Europe E-Bike Market Size, Share, Trends and Forecast by Mode, Motor Type, Battery Type, Class, Design, Application, and Country, 2026-2034

Europe E-Bike Market Size, Share, Trends & Forecast (2026-2034)

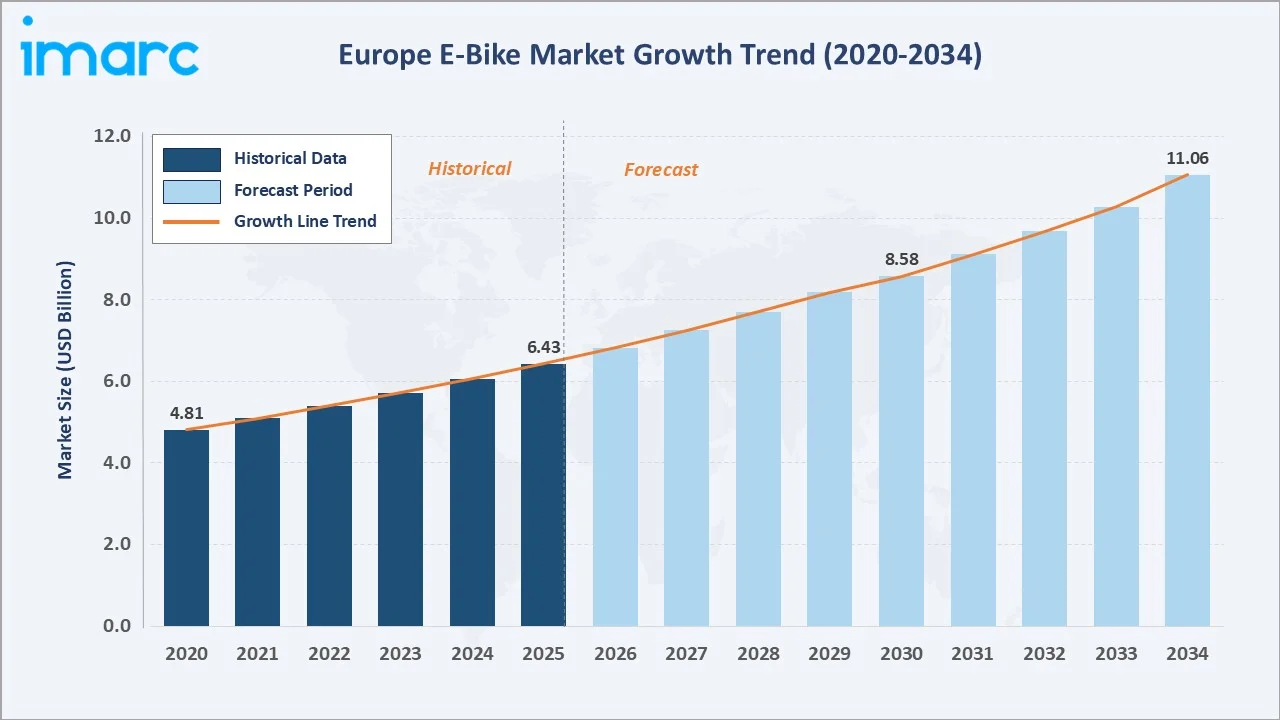

Europe e-bike market reached USD 6.43 Billion in 2025 and is projected to reach USD 11.06 Billion by 2034, growing at a CAGR of 6.0% during 2026-2034. Rising demand for sustainable urban mobility, escalating fuel prices, government subsidies promoting eco-friendly transport, and rapid advances in lithium-ion battery and mid-drive motor technology are the primary growth catalysts driving the European e-bike market forward.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.43 Billion |

|

Forecast Market Size (2034) |

USD 11.06 Billion |

|

CAGR (2026-2034) |

6.0% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Country |

Germany (32.8% share, 2025) |

|

Fastest Growing Segment |

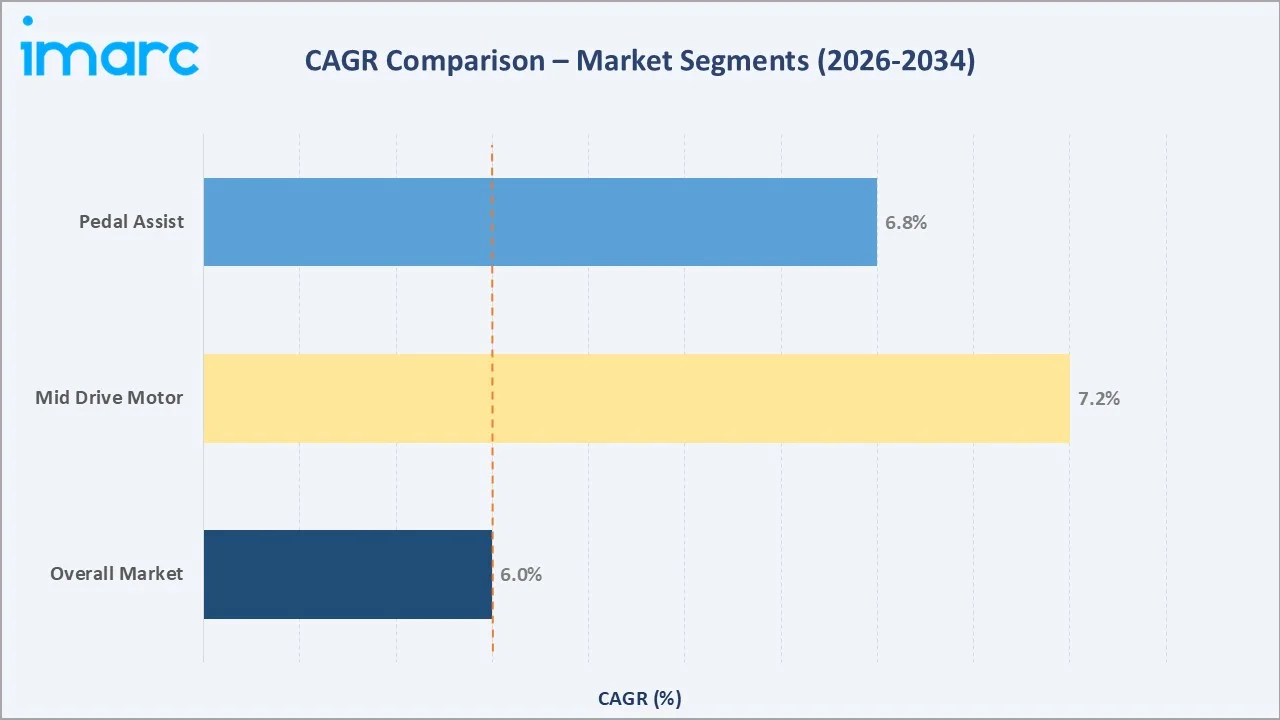

Mid Drive Motor (CAGR 7.2%, 2026-2034) |

To get more information on this market, Request Sample

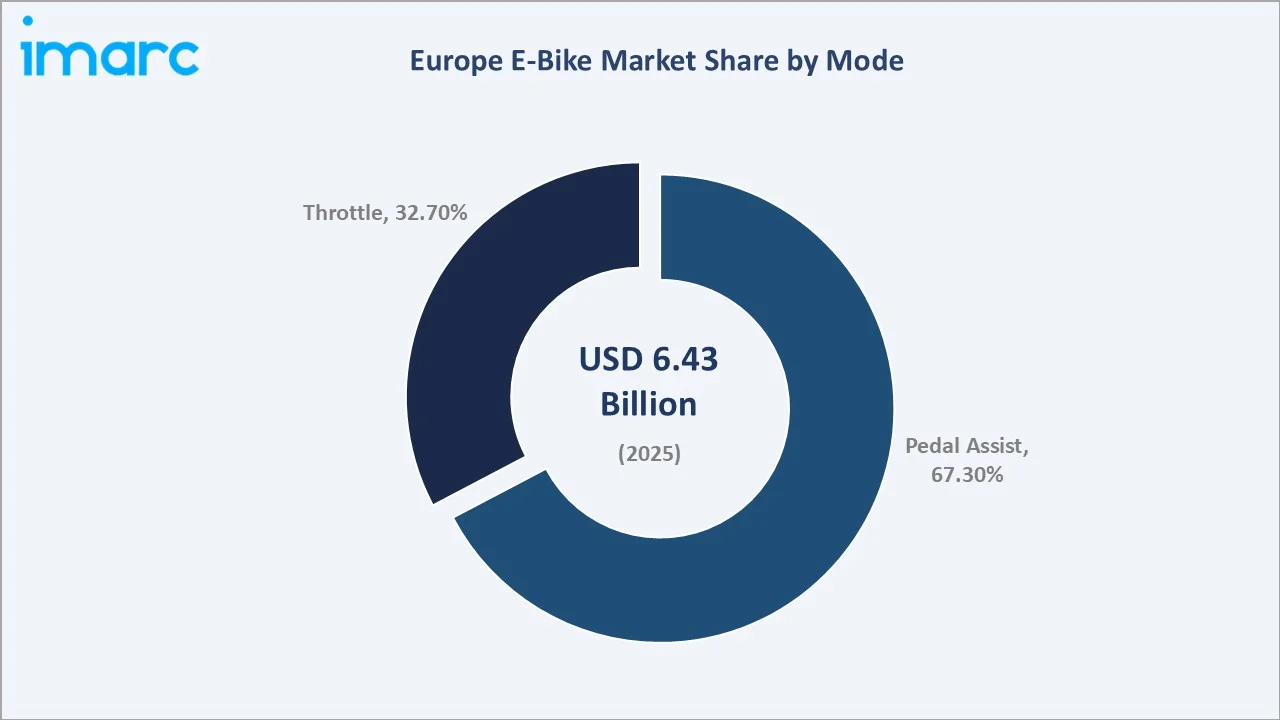

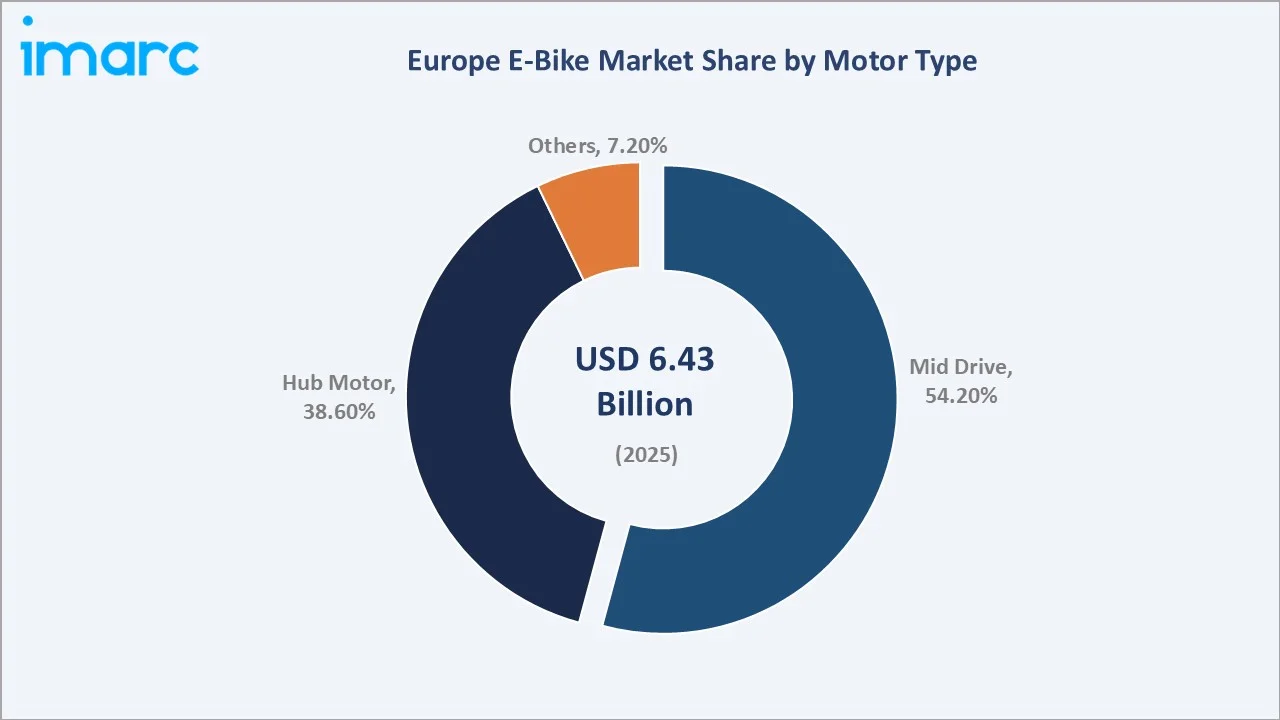

Pedal assist dominates the mode segment with a 67.3% share in 2025, supported by regulatory alignment with the EU's EN 15194 standard defining pedelecs as bicycles. Mid-drive motors lead the motor type segment at 54.2%, preferred for their superior torque distribution and energy efficiency in hilly European terrain.

With consistent year-on-year demand reinforced by expanding cycling infrastructure, growing environmental awareness, and increasing availability of performance-oriented e-bike models at accessible price points, the European e-bike market is positioned for robust, sustained growth over the forecast horizon.

Executive Summary

The European e-bike market is experiencing robust, structurally driven growth, underpinned by urban mobility transformation, decarbonization policy imperatives, and a profound consumer shift toward sustainable personal transportation. The market reached USD 6.43 Billion in 2025 and is forecast to reach USD 11.06 Billion by 2034 at a CAGR of 6.0%, representing cumulative incremental revenue of approximately USD 4.63 Billion over the forecast decade.

Pedal assist e-bikes account for 67.3% of market value in 2025, reinforced by their classification as conventional bicycles under EU legislation, enabling use on bike lanes and eliminating registration requirements. Mid-drive motors dominate the motor type segment at 54.2%, owing to their superior torque, power efficiency, and compatibility with multi-speed drivetrains preferred across European cycling terrain.

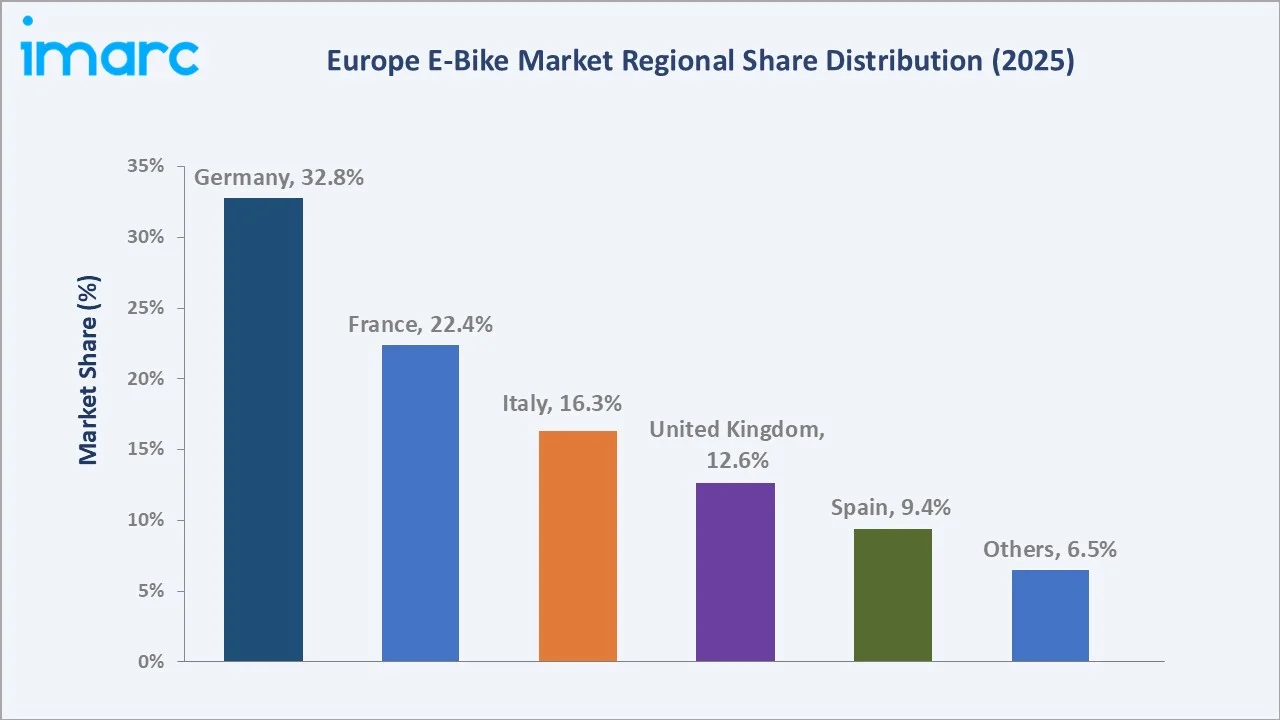

Germany leads the European market with a 32.8% share. A new EV incentive program, with a budget of EUR 3 billion by 2029, effective from January 1, 2026, in Germany. France (22.4%) and Italy (16.3%) follow, both leveraging national incentive schemes that have stimulated strong replacement demand for conventional bicycles.

Key Market Insights

|

Insight |

Data |

|

Dominant Segment (Mode) |

Pedal Assist – 67.3% share (2025) |

|

Fastest Growing Segment (Mode) |

Pedal Assist – CAGR 6.8% (2026-2034) |

|

Dominant Segment (Motor Type) |

Mid Drive – 54.2% share (2025) |

|

Fastest Growing Segment (Motor) |

Mid Drive – CAGR 7.2% (2026-2034) |

|

Leading Country |

Germany – 32.8% share (2025) |

|

Market Growth Rate |

6.0% CAGR (2026-2034) |

|

Top Companies |

Accell Group, Robert Bosch GmbH, Giant Bicycles, Riese & Müller GmbH, and Yamaha Motor Co. Ltd. |

|

Market Opportunity |

E-cargo and urban commuter segment projected at USD 3.2 Billion by 2034 |

Key Analytical Observations Supporting The Above Data:

- Pedal assist accounts for 67.3% of European e-bike revenue in 2025: benefiting from EU regulatory equivalence with conventional bicycles (EN 15194), enabling access to full cycling infrastructure without registration or insurance requirements.

- Mid-drive motors lead the motor type segment at 54.2%: preferred for superior torque distribution, natural pedaling feel, and compatibility with derailleur and internal gear hub drivetrains across mountain, trekking, and urban e-bike categories.

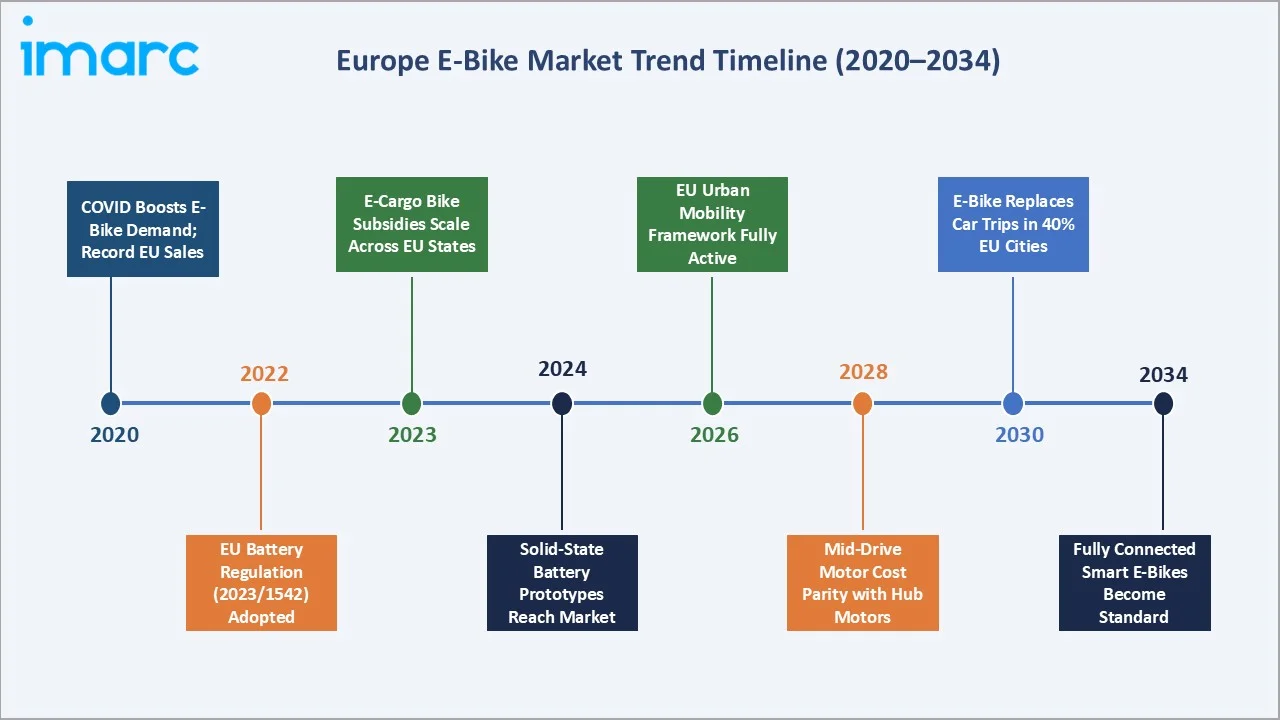

- Germany holds 32.8% of the European market share in 2025: E-bike sales remained strong, with approximately 2 million e-bikes sold. According to data compiled and shared by ZIV, there are now over 17 million e-bikes on the roads in Germany.

- The e-cargo bike sub-segment is the fastest-growing application: growing at approximately 15% CAGR in 2025, driven by last-mile logistics operators including DHL, UPS, and Amazon deploying electric cargo bikes as low-emission urban delivery alternatives.

- Battery technology is reshaping price-performance dynamics: Battery pack prices in Europe declined by 8% in real terms in 2025 compared to 2024 due to higher local production costs and a greater reliance on imported batteries, which generally carry a premium, bringing premium e-bike models within reach of mainstream consumers.

Europe E-Bike Market Overview

The European e-bike market encompasses a diverse product ecosystem spanning pedal-assist pedelecs (EN 15194 compliant), speed pedelecs (S-Pedelecs, up to 45 km/h), throttle-operated e-bikes, e-mountain bikes (e-MTBs), e-cargo bikes, urban commuter e-bikes, and folding e-bikes across city, trekking, mountain, and cargo application categories.

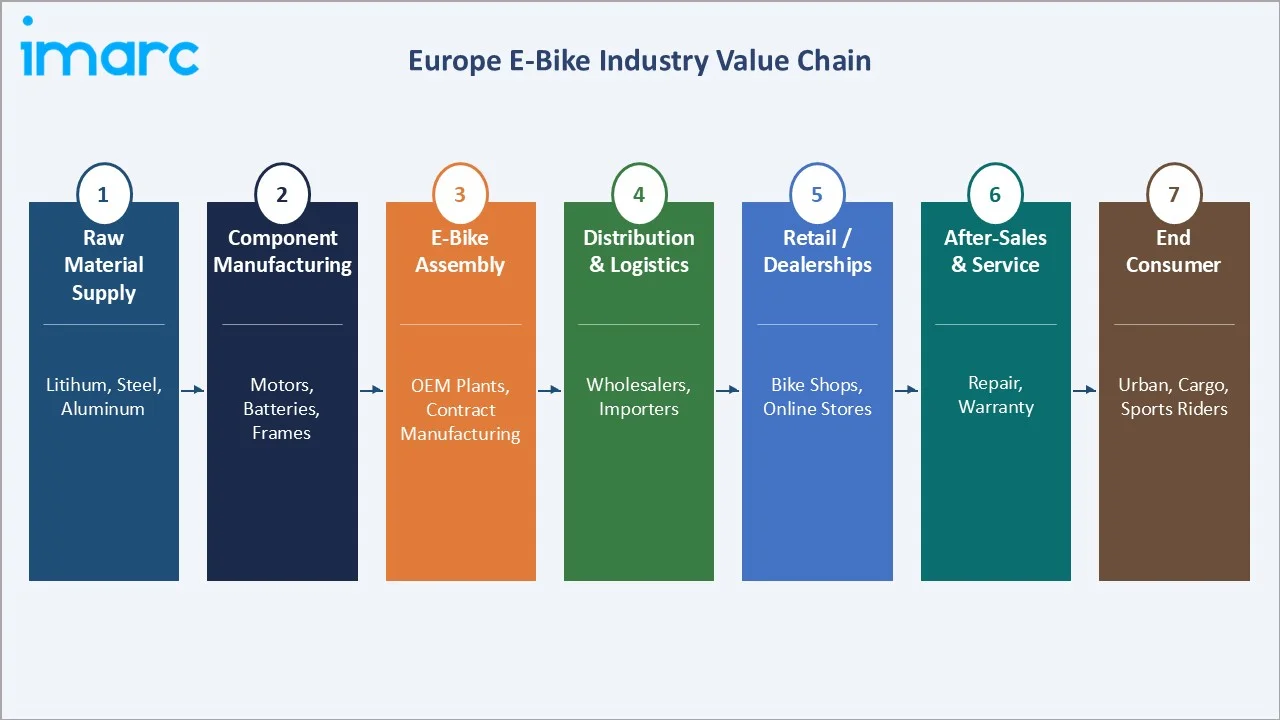

The market's value chain spans raw material sourcing (lithium, cobalt, aluminum), battery cell manufacturing, motor and drivetrain component production, e-bike assembly (both OEM and ODM), brand development, multi-channel distribution, retail dealerships, and after-sales service networks. European brands predominantly source motors and batteries from leading technology suppliers while assembling final products in European or Taiwanese facilities.

Macroeconomic drivers, including urbanization, rising fuel costs, tightening CO₂ emission regulations, and post-pandemic cycling infrastructure investment, are key structural growth catalysts. The EU's European Green Deal and Fit for 55 package have catalyzed over EUR 2.5 billion in cycling infrastructure investment across member states since 2021, fundamentally improving the commuter e-bike value proposition in major urban centers.

Market Dynamics

To evaluate market opportunities, Request Sample

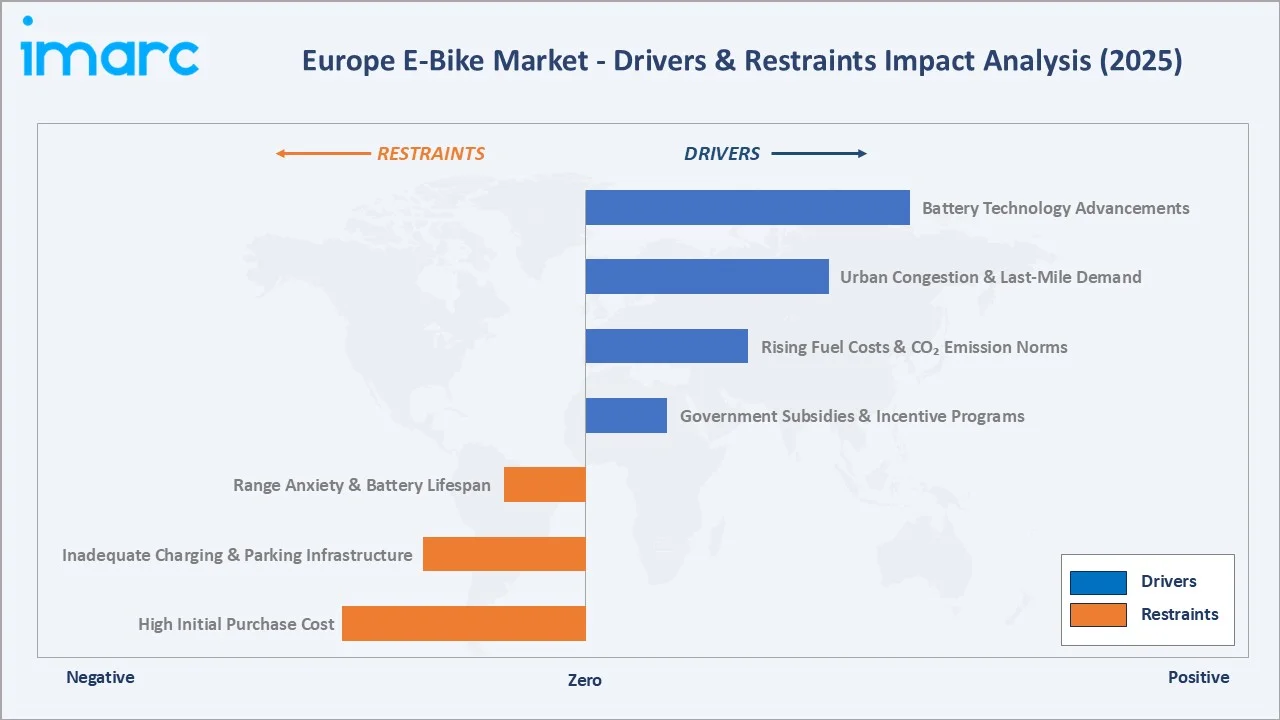

Market Drivers

- Government Subsidies & Incentive Programs: France’s “Coup de Pouce Vélo” scheme, which offers direct purchase grants to reduce the cost of new e‑bikes. Spain’s national electric bike purchase subsidies, where the government has allocated EUR 20 million for rebates on e‑bike purchases for individuals and companies under its broader sustainable transport initiative.

- Rising Fuel Costs & CO₂ Emission Norms: European gasoline and diesel prices averaged EUR 1.70–1.90 per litre in 2024–2025, strengthening the total cost of ownership case for e-bike commuting vs. personal vehicle use.

- Urban Congestion & Last-Mile Demand: European cities are increasingly designating low-emission zones (LEZs) and car-free areas, directly benefiting e-bike adoption. E-bikes average 20–40 minutes faster than cars for urban commutes under 15 km in congested European city centers, offering a compelling commuter value proposition.

- Battery Technology Advancements: Lithium-ion battery energy density improvements have extended average e-bike range from 60–80 km in 2020 to 100–150 km in 2025 per charge at equivalent battery weight. Emerging solid-state battery technology is projected to extend ranges to 200+ km by 2028, further reducing range anxiety.

Market Restraints

- High Initial Purchase Cost: Quality mid-range pedal-assist e-bikes retail at EUR 1,800–4,000 in Europe, presenting a significant upfront cost barrier relative to conventional bicycles (EUR 300–800). Premium e-MTBs and cargo e-bikes exceed EUR 5,000–12,000, limiting mass-market penetration in price-sensitive segments.

- Inadequate Charging & Parking Infrastructure: Public e-bike charging infrastructure remains underdeveloped in Eastern and Southern Europe. The lack of secure, covered e-bike parking in apartment blocks, where 60%+ of urban Europeans reside, creates battery charging accessibility barriers for would-be e-bike adopters.

- Range Anxiety & Battery Lifespan Concerns: Consumer concerns about battery degradation over time, replacement cost (EUR 300-800+), and range adequacy in adverse weather conditions remain purchase hesitation factors, particularly among older demographic segments less familiar with battery technology management.

Market Opportunities

- E-Cargo Bike Urban Logistics Expansion: The rapid growth of urban last-mile logistics, driven by e-commerce, is generating surging institutional demand for e-cargo bikes. The European e-cargo bike segment is estimated to grow at 15% CAGR through 2034, with fleet deployments by DHL, Amazon Logistics, and municipal services representing a structurally recurring demand source.

- Emerging Eastern European Markets: Poland, the Czech Republic, Hungary, and Romania represent high-growth emerging markets for e-bike adoption, as rising disposable incomes, improving urban cycling infrastructure, and expanding EU subsidy programs drive initial market penetration from a low base.

- Connected E-Bike Platform Development: IoT-enabled e-bikes with GPS tracking, over-the-air software updates, theft prevention, ride analytics, and integration with urban mobility-as-a-service platforms represent a significant value-added technology opportunity, commanding a 20–35% price premium in connected-feature equipped models.

Market Challenges

- Battery Supply Chain and Critical Mineral Dependency: European e-bike manufacturers face strategic exposure to lithium and cobalt supply chain concentration, with over 60% of global lithium processing controlled by China. EU Battery Regulation 2023/1542 imposes increasing due diligence, recycled content, and carbon footprint requirements that add compliance complexity.

- Regulatory Fragmentation Across Member States: While EU EN 15194 defines pedelec standards, divergent national interpretations of speed pedelec (S-Pedelec) classification, helmet mandates, and shared infrastructure access rules across member states create market complexity for pan-European brands and distribution networks.

- Counterfeit and Low-Quality Import Competition: Rising volumes of non-compliant e-bikes from Chinese manufacturers, failing EU EMC, battery safety, and CE marking requirements, entering via grey market channels, are depressing price benchmarks and eroding brand differentiation for compliant European manufacturers.

Emerging Market Trends

1. E-Cargo Bike Adoption for Urban Last-Mile Logistics

In Amsterdam, Copenhagen, and Paris, e-cargo bikes now account for 15–25% of last-mile commercial deliveries. Major logistics operators have placed fleet orders exceeding 100,000 units collectively since 2022, and European municipalities are actively restricting diesel delivery vehicles in city centres, creating a structural demand pull for e-cargo bike deployment.

2. Subscription and Lease Models: Democratizing Access

Subscription and employer lease models are significantly expanding e-bike market access beyond affluent early adopters. Germany's JobRad, the Netherlands' fietsplan, and France's Forfait Mobilité Durables collectively facilitate over 2 million e-bike lease agreements annually, spreading upfront cost across monthly payments and enabling higher-specification model adoption than outright purchase would allow.

3. Integration with Urban Mobility-as-a-Service (MaaS) Platforms

E-bikes are increasingly integrated into multimodal Mobility-as-a-Service platforms such as Whim (Helsinki), Jelbi (Berlin), and Navya (Paris), allowing seamless journey planning combining e-bike sharing, public transit, and car sharing. Connected e-bike APIs enabling real-time availability, booking, and payment integration represent a growing B2B platform opportunity estimated at EUR 450 million by 2030.

4. Solid-State Battery Technology Approaching Commercial Viability

Solid-state battery prototypes from manufacturers including QuantumScape, Solid Power, and Toyota have demonstrated energy densities of 400–500 Wh/kg in laboratory settings, compared to 200–250 Wh/kg for current lithium-ion cells.

Industry Value Chain Analysis

The European e-bike value chain encompasses raw material extraction, battery cell and motor manufacturing, bicycle frame and component production, final assembly, brand and channel development, and post-sale service, with value accruing disproportionately at the motor/battery technology and brand/distribution stages.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Albemarle Corp. (lithium), AMAG Austria (aluminium) |

|

Battery Cell Manufacturing |

CATL, Samsung SDI, LG Energy Solution, Panasonic |

|

Motor & Drivetrain Components |

Bosch eBike Systems, Shimano STEPS, Yamaha Motor, TQ Systems |

|

E-Bike Frame & Assembly |

Giant Manufacturing, Merida Industry, Accell Group, Riese & Müller |

|

Distribution & Logistics |

Accell Distribution, Canyon Direct, Pon Holdings |

|

Retail / Dealer Network |

Specialized Dealers, Decathlon, Online Channels (Canyon, Trek) |

|

End Consumers / Fleet Operators |

Urban commuters, e-cargo logistics operators, sports/leisure riders, rental fleets |

Technology Landscape in the European E-Bike Industry

Mid-Drive Motor Technology Evolution

Mid-drive motor systems have undergone substantial performance and efficiency improvements, with leading systems from Bosch (Performance Line CX), Shimano (EP8), and Brose (Drive S Mag) achieving peak torque outputs of 85–90 Nm at weights below 2.5 kg.

Battery Management Systems & Fast Charging

Fast-charging technology from Bosch and Shimano enables 0–80% charge in 1.5–2 hours for standard 500–625 Wh packs. Wireless charging pad integration and standardized battery sharing systems (as pioneered by e-bike rental operators) are emerging as the next-generation charging convenience features.

Connected Mobility and Smart E-Bike Platforms

Bosch's eBike Connect, Garmin integration, and Specialized's TURBO Connect Unit demonstrate how connected e-bike platforms create recurring software and service revenue streams, supplementing initial hardware sales, reshaping the industry's business model economics.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Mode |

Pedal Assist |

67.3% |

2025 |

|

Motor Type |

Mid Drive |

54.2% |

2025 |

|

Battery Type |

Lithium Ion |

82.4% |

2025 |

|

Class |

Class I |

48.5% |

2025 |

|

Design |

Non-Foldable |

74.6% |

2025 |

|

Application |

City/Urban |

56.2% |

2025 |

|

Country |

Germany |

32.8% |

2025 |

By Mode

To access detailed market analysis, Request Sample

Pedal assist dominates the mode segment with a 67.3% share in 2025 (approximately USD 4.32 Billion), benefiting from its classification as a conventional bicycle under EU regulations. Throttle-operated e-bikes account for 32.7% (~USD 2.11 Billion), representing a substantial and growing segment driven by commuter demand for effortless operation and adoption in e-cargo and last-mile delivery applications.

By Motor Type

Mid-drive motors lead the motor type segment with a 54.2% share in 2025 (~USD 3.49 Billion). Hub motors account for 38.6% (~USD 2.48 Billion), while other motor configurations (including friction drive and less common topologies) contribute 7.2% (~USD 0.46 Billion).

Mid-drive motors' dominance reflects European consumer preference for the natural pedaling feel, balanced weight distribution, and efficient use of the bicycle's existing gearing system they provide. Hub motors retain significant market share in entry-level urban commuter and cargo e-bike segments due to their lower unit cost and simpler integration.

Regional Market Insights

Germany's market leadership (32.8%, 2025) reflects that the e-bikes hold 53% of the market share of the total bike market in 2024, supported by an expansive cycling infrastructure network (over 70,000 km of dedicated cycle paths), strong employer commuter bike benefit programs, and a deeply embedded cycling culture.

|

Country |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

Germany |

32.8% |

World's highest e-bike adoption; JobRad employer scheme; dense cycling infrastructure |

EN 15194 compliance; S-Pedelec registration requirement; WEEE battery recycling |

|

France |

22.4% |

Bonus Vélo subsidy (up to EUR 400); Forfait Mobilité Durables; growing urban bike lanes |

French EPAC (Electrically Power Assisted Cycles) standard; ZFE low-emission zones in Paris/Lyon |

|

Italy |

16.3% |

Strong cycling tourism culture; Conto Energia Bici subsidy; Mediterranean urban density |

Italian DL 76/2020 e-bike incentive decree; urban area cycling plan requirements |

|

United Kingdom |

12.6% |

Cycle-to-Work scheme; post-Brexit shift to domestic brands; growing commuter segment |

EAPC regulations (max 250W, 25 km/h); DfT cycling investment programme |

|

Spain |

9.4% |

Urban congestion relief; growing cycling tourism in Catalonia/Basque Country; MOVES III subsidy |

Spanish MOVES III incentive (up to EUR 900); Regional cycling infrastructure plans |

|

Others |

6.5% |

Growing adoption in the Netherlands, Belgium, Switzerland, Poland, and Sweden |

Varied national regulations; EU CFP compliance; increasing infrastructure investment |

Northern European markets, including the Netherlands, Belgium, Denmark, and Sweden, demonstrate the highest per-capita e-bike adoption globally. As of January 1, 2025, there were 35,400 high-speed e-bikes in the Netherlands, an increase of over 2,000 compared to the previous year. These markets, however, have relatively smaller absolute populations, making Germany, France, and Italy the volume leaders in absolute terms.

Competitive Landscape

The European e-bike market exhibits a moderately concentrated competitive structure at the branded manufacturer level, with the top five players, Accell Group, Robert Bosch GmbH, Giant Bicycles, Riese & Müller GmbH, and Yamaha Motor Co. Ltd., collectively influencing approximately 35–40% of market value through direct sales and technology supply.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Accell Group |

Haibike, Winora, Ghost, Batavus, Koga, Lapierre, Raleigh, Sparta, Babboe, and Carqon |

Market Leader |

Europe's largest e-bike brand portfolio; pan-European distribution; mass-market and premium segments |

|

Robert Bosch GmbH |

Bosch eBike Systems |

Market Leader |

Leading motor & system supplier; Bosch-powered e-bikes command 35%+ of premium European market |

|

Giant Bicycles |

Giant, Liv |

Strong Challenger |

World's largest bicycle manufacturer; competitive value-performance ratio; global supply chain |

|

Riese & Müller GmbH |

Riese & Müller |

Strong Challenger |

German premium e-bike specialist; top-tier cargo and trekking e-bike portfolio; domestic manufacturing |

|

Yamaha Motor Co. Ltd. |

Yamaha e-bike Systems (PW Series) |

Challenger |

Pioneer e-bike motor supplier; growing direct brand presence in Europe; reliability reputation |

A substantial long tail of specialist e-bike brands, private-label importers, and emerging direct-to-consumer brands accounts for the balance. Additionally, numerous regional brands and new entrants continue to innovate in design, battery technology, and pricing strategies to capture market share.

Key Company Profiles

Accell Group

Accell Group, headquartered in Heerenveen, Netherlands, is one of Europe's largest e-bike companies by branded portfolio breadth and sales volume. Operating brands across the Netherlands, Germany, France, the UK, and other European markets.

- Product Portfolio: Full-spectrum urban commuter, trekking, performance, and children's e-bikes across 10 European brand identities; cargo and speed pedelec models across the portfolio.

- Recent Developments: Launched Ghost E-ASX e-MTB range with Bosch Performance CX motor for 2024 season; expanded Batavus urban cargo range.

- Strategic Focus: Consolidation of European market leadership through brand portfolio management; premium segment growth via Ghost, Haibike, and Winora brands; sustainability in manufacturing and supply chain.

Robert Bosch GmbH

Bosch eBike Systems, a division of Robert Bosch GmbH headquartered in Kusterdingen, Germany, is the world's leading supplier of e-bike drive systems and the defining technology standard in the European premium e-bike market.

- Product Portfolio: Performance Line CX (up to 100 Nm), Performance Line Speed (45 km/h), Active Line Plus (urban), Cargo Line (heavy-duty cargo) motor systems; PowerTube integrated batteries (400–800 Wh); eBike Flow app platform.

- Recent Developments: Launched Smart System platform with OTA firmware updates and ABS integration in 2023; announced Bosch eBike ABS with 20% improved braking performance; partnered with HERE Technologies for navigation integration.

- Strategic Focus: Technology platform standardization and ecosystem lock-in; smart connected e-bike system leadership; ABS and safety technology expansion.

Giant Bicycles.

Giant Bicycles, headquartered in Taichung, Taiwan, is the world's largest bicycle manufacturer and a significant force in the European e-bike market through its Giant and Liv brands. Giant operates a European distribution headquarters in the Netherlands and supplies e-bikes assembled in Taiwan and the Netherlands to over 30 European countries.

- Product Portfolio: Fathom E+, Trance X E+, FastRoad E+, Road E+ (with Yamaha motor systems); Liv e-bikes targeting female riders; urban, trekking, e-MTB, and e-road categories.

- Recent Developments: Expanded European assembly operations to reduce supply chain lead times post-2022; launched EnergyPak Smart battery system with enhanced diagnostics in 2024.

- Strategic Focus: Volume leadership through competitive value-performance positioning; European market presence deepening through premium model launches; female cyclist segment via Liv brand.

Market Concentration Analysis

The European e-bike market exhibits moderate concentration at the branded manufacturer level, with the top five players collectively influencing 35–40% of market value. However, the market is significantly more concentrated at the motor and battery system level, where Robert Bosch GmbH and Yamaha Motor Co. Ltd. collectively power an estimated 55–65% of premium European e-bikes.

The branded e-bike segment features over 200 active European brands, creating significant fragmentation below the top tier. Private equity consolidation activity has been substantial since 2019: the consolidation of Derby Cycle, Gazelle, and other brands into portfolio structures represents the dominant M&A trend.

Investment & Growth Opportunities

Fastest Growing Segments

E-cargo bikes (CAGR ~15%), connected e-bike platforms (CAGR ~18%), and speed pedelec commuter segment (CAGR ~9.5%) represent the three highest-growth investment vectors in the European e-bike market through 2034. Together, these niches address an incremental addressable market of approximately USD 3.2 Billion by 2034.

Emerging Market Expansion

Eastern Europe, particularly Poland, the Czech Republic, Romania, and Hungary, represents the most compelling geographic investment opportunity within Europe, as growing incomes, EU structural fund investment in cycling infrastructure, and nascent national e-bike subsidy programs drive initial market development from a low penetration base. City-level cycling infrastructure investment in Warsaw, Prague, and Budapest is accelerating adoption curves.

Venture and Institutional Investment Trends

- Solid-state battery startups, with e-bike-applicable technology (QuantumScape, Solid Power), are attracting significant venture investment, with commercialization timelines of 2027–2030 representing a potentially transformative supply chain inflection for the European market.

- E-bike subscription and fleet management platforms are attracting growth equity investment, with operators like Swapfiets (Netherlands), Cycleurope's subscription service, and B2B fleet leasing platforms targeting the corporate commuter and logistics operator segments.

- Battery recycling and second-life platforms are emerging as regulated infrastructure requirements under the EU Battery Regulation 2023/1542, creating investment opportunities in collection networks, second-life battery grading, and materials recovery operations.

Future Market Outlook (2026-2034)

The European e-bike market is positioned for sustained, broad-based growth through 2034. From a base of USD 6.43 Billion in 2025, the market is projected to reach USD 11.06 Billion by 2034 at a CAGR of 6.0%, representing cumulative incremental market value creation of approximately USD 4.63 Billion over the forecast horizon.

Regulatory evolution, particularly the EU's Urban Mobility Framework, the mandatory extension of cycling infrastructure under the revised TEN-T regulation, and increasingly stringent ICE vehicle restrictions in urban LEZs, will structurally reinforce e-bike adoption across the forecast period. Countries that extend and simplify e-bike purchase subsidies will see adoption curves steepen; policy reversal or subsidy withdrawal (as occurred in Germany in 2023–2024 for e-cars) represents a downside scenario risk for near-term growth.

Long-term, three structural macro-themes anchor the market's trajectory: urban decarbonization mandates creating a regulatory tailwind for zero-emission mobility; battery cost deflation continuing to expand the addressable consumer market; and the transformation of urban logistics toward e-cargo-centric last-mile delivery. The European e-bike sits at the intersection of all three, ensuring its structural growth through 2034 and beyond.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 140 industry participants in 2024–2025, including e-bike manufacturers, motor and battery system suppliers, retail dealers, fleet operators, urban mobility planners, and consumer associations across Germany, France, Italy, the UK, and the Netherlands.

Secondary Research

Secondary research encompassed a systematic review of European Commission transport statistics, national cycling federation data, company annual reports, trade publications (Bike Europe, ElectricBike Business), industry databases (Euromonitor, Statista), and publicly available regulatory and infrastructure investment documentation. Over 220 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating EU mobility statistics, national e-bike registration and sales data, battery cost deflation indices, and historical market evolution patterns. A base-case CAGR of 6.0% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates.

Europe E-Bike Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Modes Covered | Throttle, Pedal Assist |

| Motor Types Covered | Hub Motor, Mid Drive, Others |

| Battery Types Covered | Lead Acid, Lithium Ion, Nickel-Metal Hydride (NiMH), Others |

| Classes Covered | Class I, Class II, Class III |

| Designs Covered | Foldable, Non-Foldable |

| Applications Covered | Mountain/Trekking Bikes, City/Urban, Cargo, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Accell Group, Robert Bosch GmbH, Giant Bicycles, Riese & Müller GmbH, Yamaha Motor Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe e-bike market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Europe e-bike market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe e-bike industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe E-Bike Market Report

The Europe e-bike market reached USD 6.43 Billion in 2025 and is projected to reach USD 11.06 Billion by 2034, growing at a CAGR of 6.0% during 2026-2034.

The Europe e-bike market is expected to grow at a CAGR of 6.0% during 2026-2034, supported by government subsidies, battery technology advances, and expanding cycling infrastructure across the continent.

Pedal assist (pedelec) dominates with a 67.3% share in 2025, benefiting from EU regulatory equivalence with conventional bicycles under EN 15194 and consumer preference for a natural cycling experience.

Mid-drive motors lead with a 54.2% share in 2025, preferred for superior torque distribution, energy efficiency, natural pedaling feel, and compatibility with multi-speed drivetrains across trekking, mountain, and urban e-bike categories.

Germany leads with a 32.8% share in 2025, supported by the world's highest absolute e-bike sales volume (~5.3 million units in 2024), extensive cycling infrastructure, and strong employer commuter bike benefit schemes.

Key players include Accell Group, Robert Bosch GmbH, Giant Bicycles, Riese & Müller GmbH, and Yamaha Motor Co. Ltd., among others.

Key trends include the rapid growth of e-cargo bikes for urban logistics, subscription and lease model adoption expanding market access, connected e-bike platform development, and solid-state battery technology approaching commercial viability for extended-range e-bikes.

Key challenges include high initial purchase costs limiting mass-market penetration, inadequate charging and secure parking infrastructure, EU Battery Regulation compliance complexity, and regulatory fragmentation across member states for speed pedelecs and throttle e-bikes.

High-priority opportunities include e-cargo bike fleet deployment infrastructure, connected e-bike platform development, solid-state battery technology investment, e-bike subscription platform scaling, and market entry in high-growth Eastern European markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)