Europe Dry Eye Syndrome Market Size, Share, Trends and Forecast by Disease Type, Drug Type, Product, Distribution Channel, and Country, 2026-2034

Europe Dry Eye Syndrome Market Size, Share, Trends & Forecast (2026-2034)

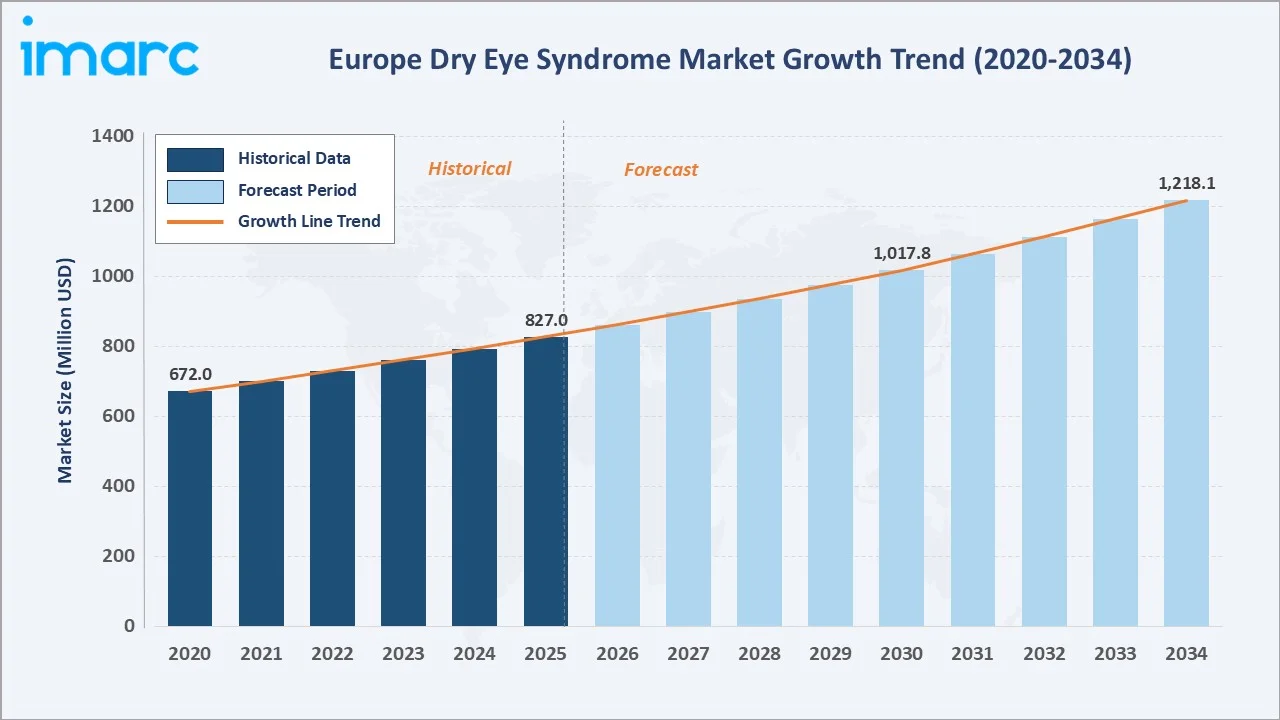

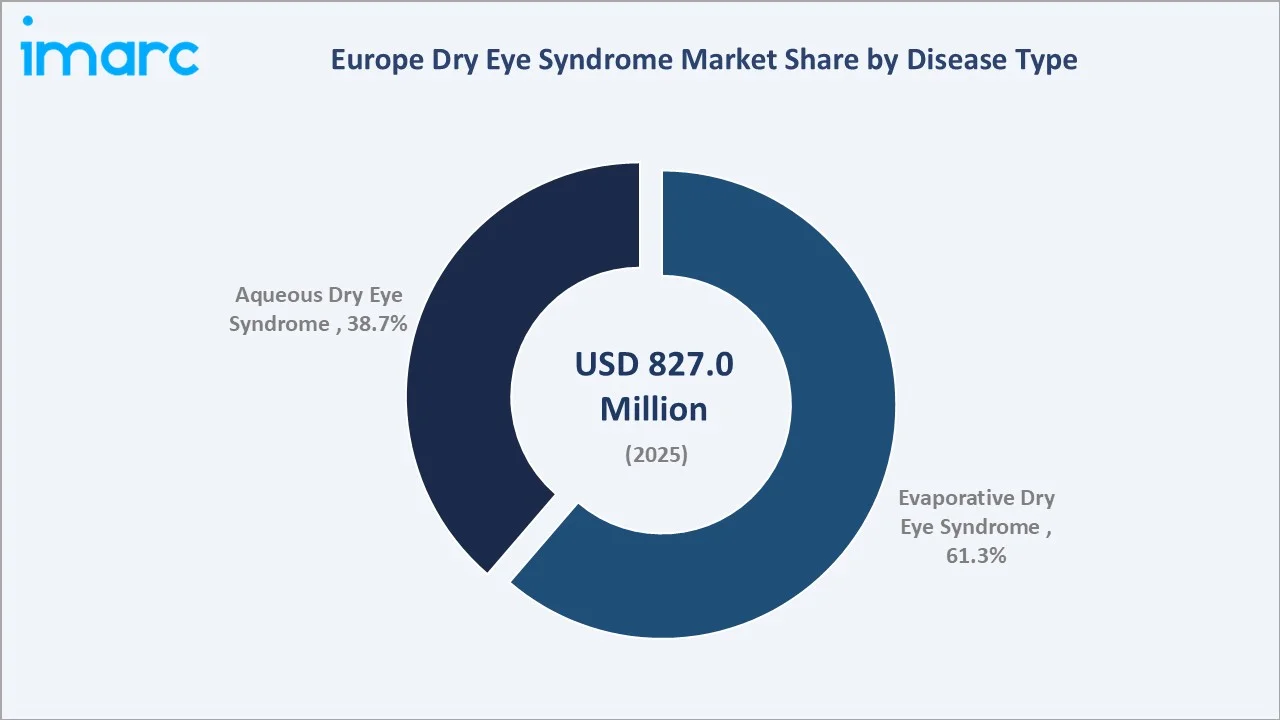

The Europe dry eye syndrome market was valued at USD 827.0 Million in 2025 and is projected to reach USD 1,218.1 Million by 2034, exhibiting a CAGR of 4.24% during the forecast period (2026-2034). Growth is anchored by an aging population, persistent digital screen exposure, and broadening adoption of preservative-free formulations. As per the ‘2025 International Study of Dry Eye Sufferers’ survey conducted across the United Kingdom, France, Germany, and Poland found that 58% of the adult respondents reported dry eye symptoms, underscoring a sizeable unmet demand pool.

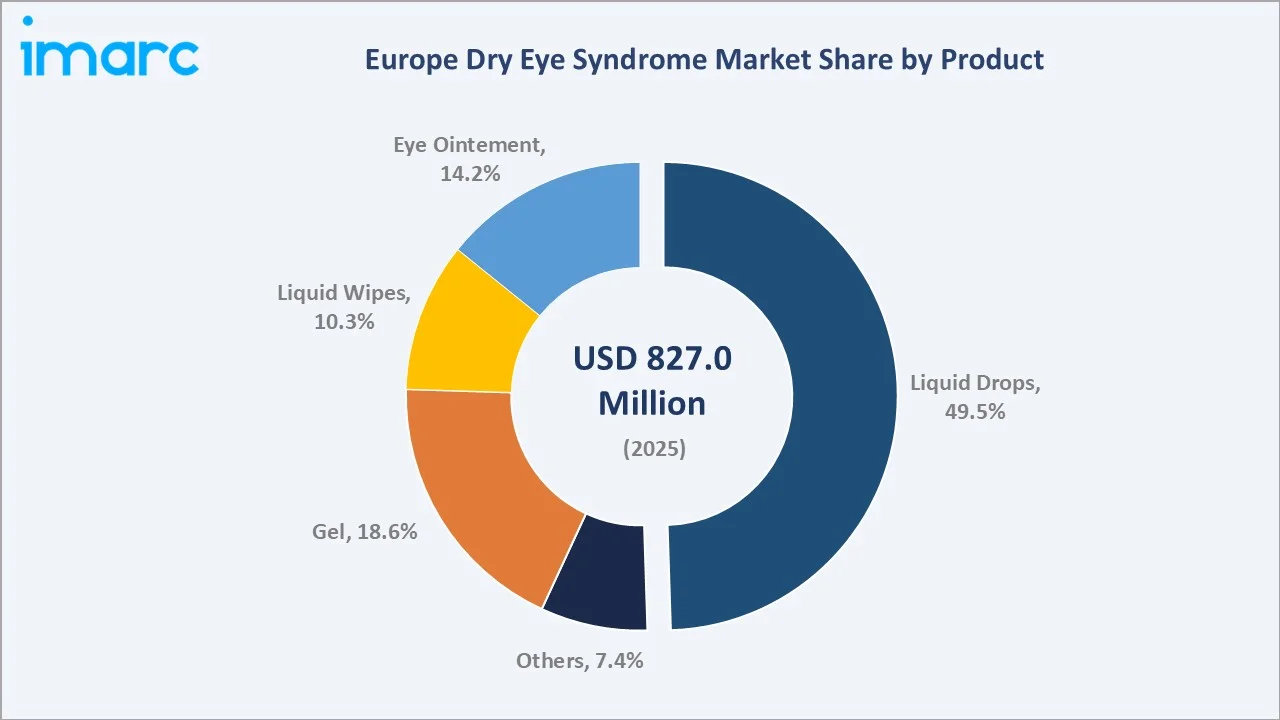

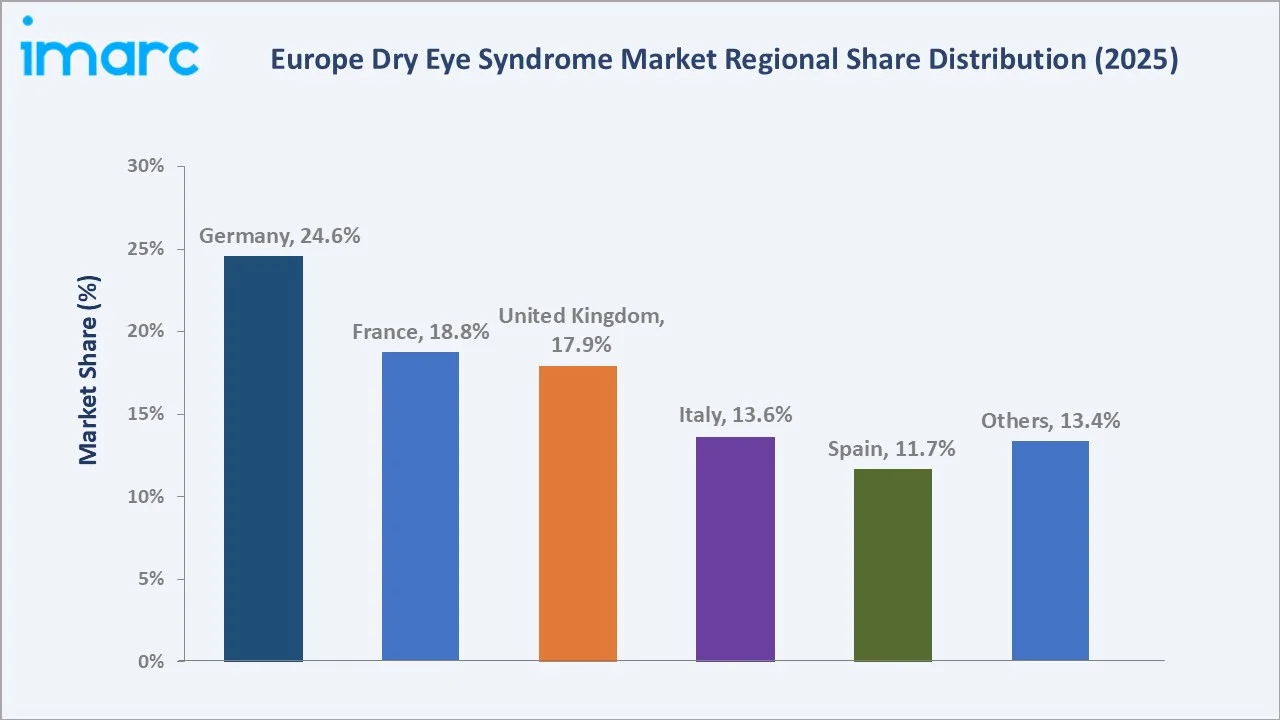

Evaporative dry eye syndrome leads the disease type segment at 61.3%, liquid drops dominate the product segment at 49.5%, and Germany commands 24.6% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 827.0 Million |

|

Forecast Market Size (2034) |

USD 1,218.1 Million |

|

CAGR (2026-2034) |

4.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Country |

Germany (24.6%, 2025) |

|

Fastest Growing Country |

Spain (11.7%, 2025) |

|

Leading Disease Type |

Evaporative Dry Eye Syndrome (61.3%, 2025) |

|

Leading Product |

Liquid Drops (49.5%, 2025) |

The Europe dry eye syndrome market expanded from USD 672.0 Million in 2020 to USD 827.0 Million in 2025, supported by widening diagnostic coverage, deeper community ophthalmology networks, and a clear shift toward preservative-free regimens. Anchored at USD 1017.8 Million in 2030, the trajectory to USD 1,218.1 Million by 2034 reflects sustained demand from an aging population and a digitally dependent workforce.

To get more information on this market, Request Sample

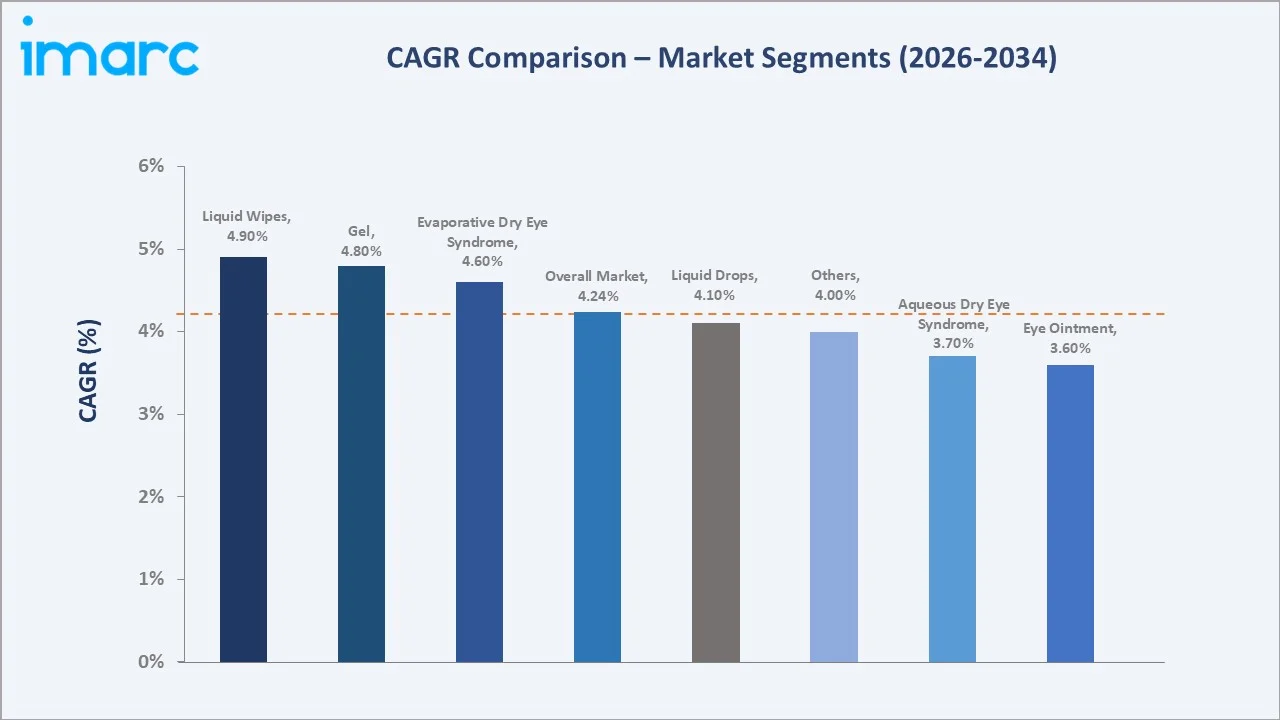

CAGR trajectories across disease type and product sub-segments show liquid wipes and gel expanding marginally faster than the overall 4.24% market CAGR, driven by routine lid hygiene adoption in meibomian gland dysfunction management and clinical preference for longer-residence gels in moderate-to-severe patients.

Executive Summary

The Europe dry eye syndrome market is on a steady expansion path from USD 672.0 Million in 2020 to USD 1,218.1 Million by 2034. Once seen as a minor discomfort, dry eye is now recognized as a chronic ocular surface disorder. Demographic aging, longer hours at digital devices, and stronger clinical consensus around tear film homeostasis are converting symptomatic sufferers into long-term users of artificial tears, gels, ointments, and prescription therapies, while innovation in semifluorinated alkanes, thermoreceptor agonists, and preservative-free combinations is reshaping the prescription tier.

Evaporative dry eye syndrome dominates disease type at 61.3% in 2025, supported by rising clinical recognition of meibomian gland dysfunction and lifestyle factors that destabilize the tear film. Liquid drops lead the product segment at 49.5%, owing to broad pharmacy availability and patient familiarity. On the basis of country, Germany commands 24.6% share, supported by strong healthcare infrastructure, high aging population, and widespread access to ophthalmic treatment. The number of people in Germany aged 65 and above is expected to increase by 41% to reach 24 Million by 2050, making up almost a third of the overall population.

Key Market Insights

|

Insight |

Data |

|

Leading Disease Type |

Evaporative Dry Eye Syndrome - 61.3% share (2025) |

|

Second Disease Type |

Aqueous Dry Eye Syndrome - 38.7% share (2025) |

|

Leading Product |

Liquid Drops - 49.5% share (2025) |

|

Second Product |

Gel - 18.6% share (2025) |

|

Leading Country |

Germany - 24.6% share (2025) |

|

Fastest Growing Country |

Spain - 11.7% share (2025) |

|

Top Companies |

Bausch + Lomb, AbbVie Inc., Alcon Inc., Santen Pharmaceutical Co., Ltd. |

Key Analytical Observations Expanding on the Data Above:

- Evaporative dry eye syndrome dominance at 61.3% reflects the growing share of meibomian gland dysfunction in the diagnosed pool. Long screen hours, air-conditioned offices, and urban air quality continue to weaken the tear lipid layer, while clinical training in meibography and lipid-layer interferometry has lifted detection rates across community optometry chains.

- Aqueous dry eye syndrome at 38.7% remains a meaningful subset, especially among older female patients and those with autoimmune comorbidities, such as Sjögren’s syndrome. Demand here skews toward prescription immunomodulators and high-viscosity tear substitutes, supporting higher per-patient value.

- Liquid drops at 49.5% reflect strong over-the-counter habits, affordable pricing, and broad shelf availability across European pharmacies. The shift from preserved bottles to single-dose preservative-free units is lifting average selling prices without disturbing the segment’s dominant share.

- Gel at 18.6% is gaining traction among patients with moderate-to-severe dry eye symptoms requiring longer ocular surface retention and overnight lubrication. Its thicker viscosity supports extended moisture persistence and improved symptom relief, particularly in chronic and post-surgical dry eye cases.

- Germany at 24.6% leads regional spending, supported by a mature health insurance mix, dense ophthalmology coverage, and a strong manufacturing base. In 2023, Germany had 96 statutory health insurance providers, covering approximately 87% of its population. The country also benefits from high diagnosis rates, advanced eye care infrastructure, and broad availability of prescription as well as over-the-counter ophthalmic treatments.

Europe Dry Eye Syndrome Market Overview

Dry eye syndrome, also termed keratoconjunctivitis sicca, is a multifactorial disease of the ocular surface marked by loss of tear film homeostasis. Patients experience irritation, redness, fluctuating vision, and visual fatigue, with chronic cases often progressing to corneal damage. Treatment combines self-care lubricants, prescription immunomodulators, anti-inflammatory agents, and lid hygiene devices.

The European ecosystem integrates suppliers of active pharmaceutical ingredients and ophthalmic-grade excipients, manufacturers of drops, gels, ointments, wipes and diagnostic devices, regulatory bodies, hospital and community ophthalmology networks, and retail and online pharmacy chains. Population aging, regional health insurance coverage, and patient-paid premium tiers together shape demand across prescription and self-care channels.

Market Dynamics

To evaluate market opportunities, Request Sample

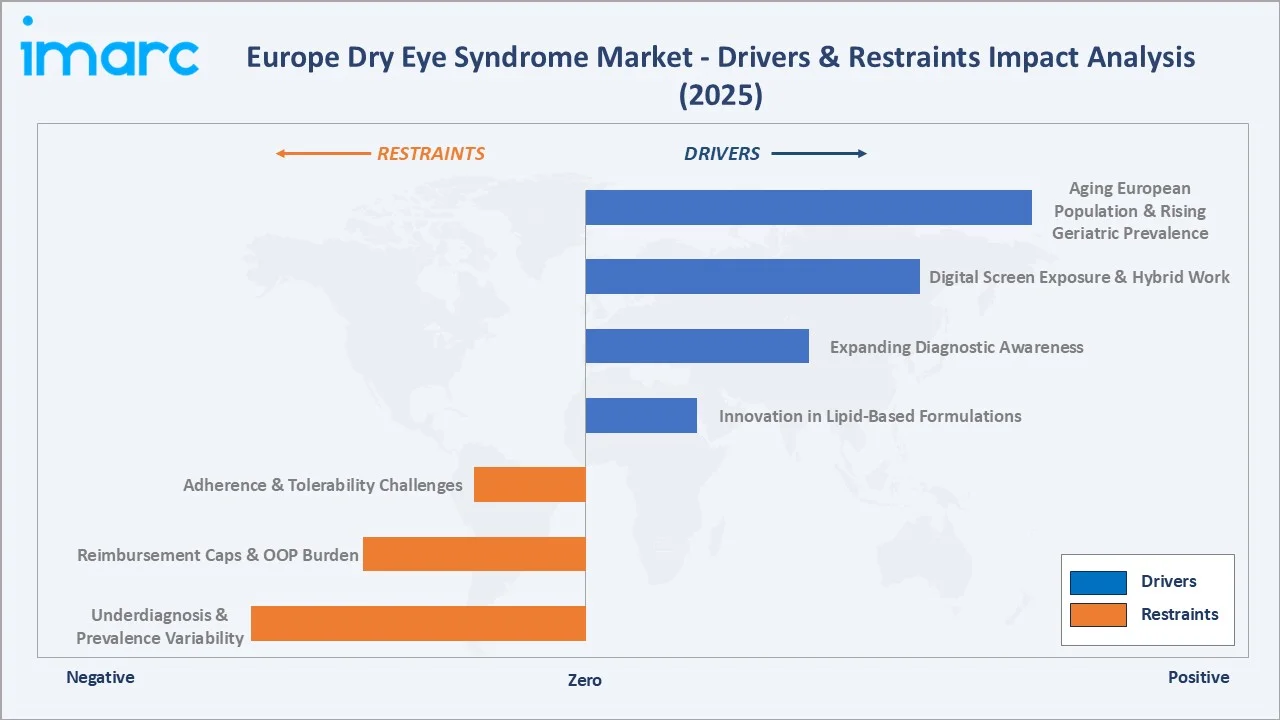

Market Drivers

- Aging European Population and Rising Geriatric Prevalence: A growing share of Europeans over 60, combined with post-menopausal hormonal change and chronic conditions, such as diabetes, is enlarging the patient base. In 2025, nearly one in five (19%, 11 Million) individuals in England were aged 65 and older, while close to two in five (38%, 22 Million) were aged 50 and older.

- Digital Screen Exposure and Hybrid Work: Extended use of laptops, tablets, and mobile phones reduces blink rate and accelerates tear evaporation. Hybrid working patterns have made digital eye strain a sustained year-round trigger and a recurring purchase driver in over-the-counter retail.

- Expanding Diagnostic Awareness and Optometry Screening: European optometry networks have widened routine dry eye screening, and patient education campaigns by ophthalmic societies have improved symptom recognition, converting previously undiagnosed sufferers into formal patients accessing branded treatments.

- Innovation in Lipid-Based and Water-Free Formulations: Preservative-free single-dose units, hyaluronic acid formulations, lipid-based gels, and water-free semifluorinated alkanes have collectively elevated the standard of care, lifting the average selling price of the category.

Market Restraints

- Underdiagnosis and Prevalence Variability Across Studies: Differences in diagnostic criteria and clinical assessment methods across European countries continue to create inconsistent estimates of dry eye prevalence. This lack of standardization complicates payer decision-making and slows reimbursement adoption for newer prescription therapies.

- Reimbursement Caps and Out-of-Pocket Burden: National health systems across France, Italy, Germany, and Spain apply tight cost-effectiveness thresholds. Many artificial tears remain self-paid, while prescription products face price referencing and parallel-import competition that limit branded margins.

- Adherence and Tolerability Challenges in Chronic Use: Dry eye treatment requires sustained adherence over months or years. Stinging on instillation and slow symptomatic relief raise drop-out rates once symptoms partially resolve, creating churn for repeat prescription brands.

Market Opportunities

- Premium Preservative-Free Portfolios: Multidose preservative-free bottles and single-dose vials are gaining traction as concerns around benzalkonium chloride toxicity grow, creating room for premium pricing and trade-up from preserved generics into specialty preservative-free ranges.

- Novel Mechanism Prescription Therapies: Semifluorinated alkanes, thermoreceptor agonists, and nasal neurostimulation sprays open new lines of treatment for patients failing conventional drops, building a premium prescription tier and creating space for high-value European launches.

Market Challenges

- Regulatory Fragmentation Across European Markets: National authority requirements for preservative-free packaging, pediatric data, and post-marketing surveillance lengthen approval timelines and elevate compliance costs. Country-level pricing negotiations further extend time-to-revenue for prescription dry eye products.

- Generic and Private-Label Pressure on Branded Therapies: Loss of exclusivity on legacy immunomodulators and the proliferation of pharmacy own-label artificial tears continue to compress branded margins. Manufacturers must differentiate through formulation innovation, preservative-free delivery, and patient-support services.

Emerging Market Trends

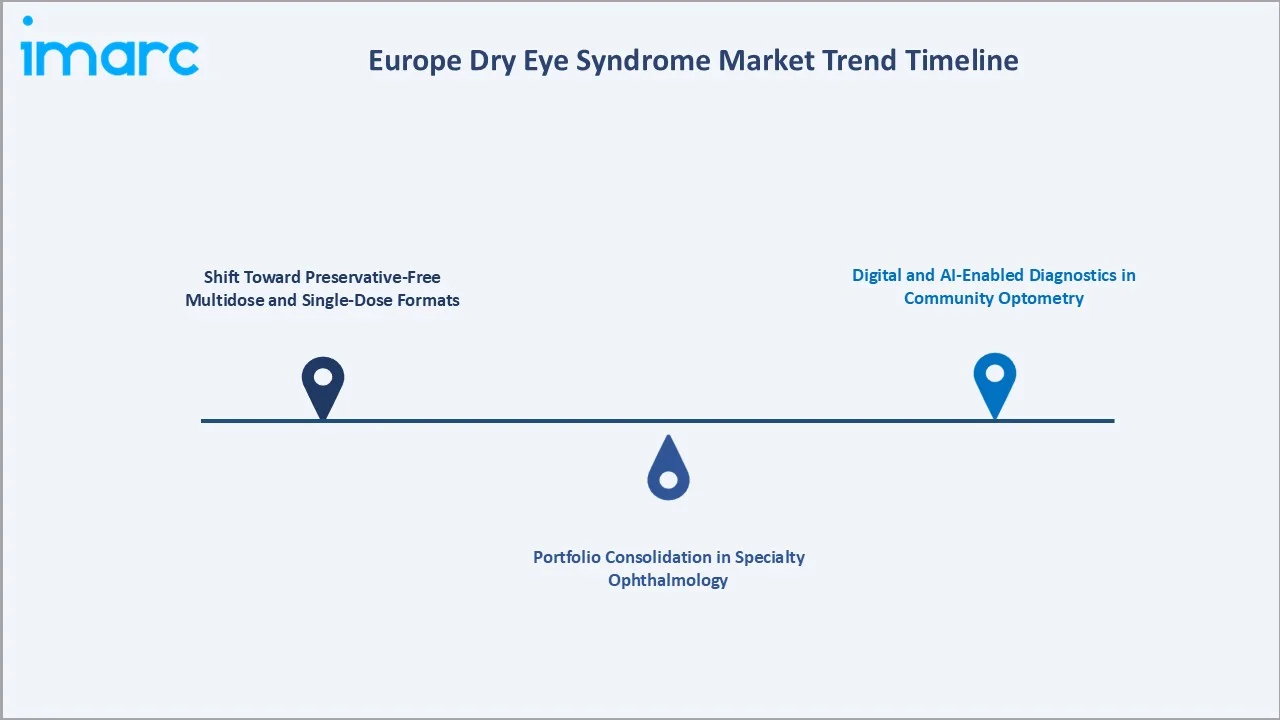

1. Shift Toward Preservative-Free Multidose and Single-Dose Formats

European ophthalmologists are steering patients away from preserved multidose bottles toward preservative-free single-dose vials and airless pumps. Concerns around benzalkonium chloride causing additional ocular surface inflammation have made preservative-free formats the new clinical default for moderate-to-severe patients, and national prescribing guidance in France and Germany now favors these options for chronic users.

2. Portfolio Consolidation in Specialty Ophthalmology

Large ophthalmic and pharmaceutical companies are increasingly consolidating dry eye treatment portfolios through acquisitions, licensing agreements, and strategic partnerships. Firms are focusing on combining prescription therapies, over-the-counter lubricants, diagnostic technologies, and lid-care products within integrated eye-care platforms. This consolidation is strengthening distribution networks across Europe.

3. Digital and AI-Enabled Diagnostics in Community Optometry

Tear meniscus imaging, infrared meibography, and AI-powered ocular surface analysis are migrating from research hospitals to high-street optometry clinics in the United Kingdom, Germany, and the Nordics. Integrated workstations allow optometrists to grade dry eye severity in minutes and triage patients to over-the-counter products or specialist referral.

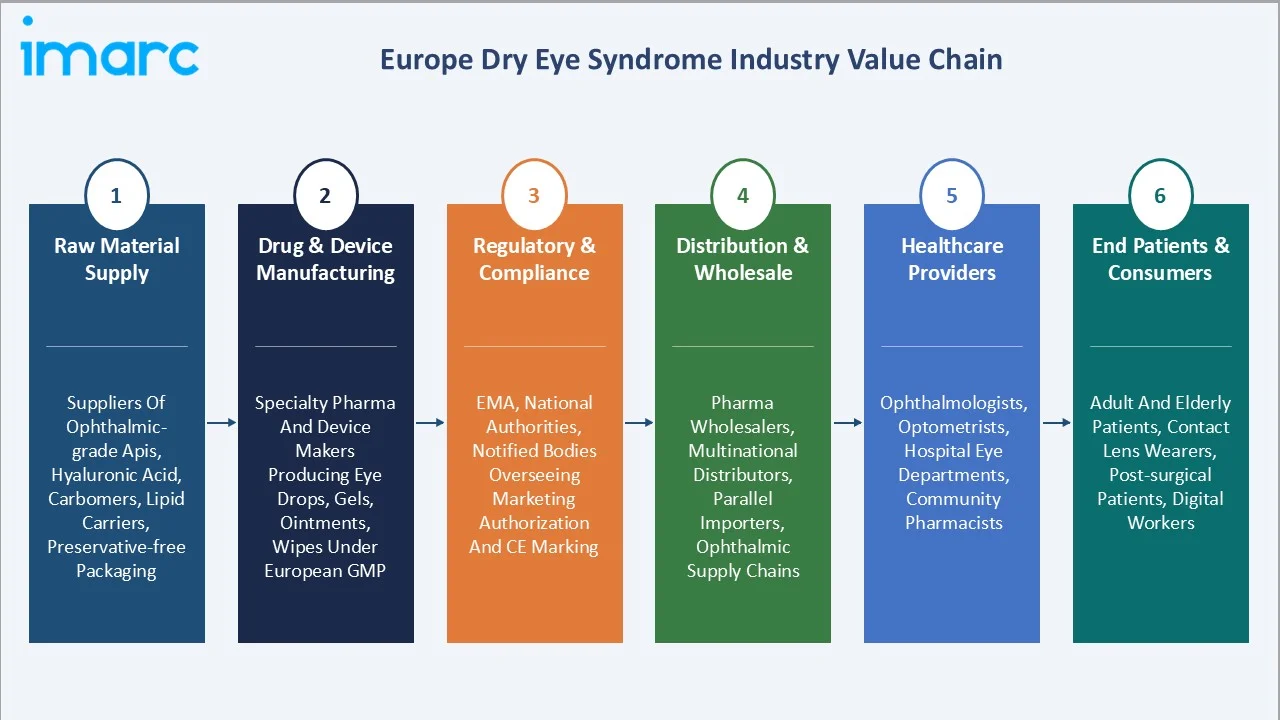

Industry Value Chain Analysis

The Europe dry eye syndrome value chain spans six interconnected stages, from raw material supply through end-patient consumption. Drug formulation and device manufacturing capture the highest value-add, while distribution and healthcare provider relationships create durable competitive advantages.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of ophthalmic-grade APIs, hyaluronic acid, carbomers, lipid carriers, and preservative-free packaging components |

|

Drug & Device Manufacturing |

Specialty pharmaceutical manufacturers and medical device makers producing eye drops, gels, ointments, wipes, and diagnostic instruments under European GMP standards |

|

Regulatory & Compliance |

EMA, national competent authorities, and notified bodies overseeing marketing authorization, pharmacovigilance, and CE marking of devices and combination products |

|

Distribution & Wholesale |

Pharmaceutical wholesalers, multinational distributors, parallel importers, and dedicated ophthalmic supply chains servicing hospitals and pharmacies |

|

Healthcare Providers |

Ophthalmologists, optometrists, hospital eye departments, ambulatory clinics, and community pharmacists handling diagnosis, prescription, and counselling |

|

End Patients & Consumers |

Adult and elderly patients with chronic dry eye, contact lens wearers, post-refractive-surgery patients, and digital workers using self-care and prescribed therapies |

Vertically integrated specialty eye-care companies capture larger margins through in-house formulation development, dedicated sterile-fill manufacturing, and direct engagement with ophthalmologist and optometrist channels.

Technology Landscape in the Europe Dry Eye Syndrome Industry

Lipid-Based and Water-Free Formulation Science

Lipid-based emulsions, cationic nanoemulsions, and semifluorinated alkanes are extending the duration of action of artificial tears, helping patients reduce instillation frequency. Cyclosporine and lifitegrast remain anchors of the immunomodulator tier, while perfluorohexyloctane introduces a non-aqueous mechanism that addresses meibomian gland dysfunction at its root.

Preservative-Free Delivery Systems

Single-dose units, ABAK and COMOD multidose airless pumps, and micro-dosing devices have reduced the need for preservatives without compromising sterility, allowing brands to scale chronic-use prescriptions while maintaining ocular surface health.

Diagnostic Imaging and AI-Enabled Analytics

High-resolution meibography, interferometry-based lipid layer assessment, and AI-assisted tear film analytics are converting subjective dry eye evaluation into quantitative practice. Several European optometry chains operate dry eye clinics built around these technologies, allowing earlier triage into appropriate treatment tiers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Disease Type |

Evaporative Dry Eye Syndrome |

61.3% |

2025 |

|

Drug Type |

🔒 |

🔒 |

2025 |

|

Product |

Liquid Drops |

49.5% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Country |

Germany |

24.6% |

2025 |

By Disease Type

Evaporative dry eye syndrome commands a 61.3% majority share in 2025, driven by the rising prevalence of meibomian gland dysfunction, increased digital screen exposure, and lifestyle factors that destabilize the tear lipid layer. Demand skews toward lipid-restoring drops, gels, and warm-compress devices targeting the underlying glandular component.

To access detailed market analysis, Request Sample

Aqueous dry eye syndrome at 38.7% in 2025 reflects patients with reduced lacrimal gland secretion, including those with Sjögren’s syndrome, post-LASIK patients, and elderly users on tear-suppressing systemic medications. Treatment moves to prescription immunomodulators, such as cyclosporine and lifitegrast, supporting higher per-patient value.

By Product

Liquid drops dominate the product mix at 49.5% in 2025, supported by their position as the default self-care option across European pharmacies. Strong consumer familiarity, broad price-point coverage, and availability of single-dose preservative-free units keep this category foundational.

Gel accounts for 18.6% in 2025, favored for moderate-to-severe dry eye where longer ocular surface retention improves relief. It also supports overnight lubrication and extended symptom control in patients with chronic ocular surface irritation.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

24.6% |

Large geriatric population, statutory health insurance coverage, mature ophthalmology network, and domestic manufacturing of preservative-free products |

|

France |

18.8% |

High eye-care spending, extensive optometry infrastructure, supportive regulatory framework, and rising adoption of preservative-free prescriptions |

|

United Kingdom |

17.9% |

Expanding private ophthalmology, high digital device penetration, growing dry eye awareness, and active over-the-counter retail eye care segment |

|

Italy |

13.6% |

Aging population, developed pharmacy retail, increasing diagnosis rates, and growing demand for premium artificial tears and combination therapies |

|

Spain |

11.7% |

Rising disposable income, expanding ophthalmology referrals, growing digital eye strain prevalence, and uptake of preservative-free single-dose formats |

|

Others |

13.4% |

Increasing healthcare access, growing branded product penetration, awareness campaigns, and pharmacy chain expansion across Central and Northern Europe |

Germany at 24.6% in 2025 leads the market, supported by a dense ophthalmology network, broad health insurance coverage, and a strong domestic manufacturing base. It also benefits from high patient awareness, early diagnosis rates, and strong availability of prescription as well as over-the-counter dry eye therapies.

France at 18.8% in 2025 remains a major contributor to the Europe dry eye syndrome market, supported by high eye-care expenditure, extensive optometry infrastructure, and favorable regulatory support for ophthalmic products.

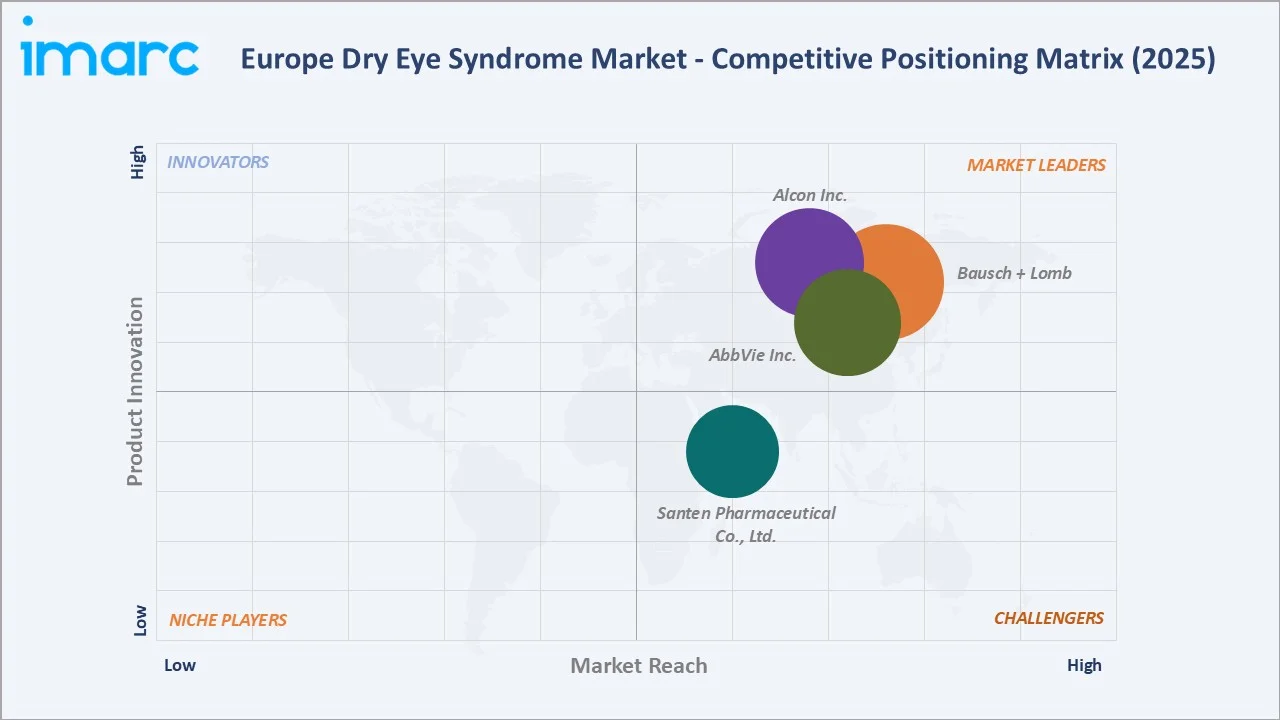

Competitive Landscape

The Europe dry eye syndrome market is moderately consolidated, with multinational eye-care leaders controlling a majority of branded prescription value while regional specialists and generic players compete intensively in the over-the-counter tier. Product breadth, preservative-free capability, ophthalmologist relationships, and pharmacy-channel reach are the decisive competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Bausch + Lomb |

Artelac Complete |

Leader |

Broad eye-care portfolio across prescription and over-the-counter; ophthalmologist engagement |

|

AbbVie Inc. |

Refresh |

Leader |

Leading OTC artificial tear franchise in Europe; broad pharmacy and retail distribution |

|

Alcon Inc. |

Systane Complete, Systane Ultra |

Leader |

Vision-care heritage combined with prescription pharmaceutical expansion; broad retail and surgical reach |

|

Santen Pharmaceutical Co., Ltd. |

Cationorm, Ikervis |

Challenger |

Specialty ophthalmology focus; preservative-free cationic emulsion expertise; targeted European launches |

Key players include Bausch + Lomb, AbbVie Inc., Alcon Inc., and Santen Pharmaceutical Co., Ltd., among others.

Key Company Profiles

Bausch + Lomb

Bausch + Lomb is a leading global eye health company headquartered in Vaughan, Ontario. Its European dry eye portfolio is anchored by the Artelac range of preservative-free artificial tears, which is exclusive to European markets.

- Product Portfolio: Artelac Complete and the broader Artelac range of preservative-free eye drops.

- Recent Developments: In December 2025, the Relief of Eye Surface by Triple Action (RESTA) study was published confirming Artelac Complete's non-inferiority in improving ocular surface staining at Day 28, with significantly improved patient quality of life at Day 90.

- Strategic Focus: Artelac range leadership in European preservative-free OTC dry eye; deepening ophthalmologist and optometrist relationships; investing in clinical evidence generation through European congresses.

AbbVie Inc.

AbbVie Inc., headquartered in North Chicago, Illinois, became a major force in ophthalmology through its 2020 acquisition of Allergan. Its European eye care operation is anchored by a long-established immunomodulator franchise and a broad lubricant drops portfolio.

- Product Portfolio: Refresh range of artificial tears and gels; preservative-free formulations.

- Recent Developments: AbbVie continues to invest in lifecycle management for its dry eye brands, with European launches of preservative-free Refresh variants and real-world evidence programs presented at major ophthalmology meetings.

- Strategic Focus: Leading OTC artificial tear franchise in Europe; broad pharmacy and retail distribution.

Santen Pharmaceutical Co., Ltd.

Santen Pharmaceutical Co., Ltd., headquartered in Osaka, Japan, is a specialty ophthalmology company with a strong European presence. The company focuses on prescription eye-care therapies and continues to expand its dry eye treatment portfolio through targeted product launches and regional distribution partnerships.

- Product Portfolio: Ikervis, Cationorm (cationic emulsion eye drops), and a complementary surgical and vision-correction range.

- Recent Developments: Santen continues to invest in cationic emulsion and preservative-free formulation science and is expanding sustainable packaging through plant-derived bottles in selected European markets.

- Strategic Focus: Specialty ophthalmology focus; preservative-free cationic emulsion expertise; long-term investment in European registration, manufacturing, and clinical evidence.

Market Concentration Analysis

The Europe dry eye syndrome market is moderately concentrated. The top four companies, namely Bausch + Lomb, AbbVie Inc., Alcon Inc., and Santen Pharmaceutical Co., Ltd., collectively hold an estimated 50% to 60% of branded revenue across prescription and major over-the-counter categories in 2025.

Barriers to entry include EMA approval requirements for prescription products, the complexity of preservative-free packaging, multi-year ophthalmologist channel building, and the capital expenditure for dedicated sterile-fill manufacturing.

Consolidation continues through portfolio acquisitions, in-licensing of specialty molecules, and bundling of devices, drops, and lid hygiene products into unified dry eye programs. Regional players retain strong positions through pharmacy relationships and tailored preservative-free portfolios.

Investment & Growth Opportunities

Fastest-Growing Segments

Liquid wipes at 10.3% and gel at 18.6% expand marginally faster than the overall 4.24% market CAGR through 2034, driven by routine lid hygiene adoption in meibomian gland dysfunction management and rising clinical preference for longer-residence gels in moderate-to-severe patients.

Emerging Markets

Spain at 11.7% is the fastest-growing country, supported by rising disposable income, expanding private ophthalmology, and accelerating preservative-free uptake. The United Kingdom also delivers above-average growth and offers attractive opportunities for preservative-free portfolios.

Venture & Investment Trends

Investment is concentrated in semifluorinated alkane platforms, TRPM8 agonists, nasal neurostimulation sprays, AI-enabled diagnostic devices, and connected adherence tools. Private equity interest in eye-care platforms has also increased as the category benefits from chronic-use demand and stable cash flows.

Future Market Outlook (2026-2034)

The Europe dry eye syndrome market is forecast to expand from USD 827.0 Million in 2025 to USD 1,218.1 Million by 2034 at a CAGR of 4.24%, adding roughly USD 391 Million in incremental value. Demographic aging, persistent digital exposure, and rising standards of care will keep the trajectory firmly positive.

Four forces will shape the market through 2034: deeper preservative-free penetration; commercialization of novel mechanism therapies; AI-enabled diagnostics in community optometry; and continued portfolio consolidation among multinational eye-care leaders.

By 2034, preservative-free products are expected to capture a significantly larger share of European dry eye spending, prescription premium tiers will sit alongside established artificial tears, and community optometry-led dry eye clinics will be the primary touchpoint for new diagnosis and ongoing management.

Research Methodology

Primary Research

Primary research included structured interviews with ophthalmologists, optometrists, pharmacy chain managers, and senior commercial executives at leading European eye-care companies, validating market sizing, segmentation splits, channel dynamics, and competitive intensity.

Secondary Research

Secondary sources included peer-reviewed journals such as Investigative Ophthalmology & Visual Science and The Ocular Surface, EMA publications, regulatory databases, European Dry Eye Society and EuDEC congress materials, national statistics, annual reports, and press releases.

Forecasting Models

Market forecasts combined top-down and bottom-up models, weighting demographic projections, prevalence assumptions, prescription-to-OTC mix evolution, and price tier dynamics. Scenario analysis addressed reimbursement variation, preservative-free penetration speed, and new product launch timing.

Europe Dry Eye Syndrome Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Disease Types Covered | Evaporative Dry Eye Syndrome, Aqueous Dry Eye Syndrome |

| Drug Types Covered | Anti-inflammatory Drugs, Lubricant Eye Drops, Autologous Serum Eye Drops |

| Products Covered | Liquid Drops, Gel, Liquid Wipes, Eye Ointment, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Bausch + Lomb, AbbVie Inc., Alcon Inc., Santen Pharmaceutical Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe dry eye syndrome market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe dry eye syndrome market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe dry eye syndrome industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Dry Eye Syndrome Market Report

The Europe dry eye syndrome market was valued at USD 827.0 Million in 2025, supported by aging demographics, rising digital exposure, and stronger ophthalmology infrastructure.

The market is projected to grow at a CAGR of 4.24% from 2026 to 2034, reaching USD 1,218.1 Million, supported by preservative-free adoption, novel prescription therapies, and rising diagnostic awareness.

Evaporative dry eye syndrome leads at 61.3% in 2025, driven by rising meibomian gland dysfunction prevalence, digital screen use, and broader clinical recognition. Aqueous dry eye at 38.7% remains a meaningful prescription-led subset.

Liquid drops lead at 49.5% in 2025, owing to broad pharmacy availability, affordable pricing, and strong consumer familiarity. Gel at 18.6% is the second-largest format.

Germany commands 24.6% in 2025, led by mature ophthalmology coverage, strong insurance access, and a robust manufacturing base.

Leading players include Bausch + Lomb, AbbVie Inc., Alcon Inc., and Santen Pharmaceutical Co., Ltd., among others.

Preservative-free adoption is driven by clinical concerns over benzalkonium chloride toxicity in chronic users, supportive national prescribing guidance, and rising patient preference for single-dose and airless multidose formats.

Perfluorohexyloctane drops, TRPM8 agonists, and nasal neurostimulation sprays are introducing new mechanisms beyond traditional artificial tears and immunomodulators, building a premium prescription tier expected to scale over 2026-2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade