Europe Automotive Exhaust Aftertreatment Systems Market Size, Share, Trends and Forecast by Vehicle Type, Fuel Type, Filter Type, and Country, 2026-2034

Europe Automotive Exhaust Aftertreatment Market Size and Share:

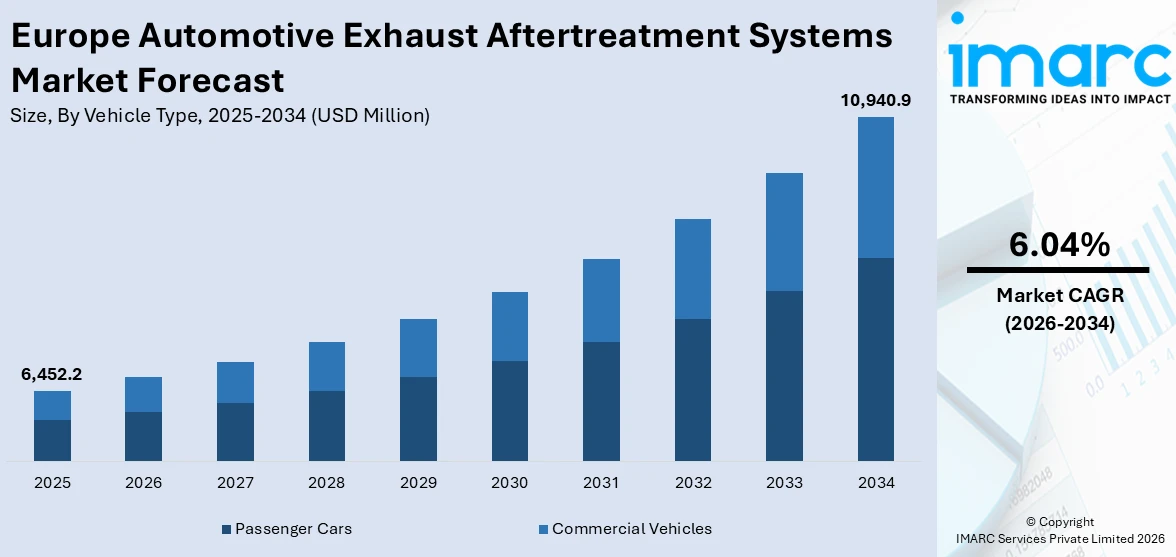

The Europe automotive exhaust aftertreatment systems market size was valued at USD 6,452.2 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 10,940.9 Million by 2034, exhibiting a CAGR of 6.04% during 2026-2034. The market is experiencing steady growth, driven by stringent emission regulations, rising hybrid vehicle adoption, and advancements in material technologies. Increasing demand for sustainable mobility solutions and real-world emissions compliance continues to fuel innovation. These factors are collectively contributing to the expansion of the Europe automotive exhaust aftertreatment systems market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 6,452.2 Million |

| Market Forecast in 2034 | USD 10,940.9 Million |

| Market Growth Rate 2026-2034 | 6.04% |

The market is driven by the region’s strategic commitment to achieving carbon neutrality and its ambitious climate targets under the European Green Deal. According to the European Environment Agency, the EU has shown a firm strategic commitment under the European Green Deal towards achieving carbon neutrality by 2050, along with cutting net greenhouse gas emissions by 55% by 2030. This has led to enhanced governmental support for research and development in emission-reduction technologies, particularly targeting nitrogen oxides (NOx), carbon monoxide (CO), and particulate matter (PM). Additionally, the lifecycle emissions of vehicles, including those from production and disposal, are receiving growing regulatory scrutiny, pushing manufacturers to develop more efficient, sustainable aftertreatment solutions. The integration of digital diagnostics and onboard sensors to monitor system performance and ensure compliance is further contributing to the Europe automotive exhaust aftertreatment systems market growth by enabling predictive maintenance and real-time emissions tracking.

To get more information on this market Request Sample

Moreover, the rising penetration of synthetic fuels and biofuels in the transportation sector necessitates exhaust aftertreatment systems that can adapt to varying combustion characteristics and chemical profiles. Fleet operators, particularly in the commercial vehicle segment, are increasingly prioritizing low-emission compliance to meet environmental benchmarks and avoid penalties in low-emission zones (LEZs) and ultra-low-emission zones (ULEZs). As supply chain resilience becomes more critical, localized production and material sourcing for exhaust components are also emerging as influential factors. Together, these developments are reinforcing the importance of advanced aftertreatment systems within Europe’s evolving automotive landscape.

Europe Automotive Exhaust Aftertreatment Systems Market Trends:

Regulatory Push Driving Advanced Aftertreatment Adoption

One of the prominent Europe automotive exhaust aftertreatment systems market trends is the increasing stringency of regulations. Beginning January 1, 2025, the Euro 6e-bis Standard introduced more rigorous testing procedures for plug-in hybrid vehicles (PHEVs), resulting in higher CO₂ emission figures and potential tax penalties for models emitting over 50g/km. This regulatory pressure is pushing manufacturers to adopt advanced aftertreatment technologies that ensure compliance. Simultaneously, the EU’s Real Driving Emissions (RDE) framework now mandates that testing reflect 95% of real-world driving conditions, including variables like altitude, ambient temperature, payload, and vehicle dynamics. These policies are creating strong market incentives for innovation in exhaust systems that can maintain performance and emissions control in real-life conditions, beyond traditional laboratory tests.

Electrification Trends Redefining Aftertreatment Strategies

The electrification wave is reshaping the landscape of Europe’s exhaust aftertreatment systems, though traditional engines remain relevant. According to ACEA, in Q1 2025, battery-electric vehicle sales increased by 23.9% to 412,997 units, representing 15.2% of the EU car market. Additionally, hybrid-electric car registrations surged by 20.7%, reaching 964,108 units, or 35.5% of the market. While these vehicles emit fewer pollutants, the majority of hybrids still rely on internal combustion engines (ICEs), which require efficient aftertreatment systems to remain compliant with environmental standards. The transition toward hybrids, especially plug-in hybrids affected by Euro 6e-bis rules, is prompting the development of aftertreatment technologies that operate efficiently in dynamic powertrain modes, ensuring reduced emissions regardless of drive cycle.

Technological Innovation and Material Advancements

Advancements in materials and technologies are primarily creating a positive Europe automotive exhaust aftertreatment systems market outlook. With a rising emphasis on sustainability and performance, manufacturers are leveraging advanced materials and coatings that enhance durability and system efficiency, supporting longer operational life and lower emissions. This is critical as internal combustion engines remain in widespread use despite electrification trends. Meanwhile, the enforcement of real-world driving emissions (RDE) standards—covering 95% of real driving conditions—has accelerated the need for robust aftertreatment systems that perform consistently across diverse operational environments. These innovations are vital as OEMs aim to address challenges posed by the Euro 6e-bis standards and fluctuating demand for ICE and hybrid models amid shifting market dynamics.

.webp)

Europe Automotive Exhaust Aftertreatment Systems Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Europe automotive exhaust aftertreatment systems market, along with forecasts at the regional/country levels from 2026-2034. The market has been categorized based on vehicle type, fuel type, and filter type.

Analysis by Vehicle Type:

- Passenger Cars

- Commercial Vehicles

Passenger cars play a pivotal role in the market due to their high volume and direct regulatory exposure. As the region enforces increasingly stringent emission standards, particularly for urban mobility, passenger vehicles must integrate efficient aftertreatment systems to reduce pollutants such as NOx and particulate matter. This segment includes a growing share of hybrid and plug-in hybrid models, which require adaptable exhaust solutions to manage emissions across varying powertrain modes. Additionally, consumer demand for fuel-efficient and environmentally friendly cars drives automakers to invest in compact, lightweight aftertreatment technologies, further elevating the segment’s importance within the evolving European emissions landscape.

Commercial vehicles represent a significant segment in the Europe automotive exhaust aftertreatment systems market due to their high emissions output and operational intensity. These vehicles, including trucks, vans, and buses, are essential to freight and passenger transport but contribute substantially to urban air pollution. Consequently, they face rigorous compliance requirements under EU emissions regulations, necessitating robust aftertreatment systems such as selective catalytic reduction (SCR), diesel particulate filters (DPF), and advanced NOx control technologies. Given their longer lifespans and higher fuel consumption, commercial vehicles demand durable, cost-effective solutions. Their critical role in logistics and public transportation further enhances their prominence in the regional aftertreatment ecosystem.

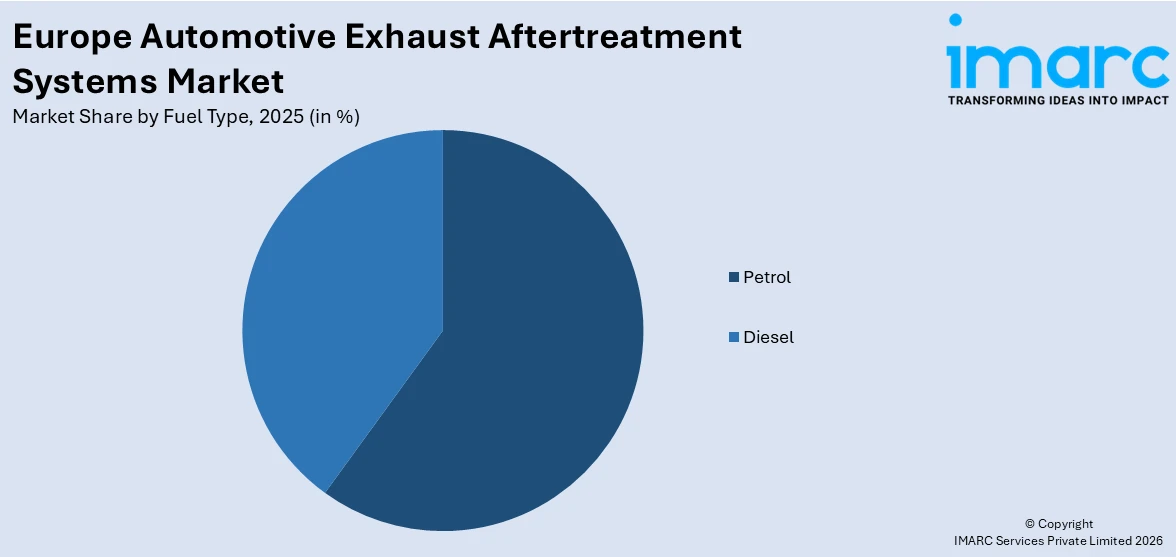

Analysis by Fuel Type:

Access the comprehensive market breakdown Request Sample

- Petrol

- Diesel

Petrol-powered vehicles continue to represent a substantial share of the Europe automotive exhaust aftertreatment systems market, especially within the passenger car segment. As emission norms tighten, even petrol engines—once considered cleaner than diesel—are subject to advanced aftertreatment requirements to curb pollutants like carbon monoxide, hydrocarbons, and particulate matter. The introduction of Gasoline Particulate Filters (GPFs) has become essential in meeting Euro 6 and newer emission standards. Additionally, the rise of turbocharged petrol engines, which improve efficiency but increase exhaust particulates, further drives the need for effective aftertreatment solutions. As consumer preference shifts from diesel to petrol, this segment maintains a strong regulatory and technological focus.

Diesel engines, widely used in commercial vehicles and some passenger cars, hold a prominent position in the market due to their higher emission levels of nitrogen oxides (NOx) and particulate matter (PM). To comply with stringent European regulations, diesel vehicles rely heavily on technologies such as Selective Catalytic Reduction (SCR), Diesel Oxidation Catalysts (DOC), and Diesel Particulate Filters (DPF). Despite a gradual decline in diesel car sales, the technology remains critical for long-haul, high-torque applications where diesel’s fuel efficiency is unmatched. Therefore, the diesel segment continues to drive innovation and demand for advanced, high-durability aftertreatment systems across Europe.

Analysis by Filter Type:

- Particulate Matter Control System

- Carbon Compounds Control System

- Emission Control Using Decision Matrix

- NOx Control System

Particulate Matter (PM) Control Systems play a crucial role in the market, especially as emission standards increasingly target fine particulate emissions from both diesel and gasoline engines. Technologies such as Diesel Particulate Filters (DPFs) and Gasoline Particulate Filters (GPFs) are vital in trapping and oxidizing soot particles before they exit the tailpipe. With urban air quality concerns intensifying and stricter Euro standards in place, PM control systems are no longer limited to heavy-duty vehicles but are now standard in many passenger cars as well. Their ability to significantly reduce health-impacting particulates makes them indispensable in the region’s clean mobility framework.

Carbon Compounds Control Systems are essential in limiting the release of harmful carbon-based emissions such as carbon monoxide (CO), carbon dioxide (CO₂), and unburned hydrocarbons. These systems typically include three-way catalytic converters, which oxidize CO and hydrocarbons into less harmful substances while reducing NOx emissions. In Europe, where reducing greenhouse gas emissions is a regulatory priority under the Green Deal, carbon compound control technologies are under constant development. Their integration into both petrol and hybrid vehicles ensures that even as engine technologies evolve, emissions of carbon compounds remain within permissible levels. This segment is central to both regulatory compliance and environmental sustainability initiatives.

Emission Control Using Decision Matrix refers to advanced, algorithm-driven systems that optimize the operation of various aftertreatment components based on driving conditions, engine load, fuel type, and real-time emissions data. These intelligent systems play a growing role in the Europe automotive exhaust aftertreatment market by ensuring that emissions remain within regulatory limits under real-world driving conditions, as mandated by the EU’s Real Driving Emissions (RDE) framework. By coordinating components such as SCR, DPF, and EGR (Exhaust Gas Recirculation), these systems enhance overall efficiency and system responsiveness. Their increasing adoption highlights the shift toward data-driven, adaptive emissions management strategies that improve long-term compliance and performance.

NOx Control Systems are a cornerstone of Europe’s automotive exhaust aftertreatment system technologies, particularly in diesel-powered and hybrid vehicles. Nitrogen oxides are among the most heavily regulated pollutants due to their contribution to smog and respiratory issues. To reduce NOx levels, technologies like Selective Catalytic Reduction (SCR), NOx Storage Catalysts (NSC), and Exhaust Gas Recirculation (EGR) are extensively deployed. The enforcement of Euro 6 and upcoming Euro 7 standards has intensified the need for precise and efficient NOx reduction. These systems are especially critical for commercial and long-distance vehicles, where high combustion temperatures lead to increased NOx production. Their prominence reflects Europe’s strong regulatory and environmental priorities.

Country Analysis:

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Netherlands

- Switzerland

- Poland

- Others

Germany holds a leading position in the Europe automotive exhaust aftertreatment systems market due to its dominant automotive industry, home to major OEMs like Volkswagen, BMW, and Mercedes-Benz. The country's commitment to engineering excellence and emissions innovation drives significant investment in aftertreatment research and development. Germany is also a key player in shaping EU environmental policies and is often among the first to implement stricter emission regulations. With its strong presence in both passenger and commercial vehicle production, the demand for advanced exhaust systems is substantial. Furthermore, Germany’s growing focus on hybrid and low-emission vehicles reinforces its central role in advancing aftertreatment technologies.

The United Kingdom plays a significant role in the market, supported by a strong automotive engineering sector and regulatory alignment with EU emission standards. Despite Brexit, the UK continues to enforce stringent emission rules and invest in low-emission transportation solutions. Key vehicle manufacturers and Tier 1 suppliers in the country are actively engaged in developing innovative emission control technologies. The rise of hybrid and plug-in hybrid vehicle adoption, along with nationwide efforts to reduce urban air pollution, supports ongoing demand for particulate filters, NOx control systems, and integrated aftertreatment solutions. The UK’s focus on sustainability enhances its importance in the regional market.

France is a vital contributor to the market’s expansion, driven by strong environmental policies and a sizable domestic auto industry led by manufacturers like Renault and Peugeot. The country has taken aggressive steps to reduce vehicle emissions, especially in urban centers, where air quality has become a pressing public health issue. France actively supports the development and implementation of real-world driving emissions (RDE) standards, pushing manufacturers toward more robust aftertreatment systems. Its support for hybrid and electrified vehicle technologies also encourages innovation in systems that function efficiently across diverse powertrains. These factors make France a key market for exhaust aftertreatment solutions.

Italy plays a prominent role in the Europe automotive exhaust aftertreatment systems market, backed by a well-established automotive sector and regulatory commitment to reducing vehicular emissions. Home to major brands like Fiat and Iveco, Italy is influential in both passenger and commercial vehicle segments. The country has implemented strict low-emission zones (LEZs) in major cities, increasing demand for advanced exhaust control technologies, particularly in urban delivery and logistics fleets. Additionally, Italy’s engineering expertise and supplier network contribute significantly to the production of catalytic converters, filters, and related components. This industrial and regulatory alignment positions Italy as a strong regional player in aftertreatment innovation and adoption.

Competitive Landscape:

The competitive landscape of the Europe automotive exhaust aftertreatment systems market is characterized by strong technological innovation, strategic collaborations, and increasing R&D investments. Key players are focusing on developing integrated systems that meet evolving emission standards, particularly under the Euro 6e-bis and upcoming Euro 7 frameworks. The market is also witnessing a shift toward lightweight, durable materials and intelligent emission control solutions compatible with hybrid powertrains. Companies are expanding their presence through partnerships with automakers and component suppliers, while regulatory pressure continues to drive differentiation. The Europe automotive exhaust aftertreatment systems market forecast predicts continued growth, with increasing demand for real-world emissions compliance and sustainable mobility accelerating the adoption of advanced aftertreatment technologies across both passenger and commercial vehicle segments. For instance, in May 2025, Johnson Matthey announced the sale of its Catalyst Technologies business to Honeywell but will retain its automotive catalysts division within its Clean Air segment. This division remains focused on producing catalysts essential for automotive exhaust aftertreatment systems, helping vehicles meet stricter emission standards. The sale allows Johnson Matthey to concentrate on Clean Air and PGM Services while continuing to support emissions reduction technologies in the automotive sector.

The report provides a comprehensive analysis of the competitive landscape in the Europe automotive exhaust aftertreatment systems market with detailed profiles of all major companies.

Latest News and Developments:

- May 2025: Katcon Global and Tata AutoComp formed a joint venture in Monterrey to produce advanced composites for automotive applications. Building on 13 years of collaboration in exhaust systems and emission after-treatment, the venture aims to support North American and European OEMs with lightweight solutions and regulatory compliance.

- December 2024: DEUTZ acquired a 50% stake in HJS Emission Technology, strengthening their long-standing partnership in exhaust aftertreatment. HJS, a leader in high-volume exhaust systems, will enhance DEUTZ’s capabilities in sustainable mobility and emissions reduction.

- October 2024: MAN Engines launched the D3872 engine for workboats, meeting EU Stage V emission standards for inland navigation. The engine features an advanced exhaust gas aftertreatment system, integrating a diesel particulate filter and SCR system. The D3872 will be available in Q3 2025, with plans for further emissions stages.

Europe Automotive Exhaust Aftertreatment Systems Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles |

| Fuel Types Covered | Petrol, Diesel |

| Filter Types Covered | Particulate Matter Control System, Carbon Compounds Control System, Emission Control Using Decision Matrix, NOx Control Systems |

| Countries Covered | Germany, United Kingdom, France, Italy, Russia, Spain, Netherlands, Switzerland, Poland, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe automotive exhaust aftertreatment systems market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe automotive exhaust aftertreatment systems market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe automotive exhaust aftertreatment systems industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Automotive Exhaust Aftertreatment Systems Market Report

The automotive exhaust aftertreatment systems market in Europe was valued at USD 6,452.2 Million in 2025.

The Europe automotive exhaust aftertreatment systems market is projected to exhibit a (CAGR) of 6.04% during 2026-2034, reaching a value of USD 10,940.9 Million by 2034.

The market is primarily driven by stringent emission regulations, rising production of hybrid vehicles, and growing focus on real-world emissions compliance. Additionally, advancements in catalytic converter technologies, increased investment in sustainable vehicle systems, and the adoption of lightweight, durable materials are further accelerating market growth across the region.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade