Europe Chocolate Market Size, Share, Trends and Forecast by Product Type, Product Form, Application, Pricing, Distribution, and Country, 2026-2034

Europe Chocolate Market Size, Share, Trends & Forecast (2026-2034)

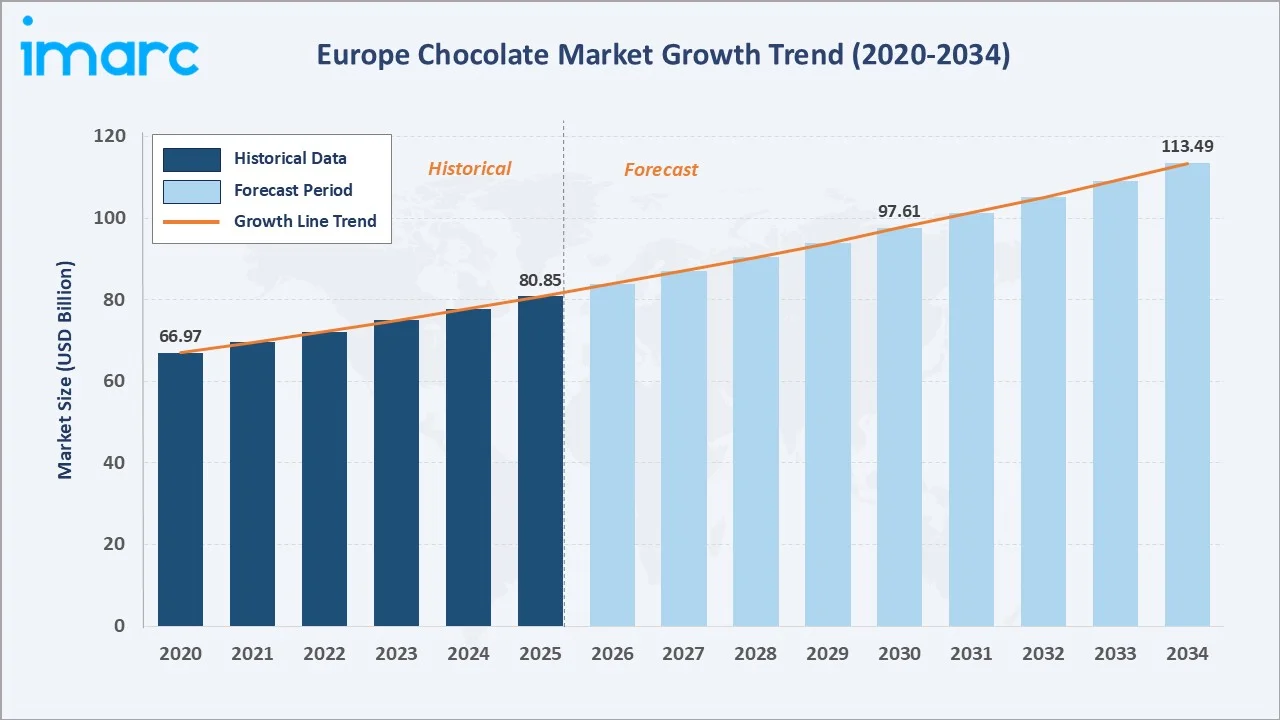

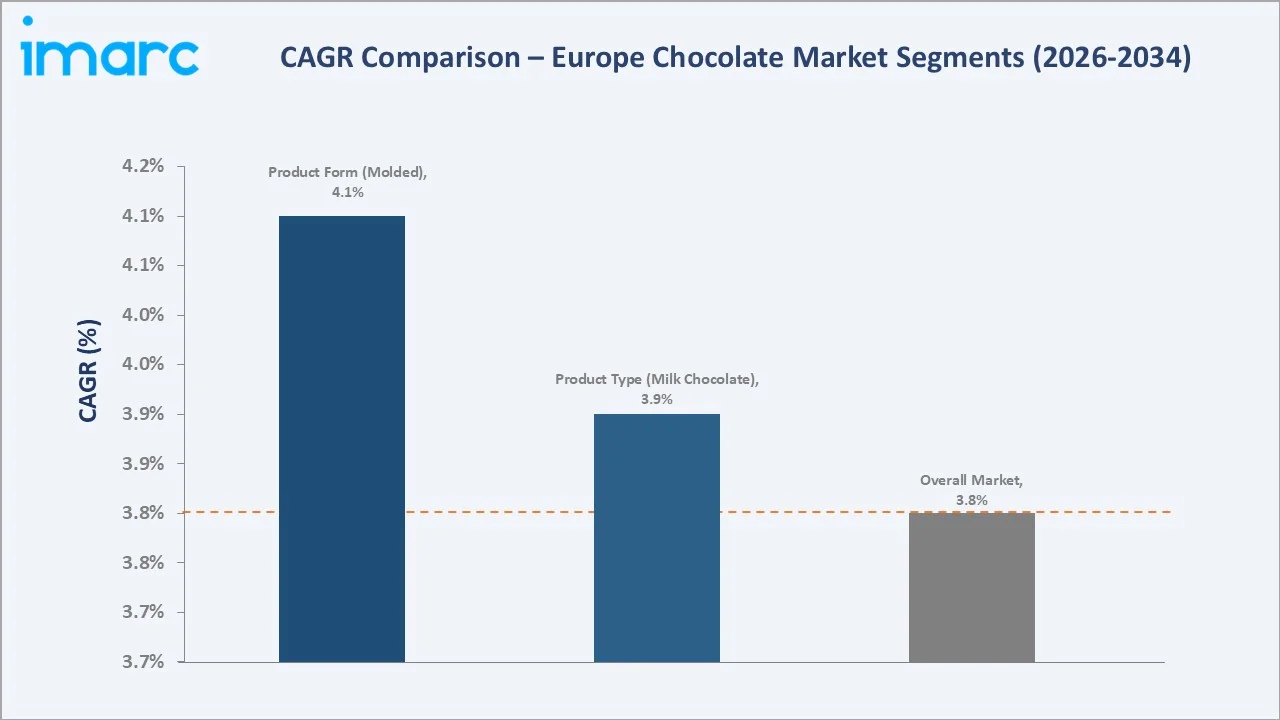

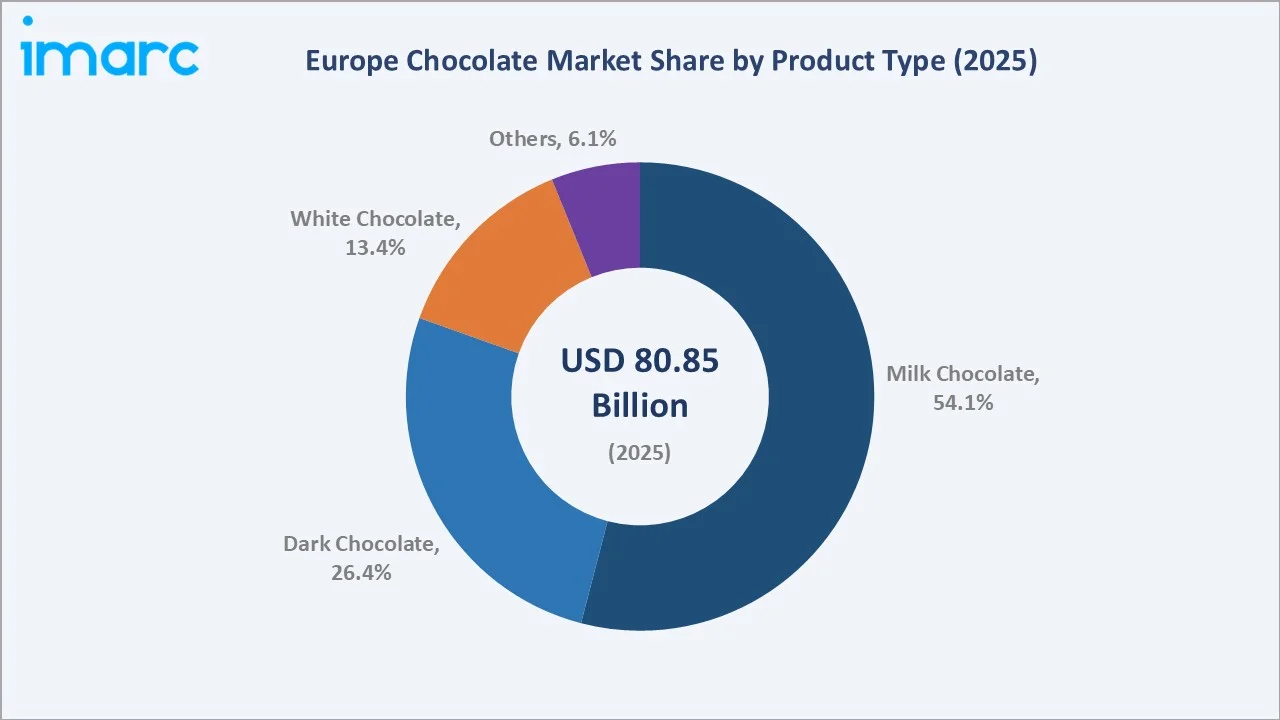

The Europe chocolate market size was valued at USD 80.85 Billion in 2025 and is projected to reach USD 113.49 Billion by 2034, growing at a compound annual growth rate (CAGR) of 3.8% during 2026-2034. Rising demand for premium and artisanal chocolates, growing health-conscious innovation, and expanding e-commerce distribution channels are the key growth drivers shaping this vibrant market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 80.85 Billion |

|

Forecast Market Size (2034) |

USD 113.49 Billion |

|

CAGR (2026-2034) |

3.8% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

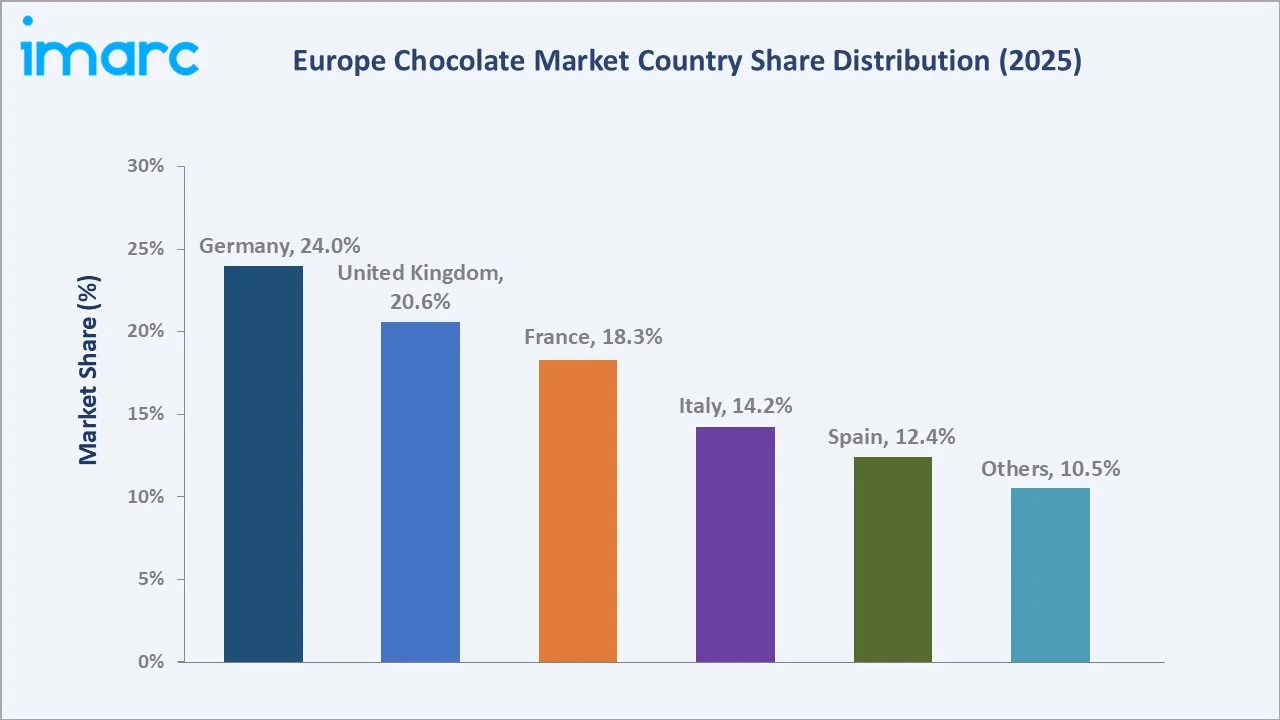

Largest Country |

Germany (24.0% share, 2025) |

To get more information on this market, Request Sample

Germany dominates the European chocolate market with a 24.0% share in 2025, driven by strong domestic consumption, established confectionery manufacturers, advanced processing capabilities, and extensive retail distribution networks. Milk chocolate leads product type demand at 54.06%, with molded chocolate commanding 59.02% of the product form segment.

With applications spanning confectionery, bakery, beverages, and foodservice, the Europe chocolate market is expected to continue expanding, supported by innovations in sustainable sourcing, functional product formats, and increasing adoption of premium and artisanal offerings across diverse consumer segments.

Executive Summary

The European chocolate market is on a sustained growth path, underpinned by cultural traditions, high per capita consumption, and evolving preferences for premium, health-conscious, and ethically sourced products. The market reached USD 80.85 Billion in 2025 and is forecast to surpass USD 113.49 Billion by 2034, reflecting a healthy CAGR of 3.8% over the forecast period.

Germany leads regionally with a 24.0% revenue share in 2025, supported by an established domestic manufacturing base, world-class confectionery brands, and sophisticated retail infrastructure. The United Kingdom (20.6%) and France (18.3%) are the second and third largest markets, with Italy (14.2%) and Spain (12.4%) contributing meaningfully. Milk chocolate commands 54.06% of product type demand while molded chocolate leads product form at 59.02%, driven by gifting traditions and premium praline demand.

Leading players, including Mars, Incorporated, Ferrero, Mondelēz International, Chocoladefabriken Lindt & Sprüngli AG, Nestlé, and Barry Callebaut, continue to invest in product development, sustainable sourcing, and manufacturing upgrades. In September 2025, Mars, Incorporated announced a EUR 1.0 billion EU manufacturing investment; Lindt & Sprüngli raised its 2025 growth outlook; and Ferrero invested EUR 95 million to upgrade cocoa processing facilities in Italy and Germany.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Milk Chocolate – 54.06% share (2025) |

|

Largest Segment (Product Form) |

Molded – 59.02% share (2025) |

|

Leading Country |

Germany – 24.0% revenue share (2025) |

|

Second Largest Country |

United Kingdom – 20.6% share (2025) |

|

Top Companies |

Mars, Incorporated, Ferrero, Mondelēz International, Chocoladefabriken Lindt & Sprüngli AG, Nestlé, and Barry Callebaut |

|

Market Opportunity |

Cocoa-free and functional chocolate segments projected for accelerated growth through 2034 |

Key Analytical Observations:

- Milk chocolate accounts for 54.06% of the European chocolate market in 2025, preferred for its creamy taste, cross-demographic appeal, and versatility across confectionery formats, including bars, seasonal specialties, and bite-sized products.

- Molded chocolate leads product forms at 59.02% in 2025, fueled by strong gifting demand during Christmas and Easter, premium pralines, and elaborate seasonal figurines that command higher price points.

- Germany holds 24.0% of the European market in 2025, underpinned by exceptional per capita consumption, established confectionery manufacturers, and Cargill's acquisition of German KVB to expand European chocolate processing capacity.

- Dark chocolate is the fastest-growing product type, gaining market share as consumers associate higher cocoa content with antioxidant benefits and cardiovascular health advantages.

- Sustainability compliance with the EU Deforestation Regulation is reshaping cocoa procurement standards across the industry, with manufacturers investing heavily in traceable, deforestation-free supply chains.

Europe Chocolate Market Overview

Europe occupies a pre-eminent position in the global chocolate ecosystem, functioning simultaneously as the world's largest per capita consumption region, a center of confectionery manufacturing excellence, and a primary driver of global cocoa demand. The European chocolate industry spans the full value chain from cocoa bean processing and couverture manufacturing through to retail confectionery, industrial chocolate supply, and premium artisanal production.

Consumer preferences across Europe are evolving rapidly, with the convergence of indulgence and wellness creating new product categories. Chocolate has entered premium gifting, functional nutrition, and specialty food segments that justify significantly higher price points. The EU's regulatory environment around cocoa deforestation, sugar content labeling, and ethical sourcing certifications is reshaping procurement and production standards across the industry.

Macroeconomic factors, including premiumization, sustainability mandates, and rising health consciousness, are primary growth catalysts. Europe's confectionery manufacturing heritage and consumer sophistication continue to set global quality benchmarks, while innovation in cocoa-free alternatives and functional formats opens new growth vectors beyond traditional confectionery.

Market Dynamics

To evaluate market opportunities, Request Sample

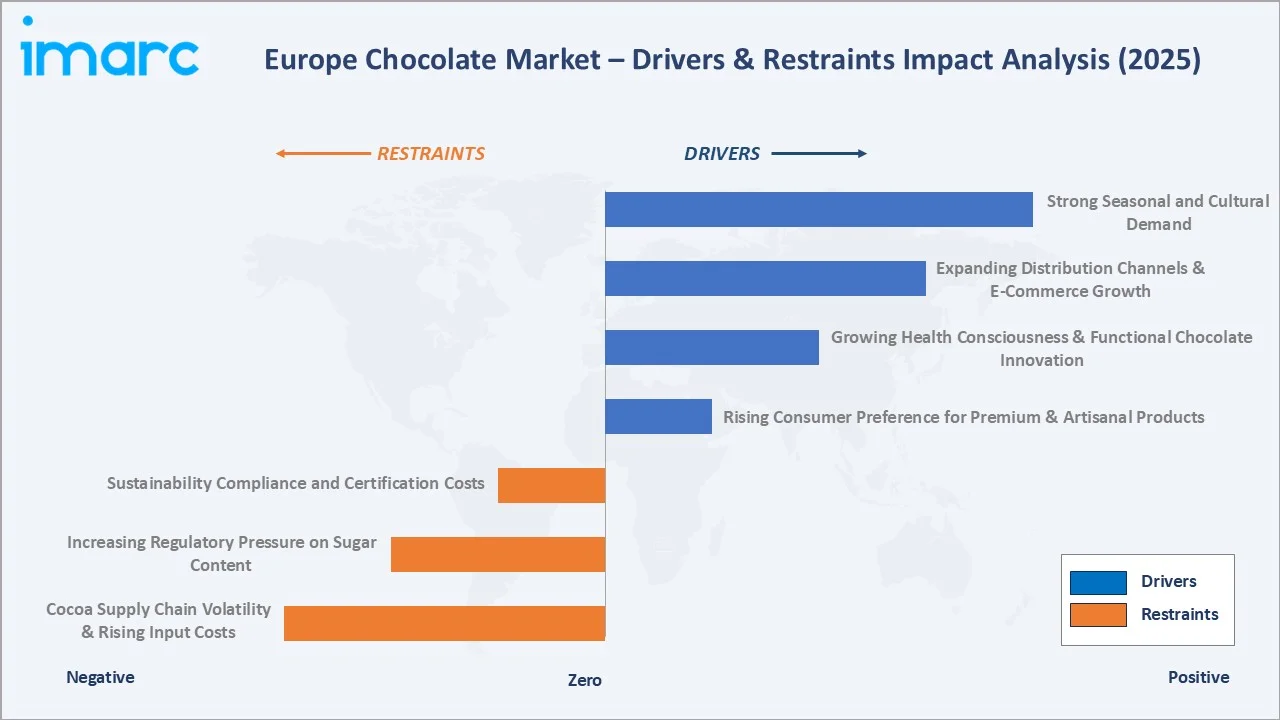

Market Drivers

- Rising Consumer Preference for Premium and Artisanal Products: Lindt & Sprüngli raised its 2025 growth outlook, driven by strong consumer loyalty and high demand for premium lines, with its EXCELLENCE Fusion line launched in August 2025, blending dark chocolate with milk or white layers for discerning consumers.

- Growing Health Consciousness and Functional Chocolate Innovation: Ferrero launched reduced-sugar premium chocolate pralines for health-conscious Europeans and invested EUR 95 million to upgrade sustainable cocoa processing facilities in Northern France.

- Expanding Distribution Channels and E-commerce Growth: The European e-commerce market was valued at USD 4.3 trillion in 2025, projecting to reach USD 8.6 trillion by 2034. Direct-to-consumer business models enable artisanal producers and premium brands to reach target audiences while maintaining brand storytelling and customer relationships.

- Strong Seasonal and Cultural Demand: Seasonal occasions, including Christmas and Easter, generate significant demand surges for molded chocolates, advent calendars, and decorative gifting formats. This cultural integration ensures reliable baseline demand underpinning market stability throughout economic cycles.

Market Restraints

- Cocoa Supply Chain Volatility and Rising Input Costs: Instability driven by climate variability, production concentration in West Africa, and rising commodity prices translates into increased manufacturing costs, pressuring profit margins and complicating pricing strategies across all market tiers.

- Increasing Regulatory Pressure on Sugar Content: Expanding frameworks targeting sugar consumption create formulation challenges and marketing restrictions, requiring manufacturers to accelerate development of reduced-sugar alternatives while maintaining consumer-preferred taste profiles.

- Sustainability Compliance and Certification Costs: Implementation of deforestation-free sourcing regulations and supply chain due diligence obligations imposes significant operational and financial burdens, particularly challenging for smaller manufacturers.

Market Opportunities

- Cocoa-Free and Alternative Chocolate Innovation: European foodtech startup Win-Win raised GBP 3 million Series A in July 2025 to expand cocoa-free chocolate alternatives in the United Kingdom and Europe. Foreverland secured EUR 6 million in funding to scale its cocoa-free chocolate ingredient, Choruba, across Europe, targeting expansion and new partnerships with confectionery manufacturers.

- Premium and Functional Chocolate Segments: Growing consumer willingness to invest in organic, fair-trade, and functional chocolate formats enriched with probiotics, plant proteins, and adaptogens opens substantial revenue expansion opportunities across multiple distribution channels.

- Sustainable Supply Chain Leadership: Manufacturers achieving traceable, deforestation-free cocoa supply chains ahead of EU regulatory deadlines are positioned to gain preferential access to institutional buyers and sustainability-conscious premium retailer partners.

Market Challenges

- Packaging Sustainability Requirements: Tightening EU packaging sustainability regulations necessitate significant investment in recyclable and compostable chocolate packaging across all product tiers and distribution formats.

- Competition from Health-Focused Snack Alternatives: Chocolate competes against protein bars, nut-based snacks, and other indulgent products positioned on functional health credentials, requiring continuous innovation to maintain relevance among health-conscious consumers.

Emerging Market Trends

1. Premiumization and Bean-to-Bar Movement

In November 2025, Barry Callebaut recently partnered with German food-tech innovator Planet A Foods to jointly develop sustainable chocolate alternatives, reducing reliance on traditional cocoa. Artisanal chocolatiers and bean-to-bar producers gain traction by offering transparency in sourcing, unique regional varieties, and handcrafted production methods.

2. Sustainable and Ethical Sourcing Transformation

Sustainability has emerged as a central pillar shaping purchasing decisions, with consumers actively seeking Fair Trade, Rainforest Alliance, and organic certifications. In 2024, Colombian chocolate maker Compañía Nacional de Chocolates launched a Traceability and Zero Deforestation Program with Farmforce, ensuring 100% sustainable, traceable cocoa compliant with EU regulations.

3. Functional and Reduced-Sugar Innovation

The intersection of indulgence and wellness drives a wave of product innovation. Manufacturers are developing vegan-friendly formats, probiotic-enriched chocolates, keto-compatible products, and reduced-sugar variants. Market penetration of functional chocolate formats is estimated to grow from 8% in 2025 to 18% by 2034.

4. E-Commerce and Direct-to-Consumer Expansion

E-commerce channels experience rapid growth as consumers appreciate convenience, product variety, and the ability to discover specialty chocolates unavailable through traditional retail. Subscription boxes, personalized gifting platforms, and corporate chocolate services represent high-margin emerging revenue streams for both established brands and artisanal producers.

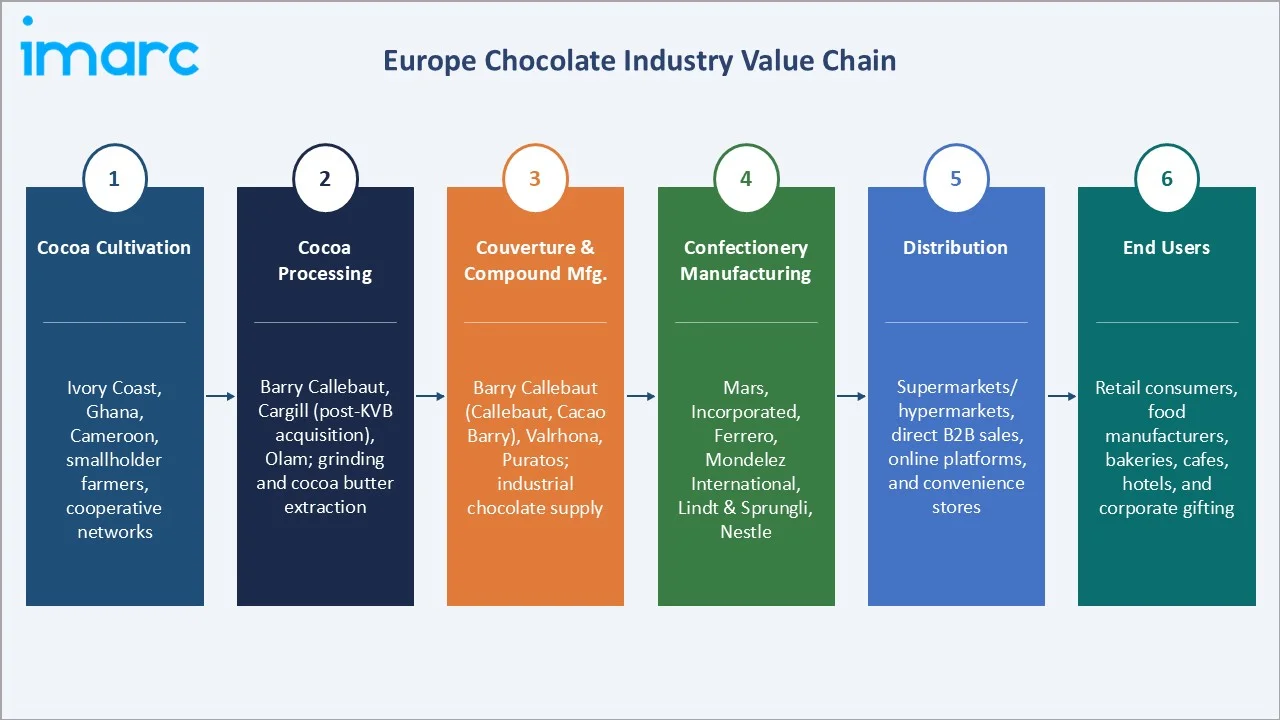

Industry Value Chain Analysis

The European chocolate value chain spans cocoa bean cultivation through end-consumer gifting, with each stage populated by specialized operators whose performance directly influences product quality, sustainability credentials, and cost.

|

Stage |

Key Players / Examples |

|

Cocoa Cultivation |

Ivory Coast, Ghana, Cameroon, smallholder farmers, cooperative networks |

|

Cocoa Processing |

Barry Callebaut, Cargill (post-KVB acquisition), Olam; grinding and cocoa butter extraction |

|

Couverture & Compound Mfg. |

Barry Callebaut (Callebaut, Cacao Barry), Valrhona, Puratos; industrial chocolate supply |

|

Confectionery Manufacturing |

Mars, Incorporated, Ferrero, Mondelēz International, Chocoladefabriken Lindt & Sprüngli AG, Nestlé |

|

Distribution |

Supermarkets/hypermarkets, direct B2B sales, online platforms, and convenience stores |

|

End Users |

Retail consumers, food manufacturers, bakeries, cafes, hotels, and corporate gifting |

Technology Landscape in the European Chocolate Industry

Advanced Cocoa Processing Technology

Modern European chocolate manufacturers deploy precision tempering equipment, controlled-atmosphere fermentation systems, and continuous conching technology that produce superior flavor development and texture consistency at scale. Cargill's expanded German KVB facilities incorporate next-generation grinding technology for ultra-fine cocoa particles used in smooth-texture premium applications.

Cocoa-Free Alternative Technology

European foodtech companies are pioneering cocoa-free chocolate production using fermented oats, carob, date derivatives, and precision-fermented flavor compounds that replicate cocoa taste profiles without commodity exposure. Planet A Foods and Win-Win represent the vanguard of this technology wave, attracting institutional investment and major manufacturer partnerships.

Sustainable Packaging Innovation

Manufacturers are investing in mono-material recyclable wrappers, compostable foils, and minimalist paper packaging that reduce plastic content while maintaining product freshness. EU packaging sustainability regulations coming into force between 2025 and 2030 are accelerating adoption timelines across all product tiers.

Traceability and Supply Chain Digitization

Blockchain-based cocoa traceability platforms enable manufacturers to verify deforestation-free, child-labor-free sourcing at the farm level. Farmforce's integration with Compañía Nacional de Chocolates demonstrates the scalability of digital traceability systems that will be mandatory under EU Deforestation Regulation compliance frameworks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Milk Chocolate |

54.06% |

2025 |

|

Product Forms |

Molded |

59.02% |

2025 |

|

Applications |

Food Products |

72.05% |

2025 |

|

Pricing |

Everyday Chocolate |

47.16% |

2025 |

|

Distribution |

Supermarkets and Hypermarkets |

45.07% |

2025 |

|

Country |

Germany |

24% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Milk chocolate dominates the European chocolate market with a 54.06% share in 2025, equivalent to approximately USD 43.68 Billion. Its commanding position reflects universally appealing taste characteristics, strong brand heritage, and extensive product format diversity spanning filled bars, seasonal specialties, and bite-sized confections.

Dark chocolate holds a 26.38% share and represents the fastest-growing product type, supported by health-driven consumer narratives around antioxidants and reduced sugar. White chocolate accounts for 13.42%, primarily serving confectionery manufacturing applications.

By Product Form

Molded chocolate leads product forms with a 59.02% share in 2025 (approximately USD 47.72 Billion). Molded products address both everyday consumption and special occasion gifting requirements, with manufacturing advances enabling consistent quality across large production volumes while maintaining artisanal appearance.

Countlines represent a key segment in the European chocolate market, driven by strong demand for convenient, single-serve chocolate bars consumed on the go. Growth is supported by product innovation in flavors, healthier variants, and premium positioning, alongside widespread availability across retail and vending channels.

Regional Market Insights

Europe's chocolate market exhibits meaningful geographic differentiation, with Germany, the United Kingdom, and France collectively accounting for approximately 63% of total regional consumption. Each country reflects distinct consumer preference profiles, retail channel mixes, and regulatory environments that shape competitive dynamics.

|

Country |

Share |

Key Growth Drivers |

Consumer Trend |

Regulatory Context |

|

Germany |

24.0% |

High per capita consumption, domestic manufacturing |

Premiumization, organic, seasonal gifting |

EU Deforestation Reg; sugar labeling |

|

United Kingdom |

20.6% |

Gifting culture, e-commerce, countline demand |

Sustainability, reduced sugar, ethical sourcing |

UK HFSS advertising rules; eco labeling |

|

France |

18.3% |

Artisanal heritage, praline tradition |

Premium dark, single-origin, luxury gifting |

EU organic certification; fair trade |

|

Italy |

14.2% |

Gianduia tradition, confectionery heritage |

Pralines, seasonal, regional varieties |

EU food labeling: geographic indications |

|

Spain |

12.4% |

Rising disposable income, gift market growth |

Value-tier growth, seasonal peaks, private label |

Nutri-Score labeling; sugar tax initiatives |

|

Others |

10.5% |

Nordic premiumization, Eastern Europe growth |

Health-oriented, plant-based, sustainability |

Varying national and EU baseline standards |

Germany's market leadership reflects manufacturing sophistication alongside consumption volume. Cargill strengthened its European chocolate presence by acquiring German KVB, gaining two plants and boosting capacity to supply customized cocoa and chocolate solutions across Germany and the EU. France's artisanal heritage creates a premium halo supporting above-average pricing across all channels.

Competitive Landscape

The European chocolate market operates within a highly competitive environment characterized by established multinational confectionery corporations alongside regional manufacturers and emerging artisanal producers. Market leaders leverage extensive distribution networks, strong brand portfolios, and significant marketing investments.

|

Company |

Brand Name |

Market Position |

Core Strength |

|

Mars, Incorporated |

Galaxy, Bounty, Maltesers |

Market Leader |

EUR 1 Billion EU investment; scale manufacturing; broad countline portfolio |

|

Ferrero |

Ferrero Rocher, Nutella, Kinder |

Market Leader |

Premium praline heritage; EUR 95M facility upgrades; reduced-sugar innovation |

|

Mondelēz International |

Milka, Cadbury, Toblerone |

Strong Challenger |

Milka chocolate milk drinks launched in Germany, Austria, and Poland (2024) |

|

Chocoladefabriken Lindt & Sprüngli AG |

Lindor, Excellence |

Strong Challenger |

Raised 2025 growth outlook; EXCELLENCE Fusion launched Aug 2025; premium leadership |

|

Nestlé |

KitKat, Aero, Quality Street |

Strong Challenger |

R&D investment in reduced sugar; broad pan-European distribution footprint |

|

Barry Callebaut |

Callebaut, Cacao Barry |

B2B Leader |

Planet A Foods partnership for sustainable alternatives; B2B industrial supply dominance |

Key Company Profiles

Mars, Incorporated

Mars, Incorporated is a global confectionery leader with a powerful portfolio of chocolate brands, including Galaxy, Bounty, Maltesers, Snickers, and Twix, that command significant shelf space across European markets.

- Product Portfolio: Full-spectrum chocolate confectionery spanning countlines, seasonal gifting, premium tablets, and foodservice ingredients.

- Recent Developments: EUR 1 billion EU manufacturing investment announced to modernize facilities across Europe.

- Strategic Focus: Manufacturing modernization; sustainability investment; premium segment expansion via core brand innovation.

Ferrero

Ferrero is an Italian-headquartered multinational commanding iconic chocolate brand positions across Europe through Ferrero Rocher, Nutella, Kinder, and Mon Chéri. The company launched reduced-sugar premium pralines addressing health-conscious European consumers.

- Product Portfolio: Premium pralines, hazelnut spreads, children's confectionery, seasonal gifting formats.

- Recent Developments: Investment of EUR 95 million (USD 108 million) facility upgrades at Villers-Ecalles, in northern France, which includes two new warehousing units, along with additional modernization initiatives.

- Strategic Focus: Premium differentiation; sustainable sourcing; health-conscious product innovation; Eastern European expansion.

Mondelēz International

Mondelēz International commands the European chocolate market through Milka, Cadbury, and Toblerone brands, leveraging extensive manufacturing and retail distribution networks.

- Product Portfolio: Milka tablets and seasonal products, Cadbury countlines, Toblerone premium bars.

- Recent Developments: In May 2024 announced the launch of Milka chocolate milk drinks in partnership with Arla Foods across Germany, Austria, and Poland.

- Strategic Focus: Category extension; sustainable cocoa sourcing; digital commerce acceleration.

Market Concentration Analysis

The European chocolate market exhibits moderate-to-high concentration at the top tier, with the five largest players collectively accounting for approximately 55–60% of total regional revenue in 2025. A substantial long tail of regional manufacturers, artisanal producers, and private-label suppliers ensures meaningful fragmentation below the top tier.

Consolidation activity is accelerating, driven by sustainability compliance costs, the need for scale in traceable cocoa sourcing, and investment requirements for reduced-sugar and functional product development. Larger manufacturers enjoy significant advantages in achieving EU regulatory compliance and funding R&D for alternative formulations. Private equity interest remains elevated, targeting mid-tier manufacturers with certified sustainable product portfolios and regional distribution networks.

Investment & Growth Opportunities

Fastest Growing Segments

Cocoa-free and alternative chocolate systems (estimated CAGR exceeding 15%), functional and enriched chocolate formats (12% CAGR), and premium artisanal/bean-to-bar segments (9% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a combined European addressable market estimated at USD 8+ billion by 2030.

Emerging Market and Channel Expansion

Eastern European markets, including Poland, the Czech Republic, and Romania, represent meaningful incremental growth opportunities as rising disposable incomes support premiumization. E-commerce and direct-to-consumer subscription models represent particularly high-ROI investment themes, enabling premium brand storytelling and margin capture superior to traditional retail channels.

Venture and Institutional Investment Trends

- Key investment themes include cocoa-free flavor technology, AI-powered supply chain traceability platforms, and sustainable packaging innovation addressing EU regulatory requirements.

- Family offices and PE firms are increasingly targeting premium artisanal chocolate platforms that consolidate regional craft brands under shared operations and marketing infrastructure.

- Sustainability-linked financing is available to manufacturers demonstrating measurable progress against EU Deforestation Regulation compliance metrics and Scope 3 emissions reduction targets.

Future Market Outlook (2026-2034)

The European chocolate market is positioned for sustained, broad-based growth through 2034. From a base of USD 80.85 Billion in 2025, the market is projected to reach USD 113.49 Billion by 2034, representing total incremental value creation of USD 32.64 Billion over the forecast decade.

Regulatory evolution, particularly the EU Deforestation Regulation, updated sustainability certification requirements, and tightening sugar content regulations, will drive significant product reformulation investment. Manufacturers achieving certification-ready, eco-compliant product portfolios are positioned to capture disproportionate shares of institutional and premium consumer demand.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including chocolate manufacturers, distribution channel operators, retail buyers, sustainability certification bodies, foodtech entrepreneurs, and end consumers across Germany, the United Kingdom, France, Italy, and Spain.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, EU regulatory documentation, industry associations (Caobisco, European Cocoa Association), retail data sources (IRI, Nielsen), and trade publications. Over 200 secondary sources were reviewed and triangulated for accuracy.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, cocoa production data, per capita consumption indices, and historical market evolution. The base-case CAGR of 3.8% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates.

Europe Chocolate Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | White Chocolate, Milk Chocolate, Dark Chocolate, Others |

| Product Forms Covered | Molded, Countlines, Others |

| Applications Covered |

|

| Pricings Covered | Everyday Chocolate, Premium Chocolate, Seasonal Chocolate |

| Distributions Covered | Direct Sales (B2B), Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Mars, Incorporated, Ferrero, Mondelēz International, Chocoladefabriken Lindt & Sprüngli AG, Nestlé, Barry Callebaut, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Chocolate Market Report

The Europe chocolate market size was valued at USD 80.85 Billion in 2025 and is projected to reach USD 113.49 Billion by 2034.

The Europe chocolate market is expected to grow at a CAGR of 3.8% during the forecast period from 2026 to 2034, supported by premiumization trends, health-conscious innovation, and expanding e-commerce distribution.

Germany leads the market with a 24.0% revenue share in 2025, driven by exceptional per capita consumption, an established domestic manufacturing base, and sophisticated retail infrastructure.

Milk chocolate dominates the product type segment with a 54.06% share in 2025. Its dominance reflects universal taste appeal, strong brand loyalty, and versatility across gifting, seasonal, and everyday consumption formats.

Molded chocolate leads the product form segment with a 59.02% share in 2025, driven by strong demand for traditional chocolate bars, premium pralines, and seasonal figurines across both everyday retail and gifting channels.

Key players include Mars, Incorporated, Ferrero, Mondelēz International, Chocoladefabriken Lindt & Sprüngli AG, Nestlé, and Barry Callebaut.

Key drivers include rising consumer preference for premium and artisanal products, growing health consciousness driving functional chocolate innovation, expanding e-commerce distribution, and sustained seasonal demand during Christmas and Easter.

Key challenges include cocoa supply chain volatility, increasing regulatory pressure on sugar content, sustainability compliance requirements under the EU Deforestation Regulation, and competition from health-focused snack alternatives.

Significant opportunities exist in cocoa-free alternative chocolate technology, functional and enriched chocolate formats, premium artisanal segment consolidation, and e-commerce direct-to-consumer models. Eastern European market expansion represents a meaningful incremental geographic opportunity as disposable incomes rise.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)