Europe Dental Implants Market Size, Share, Trends and Forecast by Material, Product, End Use, and Country, 2026-2034

Europe Dental Implants Market Size, Share, Trends & Forecast (2026-2034)

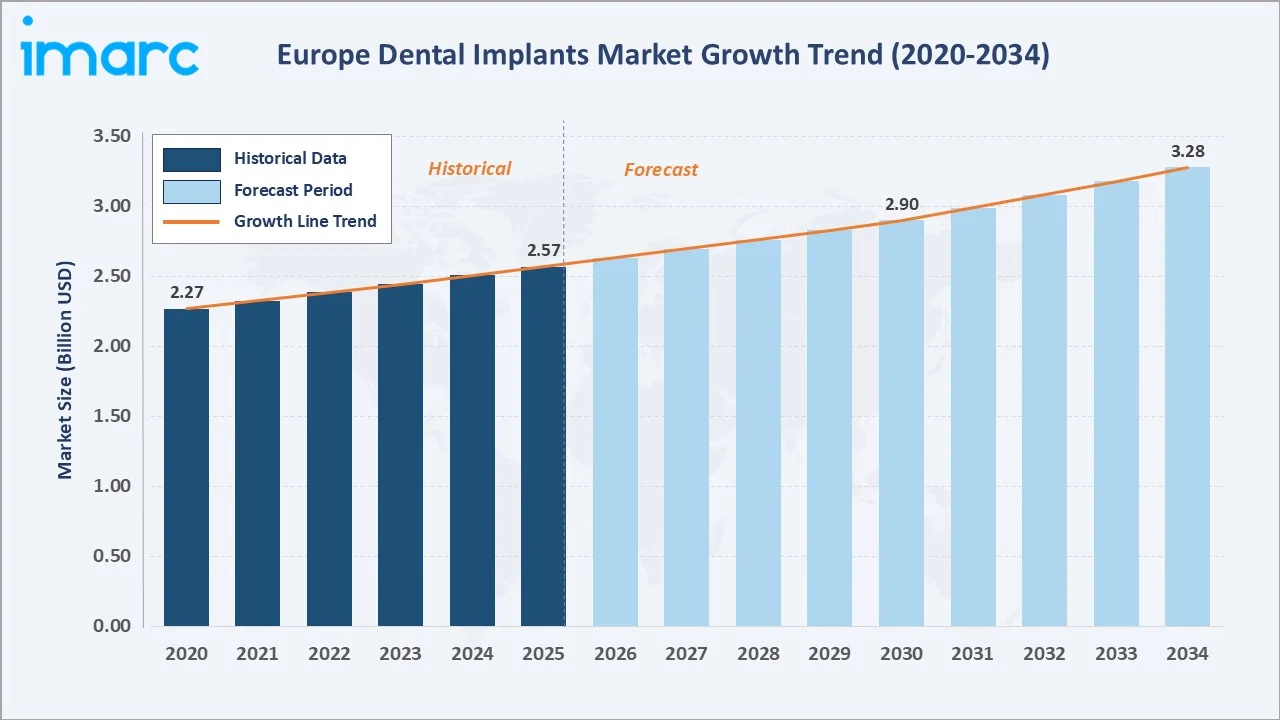

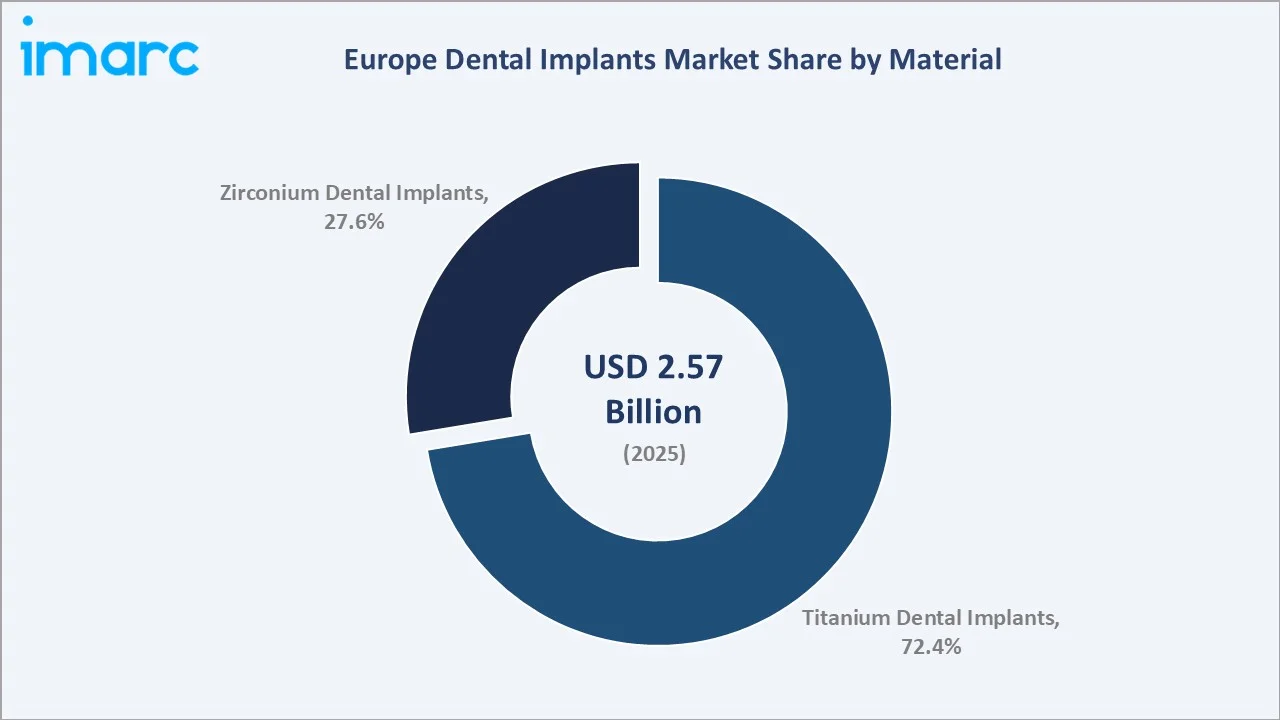

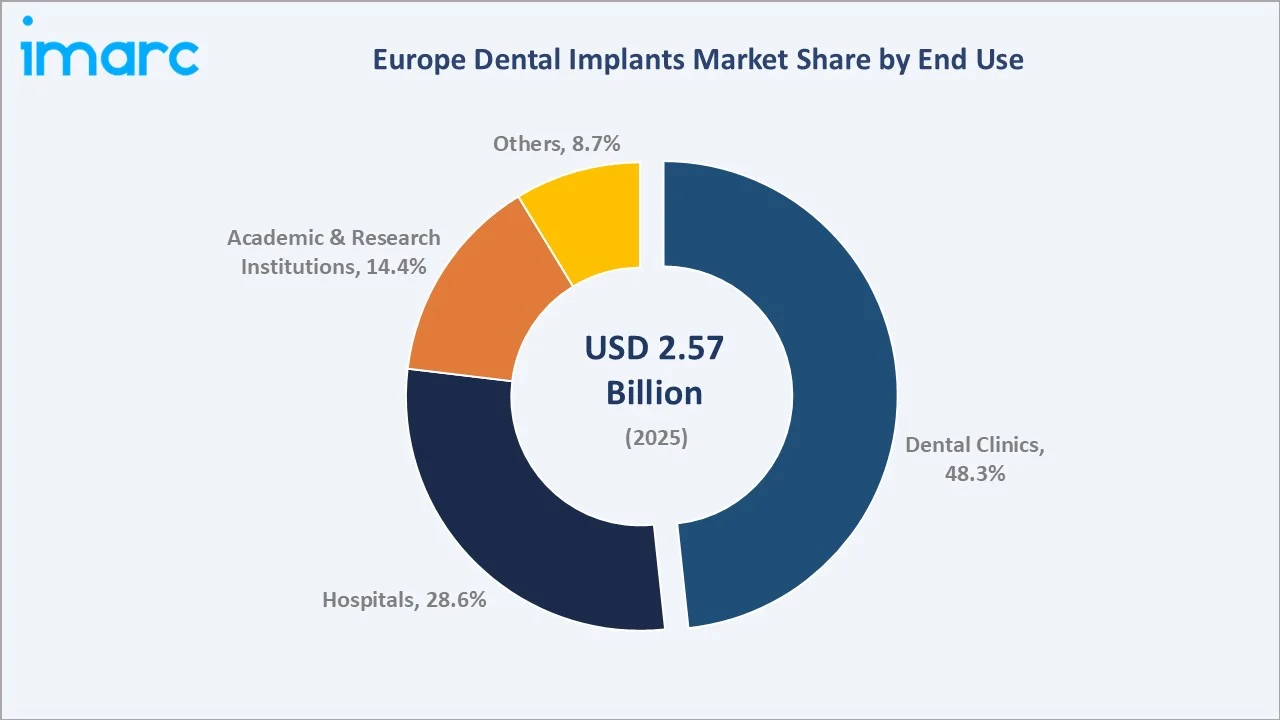

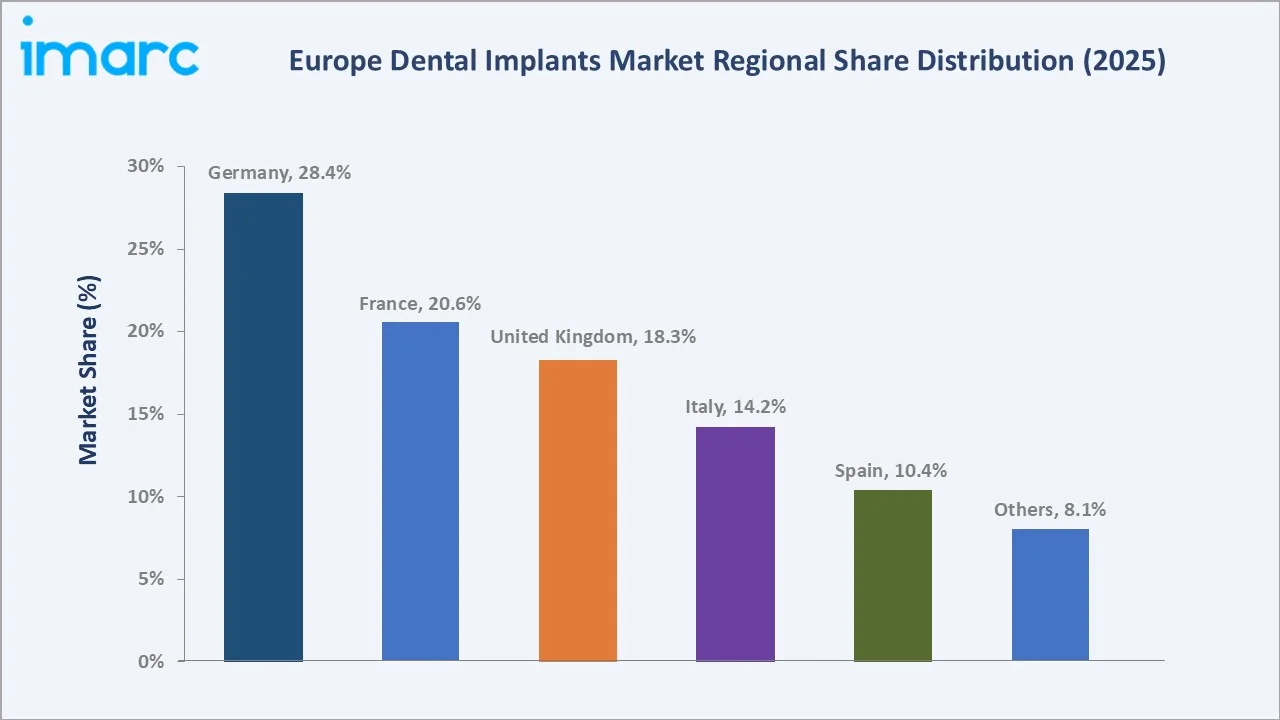

The Europe dental implants market size was valued at USD 2.57 Billion in 2025 and is projected to reach USD 3.28 Billion by 2034, exhibiting a CAGR of 2.50% during the forecast period 2026-2034. Rising edentulism rates across ageing European populations (More that one-fifth or 22.0% of Europeans were aged 65 or older in 2025, per Eurostat), expanding digital implantology infrastructure, and increasing uptake of private dental insurance are the primary catalysts driving steady market expansion. Titanium Dental Implants dominate the material segment with 72.4% in 2025, while Dental Clinics lead the end-use channels with 48.3%. Germany accounts for the largest country share at 28.4% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.57 Billion |

|

Forecast Market Size (2034) |

USD 3.28 Billion |

|

CAGR (2026-2034) |

2.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (28.4% share, 2025) |

|

Second Largest Country |

France (20.6% share, 2025) |

|

Leading Material |

Titanium Dental Implants (72.4%, 2025) |

|

Leading End Use |

Dental Clinics (48.3%, 2025) |

The Europe dental implants market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by demographic ageing, digital implantology adoption, and growing access to premium dental care across key European markets.

To get more information on this market, Request Sample

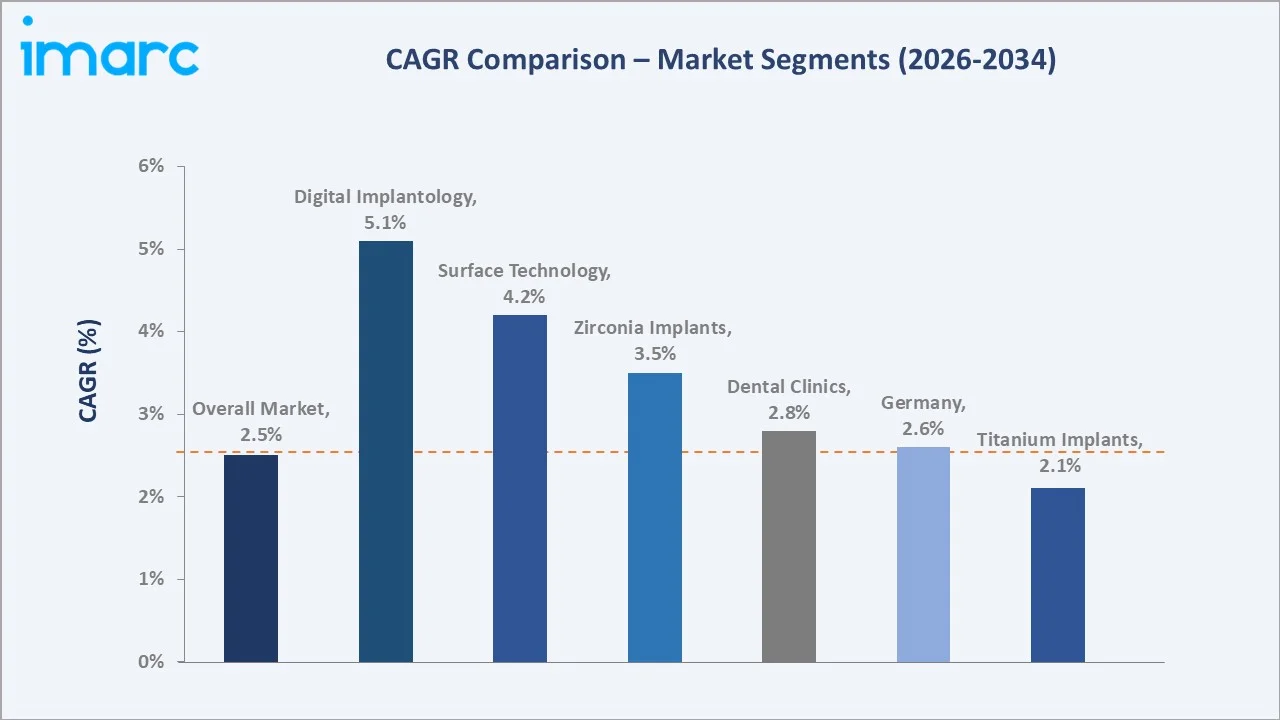

Segment-level CAGR comparisons highlighting zirconium implants and digital implantology as the two fastest-growing sub-categories within the Europe dental implants industry through 2034.

Executive Summary

The European dental implants market is on a stable, sustained growth path, expanding from USD 2.57 Billion in 2025 to an estimated USD 3.28 Billion by 2034 at a CAGR of 2.50%. This trajectory is anchored on three structural forces: demographic ageing, increasing implant procedure volumes, and a steady migration toward premium implant materials.

Germany commands the market with a 28.4% share in 2025, driven by a highly organised dental care system, universal insurance frameworks partially reimbursing implant procedures, and strong domestic manufacturers. France at 20.6% and the United Kingdom at 18.3% follow, with both markets demonstrating growing adoption of immediate implant loading protocols and computer-guided implant surgery systems from leading manufacturers.

Titanium Dental Implants retain a commanding 72.4% share in 2025, owing to decades of peer-reviewed clinical validation, superior osseointegration properties, and cost-effectiveness across patient demographics. Zirconium Dental Implants, holding a 27.6% share, represent the fastest-growing segment, driven by patient demand for metal-free restorations and the rapid commercialisation of second-generation monolithic zirconia frameworks in boutique dental clinics across Western Europe.

Key Market Insights

|

Insight |

Data |

|

Leading Material Type |

Titanium Dental Implants - 72.4% share (2025) |

|

Fastest Growing Material |

Zirconium Dental Implants - higher CAGR vs. titanium |

|

Leading End Use |

Dental Clinics - 48.3% share (2025) |

|

Largest Country Market |

Germany - 28.4% revenue share (2025) |

|

Second Largest Country |

France - 20.6% revenue share (2025) |

|

Top Companies |

Institut Straumann AG, Dentsply Sirona, Envista, ZimVie Inc., Osstem Implant |

Key Analytical Observations Supporting the Above Data:

- Titanium dental implants' 72.4% dominance in 2025 reflects their unmatched clinical track record, global regulatory acceptance, and wide adoption across both public and private dental facilities throughout all five major European markets.

- Dental Clinics account for 48.3% of total procedure volumes in 2025, as outpatient settings increasingly offer same-day implant protocols leveraging cone-beam computed tomography (CBCT) and intraoral digital scanners.

- Germany's 28.4% market leadership reflects the country's systematic approach to dental care reimbursement, rising registered dental practices, and one of Europe's highest implant-procedure-per-capita rates as of 2024.

Europe Dental Implants Market Overview

Dental implants are titanium or zirconia fixtures surgically placed into the jawbone to replace missing tooth roots, providing a permanent anchoring base for crowns, bridges, or dentures. The procedure spans three phases: implant placement, osseointegration (bone bonding), and prosthetic loading. Modern systems integrate digital workflows - from digital impressions to CAD/CAM-milled prosthetics - reducing chair time and improving surgical precision across European dental facilities.

Europe represents one of the most mature and regulated dental implant markets globally, benefitting from CE-Mark regulatory infrastructure ensuring device quality, comprehensive dental education systems, and an increasingly digital clinical ecosystem. Macroeconomic enablers include rising household incomes in Central and Eastern Europe, growing awareness campaigns by national dental associations, and a surge in cosmetic dental procedures driven by social-media-influenced aesthetic standards across all age segments.

