Europe Display Market Size, Share, Trends and Forecast by Display Type, Technology, Application, Industry Vertical, and Country, 2026-2034

Europe Display Market Summary:

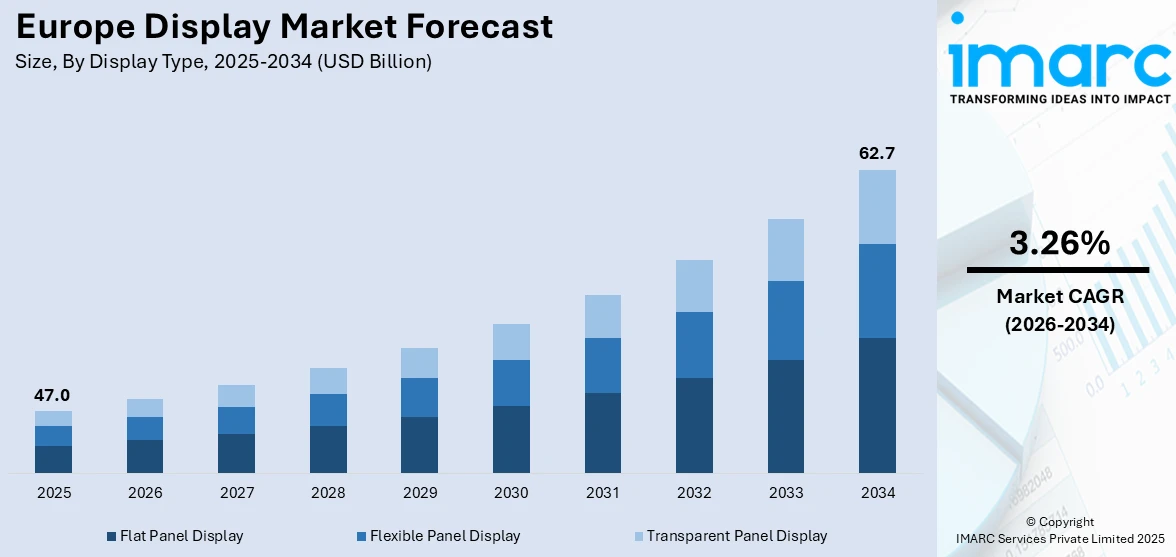

The Europe display market size was valued at USD 46.96 Billion in 2025 and is projected to reach USD 62.71 Billion by 2034, growing at a compound annual growth rate of 3.26% from 2026-2034.

The Europe display market is witnessing an appreciable growth trajectory as various industries throughout the region are increasingly embracing high-end visual technology solutions with respect to their products and/or services. As the consumer base is becoming more quality-conscious with respect to the quality of visual displays, the increased need for energy-efficient and visually engaging display solutions is impacting the Europe display market share positively. Thus, the rise of connected device networks and the progress of smart infrastructure development are boosting the Europe display market.

Key Takeaways and Insights:

- By Display Type: Flat panel display dominates the market with a share of 70% in 2025, driven by widespread adoption in televisions, monitors, laptops, and smartphones across the region.

- By Technology: OLED leads the market with a share of 33% in 2025, owing to its superior color accuracy, energy efficiency, and growing integration across premium consumer electronics devices.

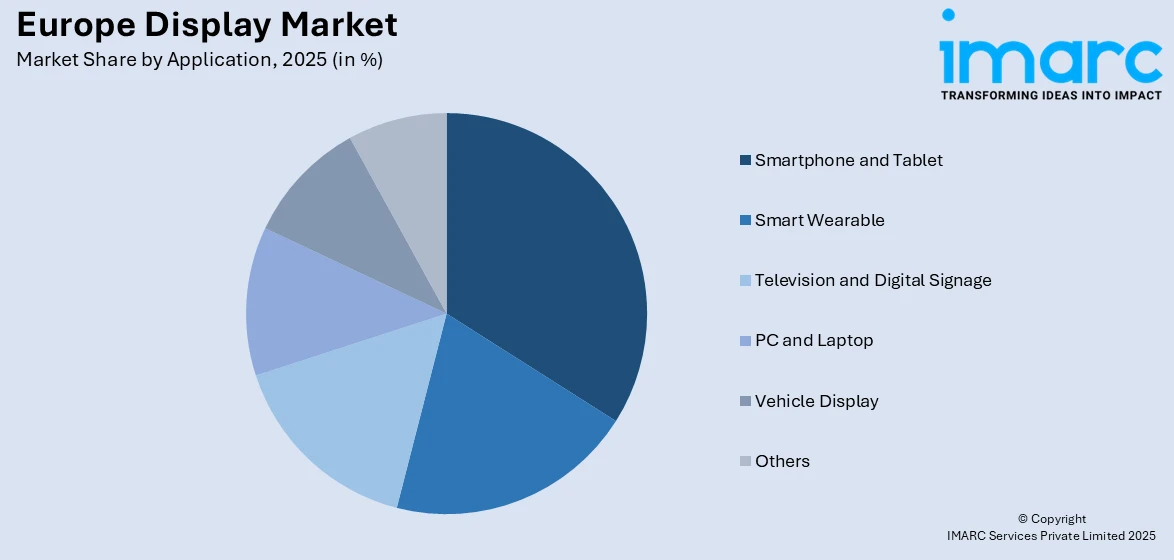

- By Application: Smartphone and tablet hold the largest share of 35% in 2025, reflecting sustained consumer demand for high-resolution portable displays and frequent device upgrade cycles.

- By Industry Vertical: Consumer electronics dominates the market with a share of 34% in 2025, supported by the region’s high household penetration of smart televisions, gaming monitors, and personal computing devices.

- Key Players: The Europe display market features a competitive landscape with established technology manufacturers focusing on product innovation, capacity expansion, strategic partnerships, and next-generation display development to strengthen their regional market position.

To get more information on this market Request Sample

The display market in Europe is heading for progress due to the encouragement of advanced visual technologies in the region across consumer, commercial, and industrial verticals. The use of organic light-emitting diode display and flexible display solutions has been increasingly noted to be in development, which would show advanced energy performance and design versatility. For example, at IAA MOBILITY 2025 in Munich, Samsung Display showcased a range of next‑generation automotive OLED displays, including flexible and multi‑lamination digital cockpit solutions, and officially launched its dedicated DRIVE™ automotive OLED brand, reinforcing OEM interest in advanced displays for mobility. Stricter European regulations for energy efficiency and sustainability are motivating manufacturers to develop environmentally friendly display products. Moreover, the rapid progression of automotive demand for integrated cockpit displays and digital instrument clusters is inviting more growth opportunities. Increased digital signage networks across retail, transportation, and hospitality segments are encouraging the demand for advanced flat panel and transparent display solutions across the region.

Europe Display Market Trends:

Rising Adoption of OLED and Next-Generation Display Technologies

There is a significant move in Europe from traditional liquid crystal display technology to organic light-emitting diode and other display technologies. For instance, in 2025 LG Display reported that sales of OLED TVs in Europe hit record highs in the first quarter of the year, prompting the company to boost production capacity and invest in new OLED technology facilities, reflecting strong regional uptake of high‑performance panels over LCDs. There is a greater need for enhanced color gamut, higher contrast ratios, and lesser thickness, and investment in R&D is giving the technological industry a large push in relation to high-quality display products in the region for TV sets, smartphones, and many other products where displays are used.

Expanding Integration of Displays in Automotive Applications

The European automotive industry is embracing advanced display technologies quickly, and the dashboard display, infotainment display, and heads-up displays in the region have turned into standard fare on premium-class as well as mid-range models. The move toward connected and autonomous driving has driven the adoption of displays. At IAA Mobility 2025 in Munich, Valeo and Ennostar partnered to unveil an advanced Mini LED high‑definition automotive exterior display, showcasing a next‑generation digital signaling system with superior brightness and resolution. This technology expands the role of vehicle displays beyond the cabin to exterior safety and V2X communication.

Growing Demand for Digital Signage and Interactive Displays

Digital signage as well as interactive display technologies are gaining importance in European retail, hospitality, transportation, and corporate spaces, including business environments. These display technologies are being utilized for effective and captivating business communications, customer engagement, and information dissemination. For example, at Integrated Systems Europe (ISE) 2025, Europe’s largest display tech exhibition, Samsung Electronics showcased award‑winning AI‑driven digital signage solutions, including interactive and transparent MICRO LED displays. These demonstrations highlight how advanced signage technology is being positioned for use in retail storefronts, corporate lobbies, hotels, and transit hubs across the region. The growing importance of smart cities and digital infrastructure development is fueling the adoption of transparent display technologies in this particular region as well.

Market Outlook 2026-2034:

The Europe display market is positioned for sustained growth, driven by continuous technological innovation, expanding application areas, and rising consumer demand for premium visual experiences across diverse sectors. The increasing integration of advanced display solutions in automotive, healthcare, retail, and industrial environments is broadening the market's revenue base. Supportive regulatory frameworks promoting energy-efficient technologies, coupled with the region's strong emphasis on digital transformation and smart infrastructure development, are further reinforcing long-term growth prospects and creating a more competitive and dynamic display landscape across Europe. The market generated a revenue of USD 46.96 Billion in 2025 and is projected to reach a revenue of USD 62.71 Billion by 2034, growing at a compound annual growth rate of 3.26% from 2026-2034.

.webp)

Europe Display Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Display Type |

Flat Panel Display |

70% |

|

Technology |

OLED |

33% |

|

Application |

Smartphone and Tablet |

35% |

|

Industry Vertical |

Consumer Electronics |

34% |

Display Type Insights:

- Flat Panel Display

- Flexible Panel Display

- Transparent Panel Display

The flat panel display dominates with a market share of 70% of the total Europe display market in 2025.

Flat panel displays are continuing to underpin the Europe display market, as these are used ubiquitously across diverse categories of consumer electronics devices, signages, and industrial monitoring systems. These are known for their flat nature, lightweight design, and high resolution. Flat panel displays are being used in televisions, monitors, laptops, and signages. For example, in May 2025 Sony Europe announced it would debut a world‑first dynamic eye‑responsive advertising display powered by AI on its professional BRAVIA flat panel screens at the Digital Signage Summit Europe, demonstrating how flat panels are evolving beyond static use and gaining traction in interactive commercial environments across the region. The increasing demand from European consumers for large-size displays is adding strength to this particular display market. The quest for large-size displays itself is serving to increase demand for flat panel displays.

Moreover, it is worth mentioning that the adoption of flat panel displays will continue to be furthered through improvements made in backlighting technologies, panel refresh rates, and color quality standards, particularly for professional and entertainment-oriented environments. European companies are adopting flat panel display technologies as an optimal option for corporate, control room, and public information system environments, thus furthering the business requirements for effective communication tools. Moreover, there are applications of this technology within the education and healthcare segments of society, extending the overall application potential of this technology within the region.

Technology Insights:

- OLED

- Quantum Dot

- LED

- LCD

- E-Paper

- Others

The OLED leads with a share of 33% of the total Europe display market in 2025.

Organic light-emitting diode technology has started to gain a lead as the preferred display solution throughout Europe, with its capability for excellent color accuracy, true black levels, and higher energy efficiency than conventional displays. The increasing penetration of OLED panels into premium smartphones, high-end TVs, and gaming monitors strengthens its positioning in the market. Both European consumers and manufacturers are increasingly leaning toward OLED technology because of its thinner form factors and flexible design capabilities, thus opening more innovative product development avenues across several consumer and commercial device categories.

This is also driven by the increasing OLED panel penetration into automotive cockpit displays, wearable devices, and professional-grade monitors, which all require high color calibration and good contrast performances. In this regard, European car manufacturers have installed digital instrument clusters and infotainment systems with OLED panels to take users' in-car visual experiences to the next level. Moreover, manufacturing processes are getting better little by little, improving production yields while gradually lowering costs, which makes the OLED display products increasingly accessible in more mid-range product categories and supports wider market diffusion across the region.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Smartphone and Tablet

- Smart Wearable

- Television and Digital Signage

- PC and Laptop

- Vehicle Display

- Others

The smartphone and tablet dominate with a market share of 35% of the total Europe display market in 2025.

High smartphone penetration, coupled with the trend of frequent replacement cycles, has continuously driven growth in the Europe display market, with the most significant revenue contribution coming from the smartphone and tablet segment. Moreover, there is an ever-growing demand for high-resolution, colorful, and power-efficient displays in portable devices across Europe. In 2025, Chinese smartphone maker Oppo said at the launch of its Find X9 Pro in Barcelona that AI‑powered features are expected to encourage European consumers under 35 to replace their devices more often, highlighting how innovations in display‑driven features could help sustain upgrade cycles in the region. The transition toward premium handsets that boast larger screens, foldable designs, and improved touch responsiveness continues to generate substantial demand for value-added display panels. The increasing usage of tablets as productivity and entertainment devices is driving the demand for quality display technologies.

This segment is further agrarian due to the widening access to high-definition and ultra-high-definition-capable content to view on portable devices. The functions of streaming services, mobile gaming, and augmented reality have further forced consumers to turn toward devices with superior display capabilities such as higher refresh rates and wider color gamuts. European manufacturers and retailers are responding to increasing demand by offering a wider variety of smartphone and tablet models featuring advanced display technologies to meet diverse consumer preferences at multiple price points, further strengthening the segment to drive the market expansion.

Industry Vertical Insights:

- BFSI

- Retail

- Healthcare

- Consumer Electronics

- Military and Defense

- Automotive

- Others

The consumer electronics leads with a share of 34% of the total Europe display market in 2025.

Consumer electronics is the primary industry segment of the display market in Europe. This segment is attributed to the significant consumption of smart TV sets, gaming consoles, personal computers, and other portable entertainment devices by individuals residing in the region. The European consumer places significant emphasis on display visualization, thereby leading to the adoption of high-end display technologies by manufacturers of consumer electronic devices. Similarly, the increasing trend of using high-definition gaming and streaming services is resulting in the adoption of premium display panels with high refresh rates.

The consumer electronics space continues to be fueled by the progression of new product categories that require state-of-the-art display technologies, including virtual reality equipment, home electronics, and innovative portable media players. Over the past few years, there has been an increase in the number of households in Europe that are adopting a multiview or multiscreening experience between their TVs, computer monitors, and other personal devices. This has led to new advancements in displays that allow for better interconnectivity, efficiency, and quality, thereby sustaining the consumer electronics space as a driver of growth in the Europe display market.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany represents a key market for displays in Europe, supported by its strong automotive and consumer electronics manufacturing base. The country's emphasis on technological innovation and industrial digitalization is driving consistent demand for advanced flat panel and OLED display solutions. Growing integration of high-resolution displays in automotive cockpits, smart manufacturing systems, and retail environments is further reinforcing Germany's prominent position within the regional display landscape.

France is witnessing growing demand for display technologies, driven by expanding retail digitalization, rising consumer electronics adoption, and investments in smart city infrastructure. The country's thriving creative, media, and entertainment sectors further support the deployment of premium visual solutions. Increasing adoption of digital signage across transportation hubs, hospitality venues, and public institutions is creating additional opportunities for advanced display integration throughout the country.

The United Kingdom's display market is bolstered by strong consumer spending on smart televisions, gaming devices, and portable electronics. Growing digital signage adoption across retail, hospitality, and transportation sectors is further contributing to market expansion. The country's well-established technology ecosystem and increasing enterprise demand for interactive display solutions in corporate and educational environments are sustaining consistent growth across multiple application segments.

Italy is experiencing steady growth in display adoption, supported by increasing demand from its automotive and fashion retail industries. The country's emphasis on design-forward consumer electronics and expanding digital signage networks is encouraging the integration of modern display technologies. Rising investments in tourism-driven digital infrastructure and the modernization of public communication systems are further contributing to the growing deployment of advanced displays.

Spain's display market is growing as the country invests in digital infrastructure and smart tourism initiatives. Rising consumer preference for high-definition televisions and smartphones, along with expanding commercial display applications in retail and hospitality, is supporting market development. The government's focus on urban digitalization and sustainable technology adoption is further encouraging the integration of energy-efficient display solutions across public and private sectors.

The remaining European countries are collectively contributing to the display market's expansion through increasing consumer electronics adoption, rising digital signage deployment, and growing investments in smart infrastructure. Nations across Scandinavia, Benelux, and Eastern Europe are progressively embracing advanced display technologies in retail, healthcare, and transportation applications, supported by improving digital connectivity and expanding commercial modernization initiatives throughout the region.

Market Dynamics:

Growth Drivers:

Why is the Europe Display Market Growing?

Accelerating Digital Transformation Across Industries

The Europe display market is being propelled by the region’s accelerating digital transformation across key industries, including retail, healthcare, automotive, and financial services. Businesses are rapidly adopting advanced display solutions to enhance customer experiences, streamline operations, and improve visual communication. As per sources, PPDS (Philips Professional Display Solutions) launched its ultra‑wide 32:9 Philips Stretch 3150 digital signage display, designed for retail, transportation, healthcare, hospitality, and public venues. The launch demonstrates how professional display makers are expanding their product portfolios to support diverse commercial and institutional digital transformation use cases across the region. Interactive touchscreens, digital dashboards, and smart kiosks are becoming integral to modern commercial environments, creating sustained demand for high-quality display technologies. The broader push toward paperless operations and data-driven decision-making is further encouraging the deployment of digital displays in conference rooms, control centers, and public-facing interfaces, reinforcing the market’s growth trajectory.

Rising Consumer Demand for Premium Visual Experiences

European consumers are increasingly seeking superior visual experiences across their personal devices and home entertainment systems. The growing popularity of high-definition streaming content, immersive gaming, and augmented reality applications is driving demand for displays with higher resolutions, wider color gamuts, and improved refresh rates. Reflecting this trend, LG Electronics in 2025 became the first brand to surpass 10 million OLED TV sales in Europe, highlighting strong regional consumer preference for premium self‑emissive display technology that delivers exceptional picture quality and immersive viewing experiences. Manufacturers are responding by introducing innovative products that deliver enhanced picture quality and energy efficiency. This consumer-driven preference for premium viewing experiences is accelerating the adoption of advanced display technologies, including organic light-emitting diode and quantum dot solutions, across televisions, monitors, smartphones, and wearable devices throughout the region.

Expanding Automotive Display Integration

The European automotive sector’s shift toward connected, electric, and autonomous vehicles is creating significant opportunities for display manufacturers. Modern vehicles increasingly feature multi-display cockpit configurations, including digital instrument clusters, central infotainment screens, heads-up displays, and rear-seat entertainment systems. This trend is driven by consumer expectations for seamless digital experiences inside vehicles and regulatory requirements for advanced driver assistance interfaces. In January 2026, HARMAN, the automotive technology unit under Samsung Electronics, introduced a suite of advanced in‑vehicle visual display technologies engineered to deliver smarter, context‑aware digital cockpit experiences tailored for connected and autonomous driving platforms in Europe. The growing integration of curved, flexible, and transparent display technologies into vehicle interiors is establishing the automotive sector as a high-growth vertical, contributing meaningfully to the overall expansion of the Europe display market.

Market Restraints:

What Challenges the Europe Display Market is Facing?

High Manufacturing and Material Costs

The production of advanced display technologies, particularly organic light-emitting diode and micro-LED panels, involves complex manufacturing processes and expensive raw materials. These elevated costs are often passed on to end consumers, limiting mass-market adoption and constraining demand growth in price-sensitive segments. The reliance on specialized components sourced from global supply chains further amplifies cost pressures for European manufacturers.

Competition from Alternative Display Technologies

The emergence of competing display technologies, such as micro-LED and mini-LED, poses a challenge to the established market position of certain display solutions. As newer technologies continue to mature and demonstrate comparable or superior performance characteristics, some market segments face potential disruption. This evolving competitive landscape creates uncertainty for manufacturers investing in current-generation display production and can divert consumer and enterprise spending.

Supply Chain Dependencies and Geopolitical Risks

Europe’s display market remains heavily dependent on imported components and panels, primarily sourced from manufacturing hubs in East Asia. This reliance on external supply chains exposes the market to potential disruptions caused by geopolitical tensions, trade policy shifts, and logistical bottlenecks. Limited domestic panel manufacturing capacity further heightens vulnerability, creating challenges for European brands seeking to maintain consistent product availability and competitive pricing.

Competitive Landscape:

The Europe display market is characterized by a dynamic and competitive environment, with manufacturers continuously striving to differentiate their offerings through technological innovation, product design, and strategic positioning. Market participants are investing heavily in the development of next-generation display technologies, including organic light-emitting diode, micro-LED, and quantum dot solutions, to meet the region’s growing demand for superior visual performance and energy efficiency. Strategic partnerships between display producers and end-use industries, particularly automotive and consumer electronics, are becoming increasingly prevalent, enabling customized solutions that address specific application requirements. Additionally, companies are focusing on expanding their distribution networks and strengthening after-sales support across key European markets. The emphasis on sustainability and compliance with stringent European energy regulations is also shaping competitive strategies, as manufacturers prioritize eco-friendly production processes and recyclable materials to align with regional environmental standards.

Europe Display Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Display Types Covered | Flat Panel Display, Flexible Panel Display, Transparent Panel Display |

| Technologies Covered | OLED, Quantum Dot, LED, LCD, E-Paper, Others |

| Applications Covered | Smartphone and Tablet, Smart Wearable, Television and Digital Signage, PC and Laptop, Vehicle Display, Others |

| Industry Verticals Covered | BFSI, Retail, Healthcare, Consumer Electronics, Military and Defense, Automotive, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Display Market Research Report Report

The Europe display market size was valued at USD 46.96 Billion in 2025.

The Europe display market is expected to grow at a compound annual growth rate of 3.26% from 2026-2034 to reach USD 62.71 Billion by 2034.

The flat panel display held the largest share at 70%, driven by widespread adoption across televisions, monitors, laptops, and smartphones, supported by continuous advancements in panel resolution and energy efficiency.

Key factors driving the Europe display market include accelerating digital transformation across industries, rising consumer demand for premium visual experiences, expanding automotive display integration, growing digital signage deployment, and supportive regulatory frameworks promoting energy-efficient technologies.

Major challenges include high manufacturing and material costs for advanced display technologies, intensifying competition from emerging alternatives such as micro-LED, supply chain dependencies on East Asian component suppliers, geopolitical trade uncertainties, and limited domestic panel manufacturing capacity within the region.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade