Europe Luxury Yacht Market Size, Share, Trends and Forecast by Type, Size, Material, Application, and Country, 2026-2034

Europe Luxury Yacht Market Size, Share, Trends & Forecast (2026-2034)

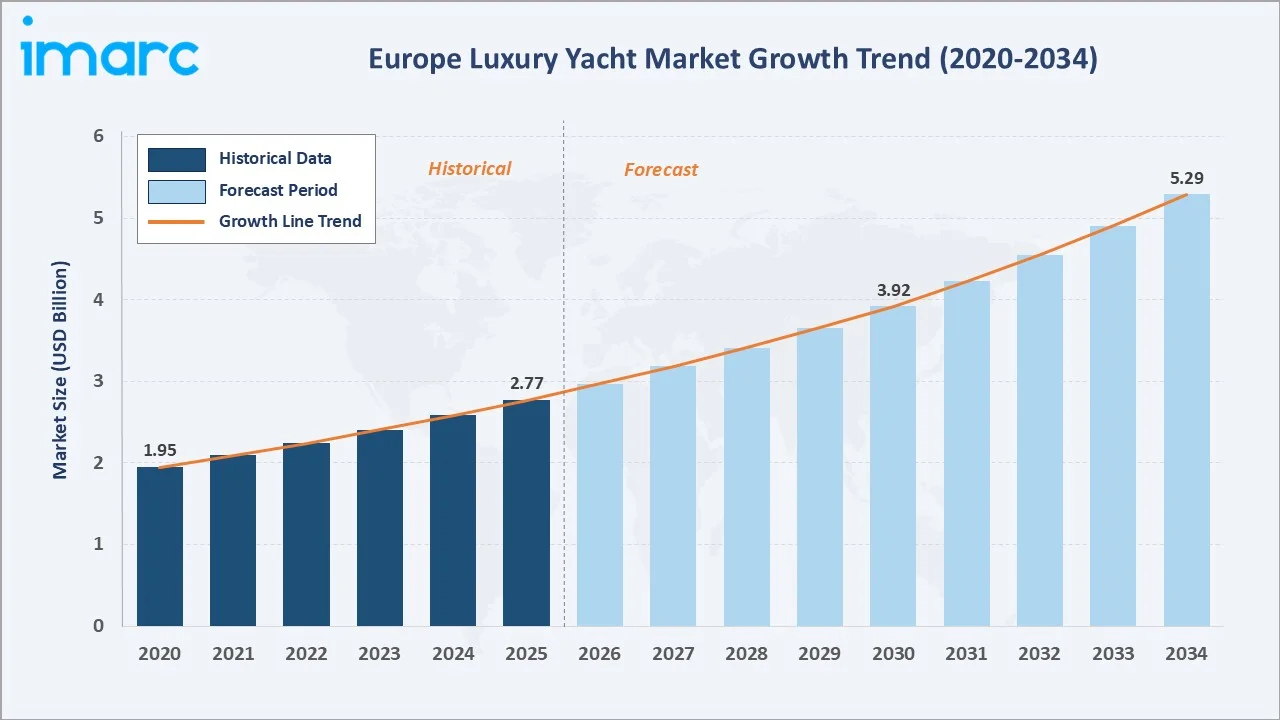

The Europe luxury yacht market reached USD 2.77 Billion in 2025 and is projected to reach USD 5.29 Billion by 2034, exhibiting a CAGR of 7.25% during 2026-2034. Growth is anchored by Italy's premier shipbuilding cluster, Northern European custom yards in Germany and the Netherlands, an expanding base of European and international HNWIs and UHNWIs, hybrid-electric propulsion adoption, and the Mediterranean's position as the global epicenter of luxury yacht charter and ownership.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.77 Billion |

|

Market Forecast (2034) |

USD 5.29 Billion |

|

CAGR (2026-2034) |

7.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The Europe luxury yacht market is further driven by the region’s strong maritime heritage, high concentration of affluent consumers, and well-developed coastal tourism infrastructure across destinations such as Italy, France, Spain, Greece, Croatia, and Monaco.

To get more information on this market, Request Sample

Rising demand for personalized leisure experiences, premium marine craftsmanship, and exclusive charter services is supporting the growth of luxury yachts across both private ownership and rental models. The presence of established shipyards, advanced design studios, and high-end marina facilities further strengthens Europe’s position as a key hub for luxury yacht manufacturing, sales, and operations.

Executive Summary

Europe accounts for the largest share of global luxury yacht production, with more than 40% of the world's superyachts built in shipyards across Italy, Germany, and the Netherlands. The market is structurally fragmented at the volume tier and highly concentrated at the bespoke superyacht tier, with Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, and Feadship collectively shaping competitive intensity across the 24-metre to 130-metre length range.

According to Knight Frank’s Wealth Report 2026, Europe’s ultra-high-net-worth individual population, defined as people with at least USD 30 million (EUR 25.7 million) in wealth, increased by 26% over the past five years, adding 37,428 new members between 2021 and 2026. Along with that, rising marine tourism and the European blue economy collectively underpin sustained demand through 2034.

The 2025 Monaco Yacht Show showcased over 120 superyachts ranging from 24 to over 110 meters. Industry consolidation continues alongside accelerated investment in hybrid propulsion, hydrogen fuel cells, and lightweight composites. Feadship's 118.8-metre Breakthrough, the world's first hydrogen fuel cell superyacht, was sold in September 2025, signaling that alternative propulsion has moved from concept to contracted delivery.

Key Market Insights

|

Indicator |

Value (2025) |

|

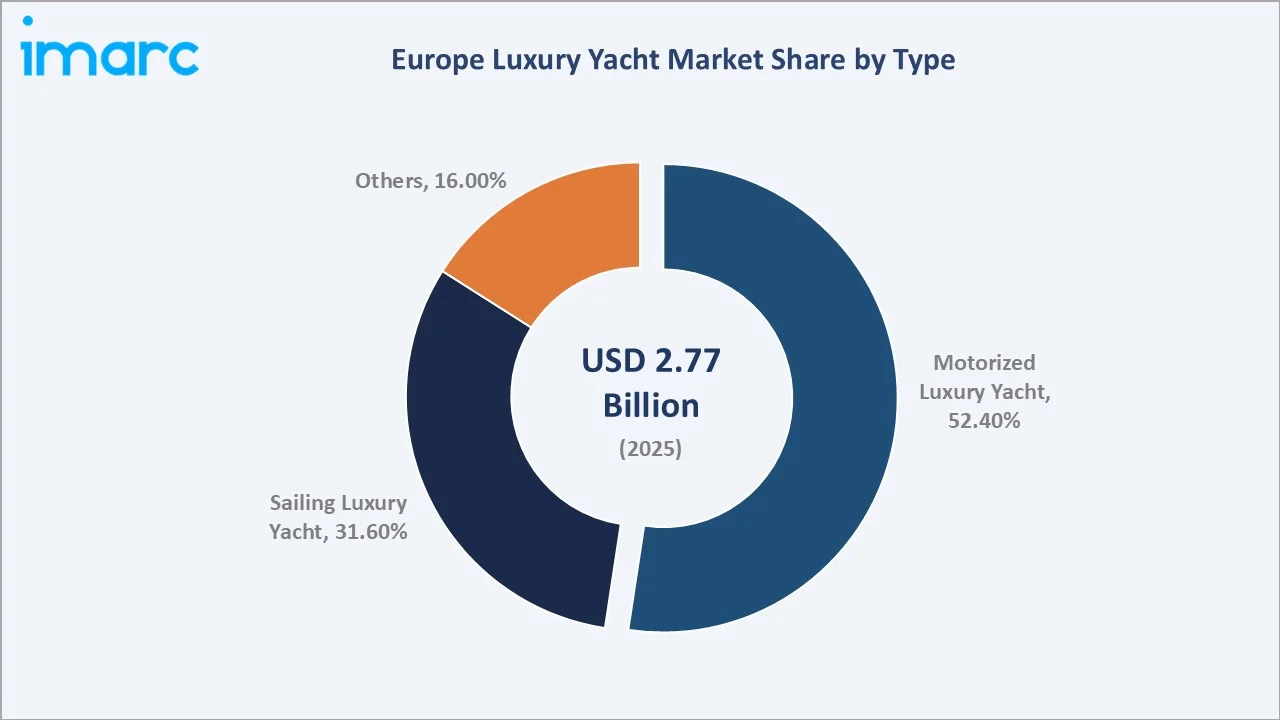

Leading Type |

Motorized Luxury Yacht (52.4%) |

|

Fastest-Growing Type |

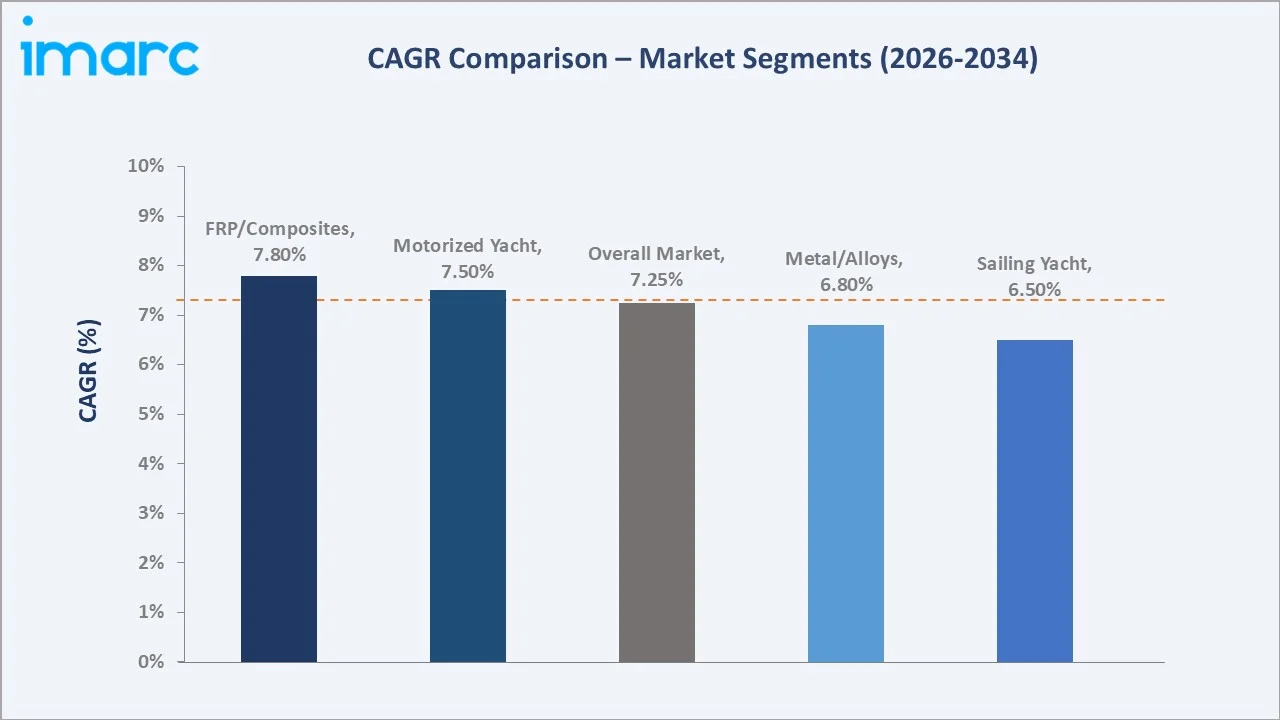

Motorized Luxury Yacht (7.80% CAGR) |

|

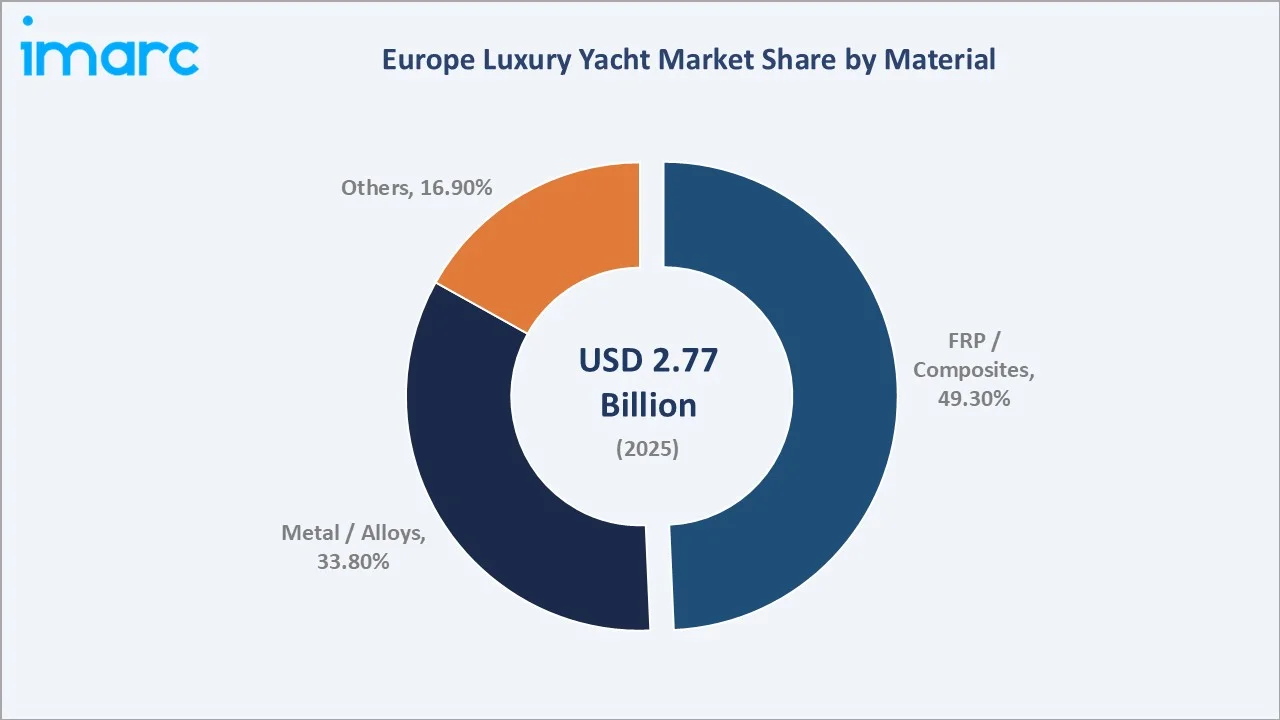

Leading Material |

FRP/ Composites (49.3%) |

|

Fastest-Growing Material |

FRP/Composites (7.80% CAGR) |

|

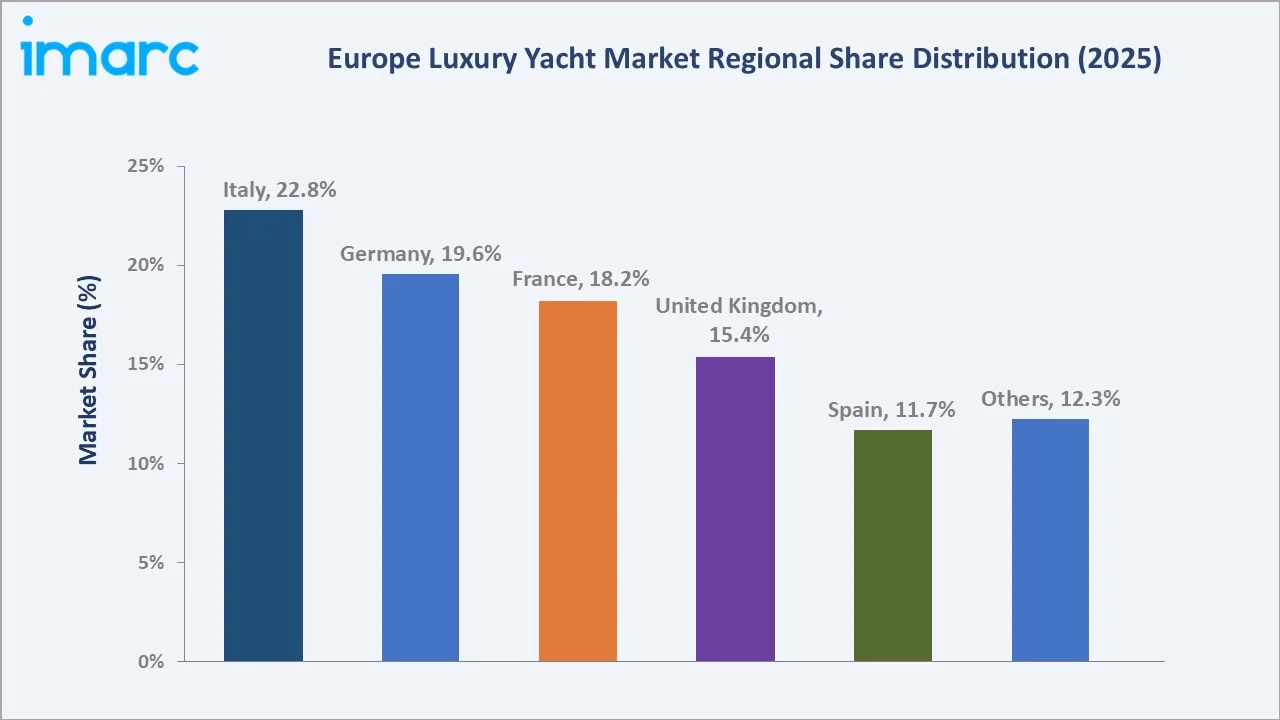

Largest Country |

Italy (22.8%) |

|

Key Players |

Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, and Feadship |

Key Analytical Observations Supporting the Above Data:

- Motorized luxury yachts account for 52.4% of the Europe market in 2025, reflecting buyer preference for higher cruising speed, larger interior volume, and superior amenity integration across the 24-metre to 130-metre fleet, with Azimut Benetti S.p.A., Sanlorenzo S.p.A, and Ferretti Group anchoring the segment.

- Sailing luxury yachts at 31.6% retain a structural base in Mediterranean owners and the bespoke superyacht charter market, supported by builders such as Perini Navi and Royal Huisman delivering 40-metre-plus sailing flagships including the 61.4-metre Katana at Monaco 2025.

- FRP/composites at 49.3% dominate the material mix and are growing at approximately 7.80% CAGR through 2034, supported by lightweight strength, design flexibility, and lower lifecycle fuel burn that align with EU emissions priorities and Superyacht Eco Association (SEA) Index ratings.

- Metal/alloys at 33.8% remain the construction standard for 50-metre-plus expedition and full-custom megayachts where aluminum and steel hulls deliver transoceanic range, ice-class capability, and structural integrity prioritized by UHNWI buyers and Dutch and German yards.

- Italy's 22.8% share reflects its position as the world's largest luxury yacht production cluster, with Azimut Benetti S.p.A., Sanlorenzo S.p.A, and Ferretti Group delivering both serial and semi-custom platforms across the 24–100-metre spectrum from Viareggio, La Spezia, Forlì, and Livorno.

Europe Luxury Yacht Market Overview

A luxury yacht is a crewed sail- or motor-powered vessel of typically 24 meters or longer, manufactured from advanced materials including FRP/composites, carbon fiber, aluminum, and steel, and equipped with premium amenities such as on-board pools, spas, helipads, hybrid propulsion, advanced navigation suites, and bespoke interiors.

Europe's luxury yacht market spans motorized luxury yachts (planing, semi-displacement, displacement), sailing luxury yachts, explorer/expedition yachts, and emerging hybrid-electric platforms across 75–120 feet, 121–250 feet, and above 250 feet length categories.

Macroeconomic drivers include the structural expansion of European wealth (183,953 UHNWIs in 2026), the post-pandemic preference for private travel, and the EU Green Deal targeting climate neutrality by 2050.

Market Dynamics

To evaluate market opportunities, Request Sample

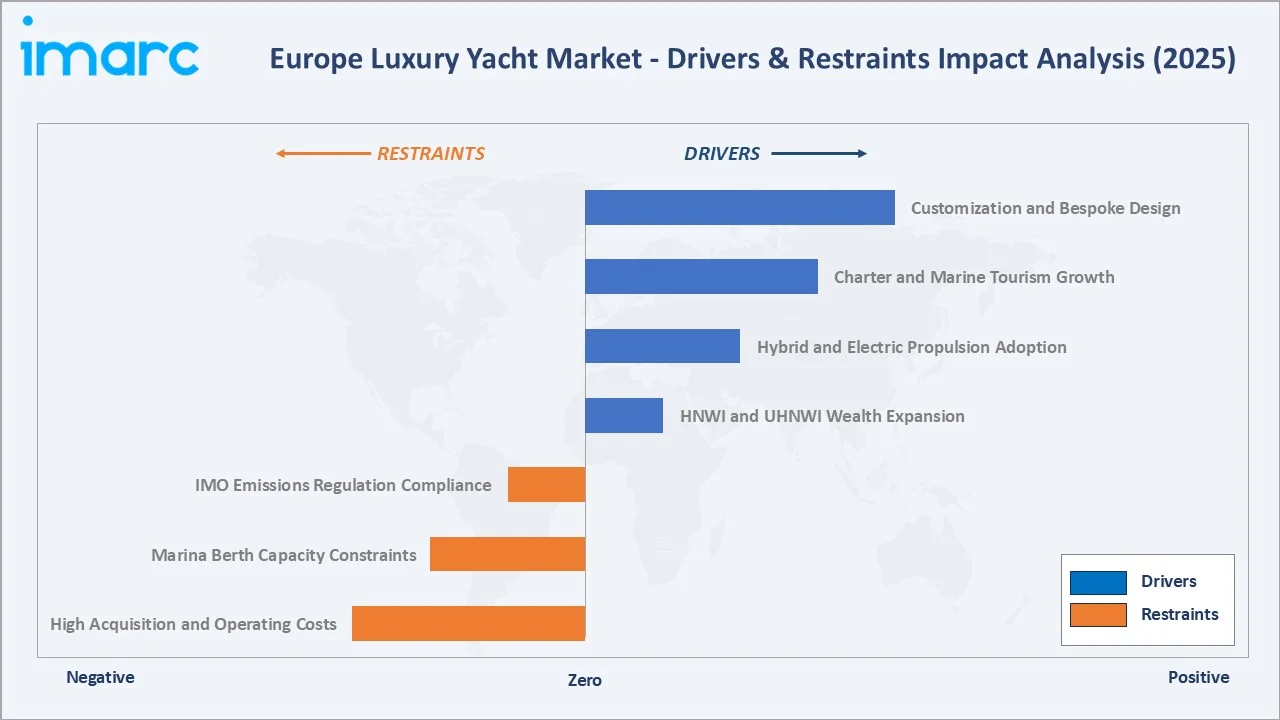

Market Drivers

- HNWI and UHNWI Wealth Expansion: According to Knight Frank’s Wealth Report 2026, there are more than 710,000 UHNWIs worldwide, with Europe accounting for 25.8%. Europe’s UHNWI population rose from 146,525 in 2021 to 183,953 in 2026, sustaining discretionary spending on luxury yachts as both status assets and lifestyle investments.

- Hybrid and Electric Propulsion Adoption: Builders are scaling hybrid diesel-electric, battery, and hydrogen fuel cell platforms. Feadship's 118.8-metre Breakthrough delivered the world's first hydrogen fuel cell superyacht; Feadship's 79.5-metre Valor combines hybrid diesel-electric, solar, and battery propulsion. Sanlorenzo's January 2024 Volvo Penta partnership accelerates marine decarbonization.

- Charter and Marine Tourism Growth: The Mediterranean basin, France, Italy, Spain, Greece, and Monaco, anchors global luxury yacht charter activity. Marina modernization programs across France, Spain, and Greece, and rising experiential travel spend among UHNWIs are translating into multi-use yachts designed for both private leisure and high-end charter.

- Customization and Bespoke Design: UHNWI buyers increasingly demand fully personalized interiors and exteriors. Sanlorenzo, Lürssen, Feadship, and Oceanco specialize in client-led design, with average build cycles of 24–48 months and high-margin order books extending beyond 2030 across the 50-metre-plus segment.

Market Restraints

- High Acquisition and Operating Costs: Entry-level yachts measuring 24–30 meters typically cost EUR 3–8 million, while mid-size yachts of 30–50 meters range from EUR 8–40 million. Large superyachts above 50 meters generally start at EUR 40 million and can exceed EUR 200 million for the most exclusive vessels. Annual operating costs typically equate to approximately 10% of build value, including berthing, crew, fuel, insurance, refit, and classification compliance.

- Marina Berth Capacity Constraints: Premium Mediterranean marinas operate near full capacity, with rising berthing fees and limited 80-metre-plus slots. Private equity capital is being deployed into marina expansion, but supply remains structurally tight against the growing 24-metre-plus active fleet.

- IMO Emissions Regulation Compliance: IMO greenhouse-gas targets aim to reduce the carbon intensity of international shipping by at least 40% compared with 2008 levels. While yachts represent a small share of marine emissions, the regulatory floor compels new investment in low-emission propulsion, with shore-power retrofit packages and certified hybrid systems becoming specification requirements in EU ports.

Market Opportunities

- Hybrid and Hydrogen Propulsion Retrofits: The European 24-metre-plus active fleet exceeds 5,000 yachts, creating a significant retrofit opportunity. Yards offering certified hybrid auxiliaries, shore-power packages, and modular battery integration are positioned to capture new-build and refit revenue concurrently.

- Explorer and Expedition Yachts: Demand for ice-class, long-range explorer yachts continues expanding, exemplified by Feadship Valor and Oceanco's 130-metre Project Y727. UHNWI owners are extending cruising grounds beyond the Mediterranean to polar regions, driving premium pricing and bespoke specification depth.

Market Challenges

- Skilled Labor Shortages in Shipyards: European yards face a tightening supply of master craftspeople (joinery, marine engineering, composite specialists), constraining capacity expansion at Italian and Dutch facilities and lengthening build cycles for new orders, particularly above 50 meters.

- Rising Insurance and Financing Costs: Boat International noted that yacht ownership costs extend far beyond the purchase price, with annual maintenance typically reaching 5–10% of the yacht’s original value and insurance costing around 0.5–2% of the vessel’s value.

Emerging Market Trends

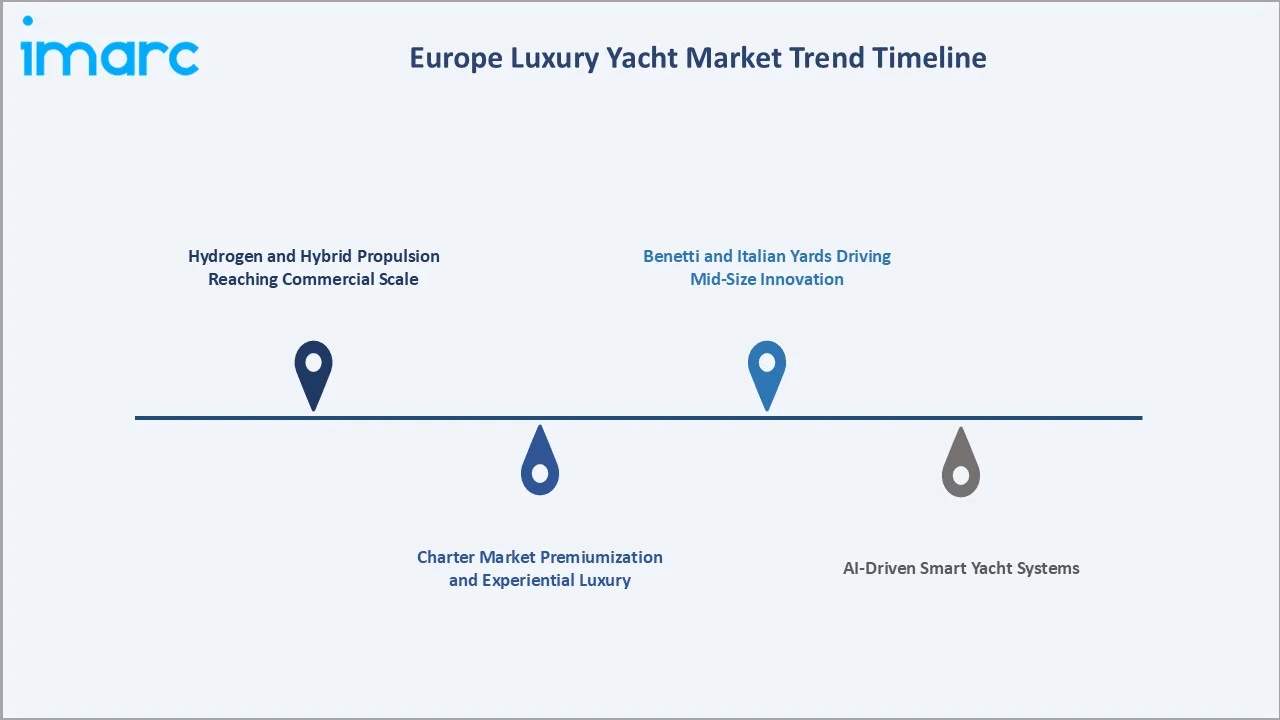

1. Hydrogen and Hybrid Propulsion Reaching Commercial Scale

Feadship's 118.8-metre Breakthrough, the world's first hydrogen fuel cell superyacht, was delivered and sold in 2025, validating fuel cells for large yacht propulsion. Feadship's 79.5-metre Valor, delivered in September 2025, combines hybrid diesel-electric, solar, and battery propulsion and earned the YCM Explorer Award for technological innovation.

2. Benetti and Italian Yards Driving Mid-Size Innovation

At the Monaco Yacht Show 2025, Benetti unveiled the B.Loft 58M and B.Now 52M, both designed to maximize volume and natural light. The B.Now 67M Lady Estey was delivered as the new flagship of the Oasis Deck line (September 2025), while Benetti also introduced the B.Neos concept in September 2025, emphasizing silent operation and informal living spaces.

3. AI-Driven Smart Yacht Systems

European builders are integrating AI-powered energy management, predictive maintenance, integrated bridge systems, and Starlink-based high-speed connectivity. Next Yacht Group unveiled the Next AI-Integrated System, described as the first local-first AI assistant for luxury yachts, debuting aboard the 33.7-meter AB 110 at the 2025 Fort Lauderdale International Boat Show.

4. Charter Market Premiumization and Experiential Luxury

Brokerage and charter activity at Monaco 2025 totaled USD 2.9 Billion in listed asking value across 70 yachts on sale (up from USD 2.3 Billion in 2024). Charter operators are introducing dynamic pricing, blockchain-secured contracts, and experiential itineraries spanning the Mediterranean, Caribbean, and Norwegian fjords, expanding addressable charter revenue per yacht.

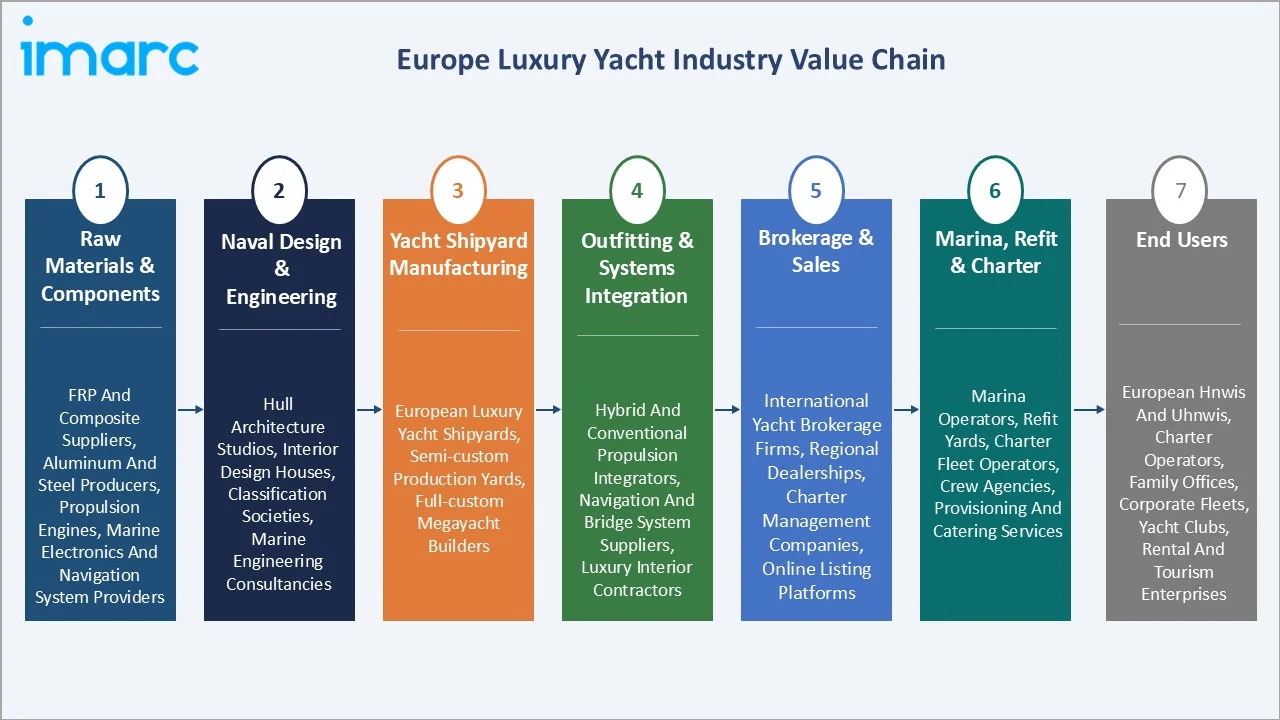

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

Raw Materials & Components |

FRP and composite suppliers, aluminum and steel producers, propulsion engines, marine electronics and navigation system providers |

|

Naval Design & Engineering |

Hull architecture studios, interior design houses, classification societies, marine engineering consultancies |

|

Yacht Shipyard Manufacturing |

European luxury yacht shipyards, semi-custom production yards, full-custom megayacht builders |

|

Outfitting & Systems Integration |

Hybrid and conventional propulsion integrators, navigation and bridge system suppliers, luxury interior contractors |

|

Brokerage & Sales |

International yacht brokerage firms, regional dealerships, charter management companies, online listing platforms |

|

Marina, Refit & Charter |

Marina operators, refit yards, charter fleet operators, crew agencies, provisioning and catering services |

|

End Users |

European HNWIs and UHNWIs, charter operators, family offices, corporate fleets, yacht clubs, rental and tourism enterprises |

Technology Landscape in the Europe Luxury Yacht Industry

Conventional Diesel-Electric and Displacement Hulls

Conventional twin-screw and triple-screw diesel platforms remain the dominant propulsion architecture across the 24–100-metre fleet. MAN, MTU, Caterpillar, and Volvo Penta engines pair with displacement and semi-displacement hulls engineered for transoceanic range and fuel efficiency aligned with EPA Tier III and IMO Tier III standards.

Hybrid Diesel-Electric and Battery Propulsion

Hybrid platforms now span the 40–120-metre range. Feadship's 79.5-metre Valor and Sanlorenzo's SX series demonstrate hybrid diesel-electric with substantial battery banks enabling silent zero-emission cruising in protected areas, validated by SEA Index and Yacht Environmental Transparency Index (YETI) ratings.

Hydrogen Fuel Cells and Alternative Fuels

Feadship's 118.8-metre Breakthrough demonstrates commercial hydrogen fuel cell propulsion in a superyacht. Other builders are evaluating methanol, biofuels, and ammonia for long-range applications. The IMO greenhouse-gas targets to reduce CO2 by at least 40% compared with 2008 levels are accelerating fleet-wide R&D in alternative fuels for next-generation builds.

Smart Yacht Systems and Connectivity

Integrated bridge systems, AI-powered energy management, predictive maintenance, and Starlink/VSAT high-speed connectivity are standard on new 40-metre-plus builds. Voice-activated control, IoT-enabled climate management, and remote diagnostics define modern luxury yacht user experience.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Motorized Luxury Yacht |

52.4% |

2025 |

|

Size |

🔒 |

🔒 |

2025 |

|

Material |

FRP/ Composites |

49.3% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Country |

Italy |

22.8% |

2025 |

By Type

Motorized luxury yachts dominate with a 52.4% share in 2025, supported by buyer preference for higher cruising speed, larger interior volume, and amenity-rich layouts across the planing, semi-displacement, and displacement categories. Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, and Feadship anchor this segment, with the 24-metre to 100-metre length range accounting for the majority of unit volume.

To access detailed market analysis, Request Sample

Sailing luxury yachts represent 31.6% of the market in 2025 and maintains a structural base in Mediterranean owners and the bespoke superyacht charter market. The 61.4-metre Perini Navi Katana led sailing yacht debuts at Monaco 2025, while Royal Huisman and Vitters continue to deliver 50–60-metre custom sailing flagships.

By Material

FRP/composites dominate the material mix with a 49.3% share in 2025 and are projected to grow at approximately 7.80% CAGR through 2034. Composite construction delivers lightweight strength, design flexibility, and lower lifecycle fuel burn, aligning with EU emissions priorities.

Metal/alloys account for 33.8% in 2025, with aluminum and steel hulls remaining the construction standard for 50-metre-plus expedition and full-custom megayachts where transoceanic range, ice-class capability, and structural integrity are prioritized. Dutch yards and German yards lead this category.

Regional Market Insights

Italy at 22.8% leads Europe's luxury yacht market, anchored by the world's densest shipbuilding cluster across Viareggio, La Spezia, Forli, Livorno, and Ancona. Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group collectively produce a substantial share of the world's 24-metre-plus yacht output.

Germany at 19.6% holds the second-largest share, anchored by Lürssen's leadership in 100-metre-plus bespoke megayachts. The German Federal Ministry for Economic Affairs cites Lürssen as a global leader in ultra-luxurious and technologically advanced superyachts.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Italy |

22.8% |

World's densest yacht-building cluster; concentration of leading semi-custom and bespoke shipyards; participation in major international yacht shows |

|

Germany |

19.6% |

Established custom shipyards along the northern coast; precision engineering and hybrid propulsion focus targeting UHNWI clientele |

|

France |

18.2% |

World-class charter destinations along the Mediterranean coast; well-developed marina infrastructure and superyacht refit yards |

|

United Kingdom |

15.4% |

Established production base for performance motor yachts; strong motor yacht heritage; export focus across European and global markets |

|

Spain |

11.7% |

Leading European refit hubs in the Mediterranean; growing charter activity in the Balearic Islands; rising marina capacity for superyachts across coastal cities |

|

Others |

12.3% |

Netherlands as a global hub for full-custom superyachts; Polish leadership in luxury catamaran manufacturing |

Spain at 11.7% has emerged as the leading European refit and Mediterranean charter hub owing to the Balearic nautical sector, which comprises more than 800 companies and generates over EUR 1.1 billion in annual turnover, while contributing 3.1% to Balearic GDP (according to the Balearic Marine Cluster).

Competitive Landscape

Europe's luxury yacht market exhibits moderate concentration. Leading players include Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, and Feadship.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Azimut Benetti S.p.A. |

Azimut, Benetti, Yachtique, Lusben |

Market Leader |

Broad portfolio spanning entry-level to mega-yachts; flagship semi-custom design innovation |

|

|

Sanlorenzo, Bluegame |

Market Leader |

Fully custom motor yacht expertise across multiple length categories; explorer yacht specialization |

|

Ferretti Group |

Ferretti Yachts, Pershing, Riva, Itama, Custom Line, Wally, CRN |

Market Leader |

Multi-brand portfolio spanning performance, classic, and lifestyle segments; hybrid propulsion integration across all brands |

|

Princess Yachts Limited |

Princess |

Strong Challenger |

UK-built flybridge, sports yacht, and motor yacht ranges; established performance motor yacht heritage |

|

Feadship |

Feadship |

Premium Leader |

Pioneer in custom superyacht construction; leadership in alternative propulsion and hybrid-electric platforms |

Volume yards such as Azimut Benetti S.p.A. and Ferretti Group leverage broad product portfolios and global dealer networks, while bespoke specialists such as Feadship dominate the 80-metre-plus full-custom segment.

Key Company Profiles

Azimut Benetti S.p.A.

Azimut Benetti S.p.A., headquartered in Avigliana, Italy, is one of the world’s largest privately held luxury yacht builders, operating multiple shipyards across Italy.

- Product Portfolio: Azimut Atlantis, Magellano, S, Flybridge, and Grande lines from 12 to 38 meters; Benetti B.Now (50/52/67M), B.Loft 58M, B.Neos, and full-custom 60–110-metre superyachts.

- Recent Developments: In September 2025, Azimut unveiled the Magellano 27M, a long-range Voyager yacht, with interiors by AMDL CIRCLE & Michele De Lucchi. The yacht features a 26.2-meter length, five cabins, a glazed main-deck loggia, and a design focused on exploration, comfort, and refined sea living.

- Strategic Focus: Volume leadership through Azimut; semi-custom and bespoke leadership through Benetti; Oasis Deck design innovation; hybrid propulsion integration; modular customization across product tiers.

Sanlorenzo S.p.A

Sanlorenzo S.p.A, headquartered in Ameglia, Italy, is a publicly listed Italian shipyard specializing in fully customized luxury motor yachts.

- Product Portfolio: SD displacement, SL planing, SX crossover, and SP performance lines from 24 to 73 meters; Bluegame BG and BGM crossover yacht ranges; full-custom 50-metre-plus superyacht series.

- Recent Developments: In April 2026, Sanlorenzo S.p.A opened its first London showroom in Mayfair, on Park Lane, strengthening its international footprint in a key luxury and cultural hub. The showroom serves as a private consultation space for Sanlorenzo and Bluegame clients, highlighting the company’s focus on design, craftsmanship, and personalized yachting experiences.

- Strategic Focus: Fully customized motor yacht builds; sustainability leadership; methanol fuel cell technology development; Asia-Pacific expansion through subsidiary network and global dealer presence.

Market Concentration Analysis

Europe's luxury yacht market is moderately concentrated. The top five players, Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, and Feadship, collectively hold a substantial share. The market is structurally bifurcated: volume yards leverage scale and dealer networks across the 24–50-metre segment, while bespoke yards dominate 50-metre-plus custom builds where technical complexity, reputation, and project management outweigh scale advantages.

Investment & Growth Opportunities

Fastest Growing Segments

- FRP/Composites and hybrid-electric motorized yachts represent the highest-growth segments through 2034, supported by EU emissions policy, lightweight performance advantages, and lower lifecycle fuel costs.

- Explorer and expedition yachts in the 50–80-metre range with ice-class capability are expanding cruising grounds beyond the Mediterranean and capturing premium pricing from UHNWI buyers.

Emerging Market Expansion

- Spain's refit and charter capacity is expanding rapidly, with MB92 Barcelona and Palma de Mallorca emerging as leading European refit hubs for 50-metre-plus superyachts.

- Poland is gaining traction in solar-electric luxury catamarans, while Mediterranean charter operators are extending itineraries into Greece, Croatia, and Türkiye.

Venture and Institutional Investment Trends

- Private equity capital is entering marina expansion to secure berth supply for the growing 24-metre-plus fleet across the Mediterranean and Northern Europe.

- Strategic partnerships such as Sanlorenzo–Volvo Penta (2024) and yard collaborations with hydrogen and battery integrators are accelerating sustainability investment cycles.

- Fractional ownership and yacht-as-a-Service models are emerging to broaden the addressable buyer base, with charter pools and timeshare structures unlocking new revenue streams for yards and operators.

Future Market Outlook (2026-2034)

Europe's luxury yacht market is positioned for sustained, sustainability-led expansion through 2034. From USD 2.77 Billion in 2025, the market is projected to reach USD 5.29 Billion by 2034, representing incremental value of USD 2.52 Billion at a 7.25% CAGR, increasingly composed of hybrid-electric platforms, hydrogen-ready megayachts, and AI-driven smart yacht systems.

The material mix is expected to shift toward composites and lightweight alloys, with FRP/composites growing from 49.3% toward 55% by 2034. Italy will retain manufacturing leadership while Germany and the Netherlands deepen their bespoke 80-metre-plus segment dominance. Hydrogen fuel cell superyachts, demonstrated by Feadship Breakthrough, will progress from pilot to small-series deployment by 2030.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, European shipyard executives, naval architects, brokers, charter operators, marina managers, and yacht owners, validating market sizing, segmentation, regional shares, and sustainability adoption trends.

Secondary Research

Secondary research covered Eurostat blue-economy statistics, European Boating Industry data, Monaco Yacht Show 2025 official figures, OEM annual reports, IMO emissions documentation, and industry publications including BOAT International, SuperYacht Times, YachtBuyer, and Robb Report.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating country-level yacht registrations, average build value by length category, propulsion and material mix, and shipyard order books. The 7.25% CAGR reflects validation against Eurostat HNWI data, European Boating Industry blue-economy estimates, and announced shipyard order pipelines.

Europe Luxury Yacht Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Sailing Luxury Yacht, Motorized Luxury Yacht, Others |

| Sizes Covered | 75-120 Feet, 121-250 Feet, Above 250 Feet |

| Materials Covered | FRP/ Composites, Metal/ Alloys, Others |

| Applications Covered | Commercial, Private |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, Feadship, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Luxury Yacht Market Report

The Europe luxury yacht market reached USD 2.77 Billion in 2025 and is projected to reach USD 5.29 Billion by 2034.

The market is expected to grow at a CAGR of 7.25% during 2026-2034, driven by HNWI/UHNWI wealth expansion, hybrid propulsion adoption, and Mediterranean charter growth.

Italy leads with a 22.8% share in 2025, anchored by the world's densest yacht-building cluster across Viareggio, La Spezia, Forlì, and Livorno.

Motorized luxury yachts dominate with a 52.4% share in 2025, reflecting buyer preference for higher speed, greater interior volume, and amenity-rich layouts.

FRP/composites hold 49.3% of the market, supported by lightweight strength, design flexibility, and lower lifecycle fuel burn.

Key players include Azimut Benetti S.p.A., Sanlorenzo S.p.A, Ferretti Group, Princess Yachts Limited, and Feadship.

FRP/composites are growing at approximately 7.80% CAGR through 2034 due to weight savings, lower emissions, design flexibility, and alignment with EU Green Deal and IMO emissions targets.

Key challenges include high acquisition and operating costs, marina berth capacity constraints, IMO emissions compliance, skilled labor shortages, and rising insurance and financing costs.

Hybrid and hydrogen propulsion retrofits, explorer/expedition yachts, sub-500 GT platforms, refit yards, and fractional ownership models represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)