Europe Breakfast Cereals Market Size, Share, Trends and Forecast by Category, Product Type, Distribution Channel, and Country, 2026-2034

Europe Breakfast Cereals Market Size and Share:

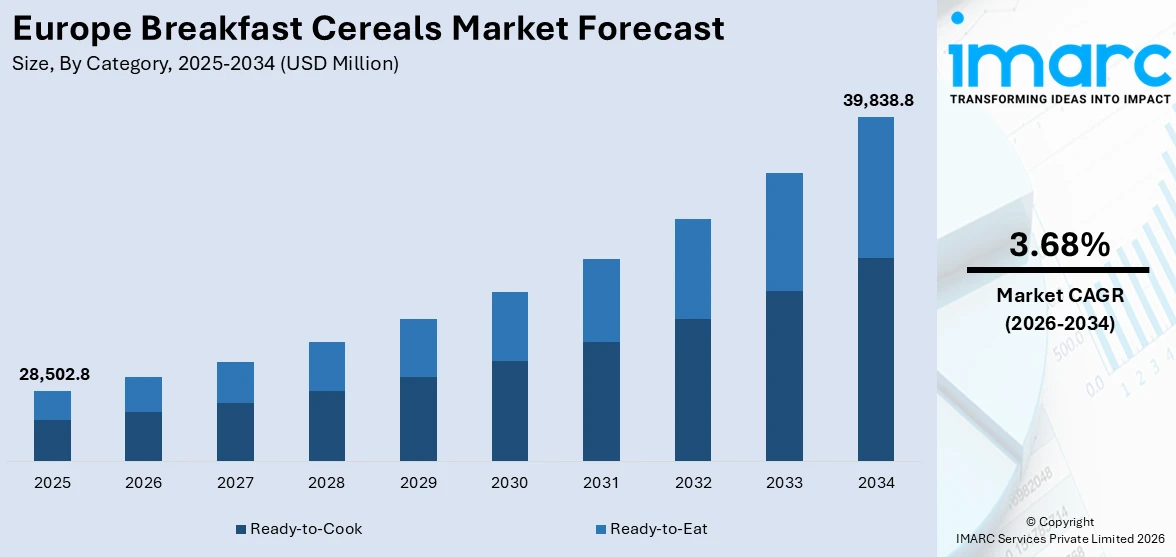

The Europe breakfast cereals market size was valued at USD 28,502.8 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 39,838.8 Million by 2034, exhibiting a CAGR of 3.68% during 2026-2034. The market is influenced by changing consumer preferences toward healthier, convenient, and functional foods and growing consciousness regarding balanced diets, as well as hectic lifestyles. Sustainability trends, such as environment-friendly packaging and ethical sourcing, also shape purchase behavior. Growth in plant-based and gluten-free diets is driving innovation across categories, while retail growth, including online grocery websites, continues to enhance convenience and product transparency. These conditions contribute to the development of the industry and influence competitive tactics among producers competing for a greater Europe breakfast cereals market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 28,502.8 Million |

| Market Forecast in 2034 | USD 39,838.8 Million |

| Market Growth Rate (2026-2034) | 3.68% |

One of the key drivers of the Europe breakfast cereals market is the increasing focus on health and nutrition levels across the continent. Consumers in Europe are increasingly aware of the importance of diet in preventing conditions such as chronic illness and general well-being. Consequently, there is a clear trend away from classic, sugar-rich cereals to those full of fiber, protein, whole grains, and supplementary vitamins. There are robust public health programs in countries like Germany, Sweden, and the Netherlands that encourage equilibrium diets, which have led consumer behavior toward healthier diet options. Breakfast cereals are increasingly being marketed not just as a convenience meal but also as a functional food to promote digestive health, heart health, and weight management. Clean-label and minimally processed options are in great demand, especially in regions that have highly advanced food regulation standards, like Western and Northern Europe. This transformation is urging both established brands and new players to innovate and diversify product portfolios to offer high-nutrition and health-supportive ingredients, which further supports the Europe breakfast cereals market growth.

To get more information on this market Request Sample

The other key driver of the Europe breakfast cereals market is the continent's strong culture of sustainability and ethical consumption. European consumers are concerned with what goes into their food and how they are produced and packaged. Markets like France, Switzerland, and the Nordic countries have strong preferences for cereals that use organic ingredients, fair-trade grains, and recyclable or biodegradable packaging. Brands that can demonstrate transparency in their sourcing and a commitment to reducing their environmental footprint are gaining favor. Furthermore, the fast growth of online shopping for groceries throughout Europe has facilitated the ability of consumers to shop for an extensive variety of specialty cereals, such as gluten-free, plant-based, and environmentally friendly options. Digital platforms also allow ethical, smaller brands to compete better with big companies by reaching targeted audiences and providing subscription services. This technology transition, coupled with awareness on sustainability, is revolutionizing the market dynamics and affecting product innovation as well as distribution strategies.

Europe Breakfast Cereals Market Trends:

Health-Oriented Evolution and Growing Wellness Awareness

Throughout Europe, the market for breakfast cereals is undergoing a remarkable shift as consumers place greater emphasis on health and wellbeing. For example, according to a report by the IMARC Group, the German health and wellness industry as a whole reached USD 171.26 Billion in 2024 and is expected to increase at a compound annual growth rate (CAGR) of 4.28% from 2025 to 2033, reaching USD 260.42 Billion. Conventional sweet cereals are gradually being overtaken by ones that contain whole grains, high fiber content, protein fortification, and few additives. This health-oriented change can be seen in how both long-established brands and newcomers are reformulating or introducing cereals that fit wellness trends. In European markets such as Scandinavia, Germany, and the UK, buyers are increasingly demanding cereals that provide digestive health support, heart health support, and balanced energy. Chia seeds, flaxseeds, and supplementary vitamins are becoming increasingly standard as functional ingredients in day-to-day cereal products. Local food labeling regulations in addition to public health policies within European countries continue to facilitate openness, allowing consumers to make well-informed purchasing decisions. The outcome is a more discerning consumer who prefers cereals as part of an overall healthy lifestyle that is driving the consistent expansion of high-nutrition breakfast foods across the continent and further ensuring a smooth growth trajectory for the Europe breakfast cereals market outlook.

Sustainability and Ethical Sourcing in European Cereal Production

Environmental awareness is a characteristic feature of the European breakfast cereal industry, where consumers are increasingly inclined towards products which are sustainably packaged and ethically sourced. A survey indicates that 58% of Europeans think about the climate impact while making food and drink purchases. This has encouraged companies producing cereals throughout the region to embrace new methods like recyclable packaging, compostable products, and utilizing responsibly sourced grains. Consumers in Western and Northern Europe, where most of the environmentally conscious consumers are found, tend to judge companies on their environmental impact, hence a market where green credentials count as a competitive edge. Sourcing of local ingredients to minimize food miles is also on the rise, particularly in nations such as France, Germany, and the Netherlands. Moreover, organic production techniques and fair-trade processes have become increasingly prevalent due to customer pressure for accountability and transparency. Several breakfast cereal brands are also moving away from plastic packaging toward paper-based packaging, which is aligned with the European Union's regulatory initiative towards greener materials. Overall, sustainability is now a mainstream expectation rather than a niche issue, which determines the Europe breakfast cereals market demand.

Plant‑Based and Gluten‑Free Appeal Driving Portfolio Diversification

Growing demand for plant-based and gluten-free breakfast cereals in Europe is driven by food preferences, changing lifestyles, and growing health consciousness. Consumers are increasingly shunning dairy-based and wheat-based foods and opting instead for those supporting vegan and gluten-free diets. For instance, in France, the retail market for plant-based foods across five categories reached €537 Million in 2024, recording a growth of 8.8% in comparison to 2023 and 20.5% in comparison to 2022, according to the Good Food Institute (GFI). This trend is particularly strong in urban centers, where younger generations are more inclined to follow vegetarian diets. Companies have since brought out cereals that are based on alternative grains such as quinoa, buckwheat, and millet, which not only meet gluten intolerance but also bring nutrient variety. Plant-based slogans now appear on labels commonly, which mirrors the larger market trend towards inclusivity in food options. These breakfast cereals tend to focus on clean labels, being free of artificial ingredients or animal-derived ones. Ethical considerations, food allergy issues, or simply wellness are compelling European consumers to opt for cereal products that are specifically formulated to meet individual dietary requirements—stretching the category far beyond conventional forms.

Europe Breakfast Cereals Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Europe breakfast cereals market, along with forecasts at the regional and country levels from 2026-2034. The market has been categorized based on category, product type, and distribution channel.

Analysis by Category:

- Ready-to-Cook

- Ready-to-Eat

Ready-to-cook cereals in Europe are products such as rolled oats, semolina, and multigrain mixtures that need to be boiled or heat-treated before being ready for consumption. They target health-conscious consumers looking for less processed products. Ready-to-cook cereals are highly demanded for their nutritional content and tend to be selected by those consumers who enjoy a warm, home-like breakfast experience with options on extra added ingredients.

Ready-to-eat cereals dominates the Europe breakfast cereals market trends due to their convenience and minimal preparation. Products like cornflakes, granola, and muesli cater to busy consumers who want a quick yet nutritious meal. These cereals are typically consumed with milk or yogurt and often come enriched with vitamins, minerals, and functional ingredients to support health and wellness goals.

Analysis by Product Type:

Access the comprehensive market breakdown Request Sample

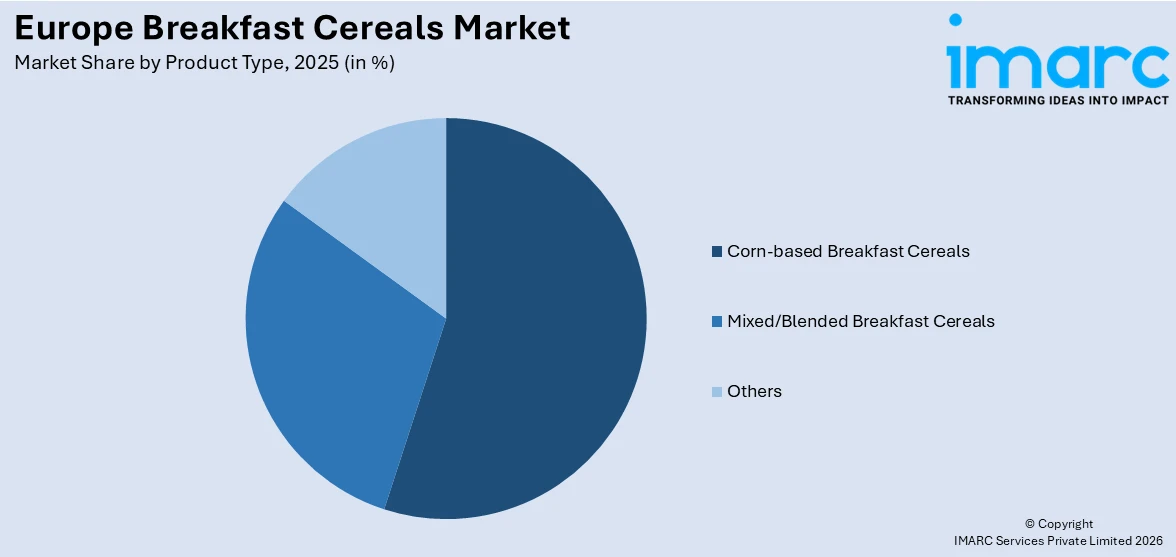

- Corn-based Breakfast Cereals

- Mixed/Blended Breakfast Cereals

- Others

Breakfast cereals made from corn are globally popular throughout Europe for their lightness and speed of preparation. Such common forms are cornflakes and puffed corn, which are usually fortified with basic nutrients. They're enjoyed by a wide majority because of their affordability, minimal flavor, and versatility. They're particularly loved by children and are normally served with milk or fruit.

Mixed or blended breakfast cereals combine various grains such as oats, wheat, barley, and rice, often enriched with nuts, seeds, or dried fruits. This segment appeals to health-conscious consumers seeking variety and balanced nutrition. Muesli and granola are prominent examples in Europe, known for offering fiber, protein, and essential micronutrients in a single, flavorful serving.

Analysis by Distribution Channel:

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Stores

- Others

According to the Europe breakfast cereals market analysis, supermarkets and hypermarkets are the key distribution channels for the industry, providing under one roof a broad assortment of brands and types of products. They have a strong presence, large shelf space, and offer promotional deals, which grab the attention of casual shoppers. These stores offer consumers the convenience of comparing and purchasing premium and low-cost cereals in large quantities.

Specialty stores target niche consumer tastes, commonly targeting organic, gluten-free, or wellness-oriented breakfast cereals. These stores attract consumers who want higher-quality or diet-restricted products not necessarily offered in mass retail. Consumers in Europe are increasingly shopping from specialty retailers for carefully selected, ethically produced, and sustainably packaged cereals consistent with individual values and health aspirations.

Online retailers are fast expanding as a distribution channel in the Europe breakfast cereals market. Convenience, wider choice, and home delivery are attracting tech-savvy and busy consumers. Most brands leverage digital channels to introduce exclusive or tailored cereal variants. Health-oriented e-commerce and subscription models also contribute to growth in this segment.

Analysis by Country:

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Netherlands

- Switzerland

- Poland

- Others

Germany is the leader in health-oriented breakfast cereals, where there is strong demand for organic, whole grain, and low-sugar types. Sustainability and local sourcing are major drivers of consumer choice.

The UK cereal market is mature, with the drivers being convenience, health trends, and plant-based foods. Ready-to-eat cereals are predominant, with increasing demand for gluten-free and fortified foods.

Natural and minimally processed cereals are in favor among French consumers. Organic and muesli products are favorites, demonstrating the nation's focus on clean labels, traditional consumption, and nutritional openness.

Italy's breakfast cereal market is growing due to increasing health consciousness. Although classic breakfasts are common, younger consumers are opening up to cereals, particularly whole grain and functional blends.

Russia has increasing demand for breakfast cereals as a result of urbanization and lifestyle changes. Value-for-money, filling options are in demand, though premium and health-focused cereals are slowly picking up.

Spanish cereal market is influenced by the demand for healthy and convenient food. Ready-to-eat cereals, particularly low-sugar and high-fiber, are becoming increasingly popular among working family households.

The Netherlands prioritizes health and sustainability in the choice of food. Customers tend to prefer cereals that contain plant-based, organic, and environmental-friendly characteristics, indicating the high ethical consumption culture in the country.

Switzerland prefers high-quality, natural cereals. Muesli was developed in Switzerland and continues to be a mainstay, frequently supplemented with nuts, seeds, and organic constituents for extra nutrition.

Poland's market for breakfast cereals is expanding, driven by health trends and urbanization. Demanding but affordable ready-to-eat meals are in vogue, though there's also growing interest in healthy, fiber-containing and locally manufactured cereals.

Competitive Landscape:

Major players according to the Europe breakfast cereal market forecast, are aggressively adopting a variety of strategies to address changing consumer needs and retain competitive edge. One significant area of focus has been reformulation of products to fit health and wellness trends, such as lowering sugar levels, adding fiber, and using functional ingredients like probiotics, vitamins, and vegetable proteins. Food companies are also diversifying their product lines to offer organic, gluten-free, and vegan-friendly foods, addressing consumers with special dietary requirements. Sustainability is a vital area of investment as well, with most top brands shifting toward recyclable or biodegradable packaging and using locally sourced ingredients from certified sustainable farms to help minimize the environmental footprint. To consolidate their market position, brands are boosting digital marketing and increasing distribution channels via e-commerce websites, bringing products within reach of a larger group of consumers. Further, partnerships with health professionals and nutritionists are being employed to speak about scientifically proven advantages of their cereals. Flavor and texture innovation, aligned with European tastes at the regional level, is also assisting brands in standing out in a highly competitive market. These factors together indicate an overall strategy that harmonizes health awareness, environmental friendliness, and consumer participation, each of them all-important drivers in the development of the Europe breakfast cereal market.

Latest News and Developments:

- July 2025: The Ferrero Group, a multinational firm based in Alba, Italy, announced plans for the acquisition of WK Kellogg Co for a total transaction value of USD 3.1 Billion. This acquisition is a part of Ferrero’s ongoing expansion strategy and includes the production, advertising, and distribution of WK Kellogg Co.’s renowned range of breakfast cereals across Canada, the Caribbean, and the United States.

- March 2025: Renowned breakfast cereals manufacturer Kellogg introduced Kellogg’s Town, a novel digital experience that will completely transform how breakfast enthusiasts in Europe engage with one of the most prominent breakfast cereal brands in the world. Launched in 23 markets across Europe in 16 languages, this next-generation experience was created and developed by Merkle in collaboration with Dentsu Creative. It is expected to support the brand's future transformation objectives.

- October 2024: Kellanova announced an investment of USD 98.3 Million to increase manufacturing output at its breakfast cereals factory in Wrexham, North Wales, UK. This will be the company's greatest investment in British cereal manufacturing in more than 30 years. Through this expansion, the existing yearly output at the Wrexham factory is expected to more than double to approximately 1.5 million boxes of cereal per day, making it the largest cereal production facility in Europe.

- September 2024: Switzerland-based Nestle announced the launch of a new fruit-shaped and fruit-flavored breakfast cereal in Romania, the Trix cereal. Manufactured using whole grains, calcium, B group vitamins, and iron, the Trix cereal is available in a variety of flavors, including orange, grape, lemon, raspberry, and watermelon.

Europe Breakfast Cereals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Categories Covered | Ready-to-Cook, Ready-to-Eat |

| Product Types Covered | Corn-based Breakfast Cereals, Mixed/Blended Breakfast Cereals, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| Countries Covered | Germany, United Kingdom, France, Italy, Russia, Spain, Netherlands, Switzerland, Poland, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe breakfast cereals market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe breakfast cereals market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the breakfast cereals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Breakfast Cereals Market Report

The breakfast cereals market in Europe was valued at USD 28,502.8 Million in 2025.

The Europe breakfast cereals market is projected to exhibit a CAGR of 3.68% during 2026-2034, reaching a value of USD 39,838.8 Million by 2034.

The European breakfast cereals market is driven by busy lifestyles that demand convenient, nutritious options. Increasing health consciousness fuels demand for high-fiber, low-sugar, and plant-based varieties. Product innovation, including organic and gluten-free choices, coupled with expanding e-commerce accessibility, further propels market growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)