Europe Dairy Market Size, Share, Trends and Forecast by Product Type and Country, 2026-2034

Europe Dairy Market Size, Share, Trends & Forecast (2026-2034

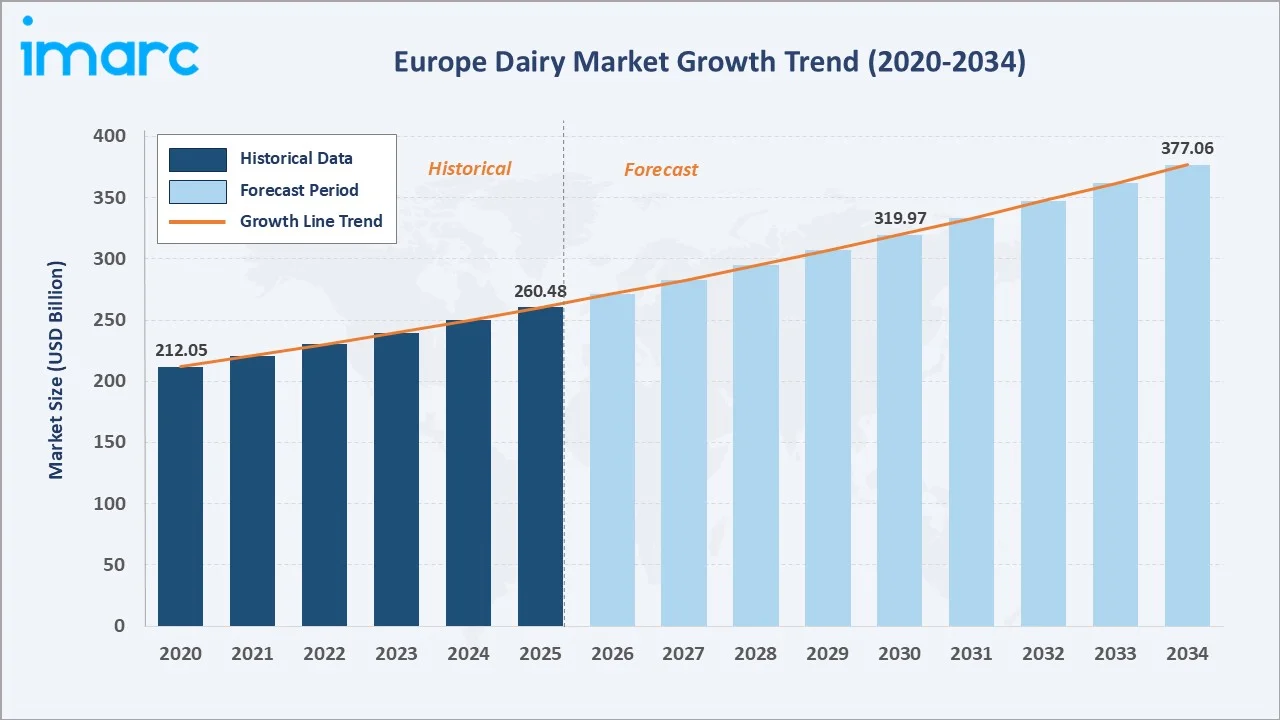

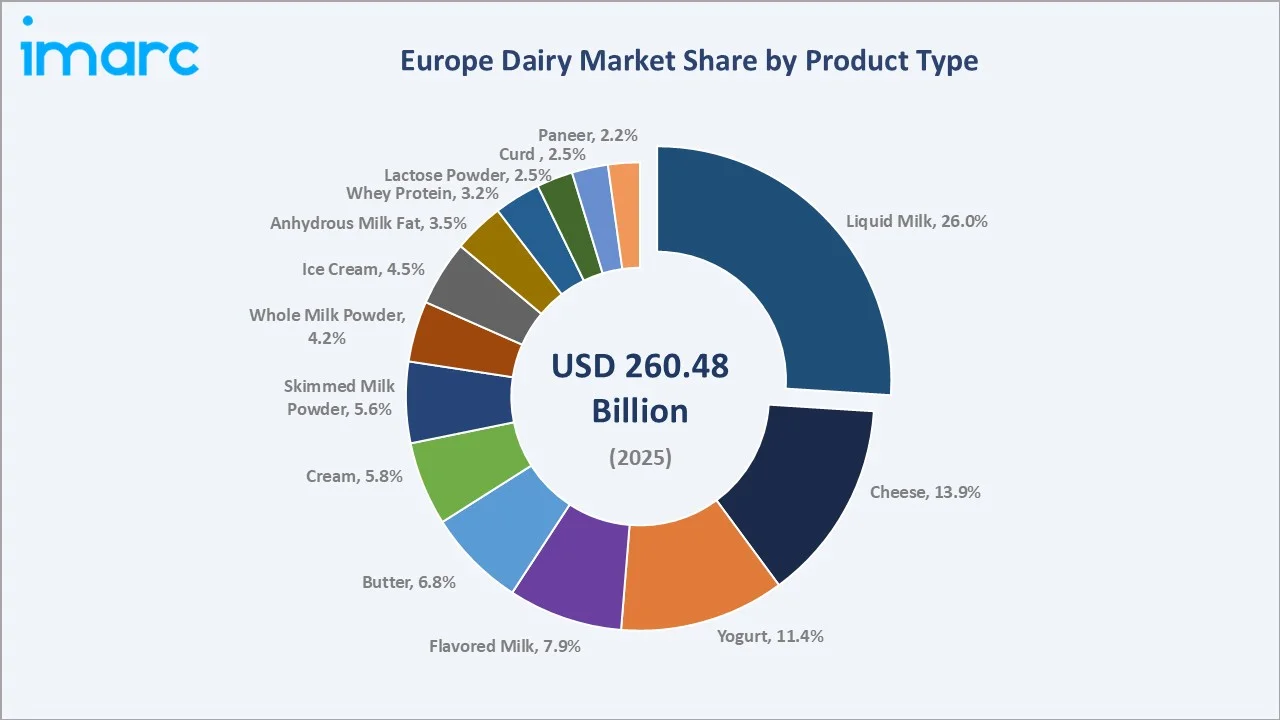

The Europe dairy market size was valued at USD 260.48 Billion in 2025 and is projected to reach USD 377.06 Billion by 2034, exhibiting a CAGR of 4.20% during the forecast period 2026-2034. Strong demand for healthy and diversified dairy products, advanced dairy farming infrastructure, and deep-rooted culinary traditions across Europe are primary growth enablers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 260.48 Billion |

