Europe Conveyor Belt Market Size, Share, Trends and Forecast by Type, End Use, and Country 2026-2034

Europe Conveyor Belt Market Size, Share, Trends & Forecast (2026-2034)

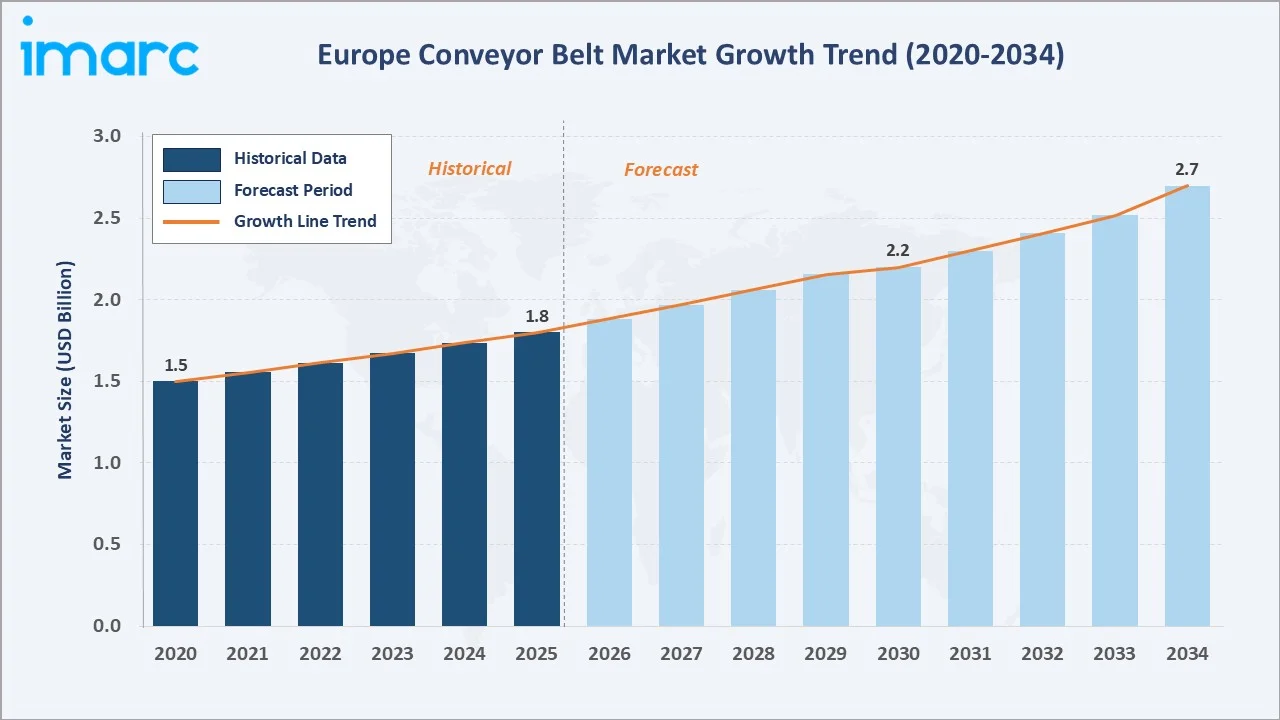

The Europe conveyor belt market size reached USD 1.8 Billion in 2025 and is projected to reach USD 2.7 Billion by 2034, exhibiting a CAGR of 4.10% during 2026-2034. Rising adoption of automation and Industry 4.0 technologies across German manufacturing, increasing mining activity across Eastern and Southern Europe, and growing e-commerce logistics infrastructure are the primary forces driving Europe conveyor belt market growth.

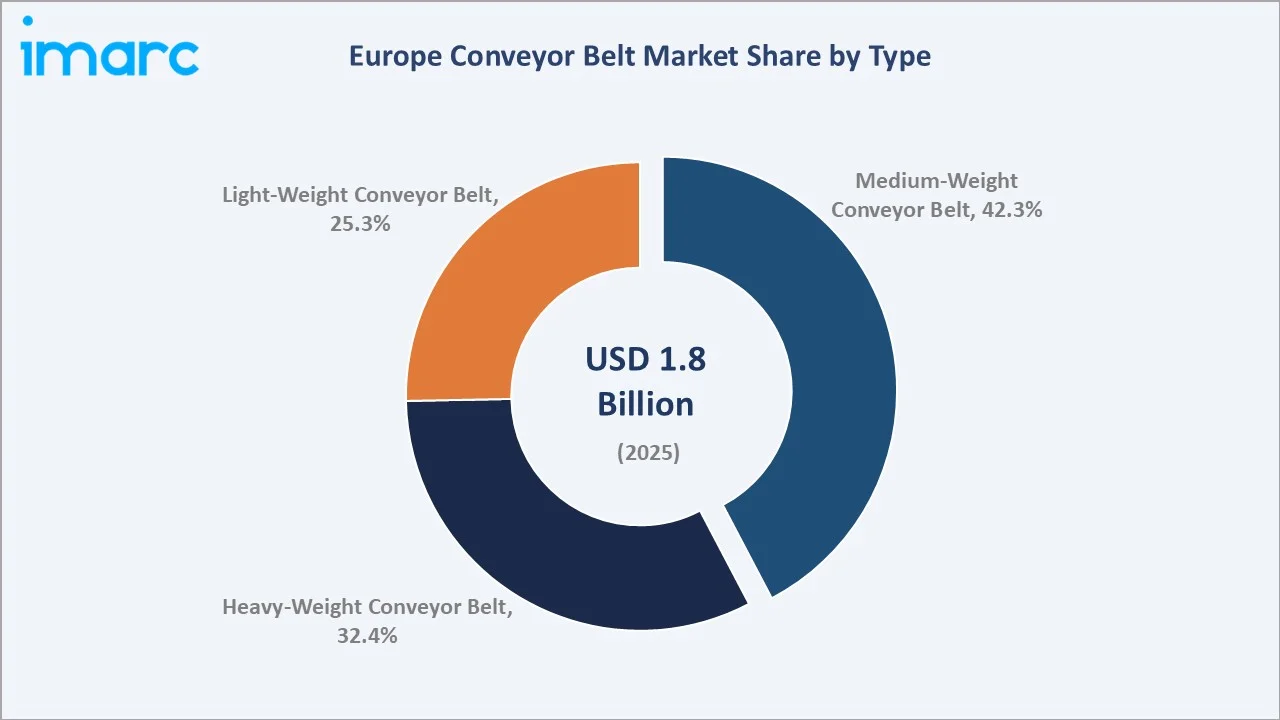

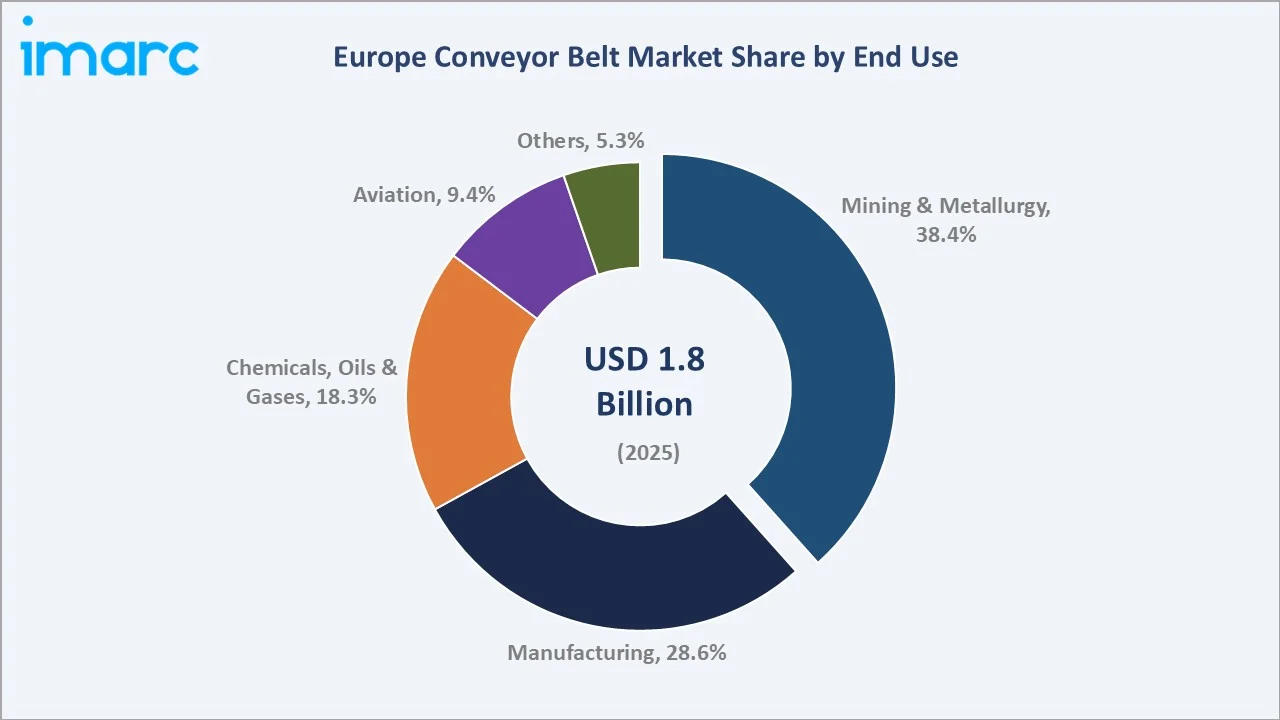

Medium-weight conveyor belt dominates the type mix at 42.3% in 2025, while mining and metallurgy leads the end-use segment at 38.4%. Germany commands a dominant 28.4% country share in 2025, reflecting its position as Europe's largest industrial economy.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.8 Billion |

|

Forecast Market Size (2034) |

USD 2.7 Billion |

|

CAGR (2026-2034) |

4.10% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (28.4% share, 2025) |

|

Second Country |

United Kingdom (20.6% share, 2025) |

|

Leading Type |

Medium-Weight Conveyor Belt (42.3%, 2025) |

|

Leading End Use |

Mining and Metallurgy (38.4%, 2025) |

To get more information on this market, Request Sample

The Europe conveyor belt market growth trajectory from 2020 through 2034, with historical expansion to USD 1.8 Billion in 2025, reflects consistent industrial-driven demand, while the forecast to USD 2.7 Billion captures accelerating automation investment, mining sector expansion, and Germany-led industrial reinvestment cycles.

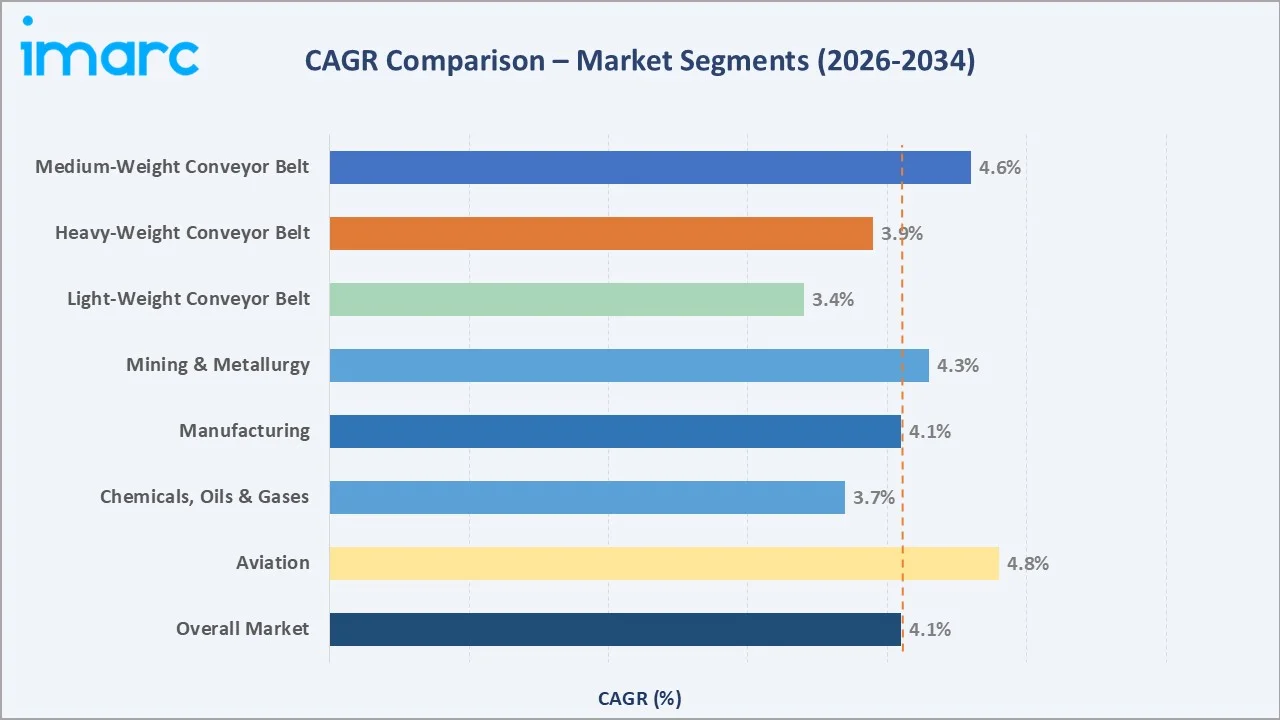

The CAGR trajectories across key type, end-use, and country sub-segments, with aviation at ~4.8% CAGR and medium-weight conveyor belts at ~4.6% CAGR, are the fastest-growing categories within the Europe conveyor belt industry analysis through 2034.

Executive Summary

The Europe conveyor belt market is on a sustained growth trajectory from USD 1.8 Billion in 2025 to USD 2.7 Billion by 2034. Conveyor belts, essential material-handling components deployed across mining operations, manufacturing plants, airport baggage systems, and chemical processing facilities, benefit from the non-discretionary nature of industrial infrastructure demand.

Medium-weight conveyor belt dominates type at 42.3% in 2025, owing to its broad applicability across general manufacturing and logistics. Heavy-weight conveyor belt (32.4%) commands premium positioning in mining and bulk material transport, growing robustly as European mining output expands. Light-weight conveyor belt (25.3%) serves food processing, packaging, and electronics manufacturing at the fastest material CAGR.

Germany dominates at 28.4% in 2025, reflecting its position as Europe's manufacturing and automotive powerhouse. The United Kingdom (20.6%) and France (18.3%) follow, driven by logistics automation, aviation expansion, and chemical processing industries.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Medium-Weight Conveyor Belt – 42.3% share (2025) |

|

Leading End Use |

Mining and Metallurgy – 38.4% share (2025) |

|

Leading Country |

Germany – 28.4% revenue share (2025) |

|

Second Country |

United Kingdom – 20.6% revenue share (2025) |

|

Top Companies |

Continental AG, Habasit, Semperit AG Holding, Forbo Movement Systems, Bando Chemical Industries, LTD. |

Key Analytical Observations Supporting the Above Data:

- Medium-weight conveyor belt, with 42.3% in 2025, dominates because of its versatility across general manufacturing, food processing, logistics, and packaging applications, offering the optimal balance of durability and cost for the broadest range of European industrial specifications.

- Mining and metallurgy end use, with 38.4% in 2025, leads because European mining output, particularly in iron ore, copper, coal, and potash, requires heavy-duty continuous conveying systems that are operationally irreplaceable, with uptime directly tied to extraction throughput.

- Germany's 28.4% dominance in 2025 reflects multiple structural forces: the world's third-largest automotive production base, a dense machinery and equipment manufacturing sector, and the highest per-capita industrial robot density in Europe, all generating sustained conveyor belt demand.

- The United Kingdom, with 20.6% in 2025, benefits from a growing logistics and e-commerce infrastructure, Heathrow's expansion-linked baggage handling upgrades, and post-Brexit reshoring of manufacturing capacity stimulating domestic conveyor procurement.

Europe Conveyor Belt Market Overview

A conveyor belt is a continuous loop of material carried on a series of pulleys that transports goods, materials, or components between two points in an industrial or commercial setting. Product configurations span light-weight fabric belts, medium-weight multi-ply rubber belts, and heavy-weight steel cord belts, each defined by tensile strength, temperature resistance, cover compound, and belt width.

The European ecosystem integrates polymer and rubber raw material suppliers, belt manufacturing facilities, surface treatment and splicing service providers, industrial distributors and steel service centers, EPC and installation contractors, and diverse end-use industries spanning mining, manufacturing, chemicals, aviation, and logistics.

Market Dynamics

To evaluate market opportunities, Request Sample

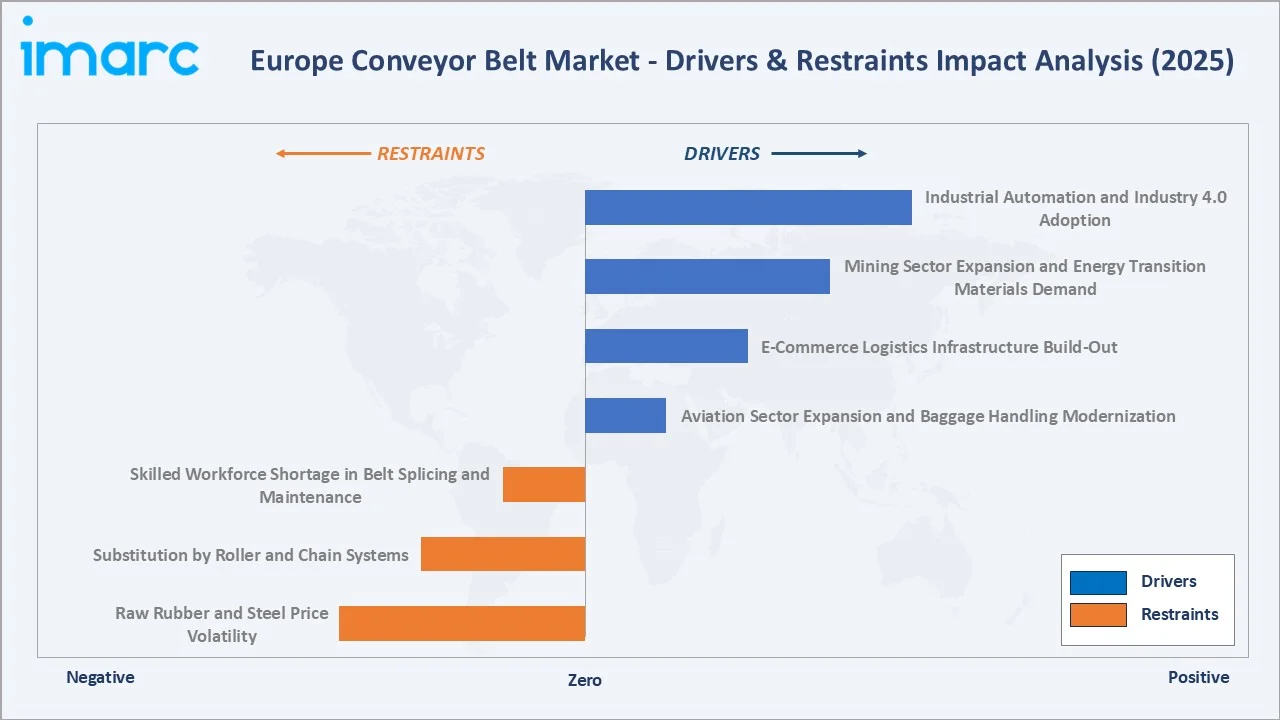

Market Drivers

- Industrial Automation and Industry 4.0 Adoption: Germany's Industrie 4.0 framework and EU-wide smart manufacturing investment are integrating IoT-enabled conveyor systems into production lines, increasing replacement cycle frequency as manufacturers upgrade legacy belts to smart-sensor-equipped systems with predictive maintenance capability.

- Mining Sector Expansion and Energy Transition Materials Demand: European critical mineral mining for EV batteries and renewable energy infrastructure, particularly in Scandinavia, Poland, and the Iberian Peninsula, is driving demand for heavy-duty conveyor belts in underground and open-cast mining operations processing copper, lithium, cobalt, and iron ore.

- E-Commerce Logistics Infrastructure Build-Out: EU e-commerce revenue surpassed EUR 887 billion in 2024, generating sustained demand for lightweight and medium-weight conveyor systems in fulfillment centers, parcel sorting facilities, and last-mile logistics hubs operated by Amazon, DHL, and regional retail chains.

- Aviation Sector Expansion and Baggage Handling Modernization: European airport capacity expansion programs, including expansions at Heathrow, Frankfurt, and Charles de Gaulle airports, are integrating next-generation baggage handling conveyor systems featuring improved energy efficiency, modular reconfiguration, and RFID tracking integration.

Market Restraints

- Raw Rubber and Steel Price Volatility: European conveyor belt manufacturers are exposed to global natural rubber price swings and European steel price cycles, impacting production cost predictability. Supply chain disruptions from geopolitical events and shipping bottlenecks amplify material cost uncertainty for belt manufacturers reliant on imported raw materials.

- Substitution by Roller and Chain Systems: In certain mining and bulk material handling applications, roller conveyor systems and chain-driven carriers compete effectively with belt conveyors, particularly where belt wear rates are high or where spillage containment is challenging, limiting belt penetration in specific heavy industrial sub-segments.

Market Opportunities

- Smart Belt Monitoring and Predictive Maintenance Services: The deployment of embedded sensor technologies, including belt condition monitoring via vibration analysis, thermal imaging, and strain gauging, is creating a recurring software-and-services revenue stream for belt manufacturers offering condition-based maintenance contracts alongside physical belt supply.

- Sustainable and Recycled-Material Conveyor Belts: EU circular economy regulations, EPR frameworks, and corporate sustainability commitments are creating demand for conveyor belts manufactured with recycled rubber content, bio-based polymers, and low-carbon production processes, allowing manufacturers to command premium pricing in ESG-conscious procurement.

Market Challenges

- CBAM and Carbon Cost Impact on Steel Cord Belt Supply Chains: The EU's Carbon Border Adjustment Mechanism will impose carbon costs on steel imports from high-emission origins, affecting the cost competitiveness of steel cord conveyor belts that depend on imported steel wire from non-EU suppliers with higher carbon intensities.

- Skilled Workforce Shortage in Belt Splicing and Maintenance: The specialized skills required for hot-vulcanized belt splicing and conveyor system maintenance are in short supply across Europe's aging industrial workforce, creating service capacity constraints and increasing turnaround times for belt replacement programs in mining and manufacturing.

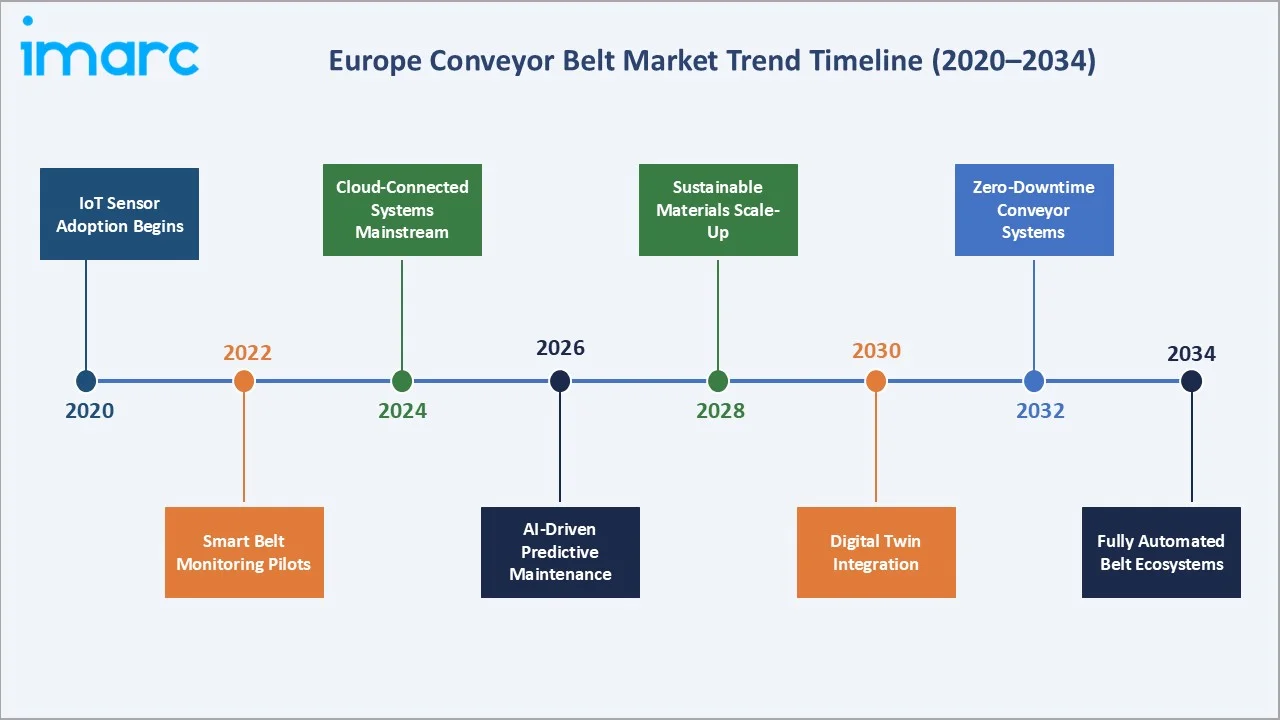

Emerging Market Trends

1. Cloud-Connected Smart Conveyor Systems Reshaping Operations

The integration of IoT sensors and cloud connectivity into conveyor systems is transforming real-time operational monitoring across Europe's industrial sectors. Smart belt systems track speed, load weight, power draw, and wear parameters continuously, enabling remote diagnostics and predictive maintenance scheduling that reduces unplanned downtime by 30-40%.

2. Sustainable and Recycled-Content Belt Materials

European belt manufacturers are increasingly incorporating recycled rubber, bio-based polymers, and low-carbon fabric composites into belt production, driven by EU circular economy regulations and corporate ESG commitments. Eco-certified belts are gaining specification preference in food processing, logistics, and public-sector procurement across Germany, the Netherlands, and Scandinavia.

3. Modular Conveyor Systems for Lean Manufacturing

Lean manufacturing principles are driving adoption of modular, reconfigurable conveyor systems across automotive, electronics, and packaging sectors. Plug-and-play conveyor modules that can be rearranged without specialized tooling reduce changeover times and support just-in-time manufacturing objectives, particularly in flexible assembly lines across Germany and Czech Republic.

4. Underground Mining Belt Technology Advancement

European underground mining operations are adopting next-generation steel cord conveyor belts with integrated fire-resistant compounds, anti-static properties, and real-time belt tension monitoring. The transition to higher-capacity belts reduces the number of belt sections required in long-haul underground mine tunnels, improving operational efficiency and safety compliance.

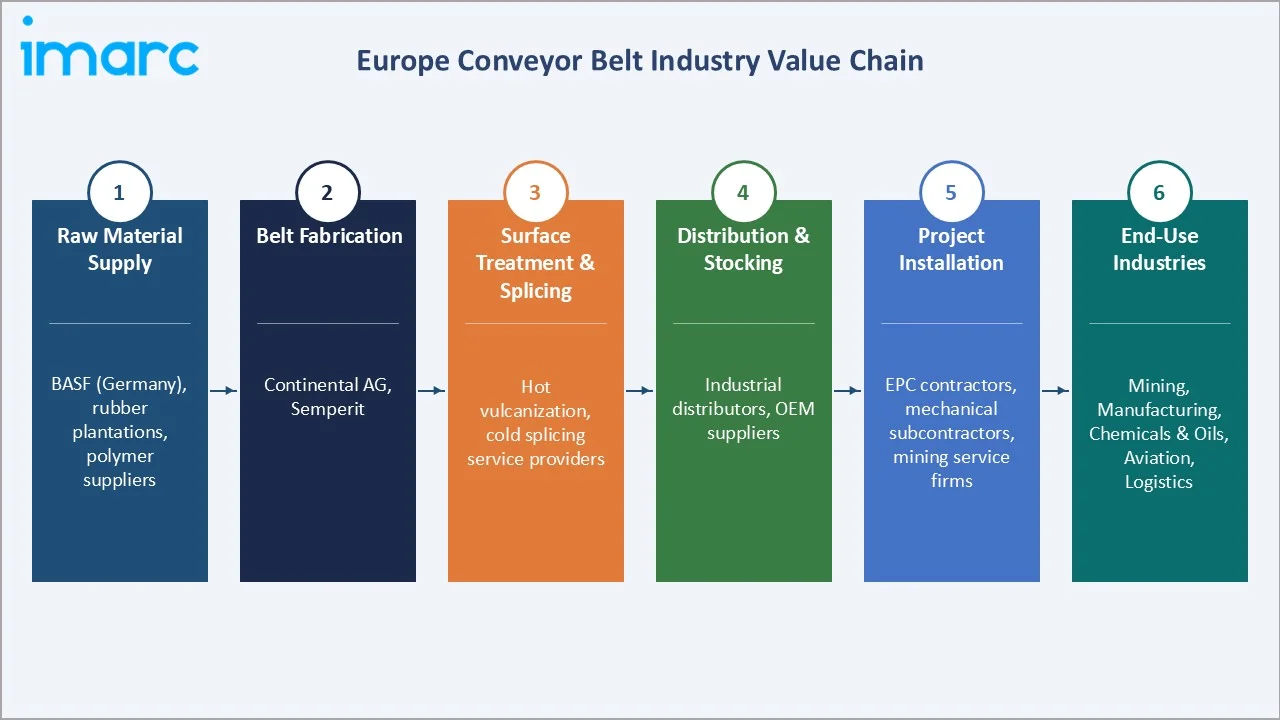

Industry Value Chain Analysis

The European conveyor belt value chain spans six stages from raw material procurement through end-use installation. Belt fabrication and compound development capture the highest value-add margins, while distribution logistics and project-specific splicing services generate significant working capital requirements favoring vertically integrated manufacturers with captive service capabilities.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

BASF (Germany); rubber plantations; polymer suppliers |

|

Belt Fabrication |

Continental AG, Semperit |

|

Surface Treatment & Splicing |

Hot vulcanization; cold splicing service providers |

|

Distribution & Stocking |

Industrial distributors, OEM suppliers |

|

Project Installation |

EPC contractors, mechanical subcontractors, mining service firms |

|

End-Use Industries |

Mining, Manufacturing, Chemicals & Oils, Aviation, Logistics |

Integrated belt manufacturers with captive compounding capabilities and in-house vulcanization infrastructure, such as Continental AG's integrated polymer and steel cord sourcing model, achieve lower unit cost structures than processors reliant on spot market rubber procurement, providing meaningful competitive advantage in commodity belt market segments.

Technology Landscape in the Europe Conveyor Belt Industry

Belt Compounding and Vulcanization Technology

Modern European conveyor belt production employs advanced rubber compounding lines using Banbury mixers and continuous twin-screw extruders to produce consistent cover compound formulations. Hot-vulcanization in belt presses operating at 150-160°C and 1.5-2.0 MPa produces metallurgically bonded belt joints achieving 95%+ of the parent belt tensile strength, the industry gold standard for mining belt splicing.

Steel Cord and High-Tensile Fabric Reinforcement

Steel cord conveyor belts using high-carbon steel wire cords of 2.5-10mm diameter achieve tensile strengths from ST 500 to ST 10000 N/mm, enabling single-flight conveyor distances exceeding 30km in modern open-cast mining operations. High-strength polyester-polyamide (EP) fabric belts provide tensile ratings to EP 2000/4 for medium-heavy-duty applications at significantly lower belt mass than steel cord alternatives.

Digital Belt Monitoring and BIM Integration

Leading European belt manufacturers are investing in belt condition monitoring systems embedding inductive sensors at splice joints and cover wear measurement arrays that transmit data via OPC-UA protocols to plant maintenance management systems. Continental's ContiSense technology embeds sensors directly into belt body rubber, enabling real-time temperature and wear monitoring without external sensor installation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Medium-Weight Conveyor Belt |

42.3% |

2025 |

|

End Use |

Mining and Metallurgy |

38.4% |

2025 |

|

Country |

Germany |

28.4% |

2025 |

By Type

To access detailed market analysis, Request Sample

Medium-weight conveyor belt commands a 42.3% majority share in 2025, owing to its fundamental applicability across general manufacturing, food processing, logistics, and packaging applications. The cost-performance balance of multi-ply EP fabric belts makes medium-weight the default specification across the broadest range of European industrial applications.

Heavy-weight conveyor belt at 32.4% in 2025 is irreplaceable in mining, quarrying, and bulk material handling where high-tensile steel cord construction withstands the severe mechanical impact of loading ore, aggregate, and coal. The substantial per-unit value of heavy belts generates revenue significance disproportionate to unit volume share.

Light-weight conveyor belt (25.3%) serves food processing, electronics, and express parcel applications where FDA-compliant cover compounds and precise belt tracking are critical specification requirements.

By End Use

Mining and metallurgy end use dominates at 38.4% in 2025, reflecting Europe's sustained demand for conveyor belts in iron ore, coal, copper, salt, and potash mining operations, along with steel and aluminum production facilities that use belt conveyors for raw material feeding and finished product handling across integrated plant layouts.

Manufacturing at 28.6% in 2025 spans automotive assembly, electronics, food and beverage processing, and machinery production, all highly dependent on precision conveyor systems for production line synchronization. Chemicals, oils and gases (18.3%) require specialized oil-resistant, chemical-resistant, and antistatic conveyor belt compounds for safe material handling in hazardous environments. Aviation (9.4%) covers airport baggage handling conveyor systems, growing as European airports invest in capacity expansion and system modernization. Others (5.3%) includes retail logistics, postal sorting, and agri-food processing.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

28.4% |

Strong automotive and machinery sector; high automation adoption; export-driven manufacturing |

|

United Kingdom |

20.6% |

Mining & logistics; post-Brexit industrial reshoring; airport baggage handling upgrades |

|

France |

18.3% |

Aerospace supply chain demand; TGV rail infrastructure; chemical processing industry |

|

Italy |

14.2% |

Food processing sector; marble and quarrying industry; precision manufacturing |

|

Spain |

10.4% |

Agri-food exports; port logistics expansion; mining activity in Iberian Peninsula |

|

Others |

8.1% |

Poland, Netherlands, Belgium – growing manufacturing and logistics hubs |

Germany's 28.4% market dominance in 2025 is driven by the highest concentration of industrial conveyor belt end-users in Europe. Germany's automotive production base of 3.9 million vehicles annually, machinery exports exceeding EUR 225 billion, and chemical industry output from BASF, Bayer, and Evonik all generate high belt consumption in assembly, processing, and logistics.

The United Kingdom, with 20.6% in 2025, is experiencing conveyor belt demand growth from expanding logistics and fulfillment infrastructure, ongoing airport modernization programs, and resurgent mining activity in Scotland and Wales. France's 18.3% share reflects demand from aerospace supply chains, high-speed rail infrastructure maintenance, and agri-food processing industries across the Loire Valley and Normandy.

Competitive Landscape

The Europe conveyor belt market is moderately fragmented, with regional leaders holding strong positions in their home markets while several large global suppliers compete across multiple geographies. Germany and Austria are home to Europe's most technically advanced belt manufacturers, while UK and Swiss companies lead in specialty and food-grade applications.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Continental AG |

Conveyor Belts, Steel Cord Belts, Textile Conveyor Belts, Pipe Conveyor Belts |

Leader |

Pan-European leader; automotive & mining; advanced belt technologies |

|

Habasit |

Fabric-Based Conveyor Belts, Timing Belts, Modular Plastic Belts |

Leader |

Swiss precision; food-grade belts; global distribution network |

|

Semperit AG Holding |

Steel Belts, Textile Belts, Pipe Conveyor Belts |

Challenger |

Austria-based; bulk material handling; cement & power plants |

|

Forbo Movement Systems |

Light-Weight Conveyor Belts, Flat Belts, Timing Belts |

Challenger |

Logistics & packaging; airport conveyor systems |

|

Bando Chemical Industries, LTD. |

Rubber Conveyor Belts, Light-Weight Belts, Timing Belts |

Emerging |

Japan-origin; European expansion; light manufacturing focus |

Key players include Continental AG, Habasit, Semperit AG Holding, Forbo Movement Systems, Bando Chemical Industries, LTD., and others.

Key Company Profiles

Continental AG

Continental AG is one of the Europe's largest conveyor belt manufacturer, headquartered in Hanover, Germany. Its ContiTech division produces the full range of textile, steel cord, and specialty conveyor belts, serving mining, industrial, and logistics markets globally with product ranges certified to DIN, ISO, and EN standards.

- Product Portfolio: Steel cord conveyor belts, textile conveyor belts, pipe conveyor belts, and underground mining belts with CONTISense embedded monitoring technology.

- Recent Developments: In February 2026, On February 2, 2026, Continental AG announced that it has finalized the sale of its ContiTech business unit, Original Equipment Solutions (OESL), to Regent L.P. The agreement for this transaction had originally been signed in August 2025. This divestment is part of Continental’s broader strategic initiative to strengthen its focus on industrial customers within the ContiTech division.

- Strategic Focus: Continental's strategy leverages its polymer science expertise and global distribution network to compete on total lifecycle cost across the full belt weight spectrum, while expanding its smart belt monitoring services portfolio to capture recurring software revenue streams alongside physical belt supply contracts.

Habasit

Habasit is a Swiss specialty conveyor belt manufacturer headquartered in Reinach, known for its precision fabric-based conveyor and processing belts serving food, pharmaceutical, and light manufacturing applications. The company maintains a global distribution network of 70+ affiliates.

- Product Portfolio: Fabric-based conveyor belts, plastic modular belts, and timing belts with food-grade FDA and EU-compliant cover compounds for hygienic processing applications.

- Recent Developments: In October 2025, Habasit introduced a new generation of folder-gluer belts designed to improve efficiency and reliability in packaging operations. Folder-gluer machines play a critical role in carton production by ensuring precise folding and accurate adhesive application, but they often face challenges such as belt wear, inconsistent grip, misalignment, and maintenance-related downtime.

- Strategic Focus: Habasit focuses on specification advantage in food safety and hygienic processing segments, where its FDA-compliant compound expertise, tight dimensional tolerances, and rapid custom-order delivery create defensible premium pricing over commodity Asian belt imports.

Semperit AG Holding

Semperit AG Holding, a division of the Semperit Group headquartered in Vienna, Austria, is a leading European manufacturer of conveyor belts with particular strength in steel cord and fabric belts for heavy-duty bulk material handling in mining, cement, and power generation applications.

- Product Portfolio: Steel cord conveyor belts, multi-ply fabric conveyor belts, pipe conveyor belts, and heat-resistant and oil-resistant specialty belts engineered for mining, cement production, power plants, and chemical processing applications across European and export market.

- Recent Developments: In August 2023, Semperit AG Holding announced the successful completion of its acquisition of the RICO Group, following all required regulatory approvals. The acquisition represents a key step in Semperit’s strategic growth plan, aimed at strengthening its position in industrial applications.

- Strategic Focus: Semperit differentiates on engineering depth and application-specific belt customization for extreme operating conditions, targeting European mine operators, cement producers, and power utilities where belt reliability, fire resistance certification, and total lifecycle cost performance take precedence over commodity pricing, while expanding its service and splicing capabilities to capture recurring maintenance revenue alongside physical belt supply contracts.

Market Concentration Analysis

The Europe conveyor belt market is moderately fragmented at the regional level, with no single company holding more than 12-15% of total European market revenue. Germany and Austria host Europe's largest specialized belt manufacturers, while the UK, Switzerland, and France are home to specialty segment leaders in food-grade, lightweight, and mining applications.

Consolidation is accelerating through strategic M&A, as demonstrated by the Michelin-Fenner and AMMEGA (Ammeraal-Megadyne) combinations. Private equity-backed consolidation of regional belt distributors and service companies is generating more integrated supply chain solutions for large industrial and mining customers across the continent.

Investment & Growth Opportunities

Fastest-Growing Segments

Aviation conveyor systems at ~4.8% CAGR through 2034 represent the highest-growth end-use segment, driven by European airport capacity expansion programs and the transition to fully automated baggage handling across hub airports. Light-weight conveyor belt at ~3.4% CAGR captures food processing and e-commerce logistics growth at attractive margins.

Emerging Country Markets

Poland and Czech Republic are the fastest-growing country markets within the "Others" grouping, driven by manufacturing nearshoring as European companies relocate production from Asia. Poland's expanding automotive components sector, logistics infrastructure, and coal mining output generate growing conveyor belt procurement across multiple end-use categories.

Venture & Investment Trends

Private equity interest in smart belt monitoring software platforms is growing alongside industrial IoT consolidation. EU Innovation Fund and Horizon Europe grants are supporting sustainable material R&D at belt manufacturers developing bio-based and recycled-content belt compounds, creating first-mover certification advantages in green procurement tenders across the European public sector and major industrial operators.

Future Market Outlook (2026-2034)

The Europe conveyor belt market is forecast to expand from USD 1.8 Billion in 2025 to USD 2.7 Billion by 2034 at a CAGR of 4.10%, adding USD 0.9 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's industrial infrastructure-linked, non-discretionary demand characteristics.

Three technological forces will most significantly shape the Europe conveyor belt landscape through 2034. Smart belt monitoring systems with embedded sensors and cloud connectivity will become standard specification for new belt installations in mining and manufacturing by 2028. Sustainable belt materials meeting EU circular economy requirements will capture a significant share of European belt procurement by 2030. Modular, AI-optimized conveyor configurations supporting flexible manufacturing and logistics will become the design standard for new European industrial facilities.

Research Methodology

Primary Research

Primary research encompassed structured interviews with European conveyor belt industry stakeholders, including senior commercial managers at belt manufacturers, mining procurement specialists, airport infrastructure managers, food processing plant engineers, and logistics automation integrators. Primary data validated market sizing, type and end-use segment shares, country demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Eurostat industrial production statistics, European Mining Association production data, IATA European air traffic data, EU Circular Economy Action Plan documentation, DIN and ISO conveyor belt standard publications, and trade publications including Bulk Solids Handling, Mining Technology, and Conveyor & Material Handling International.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, industrial production indices, mining output projections, logistics sector investment data, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

Europe Conveyor Belt Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Medium-Weight Conveyor Belt, Light-Weight Conveyor Belt, Heavy-Weight Conveyor Belt |

| End Uses Covered | Mining and Metallurgy, Manufacturing, Chemicals, Oils and Gases, Aviation, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Continental AG, Habasit, Semperit AG Holding, Forbo Movement Systems, Bando Chemical Industries, LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Conveyor Belt Market Report

The Europe conveyor belt market reached USD 1.8 Billion in 2025, reflecting consistent demand from industrial manufacturing, mining operations, aviation infrastructure, and e-commerce logistics across the continent.

The market is projected to reach USD 2.7 Billion by 2034, growing at a CAGR of 4.10% during 2026-2034. Growth is driven by accelerating industrial automation, critical minerals mining expansion, and logistics infrastructure investment across Europe.

Medium-weight conveyor belt leads with a 42.3% share in 2025. Its broad applicability across general manufacturing, food processing, logistics, and packaging applications makes it the default specification for the widest range of European industrial conveying requirements, offering the optimal balance of durability and cost-effectiveness.

Mining and metallurgy dominate with a 38.4% share in 2025, reflecting sustained demand for heavy-duty conveyor belts in iron ore, coal, copper, salt, and potash mining operations across Scandinavia, Poland, the United Kingdom, and the Iberian Peninsula, along with integrated steel and aluminum production facilities requiring continuous bulk material handling systems.

Germany leads with a 28.4% share in 2025, driven by its position as Europe's largest automotive, machinery, and chemical industry base. Germany's automotive production of approximately 3.9 million vehicles annually, machinery exports exceeding EUR 225 billion, and a dense industrial manufacturing ecosystem generate the continent's highest per-capita conveyor belt demand.

Key trends include the integration of IoT sensors and cloud-connected smart conveyor monitoring systems enabling predictive maintenance, the shift toward sustainable and recycled-content belt materials driven by EU circular economy regulations, the adoption of modular conveyor configurations supporting lean manufacturing principles, and the deployment of next-generation steel cord belts with embedded fire-resistant and anti-static compounds for underground mining applications.

The leading companies in the Europe conveyor belt market include Continental AG, Habasit, Semperit AG Holding, Forbo Movement Systems, Bando Chemical Industries, LTD., and others.

Key restraints include raw rubber and steel price volatility that creates input cost uncertainty for European belt manufacturers, competition from roller and chain conveyor systems in specific heavy industrial sub-segments, the EU Carbon Border Adjustment Mechanism imposing carbon costs on steel cord belt supply chains dependent on non-EU steel imports, and a shortage of skilled workers qualified in hot-vulcanized belt splicing and conveyor system maintenance across Europe's aging industrial workforce.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)