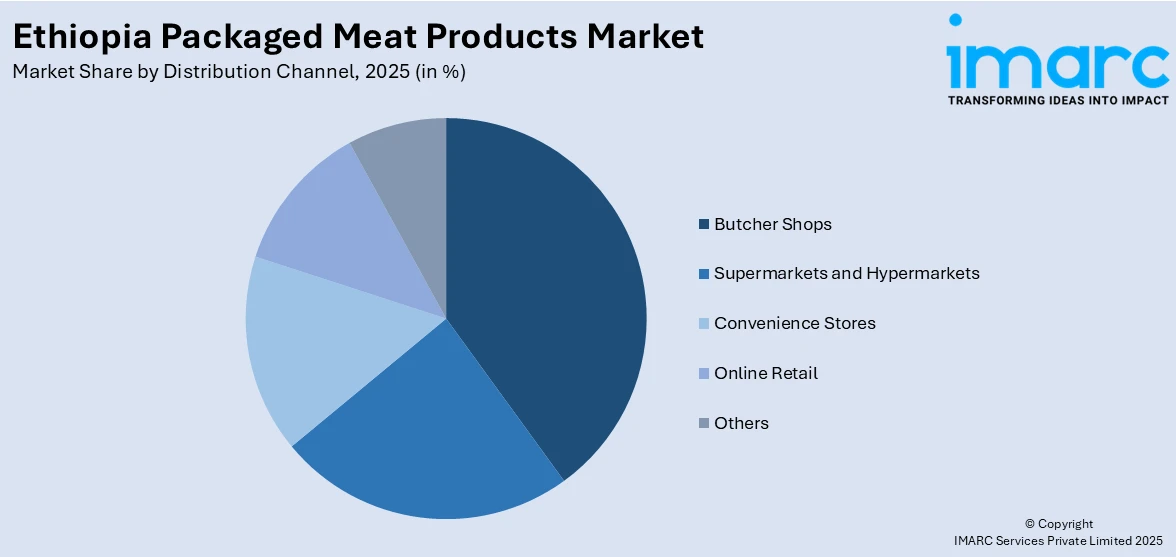

By Distribution Channel: Butcher shops account for the largest share of 31.7% in 2025, driven by deep-rooted consumer trust, personalized service, and accessibility across both urban and semi-urban communities.

-

By End User: Household consumers leads the market with a share of 58.3% share in 2025, underscoring the central role of home-based meat preparation in Ethiopian food culture and daily dietary routines.

-

By Region: Addis Ababa dominate the market with a share of 34.9% 2025, supported by higher population density, stronger purchasing power, and greater availability of modern retail and cold chain infrastructure.

-

Key Players: The Ethiopia packaged meat products market features a mix of domestic abattoirs, regional processors, and emerging agro-industrial enterprises competing across price segments and product categories to expand their footprint.

To get more information on this market Request Sample

The Ethiopia packaged meat market is transforming as part of a larger economic change and an increase in the rate of urbanization. The demand for packaged and ready-to-use meat is increasing due to the rising rate of urbanization and an increase in the need for convenience and hygiene associated with these types of meats compared to unpackaged meats. In December 2025, the Ethiopian government and international partners launched the UPLIFT programme to strengthen the poultry value chain and attract long‑term investment, which is expected to improve meat supply systems and support market‑ready products. Various government initiatives aimed at modernizing the livestock value chain, as well as increased private sector investments in meat technology, are also working as a catalyst for these supplies. Health consciousness is rising, and hence, meat packaged with quality is becoming a growing need for residents living in urban areas. The hotel industry is also flourishing, providing an opportunity for this type of supply to originate.

Ethiopia Packaged Meat Products Market Trends:

Growing Urban Demand for Convenience-Oriented Meat Formats

Ethiopia’s rising urban civilization faces the trend of packaged meat products due to their associated convenience, hygienic, and longer storage life. The rising numbers of dual-income families and declining family sizes among the Ethiopian city populace have increasingly stimulated the packaged model of meat. In the fiscal year ending June 2025, Ethiopia earned US $120 million from exports of meat and halal‑certified by‑products, reflecting broader improvements in quality, processing, and international market acceptance that also support domestic packaged meat supply chains. This change, therefore, is prompting the rise of various meat types and consumer-friendly packaging options, increasing the Ethiopia packaged meat products market.

Expansion of Cold Chain and Processing Infrastructure

There are indications that investments in cold chain facilities and cold stores are picking up significantly in Ethiopia, driven further by government efforts aimed at modernizing facilities and attracting investors in the sector, thus improving cold chain facilities on the routes, enabling retailers to ensure standards are met during transport, starting from slaughter-houses to retail stores, an aspect considered important in venturing into new markets, packaged meats markets, apart from traditional cities. In January 2026, the Ethiopian Trading Business Corporation inaugurated a new cold storage hub in Addis Ababa capable of storing large volumes of animal products, fruits, and vegetables, as part of broader efforts by the Ministry of Trade and Regional Integration to strengthen supply chains and reduce post‑harvest losses.

Rising Food Safety and Quality Awareness Among Consumers

The consumers of Ethiopia are increasingly becoming conscious of the food safety standard, hygiene certification, and traceability of meat product origin. Such increased awareness is pushing demand towards properly labeled, sealed, and quality-assured packaged offerings over their loose, unpackaged variants. In 2024, the Ethiopian government launched a comprehensive National Food Safety Master Plan to strengthen food safety systems, improve regulatory compliance, and align domestic standards with international best practices, a move expected to boost consumer trust in certified and traceable food products. This is being further reinforced by increased consumer confidence in branded and certified packaged meat products through regulatory efforts to strengthen food safety frameworks and increased encouragement towards compliance among processors.

Market Outlook 2026-2034:

The Ethiopia packaged meat products market is poised for sustained expansion over the forecast period, underpinned by accelerating urbanization, ongoing infrastructure modernization, and shifting consumer preferences toward safe, conveniently packaged protein sources. The development of cold chain networks and growing investment in modern processing facilities are expected to enhance market access and broaden product availability across diverse regions. Rising household incomes, increasing food safety awareness, and the gradual formalization of meat supply chains are further anticipated to strengthen demand and support long-term market growth. The market generated a revenue of USD 29.15 Million in 2025 and is projected to reach a revenue of USD 62.18 Million by 2034, growing at a compound annual growth rate of 8.78% from 2026-2034.

Ethiopia Packaged Meat Products Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Fresh Packaged Cuts |

33.8% |

|

Source |

Cattle/Beef |

37.6% |

|

Packaging Type |

Plastic Films and Wraps |

29.4% |

|

Distribution Channel |

Butcher Shops |

31.7% |

|

End User |

Household Consumer |

58.3% |

|

Region |

Addis Ababa |

34.9% |

Product Type Insights:

- Fresh Packaged Cuts

- Chilled or Frozen Packaged Meat

- Processed Meat Products

- Ready-to-Cook Meat Meals

- By-products

The fresh packaged cuts dominates with a market share of 33.8% of the total Ethiopia packaged meat products market in 2025.

Fresh packaged cuts continue to hold their position as the market leader in the packaged meat market in Ethiopia due to the long-standing cultural traditions of the people of the country preferring to consume fresh, unprocessed, or less processed meat in their day-to-day food preparations. In the first half of 2025, Ethiopia expanded chilled goat carcass exports to key Middle Eastern markets, shipping over 5,203 metric tonnes valued at approximately USD 39.09 million, a development that highlights the country’s growing capability in processing and supplying halal‑certified fresh and chilled meat that meets strict hygiene and traceability standards. Fresh packaged cuts of meat are readily available to their customers through traditional distribution channels like open markets and street shops.

The segment is also further supported by the increasing adoption of hygienic packaging techniques by domestic meat processing industries, further enhancing the appeal and shelf life of the products while making minimal alterations to the experience of consuming fresh meat. Urban consumers prefer fresh cuts that have been pre-portioned, thereby saving time while cooking, and maintaining the authenticity as well as health benefits of consuming home-cooked food. The awareness of food safety protocols and quality is further supporting a gradual shift in consumption patterns, choosing fresh cuts over unpackaged,loose variants.

Source Insights:

- Cattle/Beef

- Sheep/Lamb

- Goat/Chevon

- Poultry

- Others

The cattle/beef leads with a share of 37.6% of the total Ethiopia packaged meat products market in 2025.

Cattle and beef products hold the largest share in Ethiopia’s packaged meat market, underpinned by the cultural centrality of beef in Ethiopian cuisine and the country’s substantial cattle population. Beef is a staple in traditional dishes and is consumed widely across household, food service, and institutional channels. The availability of diverse cattle breeds suited to local agroecological conditions supports consistent supply, while growing investments in feedlot operations and commercial breeding programs are enhancing the quality and volume of beef available for processing and packaging.

Beef's prominence is further reinforced by its adaptability across diverse product formats, from fresh cuts and minced preparations to processed varieties. The adoption of improved slaughter and packaging practices at modern abattoirs is elevating the quality of packaged beef, broadening its consumer appeal. Additionally, strengthening food safety certification frameworks and traceability measures are building greater consumer trust in commercially packaged beef products, consolidating the segment's dominant position across distribution channels and end-user categories in the market.

Packaging Type Insights:

- Cans

- Vacuum Packs

- Trays

- Plastic Films and Wraps

- Others

The plastic films and wraps dominates with a market share of 29.4% of the total Ethiopia packaged meat products market in 2025.

Plastic films and wraps constitute the most widely used packaging format in Ethiopia's packaged meat market, driven by their cost-effectiveness, lightweight characteristics, and suitability for short-term meat preservation. These packaging solutions align well with the country's predominant retail landscape, where butcher shops and smaller outlets require flexible, easy-to-use wrapping materials that maintain product visibility while providing essential protection against contamination. Their practicality and accessibility make them indispensable across traditional and emerging retail environments.

The segment's dominance is reinforced by the practical advantages of plastic films in markets where advanced packaging technologies remain limited. As retail standards evolve and food safety expectations increase, plastic films and wraps are being enhanced with improved barrier properties and sealing capabilities to extend product freshness. Their widespread availability and affordability position them as the preferred packaging choice for processors and retailers serving both urban and peri-urban consumers across Ethiopia's expanding packaged meat landscape.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Butcher Shops

- Online Retail

- Others

The butcher shops leads with a share of 31.7% of the total Ethiopia packaged meat products market in 2025.

Butcher shops remain the primary distribution channel for packaged meat products in Ethiopia, anchored by strong consumer trust, personalized service, and deep accessibility across urban and semi-urban neighborhoods. Ethiopian consumers have traditionally relied on butcher shops for meat purchases, valuing the ability to inspect products firsthand, request custom cuts, and receive guidance on freshness and quality. This relationship-driven purchasing model continues to dominate despite the gradual expansion of modern retail formats across the country.

The channel's resilience is further supported by the widespread geographic presence of butcher shops, which serve as the most convenient access point for the majority of Ethiopian meat buyers. Many butcher shops are increasingly adopting basic packaging and refrigeration practices to meet evolving consumer expectations for hygiene and product safety. This gradual modernization is effectively bridging the gap between traditional meat retailing and contemporary packaged meat standards, reinforcing the channel's dominant market position.

End User Insights:

- Household Consumer

- Food Service Industry

- Institutional Buyers

The household consumers dominates with a market share of 58.3% of the total Ethiopia packaged meat products market in 2025.

Household consumers constitute the largest end-user segment in Ethiopia's packaged meat products market, reflecting the central importance of home-based meal preparation in Ethiopian food culture. The majority of meat purchased is destined for household kitchens, where traditional cooking practices involve preparing fresh and lightly processed meat into culturally significant dishes. Rising disposable incomes, urban expansion, and growing family sizes are sustaining robust household demand for conveniently packaged meat products across diverse income groups.

The increasing availability of packaged meat products in local butcher shops, convenience stores, and supermarkets is making it easier for households to access quality-controlled options. Health and hygiene awareness among urban families is gradually shifting purchasing behavior toward sealed, labeled products that provide assurance of safety and freshness. This trend is particularly notable in Addis Ababa and other major urban centers where evolving lifestyles and modern consumption patterns are accelerating demand.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Addis Ababa exhibits a clear dominance with a 34.9% share of the total Ethiopia packaged meat products market in 2025.

Addis Ababa's leadership in the packaged meat products market is underpinned by its position as Ethiopia's political, economic, and commercial capital, housing the largest concentration of middle-class and high-income consumers. The city's advanced retail infrastructure, including supermarkets, hypermarkets, and specialty food outlets, provides extensive distribution networks for packaged meat products. A thriving hospitality and food service sector further amplifies demand for standardized, quality-assured meat offerings, while the concentration of institutional buyers adds additional consumption volume to the capital's dominant market position.

The capital also benefits from superior cold chain infrastructure and close proximity to major meat processing facilities, enabling consistent product availability and freshness across retail and food service channels. Higher food safety awareness among Addis Ababa's urban population drives stronger preference for branded and certified packaged products compared to other regions. Ongoing urban expansion, sustained population growth, and increasing consumer sophistication continue to strengthen the city's position as the primary demand center for Ethiopia's packaged meat products market.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Packaged Meat Products Market Growing?

Rapid Urbanization and Changing Dietary Patterns

Ethiopia’s accelerating urbanization is fundamentally reshaping food consumption patterns across the country. As populations concentrate in cities and secondary urban centers, demand for convenient, hygienic, and shelf-stable food products is rising significantly. Urban consumers, characterized by busier lifestyles and greater exposure to modern retail environments, are increasingly seeking packaged meat products that offer time savings, portion control, and assured quality. This demographic transition is creating sustained demand for diverse packaged meat formats, from fresh cuts to ready-to-cook options. The growing middle class in urban areas demonstrates higher willingness to pay premium prices for properly packaged and branded meat products, further accelerating market expansion and encouraging processors to invest in product diversification and quality enhancement.

Government-Led Livestock Sector Modernization

The Ethiopian government has prioritized the modernization of the livestock value chain as a key component of its broader economic development strategy. Initiatives aimed at improving animal husbandry practices, establishing certified abattoirs, and upgrading meat processing infrastructure are strengthening the supply-side foundation for packaged meat products. In May 2025, the government launched the second phase of a national livestock capacity‑building project in collaboration with UNIDO and international partners to enhance meat value chain competitiveness, improve certification and inspection systems, and expand market reach for meat and livestock products. These programs focus on enhancing productivity, ensuring food safety compliance, and creating formal market linkages between producers and processors. Policy support for cold chain development, export-oriented processing facilities, and quality certification systems is creating an enabling environment for commercial meat packaging operations. As the formal meat processing sector expands, more producers gain access to standardized packaging, storage, and distribution capabilities, broadening the availability and diversity of packaged meat products across domestic markets.

Expanding Modern Retail and Cold Chain Infrastructure

The growth of modern retail formats, including supermarkets, hypermarkets, and organized convenience stores, is providing critical distribution channels for packaged meat products in Ethiopia. These outlets require standardized, properly packaged, and labeled products, driving processors to adopt higher quality and packaging standards. In 2026, French retail giant Carrefour entered the Ethiopian market through a franchise and supply agreement with Queens Supermarket PLC (Midroc Investment Group), with plans to rebrand 13 existing stores and expand into additional outlets by 2028, marking a significant expansion of modern retail infrastructure that supports distribution of packaged foods, including meats. The parallel expansion of cold chain logistics networks is enabling the safe transport and storage of perishable meat products across longer distances. Investments in refrigerated transport, cold storage facilities, and retail-level refrigeration are extending the shelf life and geographic reach of packaged meat products beyond major urban centers. This infrastructure development is particularly significant for enabling access to quality packaged meat in secondary cities and emerging market areas, where demand is growing but supply chain capabilities have historically been limited.

Market Restraints:

What Challenges the Ethiopia Packaged Meat Products Market is Facing?

Underdeveloped Cold Chain Infrastructure in Rural Areas

Despite ongoing improvements, cold chain infrastructure remains inadequate in many parts of Ethiopia, particularly in rural and semi-urban regions. Limited access to refrigeration at production, transport, and retail levels restricts the distribution of perishable packaged meat products. This infrastructure gap constrains market expansion beyond major urban centers and contributes to product spoilage and quality inconsistencies.

Consumer Preference for Unpackaged Fresh Meat

A significant portion of Ethiopian consumers, especially in traditional and lower-income segments, continue to prefer purchasing unpackaged meat directly from butcher shops and open markets. Cultural familiarity, perceived freshness, and price sensitivity favor loose meat purchases over packaged alternatives. This entrenched preference slows the transition toward branded and commercially packaged products across broader consumer demographics.

Limited Processing Capacity and Fragmented Supply Chain

Ethiopia’s meat processing sector remains relatively small and fragmented, with limited large-scale commercial operations capable of meeting growing urban demand for packaged products. Supply chain inefficiencies, including inconsistent livestock quality, informal slaughter practices, and inadequate quality control, pose challenges. These structural constraints affect product standardization, availability, and the ability to scale operations cost-effectively.

Competitive Landscape:

The Ethiopia packaged meat products market is characterized by a developing competitive landscape, with a mix of established domestic processors and emerging commercial enterprises competing for market share. Companies are focusing on upgrading processing facilities, improving packaging quality, and expanding distribution networks to reach a growing urban consumer base. Strategic investments in cold chain capabilities and food safety certifications are becoming key differentiators. The market is witnessing gradual consolidation as larger players seek to formalize supply chains and establish branded product lines, while smaller operators compete through localized distribution and competitive pricing strategies.

Recent Developments:

-

In November 2025, Ethiopia officially began trading under the African Continental Free Trade Area (AfCFTA), dispatching its first shipments of goods, including meat and other processed/packaged products, to Kenya, Somalia, and South Africa as key export markets, marking a major boost in intra‑African food trade integration.

Ethiopia Packaged Meat Products Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Fresh Packaged Cuts, Chilled or Frozen Packaged Meat, Processed Meat Products, Ready-to-Cook Meat Meals, By-products |

|

Sources Covered |

Cattle/Beef, Sheep/Lamb, Goat/Chevon, Poultry, Others |

|

Packaging Types Covered |

Cans, Vacuum Packs, Trays, Plastic Films and Wraps, Others |

|

Distribution Channels Covered |

Supermarkets and Hypermarkets, Convenience Stores, Butcher Shops, Online Retail, Others |

|

End Users Covered |

Household Consumer, Food Service Industry, Institutional Buyers |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Packaged Meat Products Market Report

The Ethiopia packaged meat products market size was valued at USD 29.15 Million in 2025.

The Ethiopia packaged meat products market is expected to grow at a compound annual growth rate of 8.78% from 2026-2034 to reach USD 62.18 Million by 2034.

Fresh packaged cuts, holding the largest revenue share of 33.8%, remains the leading product type in Ethiopia’s packaged meat market, driven by strong cultural preferences for fresh, minimally altered meat used in traditional home-prepared dishes.

Key factors driving the Ethiopia packaged meat products market include rapid urbanization and changing dietary preferences, government-led livestock sector modernization initiatives, expanding modern retail and cold chain infrastructure, and growing consumer awareness of food safety and hygiene standards.

Major challenges include underdeveloped cold chain infrastructure in rural areas, strong consumer preference for unpackaged fresh meat from traditional sources, limited processing capacity, fragmented supply chains, and structural constraints in quality standardization across the meat value chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)