|

Forecast Market Size (2034) |

USD 377.06 Billion |

|

CAGR (2026-2034) |

4.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment Product Type |

Liquid Milk – 26.0% (2025) |

|

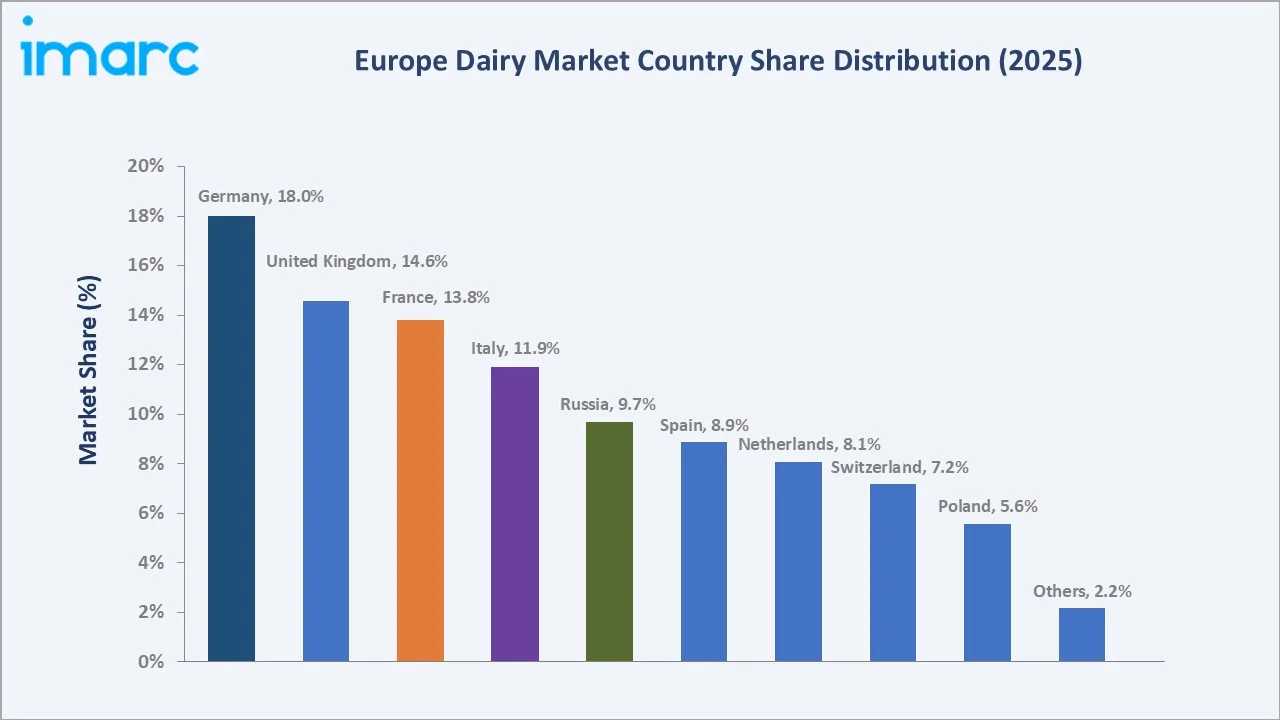

Leading Country |

Germany – 18.0% (2025) |

The Europe dairy market growth trajectory from 2020 through 2034 reflects a transition from a mature, volume-driven industry into a value-led, innovation-centric ecosystem.

To get more information on this market, Request Sample

The chart above illustrates the Europe dairy market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by health-conscious consumer spending, product innovation, and channel diversification across the region.

