Europe Cheese Market Size, Share, Trends and Forecast by Source, Type, Product, Distribution Channel, Format, and Country, 2026-2034

Europe Cheese Market Size, Share, Trends & Forecast (2026-2034)

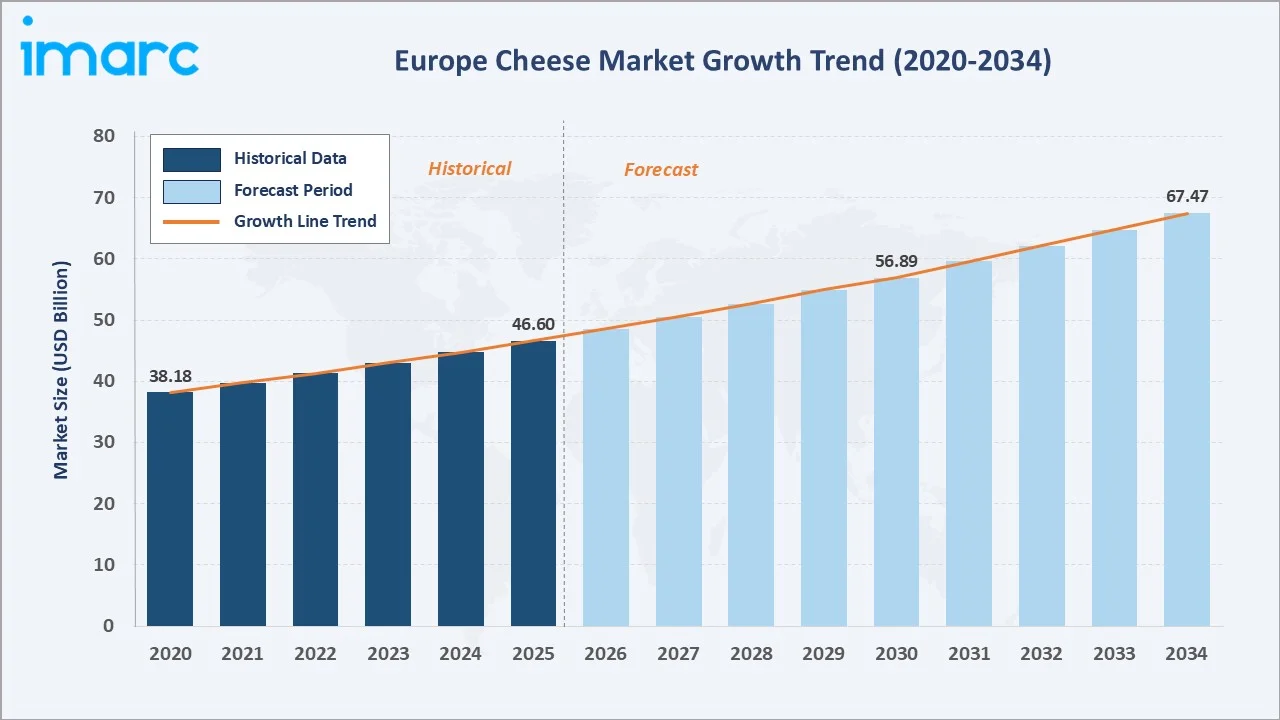

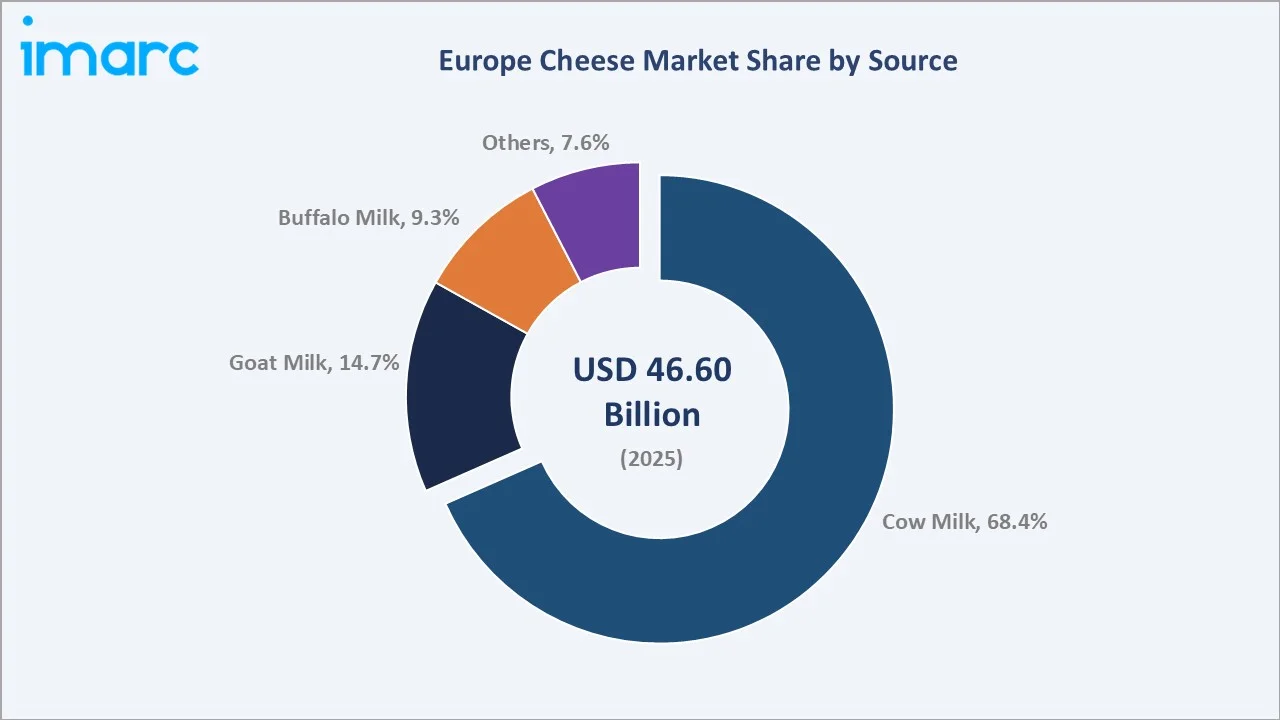

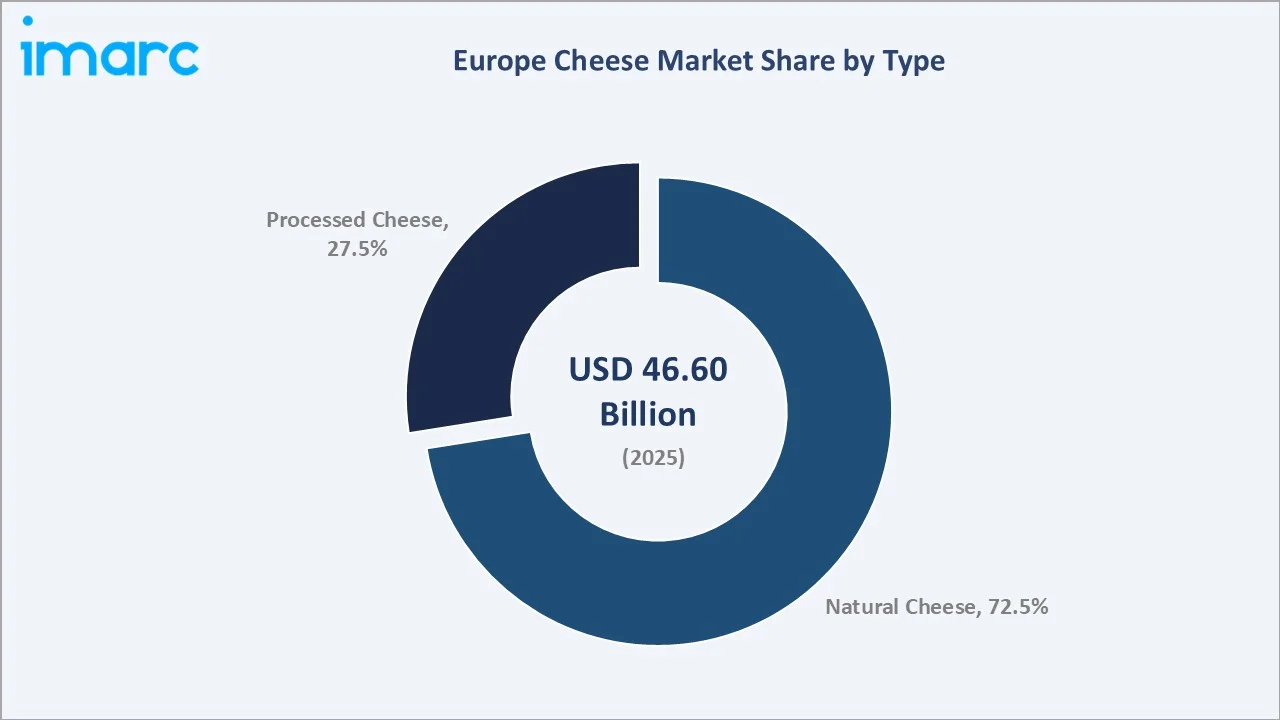

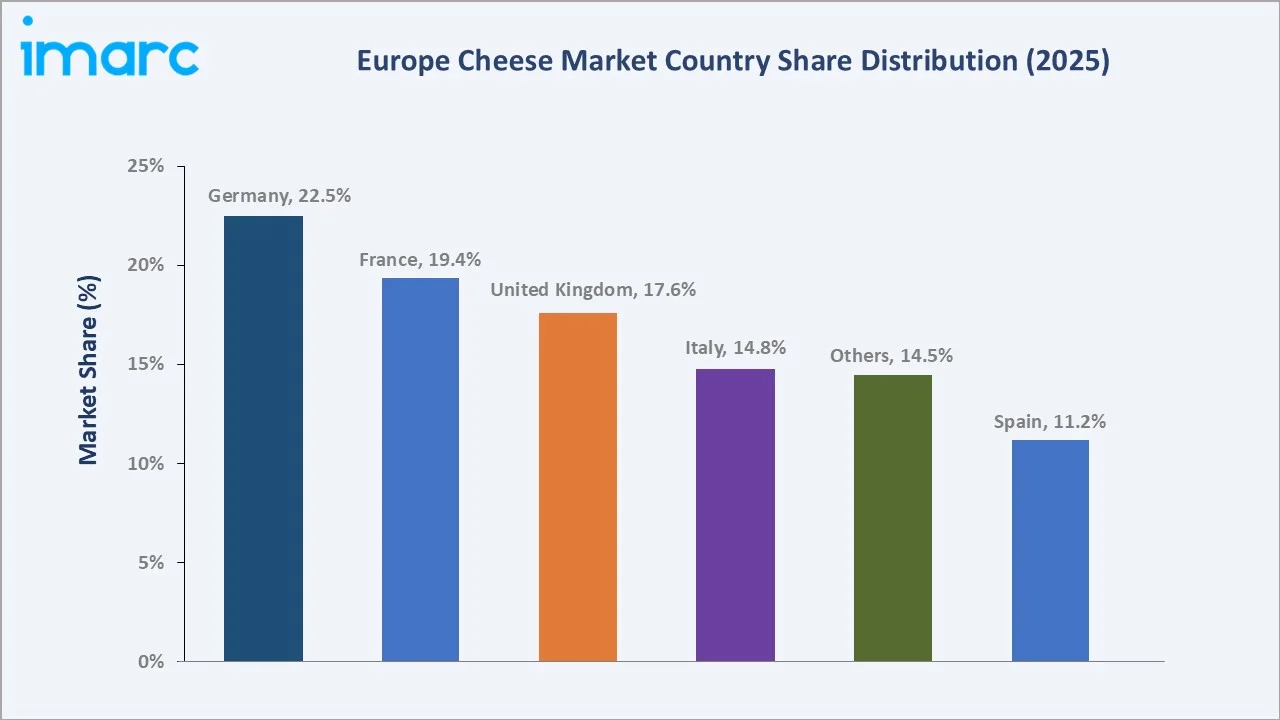

The Europe cheese market size was valued at USD 46.60 Billion in 2025 and is projected to reach USD 67.47 Billion by 2034, exhibiting a CAGR of 4.07% during the forecast period 2026-2034. Rising demand for premium and artisanal varieties, the strength of EU-protected designations such as PDO and PGI, sustained foodservice recovery, and growing consumer interest in high-protein and clean-label dairy products are propelling the Europe cheese market growth. Cow Milk leads the source segment with a 68.4% share in 2025, while Natural cheese dominates the type segment at 72.5%. Germany represents the largest country market with a 22.5% revenue share in 2025, followed closely by France and the United Kingdom.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 46.60 Billion |

|

Forecast Market Size (2034) |

USD 67.47 Billion |

|

CAGR (2026-2034) |

4.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (22.5% share, 2025) |

|

Fastest Growing Country |

Spain (CAGR ~4.85%) |

|

Leading Source |

Cow Milk (68.4%, 2025) |

|

Leading Type |

Natural Cheese (72.5%, 2025) |

The Europe cheese market growth trajectory from 2020 through 2034 reflects a stable historical expansion base supported by mature dairy infrastructure, alongside a steady forecast curve powered by premium variety adoption, foodservice penetration, and innovation in lactose-free and functional cheese categories.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight goat milk and processed cheese as the higher-growth sub-categories within the Europe cheese industry analysis through 2034, reflecting consumer diversification and convenience-format demand across European households.

Executive Summary

The Europe cheese market is undergoing structured expansion, anchored by deep cultural consumption habits, regulatory protection of regional varieties, and rising premium product penetration. The market reached USD 46.60 Billion in 2025 and is projected to climb to USD 67.47 Billion by 2034 at a CAGR of 4.07%. Eurostat reported per-capita cheese consumption in the EU at approximately 20 kg annually, among the highest globally, and continues to underpin baseline demand resilience even amid inflation-led food cost pressures.

Cow Milk dominates the source category with a 68.4% share in 2025, supported by Europe's vast bovine dairy infrastructure and large-scale industrial cheese production capacity. Goat Milk holds 14.7%, and is the fastest-growing source segment, reflecting consumer interest in distinct flavour profiles and perceived digestibility advantages. Natural Cheese leads the type segment with 72.5% in 2025, while Processed Cheese contributes 27.5%, driven by household snack formats and quick-service foodservice expansion.

Germany leads the regional landscape with 22.5% revenue share in 2025, supported by its position as one of the world's largest cheese producers and exporters. France follows closely at 19.4%, anchored by globally recognised PDO/PGI brands such as Roquefort, Camembert, and Comte. The United Kingdom contributes 17.6%, while Italy and Spain hold 14.8% and 11.2% respectively, each shaped by deeply rooted regional cheese traditions.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Cow Milk - 68.4% share (2025) |

|

Leading Type Segment |

Natural Cheese - 72.5% share (2025) |

|

Leading Country |

Germany - 22.5% revenue share (2025) |

|

Second Country |

France - 19.4% revenue share (2025) |

|

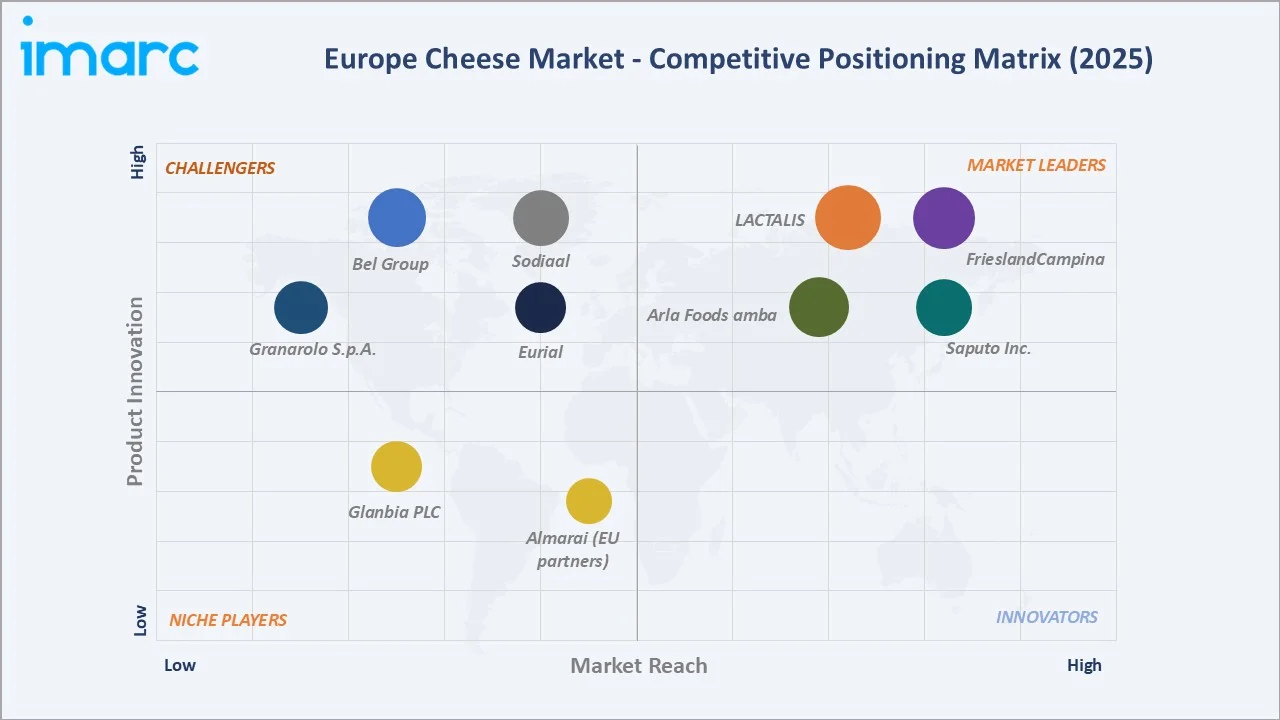

Top Companies |

LACTALIS, Arla Foods amba, FrieslandCampina, Saputo Inc., Bel Group, Sodiaal, Granarolo S.p.A., Eurial, Glanbia PLC, and Almarai |

Key Analytical Observations Supporting the Above Data:

- Cow Milk's 68.4% dominance in 2025 reflects Europe's vast bovine dairy base, with the EU producing roughly 160 Million Tonnes of cow milk in 2024, the bulk of which feeds industrial and artisanal cheese production.

- Natural Cheese leads the type segment at 72.5% in 2025, supported by entrenched culinary traditions, PDO/PGI-protected status across more than 240 cheese designations, and rising premium variety preference among urban European consumers.

- Germany's 22.5% country share in 2025 stems from its USD 6.7 Billion annual cheese export base in 2024, large-scale processing infrastructure, and strong private-label retail penetration through Aldi, Lidl, and Edeka networks across the region.

Europe Cheese Market Overview

Cheese is a ripened or fresh dairy product made by coagulating milk through the action of rennet or acidification, followed by curd separation, pressing, salting, and ageing. Europe is the world's largest cheese-producing and consuming region, accounting for over 45% of global cheese output in 2024, supported by deeply integrated dairy cooperatives, protected geographical indications, and a multi-tier retail and HoReCa ecosystem.

Applications span retail packaged formats, foodservice (pizzerias, QSRs, fine-dining), and industrial ingredient use in ready meals, sauces, and bakery. Major channels include hypermarket retail, specialty cheese counters, online direct-to-consumer artisan platforms, and B2B ingredient supply to food manufacturers.

Macroeconomic enablers include rising disposable income across Eastern Europe, foodservice recovery post-2022, EU agricultural subsidies under the Common Agricultural Policy, and growing export demand from Asia-Pacific and the Middle East.

Market Dynamics

To evaluate market opportunities, Request Sample

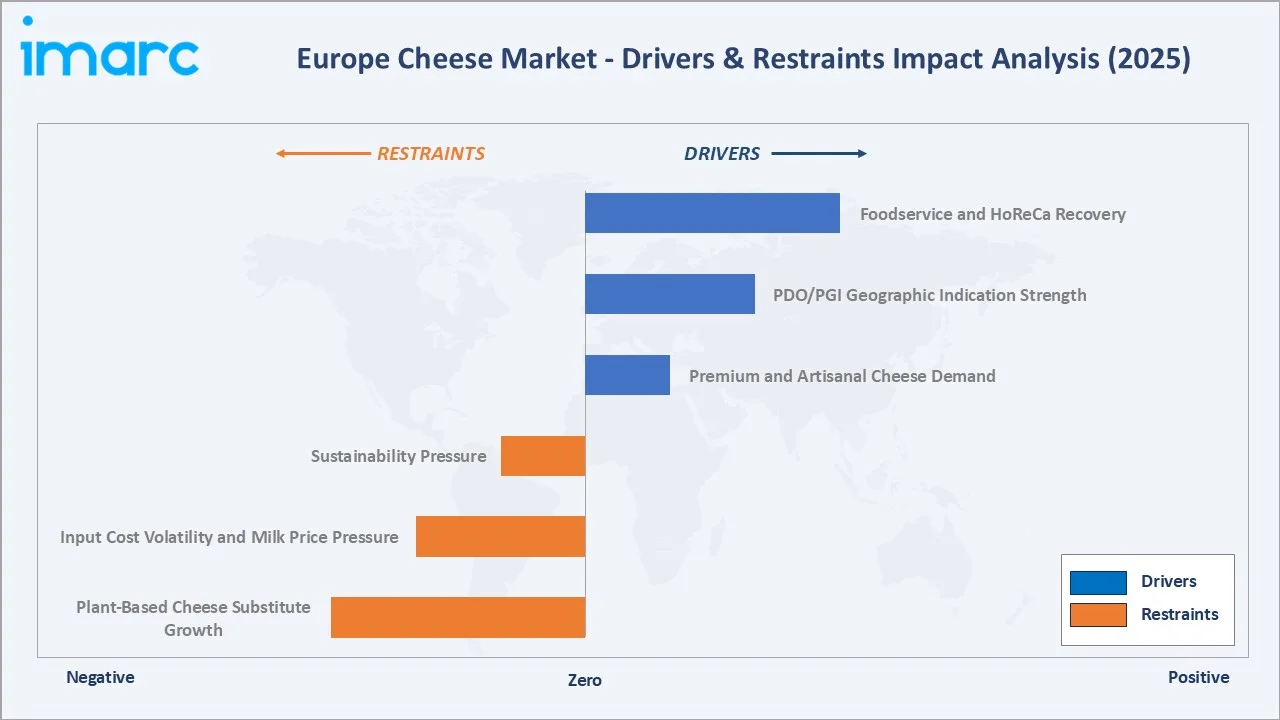

Market Drivers

- Premium and Artisanal Cheese Demand: European consumers continue to trade up to premium, single-origin, and artisanal cheese formats, supported by retail premiumisation in Germany, France, and the UK.

- PDO/PGI Geographic Indication Strength: Over 240 European cheeses carry PDO or PGI status, including Parmigiano Reggiano, Roquefort, Comte, and Manchego. For instance, Parmigiano Reggiano operates under strict EU PDO regulations, ensuring authenticity and enabling sustained premium pricing versus non-GI alternatives.

- Foodservice and HoReCa Recovery: European foodservice cheese demand has rebounded since 2022, with pizza, fast-casual Italian, and gourmet burger chains driving mozzarella and cheddar volume growth.

Market Restraints

- Plant-Based Cheese Substitute Growth: Plant-based cheese alternatives are growing and capturing share among younger urban consumers, particularly in Germany, the UK, and the Netherlands.

- Input Cost Volatility and Milk Price Pressure: European raw milk prices have fluctuated due to feed cost inflation, energy prices, and weather-driven yield variability. This pressure narrows margins for processors and drives selective product portfolio rationalisation.

Market Opportunities

- Lactose-Free and Specialty Cheese Formats: Approximately 25% of European adults experience some level of lactose intolerance, creating durable demand for lactose-free formats. Brands such as Galbani, Arla Lactofree, and Bel are accelerating SKU launches in this category.

- Export Expansion to Asia-Pacific and the Middle East: European cheese exports to Asia and MENA have grown significantly, led by Italian, French, and Dutch producers, with the European Union exporting approximately USD 5.47 billion worth of cheese globally in 2024.

- Functional and Fortified Cheese: Cheese fortified with vitamins, probiotics, and reduced-sodium variants represents a high-margin growth tier, with brands like Lactalis Galbani and Arla Skyr-cheese hybrids leading category innovation across European retail.

Market Challenges

- Sustainability and Methane Emissions Pressure: Cattle dairying is a significant methane source, and European environmental policy is intensifying scrutiny. Producers face rising costs to meet methane reduction targets.

- Private Label Margin Compression: Discounter chains such as Aldi, Lidl, and Biedronka command increasingly large cheese category share, driving price competition and squeezing branded margins, particularly in commodity cheddar, mozzarella, and gouda formats.

Emerging Market Trends

1. Premiumisation and Artisanal Cheese Renaissance

European consumers are gravitating toward small-batch, regionally distinct, and PDO-certified cheeses. Specialty cheese counters, online cheese clubs, and direct-to-consumer artisan platforms such as La Fromagerie, Neal's Yard Dairy, and Androuet are scaling rapidly.

2. Lactose-Free and Functional Cheese Innovation

Lactose-free cheese has shifted from niche to mainstream, with major brands such as Arla Lactofree, Galbani, and Hochland launching extensive ranges. Functional cheese variants are gaining shelf space across Tesco, Carrefour, Edeka, and Mercadona, addressing both medical needs and wellness positioning.

3. Sustainability and Clean-Label Dairy

Sustainability claims on cheese packaging, such as carbon-neutral, regenerative dairy, and recyclable packaging, are becoming a category baseline. Arla Foods has committed to achieving net zero emissions by 2050, while FrieslandCampina is investing significantly in regenerative agriculture and farmer sustainability programs.

4. Plant-Based Hybrid Cheese Innovation

Hybrid cheese, blending dairy with plant proteins to reduce carbon footprint and lactose content, is emerging as a flexitarian category. Bel Group's Boursin Dairy-Free range and Saputo's plant-based cheese launches signal that traditional cheesemakers are embedding plant-protein technology into their innovation pipelines.

5. Precision Fermentation and Bio-Identical Cheese

Precision-fermentation start-ups, including Formo, Those Vegan Cowboys, and DairyX, are developing animal-free dairy proteins to produce real cheese without livestock. While currently early-stage, these technologies are projected to reach commercial scale in select European markets, potentially restructuring the long-term competitive landscape.

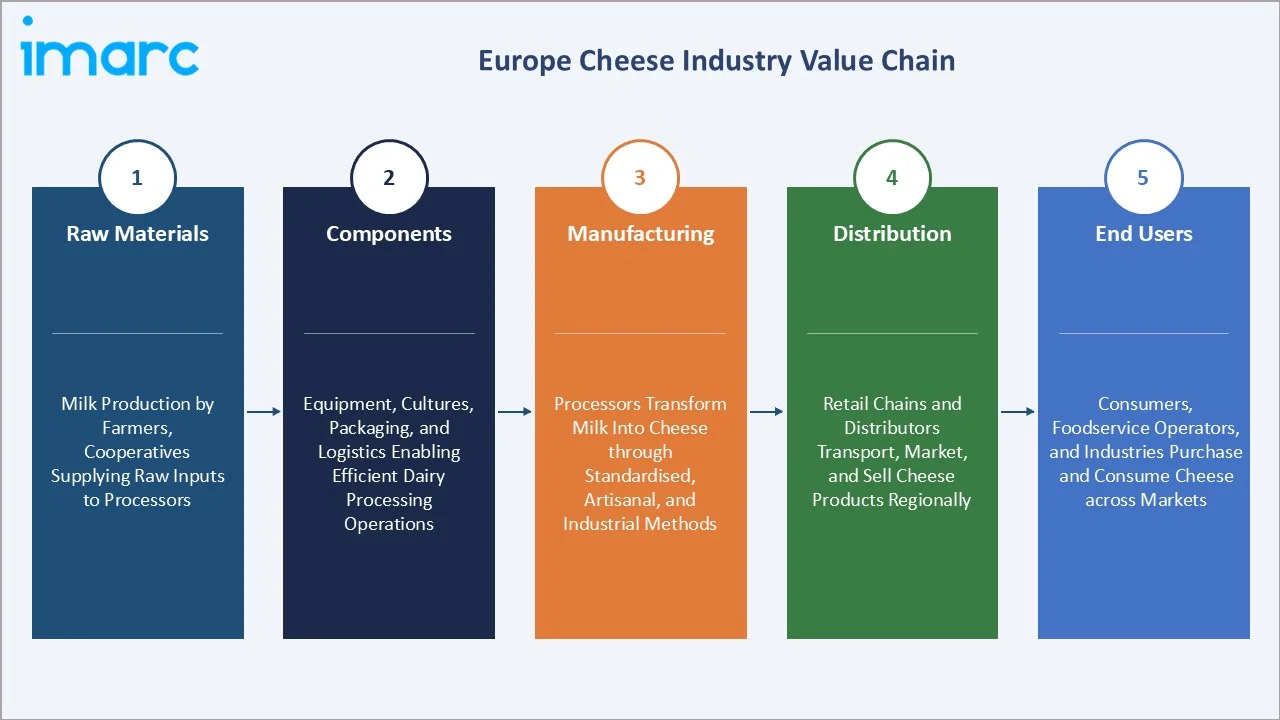

Industry Value Chain Analysis

The Europe cheese value chain spans five integrated stages from raw milk sourcing through end-consumer delivery. Each stage features distinct competitive dynamics, regulatory oversight, and margin profiles, with cooperatives and Tier-1 dairy processors capturing the highest strategic value.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Milk production by farmers, cooperatives supplying raw inputs to processors. |

|

Components |

Equipment, cultures, packaging, and logistics enabling efficient dairy processing operations. |

|

Manufacturing |

Processors transform milk into cheese through standardised, artisanal, and industrial methods. |

|

Distribution |

Retail chains and distributors transport, market, and sell cheese products regionally. |

|

End Users |

Consumers, foodservice operators, and industries purchase and consume cheese across markets. |

Tier-1 cheese manufacturers such as Lactalis, Arla, FrieslandCampina, and Saputo occupy the highest strategic value position in the European cheese value chain, integrating raw milk procurement, industrial processing, branding, and retail distribution.

Technology Landscape in the Europe Cheese Industry

Fermentation and Starter Culture Innovation

Advanced starter cultures from Chr. Hansen, DSM-Firmenich, and DuPont Danisco are enabling more consistent flavour profiles, faster ripening cycles, and improved shelf life. Adjunct cultures designed to reduce sodium content while preserving flavour are gaining adoption among health-positioned brands across Germany, France, and the Nordic region.

Sustainable Packaging and Smart Cold Chain

Recyclable, compostable, and reduced-plastic cheese packaging is a dominant innovation focus across European producers. Tetra Pak, Amcor, and Mondi are scaling fibre-based and PET-recyclable formats. IoT-enabled cold chain monitoring is becoming a baseline expectation in cheese logistics, with sensors deployed across refrigerated transport and warehouses.

Automation and Robotics in Cheese Production

European cheese plants are increasingly automated, deploying robotic curd handling, AI-driven ripening control, and automated cutting and packaging lines. GEA Group and Tetra Pak offer advanced modular and integrated cheese-making lines designed for both industrial mozzarella and flexible, smaller-batch cheddar and specialty cheese production.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Source | Cow Milk | 68.4% | 2025 |

| Type | Natural | 72.5% | 2025 |

| Product | Cheddar | 🔒 | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 🔒 | 2025 |

By Source

Cow Milk commands a 68.4% majority share in 2025, supported by Europe's bovine dairy infrastructure, scale economics, and broad applicability across cheese types ranging from mozzarella and cheddar to gouda and brie. The segment benefits from continuous productivity gains in milking technology and herd genetics across Germany, France, and the Netherlands.

To access detailed market analysis, Request Sample

Goat Milk at 14.7% in 2025 is the fastest-growing source segment, anchored by Mediterranean culinary traditions and rising premium positioning. France, Spain, and the Netherlands are the three largest goat cheese producers, with brands such as Soignon and Le Petit Billy leading domestic and export demand. Buffalo Milk represents 9.3% in 2025, concentrated in Italy where Mozzarella di Bufala Campana DOP commands strong export demand and premium pricing.

By Type

Natural Cheese dominates at 72.5% in 2025, encompassing fresh, soft, semi-hard, and hard varieties with no artificial additives or melting agents. The segment benefits from clean-label demand, PDO/PGI protection of regional varieties, and growing consumer preference for traditional production methods across France, Italy, Spain, and the UK.

Processed Cheese accounts for 27.5% in 2025, driven by household snack formats, slice formats for sandwiches and burgers, and industrial-scale food manufacturing demand. Major brands such as Bel Group's The Laughing Cow, Kraft Heinz's Philadelphia (Europe operations), and Hochland are dominant players.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

22.5% |

Largest production base, export hub, strong private-label retail (Aldi, Lidl, Edeka) |

|

France |

19.4% |

PDO/PGI variety leadership, Lactalis HQ, strong artisan and HoReCa demand |

|

United Kingdom |

17.6% |

Cheddar dominance, premium retail growth (Waitrose, M&S), foodservice rebound |

|

Italy |

14.8% |

DOP varieties (Parmigiano, Mozzarella di Bufala), strong export to US and Asia |

|

Spain |

11.2% |

Manchego DOP, rising goat milk segment, fastest-growing country market |

|

Others |

14.5% |

Smaller producers driven by export-oriented production, specialty cheeses, and intra-EU trade integration. |

Germany commands a 22.5% revenue share in 2025, the largest country position in Europe. Germany is also the EU's largest cheese producer, accounting for 22.5% in 2024, and a leading exporter to Italy, the Netherlands, and France. Strong private-label penetration through Aldi, Lidl, and Edeka, alongside premium organic cheese growth, anchors the German market's structural strength. France holds 19.4% in 2025, supported by the world's most diverse cheese variety portfolio with over 1,200 distinct cheeses and 45+ PDO designations.

The United Kingdom contributes 17.6% in 2025, anchored by cheddar production in southwest England and a premium retail cheese segment growing through Waitrose, Marks & Spencer, and Whole Foods Market. Italy at 14.8% is anchored by world-leading exports of Parmigiano Reggiano, Grana Padano, and Mozzarella di Bufala Campana, with Italian cheese exports surpassing EUR 5.4 Billion in 2024. Spain represents 11.2% in 2025 and is the fastest-growing country, fuelled by Manchego export momentum and rising goat cheese demand. Other markets (14.5%) include the Netherlands, Poland, Greece, and Nordic premium cheese.

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

LACTALIS |

President, Kraft |

Leader |

Largest global cheese player, vast SKU portfolio, PDO leadership |

|

Arla Foods amba |

Castello, Arla Apetina |

Leader |

Cooperative scale, lactose-free leadership, sustainability |

|

FrieslandCampina |

Frico |

Leader |

Dutch gouda heritage, B2B ingredients, global exports |

|

Saputo Inc. |

Cathedral City |

Leader |

UK cheddar dominance, premium positioning, scale |

|

Bel Group |

The Laughing Cow, Babybel, Boursin |

Challenger |

Snack formats, kids' cheese, plant-based hybrids |

|

Sodiaal |

Entremont, Candia |

Challenger |

French cooperative, broad cheese portfolio |

|

Granarolo S.p.A. |

Granarolo, Yomo |

Challenger |

Italian PDO leadership, fresh cheese strength |

|

Eurial |

Soignon |

Challenger |

Goat cheese leadership, French cooperative |

|

Glanbia PLC |

Truly Grass Fed, Kilmeaden |

Emerging |

Irish cheddar, B2B ingredients, US export channel |

|

Almarai (EU partners) |

Almarai Cheeses |

Emerging |

MENA-focused exports, cross-border partnerships |

The Europe cheese competitive landscape is characterised by a small number of large dairy cooperatives and Tier-1 cheese manufacturers commanding substantial retail and B2B ingredient share, alongside hundreds of regional cooperatives and PDO-protected artisan producers populating a fragmented long tail across France, Italy, Spain, and Greece.

Key Company Profiles

LACTALIS

Lactalis, founded in 1933 and headquartered in Laval, France, is the world's largest dairy company. Its cheese portfolio spans premium artisan brands and mass-market labels distributed across more than 100 countries.

- Product & Brand Portfolio: President (camembert, brie), Galbani (mozzarella, ricotta), Societe (Roquefort), Bridel, Lactel, Salakis, Galbani Santa Lucia, Parmalat dairy.

- Recent Developments: In April 2026, Lactalis completed the acquisition of Fonterra's consumer business, with the workforce expanded from 11,000 to 15,000+ employees and industrial sites from 34 to 50 in Asia/Oceania.

- Strategic Focus: Lactalis prioritises premium and PDO variety leadership, geographic expansion in Asia-Pacific, sustainability across its dairy supply chain, and continued strategic acquisitions to consolidate fragmented European cheese segments.

Arla Foods amba

Arla Foods is a Danish-Swedish dairy cooperative owned by approximately 8,400 farmers across seven European countries. Its cheese portfolio spans natural, processed, lactose-free, and organic categories distributed across more than 100 markets globally.

- Product & Brand Portfolio: Castello (premium aged cheese), Arla Lactofree, Apetina (feta-style), Havarti, Buko, Tickler cheddar.

- Recent Developments: In February 2026, Arla committed EUR 300 Million to a new cheese dairy at its Götene production site in Sweden, the largest single investment in Swedish food production history.

- Strategic Focus: Arla focuses on lactose-free leadership, sustainability, and cooperative farmer welfare, organic and premium portfolio extension, and global export expansion through its Castello and Lurpak premium portfolio.

Bel Group

Bel Group is a French dairy company founded in 1865, with operations in more than 130 countries. The company is known for its iconic snack-format cheese brands and is increasingly investing in plant-based and hybrid cheese innovation across Europe.

- Product & Brand Portfolio: The Laughing Cow, Babybel, Boursin, Kiri, Leerdammer, Nurishh (plant-based), GoGo Squeez (subsidiary).

- Recent Developments: In March 2026, Bel Group invested USD 200 Million to double Babybel cheese production capacity at its Brookings, South Dakota plant to 20,000 tonnes annually.

- Strategic Focus: Bel concentrates on healthy snacking innovation, plant-based and hybrid cheese leadership, packaging sustainability, and emerging-market expansion through portable snack-format cheese SKUs.

Market Concentration Analysis

The Europe cheese market exhibits moderate concentration. The top five companies, including Lactalis, Arla Foods, FrieslandCampina, Saputo, and Bel Group, collectively account for an estimated 28-33% of regional revenue in 2025, while the remainder is distributed across hundreds of cooperatives and regional artisanal producers operating under PDO/PGI protection.

The market structure is bifurcated. At the industrial commodity tier (cheddar, mozzarella, processed slices), consolidation is intensifying as scale economics, private-label competition, and sustainability capex requirements favour the largest players. Strategic acquisitions by Lactalis, Saputo, and Arla over 2022-2025 illustrate this consolidation trajectory.

Simultaneously, the artisan and PDO-protected segment remains highly fragmented. Over 240 PDO/PGI cheese designations across France, Italy, Spain, Greece, and Portugal sustain hundreds of small producers whose protected designation prevents large-scale competitive substitution. This dual structure - consolidating the commodity tier alongside the fragmented premium tier - is a defining feature of the European cheese market in 2025.

Investment & Growth Opportunities

Fastest-Growing Segments

Goat milk cheese is the highest-growth source segment, supported by Mediterranean variety expansion and premium retail positioning. Processed cheese is the higher-growth type segment, driven by foodservice and snack-format demand. Lactose-free formats represent the highest-growth functional category, growing steadily based on industry estimates.

Emerging Market Expansion

Eastern European markets - Poland, Romania, Czech Republic, and Hungary - represent the most accessible expansion frontier, with cheese consumption growing at 4-6% annually as disposable income rises and modern retail penetration deepens. Export markets, including Asia-Pacific (Japan, South Korea, Southeast Asia) and the Middle East offer additional structural growth runway, particularly for PDO-certified premium varieties.

Venture & Private Investment Trends

Private equity and strategic acquisitions have accelerated across European cheese, with notable activity from CapVest, Tikehau Capital, and Triton Partners in mid-market dairy assets. Venture capital is increasingly flowing into precision fermentation start-ups, including Formo (Germany), Those Vegan Cowboys (Belgium), and DairyX (Israel/EU operations), reflecting strategic interest in animal-free cheese protein technology.

Future Market Outlook (2026-2034)

The Europe cheese market forecast projects steady value expansion from USD 46.60 Billion in 2025 to USD 67.47 Billion by 2034 at a CAGR of 4.07%. This trajectory is underpinned by premium variety adoption, foodservice expansion, lactose-free innovation, and continued export growth to Asia and the Middle East, even as the category faces sustainability and plant-based substitution pressures.

Three structural shifts are likely to reshape the market through 2034. First, the rise of precision-fermentation animal-free cheese proteins, which could enter mainstream retail by 2028-2030, and reframe the competitive landscape. Second, intensifying sustainability pressure on dairy methane emissions requires substantial capex investment across the sector. Third, continued consolidation at the industrial tier alongside continued fragmentation at the artisan PDO/PGI tier.

By 2034, the European cheese industry is forecast to remain the world's largest by both production and value, with strengthened sustainability credentials, expanded lactose-free and high-protein portfolios, and emerging hybrid plant-dairy innovations. The category's resilience reflects deep cultural anchoring, regulatory protection of regional varieties, and consumer affinity for cheese as both an everyday staple and a premium culinary indulgence.

Research Methodology

Primary Research

Primary research included over 50 structured interviews conducted in 2024-2025 with European cheese industry stakeholders, including procurement directors at major dairy cooperatives, R&D leads at Tier-1 cheese manufacturers, retail category buyers at hypermarket and discounter chains, foodservice procurement leaders, and trade body representatives at organisations such as EUCDA, FIL-IDF, and Eucolait. Primary insights validated market sizing, segmentation estimates, and competitive positioning.

Secondary Research

Secondary sources include Eurostat dairy production and trade data, FIL-IDF World Dairy Situation reports, EU PDO/PGI registry, USDA Foreign Agricultural Service GAIN reports on EU dairy, ISMEA Italian dairy market data, INAO French quality designation registry, FAO global dairy outlook, and company annual reports of leading public and cooperative cheese producers, including Lactalis, Arla, FrieslandCampina, Saputo, and Bel Group.

Forecasting Models

Market size estimations and growth projections were derived using a combined top-down and bottom-up modelling approach. Top-down inputs included EU GDP forecasts, per-capita cheese consumption trends, retail and foodservice expenditure data, and dairy export volumes. Bottom-up inputs included company-level revenue tracking, segment-level pricing, and SKU-level volume estimates. Scenario analysis (base, optimistic, conservative) was performed to account for macroeconomic uncertainty.

Europe Cheese Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Cow Milk, Buffalo Milk, Goat Milk, Others |

| Types Covered | Natural, Processed |

| Products Covered | Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others |

| Formats Covered | Slices, Diced/Cubes, Shredded, Blocks, Spreads, Liquid, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | LACTALIS, Arla Foods amba, FrieslandCampina, Saputo Inc., Bel Group, Sodiaal, Granarolo S.p.A., Eurial, Glanbia PLC, Almarai (EU partners), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe cheese market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Europe cheese market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe cheese industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Cheese Market Report

The Europe cheese market was valued at USD 46.60 Billion in 2025, supported by mature dairy infrastructure, premium product expansion, and strong foodservice demand.

The market is projected to reach USD 67.47 Billion by 2034, growing at a CAGR of 4.07% during 2026-2034, driven by premiumisation, lactose-free innovation, and export growth.

Cow Milk leads with a 68.4% share in 2025, supported by Europe's vast bovine dairy infrastructure and broad applicability across cheddar, mozzarella, gouda, brie, and other major cheese types.

Natural Cheese leads with a 72.5% share in 2025, supported by entrenched culinary traditions, PDO/PGI-protected varieties, and rising premium retail demand for traditional production methods.

Germany leads with a 22.5% share in 2025, supported by its position as Europe's largest cheese producer and exporter, with strong private-label retail through Aldi, Lidl, and Edeka.

Key drivers include premium and artisanal cheese demand, PDO/PGI variety strength, foodservice recovery, lactose-free innovation, and rising export demand from Asia-Pacific and the Middle East.

Goat Milk cheese is the fastest-growing source segment at ~5.20% CAGR through 2034, fuelled by Mediterranean cuisine globalisation, premium positioning, and digestive-tolerance consumer demand.

Leading companies include LACTALIS, Arla Foods amba, FrieslandCampina, Saputo Inc., Bel Group, Sodiaal, Granarolo S.p.A., Eurial, Glanbia PLC, and Almarai.

Over 240 PDO/PGI cheese designations protect regional varieties, command 30-60% price premiums, and sustain a fragmented artisan production base alongside the consolidating industrial cheese tier.

Plant-based cheese accounts for under 2% of value in 2025 but is growing at over 12% annually, prompting traditional players such as Bel and Saputo to launch hybrid and dairy-free SKUs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)