Europe Governance, Risk and Compliance Platform Market Size, Share, Trends and Forecast by Deployment Model, Solution, Component, Service, End User, Vertical, and Country, 2026-2034

Europe Governance, Risk and Compliance Platform Market Size, Share, Trends & Forecast (2026-2034)

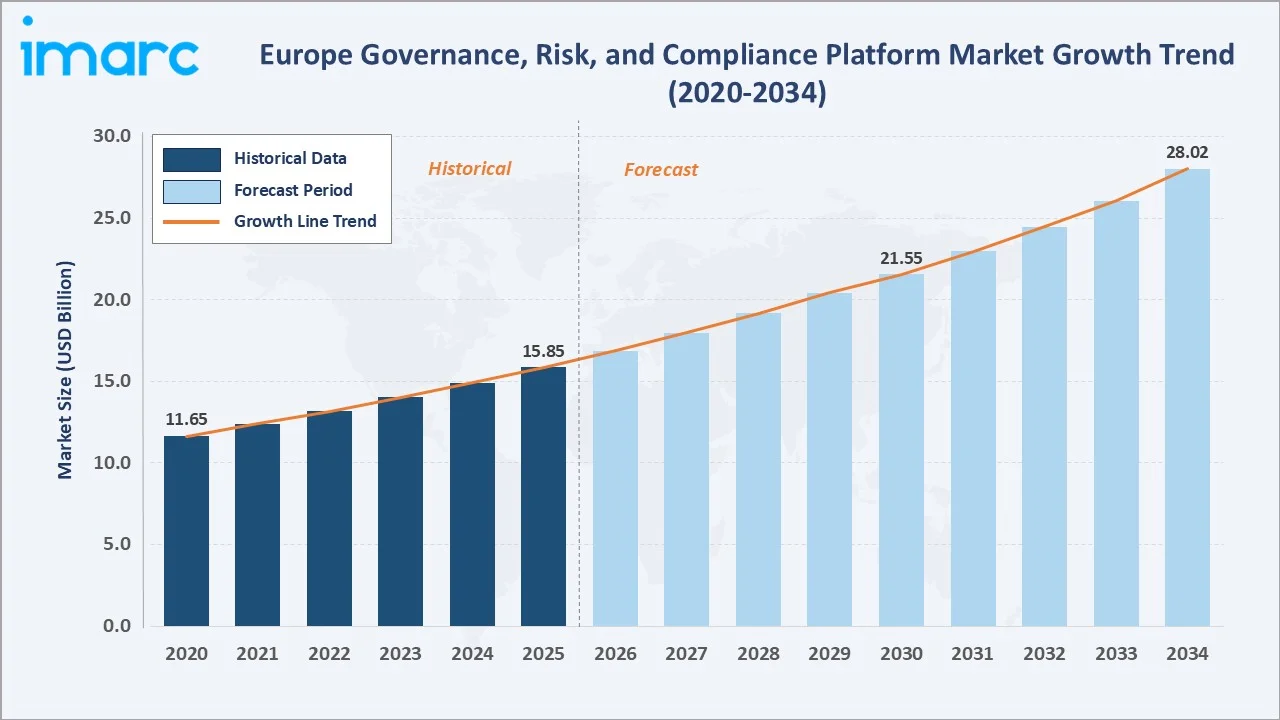

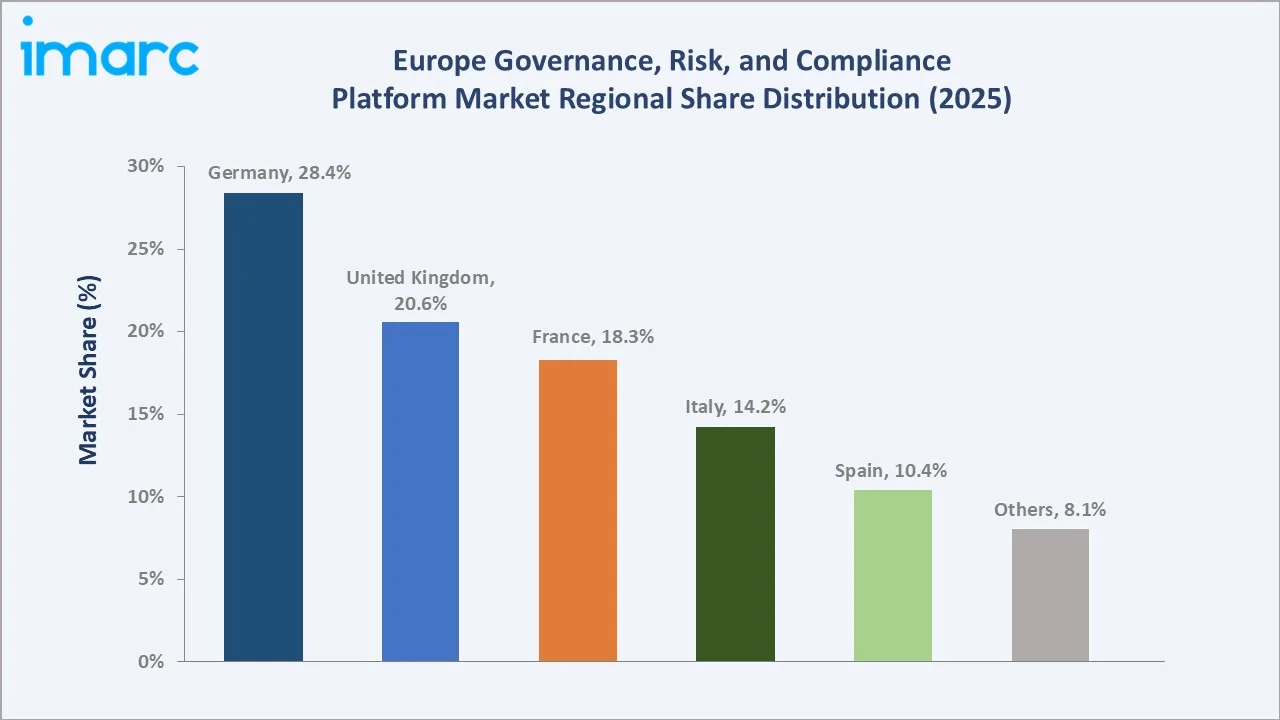

The Europe governance, risk, and compliance (GRC) platform market size was valued at USD 15.85 Billion in 2025 and is projected to reach USD 28.02 Billion by 2034, exhibiting a CAGR of 6.34% during 2026-2034. Organizations are navigating an increasingly complex regulatory landscape encompassing GDPR, DORA, NIS2, and CSRD mandates. Cybersecurity threats are escalating, with European financial institutions recording a 25% rise in external breaches in 2024. Simultaneously, the rapid migration to cloud infrastructure and digital transformation is broadening the adoption of governance, risk, and compliance platforms. On-Premises deployment leads with 55.8% share in 2025, while Software commands 60.9% of the component segment. Germany accounts for the largest country share at 28.4% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.85 Billion |

|

Forecast Market Size (2034) |

USD 28.02 Billion |

|

CAGR (2026-2034) |

6.34% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Deployment Model |

On-Premises (55.8%, 2025) |

|

Fastest Growing Model |

Cloud-Based GRC (CAGR ~9.8%) |

|

Leading Component |

Software (60.9%, 2025) |

|

Largest Country |

Germany (28.4%, 2025) |

To get more information on this market, Request Sample

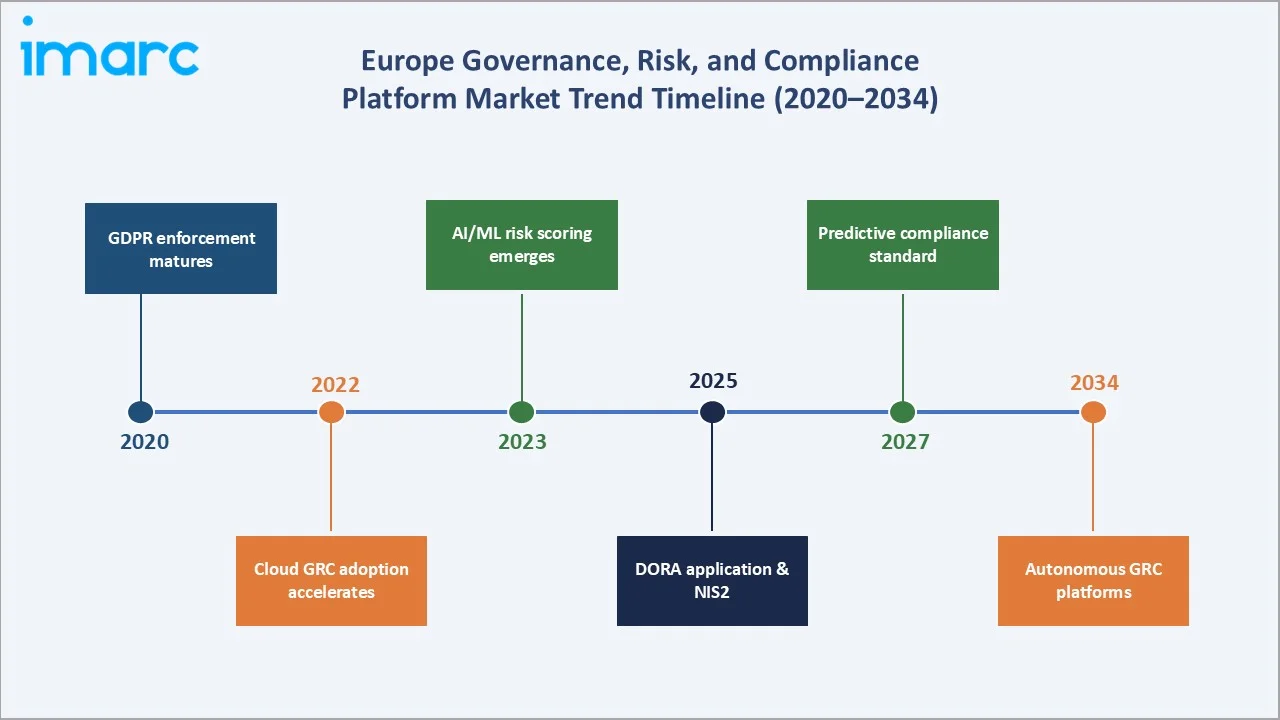

The Europe Governance, Risk and Compliance Platform market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve driven by digital transformation, tightening regulatory compliance requirements, and escalating cybersecurity risk across European enterprises.

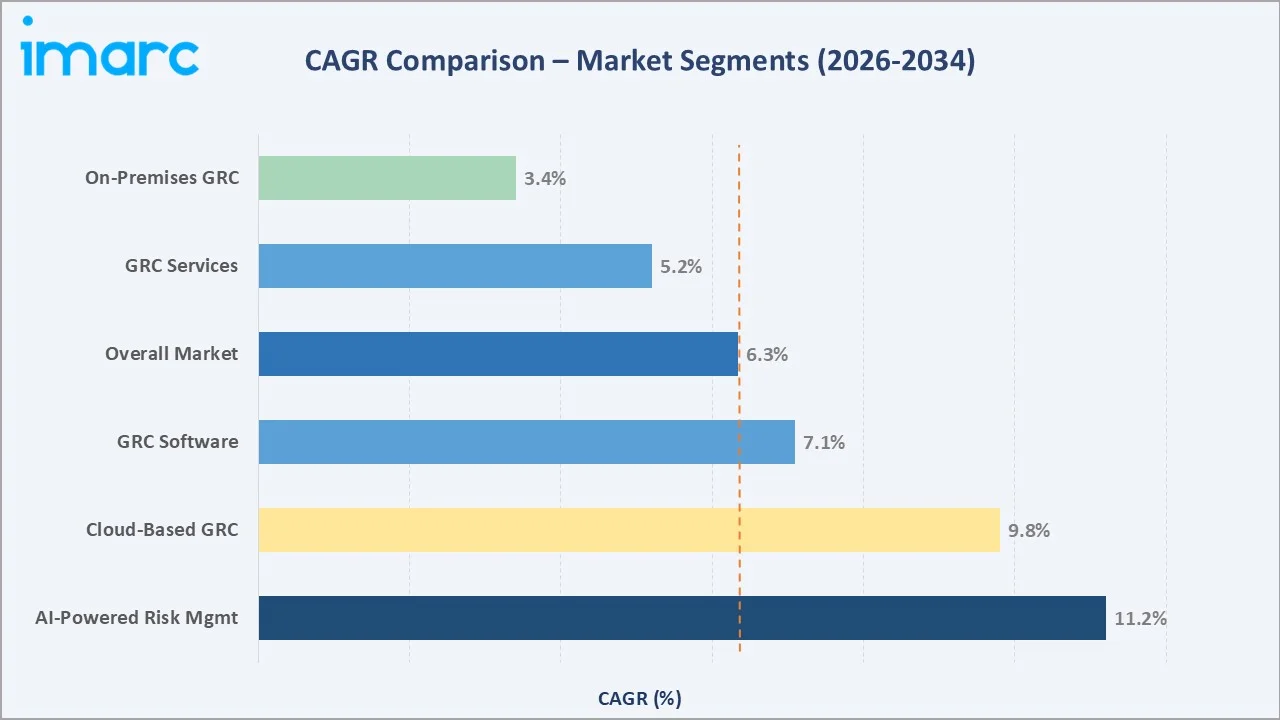

Segment-level CAGR comparisons highlighting Cloud-Based GRC and AI-Powered Risk Management as the two fastest-growing sub-categories within the Europe Governance, Risk and Compliance Platform market through 2034.

Executive Summary

The Europe Governance, Risk and Compliance Platform market is at a structural inflection point where regulatory pressure, digital risk, and enterprise governance demands converge. Valued at USD 15.85 Billion in 2025, the market is forecast to reach USD 28.02 Billion by 2034 at a CAGR of 6.34%. Organizations across BFSI, healthcare, energy, and manufacturing are deploying integrated GRC solutions to automate compliance workflows, centralize risk visibility, and efficiently meet audit obligations. The European Commission planned to present a GDPR simplification proposal in June 2025 as part of a broader omnibus package to reduce SME compliance burdens, illustrating the dynamic regulatory environment driving platform adoption.

On-premises platforms retain majority preference at 55.8% in 2025, particularly among regulated financial institutions and government bodies that prioritize data sovereignty. However, cloud-based GRC is the fastest-growing sub-segment as multinational enterprises seek scalability and cross-border collaboration. The software component dominates at 60.9%, underpinned by demand for real-time dashboards, AI-driven risk scoring, and automated regulatory change management. Germany, the United Kingdom, and France together account for over 67% of the regional market, anchored by their mature regulatory ecosystems and large enterprise density.

Emerging priorities, including ESG reporting under CSRD, third-party risk management under DORA, and operational resilience requirements, are broadening the scope of governance, risk, and compliance platforms. Vendors are integrating AI and machine learning to shift compliance posture from reactive to predictive, reinforcing the long-term growth outlook through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Model |

On-Premises - 55.8% share (2025) |

|

Leading Component |

Software - 60.9% share (2025) |

|

Fastest Growing Sub-Segment |

Cloud-Based GRC (~9.8% CAGR) |

|

Largest Country |

Germany - 28.4% share (2025) |

|

Second Largest Country |

United Kingdom - 20.6% share (2025) |

|

Top Companies |

IBM Corporation, SAP SE, MetricStream, ServiceNow, STG Partners, LLC. |

Key Analytical Observations Supporting the Above Data:

- On-Premises Dominance: On-premises' 55.8% share in 2025 reflects the risk aversion of regulated industries such as BFSI and government, where data localization is non-negotiable under GDPR and sector-specific mandates.

- Software Leadership: Software's 60.9% component share is driven by demand for configurable rule engines, AI-assisted risk scoring modules, and real-time regulatory update libraries that reduce manual compliance effort.

- Cloud Growth Acceleration: Cloud GRC platforms are projected to outpace on-premises growth through 2034 as hybrid work models require anywhere-access to compliance data and SaaS pricing lowers total cost of ownership for mid-market enterprises.

- Germany's Market Leadership: Germany accounts for 28.4% of the regional market, supported by its position as Europe's largest economy, the BaFin regulatory regime, and broad enterprise adoption in automotive and industrial manufacturing.

- AI Integration: AI-powered predictive risk analytics are becoming a standard feature expectation, with vendors embedding natural language processing for policy management and machine learning for anomaly detection across audit trails.

Europe Governance, Risk, and Compliance Platform Market Overview

GRC platforms are integrated software suites enabling organizations to unify governance policy management, enterprise risk assessment, and multi-jurisdictional compliance tracking within a single operational framework. The ecosystem spans audit management, risk registers, policy libraries, compliance calendars, incident tracking, and reporting dashboards. Key end-user verticals include BFSI, energy and utilities, healthcare, government, manufacturing, and telecom.

Macroeconomic enablers include the EU regulatory intensification cycle anchored by GDPR, DORA, NIS2, CSRD, and the upcoming EU AI Act, alongside an escalating cybersecurity threat landscape. European enterprises reported a 25% rise in external cyber breaches in 2024 (SecurityScorecard), directly accelerating GRC platform procurement across all major industry verticals.

Market Dynamics

To evaluate market opportunities, Request Sample

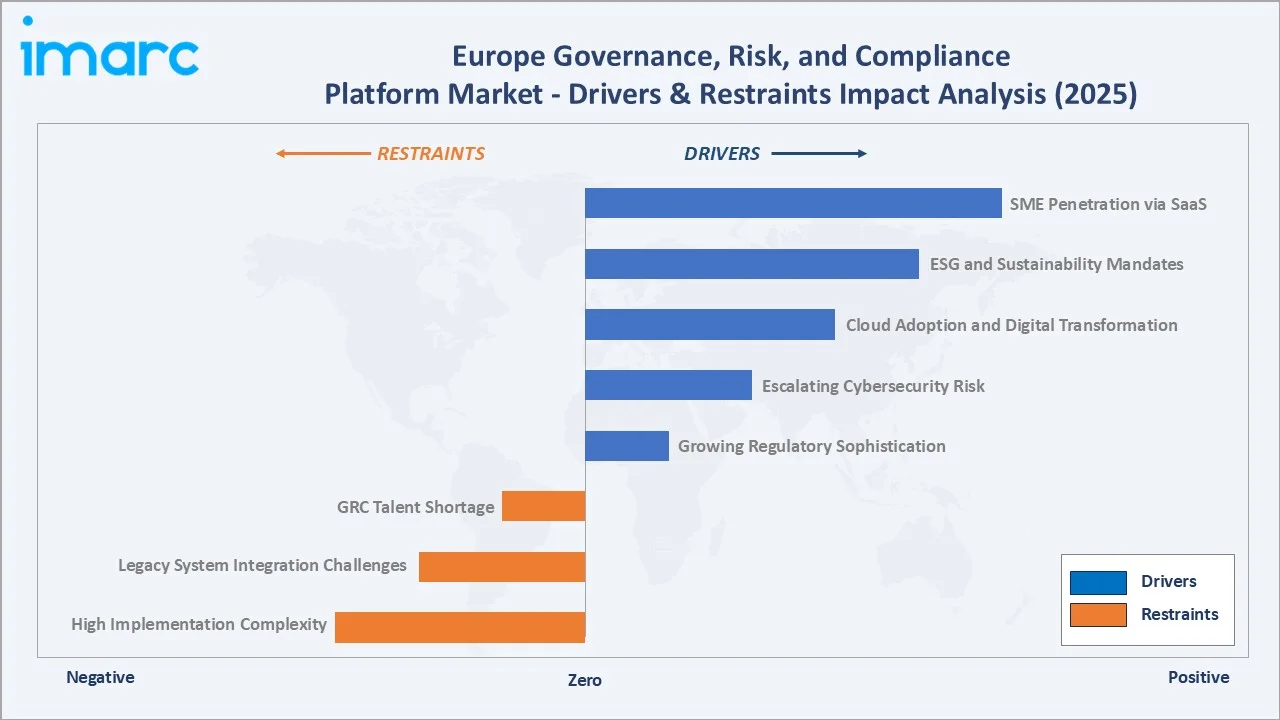

Market Drivers

- Growing Regulatory Sophistication: Organizations navigate GDPR, DORA (applied January 2025), NIS2 transposition, and CSRD mandates simultaneously. GRC platforms automate compliance tracking, documentation, and deadline management across these overlapping frameworks.

- Escalating Cybersecurity Risk: European financial institutions experienced a 25% rise in external cyber breaches in 2024. GRC platforms provide centralized vulnerability tracking, incident response workflows, and regulatory reporting against ISO 27001 and NIST CSF.

- Cloud Adoption and Digital Transformation: Enterprise migration to cloud infrastructure is generating demand for cloud-native GRC platforms. IMARC projects the Europe data center market to reach USD 130.1 Billion by 2033, reflecting the infrastructure scale underpinning this transition.

- ESG and Sustainability Mandates: CSRD applies to over 50,000 European companies from FY2024, mandating standardized ESG disclosures. GRC platforms are being extended to serve as ESG data collection, validation, and assurance engines.

Market Restraints

- High Implementation Complexity: Enterprise-wide GRC deployments require extensive process mapping, data migration, and cross-departmental change management, with large-organization rollouts spanning 12-24 months.

- Legacy System Integration Challenges: Many European organizations operate legacy ERP and risk systems lacking modern APIs, making integration with GRC platforms technically demanding and costly.

- GRC Talent Shortage: A pan-European deficit in professionals who understand both GRC platforms and regulatory requirements constrains adoption velocity, particularly for in-house deployments.

Market Opportunities

- SME Penetration via SaaS: Only ~35% of European SMEs had deployed formal GRC tools as of 2024. Cloud SaaS models with modular pricing are opening a large underserved segment as SMEs face growing NIS2 and CSRD obligations.

- TPRM Expansion under DORA: DORA's ICT third-party risk requirements and EBA outsourcing guidelines are driving demand for TPRM modules, creating an incremental revenue opportunity for vendors in the financial services vertical.

- AI-Powered Predictive Compliance: Integration of generative AI for regulatory text analysis, policy drafting, and predictive non-compliance alerts represents a key differentiation frontier, with early BFSI and healthcare adopters demonstrating measurable audit efficiency gains.

Market Challenges

- Data Privacy Conflicts: Cross-border data flows within GRC platforms for multinational organizations create regulatory conflicts between GDPR and national data residency requirements across EU member states.

- Vendor Fragmentation: The European governance, risk, and compliance platform market has over 40 active vendors competing across sub-segments. Buyers face decision fatigue and integration risk when selecting between point solutions and integrated platforms.

Emerging Market Trends

1. AI and Machine Learning Integration in Risk Management

Vendors are embedding AI capabilities across GRC platforms to automate policy gap analysis, predict audit findings, and generate regulatory change impact assessments. Machine learning models trained on historical compliance data are enabling organizations to shift from periodic compliance audits to continuous monitoring. Major vendors, including IBM OpenPages and SAP GRC, have announced generative AI roadmaps targeting automated risk narrative generation by 2026-2027.

2. Convergence of Cybersecurity and Enterprise GRC

The boundary between cybersecurity risk management and enterprise GRC is dissolving. Platforms are integrating with SIEM tools, vulnerability scanners, and threat intelligence feeds to provide a unified risk posture view. This convergence is particularly pronounced in financial services, where DORA mandates integrated ICT risk management and regulatory reporting for digital operational resilience.

3. ESG Compliance as a Core GRC Use Case

CSRD's mandatory application for large EU companies is generating a new GRC use case: ESG data management and assurance. Organizations are extending compliance frameworks to capture Scope 1, 2, and 3 emissions data, supply chain due diligence records, and diversity metrics, all requiring the audit trail and reporting capabilities central to GRC platforms.

4. Cloud-Native and Microservices Architecture Adoption

Legacy on-premises GRC platforms are being replaced by cloud-native architectures offering API-first design, containerized microservices, and real-time data synchronization across global deployments. This enables more rapid regulatory rule updates and scalable multi-entity configurations for large financial and industrial groups.

5. Consolidation and Platform Expansion by Tier-1 Vendors

The European governance, risk, and compliance platform market is experiencing strategic consolidation, with enterprise platform vendors acquiring point-solution providers to broaden compliance coverage. ServiceNow, SAP, and IBM reflect a platform-first competitive dynamic that is reshaping the vendor landscape and raising entry barriers for new entrants.

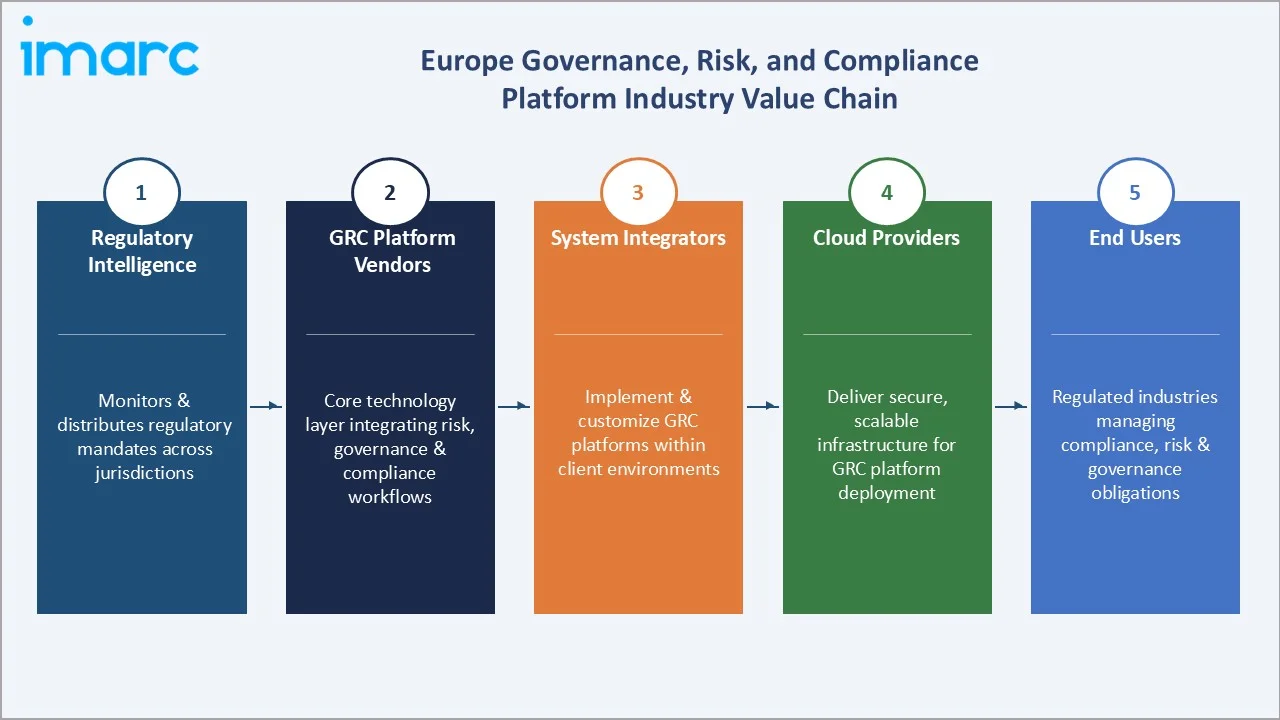

Industry Value Chain Analysis

The Europe Governance, Risk and Compliance Platform value chain encompasses five integrated stages from regulatory intelligence providers through to end-user organizations. System integrators and managed service providers play a critical intermediary role in configuring and deploying platforms for enterprise clients.

|

Stage |

Key Players / Activities |

|

Regulatory Intelligence Providers |

Aggregate, monitor, and distribute regulatory updates, legal frameworks, and compliance mandates across jurisdictions to inform downstream actors. |

|

GRC Platform Vendors |

Develop integrated software platforms that automate governance workflows, risk assessments, and compliance reporting — serving as the core technology layer. |

|

System Integrators & Consultants |

Customise, implement, and manage GRC solutions within client environments, bridging technology with operational and regulatory requirements. |

|

Cloud & Infrastructure Providers |

Supply scalable, secure cloud hosting and data infrastructure that underpins GRC platform deployment, performance, and compliance-grade data handling. |

|

End Users |

Consume GRC solutions to manage internal governance obligations, regulatory compliance, and enterprise risk across regulated industries and public sector entities. |

Governance, risk, and compliance platform vendors occupy the highest strategic value position in the value chain, integrating regulatory content, workflow automation, and analytics into turnkey compliance solutions. However, the growing importance of managed services is elevating system integrators as co-creators of value rather than mere deployment partners.

Technology Landscape in the GRC Platform Industry

Artificial Intelligence and Predictive Analytics

AI is now central to modern GRC platforms. Natural language processing (NLP) enables platforms to parse complex regulatory texts and map requirements to internal controls automatically. Machine learning models flag anomalous patterns in audit trails and predict compliance breaches before they occur. Vendors are increasingly offering pre-trained models for GDPR, DORA, and NIS2 requirement mapping, reducing configuration effort and deployment time significantly.

Cloud-Native Architecture and API Integration

API-first, microservices-based cloud architectures are replacing monolithic on-premises GRC systems, enabling faster regulatory updates and scalable multi-entity configurations. These platforms connect seamlessly with ERP systems (SAP, Oracle), SIEM tools, identity management platforms, and third-party risk data providers, creating a unified enterprise risk intelligence infrastructure that supports real-time decision-making.

Automation and Workflow Orchestration

Robotic process automation (RPA) within GRC platforms is eliminating manual evidence collection, control testing, and reporting workflows. Automated regulatory change management modules monitor official EU and national regulatory channels, triggering workflow updates when new requirements are published. This capability is particularly valued by compliance teams managing overlapping GDPR, NIS2, and DORA obligations concurrently.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Deployment Model |

On-Premises |

55.8% |

2025 |

|

Solution |

Compliance Management |

35.5% |

2025 |

|

Component |

Software |

60.9% |

2025 |

|

Service |

Consulting |

45.8% |

2025 |

|

End User |

Medium Enterprise |

🔒 |

2025 |

|

Vertical |

BFSI |

25.8% |

2025 |

|

Country |

Germany |

28.4% |

2025 |

By Deployment Model

To access detailed market analysis, Request Sample

On-premises GRC platforms held a dominant 55.8% share of the Europe market in 2025. Financial institutions, government entities, and healthcare organizations with strict data sovereignty requirements continue to prefer in-house deployment. These organizations prioritize full control over system configuration, integration with legacy enterprise systems, and compliance with sector-specific data localization rules under GDPR and national frameworks.

Cloud-based platforms held 44.2% in 2025 and represent the fastest-growing sub-segment. SaaS GRC platforms offer lower total cost of ownership, rapid deployment, automatic regulatory updates, and cross-border collaboration capabilities - critical for multinational enterprises managing compliance across multiple EU jurisdictions. Cloud's share is projected to surpass on-premises by the early 2030s as migration accelerates.

By Component

Software accounted for 60.9% of the Europe Governance, Risk, and Compliance Platform market in 2025. This encompasses core platform licenses covering audit management modules, risk registers, policy libraries, compliance calendars, and reporting dashboards. Demand is driven by organizations replacing manual spreadsheet-based compliance tracking with automated, audit-ready digital systems that can scale across global operations.

Services represented 39.1% in 2025, comprising implementation, consulting, training, and managed services. As GRC platform complexity increases and regulatory scope broadens, organizations increasingly rely on specialized providers for configuration, change management, and ongoing regulatory advisory. Managed GRC services are gaining traction among mid-market organizations lacking in-house GRC expertise.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

Regulatory Context |

|

Germany |

28.4% |

Industrial base, BFSI compliance, and GDPR enforcement depth |

BaFin, BSI, KWG, NIS2 transposition |

|

United Kingdom |

20.6% |

Financial services GRC, post-Brexit regulatory realignment |

FCA, PRA, UK GDPR, Operational Resilience PS21/3 |

|

France |

18.3% |

Banking, insurance, government GRC programs |

ACPR, AMF, ANSSI, CNIL |

|

Italy |

14.2% |

Banking sector modernization, energy utility compliance |

Banca d'Italia, Consob, ACN |

|

Spain |

10.4% |

Financial services, utilities, and the emerging tech sector |

CNMV, Banco de España, AEPD |

|

Others |

8.1% |

NIS2 and CSRD transposition driving nascent GRC adoption |

National regulators aligned with EU directives |

Germany held the largest country share at 28.4% in 2025, underpinned by its position as Europe's largest economy, the demanding regulatory environment set by BaFin and the BSI, and sector-specific compliance obligations across automotive, industrial, and financial services verticals. The country's dense Mittelstand industrial base is increasingly adopting GRC platforms as NIS2 transposition requirements extend cybersecurity obligations to mid-sized manufacturers and operators.

The United Kingdom followed at 20.6% in 2025, supported by robust financial services GRC investment under the FCA's Operational Resilience framework. Despite post-Brexit divergence from EU regulatory pathways, UK firms maintaining EU market access continue to align with GDPR and DORA requirements. France represented 18.3%, driven by ACPR-regulated banking and insurance sectors and strong government-sector GRC procurement. Italy (14.2%) and Spain (10.4%) are mid-tier markets characterized by growing GRC adoption in banking and utilities. The remaining countries (8.1%) collectively represent emerging markets where GRC adoption is nascent but accelerating under NIS2 and CSRD transposition timelines.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

IBM Corporation |

IBM OpenPages |

Leader |

AI-powered GRC, Watsonx integration, BFSI depth |

|

SAP SE |

SAP GRC |

Leader |

ERP-native GRC, CSRD/ESG module, S/4HANA integration |

|

MetricStream |

Cyber GRC |

Challenger |

Enterprise risk, audit management, cloud-native GRC |

|

ServiceNow |

Governance, Risk, and Compliance (GRC) |

Leader |

IT-centric GRC, ITSM/GRC convergence, rapid SaaS growth |

|

STG Partners, LLC |

SAI360 |

Emerging |

Cyber risk GRC, financial services legacy installed base, integrated risk management |

|

Diligent Corporation |

Diligent One |

Established Player |

Audit management, board governance, ESG reporting |

|

LogicGate, Inc. |

Risk Cloud Platform |

Emerging |

SME-friendly, no-code workflows, rapid cloud deployment |

The Europe Governance, Risk and Compliance Platform market is moderately concentrated, with a mix of global enterprise platform vendors, specialist GRC software providers, and regional players. Tier-1 vendors such as IBM and SAP benefit from deep enterprise relationships and the ability to embed GRC within broader ERP and security ecosystems. The market is experiencing consolidation as large platform vendors acquire point-solution providers to broaden compliance coverage and raise entry barriers for new entrants.

Key Company Profiles

IBM Corporation

IBM Corporation is a global technology and consulting leader headquartered in Armonk, New York, with operations in over 175 countries. In Europe, IBM maintains a significant presence across BFSI, government, and healthcare sectors, with a dedicated Risk and Compliance practice serving major financial institutions and regulated enterprises.

- Product & Platform Portfolio: IBM OpenPages GRC Platform, Watson-powered risk analytics, Financial Crimes Insight, Regulatory Change Management.

- Recent Developments: In November 2025, IBM, alongside large technology firms such as Accenture plc, Amazon Web Services EMEA, and Microsoft Ireland Operations, was officially designated as a critical third-party provider (CTPP). This designation falls under the EU Digital Operational Resilience Act (DORA).

- Strategic Focus: IBM's GRC strategy centers on AI-driven automation, deep BFSI vertical specialization, and hybrid cloud deployment supporting both on-premises and cloud configurations to serve European clients with data sovereignty requirements.

SAP SE

SAP SE is a German multinational software corporation headquartered in Walldorf, Baden-Württemberg. SAP offers ERP and GRC solutions embedded across the BFSI, manufacturing, retail, and public sector verticals in Germany, France, the UK, and the Nordics.

- Product & Platform Portfolio: SAP GRC Access Control, SAP Process Control, SAP Risk Management, SAP Sustainability Management.

- Recent Developments: In November 2025, SAP SE announced a new collaboration with France’s AI sector, which includes new and expanded partnerships with Bleu, Capgemini, and Mistral AI.

- Strategic Focus: SAP's GRC strategy leverages its dominant ERP installed base in European enterprises to cross-sell GRC and sustainability compliance modules, positioning itself as the default compliance backbone for SAP-centric organizations.

MetricStream

MetricStream is an independent GRC platform vendor headquartered in San Jose, California, with a dedicated European presence across the UK, Germany, and the Nordics. The company serves over 1,000 enterprise customers globally, with a significant concentration in the BFSI, healthcare, and energy verticals.

- Product & Platform Portfolio: MetricStream GRC Platform, M7 cloud-native suite, ESG & Sustainability Management, Third-Party Risk Management.

- Recent Developments: In September 2025, MetricStream announced that it had been named a Category Leader in Chartis Research’s Governance, Resilience, and Compliance Solutions 2025 report.

- Strategic Focus: MetricStream focuses on enterprise risk and audit management depth, cloud-native architecture leadership, and sector-specific compliance content libraries for financial services and healthcare verticals in Europe.

Market Concentration Analysis

The Europe Governance, Risk and Compliance Platform market exhibits moderate concentration among top enterprise vendors, with IBM Corporation, SAP SE, MetricStream, and ServiceNow collectively accounting for approximately 30-38% of regional market revenue in 2025. The market is characterized by a bifurcated structure: at the enterprise tier, consolidation is occurring as complex cloud and AI-integrated GRC architectures require substantial R&D investment that only the largest vendors can sustain. Simultaneously, the mid-market segment is fragmenting as no-code SaaS platforms like LogicGate and Risk Cloud enable rapid deployment for organizations with limited IT resources.

The accelerating convergence of GRC with cybersecurity risk management and ESG reporting is blurring traditional vendor categories, drawing competition from security information vendors and sustainability data platforms (Workiva, Persefoni) into the GRC perimeter. This multi-directional competitive pressure is reshaping market boundaries and creating consolidation opportunities throughout 2026-2028.

Investment & Growth Opportunities

Fastest-Growing Segments

AI-powered GRC risk management is the fastest-growing sub-segment (~11% CAGR to 2034), driven by demand for predictive compliance analytics and automated regulatory updates. Cloud-based GRC platforms (~10% CAGR) are expanding rapidly due to hybrid work models and rising SME compliance needs under NIS2 and CSRD. Third-party risk management (TPRM) is the fastest-growing module, supported by DORA-driven ICT vendor oversight requirements.

Emerging Market Expansion

Mid-market adoption across Southern and Eastern Europe is accelerating as NIS2 extends compliance obligations to a broader base of enterprises. ESG compliance is the most significant new growth area, with CSRD driving demand for GRC-linked data management and reporting across ~50,000 European companies through 2026–2028.

Venture & Private Investment Trends

Investment in Europe’s GRC platforms is rising, supported by strong compliance-driven demand and consolidation potential. Key deals include acquisitions and investments by Clearlake Capital, Insight Partners, and Thoma Bravo. European RegTech firms raised approximately USD 724 million in 2024, with investment concentrated in the UK, France, and Germany. Despite a slowdown in deal activity, investor focus remains on AI-driven compliance and financial crime solutions, while broader fintech and cybersecurity convergence continues to support M&A activity across the GRC ecosystem.

Future Market Outlook (2026-2034)

The Europe Governance, Risk and Compliance Platform market forecast projects steady value expansion from USD 15.85 Billion in 2025 to USD 28.02 Billion by 2034 at a CAGR of 6.34%, underpinned by regulatory intensification, digital transformation, and the integration of AI-driven automation across compliance and risk management functions. Three structural forces will shape the market through 2034. First, the EU regulatory pipeline - including the AI Act, Cyber Resilience Act, and CSRD second-wave expansion - will continuously expand the addressable compliance scope for GRC platforms. Second, the convergence of cybersecurity and GRC will drive platform consolidation, with unified risk intelligence platforms replacing standalone GRC, SIEM, and vulnerability management tools. Third, cloud-native SaaS penetration into the European SME segment will unlock the largest volume growth opportunity of the forecast period.

By 2034, the Europe Governance, Risk, and Compliance Platform market is forecast to have completed its transition from compliance-centric tooling to strategic risk intelligence infrastructure. AI-native platforms offering continuous monitoring, predictive non-compliance alerts, and automated regulatory change management will define the competitive frontier. Organizations treating governance, risk, and compliance platforms as strategic decision-support assets - rather than reactive compliance systems - will achieve measurable operational resilience advantages in an increasingly complex regulatory and threat environment.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with European governance, risk, and compliance market stakeholders, including compliance and risk management directors at BFSI organizations, platform product managers, system integrator engagement leads, and enterprise risk consultants. Primary insights validated market sizing, segmentation estimates, vendor positioning, and regulatory impact assessments across key European markets.

Secondary Research

Secondary sources include European Commission legislative documents (GDPR, DORA, NIS2, CSRD), EBA and BaFin regulatory publications, SecurityScorecard European Cyber Risk Report (2024), IMARC Group internal databases, Gartner Magic Quadrant for IT Risk Management, company annual reports and investor presentations, and trade publications including GRC World Forums, Compliance Week Europe, and Risk.net.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, regulatory adoption indices, enterprise technology spending trends, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty and regulatory timeline variability.

Europe Governance, Risk and Compliance Platform Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Deployment Models Covered | On-Premises, Cloud |

| Solutions Covered | Audit Management, Risk Management, Policy Management, Compliance Management, Others |

| Components Covered | Software, Services |

| Services Covered | Integration, Consulting, Support |

| End Users Covered | Small Enterprise, Medium Enterprise, Large Enterprise |

| Verticals Covered | BFSI, Construction and Engineering, Energy and Utilities, Government, Healthcare, Manufacturing, Retail and Consumer Goods, Telecom and IT, Transportation and Logistics, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | IBM Corporation, SAP SE, MetricStream, ServiceNow, STG Partners, LLC, Diligent Corporation, LogicGate, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe governance, risk and compliance platform market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe governance, risk and compliance platform market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe governance, risk, and compliance platform industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Governance, Risk and Compliance Platform Market Report

The Europe governance, risk, and compliance platform market was valued at USD 15.85 Billion in 2025, driven by escalating regulatory complexity and rising cybersecurity risk.

The market is projected to reach USD 28.02 Billion by 2034, growing at a CAGR of 6.34% during 2026-2034, driven by DORA, NIS2, CSRD mandates, and cloud-based platform adoption.

On-Premises deployment leads with a 55.8% share in 2025, driven by data sovereignty requirements, security control preferences, and legacy system integration needs among regulated enterprises.

Software leads with a 60.9% share in 2025, driven by demand for AI-powered risk scoring, automated compliance calendars, and real-time regulatory dashboards.

Germany leads with a 28.4% share in 2025, driven by its position as Europe's largest economy, the BaFin regulatory framework, and strong industrial and financial services GRC adoption.

Key drivers include GDPR, DORA, and NIS2 compliance requirements, a 25% rise in European cyber breaches in 2024, cloud digital transformation adoption, and CSRD-driven ESG reporting obligations.

Leading companies include IBM Corporation, SAP SE, MetricStream, ServiceNow, STG Partners, LLC, Diligent Corporation, LogicGate, Inc., and others.

Cloud-based GRC is the fastest-growing deployment model at ~9.8% CAGR through 2034, while AI-powered risk management is the fastest-growing functional sub-segment at ~11.2% CAGR.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)