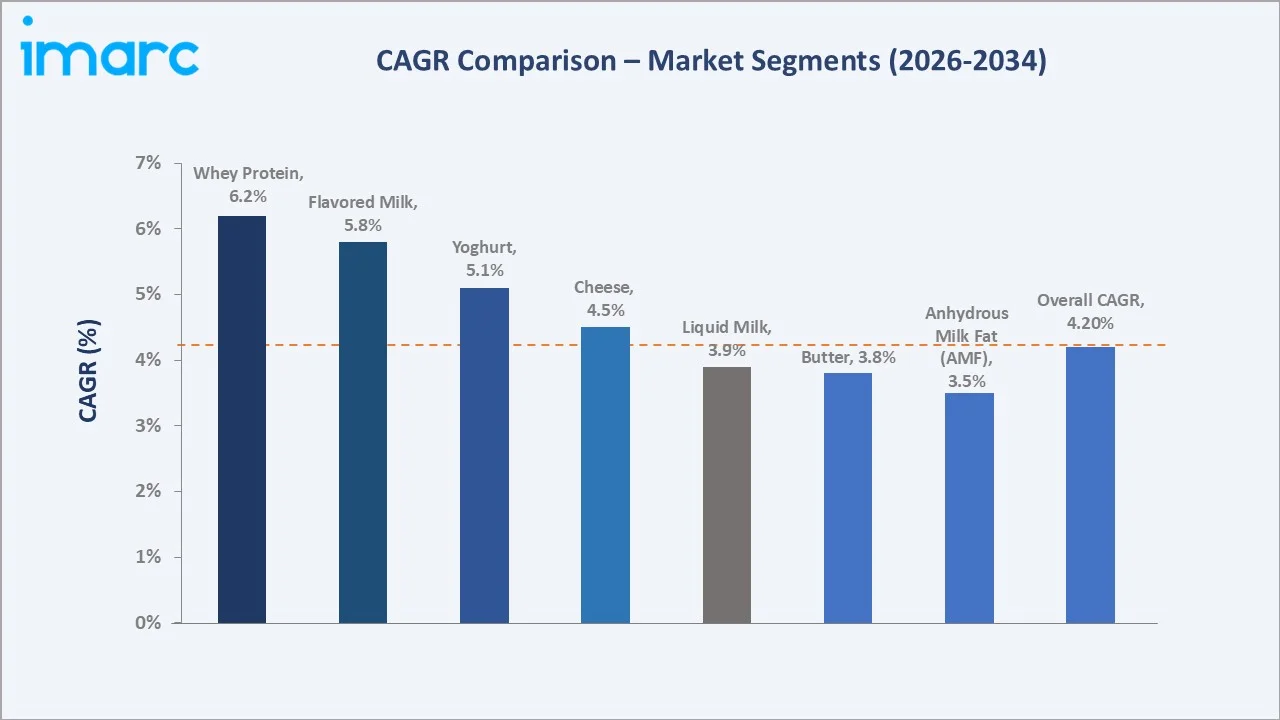

Segment-level CAGR comparisons highlight whey protein (~6.2%) and yoghurt (~5.1%) as the fastest-growing sub-categories in the Europe dairy market forecast through 2034, outpacing the overall market CAGR of 4.20%.

Executive Summary

The Europe dairy market is one of the most developed food categories globally. Valued at USD 260.48 Billion in 2025, it is forecast to reach USD 377.06 Billion by 2034 at a CAGR of 4.20%. Europe's dairy sector benefits from well-established processing infrastructure, deep consumer tradition in dairy consumption, and strong cooperative models that enhance supply chain efficiency.

Liquid milk maintains its position as the dominant product segment at a 26.0% share in 2025. Cheese accounts for 13.9%, driven by culinary heritage and strong export performance. Yoghurt holds 11.4%, benefiting from probiotic-enriched and functional variants. Germany leads all countries with an 18.0% market share in 2025, reinforced by advanced dairy processing capacity and its role as total EU milk production is estimated to be around 155 million tonnes per year.

Key growth drivers include rising consumer awareness of nutritional benefits, expanding lactose-free and fortified product demand, accelerating sustainable farming practices, and increasing penetration of value-added dairy in Eastern European markets. The dairy market outlook remains positive, supported by functional dairy innovation, strong retail infrastructure, and growing exports from leading European cooperatives.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Liquid Milk – 26.0% share (2025) |

|

Second Largest Product Type |

Cheese – 13.9% share (2025) |

|

Third Largest Product Type |

Yoghurt – 11.4% share (2025) |

|

Leading Country |

Germany – 18.0% market share (2025 |

|

Second Leading Country |

United Kingdom – 14.6% share (2025) |

|

Top Companies |

Arla Foods, Lactalis, Danone, FrieslandCampina, DMK Group |

|

Market Opportunity |

Functional dairy, lactose-free, Eastern Europe expansion |

Key Analytical Observations:

- Liquid milk's 26.0% dominance in 2025 reflects its foundational role in European diets, with household consumption in Germany and France accounting for the largest share of total liquid milk revenues.

- Cheese at 13.9% is anchored by Europe's rich cheese heritage – France alone produces over 1,200 cheese varieties. Export demand further reinforces segment growth momentum.

- Yoghurt's 11.4% share is driven by functional product innovation. Probiotic-enriched yoghurts, Greek-style variants, and low-sugar formats are outpacing conventional segment growth rates.

- Germany's 18.0% country dominance is supported by numerous dairy farms and highly advanced processing facilities. It produces over 33 million tonnes of raw milk annually.

- Whey protein – the fastest-growing sub-segment – Benefits from rising demand in sports nutrition, infant formula enrichment, and functional food production, supporting steady long-term expansion driven by evolving dietary preferences, increasing focus on health and wellness, and the growing incorporation of nutrient-enhanced ingredients across diverse food and beverage applications.

- Eastern European markets represent emerging growth corridors as rising middle-class incomes and improving retail infrastructure drive dairy product diversification.

Europe Dairy Market Overview

The Europe dairy market encompasses a broad range of products derived from cow, sheep, goat, and buffalo milk. Categories include liquid milk, cheese, butter, yoghurt, cream, powdered milk, and specialized ingredients such as whey protein and lactose powder. The market serves household consumers, foodservice operators, food processors, pharmaceutical companies, and infant nutrition manufacturers.

The market's ecosystem is structured around large cooperative models, multinational processors, and specialty producers. Advanced cold-chain infrastructure, stringent EU food safety standards, and well-developed retail and distribution networks ensure product quality and accessibility. Macroeconomic influences include disposable income growth, urbanization, tourism-driven foodservice demand, and EU Common Agricultural Policy (CAP) subsidies that support dairy farming profitability across the region.

Market Dynamics

To evaluate market opportunities, Request Sample

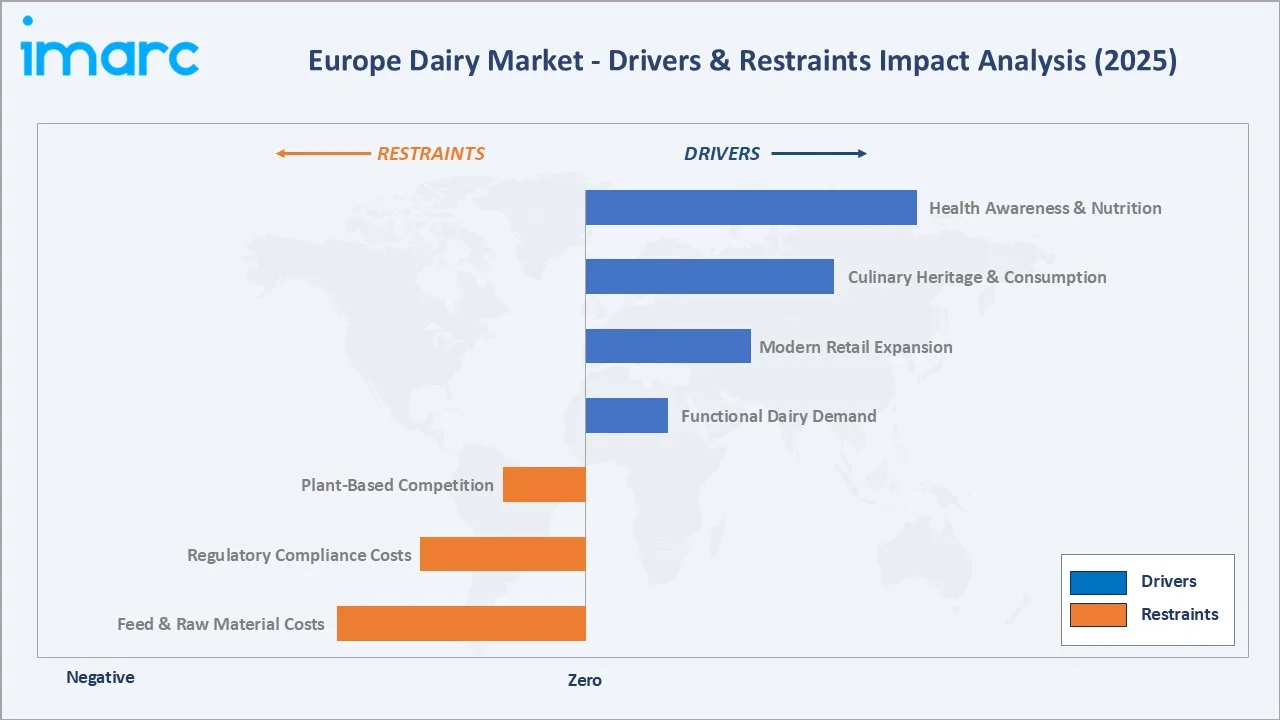

Market Drivers

- Rising Health Awareness and Nutritional Demand: European consumers are increasingly prioritizing protein-rich, calcium-fortified, and probiotic dairy products. Functional dairy offerings are gaining strong traction, driven by rising health awareness, preventive nutrition trends, and growing demand for value-added dairy across Western European markets.

- Advanced Dairy Farming Infrastructure: Europe represents a significant share of global raw milk production, supported by a well-established dairy ecosystem. Germany remains a leading producer, with substantial output driven by advanced processing infrastructure, strong cooperative networks, and high efficiency across the dairy value chain.

- Strong Culinary Heritage and Per-Capita Consumption: Per-capita cheese consumption in France exceeds 27 kg per year. European consumers average 67 kg per capita in total dairy consumption – among the highest globally – ensuring sustained base demand.

- Expanding Modern Retail and E-Commerce Channels: Modern grocery retail accounts for over 78% of European dairy distribution in 2025. E-commerce dairy sales are growing at approximately 9.4% CAGR, driven by subscription fresh dairy delivery and online grocery platforms.

Market Restraints

- Milk Price Volatility and Feed Cost Pressures: European raw milk prices experienced notable volatility during the recent period, creating margin pressure for processors and cooperatives. Fluctuations in input costs, energy prices, and supply-demand imbalances contributed to earnings uncertainty across the dairy value chain.

- Stringent Regulatory Compliance Costs: EU food safety, animal welfare, and environmental regulations require significant investment. Compliance with Green Deal sustainability targets and CAP reform requirements adds cost burdens for smaller dairy producers.

- Competition from Plant-Based Alternatives: Plant-based dairy alternatives are gaining a growing share of the European dairy-equivalent market, reflecting a steady rise in adoption over recent years. This shift is primarily driven by younger consumers increasingly opting for oat, almond, and soy-based products, influenced by health, sustainability, and dietary preferences.

Market Opportunities

- Lactose-Free and Specialty Dairy Expansion: Lactose intolerance affects a notable share of the adult population in Northern Europe, driving demand for specialized dietary options. The lactose-free dairy segment has expanded rapidly in recent years, emerging as a high-value niche with strong growth potential, supported by increasing consumer awareness and demand for digestive-friendly products.

- Dairy Ingredients Export Growth: EU dairy exports continue to represent a significant value stream, supported by strong global demand. Shipments of whey protein, skimmed milk powder, and whole milk powder to Asia Pacific and the Middle East are expanding, largely driven by rising demand for infant nutrition and fortified food applications.

- Sustainable and Regenerative Dairy Premium Segment: Carbon-neutral certified dairy products are commanding notable price premiums across Western European markets, creating a rapidly expanding premium segment. This trend is driven by environmentally conscious consumers, increasing regulatory focus on sustainability, and strong brand differentiation among producers committed to low-carbon and climate-responsible dairy production.

Market Challenges

- Environmental Sustainability and Emission Reduction Targets: The dairy sector represents a meaningful share of EU greenhouse gas emissions, placing it at the center of sustainability transformation efforts. Achieving EU Farm to Fork Strategy targets requires substantial investment in manure management, precision feeding technologies, and renewable energy adoption, driving structural changes across dairy production systems.

- Demographic Shifts and Changing Diet Patterns: Younger European consumers are adopting flexitarian and vegan dietary patterns, reducing per-capita conventional dairy consumption and requiring producers to innovate with functional and hybrid dairy-plant products.

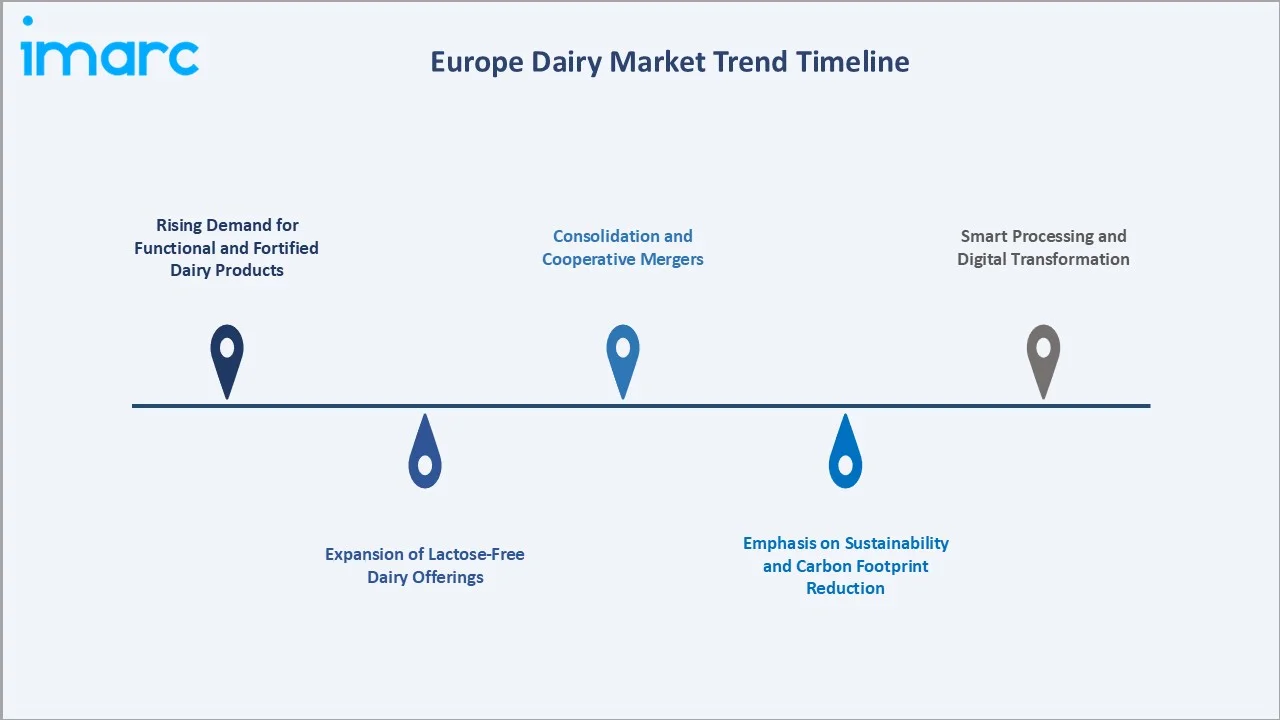

Emerging Market Trends

1. Rising Demand for Functional and Fortified Dairy Products

European consumers increasingly seek dairy with added health benefits. Manufacturers are developing probiotic-enriched yoghurts, high-protein milk beverages, and calcium-fortified products targeting athletes, elderly consumers, and health-conscious buyers. In December 2025, Arla Foods Ingredients showcased high-protein dairy concepts at Fi Europe in Paris. Functional dairy now represents the fastest-growing value-added sub-category across Western Europe.

2. Expansion of Lactose-Free Dairy Offerings

The lactose-free segment is rapidly expanding across Europe as awareness of lactose intolerance grows. In 2024, Latvia's Food Union expanded its Lakto brand with seven new lactose-free yoghurts. Once a niche medical product, lactose-free dairy is now mainstream, with retailers allocating prominent shelf space. Advanced lactase enzyme technologies are improving taste parity with conventional dairy products.

3. Emphasis on Sustainability and Carbon Footprint Reduction

Sustainability has become a key competitive factor in Europe's dairy industry. In 2025, Swiss producer Emmi validated its science-based CO2e reduction targets as part of its net-zero strategy. Leading cooperatives including Arla Foods and FrieslandCampina are introducing carbon-neutral product lines and regenerative farming partnerships. Carbon labeling is emerging as a differentiator in premium retail channels.

4. Consolidation and Cooperative Mergers

In April 2025, Arla Foods and DMK Group announced merger plans to form Europe’s largest dairy cooperative, bringing together a vast network of farmer-owners. This consolidation trend is reshaping competitive dynamics, enabling combined entities to achieve scale efficiencies, expand distribution reach, and strengthen investment in product innovation and R&D across the continent.

5. Smart Processing and Digital Transformation

Dairy processors are increasingly investing in IoT-enabled production monitoring, AI-powered quality control systems, and blockchain-based traceability platforms. These technologies are helping reduce waste, optimize raw milk utilization, and enhance end-to-end supply chain transparency. Digital transformation is emerging as a key efficiency lever, lowering processing costs and improving operational agility across leading European dairy facilities.

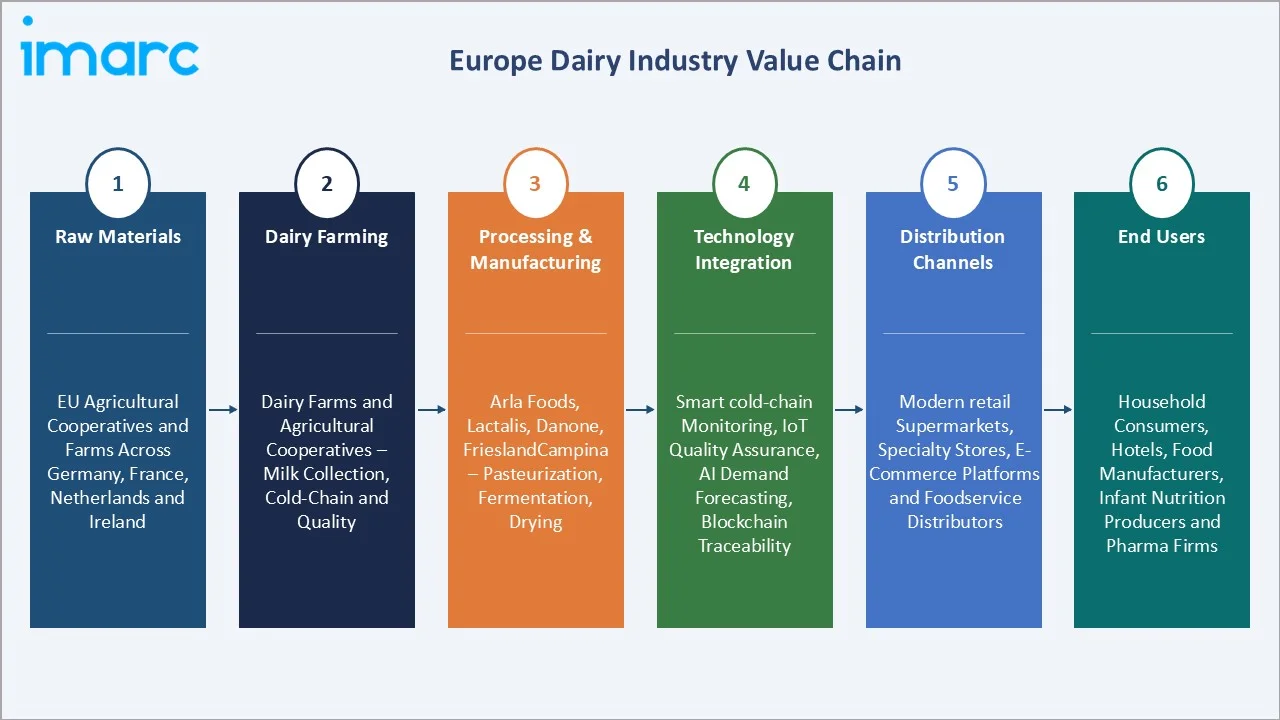

Industry Value Chain Analysis

The European dairy industry value chain spans six integrated stages from raw material supply through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and sustainability investment priorities relevant to the overall Europe dairy market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Pasture, feed, grain, water – supplied by European agricultural cooperatives and farms across Germany, France, Netherlands, and Ireland |

|

Dairy Farming |

Dairy farms and agricultural cooperatives – milk collection, cold-chain logistics, and quality assurance |

|

Processing & Manufacturing |

Arla Foods amba, LACTALIS, Danone, FrieslandCampina, DMK GROUP, Hochwald Foods GmbH, Emmi Group – pasteurization, UHT treatment, fermentation, churning, drying, and packaging operations |

|

Technology Integration |

Advanced processing automation, smart cold-chain monitoring, IoT-enabled quality assurance, AI-powered demand forecasting, and blockchain traceability |

|

Distribution Channels |

Modern retail supermarkets, specialty stores, e-commerce platforms, foodservice, and institutional distributors |

|

End Users |

Household consumers, hotels and foodservice operators, food manufacturing companies, infant nutrition producers, and pharmaceutical firms |

OEM processors hold the highest strategic value by integrating raw materials, advanced technologies, and distribution capabilities into consumer-ready products. Meanwhile, e-commerce and direct-to-consumer channels are reshaping distribution, enabling manufacturers to bypass intermediaries, strengthen brand connections, and capture higher margins.

Technology Landscape in the Dairy Industry

Advanced Processing and UHT Technology

Ultra-high temperature (UHT) processing remains a cornerstone technology in the European dairy industry, enabling extended shelf life for liquid milk without the need for refrigeration. A significant share of liquid milk consumption in continental Europe is UHT-treated, reflecting strong consumer acceptance and distribution efficiency advantages.

Membrane Filtration and Concentration Technology

Microfiltration, ultrafiltration, and nanofiltration technologies are enabling the extraction of high-value ingredients from milk streams, enhancing the overall value realization of dairy processing. These advanced separation techniques support the production of whey protein concentrates, milk protein isolates, and lactose powders, widely used in sports nutrition and infant formula applications.

Smart Connectivity and IoT in Dairy Farming

Precision dairy farming technologies, including IoT-enabled milking robots, real-time herd health monitoring systems, and data-driven feed optimization platforms, are gaining strong adoption across Northern European dairy farms. The increasing penetration of automated milking systems reflects a clear shift toward smart farming practices, improving labor efficiency, enhancing animal welfare, and ensuring greater consistency in milk yield and quality across modern dairy operations.

Sustainable Processing and Renewable Energy Integration

eading European dairy processors are integrating solar energy, biogas generated from dairy waste, and heat recovery systems to reduce carbon intensity across operations. FrieslandCampina has made notable progress in lowering emissions intensity per kilogram of dairy product through such initiatives.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product Type | Liquid Milk | 26% |

2025 |

| Country | Germany | 18% | 2025 |

By Product Type

Liquid Milk dominates the Europe dairy market with a market share of 26.0% in 2025. The segment benefits from established distribution networks delivering fresh and UHT varieties through supermarkets, convenience stores, and direct delivery channels. German and French dairy processors lead regional liquid milk production.

Regional Market Insights

The Europe dairy market is geographically diverse, with Western European nations leading in market size while Eastern European countries represent emerging growth opportunities.

Germany commands the highest country share at 18.0% in 2025, while Poland and other emerging markets are growing at above-average rates.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

18.0% |

Largest milk producer; advanced processing; high per-capita consumption |

|

United Kingdom |

14.6% |

Fresh dairy preference; strong retail brands; organic dairy growth |

|

France |

13.8% |

Cheese heritage; premium dairy; strong foodservice demand |

|

Italy |

11.9% |

Specialty cheese (Parmigiano, Mozzarella); gelato culture; premium segment |

|

Russia |

9.7% |

Large domestic market; import substitution policy; dairy modernization |

|

Spain |

8.9% |

Mediterranean diet; flavored dairy growth; foodservice expansion |

|

Netherlands |

8.1% |

Export-driven cooperative hub; dairy ingredients leadership worldwide |

|

Switzerland |

7.2% |

Premium positioning; sustainability innovation; specialty cheese exports |

|

Poland |

5.6% |

Fastest growing Eastern market; rising incomes; modernizing retail |

|

Others |

2.2% |

Emerging markets; regional cooperatives; niche dairy specialty products |

Competitive Landscape

The Europe dairy market exhibits a fragmented competitive structure with multinational corporations and regional dairy cooperatives competing across product categories. Leading players leverage scale, innovation capabilities, and established distribution networks to maintain market positions while focusing on sustainability and product diversification.

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Arla Foods amba |

Arla, Lurpak, Castello |

Leader |

Largest European cooperative; pan-European distribution; sustainability |

|

LACTALIS |

President, Galbani, Lactel |

Leader |

World's largest dairy; diverse portfolio; private-label supply |

|

Danone |

Activia, Actimel, Oikos |

Leader |

Functional dairy; probiotic innovation; health-wellness positioning |

|

FrieslandCampina |

Dutch Lady, Friso, Campina |

Leader |

Dutch cooperative; export strength; infant nutrition focus |

|

DMK GROUP |

Milram, Oldenburger |

Leader |

Germany's largest cooperative; liquid milk and butter dominance |

|

Hochwald Foods GmbH |

Bärenmarke, Tuffi, Hochwald, Glücksklee |

Challenger |

Lactose-free specialization; organic dairy portfolio |

|

Emmi Group |

Kaltbach, Caffè Latte |

Challenger |

Swiss premium dairy; sustainability-validated; specialty cheese |

|

Savencia SA |

Caprice des Dieux |

Challenger |

French specialty cheese; value-added dairy differentiation |

The competitive landscape is moderately fragmented. At the premium OEM tier, consolidation is occurring around brand equity and sustainability certification. Eastern European markets are generating competitive regional players increasingly expanding westward with cost-competitive products.

Key Company Profiles

Arla Foods amba

Arla Foods amba is a multinational dairy cooperative headquartered in Viby, Denmark. It is one of the largest dairy companies globally and a leading producer in Scandinavia and the UK. The company is owned by thousands of dairy farmers across Europe, making it a farmer-owned cooperative.

- Product Portfolio: Arla brand fresh dairy, Lurpak butter, Castello specialty cheeses, Arla Protein range, organic and Lactofree lines.

- Recent Developments: In 2025 Arla Foods Ingredients announced in November 2025 that it will showcase its innovation capabilities in milk and whey proteins through a range of new high-protein food and beverage concepts at Fi Europe 2025 in Paris.

- Strategic Focus: Cooperative scale expansion, sustainability leadership with net-zero targets, functional dairy innovation, and growing market presence in Asia and the Middle East through dairy ingredient exports.

Lactalis

Lactalis is a French multinational dairy company headquartered in Laval, France. Founded in 1933, it is the largest dairy products company in the world and a leading global player in cheese and milk-based products.

- Product Portfolio: President butter and cream, Galbani Italian cheeses, Lactel UHT milk, Société Roquefort, Parmalat UHT products, and Stonyfield organic dairy across global markets.

- Recent Developments: In 2024, Lactalis has announced plans to acquire dairy assets and brands from Bayerische Milchindustrie eG, strengthening its presence in southern Germany. The deal includes BMI’s fresh dairy operations—such as milk, yogurt, quark, cream, and ayran—along with a production facility in Würzburg, Bavaria, and several regional brands including Frankenland, Thüringer Land, and Haydi.

- Strategic Focus: Geographic diversification, private-label dairy supply to major European retailers, and broadening specialty cheese and premium dairy product ranges across key growth markets

Danone

Danone is a global food and beverage company headquartered in Paris, France. Its Fresh Dairy Products division is one of the world's largest, with significant presence across European yoghurt, functional dairy, and plant-based categories.

- Product Portfolio: Activia probiotic yoghurt, Danone drinkable yoghurt, Actimel fermented milk, and Oikos Greek yoghurt

- Recent Developments: In 2026, Danone has agreed to acquire UK-based nutrition brand Huel in a deal valued at €1 billion, strengthening its position in the fast-growing complete nutrition segment. Huel, known for its plant-based meal replacements, protein shakes, and ready-to-drink products, will benefit from Danone’s global distribution, R&D, and scale to expand into new markets

- Strategic Focus: Health and wellness positioning, probiotic innovation, sustainable dairy sourcing, and developing hybrid dairy-plant products to capture evolving European consumer preferences.

Market Concentration Analysis

The Europe dairy market exhibits moderate fragmentation. The top five players – Arla Foods, Lactalis, Danone, FrieslandCampina, and DMK Group – collectively account for an estimated 30–38% of European dairy market revenue in 2025. The remainder is distributed among regional cooperatives, specialty producers, and private-label suppliers catering to major retail chains across Europe.

The market demonstrates a bifurcated consolidation dynamic. At the premium and branded tier, M&A activity is consolidating scale – exemplified by the Arla-DMK merger announcement in 2025 and Lactalis's ongoing acquisition strategy. Simultaneously, Eastern European markets are generating competitive regional players that are increasingly expanding westward with cost-competitive products, intensifying competition across all price tiers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Whey protein is the highest-growth product sub-segment at approximately 6.2% CAGR through 2034, driven by sports nutrition demand and infant formula ingredient exports to Asia Pacific. Yoghurt and functional dairy categories are advancing at 5.1% and above, outpacing the overall market growth rate of 4.20%. Lactose-free dairy grew at over 8% CAGR in 2020–2025 and remains a premium-priced growth opportunity across Northern and Western Europe.

Emerging Market Expansion

Poland (5.6% of European dairy revenue in 2025) represents the fastest-growing established market, with rising middle-class incomes and improving modern retail infrastructure driving product diversification. Baltic states and Balkan markets are exhibiting above-average dairy consumption growth as EU membership drives income convergence. The Middle East and North Africa region provides strong incremental export opportunities for European dairy cooperatives in UHT milk, cheese, and butter.

Strategic Investment Priorities

- Dairy Processing Automation: Smart processing technologies reducing labor costs and improving yield efficiency present high ROI for mid-tier European processors seeking competitiveness gains.

- Functional Dairy R&D: Investment in clinical substantiation of probiotic claims and high-protein dairy formulations supports premium pricing and regulatory approval across EU markets.

- Sustainable Packaging: Recyclable, biodegradable, and lightweighted packaging addressing EU Green Deal mandates while meeting consumer eco-preference in Western European retail.

- Export Infrastructure: Cold-chain logistics and regulatory compliance capabilities enabling dairy ingredient and UHT product exports to high-growth international markets in Asia Pacific and the Middle East.

Future Market Outlook (2026-2034)

The Europe dairy market forecast projects steady value expansion from USD 260.48 Billion in 2025 to USD 377.06 Billion by 2034 at a CAGR of 4.20%. The market is forecast to reach USD 319.97 Billion by 2030, representing a significant mid-period milestone reflecting sustained growth momentum.

Germany and France will retain country-level market leadership through 2034, while Poland and Eastern European markets are projected to advance at above-average growth rates as per-capita dairy consumption rises with improving economic conditions. Functional dairy, lactose-free products, and high-value dairy ingredients will outpace conventional liquid milk and butter categories over the forecast horizon.

Technological disruption in the form of precision fermentation, AI-driven dairy farming, and personalized nutrition platforms may reshape product innovation timelines. Industry transformation will be driven by cooperative consolidation, sustainability-linked financing, and expansion of European dairy ingredient exports to Asia Pacific infant formula and sports nutrition markets through 2034.

Research Methodology

Primary Research

Primary research encompasses structured interviews and surveys with dairy industry stakeholders including senior executives from leading dairy cooperatives and processors, procurement managers at major retail chains, dairy farming cooperative representatives, and regulatory affairs professionals at EU agricultural bodies. A minimum of 100 primary research engagements were conducted across 12 European countries to validate quantitative data and qualitative insights.

Secondary Research

Secondary research integrates data from Eurostat dairy production and trade statistics, EU Common Agricultural Policy reports, European Dairy Association (EDA) publications, company annual reports, press releases, regulatory filings, academic journals, and reputable news sources. Historical market sizing is validated against official national dairy statistics from Germany, France, Netherlands, and the United Kingdom.

Forecasting Models

Market size forecasting employs a combination of bottom-up and top-down approaches. Bottom-up modeling aggregates product-level and country-level demand projections. Top-down modeling validates results against macroeconomic variables including GDP growth, population trends, and per-capita dairy consumption data. Statistical regression models incorporating inflation adjustments and supply-side factors ensure forecast robustness across the 2026–2034 horizon.

Europe Dairy Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Liquid Milk, Flavored Milk, Cream, Butter, Cheese, Yoghurt, Ice Cream, Anhydrous Milk Fat (AMF), Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Whey Protein, Lactose Powder, Curd, Paneer |

| Countries Covered | Germany, United Kingdom, France, Italy, Russia, Spain, Netherlands, Switzerland, Poland, Others |

| Companies Covered | Arla Foods amba, LACTALIS, Danone, FrieslandCampina, DMK GROUP, Hochwald Foods GmbH, Emmi Group, Savencia SA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Dairy Market Report

The Europe dairy market was valued at USD 260.48 Billion in 2025, driven by high per-capita dairy consumption, advanced processing infrastructure, and strong demand for value-added dairy products across the continent.

The market is projected to reach USD 377.06 Billion by 2034, growing at a CAGR of 4.20% during the forecast period 2026-2034, supported by functional dairy expansion and growing ingredient exports.

The Europe dairy market is expected to grow at a CAGR of 4.20% from 2026 to 2034, reflecting steady demand growth, product premiumization, and expansion of value-added dairy categories across the continent.

Liquid milk is the largest product segment, holding a 26.0% market share in 2025, driven by its essential role in European diets and widespread household and industrial applications.

Germany leads the Europe dairy market with an 18.0% revenue share in 2025, supported by its position as Europe's largest milk producer and highly advanced dairy processing infrastructure.

Key drivers include rising health awareness, growing demand for functional and fortified dairy products, advanced farming infrastructure, strong culinary traditions, and expanding modern retail channels.

Leading companies include Arla Foods amba, LACTALIS, Danone, FrieslandCampina, DMK GROUP, Hochwald Foods GmbH, Emmi Group, and Savencia SA.

Key trends include rising demand for lactose-free dairy, functional product innovation, sustainability and carbon footprint reduction, cooperative consolidation, and smart processing technology adoption.

The Europe dairy market is projected to reach USD 319.97 Billion by 2030, representing steady mid-period growth momentum on the path to the 2034 target of USD 377.06 Billion.

Whey protein is the fastest-growing product sub-segment, advancing at approximately 6.2% CAGR through 2034, driven by sports nutrition demand and international infant formula ingredient exports.

The Europe dairy market was valued at USD 212.05 Billion in 2020, with subsequent growth to USD 260.48 Billion by 2025 reflecting a strong historical expansion period at approximately 4.2% CAGR.

Sustainability is a critical competitive factor, with leading dairy companies investing in carbon labeling, regenerative farming, renewable energy integration, and circular packaging to meet EU Green Deal targets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade