Europe Construction Market Size, Share, Trends and Forecast by Sector and Country, 2026-2034

Europe Construction Market Size, Share, Trends & Forecast (2026-2034)

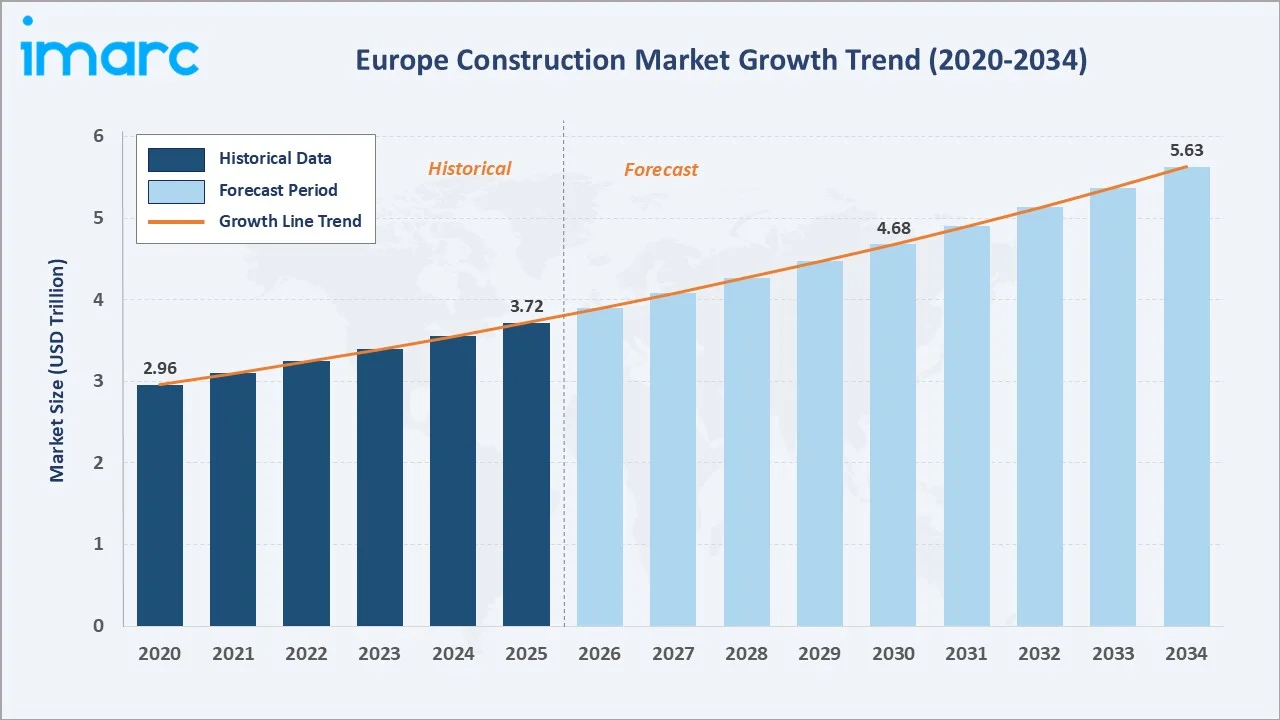

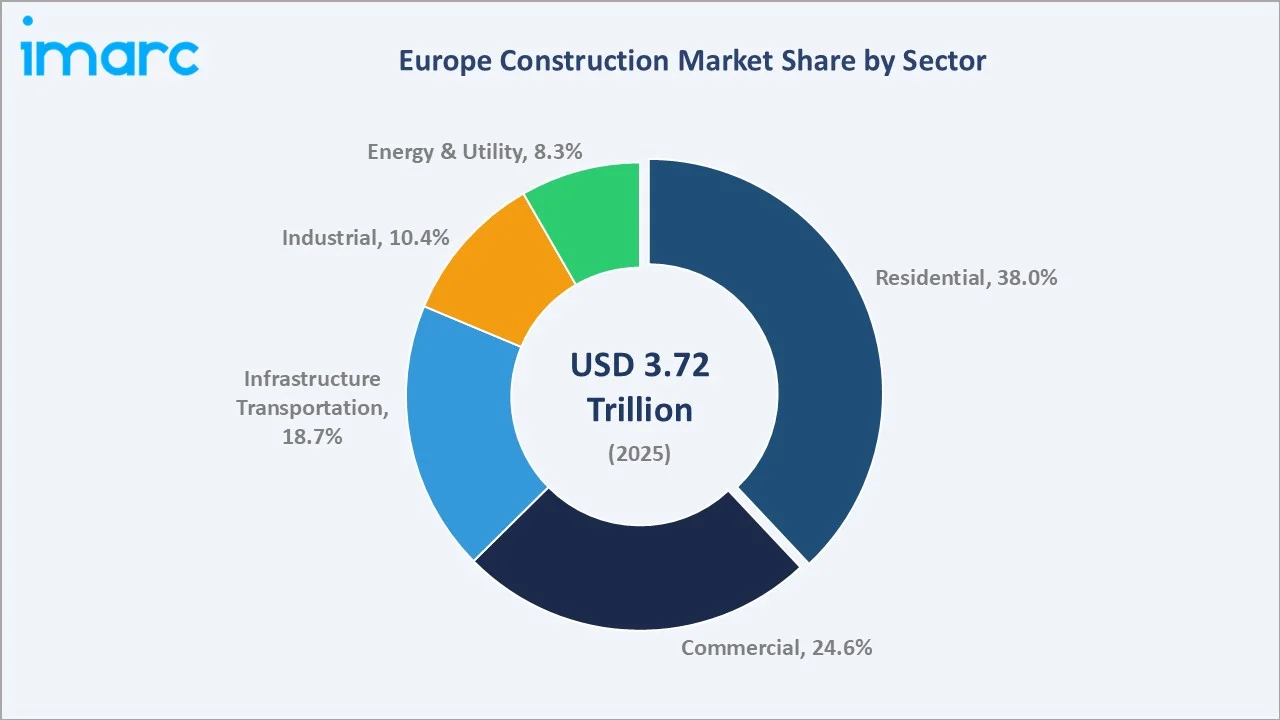

The Europe construction market size was valued at USD 3.72 Trillion in 2025 and is projected to reach USD 5.63 Trillion by 2034, exhibiting a CAGR of 4.70% during the forecast period 2026-2034. A sustained EU Green Deal policy push, record-high public investment in transport and energy infrastructure, accelerating building renovation mandates, and the scale-up of modular and prefabricated construction are driving the Europe construction market growth. Residential construction leads the sector mix at 38.0% share in 2025, while Germany dominates country demand at 25.0% of regional revenue.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.72 Trillion |

|

Forecast Market Size (2034) |

USD 5.63 Trillion |

|

CAGR (2026-2034) |

4.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (25.0% share, 2025) |

|

Leading Sector |

Residential Construction (38.0%, 2025) |

|

Second Sector |

Commercial Construction (24.6%, 2025) |

The Europe construction market growth trajectory from 2020 through 2034 reflects a resilient post-pandemic rebound, public-investment-led infrastructure expansion, and the structural build-out required to meet the EU's net-zero and housing-affordability agendas across its 27 member states plus the UK, Switzerland and Russia.

To get more information on this market, Request Sample

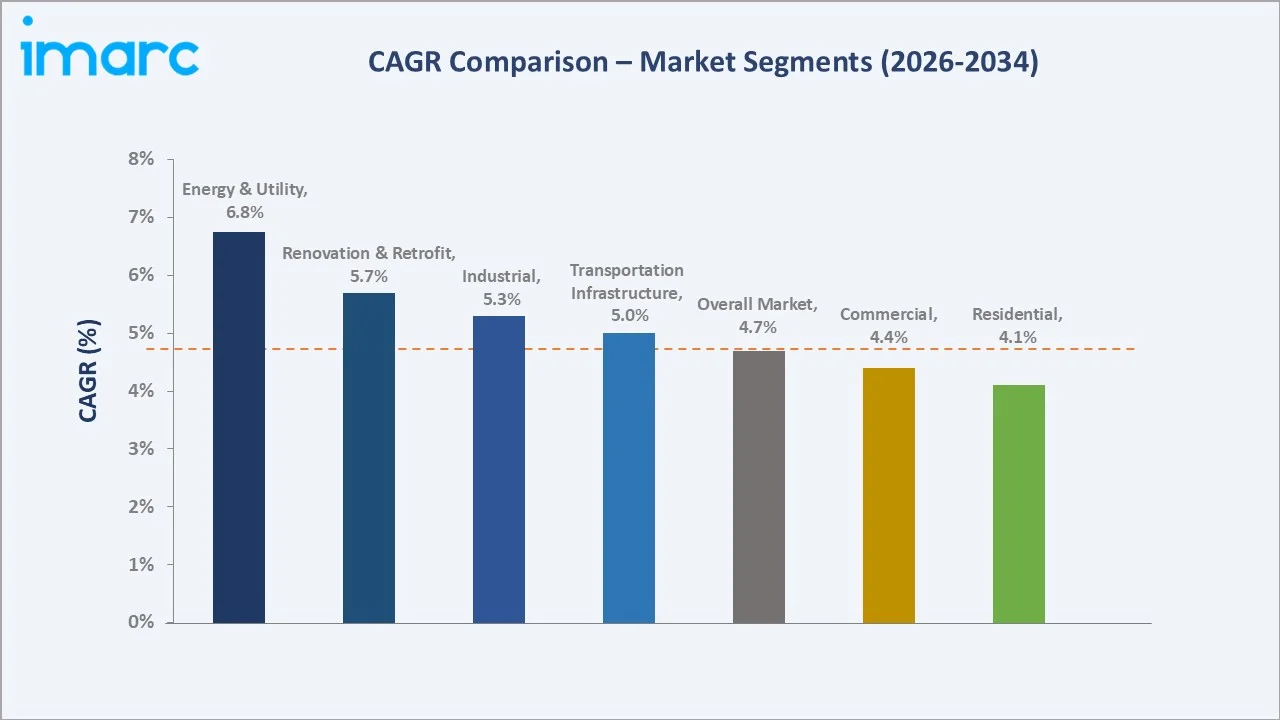

Segment-level CAGR comparisons highlight Energy & Utility and Renovation & Retrofit as the fastest-growing sub-categories within the Europe construction market forecast through 2034, outpacing traditional residential development and slower-growth commercial segments.

Executive Summary

The Europe construction market is entering a decisive decade of transformation shaped by climate policy, digitalisation, and demographic shifts. Valued at USD 3.72 Trillion in 2025, the market is forecast to reach USD 5.63 Trillion by 2034 at a CAGR of 4.70%, adding close to USD 1.91 trillion in incremental construction output over the forecast horizon.

Residential construction commands 38.0% share in 2025, anchored by acute housing shortages in German, French, and Dutch metropolitan areas and by EU-backed social and affordable-housing programmes. Commercial construction follows at 24.6%, propelled by logistics, data-centre, and healthcare capacity additions, while transportation infrastructure captures 18.7% on the back of TEN-T corridor upgrades, high-speed rail, and urban metro extensions.

Germany leads with a 25.0% share of European construction output in 2025, followed by the United Kingdom (16.8%) and France (14.7%). The Europe construction market outlook remains robust as green-building mandates, industrial reshoring, and the EUR 723 billion Recovery and Resilience Facility continue to catalyse public and private construction pipelines through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Sector |

Residential Construction – 38.0% share (2025) |

|

Second Sector |

Commercial Construction – 24.6% share (2025) |

|

Third Sector |

Infrastructure (Transportation) – 18.7% share (2025) |

|

Largest Country |

Germany – 25.0% share (2025) |

|

Second Country |

United Kingdom – 16.8% share (2025) |

|

Forecast CAGR (2026-2034) |

4.70% |

|

Top Contractors |

Vinci, ACS, Bouygues, Skanska |

|

EU Recovery Facility Outlay |

EUR 723 Billion (through 2026) |

Key Analytical Observations Supporting the Above Data:

- Residential's 38.0% dominance in 2025 reflects acute urban housing shortfalls across Germany, the UK, France, and the Netherlands, combined with EU-funded social housing programmes and robust private renovation activity tied to energy-performance upgrades.

- Commercial's 24.6% share is underpinned by the continent's logistics build-out, rapid data-centre capacity additions in Frankfurt, London, Amsterdam, Paris, and Dublin, and a wave of healthcare and hospitality investment.

- Infrastructure construction at 18.7% captures Trans-European Transport Network (TEN-T) upgrades, high-speed rail expansion in Italy and Spain, metro programmes in Paris, Warsaw, and Stockholm, and significant port modernisation across the Mediterranean and North Sea.

- Germany's 25.0% country lead reflects its scale, the federal EUR 500 billion special infrastructure fund, strong industrial-building activity, and the country's energy-efficient retrofit pipeline supported by the KfW programme.

- Energy & Utility construction at 8.3% is the most policy-sensitive slice, expanding on REPowerEU commitments, offshore-wind build-out in the North Sea, grid reinforcement, and hydrogen and battery-storage deployment across Germany, the UK, and the Nordics.

Europe Construction Market Overview

The Europe construction market encompasses the full spectrum of building and civil-engineering activity carried out across residential, commercial, industrial, infrastructure, and energy/utility end-use segments. Output is generated through new-build projects, renovation and retrofit works, and operations-and-maintenance activity across public and private assets. The market includes direct construction output, specialised trades, and the installation of mechanical, electrical, and plumbing systems delivered by an ecosystem of contractors, sub-contractors, specialist engineers, and prefabrication specialists.

Demand is shaped by a combination of demographic drivers (household formation, migration, ageing infrastructure), macroeconomic variables (interest rates, public capex, foreign direct investment), and policy frameworks (EU Green Deal, Energy Performance of Buildings Directive, REPowerEU, Fit for 55). Supply-side dynamics revolve around labour availability, raw-material costs, and the accelerating adoption of digital and industrialised construction methods such as BIM, modular manufacturing, and prefabricated components. Together these forces are redefining how assets are designed, delivered, and operated across Europe through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

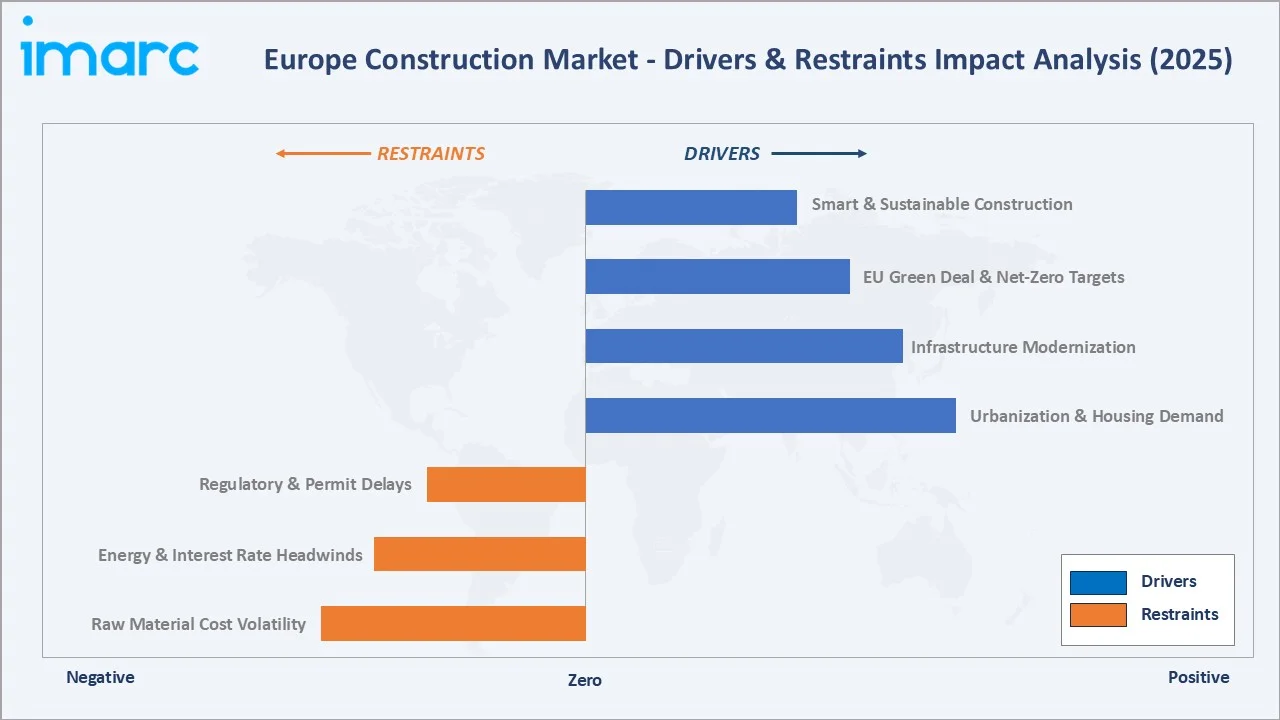

Market Drivers

- Urbanization and Housing Demand: Europe's housing deficit remains a primary growth lever. According to Eurostat, nearly 16.9% of the EU population lived in overcrowded households in 2024, alongside 9% facing arrears on housing payments, highlighting a structural supply-demand imbalance. Combined with house prices rising by over 50% since 2010, this reflects a persistent housing shortage across key markets such as Germany, France, the Netherlands, and Poland, sustaining demand in residential and affordable housing segments. Institutional build-to-rent investment across the UK, Ireland, and Spain adds a further multi-year demand layer for mid-market residential construction.

- Infrastructure Modernization: The EU's Recovery and Resilience Facility of EUR 723.8 billion and the Connecting Europe Facility continue to unlock transport, energy, and digital infrastructure programmes. The upgrade of the TEN-T core corridors, Rail Baltica, the Lyon-Turin tunnel, HS2 in the UK, and metro expansions in Paris, Madrid, and Warsaw collectively represent a multi-trillion-euro pipeline through 2034.

- EU Green Deal and Net-Zero Targets: Regulatory frameworks are structurally reshaping demand. The revised Energy Performance of Buildings Directive (EPBD) requires zero-emission standards for all new buildings from 2030 and progressive deep-retrofit obligations for the existing stock. REPowerEU mandates accelerated solar, wind, and grid build-out, while Fit for 55 is embedding decarbonisation targets across every construction sub-sector.

- Smart and Sustainable Construction: Digital delivery is moving from pilot to mainstream. BIM is now mandated or strongly recommended for public projects across the UK, France, Germany, the Nordics, Spain, and Italy. Modular, prefabricated, and off-site manufacturing solutions are scaling rapidly to address labour shortages and carbon reporting requirements, particularly in housing, hospitality, and healthcare.

Market Restraints

- Raw Material Cost Volatility: Cement, steel, and timber pricing have remained elevated and volatile post-2022, pressuring margins for contractors on fixed-price contracts and delaying smaller developer-led residential schemes.

- Energy and Interest Rate Headwinds: Higher borrowing costs through 2024-2025 have softened private residential starts in Germany, Sweden, and Finland, while sustained energy costs continue to inflate operating expenses for cement, steel, and glass producers.

- Regulatory and Permit Delays: Lengthy planning and environmental-impact approvals in Germany, France, and the UK extend project timelines and create uncertainty for large infrastructure and energy schemes.

- Skilled Labor Shortage: Construction federations across Germany, the UK, the Netherlands, and the Nordics report structural shortages of skilled trades and site engineers, constraining output and pushing wage inflation.

Market Opportunities

- Deep-Retrofit Renovation Wave: The Renovation Wave strategy targets doubling the annual energy renovation rate by 2030, covering 35 million building units. This creates a multi-decade procurement pipeline for insulation, glazing, heat pumps, MEP systems, and specialist retrofit contractors.

- Data Centre and Digital Infrastructure Build-out: FLAP-D markets (Frankfurt, London, Amsterdam, Paris, Dublin) along with Madrid and Milan are absorbing record data-centre capacity additions, with double-digit annual growth projected through 2030.

- Offshore Wind and Grid Reinforcement: North Sea, Baltic Sea, and Atlantic offshore wind pipelines, combined with cross-border interconnector and transmission upgrades, represent a multi-hundred-billion-euro construction opportunity through 2034.

Market Challenges

- Decarbonisation of Construction Materials: EU Emissions Trading System (ETS) coverage and the Carbon Border Adjustment Mechanism (CBAM) are adding cost to cement, steel, and aluminium, forcing materials producers and contractors to reformulate specifications and accelerate low-carbon alternatives.

- Fragmented Regulatory Landscape: Building codes, taxation of renovation, and procurement rules vary materially across member states and the UK, Switzerland, and Russia, complicating pan-European delivery models.

Emerging Market Trends

1. Accelerating Renovation and Decarbonisation of the Building Stock

The EPBD revision and national implementation road-maps are transforming renovation from a discretionary upgrade into a regulated requirement. Deep-retrofit activity is expanding fastest in Germany, France, Italy, and the Netherlands, where energy-performance thresholds and minimum energy-performance standards are creating structural demand for insulation, heat pumps, smart controls, and retrofit-focused contractors through 2034.

2. Modular, Prefabricated, and Off-Site Construction

Modular and prefabricated construction is scaling rapidly in the Nordics, the UK, and the Netherlands, driven by labour scarcity, carbon-reporting requirements, and the need for faster delivery of social housing, hospitality, and healthcare assets. Volumetric and panelised systems are increasingly specified for mid-rise residential and student accommodation, compressing programme times by 30-50% versus traditional methods.

3. BIM, Digital Twins, and AI-Enabled Project Delivery

BIM adoption is now pervasive on major public and private projects across the UK, France, Germany, the Nordics, and Spain. Digital twins, AI-powered scheduling, and computer-vision site monitoring are emerging as the next productivity layer, improving asset handover quality, reducing rework, and enabling predictive operations-and-maintenance planning.

4. Green Materials and Circular Construction

Low-carbon cement, recycled steel, cross-laminated timber, and circular-design principles are moving from pilot to specification standard. Public procurement in the Netherlands, Denmark, France, and Germany increasingly mandates embodied-carbon disclosures and minimum recycled-content thresholds, reshaping bidding strategy for major contractors.

5. Smart Cities and Urban Regeneration

EU Mission-backed climate-neutral-cities programmes, alongside national smart-city initiatives in Spain, Italy, and Central and Eastern Europe, are driving integrated urban regeneration packages that combine mobility, energy, digital, and social-infrastructure investment into long-duration construction pipelines.

Industry Value Chain Analysis

The Europe construction industry value chain spans five integrated stages from raw-material supply through the long operations-and-maintenance tail of built assets. Each stage features distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall Europe construction market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Cement, aggregates, steel, glass, timber, insulation – supplied by producers such as Holcim, HeidelbergCement, ArcelorMittal, Saint-Gobain, Stora Enso |

|

Building Materials & Components |

Precast concrete, structural steel, modular units, roofing, MEP components, prefabricated systems – often manufactured in-country with pan-European distribution |

|

Design & Engineering |

Architects, consulting engineers, BIM and digital-twin specialists – AECOM, Arup, Arcadis, Sweco, WSP lead the European consultancy market |

|

Construction Services |

Tier-1 and Tier-2 contractors – Vinci, ACS, Bouygues, Skanska, Strabag, Ferrovial, Balfour Beatty, NCC, Eiffage |

|

Operations & Maintenance |

Facilities management, retrofit specialists, energy-performance contractors – ISS, Sodexo Facilities, Veolia, Engie, Mitie |

Tier-1 general contractors capture the highest strategic value by integrating design-and-build capabilities, sustainability credentials, and cross-border delivery footprints. Simultaneously, facilities-management and retrofit-focused operators are emerging as strategic channels for long-term revenue as the renovation wave scales across member states.

Technology Landscape in the Europe Construction Industry

BIM, Digital Twins, and Common Data Environments

Building Information Modelling has transitioned from a delivery tool to a regulatory baseline. Level 2 BIM is mandated on centrally procured public projects in the UK; France requires BIM for major public contracts; Germany's BIM road-map targets infrastructure delivery; and Nordic countries treat BIM as default. Digital twins are emerging on airports, metros, and energy assets, enabling full-lifecycle asset optimisation.

Modular and Prefabricated Construction

Volumetric modular, panelised systems, and engineered timber are increasingly deployed on residential, education, and healthcare projects. The Nordic region and the UK lead in adoption, with suppliers such as Randek, Lindbäcks, and TopHat scaling industrialised output. Carbon benefits, tighter programme certainty, and labour savings are driving specification uptake across major contractors.

Sustainable Materials and Low-Carbon Concrete

Low-clinker cements (CEM II/III), calcined-clay binders, and recycled-aggregate concrete are being specified on flagship infrastructure and public projects. CBAM compliance pressures and ETS allowance costs are accelerating the shift, with Holcim, HeidelbergCement, and Cemex rolling out branded low-carbon product lines across European markets.

Robotics, AI, and Site Digitalisation

Autonomous site machinery, drone-based progress monitoring, computer-vision safety systems, and AI-assisted scheduling are moving from pilot to scale on major European projects. Tier-1 contractors such as Vinci and Skanska are investing in proprietary digital platforms to boost productivity and decarbonise delivery.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the Europe construction market, along with forecasts at the regional and country levels from 2026 to 2034. The market has been categorized based on sector and country.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Sector | Residential Construction | 38.0% | 2025 |

| Country | Germany | 25.0% | 2025 |

Market Breakup by Sector

Residential construction leads the Europe construction market with a 38.0% share in 2025. Demand is anchored by persistent urban housing shortages in Germany, France, the Netherlands, and the UK, combined with EU-backed affordable-housing delivery and private build-to-rent investment. Renovation of existing residential stock is an increasingly important volume driver as EPBD-aligned minimum energy-performance standards tighten through 2030 and beyond. Heat-pump installation, deep-envelope retrofit, and solar-PV integration are reshaping residential specifications across the continent.

To access detailed market analysis, Request Sample

Commercial construction represents 24.6% of European construction output, driven by logistics-and-warehouse expansion tied to reshoring and e-commerce, rapid data-centre capacity additions across FLAP-D markets, hospitality and healthcare pipelines in Southern Europe, and the refit of office stock to meet net-zero-carbon performance standards.

Transportation infrastructure construction accounts for 18.7%, supported by TEN-T corridor investments, high-speed-rail programmes in Italy, Spain, and the UK, urban metro expansion, and port and airport modernisation. Industrial construction (10.4%) captures factory and gigafactory build-out tied to battery, semiconductor, and pharmaceutical reshoring, while Energy and Utility construction (8.3%) reflects REPowerEU-driven renewables, grid reinforcement, and hydrogen infrastructure.

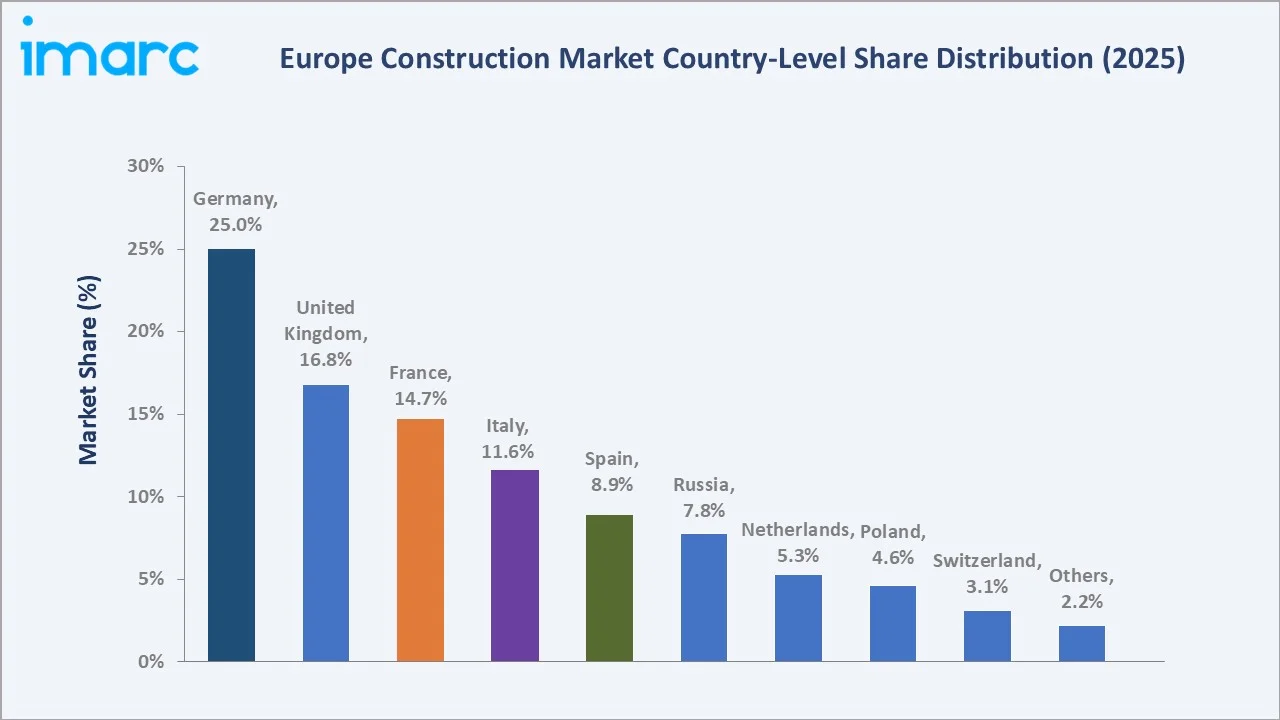

Country-Level Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

25.0% |

Federal EUR 500B special fund, KfW retrofit, industrial and data-centre build-out |

|

United Kingdom |

16.8% |

HS2, nuclear new-build, airport upgrades, Affordable Homes Programme |

|

France |

14.7% |

Grand Paris, 2024 Olympics legacy, EPR2 nuclear, France 2030 plan |

|

Italy |

11.6% |

PNRR Recovery Plan, Superbonus retrofit, high-speed rail expansion |

|

Spain |

8.9% |

Logistics, data centres, renewables, Madrid urban regeneration |

|

Russia |

7.8% |

Housing construction, transport infrastructure, regional development |

|

Netherlands |

5.3% |

Housing deficit, data centres, port and flood-defence infrastructure |

|

Poland |

4.6% |

EU cohesion funds, road and rail modernisation, residential growth |

|

Switzerland |

3.1% |

Premium residential, rail tunnels, infrastructure upgrades |

|

Others |

2.2% |

Nordics, Central and Eastern Europe, Balkans regeneration |

Germany commands 25.0% of European construction output in 2025, reflecting the combined effect of large-scale industrial and infrastructure pipelines and a deep residential renovation backlog. The federal government's EUR 500 billion special infrastructure and climate fund, the KfW energy-efficient retrofit programme, and an expanding data-centre and battery-gigafactory pipeline in Brandenburg, Saxony, and Saarland anchor long-term demand. Germany remains the largest single procurement market for both tier-1 contractors and specialised retrofit players operating across Europe.

The United Kingdom contributes 16.8% of regional revenue, supported by HS2 high-speed rail, nuclear new-build at Hinkley Point C and Sizewell C, Heathrow and regional-airport upgrades, and the Affordable Homes Programme. London, Manchester, and Birmingham continue to absorb a significant share of commercial, residential, and data-centre investment.

France accounts for 14.7%, anchored by the France’s infrastructure pipeline is underpinned by large-scale programmes including the ~€40bn Grand Paris Express, Paris 2024 Olympic legacy developments, and the EPR2 nuclear programme targeting six reactors (~€72.8bn), and the EUR 54 billion France 2030 industrial-investment plan. Italy's 11.6% share is driven by the EUR 194.4 billion PNRR Recovery and Resilience Plan, residential retrofit activity under the Superbonus scheme, and the continued build-out of the Frecciarossa high-speed rail network.

Spain (8.9%) leads Southern European logistics, data-centre, and renewable-energy construction, with Madrid, Barcelona, and Aragón absorbing record capex. Russia (7.8%) retains its position as a large but structurally constrained market shaped by sanctions and domestic infrastructure priorities. The Netherlands (5.3%), Poland (4.6%), and Switzerland (3.1%) collectively represent high-value niches in housing, logistics, rail, and premium residential construction. The remaining 2.2% captured under Others is distributed across the Nordics, Central and Eastern Europe, and the Balkans, where EU cohesion funds and regeneration programmes continue to drive mid-cycle growth.

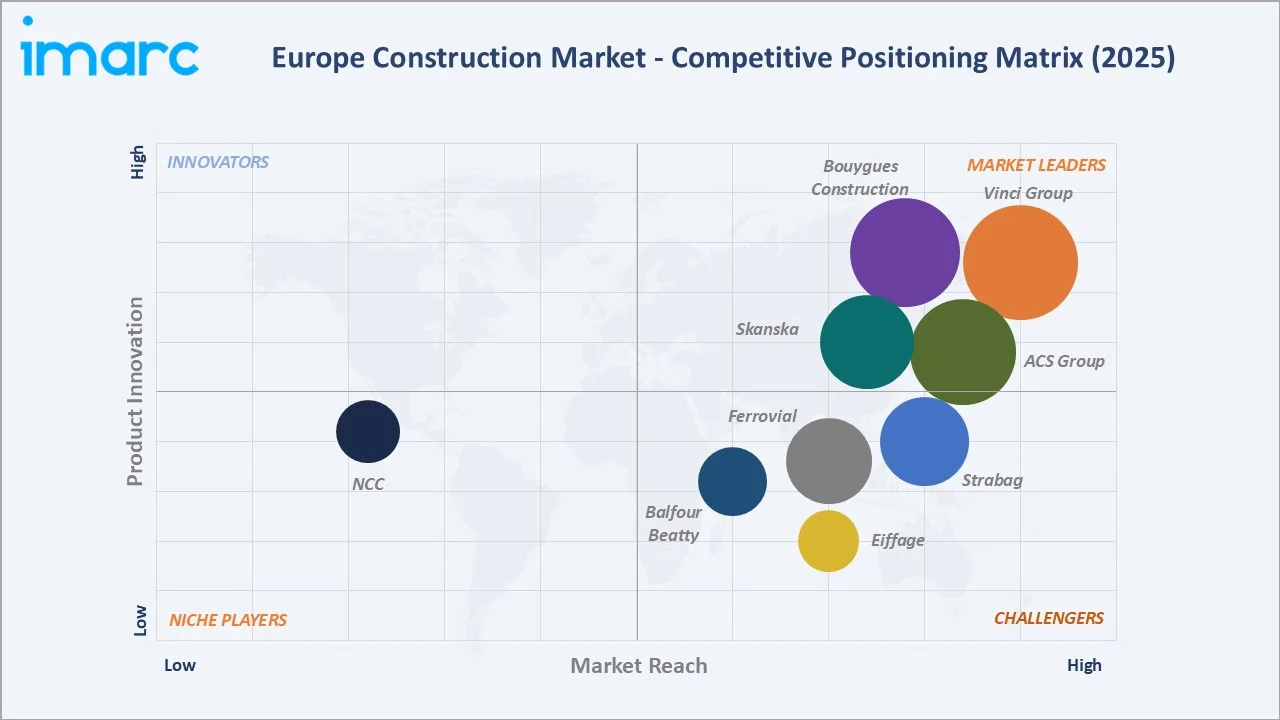

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Vinci Group |

Vinci Construction, Vinci Immobilier |

Leader |

Concessions-plus-construction model, global scale, energy transition expertise |

|

ACS Group |

ACS Group |

Leader |

Global infrastructure leadership, Spanish base, North American reach |

|

Bouygues Construction |

Bouygues Construction |

Leader |

Buildings, civil works, and transport infrastructure across France and Europe |

|

Skanska |

Skanska |

Leader |

Nordic and UK leadership, sustainability and green-building credentials |

|

Strabag |

Strabag |

Challenger |

Strong CEE presence, transport and tunnelling expertise |

|

Ferrovial |

Ferrovial |

Challenger |

Toll-road and airport infrastructure, global footprint |

|

Balfour Beatty |

Balfour Beatty |

Challenger |

UK flagship contractor, HS2 and power-transmission delivery |

|

Eiffage |

Eiffage Construction |

Challenger |

Concessions and construction across France and Western Europe |

|

NCC |

NCC |

Emerging |

Nordic specialist, sustainability leadership, civil engineering |

The Europe construction market's competitive landscape is moderately fragmented, with pan-European powerhouses competing alongside strong national champions and specialist civil, rail, and energy contractors. Leading players compete on sustainability credentials, digital delivery capability, concessions integration, and balance-sheet capacity to underwrite large public-private partnerships. Strategic consolidation, particularly around renewables and digital-infrastructure capabilities, is reshaping the landscape through 2034.

Key Company Profiles

Vinci Group

Vinci Group is Europe's largest construction and concessions group, headquartered in Rueil-Malmaison, France. Founded in 1899, it operates across construction, concessions, and energies in more than 120 countries, with construction revenue anchored in France, the UK, Germany, and Central Europe.

- Product & Platform Portfolio: Vinci's construction portfolio spans Vinci Construction (buildings, civil works, specialist networks), Eurovia/Colas for roads, Vinci Energies for electrical and digital infrastructure, and Vinci Highways and Airports within its concessions business.

- Recent Developments: In 2025, Vinci expanded its energy-transition offer through targeted acquisitions in electrical engineering and continued delivery of the Grand Paris Express metro packages and HS2 UK civil works lots.

- Strategic Focus: Vinci's strategy centres on integrating construction with long-term concessions, scaling energy-transition services through Vinci Energies, and deepening its international infrastructure footprint across Europe, North America, and emerging markets.

ACS Group

ACS, Actividades de Construcción y Servicios, is a Madrid-headquartered global infrastructure group. It operates through Hochtief in Germany and Australia, Dragados in Spain and Latin America, and Turner in North America, with combined revenue in the top tier of global contractors.

- Product & Platform Portfolio: ACS's portfolio covers transport infrastructure, energy, buildings, and industrial services. Hochtief leads on airports, rail, and tunnelling; Dragados anchors Spanish and Latin American projects; and Cimic operates in Asia Pacific.

- Recent Developments: In 2025, ACS strengthened its position in data-centre and high-tech facility construction through Turner, and continued bidding on major European high-speed-rail and tunnelling lots.

- Strategic Focus: ACS's strategy emphasises high-complexity infrastructure, data-centre construction, and long-duration concessions, combined with active portfolio management to capture the energy transition and digital-infrastructure build-out.

Bouygues Construction

Bouygues Construction, a division of Bouygues Group, is headquartered in Guyancourt, France. It operates across buildings, civil works, and energy and services, with a strong domestic position and an international footprint across Europe, the UK, and selected emerging markets.

- Product & Platform Portfolio: Bouygues' portfolio includes Bouygues Bâtiment for commercial and residential construction, Bouygues Travaux Publics for major civil engineering, Colas for roads and rail, and Equans for multi-technical services.

- Recent Developments: In February 2025, Bouygues Construction continued delivery on Grand Paris Express metro packages, Hinkley Point C civil works, and several flagship hospital-construction schemes in France.

- Strategic Focus: Bouygues' strategy focuses on low-carbon buildings, modular construction through its WeLink platform, and expanding multi-technical services via Equans across France, the UK, Belgium, and the Netherlands.

Market Concentration Analysis

The Europe construction market exhibits moderate fragmentation. The top five groups - Vinci, ACS, Bouygues, Skanska, and Strabag - collectively account for 22-28% of regional construction revenue in 2025. The remaining market is distributed across national champions such as Ferrovial, Eiffage, Balfour Beatty, NCC, and a long tail of regional and specialist contractors operating in civil, rail, energy, and residential segments.

The market is experiencing a bifurcated dynamic. Tier-1 pan-European contractors are consolidating around concessions integration, sustainability credentials, and digital-delivery capability. Simultaneously, strong national champions in Germany, Italy, Poland, and the Nordics are defending domestic positions through local supply-chain depth and political proximity. This dual dynamic is intensifying competition across public-procurement, data-centre, and energy-transition segments through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Energy and Utility construction is the fastest-expanding sub-segment, propelled by REPowerEU, offshore-wind build-out, grid reinforcement, and hydrogen infrastructure, with a projected CAGR of 6.5-7.0% through 2030. Renovation and deep-retrofit activity is the second-fastest slice, supported by EPBD-aligned minimum energy-performance standards and the Renovation Wave strategy targeting 35 million building units by 2030.

Emerging Country Expansion

Poland, Romania, and the Western Balkans represent the highest-potential emerging construction markets in Europe, underpinned by EU cohesion funds, transport-corridor investment, and residential expansion. The Nordics remain strategic for offshore wind, data centres, and modular residential construction, while Spain, Italy, and Greece continue to attract logistics, renewables, and tourism-infrastructure capital.

Venture and Strategic Investment Trends

Strategic investment is concentrating around construction-technology, modular, and decarbonised-materials players. Vinci, Skanska, and Ferrovial continue to invest in digital-delivery platforms and low-carbon concrete; private equity is actively deploying capital into European facilities-management and retrofit-services platforms; and corporate venture arms are backing robotics, AI scheduling, and sustainability-analytics start-ups through 2034.

Future Market Outlook (2026-2034)

The Europe construction market forecast projects steady value expansion from USD 3.72 Trillion in 2025 to USD 5.63 Trillion by 2034 at a CAGR of 4.70%. Germany, the UK, and France will retain their combined majority of European output, while Southern European and CEE markets will outpace the regional average on the back of PNRR, France 2030, and EU cohesion-funded programmes.

Three key shifts will reshape the Europe construction market through 2034. First, the Renovation Wave and EPBD will embed deep-retrofit activity as a structural long-duration demand layer across residential and commercial stock. Second, industrialised construction - modular, prefabricated, and digitally delivered - will move from early adoption to the default delivery mode for mid-rise housing, education, and healthcare. Third, the energy transition will transform construction portfolios, with offshore wind, grid reinforcement, nuclear new-build, and hydrogen infrastructure becoming structural revenue engines for tier-1 and specialist contractors.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with construction industry stakeholders, including senior executives at tier-1 and tier-2 contractors, procurement directors at public infrastructure agencies, product managers at leading building-materials producers, and institutional investors in European real-estate and infrastructure funds. Primary insights validated market sizing, sector segmentation, and technology-adoption timelines.

Secondary Research

Secondary sources include Eurostat construction output and short-term statistics, EU Commission Directorates-General (ENER, GROW, MOVE, REGIO), European Construction Industry Federation (FIEC), national statistics offices (Destatis, ONS, INSEE, ISTAT, INE), International Energy Agency (IEA), OECD infrastructure data, company annual reports, and trade publications including Construction Europe, ENR Europe, and Building magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, public-investment pipelines, urbanisation indices, housing-completion data, infrastructure project databases, and historical market-evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for monetary-policy, energy-price, and regulatory uncertainty.

Europe Construction Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Commercial Construction, Residential Construction, Industrial Construction, Infrastructure (Transportation) Construction, Energy and Utility Construction |

| Countries Covered | Germany, United Kingdom, France, Italy, Russia, Spain, Netherlands, Switzerland, Poland, Others |

| Companies Covered | Vinci Group, ACS Group, Bouygues Construction, Skanska, Strabag, Ferrovial, Balfour Beatty, Eiffage, NCC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Construction Market Report

The Europe construction market was valued at USD 3.72 Trillion in 2025, driven by urbanization, the EU Recovery and Resilience Facility, infrastructure modernization, and the accelerating renovation wave across the building stock.

The market is projected to reach USD 5.63 Trillion by 2034, growing at a CAGR of 4.70% during 2026-2034, supported by public-investment pipelines, EU Green Deal mandates, industrial reshoring, and the scale-up of modular and prefabricated construction.

Residential construction leads with a 38.0% share in 2025, driven by urban housing shortages, affordable-housing programmes, build-to-rent investment, and deep-retrofit activity tied to energy-performance regulations.

Commercial construction is the second-largest sector at 24.6% share in 2025, propelled by logistics expansion, data-centre capacity additions, healthcare and hospitality pipelines, and net-zero office retrofits.

Germany dominates with a 25.0% share in 2025, supported by the EUR 500 billion federal special infrastructure fund, KfW-backed residential retrofit, and a strong industrial and data-centre pipeline. The United Kingdom (16.8%) and France (14.7%) follow.

Key drivers include the EU Green Deal and Fit for 55, the Recovery and Resilience Facility (EUR 723.8 billion), REPowerEU, the Renovation Wave targeting 35 million building units, urbanization and housing deficits, and the scale-up of modular and digital construction.

Major players include Vinci Group, ACS Group, Bouygues Construction, Skanska, Strabag, Ferrovial, Balfour Beatty, Eiffage, and NCC.

The Europe construction market was valued at USD 2.96 Trillion in 2020 and USD 3.72 Trillion in 2025, reflecting a resilient historical CAGR of approximately 4.6% over 2020-2025 despite pandemic, energy-price, and monetary headwinds.

Key opportunities include deep-retrofit and renovation services, offshore wind and grid reinforcement, data-centre construction across FLAP-D markets, battery and semiconductor gigafactories, modular and prefabricated housing, and low-carbon materials and digital-delivery platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)