Europe Cybersecurity Market Size, Share, Trends and Forecast by Component, Deployment Type, User Type, Industry Vertical, and Country, 2026-2034

Europe Cybersecurity Market Size, Share, Trends & Forecast (2026-2034)

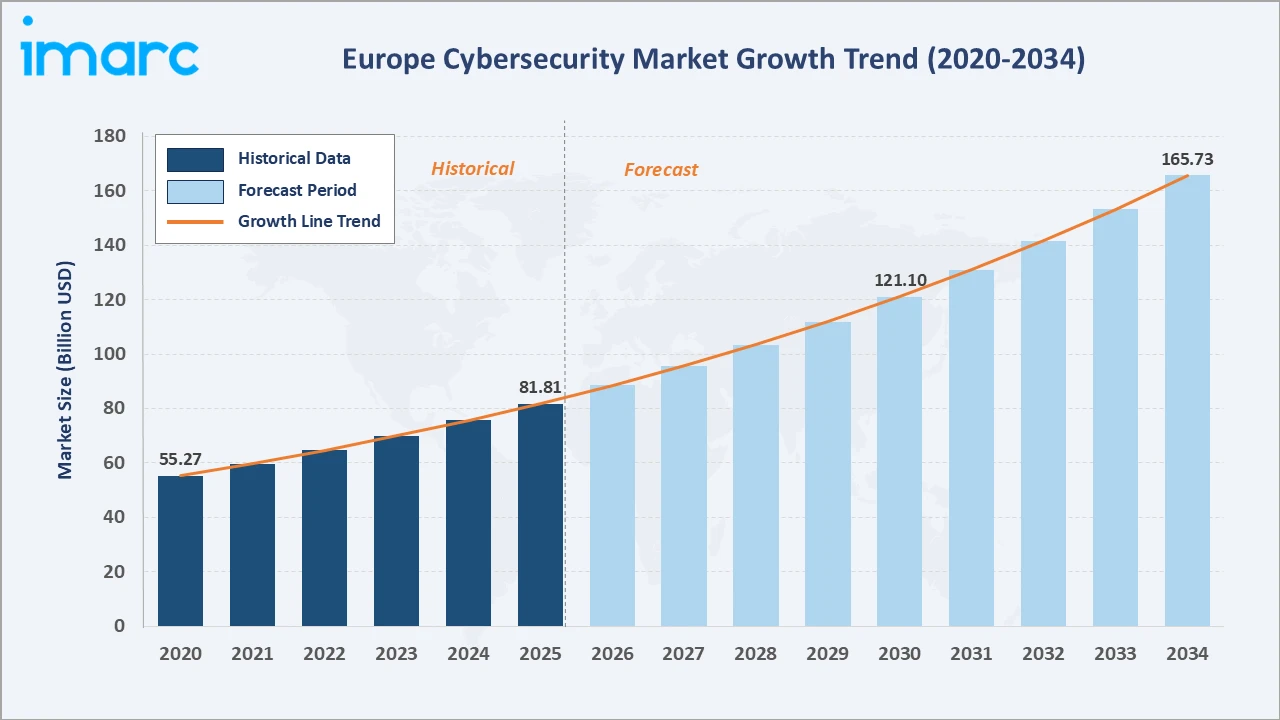

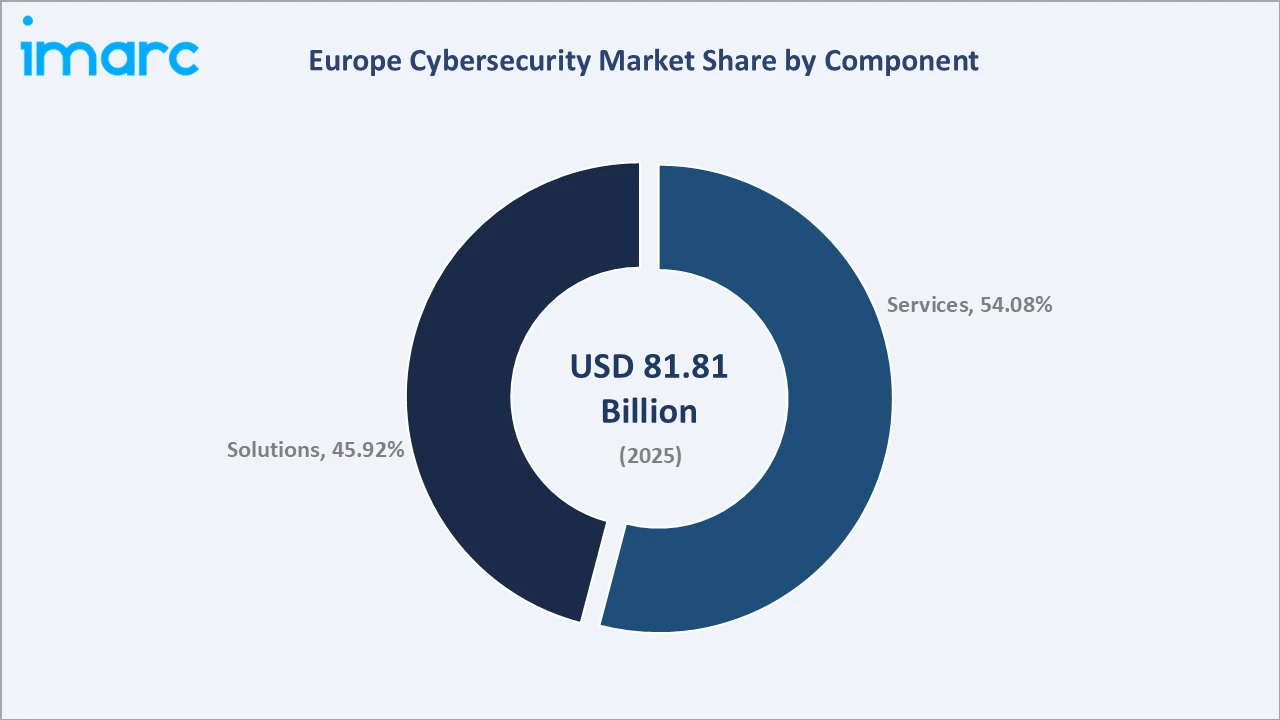

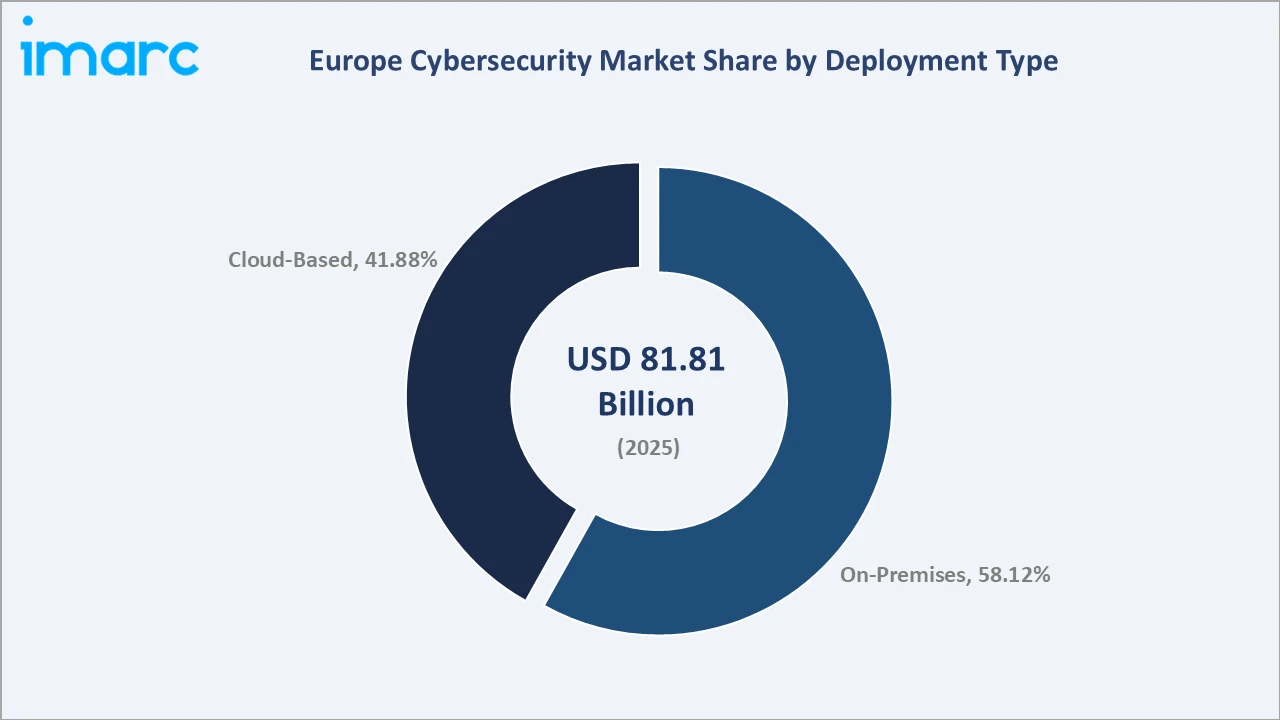

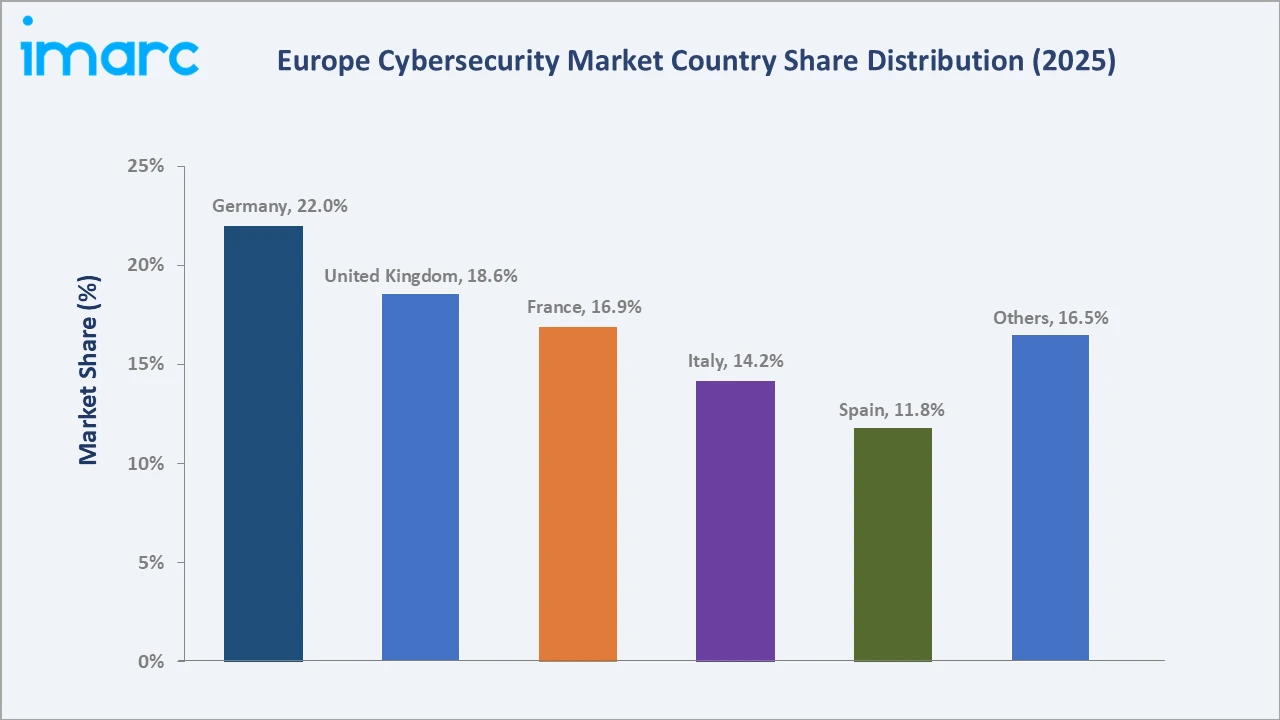

The Europe cybersecurity market reached USD 81.81 Billion in 2025 and is projected to reach USD 165.73 Billion by 2034, growing at a CAGR of 8.16% during 2026-2034. The market is driven by rising cyberattacks, stricter data protection regulations, and growing enterprise adoption of cloud, IoT, and digital payment systems. According to International Data Corporation (IDC), cybersecurity investments in Europe increased by around 12% in 2024, outperforming earlier projections by 1.6 percentage points. This rising spending is driving the Europe cybersecurity market by accelerating the adoption of advanced threat detection, cloud security, compliance solutions, and managed security services. Services lead component at 54.08%. On-premises dominates deployment at 58.12%. Germany leads regionally at 22.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 81.81 Billion |

|

Forecast Market Size (2034) |

USD 165.73 Billion |

|

CAGR (2026-2034) |

8.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Services (54.08%, 2025) |

|

Dominant Deployment Type |

On-premises (58.12%, 2025) |

|

Leading Country |

Germany (22.0%, 2025) |

Europe cybersecurity market expanded from USD 55.27 Billion in 2020 to USD 81.81 Billion in 2025, anchored at USD 121.10 Billion in 2030, and forecast to reach USD 165.73 Billion by 2034, supported by rising cyber threats, regulatory compliance needs, and rapid digital transformation across industries.

To get more information on this market, Request Sample

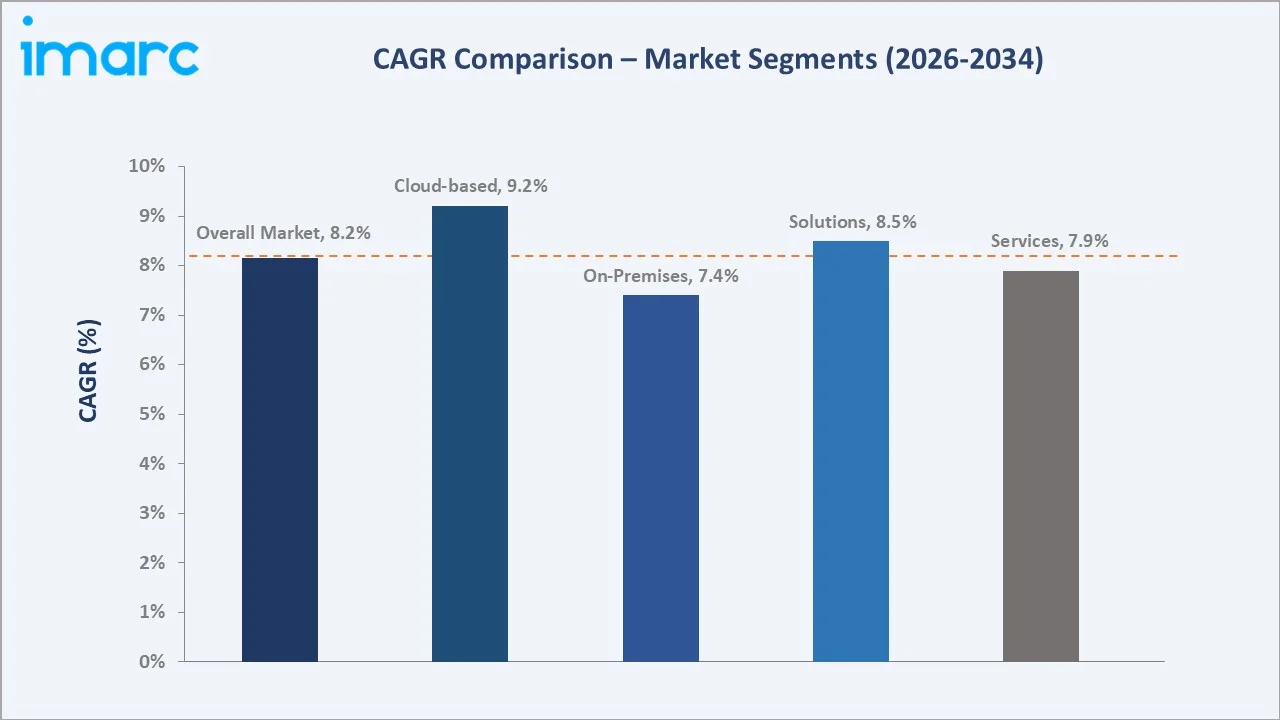

Cloud-based deployment grows fastest at ~9.2% CAGR through cloud-native application protection and SaaS security platform adoption. Solutions grow at ~8.5% CAGR through AI-native XDR and Zero Trust platform adoption, creating high CAGR through product category premium expansion.

Executive Summary

Europe cybersecurity market reached USD 81.81 Billion in 2025, driven by increasing cyberattacks, expanding digital infrastructure, and stricter regulatory frameworks. Organizations across sectors are investing heavily in cloud security, endpoint protection, identity management, and threat intelligence solutions to strengthen their security posture. The growing adoption of remote work, IoT devices, artificial intelligence, and digital payment systems is further accelerating demand for advanced cybersecurity technologies. Continued investments from both public and private sectors are expected to support sustained market expansion over the forecast period. The market is projected to reach USD 165.73 Billion by 2034.

Services at 54.08% leads through security consulting and incident response, creating Europe's most commercially recurring revenue model for security providers. On-premises at 58.12% serves critical infrastructure and government data sovereignty. Germany leads regionally at 22.0% through Europe's largest economy and most demanding regulatory framework.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Services - 54.08% share (2025) |

|

Dominant Deployment Type |

On-premises - 58.12% market share (2025) |

|

Leading Country |

Germany - 22.0% share (2025) |

|

Market Opportunity |

AI-native SOC-as-a-service; quantum-safe cryptography migration; critical infrastructure security; sovereign cloud security for European data residency; SME managed security subscription |

Key Analytical Observations Supporting the Above Data:

- Services at 54.08%: The services segment is dominant due to rising demand for managed security, consulting, compliance support, and incident response services. Many enterprises rely on external experts to manage complex threats, cloud security, and evolving regulatory requirements.

- On-premises at 58.12%: The on-premises segment is dominant, as large enterprises, government bodies, and regulated sectors prefer in-house control over sensitive data and security infrastructure. Strict compliance requirements and data sovereignty concerns further support on-premises deployment.

- Germany at 22.0%: Germany is dominant due to its strong industrial base, large enterprise IT spending, and high adoption of cybersecurity across manufacturing, automotive, BFSI, and government sectors. Rising Industry 4.0 adoption and strict data protection compliance further strengthen demand.

Europe Cybersecurity Market Overview

Europe cybersecurity market operates within the broader global cybersecurity market as one of the largest regional markets through Europe's combination of regulatory intensity, geopolitical threat environment, and enterprise cybersecurity maturity in Germany, the UK, and France.

The European cybersecurity ecosystem integrates global technology vendors, European technology champions, system integrators, and national cybersecurity authorities, creating the European threat landscape and cybersecurity certification framework. Macroeconomic factors include rapid digitalization, rising enterprise IT spending, growth in cloud-based businesses, and expanding cross-border digital trade.

Market Dynamics

To evaluate market opportunities, Request Sample

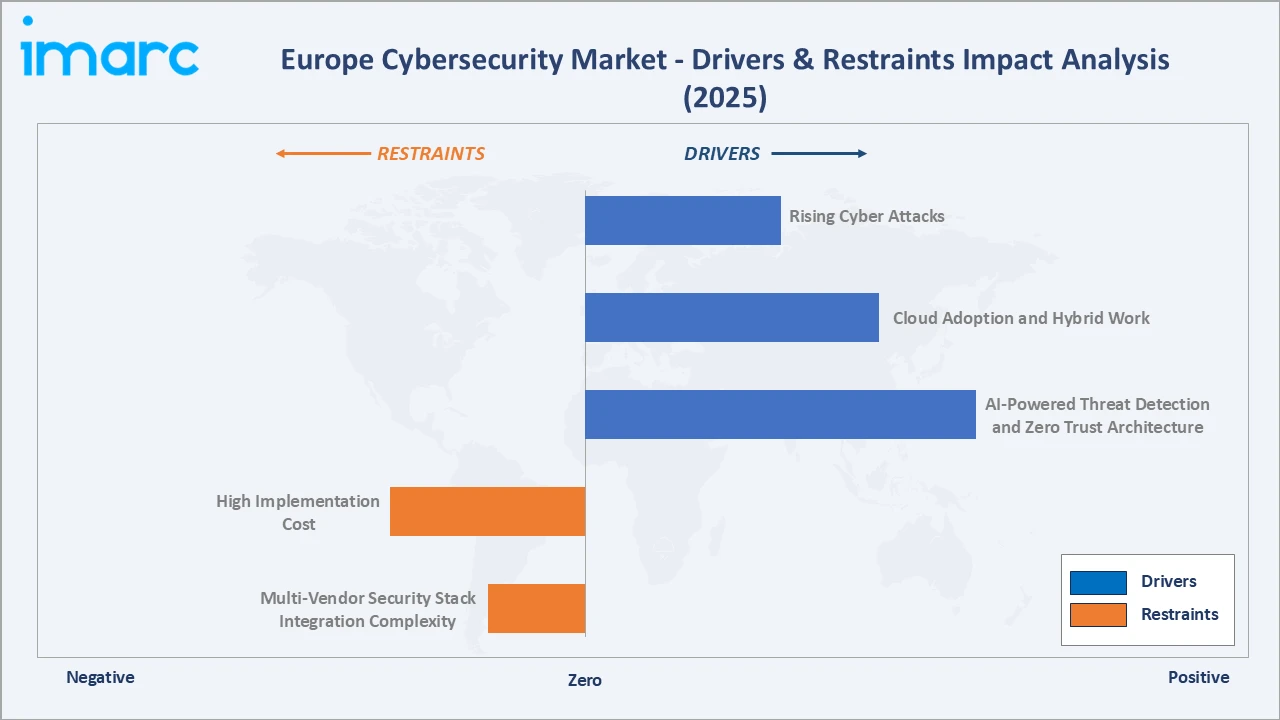

Market Drivers

- Rising Cyber Attacks: ENISA (European Union Agency for Cybersecurity) threat landscape analysed 4,875 incidents from 1 July 2024 to 30 June 2025. These rising cyberattacks are driving the market as businesses face growing risks of data breaches, ransomware, phishing, and financial fraud. This is pushing organizations to invest in advanced threat detection, endpoint protection, identity access management, and cloud security solutions. Critical sectors such as BFSI, healthcare, manufacturing, and government are increasing cybersecurity spending to protect sensitive data and operations. As attacks become more frequent and sophisticated, demand for managed security services and incident response solutions is also rising.

- Cloud Adoption and Hybrid Work: Cloud adoption and hybrid work are expanding the number of devices, networks, and applications that need protection. As employees access company systems remotely, businesses are investing in cloud security, identity access management, endpoint protection, and zero-trust solutions. Rising use of SaaS platforms and multi-cloud environments is also increasing demand for secure access, data protection, and threat monitoring tools. This shift is further boosting managed security services as companies seek continuous protection across distributed work environments.

- AI-Powered Threat Detection and Zero Trust Architecture: AI-powered threat detection and zero trust architecture are enabling faster identification of suspicious activities, malware, and insider threats. Zero trust models ensure continuous verification of users, devices, and applications, reducing risks in cloud and hybrid work environments. In June 2026, Filigran, a European open-source threat management firm, launched XTM One, an AI-native agentic layer designed to automate Continuous Threat Exposure Management workflows across its XTM Platform. By integrating OpenCTI and OpenAEV into one continuous workflow, the solution supports AI-powered threat detection and zero-trust adoption by improving real-time threat intelligence, exposure validation, and automated response capabilities across European enterprises.

Market Restraints

- High Implementation Cost: High implementation cost is hampering the market as advanced solutions require significant spending on software, hardware, skilled professionals, and ongoing maintenance. Small and medium enterprises often struggle to afford enterprise-grade tools such as zero trust, AI-based threat detection, and managed security services. Integration with legacy IT systems further increases deployment costs and complexity. As a result, budget constraints can delay cybersecurity adoption, especially among cost-sensitive organizations.

- Multi-Vendor Security Stack Integration Complexity: Multi-vendor security stack integration complexity is hampering the market as enterprises often use different tools for endpoint, cloud, network, identity, and threat monitoring. Managing these disconnected systems increases operational complexity, creates visibility gaps, and slows incident response. It also raises the need for skilled security teams and additional integration costs. As a result, some organizations delay adoption of advanced cybersecurity solutions or prefer limited deployments.

Market Opportunities

- Quantum-Safe Cryptography Migration: Quantum-safe cryptography migration is creating opportunities as organizations prepare for future risks from quantum computing. Enterprises, banks, governments, and critical infrastructure operators are expected to upgrade encryption systems to protect sensitive data and digital transactions. In May 2026, Adtran and euNetworks announced a partnership to launch Quantum Shield, a quantum-safe private connectivity service built using Adtran’s optical transport technology across euNetworks’ pan-European data center network. This supports the market by accelerating quantum-safe cryptography migration, creating demand for secure connectivity, encryption upgrades, and future-ready data protection solutions.

- Increasing Adoption of IoT, Industry 4.0, and Connected Devices: Increasing adoption of IoT, Industry 4.0, and connected devices is expanding the need to secure sensors, machines, networks, and industrial control systems. As factories, utilities, smart cities, and healthcare facilities become more connected, demand is rising for endpoint security, network monitoring, OT security, and threat detection solutions. This also supports growth in managed security services and zero-trust frameworks. Consequently, vendors can target industrial and critical infrastructure sectors with specialized cybersecurity offerings.

Market Challenges

- European Digital Sovereignty Tension: European digital sovereignty tension is challenging as organizations face pressure to balance security needs with requirements for local data storage, domestic technology adoption, and regulatory compliance. Differing national policies and concerns over reliance on non-European technology providers can complicate procurement and cybersecurity strategies. These factors may increase implementation costs, limit interoperability, and slow cross-border security deployments. As a result, businesses often face greater complexity when building unified cybersecurity frameworks across Europe.

- Limited Cybersecurity Budgets among Small and Medium-Sized Enterprises (SMEs): Limited cybersecurity budgets among SMEs are challenging, as smaller firms often cannot afford advanced tools, skilled teams, or managed security services. This slows adoption of solutions such as zero trust, cloud security, and AI-based threat detection. Many SMEs continue relying on basic security systems, increasing exposure to cyber risks. As a result, vendors face difficulty expanding penetration across cost-sensitive SME segments.

Emerging Market Trends

1. AI-Powered SOC Automation Reducing European Analyst Shortage Impact

AI-powered SOC automation reduces dependence on scarce cybersecurity analysts. Automated tools can detect threats, prioritize alerts, investigate incidents, and support faster response with minimal manual effort. This improves SOC efficiency and reduces alert fatigue across enterprises. As a result, European organizations are increasingly adopting AI-driven security operations platforms and managed SOC services.

2. SASE and Zero Trust Architecture Convergence

The convergence of Secure Access Service Edge (SASE) and zero trust architecture is emerging as organizations seek unified security for cloud, remote, and hybrid work environments. By combining network security, secure access, and continuous identity verification into a single framework, enterprises can improve visibility and reduce security gaps. This approach enhances protection for distributed users, applications, and devices while simplifying security management. Growing adoption of cloud services and stricter compliance requirements are further accelerating demand for integrated SASE and Zero Trust solutions across Europe.

3. OT and Industrial Cybersecurity Demand Acceleration

OT and industrial cybersecurity demand acceleration is emerging as manufacturers, utilities, and critical infrastructure operators increase digitalization and Industry 4.0 adoption. The growing connectivity of industrial control systems, IoT devices, and operational networks is expanding the cyberattack surface. Organizations are therefore investing in OT security, network segmentation, threat monitoring, and incident response solutions to protect critical operations. Rising concerns over ransomware attacks and infrastructure disruptions are further driving demand for specialized industrial cybersecurity technologies.

4. Expansion of Managed Detection and Response (MDR) Services

The expansion of Managed Detection and Response (MDR) services is emerging as organizations seek continuous threat monitoring and rapid incident response without building large in-house security teams. MDR providers offer round-the-clock detection, investigation, and remediation capabilities, helping businesses address increasingly sophisticated cyber threats. In March 2025, Integrity360 launched CyberFire MDR across its European markets, offering advanced threat detection, comprehensive incident response, and predictable pricing for organizations of all sizes. Built on its recent Nclose acquisition, the service already secures hundreds of thousands of endpoints with continuous, 24/7 cyber threat detection and response. The trend is particularly strong among SMEs facing cybersecurity talent shortages and budget constraints. Growing demand for outsourced security expertise is accelerating MDR adoption across Europe.

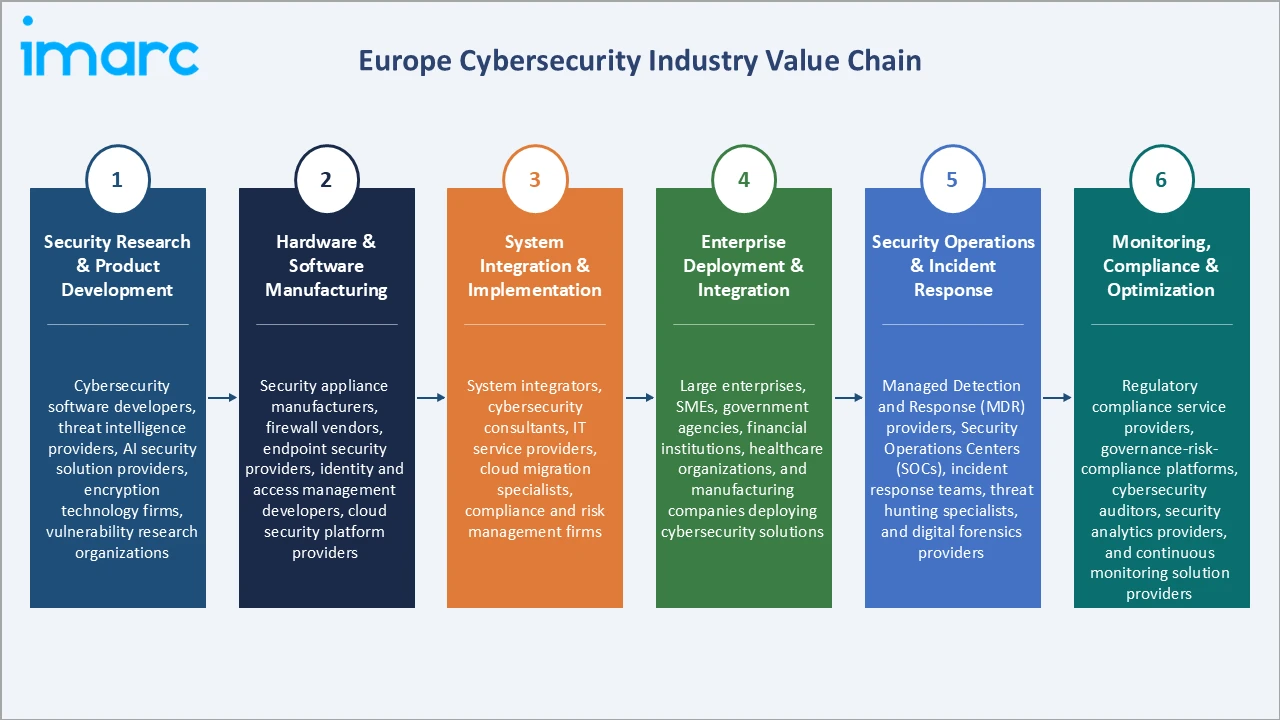

Industry Value Chain Analysis

Europe cybersecurity value chain integrates security research & product development, hardware & software manufacturing, system integration & implementation, enterprise deployment & integration, security operations & incident response, and monitoring, compliance & optimization.

|

Stage |

Key Participants |

|

Security Research & Product Development |

Cybersecurity software developers, threat intelligence providers, AI security solution providers, encryption technology firms, vulnerability research organizations |

|

Hardware & Software Manufacturing |

Security appliance manufacturers, firewall vendors, endpoint security providers, identity and access management developers, cloud security platform providers |

|

System Integration & Implementation |

System integrators, cybersecurity consultants, IT service providers, cloud migration specialists, compliance and risk management firms |

|

Enterprise Deployment & Integration |

Large enterprises, SMEs, government agencies, financial institutions, healthcare organizations, and manufacturing companies deploying cybersecurity solutions |

|

Security Operations & Incident Response |

Managed Detection and Response (MDR) providers, Security Operations Centers (SOCs), incident response teams, threat hunting specialists, and digital forensics providers |

|

Monitoring, Compliance & Optimization |

Regulatory compliance service providers, governance-risk-compliance platforms, cybersecurity auditors, security analytics providers, and continuous monitoring solution providers |

Security operations & incident response represent the most value-added stage in the Europe cybersecurity value chain, as organizations increasingly rely on continuous threat monitoring, advanced analytics, AI-driven detection, and rapid response services to combat evolving cyber threats and ensure regulatory compliance.

Technology Landscape in the Europe Cybersecurity Industry

AI and Machine Learning in Security Operations

AI and machine learning are enabling real-time threat detection, behavioral analytics, and automated incident response. These technologies help security teams identify anomalies, predict attack patterns, and prioritize high-risk threats more accurately. In May 2026, Bulgaria’s Information Services partnered with Google Cloud to enhance the country’s national cybersecurity infrastructure using AI and centralized threat intelligence. The initiative includes one of Europe’s first deployments of Google Cloud’s Cybershield solution, making Bulgaria a leading example of large-scale AI-based national cyber defense. As cyber threats become more sophisticated, organizations are increasingly adopting AI-driven security platforms to improve operational efficiency and cyber resilience.

Blockchain-Based Security Applications

Blockchain-based security applications provide decentralized and tamper-resistant methods for securing data, identities, and digital transactions. The technology enhances transparency, integrity, and traceability across digital ecosystems, reducing risks associated with fraud and unauthorized data modification. Organizations are increasingly exploring blockchain for identity management, secure information sharing, and supply chain security. Growing concerns around data privacy, cyber resilience, and digital trust are further encouraging blockchain-based cybersecurity innovations across Europe.

IoT and Connected Device Security Technologies

IoT and connected device security technologies are shaping the Europe cybersecurity industry as smart devices, sensors, and connected systems expand across homes, enterprises, healthcare, manufacturing, and smart cities. These technologies help secure device identities, communication networks, firmware, and data flows against unauthorized access and cyberattacks. Rising adoption of Industry 4.0 and critical infrastructure digitalization is increasing demand for IoT threat monitoring, endpoint protection, and network segmentation. As connected ecosystems grow, IoT security is becoming a core part of Europe’s cybersecurity technology landscape.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Services |

54.08% |

2025 |

|

Deployment Type |

On-premises |

58.12% |

2025 |

|

User Type |

Large Enterprises |

70.1% |

2025 |

|

Industry Vertical |

BFSI |

24.15% |

2025 |

|

Country |

Germany |

22.0% |

2025 |

By Component

Services lead at 54.08% (2025). European cybersecurity services encompass SOC-as-a-service, security consulting, incident response, penetration testing, security awareness training, and compliance auditing, creating the most commercially recurring revenue security market segment through multi-year managed service contracts and annual retainer structures.

To access detailed market analysis, Request Sample

Solutions at 45.92% grow fastest at ~8.5% CAGR through AI-native platform replacement of legacy security point products.

By Deployment Type

On-premises leads at 58.12% (2025). On-premises encompasses security hardware, on-premise software, and hosted virtual appliance serving European critical infrastructure, BFSI, and government sectors with the most commercially data sovereignty protected deployment above cloud-based alternatives.

Cloud-based at 41.88% grows fastest at ~9.2% CAGR through SASE, SaaS security, and cloud-native application protection adoption.

Regional Market Insights

|

Country |

Share (2025) |

Key Europe Cybersecurity Market Drivers & Characteristics |

|

Germany |

22.0% |

Driven by a strong industrial base, high enterprise cybersecurity spending, and widespread adoption of Industry 4.0, cloud security, and critical infrastructure protection solutions. |

|

United Kingdom |

18.6% |

Benefits from a mature digital economy, an advanced financial services sector, and a strong demand for cloud security, managed security services, and regulatory compliance solutions. |

|

France |

16.9% |

Supported by government-led cyber resilience initiatives, growing digital transformation programs, and increasing investments in AI-powered security and data protection technologies. |

|

Italy |

14.2% |

Witnessing rising cybersecurity adoption across manufacturing, public sector, and financial institutions, driven by increasing cyber threats and digital infrastructure modernization efforts. |

|

Spain |

11.8% |

Fueled by expanding cloud adoption, smart city projects, critical infrastructure security requirements, and increasing investments in cybersecurity awareness and threat management. |

|

Others |

16.5% |

The remaining market share comprises countries such as the Netherlands, Belgium, Sweden, Switzerland, Denmark, Norway, and other European nations, where growing digitalization, regulatory compliance requirements, and cyber resilience investments continue to support cybersecurity demand. |

Germany's 22.0% market leadership reflects Europe's largest economy's mandatory requirements, creating non-discretionary cybersecurity procurement across critical infrastructure entities. The UK's 18.6% reflects London's financial sector concentration, the most commercially active national cybersecurity support programme, and the UK's cybersecurity startup ecosystem. France's 16.9% reflects the sovereignty-risk French market positioning.

Italy's 14.2% reflects regulatory acceleration, creating an emergency cybersecurity procurement. Spain's 11.8% reflects SME cybersecurity support and digitalization acceleration, creating an expanded attack surface. Others at 16.5% encompasses the Netherlands' cloud security hub concentration, Poland's eastern-flank defence cybersecurity, and the Nordics' cybersecurity maturity, creating the most commercially geographically-diverse single market tier above the five primary country markets.

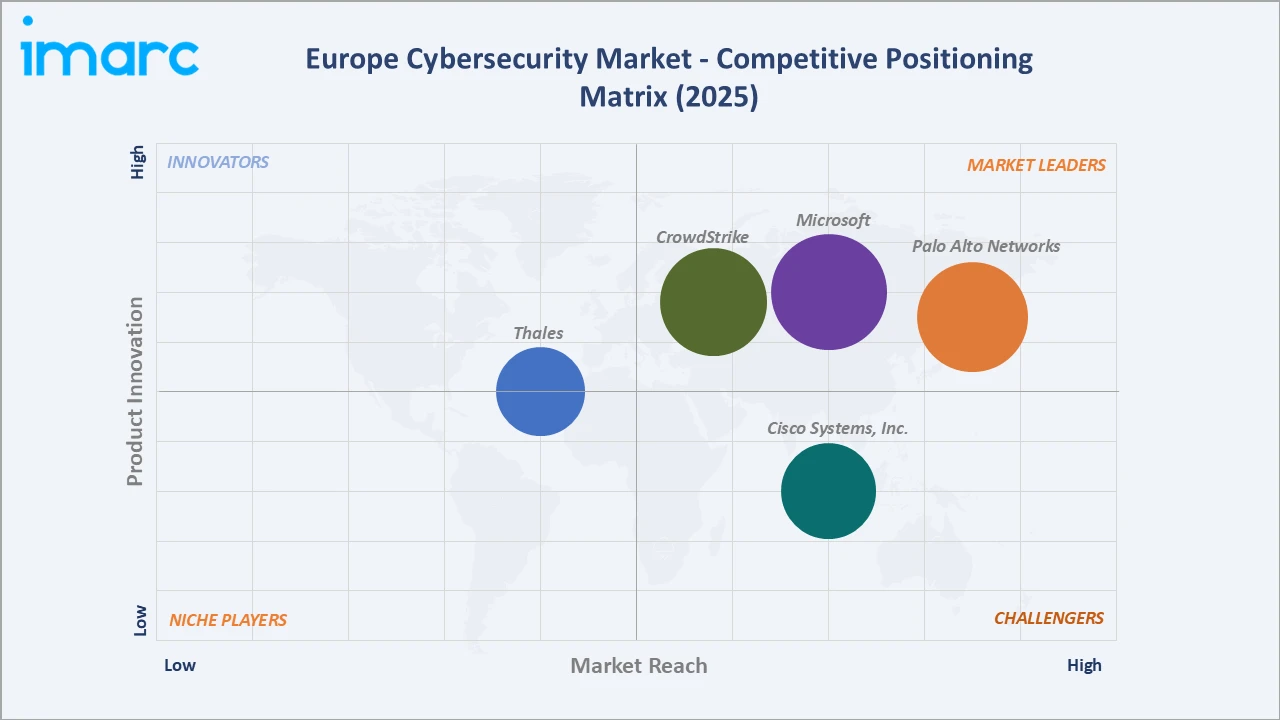

Competitive Landscape

Europe cybersecurity competitive landscape is commercially stratified between global platform leaders, legacy enterprise security incumbents, European security champions, and European system integrators.

|

Company |

Key Platforms |

Market Position |

Core Strength |

|

Palo Alto Networks |

Strata, Cortex, Prisma |

Market Leader |

Palo Alto Networks plays a pivotal role in European cybersecurity by providing AI-driven, sovereign-compliant security solutions to thousands of organizations, ensuring compliance with strict regulations. |

|

Microsoft |

Microsoft Defender, Microsoft Sentinel, Microsoft Entra, Microsoft Purview |

Market Leader |

Microsoft plays a central role in European cybersecurity by providing AI-powered threat intelligence, strengthening digital resilience against geopolitical threats, and establishing secure, sovereign cloud infrastructure. |

|

CrowdStrike |

Charlotte AI, Falcon platform |

Market Leader |

CrowdStrike holds a prominent leadership role in the European cybersecurity market by providing AI-native endpoint protection, threat intelligence, and Managed Detection and Response (MDR) services. |

|

Cisco Systems, Inc. |

Cisco Hypershield, Cisco XDR, Cisco Secure Access (SSE) |

Strong Challenger |

Cisco Systems, Inc. focuses on integrated enterprise security across networks, cloud, and AI, particularly supporting compliance with the EU regulations. |

|

Thales |

CipherTrust Data Security Platform, Imperva Application Security Platform, OneWelcome Identity Platform, Sentinel Software Monetization Platform |

Established Player |

Thales acts as a cornerstone of Europe's digital defense, operating as a top-five global player and a premier European provider of sovereign cybersecurity solutions. |

The competitive landscape is being reshaped by European digital sovereignty. AI capability is progressively the most commercially differentiating product feature dimension as market players collectively create an AI-capability race that legacy products without equivalent AI investment cannot match in threat detection accuracy, creating the most commercially accelerating product competitive differentiation vector.

Key Company Profiles

Palo Alto Networks

Palo Alto Networks is a leading cybersecurity company with a strong presence across Europe, offering a comprehensive portfolio of network security, cloud security, endpoint protection, security operations, and threat intelligence solutions.

- Key Platforms: Strata, Cortex, Prisma.

- Recent Developments: In June 2026, Deutsche Telekom and Palo Alto Networks launched Sovereign Cortex with T Security, a Europe-focused cybersecurity solution combining AI-driven protection with a data-sovereign architecture. The service targets highly regulated sectors such as healthcare, public sector, financial services, and critical infrastructure, while supporting compliance with DORA, NIS-2, and GDPR requirements.

- Strategic Focus: Strengthening its AI-powered cybersecurity portfolio through advanced threat detection, autonomous security operations, and real-time threat intelligence.

Microsoft

Microsoft is one of the leading cybersecurity providers in Europe, offering a broad portfolio of security solutions spanning identity and access management, endpoint protection, cloud security, threat intelligence, security information and event management, and extended detection and response (XDR). Through platforms such as Microsoft Defender, Microsoft Sentinel, and Microsoft Entra, the company helps enterprises, governments, financial institutions, healthcare organizations, and critical infrastructure operators strengthen their cyber resilience.

- Key Platforms: Microsoft Defender, Microsoft Sentinel, Microsoft Entra, Microsoft Purview.

- Recent Developments: In June 2025, Microsoft launched a comprehensive European Security Program offering free AI-powered cybersecurity tools to European governments facing rising state-sponsored cyber threats. Announced in Berlin, the program provides threat intelligence, automated attack disruption, and investigative support to EU member states, the UK, EU accession countries, and European Free Trade Association members at no cost.

- Strategic Focus: Expanding AI-driven cybersecurity capabilities through Microsoft Defender and Microsoft Sentinel to enhance threat detection, investigation, and automated response.

Market Concentration Analysis

Europe cybersecurity market is commercially fragmented across cybersecurity technology and service providers, with no single company commanding above 8-10% European market share. The market's fragmentation reflects cybersecurity's multi-domain nature above any single consolidated market leader position. The most commercially concentrated single cybersecurity domain is European endpoint security. Market concentration is accelerating through platformization, creating the most commercially dominant market share concentration, accelerating the competitive trend in European cybersecurity above the fragmented point-solution market's historical norm.

Investment & Growth Opportunities

Highest Growth Segments

Cloud-based security (~9.2% CAGR), AI-native XDR solutions (~10-12% CAGR from AI adoption acceleration), NIS-2 managed compliance services (~12-15% CAGR from regulatory demand), OT and industrial security (~11-13% CAGR), quantum-safe cryptography (~18-22% CAGR from near-zero base), and SME managed security subscription (~10-12% CAGR) represent Europe's highest-growth cybersecurity investment vectors through 2034.

Investment Themes

OT-Industrial cybersecurity specialization: European manufacturing sector's NIS-2 inclusion, combined with the OT security investment gap, creates the most commercially underserved infrastructure sector in European market. Investment in threat detection platform deployment capability, combined with a security assessment service, creates the most commercially secure service.

Future Market Outlook (2026-2034)

Europe cybersecurity market is projected to grow from USD 81.81 Billion in 2025 to USD 165.73 Billion by 2034, delivering an 8.16% CAGR over the forecast period, effectively doubling the European cybersecurity market above any other European enterprise technology category's comparable growth rate through regulatory mandate, threat escalation, and digital transformation convergence. The market's anchor value of USD 121.10 Billion in 2030 represents Europe's cybersecurity market maturity.

Three structural forces define Europe's cybersecurity market through 2034: regulatory expansion creates a discretionary mandatory investment floor, AI threat acceleration creates capability defensive investment urgency, and European digital sovereignty creates standard cloud security investment.

Research Methodology

Primary Research

Primary research comprised structured interviews with Europe cybersecurity market stakeholders (2025), including cybersecurity solution providers, MDR/SOC service vendors, system integrators, cloud security firms, and enterprise IT security heads. Inputs were also gathered from regulatory experts, government agencies, BFSI, healthcare, manufacturing, and critical infrastructure end users.

Secondary Research

Secondary research encompassed an extensive review of company annual reports, investor presentations, cybersecurity vendor publications, government and regulatory documents, industry association reports, and technology white papers. The research also included analysis of cybersecurity spending trends, threat intelligence reports, cloud adoption data, regulatory frameworks, as well as information from reputable industry databases and trade publications to validate market estimates and trends.

Forecasting Models

Market revenue forecasts developed using an end-use industry security spending model: European enterprise IT security budget by country and industry sector, multiplied by European enterprise IT spending by country, with a regulatory compliance premium applied.

Europe Cybersecurity Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Types Covered | Cloud-based, On-premises |

| User Types Covered | Large Enterprises, Small and Medium Enterprises |

| Industry Verticals Covered | IT and Telecom, Retail, BFSI, Healthcare, Defense/Government, Manufacturing, Energy, Others |

| Countries Covered | Germany, France, the United Kingdom, Italy, Spain, Others |

| Companies Covered | Palo Alto Networks, Microsoft, CrowdStrike, Cisco Systems, Inc., Thales, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Cybersecurity Market Report

The Europe cybersecurity market reached USD 81.81 Billion in 2025, driven by rising cyberattacks, growing cloud adoption, hybrid work models, and expanding digital infrastructure across enterprises. Strict regulations along with increasing demand for AI-based threat detection, MDR services, and zero-trust security are further supporting market growth.

The Europe cybersecurity market grows at 8.16% CAGR during 2026-2034, reaching USD 165.73 Billion by 2034. The overall growth is sustained by regulatory mandatory compliance, ransomware and nation-state attack escalation, AI threat evolution, European digital sovereignty investment, and quantum-safe cryptography migration.

Services lead at 54.08% through Europe's cybersecurity skills shortage, creating managed security service adoption for 24x7 monitoring above self-operated SOC economics for European enterprise and SME.

On-premises leads at 58.12% through European data sovereignty requirements, critical infrastructure air-gap requirements, and national security classification, creating Europe's cloud on-premises security deployment concentration.

Germany leads at 22.0% through Europe's largest economy, creating the largest absolute security budget and Germany's Industrie 4.0 OT security concentration, creating manufacturing sector cybersecurity demand.

Leading companies include Palo Alto Networks, Microsoft, CrowdStrike, Cisco Systems, Inc., and Thales, among others.

The Europe cybersecurity market is projected to reach approximately USD 121.10 Billion by 2030, with AI autonomous SOC operations, cloud-based security, and quantum-safe cryptography migration.

Three priority investment opportunities: regulatory compliance platform-as-a-service, creating the most commercially mandated new cybersecurity product in the European market, European MSSP specialization targeting SME essential entity market, and OT-industrial cybersecurity specialization for European manufacturing NIS-2 important entity compliance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)