Ethiopia Telecommunication Towers Market Size, Share, Trends and Forecast by Type of Tower, Fuel Type, Installation, Ownership, and Region, 2026-2034

Ethiopia Telecommunication Towers Market Summary:

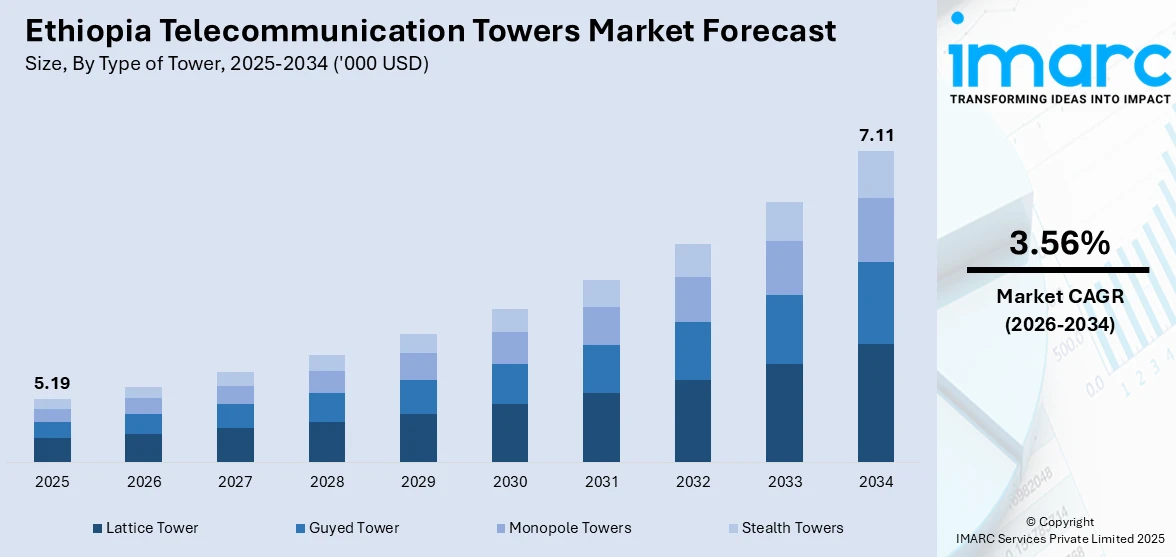

The Ethiopia telecommunication towers market size was valued at USD 5.19 Thousand in 2025 and is projected to reach USD 7.11 Thousand by 2034, growing at a compound annual growth rate of 3.56% from 2026-2034.

The Ethiopia telecommunication towers market is experiencing steady growth driven by rising mobile connectivity demands, government-led digital transformation initiatives, and expanding network coverage across urban and rural regions. Increasing subscriber penetration, accelerating deployment of advanced wireless technologies, and investments in infrastructure modernization are strengthening the telecommunications landscape. The growing need for reliable connectivity to support economic development, financial inclusion, and public service delivery continues to propel demand for telecommunication tower infrastructure nationwide.

Key Takeaways and Insights:

- By Type of Tower: Lattice tower dominates the market with a share of 44.5% in 2025, owing to its superior load-bearing capacity, structural versatility for multi-operator hosting, and suitability for both urban and rural deployments across diverse Ethiopian terrains. Growing network densification requirements are fueling continued adoption.

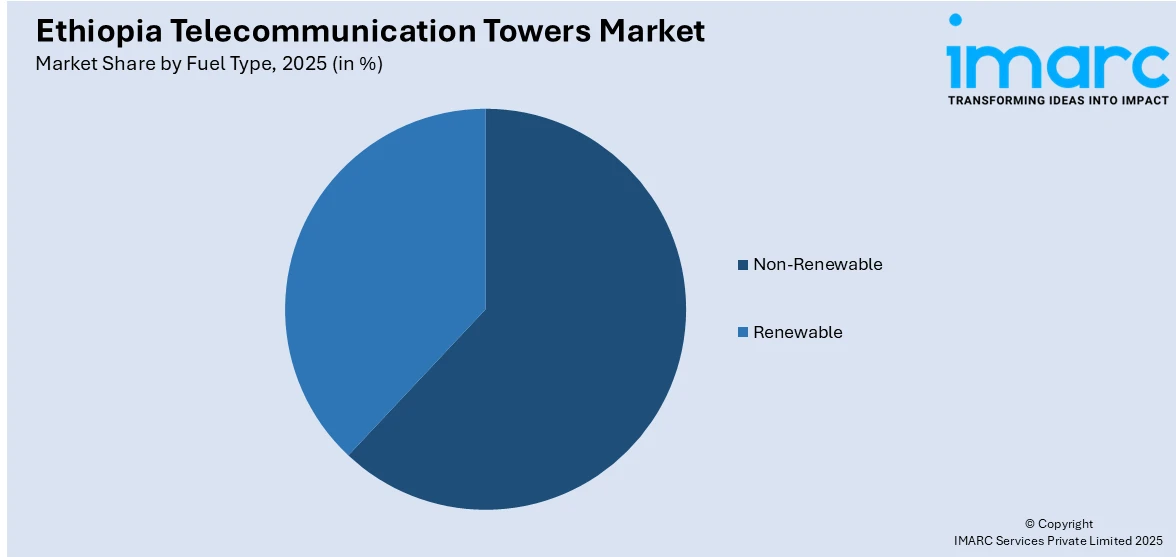

- By Fuel Type: Non-renewable leads the market with a share of 61.8% in 2025, driven by widespread reliance on diesel generators to ensure uninterrupted power supply at tower sites, particularly in off-grid and underserved regions where national electricity grid access remains limited.

- By Installation: Ground-based holds the largest segment with a market share of 72.4% in 2025, reflecting the predominance of standalone tower deployments in rural and semi-urban areas where available land and the need for wide coverage favor ground-mounted infrastructure over rooftop alternatives.

- By Ownership: Operator-owned exhibits a clear dominance in the market with 48.6% share in 2025, reflecting the current regulatory landscape where independent tower company licensing is absent, compelling mobile network operators to self-build and manage their own tower infrastructure portfolios.

- By Region: Addis Ababa represents the largest region with 36.9% share in 2025, driven by the concentration of subscriber density, commercial activity, corporate headquarters, and advanced network deployments including early 5G rollouts in the capital city and its surrounding metropolitan area.

- Key Players: Key players drive the Ethiopia telecommunication towers market by expanding network coverage, investing in advanced tower technologies, strengthening rural connectivity, and forming strategic partnerships to accelerate infrastructure deployment, improve service quality, and support the nation’s digital transformation goals across diverse geographic and demographic segments.

To get more information on this market Request Sample

The Ethiopia telecommunication towers market is advancing as the nation pursues ambitious connectivity goals under its Digital Ethiopia 2025 roadmap and broader digital transformation agenda. The telecommunications sector is undergoing a significant structural shift following the liberalization of the market, which has introduced competitive dynamics that are driving accelerated tower deployment across the country. With approximately 10,000 towers currently serving a population exceeding 129 million, Ethiopia faces one of the highest population-to-tower ratios on the African continent, underscoring the substantial infrastructure deficit that presents significant growth opportunities. The government’s emphasis on universal broadband access, coupled with operator-led investments in 4G and 5G infrastructure, is catalyzing tower construction activity. Renewable energy integration, local tower manufacturing initiatives, and planned regulatory reforms for independent tower companies are further shaping the market’s trajectory toward sustained expansion and modernization.

Ethiopia Telecommunication Towers Market Trends:

Accelerated 5G Network Deployment Driving Tower Densification

The rapid expansion of fifth-generation wireless services across Ethiopian cities is driving demand for new tower infrastructure and upgrades to existing sites. Operators are prioritizing urban centers and regional capitals for advanced network rollouts, necessitating denser tower configurations to deliver high-speed, low-latency connectivity. This trend is reshaping the tower landscape as both macro and small-cell deployments increase to accommodate growing data consumption patterns among the youth-dominated population. The state-owned operator has steadily extended its 5G services to numerous cities nationwide, reflecting the accelerating pace of next-generation network infrastructure development across the country.

Integration of Solar-on-Tower Solutions for Energy Sustainability

The adoption of renewable energy solutions at tower sites is gaining momentum as operators seek to reduce operational costs and diesel dependency. Innovative solar-on-tower configurations, which integrate photovoltaic panels directly onto telecommunication structures, are emerging as viable alternatives for space-constrained urban sites. This approach addresses persistent grid unreliability while supporting broader sustainability objectives aligned with national climate commitments. The state-owned operator has been actively deploying solar solutions across multiple sites during recent fiscal periods, demonstrating the growing commitment to green energy transition in telecommunications.

Localization of Tower Manufacturing and Supply Chain Development

The emergence of domestic tower manufacturing capabilities is transforming Ethiopia’s telecommunication infrastructure supply chain. Local production of galvanized steel towers reduces import dependency, shortens delivery timelines, and supports cost-effective network expansion across the country. This trend aligns with broader industrial development goals and strengthens the domestic telecommunications ecosystem. In May 2024, Woda Metal Industrial Park became the first Ethiopian company to supply locally manufactured telecommunication towers, delivering 68 towers valued at 50 Million Birr under an initial agreement that supports the broader ambition of constructing thousands of new tower sites nationally.

Market Outlook 2026-2034:

The Ethiopia telecommunication towers market is poised for sustained expansion over the forecast period as the country addresses its substantial connectivity infrastructure deficit through coordinated government and private sector investment. The ongoing deployment of 4G and 5G networks, combined with planned regulatory reforms to license independent tower companies, is expected to introduce competitive dynamics that will accelerate tower construction and improve tenancy ratios. Growing mobile subscriber penetration, rising data consumption, and the government’s emphasis on bridging the urban-rural digital divide through targeted rural site development will continue to drive demand for new tower infrastructure. Additionally, the integration of renewable energy solutions, expansion of fiber backhaul networks, and the emergence of local tower manufacturing capabilities are strengthening the foundation for long-term market growth and infrastructure resilience. The market generated a revenue of USD 5.19 Thousand in 2025 and is projected to reach a revenue of USD 7.11 Thousand by 2034, growing at a compound annual growth rate of 3.56% from 2026-2034.

Ethiopia Telecommunication Towers Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type of Tower |

Lattice Tower |

44.5% |

|

Fuel Type |

Non-Renewable |

61.8% |

|

Installation |

Ground-Based |

72.4% |

|

Ownership |

Operator-Owned |

48.6% |

|

Region |

Addis Ababa |

36.9% |

Type of Tower Insights:

- Lattice Tower

- Guyed Tower

- Monopole Towers

- Stealth Towers

Lattice tower dominates with a market share of 44.5% of the total Ethiopia telecommunication towers market in 2025.

Lattice towers maintain their dominant position in Ethiopia’s telecommunication infrastructure landscape owing to their exceptional structural strength and adaptability across diverse geographic conditions. These self-supporting triangular or square cross-section structures offer superior wind-load resistance, making them particularly suited for Ethiopia’s varied topography ranging from highland plateaus to lowland plains. Their modular design allows operators to install multiple antennas and equipment from different technology generations simultaneously, supporting the concurrent operation of 2G, 3G, 4G, and 5G services on a single structure.

The continued preference for lattice towers is further reinforced by their cost-effectiveness over extended operational lifespans and their capacity to accommodate infrastructure-sharing arrangements between multiple operators. As Ethiopia’s telecommunications market undergoes liberalization and competitive dynamics intensify, lattice structures provide the structural headroom necessary for co-location, which is increasingly important given regulatory discussions around mandatory infrastructure sharing. The emergence of local manufacturing through companies like Woda Metal Industrial Park, which delivered its first batch of domestically produced towers in 2024, is reducing procurement costs and lead times for lattice tower deployment, further supporting their market dominance.

Fuel Type Insights:

Access the comprehensive market breakdown Request Sample

- Renewable

- Non-Renewable

Non-renewable leads with a share of 61.8% of the total Ethiopia telecommunication towers market in 2025.

Non-renewable energy sources, predominantly diesel generators, continue to power the majority of Ethiopia’s telecommunication tower sites due to the persistent challenges of grid reliability and access across much of the country. Despite Ethiopia’s substantial hydropower capacity, distribution bottlenecks and frequent outages particularly outside major urban centers necessitate dependable backup power solutions. Diesel generators provide the consistent uptime required for continuous network operations, especially in remote and off-grid locations where grid connectivity remains absent.

The sustained dominance of non-renewable fuel sources also reflects the high initial capital expenditure required for renewable energy installations and the logistical challenges of importing solar panels and battery systems in a foreign-currency-constrained economy. However, the landscape is gradually evolving as operators increasingly recognize the long-term cost savings and operational benefits of transitioning to greener alternatives. In the 2024-2025 fiscal year alone, the state-owned operator deployed solar solutions at 141 tower sites, achieving a 40 percent reduction in diesel generator usage from six hours to two hours daily at equipped locations, signaling a slow but definitive shift toward hybrid energy models.

Installation Insights:

- Rooftop

- Ground-Based

Ground-based holds the largest segment with a 72.4% share of the total Ethiopia telecommunication towers market in 2025.

Ground-based tower installations dominate the Ethiopian market due to the country's predominantly rural demographic distribution and the extensive geographic coverage requirements that characterize its telecommunications expansion strategy. With a vast population spread across a large geographic area, ground-mounted towers provide the elevation and signal propagation necessary to serve dispersed communities across highland plateaus, rift valley lowlands, and remote pastoral areas. The availability of land in non-urban settings further favors ground-based deployments, which offer greater flexibility in antenna height and equipment hosting capacity compared to rooftop alternatives.

The strategic emphasis on closing Ethiopia's substantial connectivity gap is reinforcing the demand for ground-based installations, particularly as operators expand into previously unserved rural areas. Under its Next Horizon strategy announced in August 2025, the state-owned operator committed to developing numerous new mobile sites, with a significant proportion specifically targeting rural areas, with the vast majority expected to utilize ground-based configurations. This rural expansion initiative reflects both commercial imperatives and regulatory obligations to extend coverage to underserved populations, ensuring ground-based installations remain the backbone of Ethiopia's tower infrastructure for the foreseeable future.

Ownership Insights:

- Operator-Owned

- Joint Venture

- Private-Owned

- MNO Captive

Operator-owned represents the leading segment with a 48.6% share of the total Ethiopia telecommunication towers market in 2025.

Operator-owned towers constitute the largest ownership category in Ethiopia’s telecommunication towers market, reflecting the country’s unique regulatory environment where independent tower company licensing has not yet been formalized. The state-owned incumbent operates the majority of the nation’s tower portfolio, having built and maintained network infrastructure over its 130-year operational history. This ownership concentration is a direct consequence of the historically monopolistic market structure and the absence of a dedicated regulatory framework for tower infrastructure companies.

The operator-owned model is expected to gradually evolve as Ethiopia's telecommunications regulatory framework matures and incorporates provisions for independent tower companies. Regulatory bodies and international development institutions have recommended liberalizing the tower company market and introducing dedicated licensing frameworks for infrastructure companies that would confer rights to construct, operate, and lease telecommunications equipment. These proposed reforms aim to encourage private sector participation, improve infrastructure sharing efficiency, reduce deployment costs, and accelerate network expansion across underserved regions of the country.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Addis Ababa holds the largest share with 36.9% of the total Ethiopia telecommunication towers market in 2025.

Addis Ababa dominates the Ethiopia telecommunication towers market as the nation's political, economic, and technological epicenter. The capital city hosts the highest concentration of mobile subscribers, commercial enterprises, government institutions, and international organizations, creating intensive connectivity demands that necessitate dense tower infrastructure. Addis Ababa serves as the primary deployment zone for advanced technologies, including the country's first fifth-generation wireless network. The metropolitan area's high population density and rapid urbanization continue to drive demand for both macro towers and small-cell solutions.

The capital's role as the headquarters for major telecommunications operators further reinforces its dominance in tower infrastructure concentration. Ongoing urban expansion and the proliferation of digital financial services, e-commerce platforms, and government digital portals are intensifying network traffic volumes across the metropolitan region. Additionally, the presence of diplomatic missions, continental organizations, and multinational corporations creates premium connectivity requirements that necessitate continuous tower infrastructure investment, upgrades, and capacity enhancement to maintain reliable and high-quality telecommunications services throughout the city.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Telecommunication Towers Market Growing?

Government-Led Digital Transformation Initiatives and Regulatory Reforms

The Ethiopian government's commitment to digital transformation through strategic national programs is creating a powerful catalyst for telecommunication tower market expansion. The Digital Ethiopia roadmap established universal broadband access as a national priority, while subsequent regulatory reforms have opened the market to competition for the first time in the country's telecommunications history. The liberalization framework enabled the licensing of a second mobile operator and initiated structural changes that are driving accelerated infrastructure deployment. The Ethiopian Communications Authority is actively working to create a more competitive environment by revising regulatory frameworks, setting interconnection rates, and evaluating the introduction of tower company licenses. Recent regulatory directives have specifically established a pathway for further market entry, including provisions that could enable the formation of independent infrastructure companies. These coordinated policy actions are strengthening the institutional foundation for sustained tower market growth and encouraging private sector participation in telecommunications infrastructure development across the country.

Rapidly Expanding Mobile Subscriber Base and Rising Data Consumption

Ethiopia's rapidly growing mobile subscriber base and escalating data consumption patterns are generating substantial demand for new tower infrastructure and capacity upgrades at existing sites. The country represents the largest telecom market in East Africa, with mobile subscriptions creating continuous pressure on operators to expand and densify their networks. The youth-dominated demographic profile, combined with increasing smartphone adoption and the proliferation of data-intensive applications, is accelerating the need for enhanced network capacity and coverage. Average monthly data usage per subscriber continues to climb as digital financial services, social media platforms, and government digital services drive increased connectivity utilization. The combination of population growth, urbanization trends, and digital service proliferation ensures that demand for tower infrastructure will continue to outpace current supply. The state-owned operator continues to add millions of new customers each fiscal period, further underscoring the relentless demand trajectory driving tower deployment and reinforcing the critical need for sustained investment in telecommunications infrastructure across both urban and rural areas of the country.

Massive Capital Investment in Network Infrastructure Expansion

Unprecedented levels of capital investment by both incumbent and new-entrant operators are directly fueling the construction of new telecommunication towers across Ethiopia. The competitive dynamics introduced by market liberalization have triggered significant investment commitments as operators race to expand coverage and improve service quality. Both operators are making substantial capital expenditure commitments to build, lease, and upgrade tower infrastructure across urban and rural areas. These investments are complemented by international development financing and strategic partnerships that provide additional capital and technical expertise for network deployment. The private operator announced an ambitious multi-year plan to significantly expand its tower network, aiming to substantially multiply its operational base through large-scale construction activity. This scale of investment, combined with the incumbent's own expansion commitments under its Next Horizon strategy, is creating a robust construction pipeline that will considerably expand Ethiopia's tower inventory over the forecast period and strengthen the nation's telecommunications infrastructure foundation.

Market Restraints:

What Challenges the Ethiopia Telecommunication Towers Market is Facing?

Persistent Power Infrastructure Deficits and Grid Unreliability

Ethiopia’s inadequate power infrastructure presents a significant obstacle to telecommunication tower operations and expansion. National electricity grid coverage reaches less than 60 percent of the population, leaving substantial portions of the country without reliable power access. Frequent outages, even in connected areas, force operators to depend heavily on expensive diesel generators, significantly increasing operational expenditure. Distribution bottlenecks persist despite the country’s substantial hydropower generation capacity, and importing renewable energy equipment is constrained by chronic foreign currency shortages.

Foreign Currency Scarcity and Import Dependencies

Ethiopia’s persistent foreign currency shortages represent a major constraint on telecommunication tower deployment and maintenance. Tower construction and operation require substantial imports of specialized equipment, including antenna systems, transmission components, diesel generators, and solar power installations. The country’s limited foreign exchange reserves create procurement delays, increase costs through parallel market premiums, and force operators to frequently revise network expansion timelines. This challenge is compounded by external debt obligations that further restrict the availability of foreign currency for private sector imports.

Absence of Independent Tower Company Regulatory Framework

The lack of a formalized licensing regime for independent tower companies constrains competitive efficiency and cost optimization in Ethiopia’s tower market. Without dedicated infrastructure company licenses, operators must self-build and manage their own tower portfolios, leading to duplicative infrastructure investment and suboptimal tenancy ratios. This regulatory gap prevents the entry of specialized tower management firms that could improve operational efficiency, accelerate rural deployment, and reduce per-site costs through multi-tenant business models. The resulting market structure limits options for cost-effective tower deployment.

Competitive Landscape:

The Ethiopia telecommunication towers market features a concentrated competitive landscape shaped by the country’s evolving regulatory framework and recent market liberalization. The market structure is transitioning from a historically monopolistic model toward a more competitive environment, with operators investing heavily in tower infrastructure to expand coverage and improve service quality. Competition is primarily focused on network expansion, technology upgrades, and service differentiation, with both existing operators pursuing aggressive tower construction programs. The anticipated introduction of independent tower company licenses and a potential third mobile operator is expected to further intensify competitive dynamics, encouraging infrastructure sharing, operational efficiency improvements, and innovative deployment strategies that will reshape the tower ownership and management landscape across the country.

Recent Developments:

- In August 2025, Ethio Telecom, in collaboration with Huawei, announced the successful commercial deployment of Africa’s first Solar-on-Tower solution in Ethiopia. The innovative technology integrates photovoltaic panels directly onto telecommunication towers, addressing space constraints in urban areas. Initial results demonstrated a 40 percent reduction in diesel generator usage at equipped sites, with solar power sustaining operations for up to four hours daily.

- In August 2025, Ethio Telecom launched its "Next Horizon: Digital & Beyond 2028 Strategy," a three-year plan committing to the construction of 1,228 new mobile sites, including 322 in rural areas. The strategy also outlined plans to increase 4G LTE coverage to 85 percent of the population, deploy 5G in 10 additional cities, and convert up to 1,000 tower sites annually to green energy solutions.

Ethiopia Telecommunication Towers Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Thousand USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types of Towers Covered |

Lattice Tower, Guyed Tower, Monopole Towers, Stealth Towers |

|

Fuel Types Covered |

Renewable, Non-Renewable |

|

Installations Covered |

Rooftop, Ground-Based |

|

Ownerships Covered |

Operator-Owned, Joint Venture, Private-Owned, MNO Captive |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Telecommunication Towers Market Report

The Ethiopia telecommunication towers market size was valued at USD 5.19 Thousand in 2025.

The Ethiopia telecommunication towers market is expected to grow at a compound annual growth rate of 3.56% from 2026-2034 to reach USD 7.11 Thousand by 2034.

Lattice tower dominated the market with a share of 44.5%, owing to its superior load-bearing capacity, structural versatility for multi-operator hosting, and proven suitability across diverse Ethiopian terrains and deployment environments.

Key factors driving the Ethiopia telecommunication towers market include government-led digital transformation initiatives, rapidly expanding mobile subscriptions, massive capital investments in network infrastructure, rising data consumption, and accelerating 4G and 5G deployment across the country.

Major challenges include persistent power infrastructure deficits and grid unreliability, chronic foreign currency shortages impacting equipment imports, absence of independent tower company licensing frameworks, security concerns in conflict-affected regions, and high operational costs associated with diesel dependency.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)