Market Dynamics

To evaluate market opportunities, Request Sample

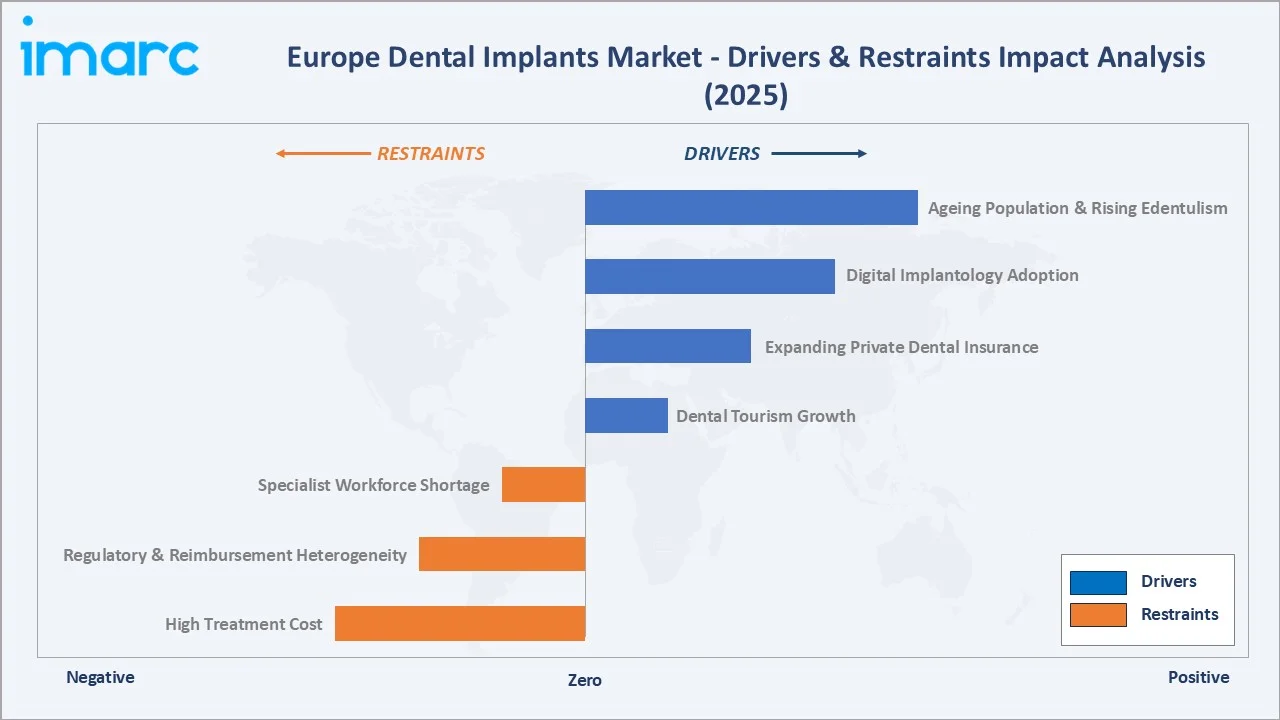

Market Drivers

- Ageing European Population and Rising Edentulism: Europe’s ageing population is driving consistent demand for restorative dental services. Tooth loss becomes increasingly common with age, leading to a higher demand for implants across major European markets.

- Digital Implantology Adoption: The use of advanced digital tools—such as CBCT imaging, intraoral scanners, and guided surgery platforms—has simplified implant procedures and improved treatment predictability. Leading systems from companies like Straumann and Dentsply Sirona are widely adopted in top-tier dental practices.

- Expanding Private Dental Insurance: Increasing enrolment in private dental plans in Germany, France, and the United Kingdom is reducing out-of-pocket cost barriers for implant procedures, particularly for patients in the 45-65 age bracket with higher cosmetic dental expenditure.

- Dental Tourism Growth: Countries including Hungary, Poland, and Croatia offer implant procedures at 40-60% below Western European prices, expanding total pan-European procedure volumes significantly.

Market Restraints

- High Treatment Cost: Implant procedures remain expensive, which limits accessibility for lower-income patients and constrains overall procedure volumes in price-sensitive regions.

- Regulatory and Reimbursement Heterogeneity: Divergent national reimbursement policies create uneven market conditions. Germany and France provide partial reimbursement, while the UK NHS does not routinely fund implant procedures, constraining NHS-dependent patient segments.

Market Opportunities

- Short Implant Technology: The advent of short (4-6 mm) and ultra-short implants is expanding the addressable patient population to those with insufficient bone volume, previously ineligible for standard implants without costly bone grafting procedures.

- Premium Zirconia Product Lines: Increasing patient demand for metal-free restorations creates a premium pricing opportunity for manufacturers launching monolithic and multi-layer zirconia implant systems, particularly in Germany, Switzerland, and Scandinavia.

- Emerging Central and Eastern European Markets: Poland, Romania, and the Czech Republic are experiencing rapid dental infrastructure development, rising private dental expenditure, and growing middle-class access to implant procedures.

Market Challenges

- Clinical Implant Failure Rates: Although implant technology continues to improve, clinical complications such as peri-implantitis remain a risk, which may deter some patients.

- Specialist Workforce Shortage: The supply of trained implantologists across Eastern and Southern Europe remains constrained, limiting procedure capacity expansion despite growing patient demand in these high-growth markets.

