Europe Eyewear Market Size, Share, Trends and Forecast by Product, Gender, Distribution Channel, and Country, 2026-2034

Europe Eyewear Market Size, Share, Trends & Forecast (2026-2034)

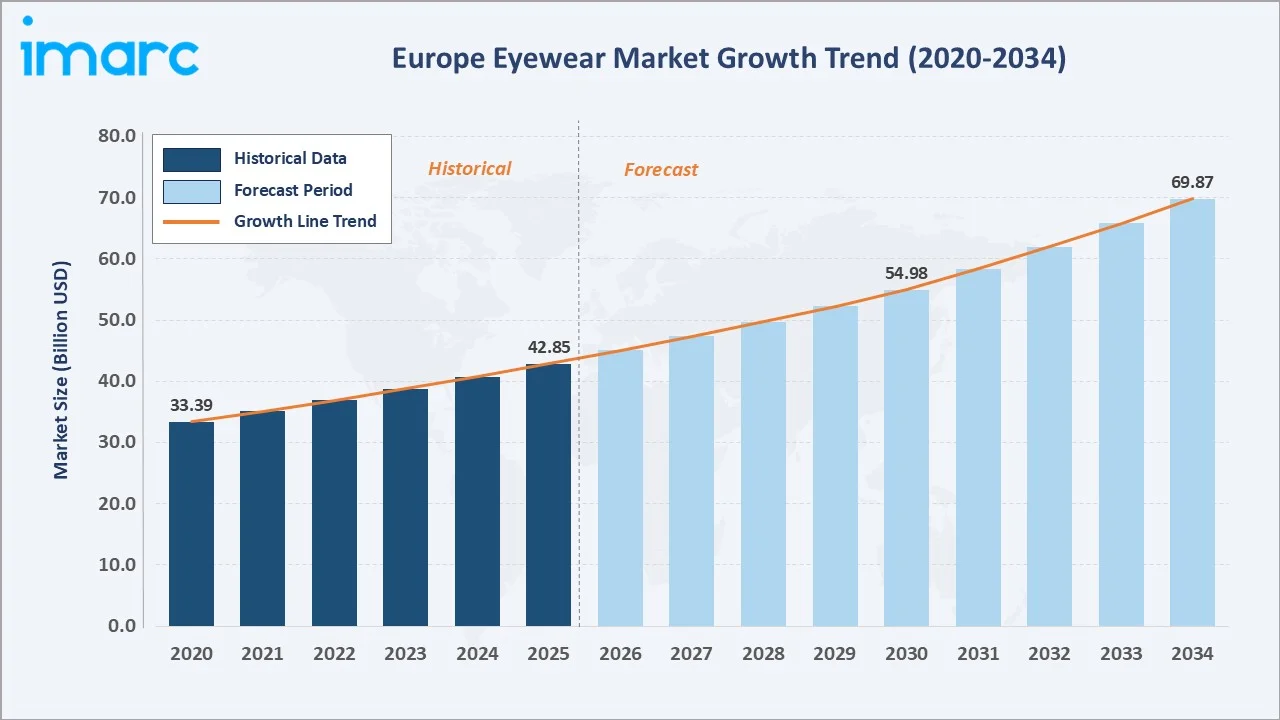

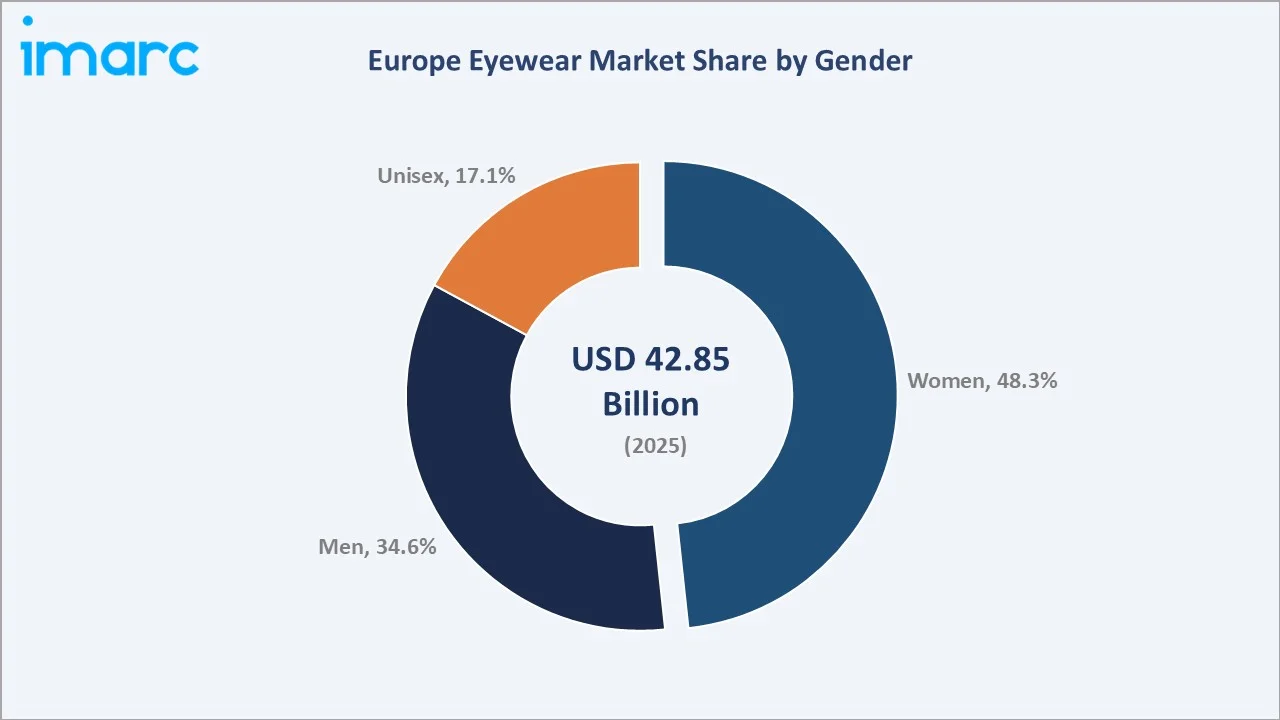

The Europe eyewear market size reached USD 42.85 Billion in 2025 and is projected to reach USD 69.87 Billion by 2034, exhibiting a CAGR of 5.11% during 2026-2034. Rising prevalence of refractive disorders, ageing demographics across Western Europe, and growing fashion-led demand for premium eyewear are primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 42.85 Billion |

|

Forecast Market Size (2034) |

USD 69.87 Billion |

|

CAGR (2026-2034) |

5.11% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

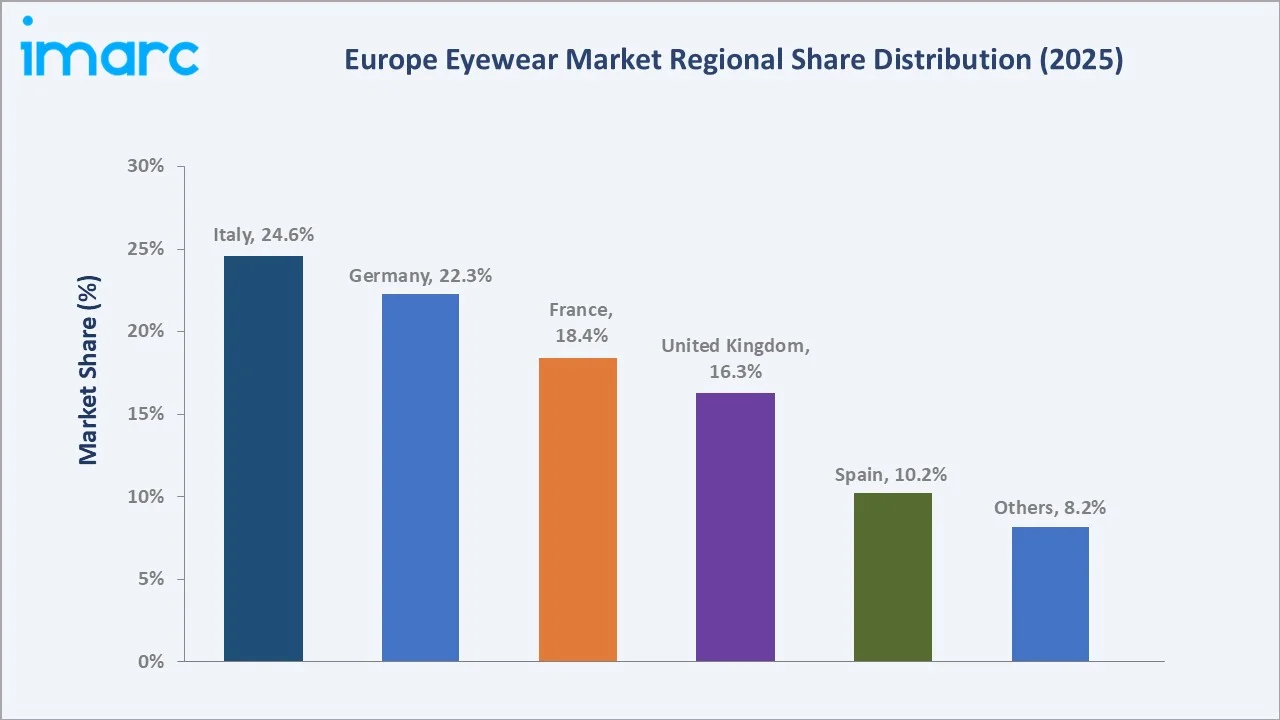

Largest Country |

Italy (24.6% share, 2025) |

|

Fastest Growing Country |

Spain (~5.6% CAGR) |

|

Leading Product Segment |

Spectacles (52.3%, 2025) |

|

Leading Gender Segment |

Women (48.3%, 2025) |

To get more information on this market, Request Sample

The Europe eyewear market growth trajectory from 2020 through 2034 contrasts historical expansion against a sustained forecast curve powered by ageing populations, screen-time-driven prescription demand, and premiumisation trends across residential and retail segments.

