Europe Laboratory Automation Market Size, Share, Trends, and Forecast by Type, Equipment and Software Type, End User, and Country, 2026-2034

Europe Laboratory Automation Market Size and Share:

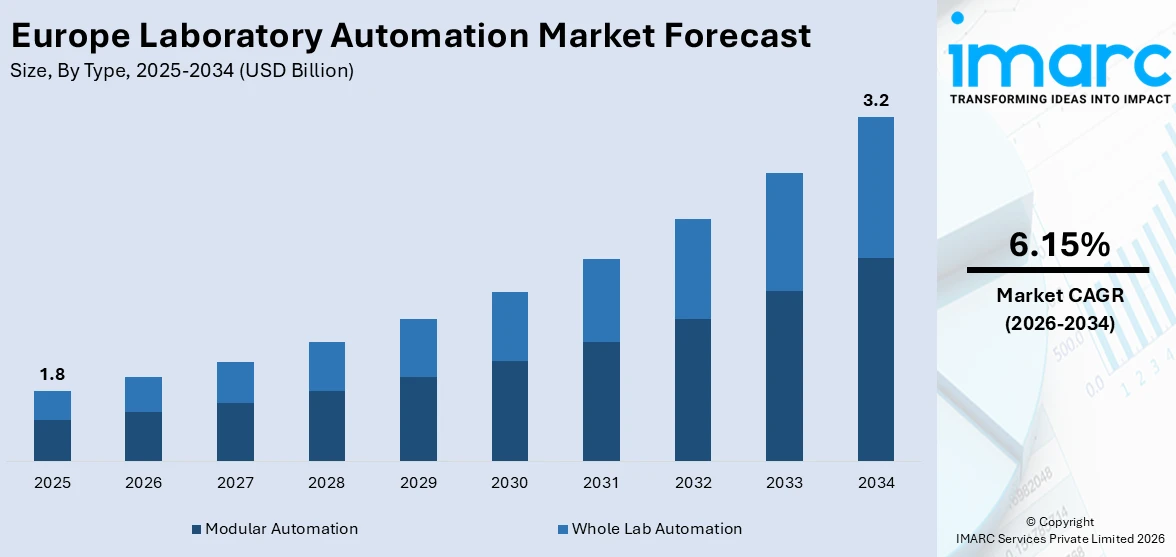

The Europe laboratory automation market size was valued at USD 1.8 Billion in 2025. Looking forward, the market is expected to reach USD 3.2 Billion by 2034, exhibiting a CAGR of 6.15% during 2026-2034. Germany currently dominates the market, holding a significant market share in 2025. The market is fueled by the growing need for precise, high-throughput diagnostics, increased healthcare expenditure, and the lack of experienced laboratory professionals. High emphasis on innovation, digitalization, and cross-border collaboration in the region also fuels the use of sophisticated automation technologies. Regulatory emphasis on quality control and data integrity further accelerates implementation, collectively contributing to the steady expansion of the Europe laboratory automation market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1.8 Billion |

|

Market Forecast in 2034

|

USD 3.2 Billion |

| Market Growth Rate 2026-2034 | 6.15% |

One of the primary drivers of the laboratory automation market in Europe is the growing emphasis on precision, consistency, and operational efficiency in clinical diagnostics. Healthcare networks throughout the region are more concerned than ever with reducing diagnostic mistakes and enhancing sample throughput. Automation technologies like robotic arms, automated sample handlers, and lab information systems are becoming more prevalent in hospitals and diagnostic labs to meet these demands. Moreover, the rise in chronic illnesses and the aging population, particularly in Western Europe, has intensified demand for faster and more accurate diagnostic services. European countries are also facing a deficit of skilled laboratory technicians, contributing even further to the momentum of automation as a method to uphold standards without adding to the workload of humans. Additionally, strict regulatory environments for clinical diagnostics in nations such as Germany and France compel labs to implement high-end technologies that minimize human mistakes and enhance traceability along the test process, which further contributes to the Europe laboratory automation market growth and development as well.

To get more information on this market Request Sample

Europe's heavy focus on scientific research and cross-border cooperation is a major driver of laboratory automation development. The continent contains some of the world's research-intensive economies, such as Germany, the Netherlands, and Sweden, that are continually investing in upgrading laboratory facilities. Most European universities and research institutions cooperate across borders, necessitating standard laboratory workflows and data handling systems that can be meaningfully accomplished only through automation. In addition, the EU's investment in digital transformation as well as financing support toward innovation in life sciences has resulted in an increase in the deployment of advanced lab automation solutions, especially in the pharmaceutical research and genomics sectors. This climate supports the incorporation of AI-based automation tools and intelligent systems able to perform complicated laboratory operations with little intervention. Besides, the emphasis on sustainability and green laboratory operation in Europe propels demand for automation systems that conserve energy, cut chemical consumption, and save reagent usage in research and clinical use.

Europe Laboratory Automation Market Trends:

Demand for Automated Hematology and Coagulation Systems in the Healthcare Sector

One of the most significant trends influencing the Europe laboratory automation market is the increasing use of automated hematology and coagulation diagnosis systems within the healthcare sector. Hospitals and diagnostic laboratories throughout the region are turning to integrated analyzers and high-end reagents to improve diagnostic accuracy and lower turnaround times. Accordingly, in July 2025, Dreampath Diagnostics secured investment from Summit Partners to scale its digital pathology solutions. The company, which manages over 250 million samples globally, aims to enhance lab efficiency, traceability, and diagnostic accuracy. Automated systems provide the capability for quicker testing, along with standardization and consistency in results, which is essential for conditions like anemia, clotting abnormalities, and chronic diseases. Additionally, European healthcare organizations are increasingly deploying cloud-based information systems to better manage laboratory data. These systems provide real-time access to test results, facilitate interdepartmental collaboration, and assist in more informed clinical decision-making. Germany, France, and the Netherlands are at the forefront of deploying digital lab solutions, driven by the requirement for precision medicine as well as the driving force for digitization within national healthcare systems. This transformation is one of the defining Europe laboratory automation market trends.

Technological Breakthroughs in Biotechnology and Pharmaceutical Sectors

Well-developed biotechnology and pharmaceutical sectors of Europe are key drivers of the laboratory automation market. EFPIA research indicates that EU pharmaceutical R&D spending rose from EUR 27.8 Billion in 2010 to EUR 46.2 Billion in 2022, increasing at an average annual rate of 4.4% over the 12 years. Several European nations have state-of-the-art research institutions and multinational pharmaceutical companies that make extensive use of automation to streamline research processes, accelerate drug discovery, and meet strict regulatory requirements. Automated systems are being used more and more in sectors like cell culture, high-throughput screening, and sample preparation, enabling scientists to carry out sophisticated experiments with greater accuracy and repeatability. This can be seen most prominently in innovation hotspots like Switzerland, the UK, and Germany, where public and private investments enable the incorporation of intelligent automation tools. Also, automation allows for quicker scaling of lab processes, critical for the production of biologics, vaccines, and tailored treatments. This increased dependence on automation is a true indication of an evident trend among European pharmaceutical and biotech companies in pursuit of staying competitive while upholding quality and safety standards, which further supports the growth of Europe laboratory automation market demand.

Overcoming Staffing Shortages through Lab Automation

One immediate concern facing laboratories throughout Europe is the increasing shortfall between increasing demand for diagnostic tests and the limited number of trained laboratory staff. Several countries face an aging workforce, combined with a lack of younger professionals entering the profession. This imbalance in the workforce has subjected laboratories to a need to sustain operation efficiency without degrading accuracy or throughput. Even while the shortage of competent labor is an issue of concern right now, reports indicate that the problem is much more widespread. In actuality, the clinical laboratory staffing deficit has persisted for more than thirty years, with an average vacancy rate of about 10%. In addition, demand increases in certain places have risen to 25%. Consequently, laboratory automation adoption has evolved into more than an amenity, as it has become a necessity. Automated systems are now being implemented to address the repetitive tasks of sample sorting, labeling, and data entry, freeing current staff to concentrate on more specialized tasks. In addition, automation eliminates human error and saves time, which allows for greater volumes of tests to be conducted with fewer personnel. Nations like Italy, Spain, and the Nordic countries have started initiating government and institutional strategies to automate laboratory operations by modernizing them. This reflects the way manpower problems are hastening the adoption of technology in the Europe laboratory automation market outlook.

.webp)

Europe Laboratory Automation Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Europe laboratory automation market, along with forecasts at the regional and country levels from 2026-2034. The market has been categorized based on type, equipment and software type, and end user.

Analysis by Type:

- Modular Automation

- Whole Lab Automation

Modular automation stands as the largest component in 2025. Modular automation is becoming the front-runner category segmentation in the Europe laboratory automation market because it is flexible, scalable, and highly adaptable to varying laboratory settings. Modular solutions differ from fixed automation systems in that laboratories can customize and scale systems according to certain workflow requirements and financial limitations. This is especially useful for clinical labs and research facilities which often change processes due to shifting test needs or changing research goals. Laboratories in Europe, particularly in fields such as pharmaceuticals, diagnostics, and biotechnology, are increasingly adopting modular configurations to incorporate new equipment and automate single steps like sample prep, data analysis, and liquid handling. The plug-and-play design of modular automation also facilitates quicker implementation and maintenance, rendering it suitable for small laboratories and larger institutions alike. With increasing demand for tailormade laboratory systems that can be upgraded with advancing technology, modular automation remains at the top of adoption rates in Europe.

Analysis by Equipment and Software Type:

- Automated Clinical Laboratory Systems

- Workstations

- LIMS (Laboratory Information Management Systems)

- Sample Transport Systems

- Specimen Handling Systems

- Storage Retrieval Systems

- Automated Drug Discovery Laboratory Systems

- Plate Readers

- Automated Liquid Handling Systems

- LIMS (Laboratory Information Management Systems)

- Robotic Systems

- Storage Retrieval Systems

- Dissolution Testing Systems

Automated clinical laboratory systems stand as the largest component in 2025. Automated clinical laboratory systems are the dominant equipment and software type segment according to the Europe laboratory automation market forecast, due to the region's growing emphasis on accuracy diagnostics and operational efficiency in the healthcare sector. These systems combine sample handling, analysis, data handling, and reporting within a single workflow, delivering drastic levels of manual intervention and turnaround times. European hospitals and diagnostic centers are deploying these systems to process high test volumes, enhance accuracy, and keep pace with stringent regulatory requirements. The extensive usage of automated clinical laboratory systems in hematology, immunoassay, and microbiology further strengthens their supremacy. The integration of software platforms supporting real-time tracking of data, remote access, and laboratory information systems further supports better decision-making and departmental coordination. Germany, France, and the UK are among the top adopters from countries, driven by a larger trend toward digital and fully automated clinical laboratories on the continent. This trend is continuing to drive market growth.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Biotechnology and Pharmaceutical Companies

- Hospitals and Diagnostic Laboratories

- Research and Academic Institutes

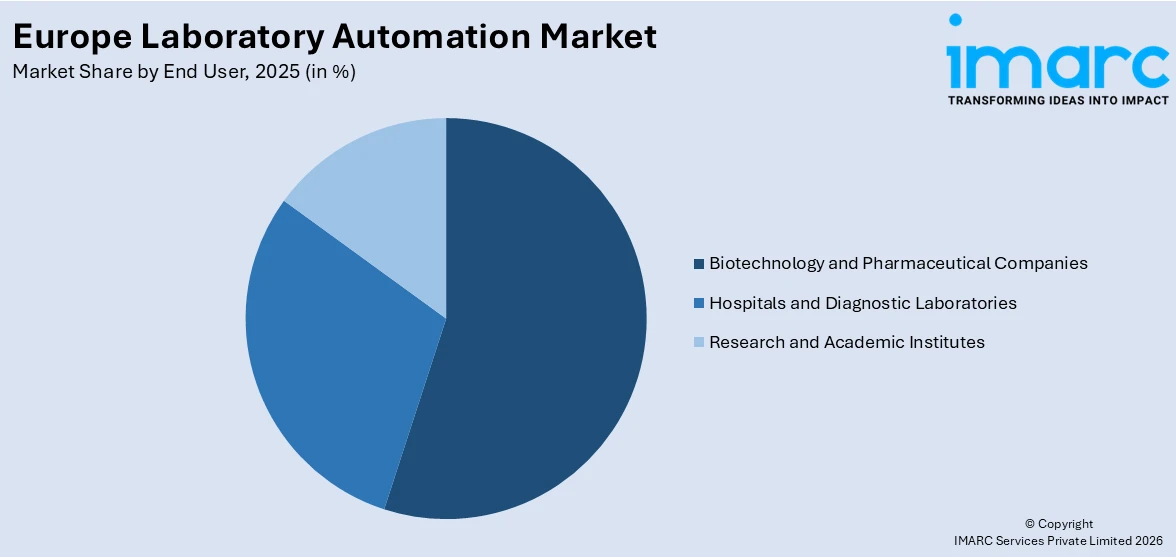

Biotechnology and pharmaceutical companies lead the market share in 2025. The biotech and pharmaceutical industries are the dominant end-user segment as per the Europe laboratory automation market analysis, driven by their ongoing need for high-throughput, accurate, and scalable lab workflows. These firms extensively depend upon automation to speed up drug discovery, intensify clinical trials, and abide by regulatory guidelines. Automated systems allow for reproducibility, uniform sample handling, and data integrity, which are key considerations for pharmaceutical R&D. Europe's robust pharmaceutical innovation base, and especially in nations such as Germany, Switzerland, and the Netherlands, fuels continued investment in sophisticated lab automation equipment. In addition, the region's increasing emphasis on biologics, vaccines, and personalized medicine requires the incorporation of module and smart automation systems that can evolve with intricate protocols. Lab automation enhances productivity while minimizing the chance of human error, enabling pharmaceutical businesses to comply with regulatory as well as commercial timelines effectively. Consequently, this segment remains a major motivator for technology adoption and market growth in the region.

Country Analysis:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

In 2025, Germany accounted for the largest market share. Germany is the dominant regional segmentation of the Europe laboratory automation market due to its sophisticated healthcare infrastructure, robust pharmaceutical and biotechnology sectors, and emphasis on innovation. The nation has many world-class research organizations, diagnostic labs, and pharmaceutical firms that continuously invest in upgrading laboratory functions. German labs are the first to adopt new technologies, such as robotic systems, automated analyzers, and laboratory information systems. Furthermore, initiatives by government and industry for digital health transformation and intelligent manufacturing also lead to more adoption of automation solutions. The focus on precision, efficiency, and observance of strict regulatory requirements in Germany also complements the functionalities of laboratory automation systems. Furthermore, it also has an aging population and increasing healthcare needs, which also lead to more dependency on automation to sustain service quality despite workforce constraints. With its strong infrastructure, talented labor force, and ongoing innovation, Germany leads the way in European laboratory automation adoption and regional market dominance.

Competitive Landscape:

Major players in the Europe laboratory automation market are making several strategic initiatives to drive innovation faster, increase market reach, and address increasing demands for streamlined laboratory workflows. Top players are investing substantially in research and development for developing sophisticated, intuitive automation systems that are specific to clinical as well as research laboratories. These initiatives involve the creation of modular platforms, artificial intelligence-based data analysis software, and end-to-end integrated solutions supporting sample processing, diagnostics, and data management. Moreover, collaborations and partnerships with healthcare providers, academic institutions, and biotech companies are helping businesses map product development with industry-specific needs. Several of the players are also looking to increase their regional presence by setting up committed service centers and distribution networks in major European nations like Germany, France, and the UK. Additionally, to bridge the skills gap and facilitate easier adoption, firms are providing integrated training initiatives and digital interfaces that make it easy to operate. Efforts also being undertaken to meet Europe's stringent regulatory requirements by embedding traceability, quality assurance, and cybersecurity elements into automation solutions. Sustainability is another area of emphasis, with companies developing energy-efficient systems and environmentally friendly consumables. Overall, these efforts are consolidating the competitive environment and fueling sustained growth in the Europe laboratory automation market.

The report provides a comprehensive analysis of the competitive landscape in the Europe laboratory automation market with detailed profiles of all major companies.

Latest News and Developments:

- July 2025: BioMed X and Servier launched Europe’s first XSeed Labs at the Spartners incubator in Paris-Saclay. The initiative will develop an AI-powered platform for designing bispecific antibodies, combining academic talent and pharma infrastructure to accelerate oncology innovation through sterically guided antibody engineering and predictive modeling.

- May 2025: MGI Tech unveiled its PrepALL liquid handling system and upgraded Smart8 at SLAS Europe in Germany. Featuring AI integration, modular design, and high-precision pipetting, the new automation tools aim to enhance lab workflows in genomics, diagnostics, and synthetic biology, offering scalable, affordable solutions for global research needs.

- April 2025: QIAGEN declared its intention to introduce three new sample preparation tools - QIAsymphony Connect (2025), QIAsprint Connect, and QIAmini (2026). These systems aim to enhance lab automation across high- and low-throughput workflows, offering improved efficiency, digital connectivity, and sustainability for diverse applications in genomics, oncology, and molecular diagnostics.

- March 2025: Covestro launched a fully automated lab in Europe to develop coating and adhesive formulations. Operating 24/7, it uses AI and robotics to run tens of thousands of tests annually, accelerating sustainable research and development (R&D), supporting circular material innovation, and enabling rapid, data-driven customization across key European industrial sectors.

- January 2025: ABB Robotics and Agilent Technologies announced a collaboration to develop automated laboratory solutions. By integrating ABB’s robotics with Agilent’s analytical instruments and software, the partnership aims to streamline laboratory workflows, enhance precision, and augment productivity across various sectors, including pharmaceuticals, biotechnology, energy, and the food and beverage industry.

Europe Laboratory Automation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Modular Automation, Whole Lab Automation |

| Equipment and Software Types Covered |

|

| End Users Covered | Biotechnology and Pharmaceutical Companies, Hospitals and Diagnostic Laboratories, Research and Academic Institutes |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe laboratory automation market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe laboratory automation market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe laboratory automation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Laboratory Automation Market Report

The Europe laboratory automation market was valued at USD 1.8 Billion in 2025.

The Europe laboratory automation market is projected to exhibit a CAGR of 6.15% during 2026-2034, reaching a value of USD 3.2 Billion by 2034.

The Europe laboratory automation market is driven by increasing demand for high-throughput diagnostics, rising healthcare digitization, skilled workforce shortages, and the growing need for accuracy and efficiency in laboratories. Advancements in biotechnology and strong governmental support for research and innovation further contribute to the market’s sustained momentum across the region.

Germany accounts for the largest share in the Europe laboratory automation market, driven by advanced healthcare infrastructure, strong pharmaceutical and biotechnology sector, and high adoption of precision diagnostic technologies. The country’s focus on digital transformation, regulatory compliance, and addressing skilled labor shortages further accelerates the demand for automated solutions across clinical, research, and industrial laboratory settings.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade