Europe Cigarette Market Size, Share, Trends, and Forecast by Type, Distribution Channel, and Country, 2026-2034

Europe Cigarette Market Size and Share:

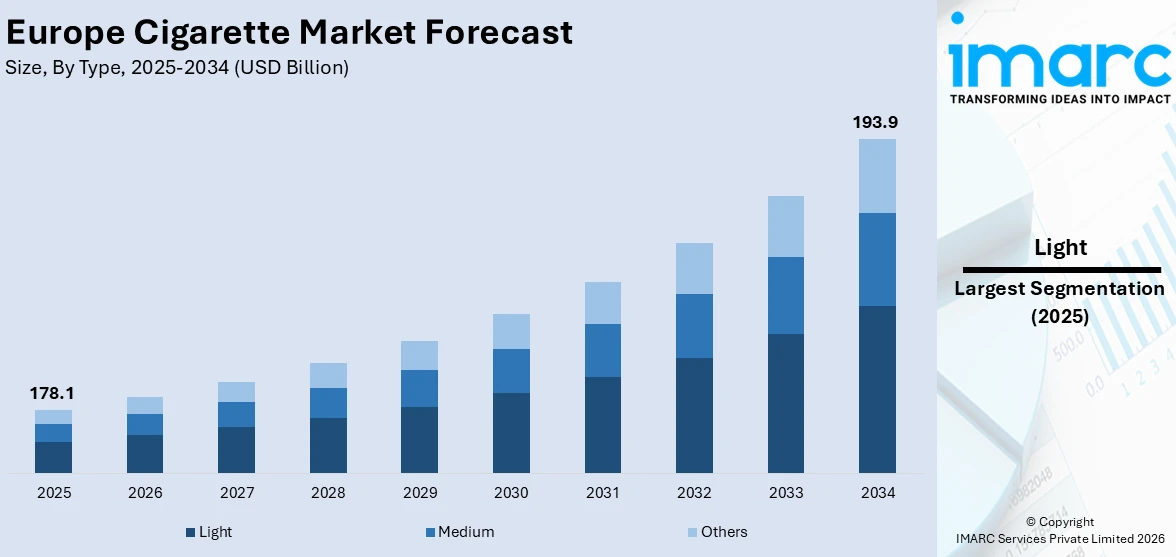

The Europe cigarette market size was valued at USD 178.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 193.9 Billion by 2034. Germany currently dominates the market, holding a significant market share in 2025. The market is driven by sustained consumer demand despite regulatory challenges, established smoking culture across European demographics, and rising disposable income levels enabling premium product consumption. Tourism influx and cultural integration of smoking in social settings further support market dynamics, alongside standardized taxation policies and robust manufacturing infrastructure across key European countries, further augmenting the Europe cigarette market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 178.1 Billion |

| Market Forecast in 2034 | USD 193.9 Billion |

The market is primarily driven by the sustained consumer demand despite increasing health awareness and regulatory pressures. In line with this, the established smoking culture across European countries and the social acceptance of tobacco consumption in certain demographics are also providing an impetus to the market. According to the European Commission, despite progress, approximately 26% of the EU population and 29% of young Europeans aged 15–24 smoke. Moreover, the considerable rise in disposable income levels is also acting as a significant growth-inducing factor for the market. In addition to this, the expanding working population creating higher stress levels is resulting in higher consumption of tobacco products as stress-relief mechanisms.

To get more information on this market Request Sample

Besides this, the growing demand for premium and luxury cigarette variants due to rising affluence and brand consciousness is creating lucrative opportunities in the market. Also, the increasing availability of products through diversified distribution channels including online platforms is impacting the Europe cigarette market growth positively. The market is further driven by the implementation of standardized taxation policies and the presence of established tobacco manufacturing infrastructure across key European countries. Apart from this, easy product accessibility across tobacco shops, convenience stores, and supermarkets is propelling the market. Although tobacco use remains unevenly distributed geographically in Europe, with countries such as Bulgaria and Serbia reporting the highest tobacco use rates at around 40% of the population aged 15 and older, while countries like the UK, Norway, and Denmark have prevalence closer to 15–17%. Some of the other factors contributing to the market include the tourism industry bringing international consumers, the cultural integration of smoking in social settings, and extensive brand loyalty among existing consumer base.

Europe Cigarette Market Trends:

Economic Prosperity and Disposable Income Growth

The Europe cigarette market experiences significant momentum from the region's robust economic foundation and rising consumer purchasing power. According to reports, the median annual disposable income per inhabitant in the EU was 19,955 PPS (Purchasing Power Standard) in 2023, reflecting the strong economic capacity of European consumers to afford tobacco products. This economic prosperity enables consumers to explore premium cigarette categories and international brands, creating a positive Europe cigarette market outlook. Higher disposable income levels facilitate brand switching behaviors and encourage experimentation with different product variants, contributing to market dynamism. The correlation between economic stability and tobacco consumption patterns demonstrates how financial security influences consumer spending on discretionary products like cigarettes, supporting sustained market demand across various price segments.

Workforce Demographics and Lifestyle Patterns

The contemporary European workforce structure significantly influences cigarette consumption patterns, creating sustained market demand through lifestyle-driven tobacco use. Professional environments and work-related stress factors contribute to smoking behaviors, particularly among adults in demanding occupations, which is one of the major Europe cigarette market trends. The established work culture across European countries normalizes smoking breaks and social smoking practices, embedding tobacco consumption into daily professional routines. Extended working hours and high-pressure work environments drive stress-relief seeking behaviors, where cigarettes serve as coping mechanisms for workplace pressures. Additionally, the social networking aspects of smoking in professional settings create peer influence dynamics that sustain consumption patterns, while the accessibility of tobacco products near commercial and industrial areas ensures convenient availability for working populations. It has been reported that in 2024, 37.3% of employed people in the EU worked between 40 and 44.5 hours per week on average, while only 7.2% worked less than 20 hours per week in their main job.

Distribution Channel Diversification and Accessibility

The Europe cigarette market benefits substantially from comprehensive distribution network expansion and enhanced product accessibility across multiple retail channels. The diversification of sales channels, including tobacco shops, supermarkets, hypermarkets, convenience stores, and online platforms, ensures widespread product availability and consumer convenience. According to the Europe cigarette market forecast, this multi-channel approach accommodates varying consumer preferences for purchasing locations and shopping behaviors, from traditional tobacco specialty stores to modern e-commerce platforms which will drive sustained market growth. The strategic placement of tobacco products in high-traffic retail locations maximizes consumer exposure and impulse purchasing opportunities. Furthermore, the integration of online retail channels with traditional distribution networks creates seamless omnichannel experiences, while regulatory compliance across different channel types maintains market legitimacy and consumer trust in product authenticity. As reported, 77% of EU internet users made at least one online purchase in 2024.

.webp)

Europe Cigarette Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Europe cigarette market, along with forecasts at the regional and country levels from 2026-2034. The market has been categorized based on type and distribution channel.

Analysis by Type:

- Light

- Medium

- Others

Light stands as the largest component in 2025, due to evolving health consciousness among consumers who seek perceived reduced-risk alternatives without complete cessation. This segment capitalizes on consumer psychology that associates "light" terminology with healthier smoking options, driving preference shifts from regular to light variants. The marketing positioning of light cigarettes as harm-reduction products appeals to health-aware smokers who wish to maintain their smoking habits while addressing health concerns. Regulatory frameworks across European countries have historically supported light cigarette categories, enabling manufacturers to develop and promote these products effectively. The segment benefits from premium pricing strategies that consumers willingly accept for perceived health benefits, generating higher profit margins. Additionally, the sophisticated packaging and branding of light cigarettes attract quality-conscious consumers, while the availability of diverse flavor profiles and nicotine levels within the light category provides extensive choice options that enhance market penetration.

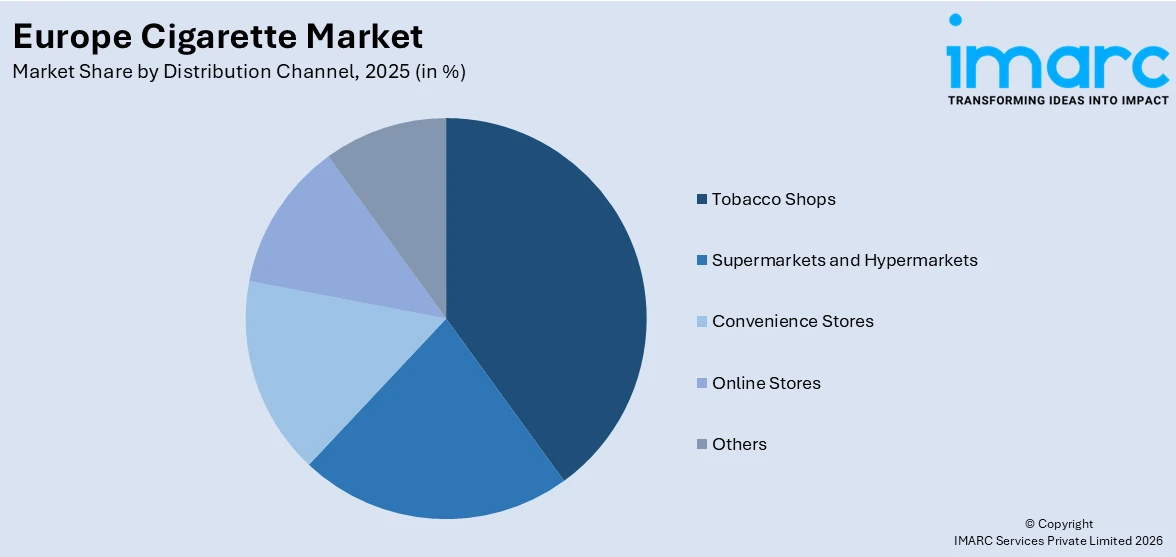

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Tobacco Shops

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

Tobacco shops maintain their position as the largest distribution channel in the European market through specialized expertise and comprehensive product portfolios that cater to diverse consumer preferences. These dedicated retail outlets provide personalized customer service and extensive product knowledge that enhances the purchasing experience for tobacco consumers. The traditional association between tobacco shops and quality assurance builds consumer trust and loyalty, particularly among experienced smokers who value expert recommendations and authentic products. Tobacco shops offer exclusive access to premium and specialty cigarette brands that may not be available through general retail channels, creating competitive advantages. The specialized nature of these outlets allows for better inventory management of various cigarette types, ensuring consistent availability of preferred brands and variants. Furthermore, tobacco shops often serve as community gathering points for smokers, fostering social connections that drive repeat business and word-of-mouth marketing.

Country Analysis:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

In 2025, Germany accounted for the largest market share in the Europe cigarette market due to its substantial population base, robust economic foundation, and established tobacco consumption culture. The country's strong industrial infrastructure supports efficient cigarette manufacturing and distribution networks, ensuring consistent product supply and competitive pricing across the market. Germany's strategic geographic position facilitates effective trade relationships with neighboring European countries, enhancing market reach and cross-border commerce opportunities. The regulatory environment in Germany provides clarity and stability for tobacco businesses, encouraging investment and market development activities. Consumer spending power in Germany supports premium cigarette consumption, while the diverse demographic composition creates demand for various cigarette types and brands. Additionally, Germany's extensive retail infrastructure, including tobacco shops, convenience stores, and supermarkets, ensures comprehensive market coverage and accessibility for consumers across urban and rural areas, strengthening its dominant market position.

Competitive Landscape:

The competitive landscape of the market is characterized by strategic initiatives focused on product innovation, market expansion, and consumer engagement enhancement. Key players are investing significantly in research and development activities to create differentiated product offerings that address evolving consumer preferences and regulatory requirements. Companies are implementing comprehensive brand portfolio management strategies, developing premium and value segments to capture diverse market opportunities while maintaining competitive positioning. Strategic partnerships and distribution agreements are being established to expand market reach and enhance supply chain efficiency across European countries. Digital marketing initiatives and e-commerce platform development are becoming increasingly important as companies adapt to changing consumer shopping behaviors and regulatory advertising restrictions. Additionally, manufacturers are focusing on sustainability initiatives and corporate social responsibility programs to improve brand perception and meet stakeholder expectations, while simultaneously investing in advanced manufacturing technologies to optimize production efficiency and product quality standards.

The report provides a comprehensive analysis of the competitive landscape in the Europe cigarette market with detailed profiles of all major companies.

Latest News and Developments:

- August 2025: South Korea’s KT&G launched its ESSE superslim cigarette brand in Germany, marking a major step in its European expansion. Partnering with Hauser, KT&G introduced ESSE Blue and Red in cities like Berlin and Munich. ESSE leads the global superslim market, selling 430 billion sticks in 2024.

- July 2025: JTI launched Sterling Dual Capsule Xtra Yellow in the UK, the country’s first lemon-flavored cigarillo. Featuring dual peppermint and lemon capsules, it expands JTI’s market-leading cigarillo range, which holds a 93.6% share. Priced at GBP 6.95, the product offers retailers a 20% introductory profit margin.

- May 2025: Aspire launched the Pixo Neo, an open-system e-cigarette featuring a 0.85-inch TFT touchscreen and compatibility with 2.0ml and 3.0ml pods. Available in three size variants under TPD and CRC standards, Pixo Neo retails for around EUR 19.90 across Europe, including Germany and Switzerland, via Aspire’s website and distributors.

- November 2024: Imperial Brands launched its Paramount cigarette brand in the UK through wholesale and independent retailers. Following its success in Germany, Paramount targets the growing value segment, which now makes up 30% of the UK market. Available in full flavour king-size and super king-size, it offers affordable quality.

- September 2024: Bulgaria-based KT International introduced new flavored variants for its Corset and The King cigarette brands, including Corset Fusion Flair and The King Chocolate Fusion. Targeting demand in Asia and the Middle East, the products offer bold capsule flavors and align with KTI’s strategy of delivering innovative, sensory-rich experiences.

Europe Cigarette Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment: Tobacco Shops, Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others

|

| Types Covered | Light, Medium, Others |

| Distribution Channels Covered | Tobacco Shops, Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Regions Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe cigarette market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe cigarette market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe cigarette industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Cigarette Market Report

The Europe cigarette market was valued at USD 178.1 Billion in 2025.

The Europe cigarette market is expected to reach USD 193.9 Billion by 2034.

The market is driven by sustained consumer demand despite regulatory pressures, rising disposable income levels with EU median reaching 19,955 PPS in 2023, expanding working population creating stress-driven consumption patterns, and diversified distribution channels enhancing product accessibility across traditional and online retail platforms.

Light cigarettes account for the largest Europe cigarette market share in 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)