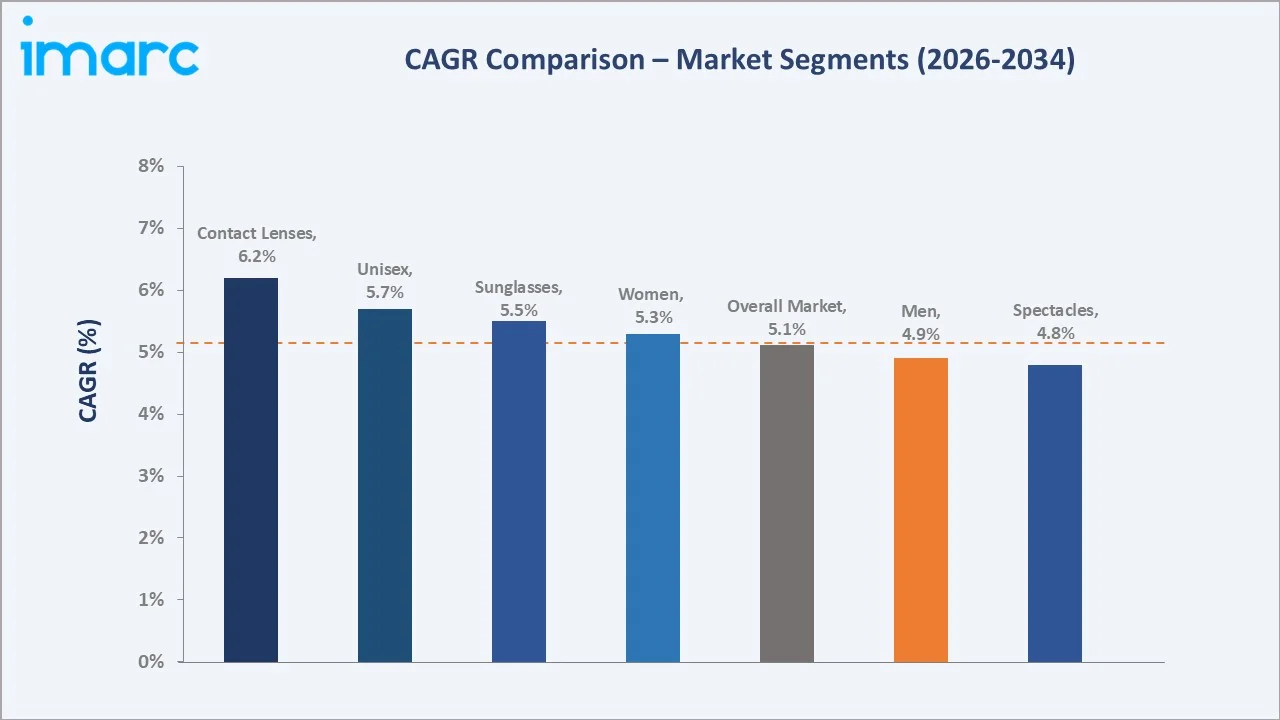

Segment-level CAGR comparisons highlight contact lens adoption and unisex segment expansion as the fastest-growing sub-categories within the Europe eyewear market forecast through 2034.

Executive Summary

The Europe eyewear market is undergoing structural transformation driven by demographic shifts, evolving lifestyle factors, and rapid technology adoption. Valued at USD 42.85 Billion in 2025, the market is forecast to reach USD 69.87 Billion by 2034 at a CAGR of 5.11%. An ageing population Europe has the world's highest share of citizens above 60 is generating sustained demand for corrective eyewear, particularly prescription spectacles.

Spectacles command a dominant 52.3% share in 2025, driven by optical corrections and fashion-forward frames at premium price points. Women consumers represent the single largest gender segment at 48.3%, reflecting higher fashion engagement and preventive healthcare participation.

Italy leads regional share at 24.6%, followed by Germany at 22.3% and France at 18.4%. The Europe eyewear market outlook remains strongly positive as premiumisation, sustainability design, and online channel expansion converge across the continent.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Spectacles – 52.3% share (2025) |

|

Second Product |

Sunglasses – 28.6% share (2025) |

|

Largest Gender |

Women – 48.3% share (2025) |

|

Fastest Growing Product |

Contact Lenses (~6.2% CAGR, 2026-2034) |

|

Leading Country |

Italy – 24.6% revenue share (2025) |

|

Second Leading Country |

Germany – 22.3% revenue share (2025) |

|

Top Companies |

EssilorLuxottica, Safilo Group S.p.A., Fielmann Group AG, Marchon Eyewear, Inc, Silhouette International Schmied AG, De Rigo Spa, Specsavers |

|

Market Opportunity |

Online channel projected at ~8.5% CAGR through 2030 |

Key Analytical Observations Supporting the Above Data:

- Spectacles Lead by Volume: Spectacles' 52.3% dominance in 2025 reflects the high prevalence of myopia and presbyopia in Europe. Germany alone accounts for 22.3% of the continent's eyewear revenue.

- Sunglasses – Premium Demand: Sunglasses' 28.6% share is driven by UV protection awareness campaigns, particularly in Southern Europe. Italian eyewear, which exports around 90% of its production closed the first half of 2025 with an export value of €2.8 billion, underpin premium positioning in this sub-segment.

- Women – Dominant Consumer: Women's 48.3% share reflects higher fashion engagement and more frequent optician visits for preventive eye care. Female consumers drive spending on designer frames and branded contact lenses across Western Europe.

- Italy – Manufacturing Powerhouse: Italy's 24.6% market share is underpinned by its status as the global eyewear manufacturing hub, housing brands such as Luxottica, Safilo, and De Rigo, which collectively generate multi-billion-euro revenues.

- Online Channel – Fastest Growing: Online eyewear retail is projected to grow at approximately 8.5% CAGR through 2030, outpacing offline channels as virtual try-on technology and direct-to-consumer platforms bypass traditional optical stores.

- Blue-Light Filter – New Standard: Blue‑light‑blocking lenses have become a mainstream product category, with many European opticians reporting that a significant portion of new prescriptions now include a blue‑light filter coating.

Europe Eyewear Market Overview

The Europe eyewear market encompasses a broad range of vision-correcting and protective products – including prescription spectacles, non-prescription sunglasses, and corrective contact lenses, serving residential consumers, healthcare professionals, and corporate buyers across the continent. Manufacturers operate within a complex ecosystem of optical retailers, independent brand showrooms, online platforms, and healthcare channels.

The industry sits at the convergence of healthcare demand, fashion preference, and technology-driven product innovation. Growth is underpinned by macroeconomic factors including an ageing European demographic, rising disposable incomes in Eastern Europe, digital eye strain driven by extended screen use, and tightening EU regulations on UV and blue-light protection standards. Simultaneously, the market is shifting toward premium, sustainable, and technology-enabled solutions, particularly blue-light-filtering lenses, AI-powered virtual fitting tools, and subscription-based contact lens models, redefining procurement and consumer engagement strategies across the region.

Market Dynamics

To evaluate market opportunities, Request Sample

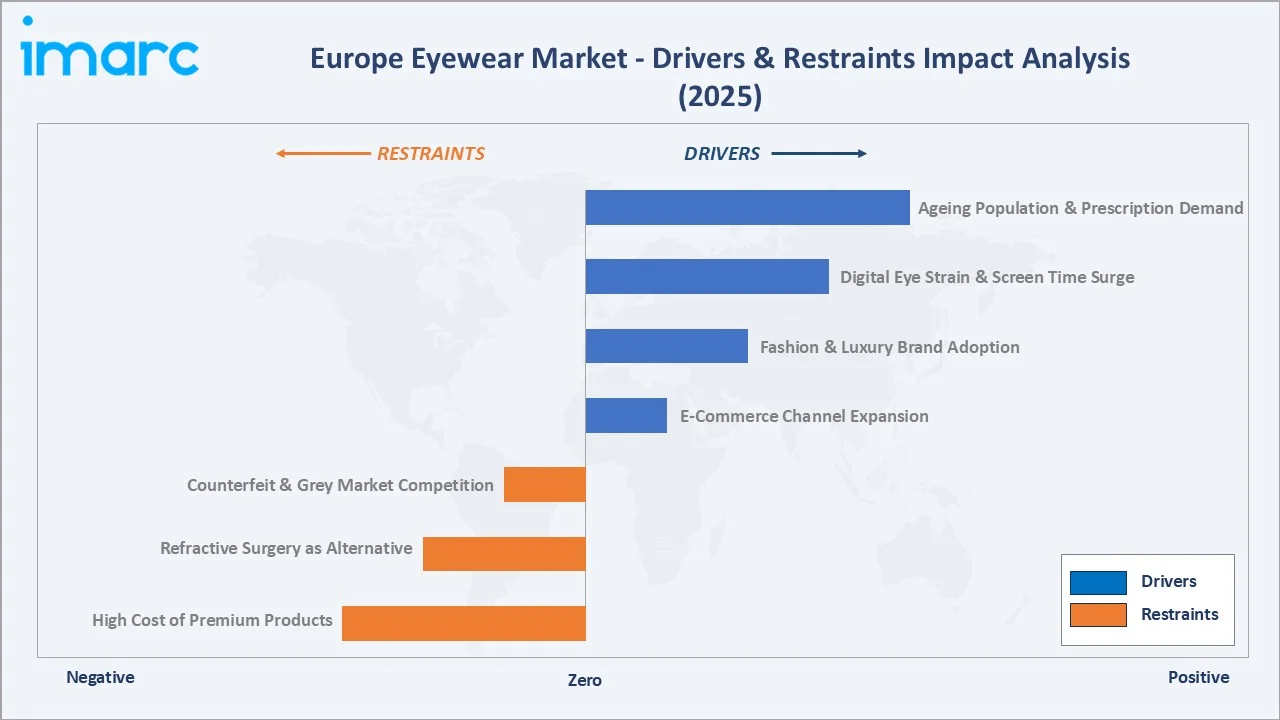

Market Drivers

- Ageing Population & Prescription Demand: Europe is home to the world's oldest population, with over 20% of residents aged 65 or above as of 2024. Age-related conditions such as presbyopia and macular degeneration generate persistent demand for progressive lenses and premium spectacle frames, creating a structural and expanding consumer base.

- Digital Eye Strain & Screen Time Surge: European workers now spend substantial time daily on screens. Rising awareness of digital eye strain – characterised by eye fatigue, blurred vision, and headaches – is accelerating prescriptions for blue‑light‑filtering lenses. Many European opticians report that a growing portion of new lens prescriptions now include blue‑light coatings.

- Fashion & Luxury Brand Adoption: Italy's luxury eyewear brands – including EssilorLuxottica, Safilo, and Marchon – maintain a premium global presence. European consumers increasingly view eyewear as a fashion accessory, driving demand for designer frames. The fashion eyewear segment continues to experience steady growth.

- E-Commerce Channel Expansion: European e‑commerce eyewear sales are steadily increasing. Virtual try‑on platforms – powered by AI and AR technology – are enabling consumers to purchase frames and contact lenses online with greater confidence, driving higher conversion rates on major platforms.

Market Restraints

- High Cost of Premium Products: Premium designer eyewear in Europe carries high price points, creating affordability barriers in Eastern European markets where per-capita healthcare expenditure is considerably lower than in Western Europe.

- Refractive Surgery as Alternative: LASIK refractive surgery continues to attract demand from younger and middle-aged adults, particularly in Germany and the UK, where procedure volumes are steadily increasing, potentially reducing long-term demand for prescription eyewear.

- Counterfeit & Grey Market Competition: The proliferation of low-cost counterfeit frames from unauthorised Asian manufacturers sold primarily through online marketplaces – erodes margin and brand equity, particularly for mid-tier European eyewear brands.

Market Opportunities

- Smart Eyewear & AR Integration: The European smart eyewear market – integrating AR displays, health monitoring, and connectivity – is in its early growth phase. Companies like EssilorLuxottica and Ray-Ban (Meta partnership) are investing heavily. The segment offers significant long-term revenue opportunity as hardware miniaturization improves.

- Eastern Europe Market Expansion: Eastern European markets – including Poland, Czech Republic, and Romania – are experiencing rapid middle-class expansion. Per-capita eyewear spending in these markets remains well below Western European levels, creating substantial catch-up growth potential.

- Sustainable Eyewear Innovation: Growing consumer consciousness around sustainable products in Western Europe is driving demand for bio-based, recycled, and biodegradable frame materials. Brands offering eco-certified eyewear are able to command notable price premiums in key markets such as France and Germany.

Market Challenges

- EU Regulatory Compliance: Compliance with EU CE marking requirements and the EU Medical Device Regulation (MDR) for certain vision-corrective products creates administrative and certification overhead for smaller manufacturers and new entrants.

- Extended Replacement Cycles: Consumers increasingly delay prescription updates due to cost concerns and time constraints, reducing replacement cycle frequency, particularly in Southern European markets affected by elevated living costs.

Emerging Market Trends

1. Blue-Light Lens Mainstreaming

Extended screen use across professional and personal contexts has elevated blue‑light‑filtering lenses from a niche offering to a mainstream prescription category. European opticians report that a growing portion of new prescriptions now include blue‑light coatings. Consumer awareness campaigns by brands like Essilor and HOYA are accelerating adoption, with blue‑light lenses expected to continue steady growth in the coming years.

2. AI-Powered Virtual Try-On & Personalisation

Augmented reality and AI-based virtual fitting tools are transforming the e‑commerce eyewear experience. Platforms such as EssilorLuxottica's GrandVision and Fielmann's digital channels now offer real-time frame fitting. These technologies are helping reduce return rates and boost online conversions, establishing digital retail as one of the fastest-growing distribution channels in Europe.

3. Sustainable & Eco-Conscious Frame Design

European consumers – particularly in France, Germany, and Scandinavia – are increasingly prioritising eco-certified and sustainable eyewear. Brands are launching collections using recycled acetate, bio-based resins, and reclaimed ocean plastic. Sustainable eyewear lines command notable price premiums, and the sub-segment is growing faster than the overall market.

4. Smart & Connected Eyewear Emergence

Smart eyewear integrating AR displays, health monitoring sensors, and wireless connectivity is moving from prototype to early commercial stage. The EssilorLuxottica and Meta partnership (Ray-Ban Stories) has achieved notable global sales. In Europe, early adoption is concentrated in Germany, France, and the UK, with mainstream adoption expected in the coming years as hardware costs decline.

5. Subscription-Based Contact Lens Models

Direct-to-consumer subscription services for daily disposable contact lenses are gaining traction across Europe. Platforms such as Lenstore and Vision Direct are experiencing strong growth. Monthly subscription models improve consumer retention and create recurring revenue streams, particularly appealing to younger and middle-aged adults.

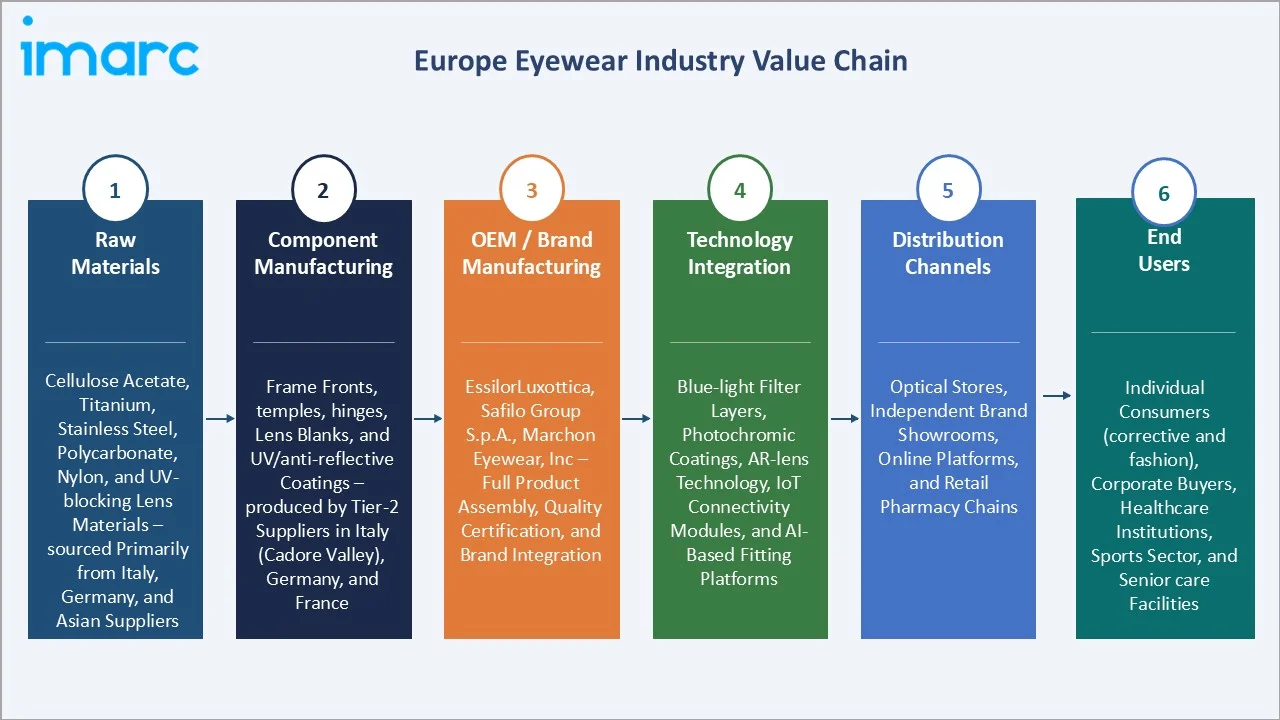

Industry Value Chain Analysis

The Europe eyewear industry value chain integrates six distinct stages from raw material extraction through final consumer delivery. Italy's Cadore Valley and Agordo district remain the world's most concentrated optical manufacturing clusters, hosting EssilorLuxottica's global headquarters and numerous Tier-1 suppliers. Each stage presents distinct competitive dynamics and margin profiles relevant to the overall Europe eyewear market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Cellulose acetate, titanium, stainless steel, polycarbonate, nylon, and UV-blocking lens materials – sourced primarily from Italy, Germany, and Asian suppliers |

|

Component Manufacturing |

Frame fronts, temples, hinges, lens blanks, and UV/anti-reflective coatings – produced by Tier-2 suppliers in Italy (Cadore Valley), Germany, and France |

|

OEM / Brand Manufacturing |

EssilorLuxottica, Safilo Group S.p.A., Marchon Eyewear, Inc – full product assembly, quality certification, and brand integration |

|

Technology Integration |

Blue-light filter layers, photochromic coatings, AR-lens technology, IoT connectivity modules, and AI-based fitting platforms |

|

Distribution Channels |

Optical stores, independent brand showrooms, online platforms, and retail pharmacy chains |

|

End Users |

Individual consumers (corrective and fashion), corporate buyers, healthcare institutions, sports sector, and senior care facilities |

OEM manufacturers hold the highest strategic value by integrating frames, lenses, coatings, and – increasingly – digital technologies into complete consumer solutions. E-commerce and direct-to-consumer channels are reshaping distribution, enabling brands to strengthen consumer relationships and capture higher margins by bypassing traditional optical retail intermediaries.

Technology Landscape in the Eyewear Industry

Lens Coating & Optical Technology

Anti-reflective, blue-light-filtering, and photochromic coatings are among the fastest-growing lens technology categories in Europe. Essilor's Crizal and Varilux product lines lead the premium progressive lens segment, while ZEISS and HOYA are investing in digitally customised freeform lens manufacturing that significantly reduces aberrations compared with conventional lenses, enhancing wearer comfort and supporting premium pricing.

Smart Materials & Frame Innovation

Bio-based acetate and titanium alloys are replacing conventional petroleum-based plastics in premium frame manufacturing. Memory metal frames – which return to original shape after bending – are gaining traction in the children's and sports segments. Nanocoating technologies are extending lens scratch and water resistance properties, improving product longevity and supporting sustainability positioning for major European brands.

Digital Fitting & AI Personalisation

AI-powered facial recognition tools are enabling precise frame-fit recommendations online and in-store. EssilorLuxottica's GrandVision platform and Fielmann's app-based fitting service are setting industry benchmarks. Virtual try-on technology helps reduce return rates and increase average order values, making digital fitting a strategic investment priority for European optical retailers.

Smart & Connected Eyewear

Early-stage smart eyewear products – including the Ray-Ban Meta smart glasses and BOSE Frames audio glasses – are creating a new technology convergence segment within the European market. Smart eyewear retail value in Europe is growing rapidly. Miniaturisation of AR displays and improvements in battery life remain critical technology hurdles to mainstream adoption, with industry consensus pointing to the late 2020s as the likely inflection point.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product | Spectacles | 52.3% |

2025 |

| Gender | Women | 48.3% |

2025 |

| Distribution channel | Online Stores |

🔒 |

2025 |

| Country | Italy | 24.6% |

2025 |

By Product

To access detailed market analysis, Request Sample

Spectacles lead the Europe eyewear market with a 52.3% share in 2025. This dominance is driven by the high prevalence of refractive conditions among European adults as well as the growing demand for designer frames as a fashion accessory.

By Gender

Women represent the dominant gender segment in the Europe eyewear market at 48.3% in 2025. Higher fashion engagement, more frequent optician visits, and greater brand consciousness among female consumers drive this leadership.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Italy |

24.6% |

Global eyewear manufacturing hub; EssilorLuxottica, Safilo, De Rigo; luxury brand exports |

|

Germany |

22.3% |

Fielmann dominance; high myopia prevalence; digital eye strain; optical engineering R&D |

|

France |

18.4% |

Designer brand affinity; UV protection awareness; luxury optical retail in Paris |

|

United Kingdom |

16.3% |

NHS optical voucher scheme; e-commerce growth; Specsavers market leadership |

|

Spain |

10.2% |

Tourism-driven sunglasses demand; growing middle class; increasing brand consciousness |

|

Others |

8.2% |

Eastern Europe catchup growth; Poland, Netherlands, Belgium; rising per-capita income |

Italy commands a 24.6% share of the Europe eyewear market in 2025, reflecting its unrivalled position as the global optical manufacturing capital. The Belluno province – home to EssilorLuxottica's headquarters – and the Cadore Valley cluster together employ a significant workforce in eyewear manufacturing. Italian eyewear exports are substantial, with the USA, France, and Germany among the top destinations.

Germany holds a 22.3% share, anchored by Fielmann AG – Europe's largest optical retailer. Germany's high myopia prevalence and strong disposable income drive volume and value equally. German consumers demonstrate high brand loyalty and above-average willingness to pay for optical technology upgrades, supporting ZEISS and HOYA's premium lens penetration.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

EssilorLuxottica |

Ray-Ban, Oakley, Persol, Oliver Peoples, Vogue Eyewear, Arnette, Alain Mikli, Costa, Bolon, Foster Grant |

Leader |

World's largest eyewear company; vertically integrated from lens to retail |

|

Safilo Group S.p.A. |

Carrera, Polaroid, Smith; licensed: BOSS, HUGO (Hugo Boss), Tommy Hilfiger, Kate Spade, Carolina Herrera |

Leader |

Licensed designer brands; strong Southern Europe and US retail presence |

|

Fielmann Group AG |

Fielmann |

Leader |

Europe's largest optical retail chain |

|

Marchon Eyewear, Inc |

Nike Vision, Flexon, Dragon, Calvin Klein, DKNY, Columbia, Lacoste, Karl Lagerfeld, Victoria Beckham, ZEISS |

Challenger |

Performance and sports eyewear; US + Europe distribution strength |

|

Silhouette International Schmied AG |

Silhouette, NEUBAU EYEWEAR, evil eye |

Challenger |

Ultra-lightweight rimless frames; Austrian precision manufacturing |

|

De Rigo Spa |

Police, Lozza, Sting, Yalea; licensed: Rodenstock Eyewear, Porsche Design Eyewear |

Challenger |

Italy-based; strong fashion segment; selective European and Asian distribution |

|

Specsavers |

Specsavers |

Emerging |

UK/Northern Europe dominance; value-for-money positioning; e-commerce growth |

The Europe eyewear market competitive landscape is moderately concentrated at the premium tier, with EssilorLuxottica commanding a dominant global position as the world's largest integrated eyewear company. Strategic differentiation increasingly centres on licensed brand portfolios, digital fitting technology, e-commerce capabilities, and sustainability credentials.

Key Company Profiles

EssilorLuxottica

EssilorLuxottica is the world's largest eyewear company, formed through the 2018 merger of Essilor International (France) and Luxottica Group (Italy). Headquartered in Paris, France, it operates across lens manufacturing, frame production, and optical retail on six continents.

- Product Portfolio: The portfolio spans iconic frame brands – Ray-Ban, Oakley, Persol, and Oliver Peoples – alongside leading lens brands including Varilux, Crizal, and Eyezen. The company also operates retail chains including LensCrafters, Sunglass Hut, and GrandVision

- Recent Developments: In 2025, EssilorLuxottica and Meta Platforms, Inc. have expanded their smart eyewear partnership by unveiling next-generation AI glasses at Meta Connect. The new lineup includes upgraded Ray-Ban Meta smart glasses and the newly introduced Oakley Meta Vanguard, designed to enhance style, connectivity, and performance.

- Strategic Focus: EssilorLuxottica's strategy centres on vertical integration from prescription lens to retail, digital fitting technology leadership, smart eyewear ecosystem development, and expansion of luxury licensed brands in high-growth Asian markets.

Safilo Group S.p.A.

Safilo Group Spa is one of Europe's largest eyewear manufacturers, headquartered in Padua, Italy. It serves 29 million customers with eyewear, contact lenses, hearing aids and primary eyecare services. It operates an omnichannel platform consisting of digital sales channels and more than 1,200 retail stores worldwide

- Product Portfolio: Safilo's portfolio includes owned brands Carrera, Polaroid, and Smith, alongside licensed designer collections for Hugo Boss, Tommy Hilfiger, and Levi's.

- Recent Developments: In 2025, Safilo Group S.p.A. has acquired a minority stake in Inspecs Group plc, marking a strategic move to strengthen its position in the optical sector. The investment is aimed at supporting Safilo’s long-term growth and expanding its presence in international markets.

- Strategic Focus: Safilo's strategy prioritises licensed brand portfolio diversification, sustainability-driven product innovation, digital transformation of sales channels, and operational efficiency through manufacturing centre consolidation in Italy and Slovenia.

Fielmann Group AG

Fielmann group AG is Europe's largest optical retail chain, headquartered in Hamburg, Germany. Founded in 1972 by Günther Fielmann, the company operates over 742 stores, serves more than 24 million customers across 14 countries.

- Product Portfolio: Fielmann offers its proprietary frame collections alongside branded spectacles, contact lenses, and hearing aids. It has established Fielmann as the dominant optical retailer in Germany, Austria, and Switzerland.

- Recent Developments: In 2026, Fielmann Group AG successfully concluded its Vision 2025 growth strategy, exceeding key targets despite challenging macroeconomic conditions. The company reported strong sales expansion, improved profitability, and significant international growth, reinforcing its position as a leading global vision care provider.

- Strategic Focus: Fielmann's strategy focuses on accelerating pan-European retail expansion through organic and acquisition-led growth, strengthening digital and e-commerce capabilities, and investing in AI-driven personalisation tools to reduce customer churn and increase repeat purchase frequency.

Market Concentration Analysis

The Europe eyewear market exhibits moderate fragmentation at the overall level, with distinct concentration patterns by segment. The top five players – EssilorLuxottica, Safilo Group S.p.A., Fielmann Group AG, Marchon Eyewear, Inc, Silhouette International Schmied AG – collectively account for approximately 35–42% of Europe eyewear market revenue in 2025.

At the premium and luxury tier, the market is highly concentrated. EssilorLuxottica alone accounts for approximately 20–25% of European eyewear revenue through its combination of iconic frame brands, optical retail chains, and prescription lens operations. This vertical integration creates a structural competitive advantage that is extremely difficult for challengers to replicate.

The market is also experiencing a bifurcated dynamic: premiumisation and brand consolidation at the top, with new e-commerce entrants and direct-to-consumer disruptors expanding the lower and mid-market. This dual dynamic is intensifying competition across all price tiers and distribution channels through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online channel sales represent the highest-growth distribution opportunity in the European eyewear market. Contact lenses are among the fastest-growing product categories. Smart eyewear – integrating AR and AI functionality – is an emerging premium technology segment, gaining strong momentum across Europe.

Emerging Market Expansion

Eastern Europe represents a high-potential regional growth opportunity within the European eyewear market. Markets such as Poland, the Czech Republic, Romania, and Hungary exhibit lower per-capita eyewear spending compared to Western Europe, alongside steadily improving income levels. Poland, in particular, represents a sizeable addressable market for eyewear brands and retailers willing to invest in localized distribution.

Venture & Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. Fielmann's expansion into Spain and the UK through store acquisitions reflects the ongoing trend of pan-European optical retail consolidation. Investments in AI-driven virtual try-on platforms, blue-light lens technology, and sustainable frame materials are key innovation priorities. Venture capital interest in direct-to-consumer e-commerce eyewear platforms – such as Mister Spex, Lenstore, and Vision Direct – is accelerating, supporting the continued growth of the online eyewear segment in Europe.

Future Market Outlook (2026-2034)

The Europe eyewear market forecast projects steady value expansion from USD 42.85 Billion in 2025 to USD 69.87 Billion by 2034 at a CAGR of 5.11%. Italy will retain its manufacturing leadership while facing increasing cost competition from Asian producers. Germany and the UK will sustain premium value growth through optical technology upgrades and e-commerce expansion. Eastern European markets will deliver above-average volume growth as incomes converge toward Western European levels.

Three structural shifts will reshape the Europe eyewear market through 2034. First, smart eyewear convergence will embed connectivity, AR displays, and health-monitoring functionality into mainstream eyewear by 2028–2030, creating a new premium product tier. Second, sustainability mandates – driven by EU Green Deal initiatives and consumer demand – will push bio-based and recycled materials to become standard in frame manufacturing. Third, AI-powered personalisation will transform prescription delivery, enabling digitally customised lenses manufactured to sub-micron precision, improving wearer outcomes and supporting premium pricing across all age groups.

The Unisex segment is projected to grow fastest at ~5.7% CAGR through 2034, reflecting broad generational and cultural shifts toward gender-neutral fashion. Contact lens subscriptions and blue-light-focused product categories will generate disproportionate revenue growth versus the overall market average of 5.11%.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with Europe eyewear industry stakeholders, including product directors at OEM manufacturers, procurement managers at optical retail chains, independent opticians across seven European markets, and institutional investors in consumer healthcare. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines specific to the European regional context.

Secondary Research

Secondary sources include European Commission healthcare statistics, WHO Vision Atlas data, Eurostat demographic databases, EU Annual Reports on Medical Devices, company annual reports from EssilorLuxottica, Safilo Group S.p.A., Fielmann Group AG, Marchon Eyewear, Inc, trade publications including Optician Magazine, Optical Prism, and Vision Monday Europe, and national optical association databases from Germany (ZVA), France (ROF), and the UK (ABDO).

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating European GDP growth rates, age-cohort demographic projections, healthcare expenditure data, e-commerce penetration indices, and historical eyewear market evolution patterns. Scenario analysis – base, optimistic, and conservative – was performed to account for macroeconomic uncertainty within the European Union and UK post-Brexit trade dynamics.

Europe Eyewear Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Spectacles, Sunglasses, Contact Lenses |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Optical Stores, Independent Brand Showrooms, Online Stores, Retail Stores |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | EssilorLuxottica, Safilo Group S.p.A., Fielmann Group AG, Marchon Eyewear, Inc, Silhouette International Schmied AG, De Rigo Spa, Specsavers, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe eyewear market from 2020-2034.

- The Europe eyewear market research report provides the latest information on the market drivers, challenges, and opportunities in the market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within the region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe eyewear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Eyewear Market Report

The Europe eyewear market was valued at USD 42.85 Billion in 2025, driven by rising prescription demand, ageing demographics, and growing fashion-led purchasing across the continent.

The market is projected to reach USD 69.87 Billion by 2034, growing at a CAGR of 5.11% during 2026-2034, supported by blue-light lens adoption, e-commerce growth, and smart eyewear emergence.

Spectacles lead with a 52.3% share in 2025, driven by the high prevalence of refractive conditions, designer frame demand, and progressive lens adoption among ageing consumers.

Contact lenses are the fastest-growing segment at ~6.2% CAGR through 2034, fuelled by daily disposable innovations and growing e-commerce subscription adoption.

Women account for 48.3% of revenue in 2025, reflecting higher fashion engagement, more frequent optician visits, and strong brand-led purchasing across Western Europe.

Italy leads with 24.6% share in 2025, anchored by its world-class optical manufacturing heritage. The country benefits from a strong ecosystem of globally recognized manufacturers, skilled craftsmanship, and established export networks.

Key players include EssilorLuxottica, Safilo Group S.p.A., Fielmann Group AG, Marchon Eyewear, Inc, Silhouette International Schmied AG, De Rigo Spa, and Specsavers.

Key drivers include an ageing population, digital eye strain, fashion premiumisation, EU regulatory standards, e-commerce expansion, and smart eyewear technology adoption.

The Europe eyewear market is projected to grow at a CAGR of 5.11% during 2026-2034, driven by rising vision care awareness, increasing screen exposure, and continuous innovation in lens technologies and premium eyewear products.

Key trends include blue-light lens mainstreaming, AI-powered virtual try-on, sustainable bio-based frame materials, smart eyewear convergence, and direct-to-consumer subscription models.

Eastern Europe represents a significant catch-up opportunity, with per-capita spending remaining below Western European levels. Poland, in particular, is expected to emerge as a sizeable market in the coming years, offering strong growth potential for eyewear brands and retailers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)