Europe Business Travel Market Size, Share, Trends and Forecast by Type, Purpose Type, Expenditure, Age Group, Service Type, Travel Type, End User, and Country 2026-2034

Europe Business Travel Market Size, Share, Trends & Forecast (2026-2034)

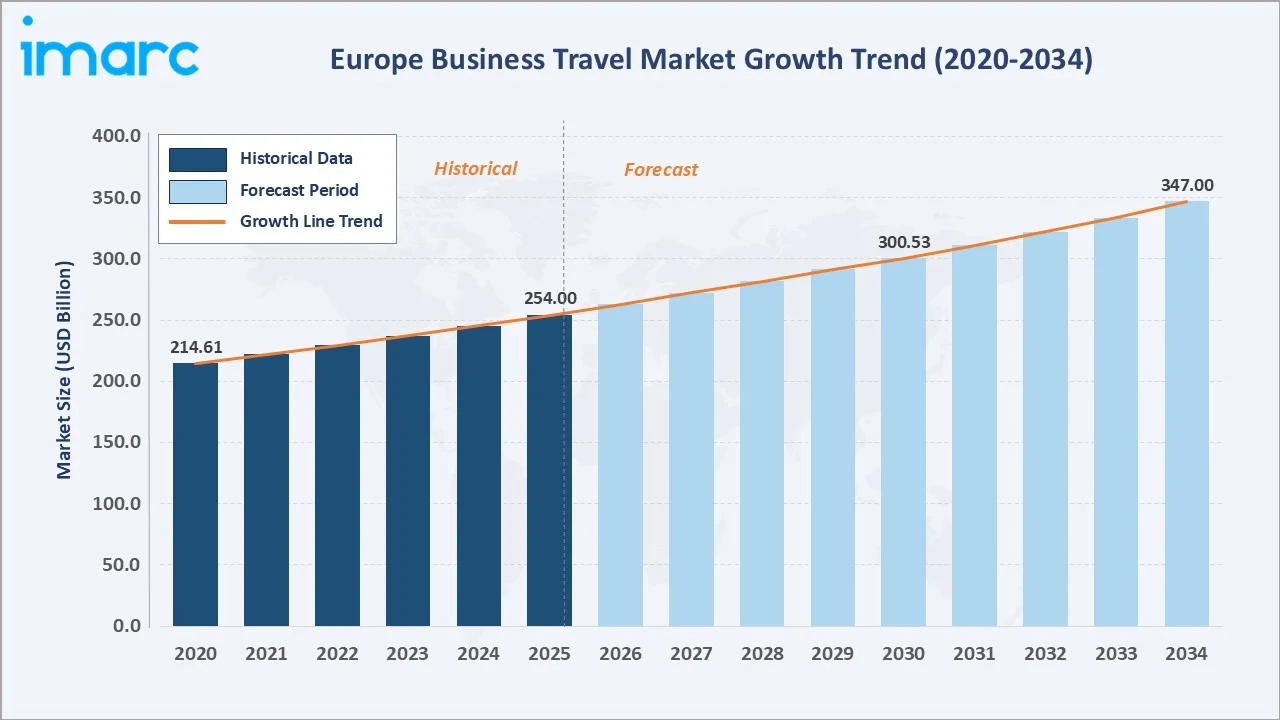

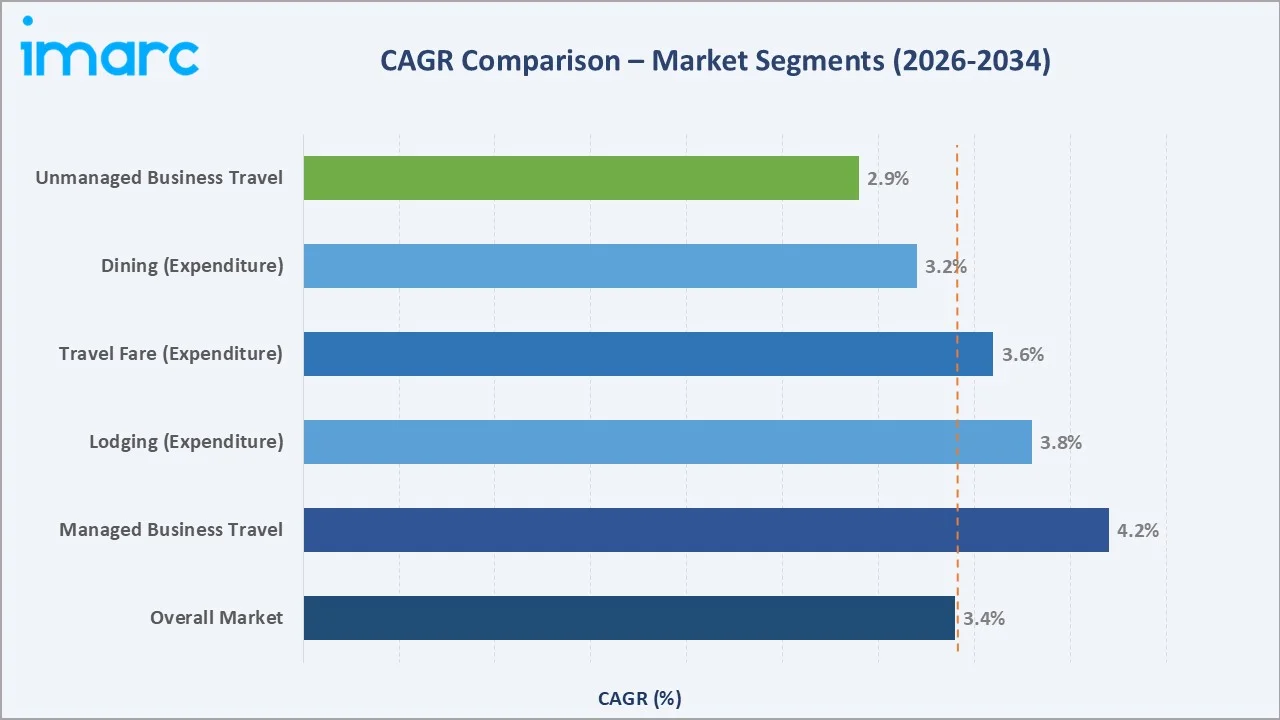

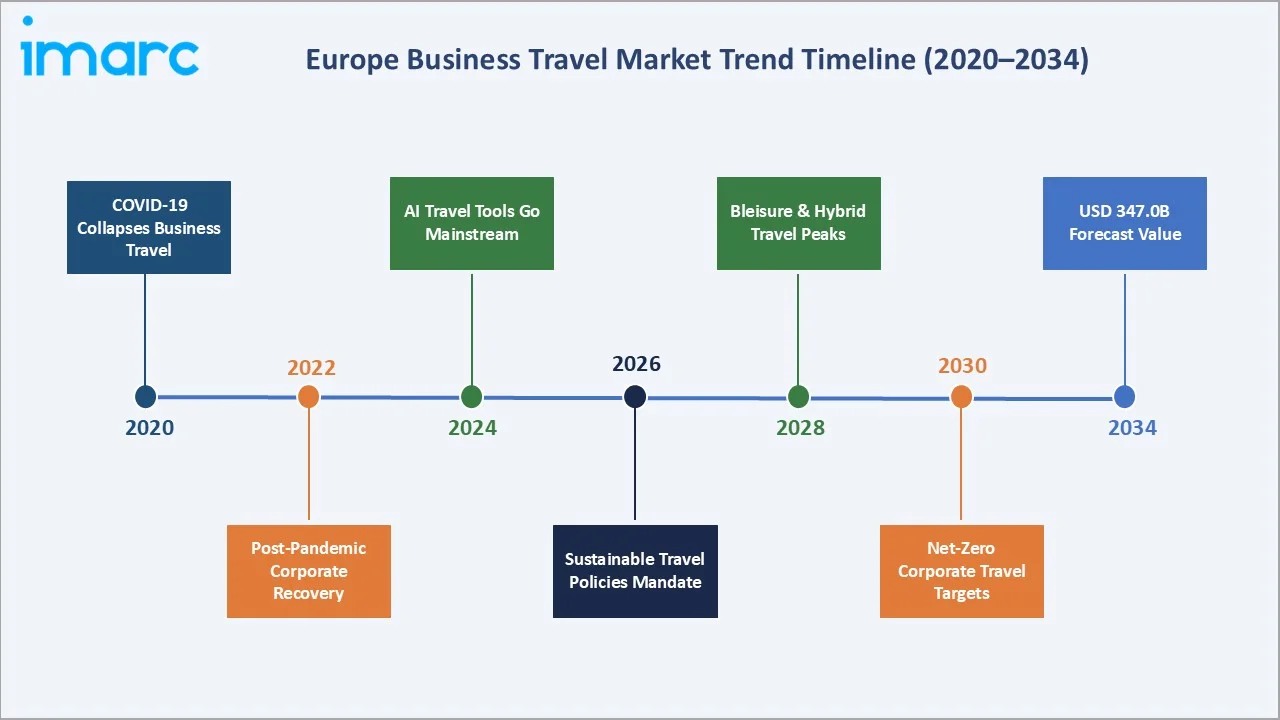

The Europe business travel market reached USD 254.00 Billion in 2025 and is projected to reach USD 347.00 Billion by 2034, growing at a CAGR of 3.42% during 2026-2034. The market is rebounding strongly, driven by resumed corporate meetings, cross-border trade events, and expanding international partnerships. Rising demand for flexible booking systems, AI-powered travel management tools, and sustainable travel options is shaping Europe business travel market growth across all key sub-segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 254.00 Billion |

|

Forecast Market Size (2034) |

USD 347.00 Billion |

|

CAGR (2026-2034) |

3.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (24.8% share, 2025) |

|

Fastest Growing Country |

Spain |

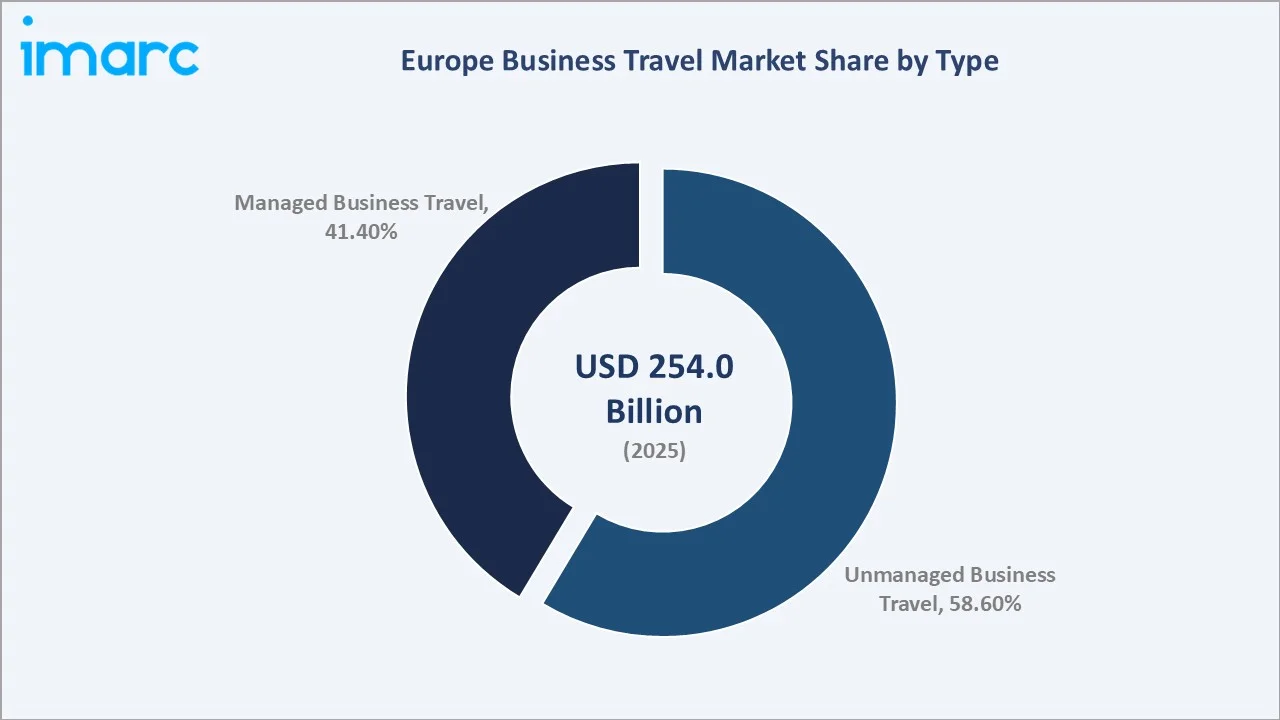

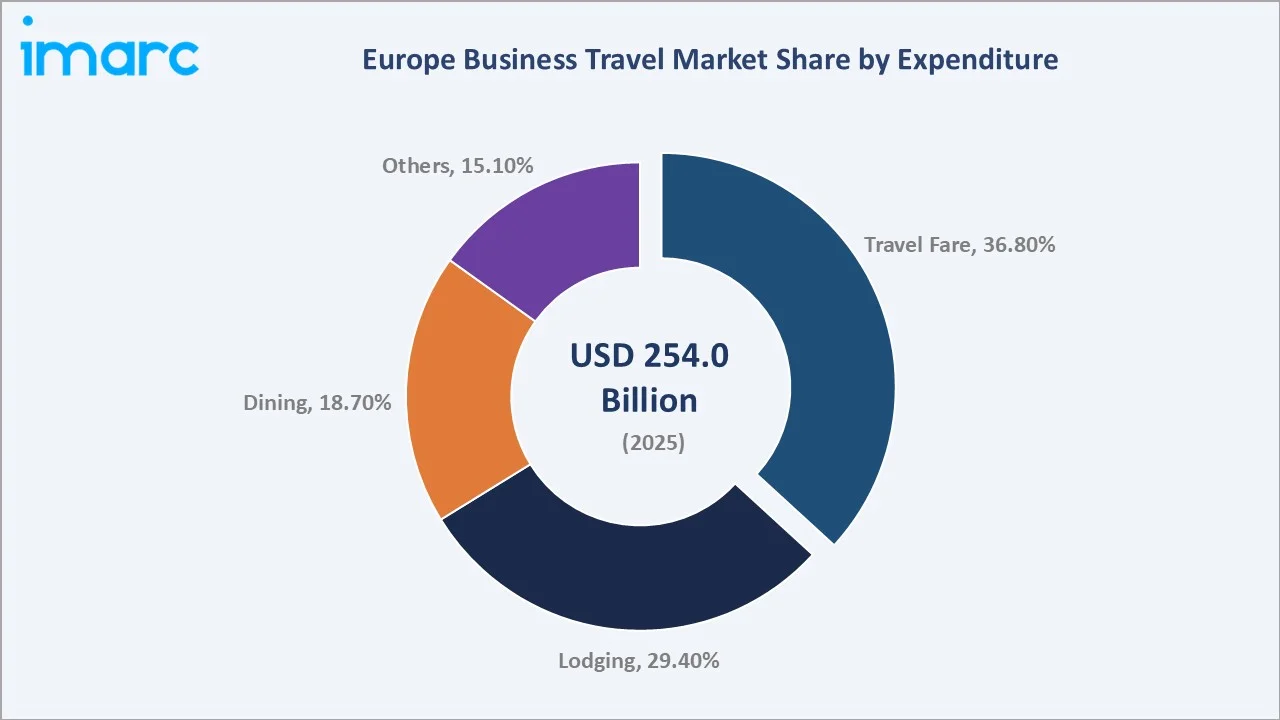

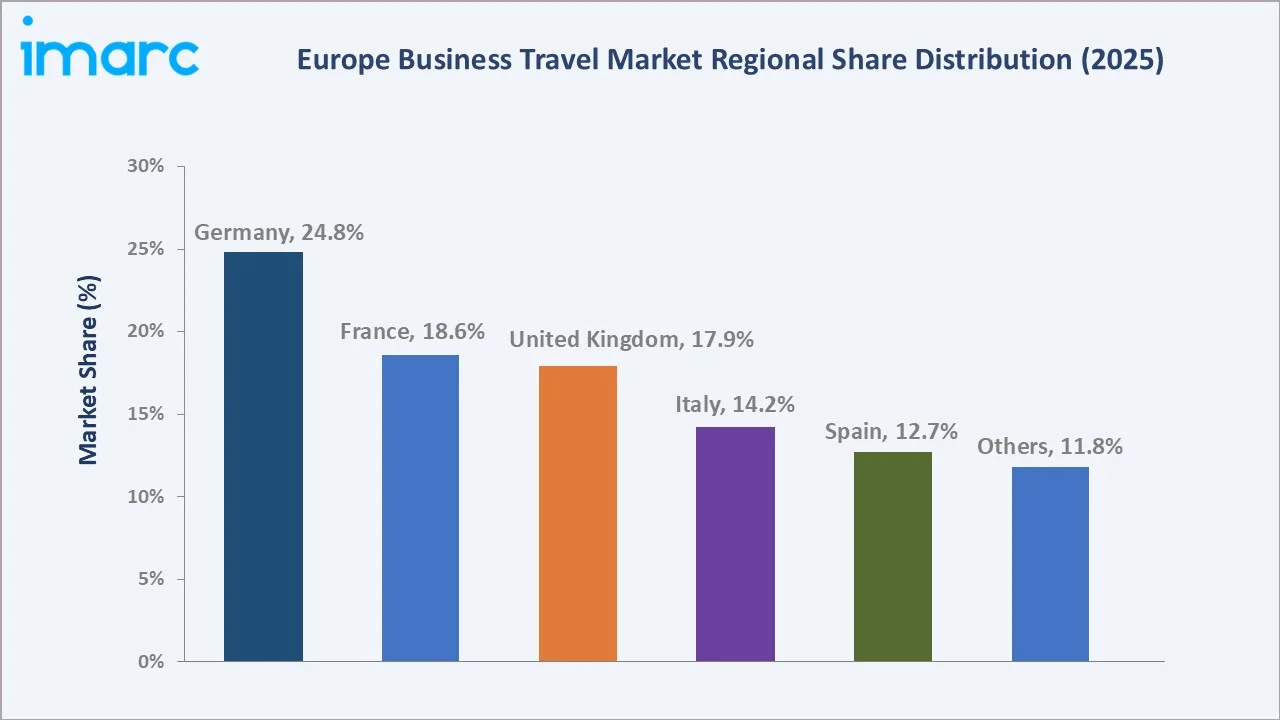

Germany dominates, holding a 24.8% country share in 2025, while unmanaged business travel leads at 58.6% of the type segment. Travel fare remains the largest expenditure category at 36.8%. Europe's business travel market benefits from its robust corporate ecosystem, deep intra-regional trade connections, and accelerating investment in digital travel management infrastructure across key economies, including France, the UK, and Italy.

To get more information on this market, Request Sample

With travel demand spanning corporate meetings, trade shows, product launches, and internal collaboration events, the Europe business travel market outlook remains robust through the forecast period, supported by AI-driven booking platforms, the rise of B-leisure travel, and the growing integration of sustainability requirements into corporate travel policies across the region.

Executive Summary

The Europe business travel market is on a steady recovery and expansion path, reaching USD 254.00 Billion in 2025 and projected to grow to USD 347.00 Billion by 2034 at a CAGR of 3.42%. This trajectory reflects Europe's resilient corporate travel ecosystem, driven by improving macroeconomic conditions, the resumption of in-person corporate engagements, cross-border trade activity, and the expanding digital infrastructure supporting seamless business travel management across the continent.

Germany leads with a 24.8% share of the European business travel market in 2025, anchored by its dominant manufacturing, automotive, and financial services sectors that generate high volumes of domestic and international corporate travel. France and the United Kingdom follow with 18.6% and 17.9% shares, respectively, supported by strong financial services and professional services industries.

Travel fare constitutes the largest expenditure category at 36.8%, followed by lodging at 29.4%, as inflationary pressures on short-haul airfares and premium hotel rates continue. AI-driven travel management systems, sustainable travel mandates, and the rise of B-leisure travel are the defining Europe business travel market trends shaping investment and operational strategies of leading travel management companies through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Unmanaged Business Travel – 58.6% share (2025) |

|

Largest Expenditure Category |

Travel Fare – 36.8% share (2025) |

|

Leading Country |

Germany – 24.8% revenue share (2025) |

|

Fastest Growing Country |

Spain (tourism infrastructure + corporate expansion) |

|

Top Companies |

American Express Global Business Travel, BCD Travel, Flight Centre Travel Group Limited, Navan, Perk, |

|

Market Opportunity |

AI-powered travel management and sustainable corporate travel platforms are poised for high growth through 2034 |

Key Analytical Observations Supporting The Above Data:

- Unmanaged business travel dominates at 58.6% (2025), driven by the high proportion of SMEs in Europe that rely on individual employee self-booking via online travel agencies and direct airline or hotel channels without centralized policy oversight.

- Travel fare holds the largest expenditure share at 36.8% in 2025, as rising short-haul airfare pricing, premium cabin upgrades, and limited carrier competition on key intra-European routes continue to push corporate air spend upward.

- Germany accounts for 24.8% of European corporate travel spending in 2025, anchored by its global export-driven manufacturing base, dense network of international trade fairs (Hannover Messe, Frankfurt IAA), and headquarters concentration of DAX-listed multinationals.

- Managed business travel at 41.4% is growing faster than the unmanaged segment, as large enterprises invest in centralized travel management platforms to improve data visibility, cost control, duty of care compliance, and carbon footprint tracking.

- AI-enhanced travel management tools are reshaping the market, with systems offering dynamic pricing insights, automated rebooking, and predictive travel disruption alerts increasingly adopted by mid-to-large corporate travel programs across Europe.

Europe Business Travel Market Overview

Europe's business travel market encompasses a broad spectrum of corporate mobility services, including airline and rail ticketing, hotel and serviced apartment accommodation, ground transportation, meeting and conference facilities, and supporting travel management software. The market ecosystem integrates travel management companies (TMCs), online booking tools, global distribution systems (GDS), corporate credit card providers, expense management platforms, and sustainability compliance services.

Macroeconomic factors, including post-pandemic corporate investment recovery, the expansion of cross-border EU trade and financial services, and the return of large-scale industry trade fairs and conferences, are the primary growth catalysts for the Europe business travel market forecast through 2034. The European Commission's push for digitalized cross-border business services and streamlined Schengen Area business visa processes is further lowering structural barriers to intra-regional corporate travel activity.

Market Dynamics

To evaluate market opportunities, Request Sample

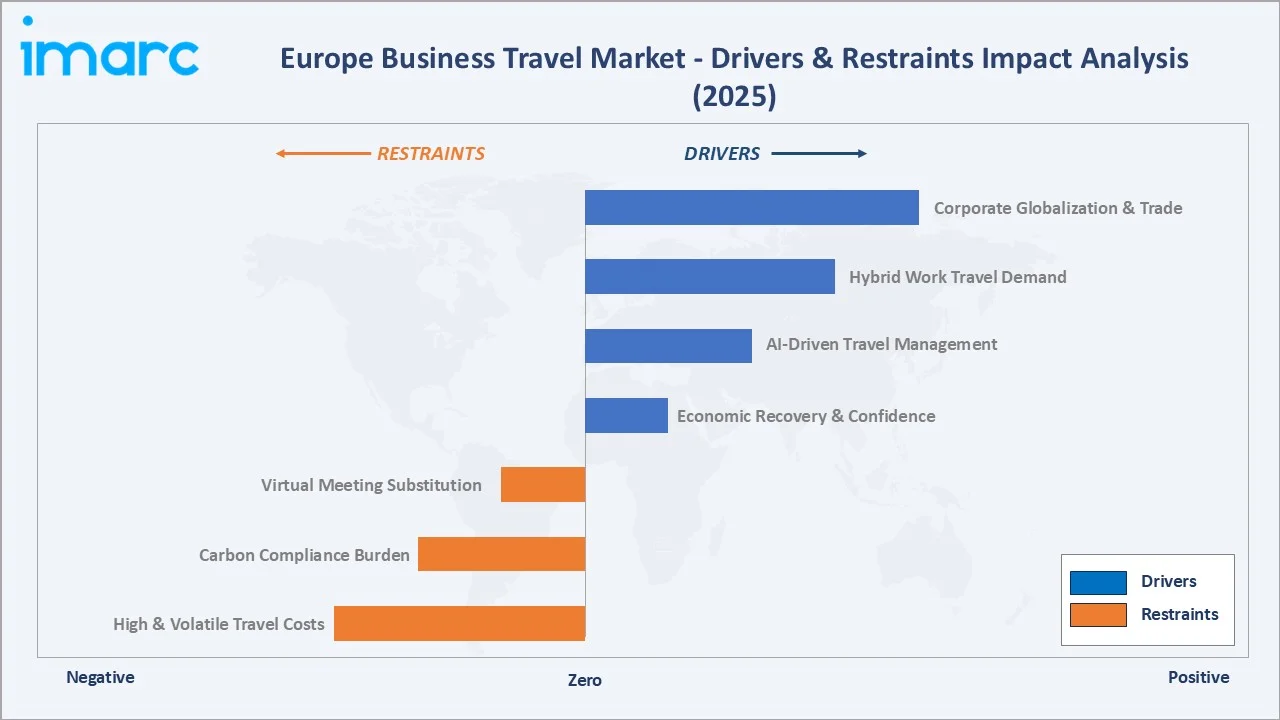

Market Drivers

- Corporate Globalization and Cross-Border Trade Expansion: Fast-paced globalization has substantially increased business activities across European industry verticals, including automotive, financial services, healthcare, pharmaceuticals, and manufacturing.

- Improving Economic Conditions and Corporate Confidence: The improving economic environment across major European economies is increasing corporate travel budgets and reinstating travel programs that were curtailed during the pandemic years.

- Growth of Hybrid Work Travel Models: Employees now combine office visits with remote work periods, fueling shorter and more frequent travel for team collaboration, client-facing engagements, and strategic offsite meetings that cannot be replicated virtually.

- Rise of AI-Driven Travel Management Systems: AI tools offer personalized itineraries, dynamic pricing insights, automated approval workflows, and real-time disruption alerts, significantly enhancing the efficiency of corporate travel programs.

These drivers reinforce a self-sustaining growth cycle, improving corporate profitability, increasing travel budgets, and technology adoption reduces per-trip management costs, enabling broader travel program deployment, while hybrid work norms institutionalize business travel as a strategic productivity tool rather than a discretionary expense across European enterprises.

Market Restraints

- High and Volatile Travel Costs: Consolidation, reducing competitive pressure among carriers, combined with fuel-cost inflation, has created significant upward pressure on travel fare budgets, constraining program expansion, particularly for cost-sensitive SME travelers.

- Carbon Regulation and Sustainability Mandates: The EU's Corporate Sustainability Reporting Directive (CSRD) and Scope 3 emissions reporting obligations are placing new cost burdens and policy complexity on corporate travel programs.

- Virtual Meeting Substitution: The proven efficiency of video conferencing platforms for routine meetings and internal coordination has permanently reduced the volume of lower-value business trips.

Market Opportunities

- Sustainable Business Travel Solutions: In June 2025, Thrust Carbon introduced the NetZero Forecaster tool to help businesses model carbon reduction strategies, reflecting the accelerating commercialization of sustainability-as-a-service for corporate travel.

- B-leisure and Experience-Enriched Corporate Travel: The blending of business and leisure travel is creating new revenue opportunities. This trend is particularly strong among under-40 business travelers, who represent a growing segment of European corporate travel volumes.

- SME Travel Management Digitization: The large and underserved SME segment in Europe represents a major growth opportunity for cloud-based, subscription-priced travel management platforms. Companies like Perk and Navan are targeting this segment with self-service tools, real-time support, and integrated expense management at price points accessible to smaller businesses.

Market Challenges

- Duty of Care and Traveler Safety Complexity: Rising geopolitical instability across parts of Europe and neighboring regions, combined with increased frequency of industrial actions affecting air and rail transport, is raising the complexity and cost of corporate duty of care programs.

- Data Privacy and Cross-Border Compliance: Managing traveler personal data across multiple countries under GDPR and local data protection regulations creates legal and operational complexity for TMCs and corporate travel departments.

Emerging Market Trends

1. Growth of Hybrid Work Travel

Employees now travel with greater strategic purpose, prioritizing team collaboration sessions, client relationship meetings, and in-person negotiations over routine internal commutes. Travel policies are adapting accordingly, incorporating real-time approval workflows, flexible cancellation provisions, and integration with digital workplace calendars.

2. Rise of AI-Driven Travel Management

Corporate travel managers are leveraging AI dashboards to optimize supplier negotiations, identify cost-saving opportunities, and track carbon emissions in real time. The accelerating adoption of AI is raising service quality expectations from TMCs and accelerating competitive differentiation among platform-based travel management solution providers across the continent.

3. Sustainable and Low-Carbon Corporate Travel

Rail-first policies replacing short-haul flights are gaining traction in markets including France, Germany, and the Netherlands, where high-speed rail networks offer competitive journey times on key inter-city routes. Airlines are expanding SAF blending mandates and carbon-neutral flight options for corporate clients, while hotel chains are extending green certification programs and carbon measurement APIs to corporate booking platforms.

4. B-leisure Travel and Extended Business Trips

Professionals under 40 are increasingly extending business trips by one to three days to incorporate leisure activities, cultural experiences, or personal wellness. This trend creates incremental spending opportunities for hotels, restaurant operators, and destination experiences in business travel hub cities such as Paris, Amsterdam, Madrid, and Milan.

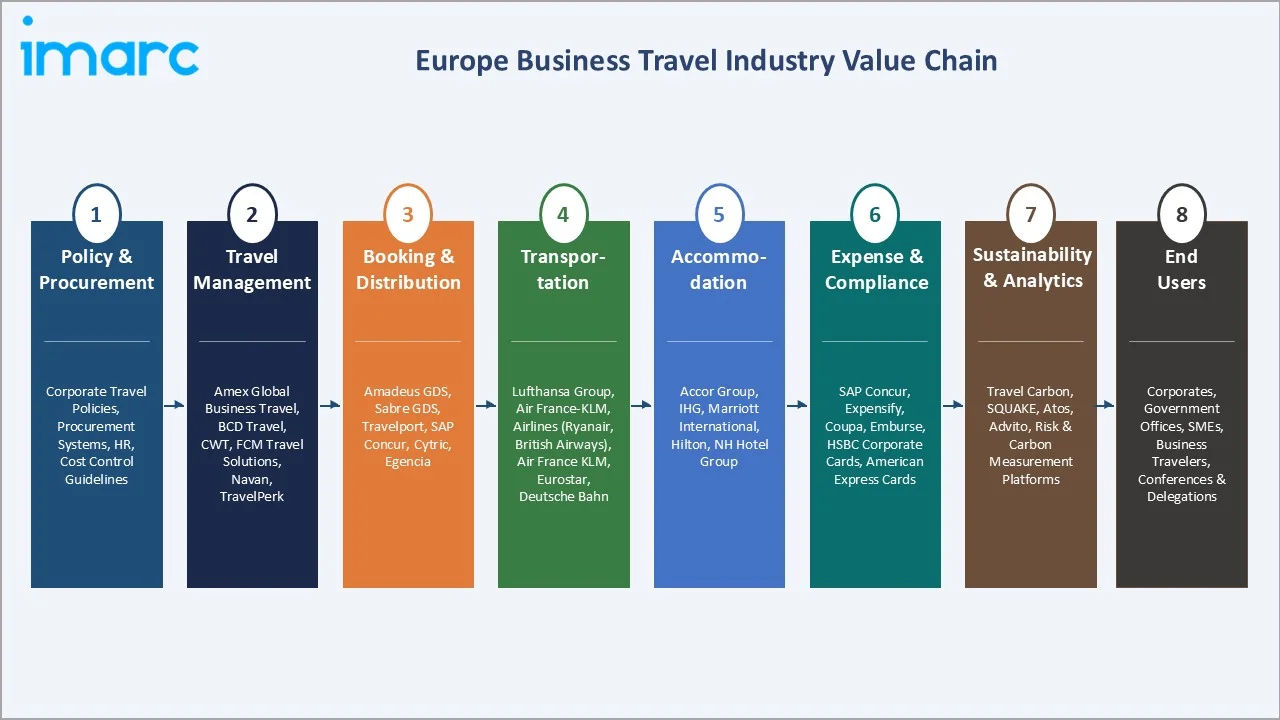

Industry Value Chain Analysis

|

Stage |

Key Participants / Examples |

|

Policy & Procurement |

Corporate travel managers, procurement departments, HR, and C-suite travel policy owners |

|

Travel Management |

American Express Global Business Travel, BCD Travel, Flight Centre Travel Group Limited, Navan, Perk |

|

Booking & Distribution |

Amadeus GDS, Sabre GDS, Travelport, online booking tools (SAP Concur and Cytric) |

|

Transportation |

Lufthansa Group, IAG (British Airways, Iberia), Air France-KLM, Eurostar, Deutsche Bahn |

|

Accommodation |

Accor Group, IHG, Marriott International, Hilton, and serviced apartment operators |

|

Expense & Compliance |

SAP Concur, Expensify, HSBC Commercial Cards, American Express corporate cards |

|

Sustainability & Analytics |

Thrust Carbon, SQUAKE – carbon measurement and offset platforms |

|

End Users |

Corporate employees, government officials, SME business owners, conference and trade show delegates |

Technology Landscape in the Europe Business Travel Industry

AI and Machine Learning in Travel Management

Chatbot-assisted booking and 24/7 virtual travel agent support are reducing administrative burden on corporate travel teams while improving employee experience. Major TMCs, including American Express Global Business Travel and BCD Travel, have made substantial investments in proprietary AI platforms, widening the capability gap between technology-forward leaders and traditional agency models.

Global Distribution Systems and NDC Adoption

The adoption of IATA's New Distribution Capability (NDC) standard is accelerating across European corporate travel channels, enabling airlines to distribute richer, personalized fare content directly through booking platforms without traditional GDS intermediation. NDC adoption is reshaping the commercial relationships between airlines, TMCs, and corporate buyers, as airlines use direct channels to offer ancillary services, dynamic pricing, and loyalty-linked upgrades not available through legacy GDS infrastructure.

Carbon Tracking and Sustainability Technology

Purpose-built carbon tracking platforms are becoming standard integrations within corporate travel management systems across Europe. Tools such as Thrust Carbon's NetZero Forecaster, launched in June 2025, enable businesses to model carbon reduction strategies by simulating transport mode shifts, cabin class adjustments, and route optimizations.

Mobile-First and Contactless Travel Technology

Corporate travelers increasingly expect seamless mobile-first experiences for every stage of the travel journey, from booking and boarding pass management to hotel check-in, expense capture, and real-time itinerary updates. NFC-enabled contactless check-in, biometric airport processing, and eSIM connectivity services are being integrated into TMC mobile apps, elevating traveler autonomy and reducing friction across the travel experience.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Unmanaged Business Travel |

58.6% |

2025 |

|

Purpose Type |

Marketing |

🔒 |

2025 |

|

Expenditure |

Travel Fare |

36.8% |

2025 |

|

Age Group |

Travelers Below 40 Years |

🔒 |

2025 |

| Service Type | Food and Lodging | 🔒 | 2025 |

| Travel Type | Group Travel | 🔒 | 2025 |

| End User | Corporate | 🔒 | 2025 |

|

Country |

Germany |

24.8% |

2025 |

By Type

The unmanaged business travel segment dominates the European business travel market with a 58.6% share in 2025, reflecting the large proportion of European SMEs and individual employees who arrange travel independently through online travel agencies, direct airline websites, and hotel booking platforms without centralized corporate travel policy oversight.

To access detailed market analysis, Request Sample

The managed business travel segment at 41.4% (approximately USD 105.2 Billion in 2025) is the fastest-growing category, as large multinational corporations invest in centralized travel programs to improve cost visibility, enforce negotiated supplier rates, and meet increasingly stringent duty of care and carbon reporting obligations. Managed programs typically leverage preferred supplier agreements with airlines, hotel chains, and ground transportation providers to achieve average cost savings of 15–25% relative to unmanaged equivalent spend.

By Expenditure

The travel fare category holds the largest expenditure share at 36.8% in 2025 (approximately USD 93.5 Billion), driven by rising short-haul airfare pricing, business class upgrades, and the expansion of intercontinental routes serving European business hubs. With demand recovery exceeding airline capacity additions on major intra-European routes, yield management pressures have kept corporate airfare benchmarks significantly above pre-pandemic levels.

The lodging category accounts for 29.4% of expenditure (approximately USD 74.7 billion in 2025), driven by strong hotel rate inflation in key European business cities. The dining category represents 18.7% (approximately USD 47.5 billion). The high and rising cost of accommodation in cities such as London, Paris, Zurich, and Amsterdam continues to push lodging's share of total corporate travel spend upward, prompting corporate travel programs to negotiate extended-stay and serviced apartment rates as cost-containment strategies.

Regional Market Insights

Germany's market leadership (24.8%, 2025) reflects its position as Europe's largest economy and its unrivaled density of global trade fair events, including Hannover Messe, Frankfurt IAA, and Bauma Munich, which collectively generate millions of inbound and outbound business travel days annually.

|

Country |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

Germany |

24.8% |

Trade fairs; automotive sector; DAX multinationals; manufacturing hub |

EU CSRD reporting; GDPR compliance |

|

France |

18.6% |

Financial services; luxury goods; Paris business hub; EU institutions |

French climate transport law; CSRD |

|

United Kingdom |

17.9% |

Financial services; professional services; London global hub |

UK Sustainable Aviation commitment; ICO |

|

Italy |

14.2% |

Manufacturing SMEs, fashion & luxury, Rome and Milan corporate activity |

EU Green Deal; Italian GDPR enforcement |

|

Spain |

12.7% |

Tourism & hospitality sector; Iberia peninsula trade; Barcelona tech hub |

CSRD; Spanish DPA regulations |

|

Others |

11.8% |

Netherlands MICE hub; Benelux financial centers; Nordics sustainability leaders |

Varies by country; EU framework |

Spain is emerging as the fastest-growing country market in the Europe business travel segment, driven by its expanding Barcelona technology ecosystem, growing MICE (meetings, incentives, conferences, and exhibitions) sector in Madrid, and the increasing international corporate footprint of Spanish multinationals.

Competitive Landscape

The Europe business travel market exhibits a moderately concentrated structure at the TMC tier, with global leaders commanding significant shares of managed corporate travel programs while regional specialists and technology-first disruptors compete aggressively in the SME and tech-sector segments. The top three TMCs, American Express Global Business Travel, BCD Travel, and Flight Centre Travel Group Limited, collectively held an estimated total European sales exceeding EUR 20.62 billion in 2024, according to BTN Europe's Leading TMCs report.

|

Company Name |

Brand/Product Name |

Market Position |

Core Strength |

|

American Express Global Business Travel |

Amex GBT |

Market Leader |

EUR 10.21B European sales (2024); end-to-end managed travel |

|

BCD Travel |

BCD Travel / TripSource |

Market Leader |

EUR 6.41B European sales; AI-driven TripSource platform; Airbus partnership (France, Germany, Spain, UK) |

|

Flight Centre Travel Group Limited |

FCM Travel |

Strong Challenger |

EUR 3.1B European sales; FCM AI Centre of Excellence; global enterprise focus |

|

Navan |

Navan |

Challenger |

EUR 2.82B European sales; SME and tech-sector focus; all-in-one platform |

|

Perk |

Perk |

Niche Player |

SME specialist; flexible cancellation (FlexiPerk); rapid European expansion |

Key Company Profiles

American Express Global Business Travel

American Express Global Business Travel is Europe's largest travel management company by revenue, with total European sales of EUR 10.21 billion in 2024. Headquartered in New York with operational headquarters in London, the company provides comprehensive travel management, expense, and meetings solutions to global enterprises. In February 2025, the company signed an NDC (New Distribution Capability) content expansion deal, covering access to NDC-only fares, special promotions, and improved digital booking across Lufthansa Group airlines.

- Product Portfolio: Neo (enterprise) and Neo1 (SME) travel management platforms; meetings and events management; data and analytics; consulting services.

- Recent Developments: Acquired CWT (Carlson Wagonlit Travel) in September 2025; continued rollout of AI-powered booking and disruption management tools across European markets.

- Strategic Focus: Market consolidation, AI platform investment, sustainability solution expansion, and SME segment penetration through digital channels.

BCD Travel

BCD Travel, headquartered in Utrecht, Netherlands, is Europe's second-largest TMC with €6.41 billion in European sales in 2024. The company specializes in providing technology-enriched travel management solutions tailored to multinational corporations.

- Product Portfolio: TripSource travel platform, DecisionSource analytics, Meetings & Events management, sustainable travel reporting tools.

- Recent Developments: Established BCD Travel partnership with Airbus in 2022, serving France, Germany, Spain, and the UK; continued expansion of sustainability measurement and reporting capabilities.

- Strategic Focus: Sustainability leadership, AI-driven platform enhancement, and enterprise travel program optimization across key European markets.

Perk

Perk, dual headquarters in Boston and London, is one of Europe's fastest-growing business travel platforms, targeting the underserved SME and technology company segment. The company's all-in-one platform combines real-time booking, expense management, and FlexiPerk flexible cancellation, addressing the corporate travel needs of Europe's large and growing technology startup and scale-up ecosystem.

- Product Portfolio: Perk Travel, Perk Expense, Perk Pay.

- Recent Developments: Rapid European market expansion across the UK, Germany, France, and Benelux; deepened integration with HR and ERP platforms popular among European SMEs.

- Strategic Focus: SME market penetration, platform ecosystem expansion, and sustainability tool integration to meet growing corporate ESG travel reporting requirements.

Market Concentration Analysis

The Europe business travel market exhibits moderate-to-high concentration at the TMC and large enterprise tier, with the top three providers – American Express Global Business Travel, BCD Travel, and Flight Centre Travel Group Limited– collectively generating well over EUR 20 billion in European sales annually as of 2024.

However, the large and fragmented SME segment, which accounts for a significant share of total unmanaged business travel, remains largely contested by technology-first platforms, online booking tools, and regional specialist agencies, ensuring a competitive mid-market below the top TMC tier.

Consolidation is accelerating. American Express Global Business Travel completed its acquisition of CWT on September 2, 2025, in a deal valued at approximately USD 540 million, bringing together two major global travel management companies after regulatory approvals.

Private equity and strategic investor interest in technology-enabled TMC platforms remains elevated, with particular attention on sustainability-integrated travel management tools, AI booking platforms, and SME-focused self-service corporate travel solutions.

Investment & Growth Opportunities

Fastest Growing Segments

AI-powered travel management platforms, sustainable corporate travel compliance solutions, and SME self-service booking tools represent the three highest-growth investment vectors within the Europe business travel market through 2034. Together, these sub-categories are growing materially faster than the overall market CAGR of 3.42%, driven by structural corporate digitization, regulatory compliance demand, and the large addressable SME travel management opportunity across Europe.

Emerging Sub-Market Expansion

Central and Eastern European corporate travel markets in Poland, the Czech Republic, and Romania represent high-growth frontiers as multinational manufacturing and technology companies expand regional operations. MICE infrastructure investment in cities including Warsaw, Prague, and Bucharest is generating incremental demand for managed corporate travel services beyond traditional Western European corridors.

Venture and Institutional Investment Themes

- Key investment themes include AI-native travel booking platforms, carbon tracking and Scope 3 compliance tools for CSRD reporting, and multi-currency expense management solutions for cross-border European corporate travel.

- Institutional investors and PE funds are targeting TMC platform consolidation plays, vertical integration between travel management, expense, and HR software, and sustainability-as-a-service subscription models for corporate travel programs.

- Corporate venture arms of airlines and hotel groups are investing in distribution technology and direct booking platforms to reduce GDS dependency and build direct corporate client relationships.

Future Market Outlook (2026-2034)

The Europe business travel market is positioned for steady, broad-based growth through 2034. From a base of USD 254.00 Billion in 2025, the market is projected to reach USD 347.00 Billion by 2034, representing total incremental value creation of USD 93.0 Billion over the forecast decade. This growth will be driven by the structural recovery of intra-European corporate mobility, accelerating AI adoption across travel management, and the growing formalization of sustainability requirements within corporate travel policy frameworks.

The EU's CSRD Scope 3 emissions reporting mandates, evolving GDPR enforcement across cross-border data practices, and national-level sustainable transport regulations will drive material investment in compliance-integrated travel management solutions. TMCs that offer seamlessly integrated carbon measurement, real-time policy enforcement, and ESG reporting dashboards will command premium pricing and stronger enterprise client retention.

Long-term, the Europe business travel market forecast trajectory is tied to three structural macro-themes: the sustained deepening of European corporate globalization driving in-person engagement needs, the technology transformation of travel management creating platform-based competitive advantages, and the regulatory-driven sustainability mandate reshaping procurement standards across the entire business travel supply chain through 2034 and beyond.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and consultations with over 100 industry participants in 2024–2025, including corporate travel managers, TMC executives, airline and hotel distribution specialists, technology platform providers, sustainability consultants, and procurement officers across Germany, France, the UK, Italy, and Spain.

Secondary Research

Secondary research encompassed a systematic review of TMC annual reports, EU regulatory publications, IATA and UNWTO industry data, BTN Europe's Leading TMCs report, European Commission trade data, and travel technology platform disclosures. Over 180 secondary sources were reviewed and triangulated to ensure analytical accuracy and data integrity across all market segments and country-level analyses.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, corporate travel program data, airline and hotel revenue trends, and historical expenditure evolution. A base-case CAGR of 3.42% reflects consensus analyst estimates validated against reported TMC revenue trajectories and European corporate travel spend surveys from 2020 through 2025.

Europe Business Travel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Managed Business Travel, Unmanaged Business Travel |

| Purpose Types Covered | Marketing, Internal Meetings, Trade Shows, Product Launch, Others |

| Expenditures Covered | Travel Fare, Lodging, Dining, Others |

| Age Groups Covered | Travelers Below 40 Years, Travelers Above 40 Years |

| Service Types Covered | Transportation, Food and Lodging, Recreational Activities, Others |

| Travel Types Covered | Group Travel, Solo Travel |

| End Users Covered | Government, Corporate, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | American Express Global Business Travel, BCD Travel, Flight Centre Travel Group Limited, Navan, Perk, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Business Travel Market Report

The Europe business travel market reached USD 254.00 Billion in 2025 and is projected to reach USD 347.00 Billion by 2034, growing at a CAGR of 3.42% during the forecast period.

The Europe business travel market is expected to grow at a CAGR of 3.42% during 2026-2034, supported by corporate globalization, economic recovery, hybrid work travel demand, and AI-driven travel management adoption across the region.

Germany leads the market with a 24.8% revenue share in 2025, driven by its position as Europe's largest economy, its dense network of global trade fairs and manufacturing sector activity, and the high concentration of DAX-listed multinational corporations generating substantial domestic and international corporate travel volumes.

Unmanaged business travel dominates with a 58.6% share in 2025, valued at approximately USD 148.8 Billion. Its dominance reflects the large proportion of European SMEs and individual travelers who book independently through online channels without centralized corporate policy oversight.

Travel fare commands the largest expenditure share at 36.8% in 2025, driven by elevated short-haul airfare pricing on key intra-European routes, limited competitive pressure from carrier consolidation, and the structural recovery of intercontinental business aviation demand serving European hub airports.

Key players include American Express Global Business Travel, BCD Travel, Flight Centre Travel Group Limited, Navan, and Perk, among others.

AI is transforming the market by enabling personalized booking recommendations, automated policy compliance, dynamic pricing optimization, and real-time disruption management across corporate travel programs.

Key challenges include rising and volatile short-haul airfare costs, increasing carbon reporting obligations under EU CSRD, the substitution risk from virtual meeting platforms, GDPR data compliance complexity for cross-border travel programs, and duty of care demands amplified by elevated geopolitical uncertainty across parts of the European region.

Significant opportunities exist in AI-native travel management platforms, sustainable corporate travel compliance tools required for CSRD Scope 3 reporting, SME-focused self-service booking solutions, and TMC platform consolidation plays targeting mid-market enterprises across rapidly growing Central and Eastern European corporate travel markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)