Emerging Market Trends

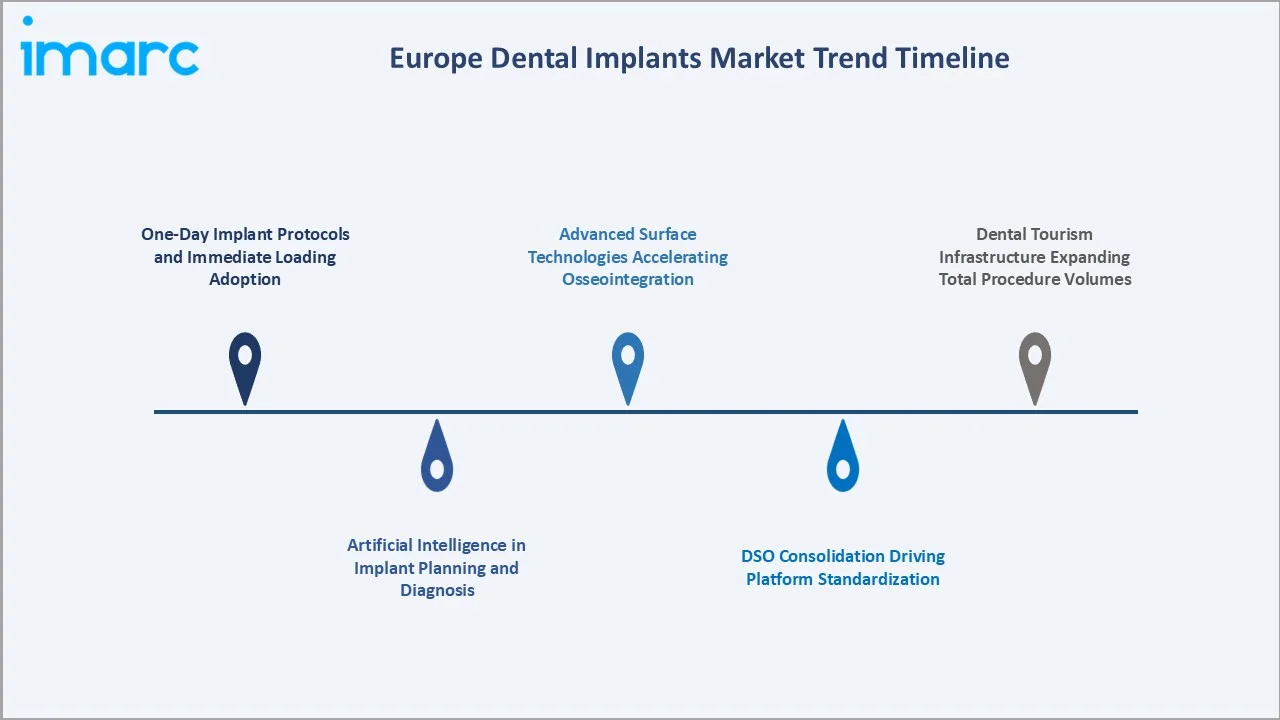

1. One-Day Implant Protocols and Immediate Loading Adoption

Immediate-loading protocols, where a provisional crown is placed on the same day as implant insertion, are increasingly adopted across Europe. This approach significantly reduces overall treatment time from several months to a single appointment, enhancing patient convenience and satisfaction. Leading implant systems, including Straumann BLX and Nobel Biocare All-on-4, are enabling this shift in premium dental practices.

2. Artificial Intelligence in Implant Planning and Diagnosis

AI-assisted diagnostic and planning tools are transforming pre-surgical workflows. Platforms integrating CBCT scan data can automate implant positioning, identify nerve proximity risks, and simulate prosthetic outcomes. Adoption of AI planning is growing in complex cases within university hospitals and specialized dental centres, with diffusion to broader dental clinics expected in the coming years.

3. Advanced Surface Technologies Accelerating Osseointegration

Manufacturers are introducing implants with hydrophilic SLA coatings, nanostructured titanium surfaces, and hybrid titanium-zirconia designs to accelerate osseointegration. Faster bone integration allows for earlier loading of implants, improving treatment efficiency and expanding clinical eligibility for immediate-placement protocols.

4. DSO Consolidation Driving Platform Standardisation

Dental Service Organisations (DSOs) are consolidating independent practices across Germany, the UK, and Spain, creating multi-site networks. These organisations standardize implant platforms across their clinics, facilitating bulk supply agreements and preferred-supplier relationships. Consolidation is driving platform standardisation and encouraging manufacturers to maintain multi-tier brand portfolios to meet diverse clinic needs.

5. Dental Tourism Infrastructure Expanding Total Procedure Volumes

Countries such as Hungary, Poland, and Croatia are developing strong dental tourism infrastructure, offering implants at lower costs than in Western Europe. This trend contributes to increased total procedure volumes across the continent and adds a meaningful incremental demand layer beyond domestic patient populations.

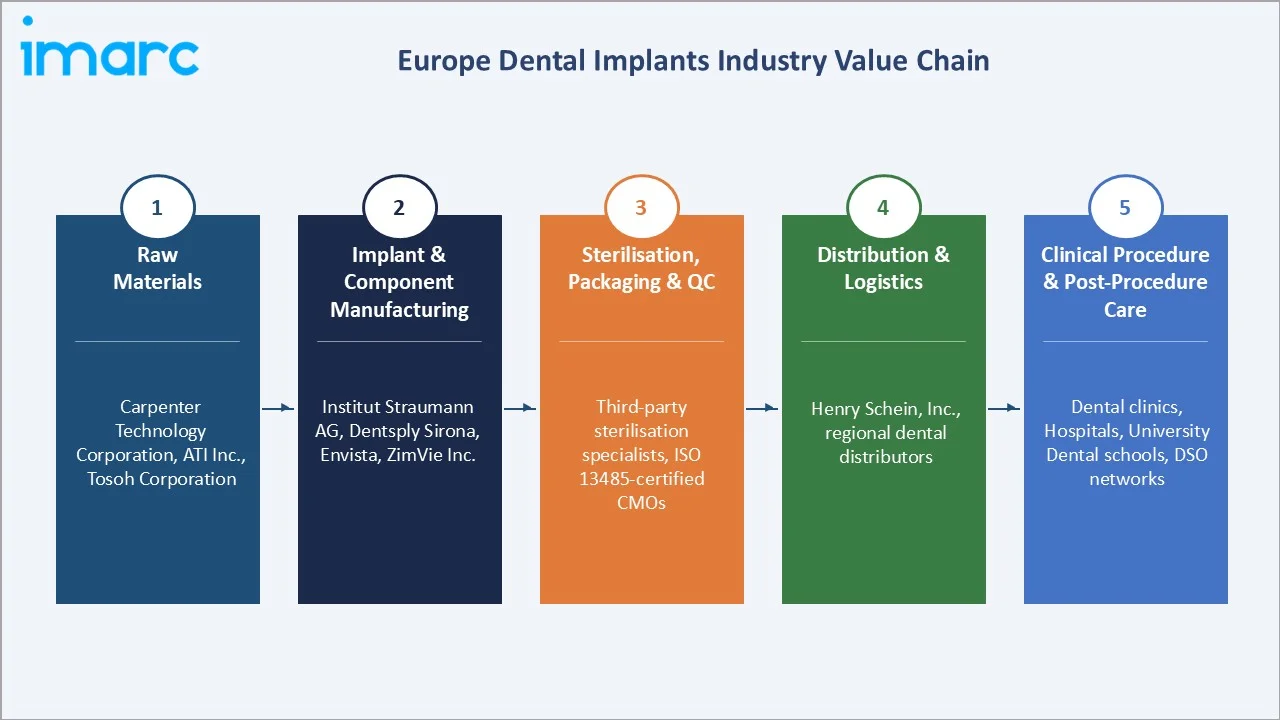

Industry Value Chain Analysis

The European dental implants value chain spans five integrated stages from raw material supply through post-procedure clinical care. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements critical to overall market performance.

|

Stage |

Key Players / Examples |

|

Raw Materials (Titanium Grade 4, Zirconia Powder) |

Carpenter Technology Corporation, ATI Inc., Tosoh Corporation |

|

Implant & Component Manufacturing |

Institut Straumann AG, Dentsply Sirona, Envista, ZimVie Inc. |

|

Sterilisation, Packaging & Quality Control |

Third-party sterilisation specialists, ISO 13485-certified CMOs |

|

Distribution & Logistics to Dental Practices |

Henry Schein, Inc., regional dental distributors |

|

Clinical Procedure & Post-Procedure Care |

Dental clinics, hospitals, university dental schools, DSO networks |

Tier-1 implant manufacturers occupy the highest strategic value position in the dental implants value chain, integrating raw material procurement, precision machining, surface treatment, and clinical support services within vertically integrated models. This position is reinforced by clinical training programmes, digital workflow ecosystems, and evidence-based marketing that create durable switching costs among implantologist user communities.

Technology Landscape in the European Dental Implants Industry

Implant Surface Technologies: SLA, SLActive, and Nanostructured Surfaces

The dental implant surface technology landscape is undergoing continuous advancement. Sandblasted and acid-etched (SLA) surfaces have been the industry benchmark for over two decades, offering reliable osseointegration across a wide range of clinical conditions. Straumann's SLActive hydrophilic surface technology, which maintains continuous surface wetting to accelerate bone cell attachment, represents the current premium tier, reporting osseointegration within 3-4 weeks. Nanostructured surface modifications creating micro-scale roughness patterns mimicking bone matrix architecture are entering commercial deployment through Dentsply Sirona's OsseoSpeed and other companies.

Digital Workflow Integration: CBCT, CAD/CAM, and Guided Surgery

The complete digital implant workflow has emerged as a key competitive differentiator for premium European dental practices. Cone-beam computed tomography (CBCT) provides three-dimensional bone volume mapping essential for implant position planning. Digital intraoral scanning eliminates traditional physical impressions, with systems from Dentsply Sirona (Primescan) now standard in tier-one practices. CAD/CAM-milled prosthetic components, guided surgical stents derived from digital treatment plans, and integrated case management platforms complete the end-to-end digital workflow ecosystem that premium manufacturers use to differentiate their clinical offering.

Zirconia Material Science: Y-TZP and Second-Generation Monolithic Systems

Yttria-stabilised tetragonal zirconia polycrystal (Y-TZP) remains the gold standard for zirconia implant bodies, offering flexural strength of approximately 900-1,200 MPa. However, first-generation zirconia implants experienced fracture risk in posterior high-load positions. Second-generation multi-layer zirconia with gradient structures combining opacity-optimised aesthetic layers with stronger structural cores entered commercial availability in Europe in 2022-2023 via Straumann's PURE Ceramic system and CeraRoot monolithic implants, significantly broadening the clinical application range of metal-free implants.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Material | Titanium Dental Implants | 72.4% |

2025 |

| Product | Endosteal Implants | 🔒 |

2025 |

| End Use | Dental Clinics | 48.3% |

2025 |

| Country | Germany | 28.4% |

2025 |

By Material

Titanium Dental Implants command a 72.4% majority share in 2025, reflecting the industry-wide dominance of titanium as the gold standard implant material backed by over 40 years of peer-reviewed clinical evidence and universal regulatory acceptance across all major European healthcare frameworks.

To access detailed market analysis, Request Sample

Zirconium Dental Implants hold a 27.6% share in 2025 and represent the fastest-growing segment, driven by patient preference for metal-free restorations, growing clinical evidence supporting Y-TZP osseointegration performance, and above-average adoption in high-income patient segments across Western Europe, where aesthetic outcomes carry a significant premium.

By End Use

Dental Clinics lead end-use channels with a 48.3% share in 2025, reflecting the outpatient and elective nature of most dental implant procedures and the high density of specialist implant practices across Western Europe.

Hospitals account for 28.6% in 2025, primarily addressing complex implant cases requiring general anaesthesia, sinus augmentation, or multi-disciplinary surgical coordination. Academic and Research Institutes at 14.4% reflect Europe's strong tradition of clinical implantology research and the dual training-and-patient-care role of university dental schools across the continent.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

28.4% |

Strong reimbursement framework, ~64,000 dental practices, high digital implantology adoption, leading domestic manufacturers |

|

France |

20.6% |

Rising private dental insurance uptake, expanding clinic networks, an ageing population, and dental tourism origin flows. |

|

United Kingdom |

18.3% |

Growth in private dental spending, the implant tourism market, rapid digital workflow adoption, and premium clinic consolidation |

|

Italy |

14.2% |

Large elderly population (23.5% aged 65+), high dental awareness, active dental tourism corridor with CEE markets |

|

Spain |

10.4% |

Dental tourism destination hub, growing implant-focused DSO chains, and expanding SME dental sector |

|

Others |

8.1% |

Growing CEE markets (Poland, Czech Republic, Romania), rising incomes, and expanding private dental insurance |

Germany commands a 28.4% share in 2025, the highest national share in the European dental implants market, driven by a systematic dental care infrastructure, registered implantologists, and partial insurance reimbursement frameworks that significantly lower patient cost barriers relative to other European markets.

France, at 20.6%, is supported by rapidly expanding private dental insurance penetration and a well-networked national dental association driving continuing implantology education. The United Kingdom, with 18.3%, is characterised by strong private dental spending growth post-NHS reform, with premium implant centres concentrated in London, Manchester, and Edinburgh, driving above-average per-procedure revenues across the market.

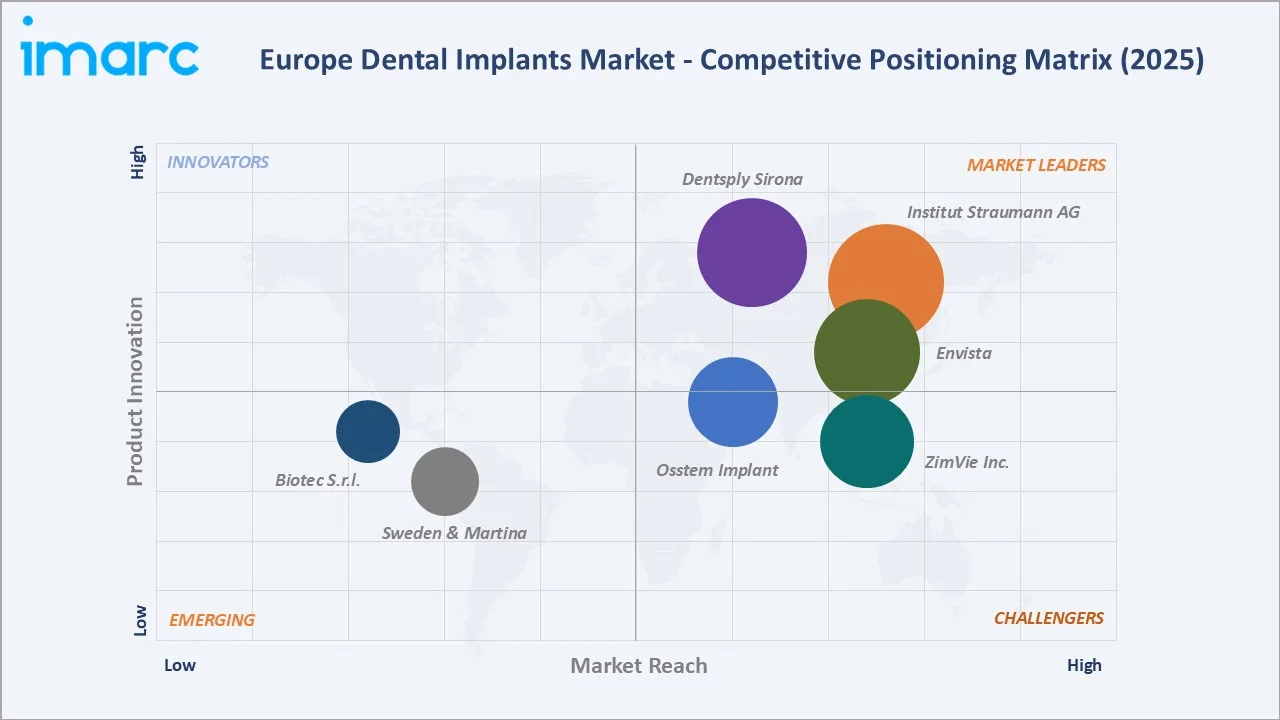

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Institut Straumann AG |

Straumann, Neodent, Medentika |

Leader |

Premium implants, SLActive surface technology, full digital workflow ecosystem |

|

Dentsply Sirona |

Ankylos, Astra Tech EV, XiVE |

Leader |

Full dental ecosystem, Primescan, guided surgery, DS Core digital platform |

|

Envista |

Nobel Biocare |

Leader |

All-on-4 full-arch system, immediate loading protocols, aesthetic focus |

|

ZimVie Inc. |

T3 Pro, Tapered Screw-Vent |

Challenger |

Hospital-grade products, bone augmentation systems, and maxillofacial integration |

|

Osstem Implant |

Osstem, Hiossen |

Challenger |

Value-to-mid segment pricing, aggressive Central and Eastern Europe expansion |

|

Sweden & Martina S.p.A. |

Sweden & Martina Implants |

Emerging |

Italy-centric operations, bone-level micro-implant specialisation |

|

Biotec S.r.l. |

BTK Implants |

Emerging |

Italian domestic market focus, educational clinical programme development |

The European dental implants competitive landscape is characterised by a small number of global premium manufacturers at the market leadership tier, competing principally on clinical evidence quality, digital workflow integration, and multi-brand portfolio coverage across price segments. Five global leaders collectively account for approximately 60-65% of total European revenue in 2025.

Key Company Profiles

Institut Straumann AG

Institut Straumann AG is a dental implant systems company, headquartered in Basel, Switzerland. The company operates across all dental implant market tiers through its multi-brand strategy, offering premium (Straumann), value-premium (Neodent), and value-segment (Medentika) products across European and global markets.

- Product & Platform Portfolio: Straumann BLX, BLT, TLX implant systems; Neodent Grand Morse; Medentika restorations; Dental Wings digital lab platform; ClearCorrect clear aligner system.

- Recent Developments: In November 2025, Straumann Group announced new partnerships to reshape its orthodontics business around ClearCorrect, combining technology collaboration with changes to its production footprint and commercial focus.

- Strategic Focus: Multi-brand total market coverage across all price tiers, SLActive surface premiumisation, digital ecosystem integration through Dental Wings, and CEE value-market expansion via Medentika.

Dentsply Sirona

Dentsply Sirona is a US-headquartered dental products company with major European manufacturing facilities in Germany and Sweden. It has a strong European presence through its Ankylos, Astra Tech EV, and XiVE implant lines that command significant market share in the DACH region.

- Product & Platform Portfolio: Ankylos, Astra Tech EV, XiVE implant systems; Primescan intraoral scanner; SureSmile guided implant surgery; DS Core integrated digital platform for case management.

- Recent Developments: In March 2025, Dentsply Sirona presented its latest advancements in digital dentistry at the International Dental Show (IDS) 2025 in Cologne, Germany.

- Strategic Focus: Full dental ecosystem integration, DS Core digital connectivity, hospital-sector penetration in Germany and France, and cross-portfolio compatibility across implant, imaging, and prosthetic restoration categories.

Envista

Envista is a US-headquartered dental products and technology group with a global footprint, supporting dental professionals across Europe, the Americas, and Asia. It operates through a portfolio of over 30 trusted dental brands.

- Product & Platform Portfolio: Nobel Biocare, Implant Direct, Alpha-Bio, DTX Studio, Dexis, Orascoptic

- Recent Developments: In February 2022, Envista Holdings Corporation renewed its partnership agreement with the Vitaldent Group. This agreement positions Envista as the preferred supplier of implants (Nobel Biocare) and clear aligners (Spark).

- Strategic Focus: Immediate loading protocol leadership, All-on-4 clinical network expansion across southern Europe, and implant tourism clinical centre partnerships.

Market Concentration Analysis

The European dental implants market demonstrates a moderate-to-high level of concentration, with a limited group of Tier-1 manufacturers dominating regional revenues. Leading companies such as Institut Straumann AG, Dentsply Sirona, Envista Holdings Corporation, ZimVie Inc., and Osstem Implant collectively account for a significant share of the regional market—commonly estimated at around 60–65% of total revenues as of 2025, based on industry analyses and company disclosures.

Among these, Institut Straumann AG maintains a clear leadership position, supported by a multi-brand portfolio strategy that spans premium, mid-range, and value segments. Its portfolio includes brands such as Straumann, Neodent, and Medentika, enabling broad coverage across diverse customer segments and geographies in Europe.

Structurally, the market reflects a bifurcated dynamic. The premium OEM segment continues to undergo consolidation, driven by strategic acquisitions and portfolio expansion initiatives. Notably, Straumann’s acquisitions of Neodent (Brazil) and Medentika (Germany) have strengthened its presence in the value and challenger segments, thereby expanding its total addressable market while reinforcing its leadership in the premium category. This evolving competitive landscape highlights a dual trend: ongoing consolidation at the high-end of the market, alongside increasing competition in the value segment, particularly from price-competitive and regionally focused manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Zirconium Dental Implants represent the highest-growth material sub-segment, driven by patient preference for metal-free aesthetics, above-average adoption in premium clinics across Germany and Switzerland, and second-generation monolithic zirconia systems overcoming earlier fracture risk concerns.

Emerging Market Expansion

Central and Eastern European markets, including Poland, the Czech Republic, Romania, and Hungary, represent the fastest-growing geographic frontiers within Europe, with implant volume CAGRs estimated at 5-7% over 2026-2034, significantly above the Western European average of approximately 1.5-2.0%. Rising household incomes, expanding private dental insurance penetration, and the growth of dental tourism destination infrastructure are the primary demand catalysts supporting investment opportunities.

Venture & Strategic Investment Trends

Notable investment activity includes Straumann Group's continued portfolio expansion, DSO consolidation transactions attracting private equity capital from Nordic Capital and KKR across Germany, Spain, and the UK, and venture investment into AI-assisted treatment planning platforms, including Overjet and Pearl.

Future Market Outlook (2026-2034)

The Europe dental implants market forecast projects steady value expansion from USD 2.57 Billion in 2025 to USD 3.28 Billion by 2034, representing a CAGR of 2.50%. While Western European markets will continue providing a stable high-volume base, the growth narrative over 2026-2034 will increasingly be shaped by Central and Eastern Europe's dental infrastructure development, the rapid commercial scaling of full-arch immediate loading protocols, and AI-driven personalised implant planning emerging as a standard clinical tool across tier-one practices.

Three structural dynamics are most likely to reshape the European dental implants market through 2034. First, DSO consolidation will accelerate platform standardisation, concentrating purchasing power among fewer, larger procurement entities and favouring manufacturers with multi-tier brand portfolios. Second, zirconia material science advances will progressively expand the clinical indications for metal-free implants beyond anterior aesthetics into posterior load-bearing applications. Third, digital workflow integration will shift competitive advantage from component hardware toward software ecosystems, clinical training programmes, and data-driven outcome analytics.

By 2034, the European dental implants industry is forecast to have completed its transition from a hardware-centric medical device market toward a digital clinical solution ecosystem, where manufacturers compete primarily on integrated digital workflows, AI-assisted planning capabilities, and outcomes-based commercial models rather than on component specifications alone.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews conducted in 2024-2025 with dental implantologists, oral and maxillofacial surgeons, procurement managers of DSO networks and hospital dental departments, implant distributor executives, and dental insurance professionals across Germany, France, the United Kingdom, Italy, and Spain. Interviews were supplemented by structured survey questionnaires capturing quantitative adoption metrics, purchasing criteria, and technology investment priorities.

Secondary Research

Secondary sources include regulatory filings and CE-Mark databases (EUDAMED), Eurostat health statistics and population ageing reports, European Association of Osseointegration (EAO) congress proceedings, peer-reviewed implantology literature from Clinical Oral Implants Research and the European Journal of Oral Implantology (2020-2025), company annual reports, and national dental association market surveys covering all five major country markets.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up and top-down forecasting models. Bottom-up estimation proceeded by country, material segment, product type, and end-use channel, cross-validated against total implant unit volume benchmarks and average selling price analysis. Forecast models incorporate macroeconomic variables including GDP per capita growth, dental care expenditure growth rates, ageing index trajectories, private dental insurance penetration, and dental tourism flow data.

Europe Dental Implants Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Titanium Dental Implants, Zirconium Dental Implants |

| Products Covered | Endosteal Implants, Subperiosteal Implants, Transosteal Implants, Intramucosal Implants |

| End Uses Covered | Hospitals, Dental Clinics, Academic and Research Institutes, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Institut Straumann AG, Dentsply Sirona, Envista, ZimVie Inc., Osstem Implant, Sweden & Martina S.p.A., Biotec S.r.l., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe dental implants market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe dental implants market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe dental implants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Dental Implants Market Report

The Europe dental implants market was valued at USD 2.57 Billion in 2025, driven by ageing demographics, rising edentulism rates, and digital implantology adoption across major European markets.

The market is projected to reach USD 3.28 Billion by 2034, growing at a CAGR of 2.50% during 2026-2034, driven by demographic ageing, zirconia premiumisation, and Central and Eastern European market expansion.

Titanium Dental Implants lead the material segment with a 72.4% share in 2025, owing to superior osseointegration properties, decades of clinical validation, and cost-effectiveness across all European healthcare settings.

Dental Clinics lead with a 48.3% share in 2025, driven by the high density of specialist outpatient dental practices offering same-day immediate loading implant protocols across Germany, France, and the United Kingdom.

Germany dominates with a 28.4% share in 2025, supported by robust dental infrastructure, partial insurance reimbursement policies, approximately 64,000 registered dental practices, and strong domestic implant manufacturers.

Key drivers include Europe's ageing population (20.3% aged 65+ in 2024 per Eurostat), rising edentulism rates, digital implantology adoption (CBCT, AI planning, guided surgery), and expanding private dental insurance penetration.

Zirconium Dental Implants are the fastest-growing material segment, driven by patient preference for metal-free restorations and second-generation monolithic zirconia system availability, addressing earlier fracture risk limitations.

Leading companies include Institut Straumann AG, Dentsply Sirona, Envista, ZimVie Inc., Osstem Implant, Sweden & Martina S.p.A., and Biotec S.r.l.

CBCT imaging, AI-assisted treatment planning, guided surgery stents, and intraoral digital scanning are improving surgical precision, expanding patient eligibility, and enabling same-day implant protocols in European dental centres.

CEE markets, including Poland, the Czech Republic, and Romania, are growing at a 5-7% CAGR, significantly above the European average of 2.50%, driven by rising incomes, expanding private dental insurance, and dental tourism infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)