Ethiopia Warehousing Market Size, Share, Trends and Forecast by Warehouse Type, End Use, and Region, 2026-2034

Ethiopia Warehousing Market Summary:

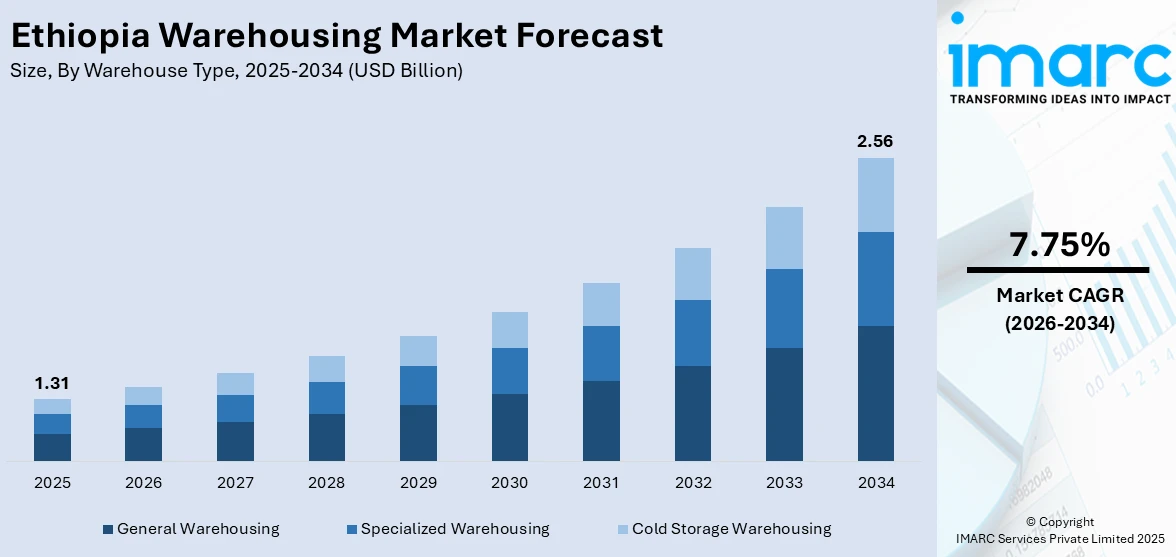

The Ethiopia warehousing market size was valued at USD 1.31 Billion in 2025 and is projected to reach USD 2.56 Billion by 2034, growing at a compound annual growth rate of 7.75% from 2026-2034.

The Ethiopia warehousing market is experiencing robust expansion as the country strengthens its logistics ecosystem and deepens trade integration across the Horn of Africa. Accelerating urbanization, rising domestic consumption, and the emergence of organized retail channels are intensifying demand for modern storage solutions. Government-led initiatives to develop industrial parks, special economic zones, and multimodal transport corridors are creating a more conducive environment for warehousing investments. Additionally, the growing agricultural processing sector and expanding e-commerce landscape are reinforcing the need for efficient, scalable, and temperature-controlled warehousing infrastructure, positioning Ethiopia as a key logistics gateway in East Africa and supporting the Ethiopia warehousing market share.

Key Takeaways and Insights:

- By Warehouse Type: General warehousing dominates the market with a share of 46.9% in 2025, owing to its versatility in handling diverse commodity categories, lower operational costs compared with specialized facilities, and strong alignment with the storage requirements of Ethiopia's expanding retail and manufacturing sectors.

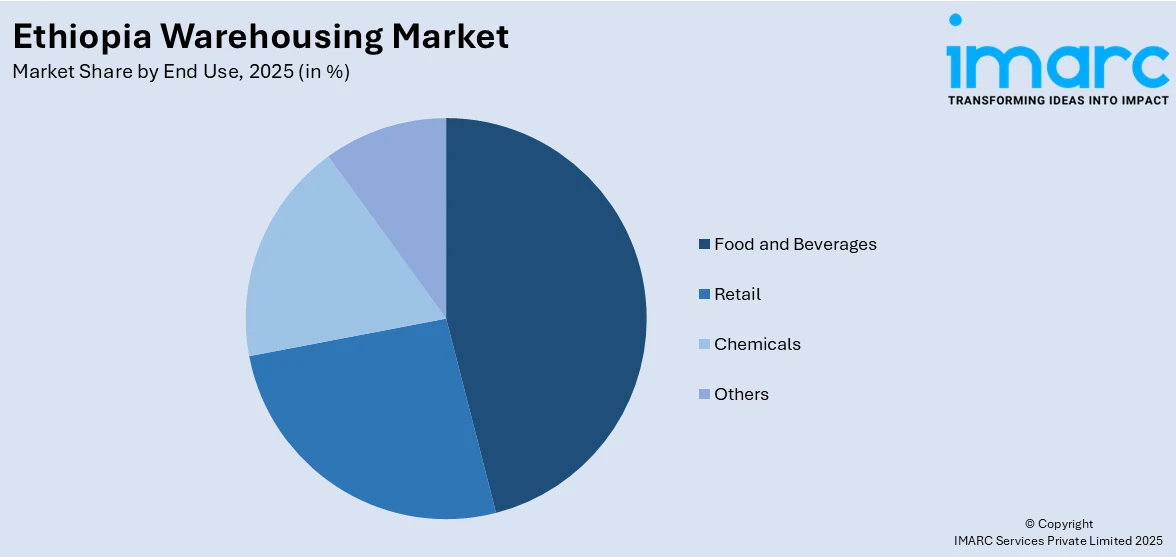

- By End Use: Food and beverages lead the market with a share of 38.6% in 2025. This dominance is driven by Ethiopia's large agricultural output, growing food processing activities, and the critical need for efficient post-harvest storage to minimize losses and support domestic and export supply chains.

- By Region: Addis Ababa represents the largest region with 42.1% share in 2025, driven by the concentration of commercial activity, industrial parks, dry port infrastructure, and the presence of major logistics operators and distribution networks serving the national capital.

- Key Players: Key players drive the Ethiopia warehousing market by expanding storage capacity, investing in modern facility infrastructure, strengthening cold chain capabilities, and forming strategic partnerships with logistics operators to improve supply chain efficiency and meet rising demand across diverse end-use sectors.

To get more information on this market Request Sample

The Ethiopia warehousing business is progressing as the nation seeks to advance its logistics infrastructure as a priority in the national development agenda. The nation's drive to transform the existing industrial parks into special economic zones has seen a significant focus on the development of the nation's logistics infrastructure. A notable focus of the government has been the enhancement of foreign direct investment in the nation's logistics infrastructure and the improvement of road and rail connectivity along the nation's trade routes. The East Africa nation has seen the expansion of electronic business platforms and the development of payment systems, which has a significant impact on the warehousing business in the country. The nation's strategic location as a gateway to the East Africa region has seen a significant focus placed on the warehousing business as it seeks to position itself strategically in the region.

Ethiopia Warehousing Market Trends:

Digital Transformation of Warehouse Operations

Ethiopia's warehousing sector is progressively adopting digital technologies to enhance operational efficiency and supply chain visibility. Logistics operators are implementing warehouse management systems, GPS tracking, and automated inventory solutions across key storage facilities. For instance, in February 2024, Ethiopian Airlines Group launched a dedicated e-commerce logistics facility at Addis Ababa Bole International Airport, equipped with consolidation, sortation, repacking, and real-time shipment tracking capabilities. The growing integration of digital platforms for trade facilitation and customs processing is reshaping how warehousing operations function, supporting the Ethiopia warehousing market growth.

Expansion of Cold Storage and Specialized Facilities

The demand for temperature-controlled and specialized warehousing facilities is rising steadily as Ethiopia seeks to reduce post-harvest losses and strengthen agricultural export supply chains. Cold storage infrastructure is expanding across urban and peri-urban areas to support food safety, pharmaceutical distribution, and perishable commodity handling. Investments in modern perishable cargo terminals and refrigerated storage facilities are providing producers with more reliable end-to-end cold chain capabilities. Government partnerships with private operators are further accelerating cold chain development across the country, enhancing Ethiopia's capacity to manage temperature-sensitive goods for both domestic consumption and international markets.

Industrial Parks Transitioning to Special Economic Zones

Transition toward Special Economic Zones Industrial parks are transitioning toward special economic zones, an initiative that seeks to integrate the logistics and warehousing sectors with industrialization. Ethiopia has promoted a majority of its industrial parks into special economic zones by offering substantial incentives such as customs duty exemption to private sector investors pouring money into integrated logistics and warehousing facilities within the sectors. As a result of integrating the sectors, a new and more efficient competitor is being developed across the country with regard to the warehousing sector.

Market Outlook 2026-2034:

The warehousing industry in the Ethiopian market is expected to continue to grow with ongoing modernization in the country's infrastructure, dynamics in policy regulation, and an increased trajectory in commercial activity in different industries. The country's government, in its push to improve the transportation infrastructure by implementing multimodal transportation systems and developing economic zones, is expected to further improve the efficiency of the logistics sector, particularly in the storage industry. Factors such as ongoing urbanization developments, the proliferation of new outlets in the retail industry, and the enhancement of the e-commerce market are also set to see the warehousing industry continue to grow in the country. The development of some critical infrastructural projects in the country, such as the ongoing Mieso-Dire Dawa Expressway and the modernization of the rail linkages, is also set to further improve the efficiency of the warehousing industry in the country and the performance of the broader market in the region. The market generated a revenue of USD 1.31 Billion in 2025 and is projected to reach a revenue of USD 2.56 Billion by 2034, growing at a compound annual growth rate of 7.75% from 2026-2034.

Ethiopia Warehousing Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Warehouse Type |

General Warehousing |

46.9% |

|

End Use |

Food and Beverages |

38.6% |

|

Region |

Addis Ababa |

42.1% |

Warehouse Type Insights:

- General Warehousing

- Specialized Warehousing

- Cold Storage Warehousing

General warehousing dominates with a market share of 46.9% of the total Ethiopia warehousing market in 2025.

General warehousing remains the most widely utilized storage format in Ethiopia, serving as the backbone of the country's logistics infrastructure. These facilities accommodate a broad spectrum of goods, including consumer products, industrial materials, and agricultural commodities, offering flexible and cost-effective storage solutions for businesses of varying scales. The growth of retail distribution networks, manufacturing activity, and import trade volumes is driving sustained demand for general warehousing capacity across major urban centers and logistics corridors. Ethiopia's industrial space demand has been rising, reflecting the strong underlying need for expanded storage capacity.

The expanding network of dry ports and inland logistics hubs is further strengthening the general warehousing segment by creating centralized storage and distribution nodes. Government initiatives to improve road connectivity and develop industrial zones are enhancing the accessibility and operational efficiency of general warehousing facilities. The Modjo dry port near Addis Ababa serves as a critical warehousing and distribution center. As trade volumes continue to grow and supply chain formalization accelerates, general warehousing is expected to maintain its leading position in Ethiopia's storage landscape.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Retail

- Food and Beverages

- Chemicals

- Others

Food and beverages lead with a share of 38.6% of the total Ethiopia warehousing market in 2025.

Food and beverages represnt the largest end-use segment for warehousing in Ethiopia, given the size of the country's agricultural production base and the critical need to avoid losses. The agricultural sector is the largest contributor to the economy of Ethiopia and the largest employer of the workforce across the country. Volumes of cereals, pulses, oil seeds, coffee, and horticulture are produced in the country. These crops need to be efficiently stored prior to the processing and distribution phase. The government is effectively introducing the receipt system for warehouses and is promoting the construction of agro-industrial parks.

The growing food processing industry and expanding consumer demand for packaged and perishable food products are further intensifying the need for dedicated warehousing infrastructure in this segment. In November 2024, Ethiopia achieved a milestone by launching its first refrigerated shipment of fruits and vegetables to Europe, exporting 12 tonnes of sugar snap and mangetout to the Netherlands via the Djibouti corridor. This development highlights the country's advancing cold chain capabilities and the increasing importance of warehousing solutions that maintain product quality throughout the distribution chain, supporting both domestic food security and export competitiveness.

Regional Insights:

- Addis Ababa

- Oromia Region

- Amhara Region

- SNNPR Region

- Tigray Region

- Others

Addis Ababa holds the largest share at 42.1% of the total Ethiopia warehousing market in 2025.

Addis Ababa appears to be the main center of operations for warehousing and logistics activities due to the concentration of trade activities and government services. Due to the proximity of the Modjo dry port, which accounts for most of Ethiopia’s containerized imports, most of the trade-related activities take place within the city. The existence of industrial parks like Bole Lemi and Kilinto, which have been recognized as special economic zones, provides integrated services that include warehousing and industrial activities reflecting the potential for attracting investors.

The capital's warehousing sector is further supported by ongoing investments in cold chain infrastructure and e-commerce logistics. In January 2025, the Ethiopian Trading Business Corporation inaugurated a cold storage facility in Addis Ababa's Akaki Kality area, built on 1.14 hectares with a capacity to store over 2,000 tons of fruits and vegetables. Additionally, Ethiopian Airlines' cargo terminal at Bole International Airport, with an annual handling capacity of one Million tonnes, positions Addis Ababa as a critical warehousing and air cargo node, reinforcing the city's dominance in the national warehousing landscape.

Market Dynamics:

Growth Drivers:

Why is the Ethiopia Warehousing Market Growing?

Expanding Infrastructure Development and Multimodal Connectivity

Ethiopia's ambitious infrastructure development program is creating a more connected and efficient logistics network that directly supports warehousing demand. The construction of new road networks, railway systems, and dry port facilities is establishing integrated multimodal transportation solutions that reduce logistics costs, improve delivery efficiency, and enhance access to warehousing facilities across the country. These improvements are particularly significant for a landlocked nation that depends on efficient trade corridors to maintain competitiveness. Major expressway projects along the eastern economic corridor are set to strengthen connectivity between inland logistics hubs and port access routes, with new toll roads running parallel to the Addis Ababa-Djibouti railway expected to significantly reduce transport time and costs along Ethiopia's primary trade corridor. Ongoing investments in modernizing railway infrastructure and developing integrated dry port facilities are further reinforcing multimodal logistics capabilities. Such infrastructure investments are expanding the reach and viability of warehousing operations across the country.

Government Policy Initiatives Promoting Special Economic Zones and Foreign Investment

The proactive policy environment set by the Ethiopian government toward developing a better environment for warehousing development through establishing special economic zones, as well as implementing various incentives, will potentially set up a better environment in favor of warehousing development, as evidenced by the formulation of various benefits with the enactment of the special economic zone proclamation, where customs duty exemption, as well as tax holiday benefits, will significantly favor warehousing development enterprises that intend to establish or set up operations within the Republic of Ethiopia. Likewise, it has been observed that there was a significant majority of industrial parks established and developed by the Ethiopian Industrial Parks Development Corporation that have been developed as special economic zones under the Ethiopian Investment Commission, significantly increasing the number of special economic zones developed within the Republic of Ethiopia, where commercial activities will be consolidated, setting a better potential for warehousing development operations, as a significant percentage of goods will be utilized for the local market environment.

Rising Urbanization and Growth of the Consumer Economy

The rapid urbanization of Ethiopia and an expanding consumer economy continue to create sustained demand for warehousing infrastructure that supports the distribution of goods across growing urban centers. With increasingly concentrated population factors, especially in urban cities, the demand has risen for organized retail, food distribution, and consumer goods storage. Equally, the emergence of e-commerce platforms and digital payment systems quickens the demand for fulfillment centers, last-mile distribution hubs, and temperature-controlled storage. Expansion of mobile money services has been disruptive, with the number of mobile money accounts recording exponential growth in recent years, according to the National Bank of Ethiopia. The rapid adoption of digital payments facilitates seamless online transactions, therefore supporting the growth of e-commerce logistics infrastructure. Consumer spending patterns are likely to continue changing, with further retail formalization pushing up demand for warehouses across Ethiopia's major population centers, requiring heavy investment in modern storage capacity.

Market Restraints:

What Challenges the Ethiopia Warehousing Market is Facing?

Inadequate Transportation and Road Infrastructure

Despite ongoing improvements, Ethiopia's transportation network remains underdeveloped in many regions, particularly in rural and semi-urban areas. Poor road conditions increase transit times, raise transportation costs, and limit the effective reach of warehousing facilities. The country's landlocked geography compounds these challenges, as import-export trade depends on the Addis-Djibouti corridor. Congestion at key logistics nodes, insufficient last-mile connectivity, and limited road capacity in secondary cities continue to constrain the efficient movement of goods to and from storage facilities, reducing overall supply chain reliability.

Foreign Exchange Constraints and Currency Volatility

Ethiopia faces significant foreign exchange shortages that affect the ability of businesses to import construction materials, warehouse equipment, and technology systems essential for modern storage operations. The Ethiopian birr has experienced considerable volatility, and access to foreign currency for imports remains tightly regulated. These constraints increase the cost of developing and maintaining modern warehousing facilities, limiting investment in advanced infrastructure. Currency instability also creates uncertainty for foreign investors considering warehousing and logistics projects, potentially slowing the pace of capacity expansion.

Limited Access to Modern Warehousing Technology and Skills

The availability of advanced warehouse management systems, automated handling equipment, and skilled logistics professionals remains limited in Ethiopia. Many businesses continue to rely on traditional storage methods that lack the efficiency and scalability required for modern supply chain operations. The shortage of Grade A warehousing space, particularly in secondary cities, restricts options for businesses seeking high-specification storage solutions. Additionally, the limited pool of trained warehouse management professionals and technicians constrains the adoption of technology-driven operational improvements, affecting service quality and throughput efficiency.

Competitive Landscape:

The competitive landscape of the Ethiopia warehousing market consists of state-run enterprises, domestic companies, and emerging international players competing to cater to the rising warehousing requirements of the country. The competitive landscape of the market is changing with the opening of opportunities by the government for foreign investment through joint ventures, thus promoting the liberalization of the country’s logistics market. Companies are shifting their strategies toward expanding storage capacity, enhancing the quality of storage facilities, and developing specialized capabilities. Collaborations are taking place between domestic companies and international players, thus enhancing the quality of the service provided. The transformation of industrial parks into special economic zones is changing the competitive landscape through the opening of opportunities for diverse investments.

Ethiopia Warehousing Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Warehouse Types Covered |

General Warehousing, Specialized Warehousing, Cold Storage Warehousing |

|

End Uses Covered |

Retail, Food and Beverages, Chemicals, Others |

|

Regions Covered |

Addis Ababa, Oromia Region, Amhara Region, SNNPR Region, Tigray Region, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Ethiopia Warehousing Market Report

The Ethiopia warehousing market size was valued at USD 1.31 Billion in 2025.

The Ethiopia warehousing market is expected to grow at a compound annual growth rate of 7.75% from 2026-2034 to reach USD 2.56 Billion by 2034.

General warehousing dominated the market with a share of 46.9%, driven by its versatility in accommodating diverse commodity types, cost-effectiveness, and strong alignment with the storage needs of Ethiopia's expanding retail and manufacturing sectors.

Key factors driving the Ethiopia warehousing market include expanding infrastructure development and multimodal connectivity, government policy initiatives promoting special economic zones, rising urbanization, growing food and beverages processing needs, and increasing e-commerce activity.

Major challenges include inadequate transportation infrastructure in secondary regions, foreign exchange constraints limiting equipment imports, limited access to modern warehousing technology, shortage of skilled logistics professionals, and high construction costs for Grade A facilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)