Europe Mattress Market Size, Share, Trends and Forecast by Product, Distribution Channel, Size, Application, and Country, 2026-2034

Europe Mattress Market Size, Share, Trends & Forecast (2026-2034)

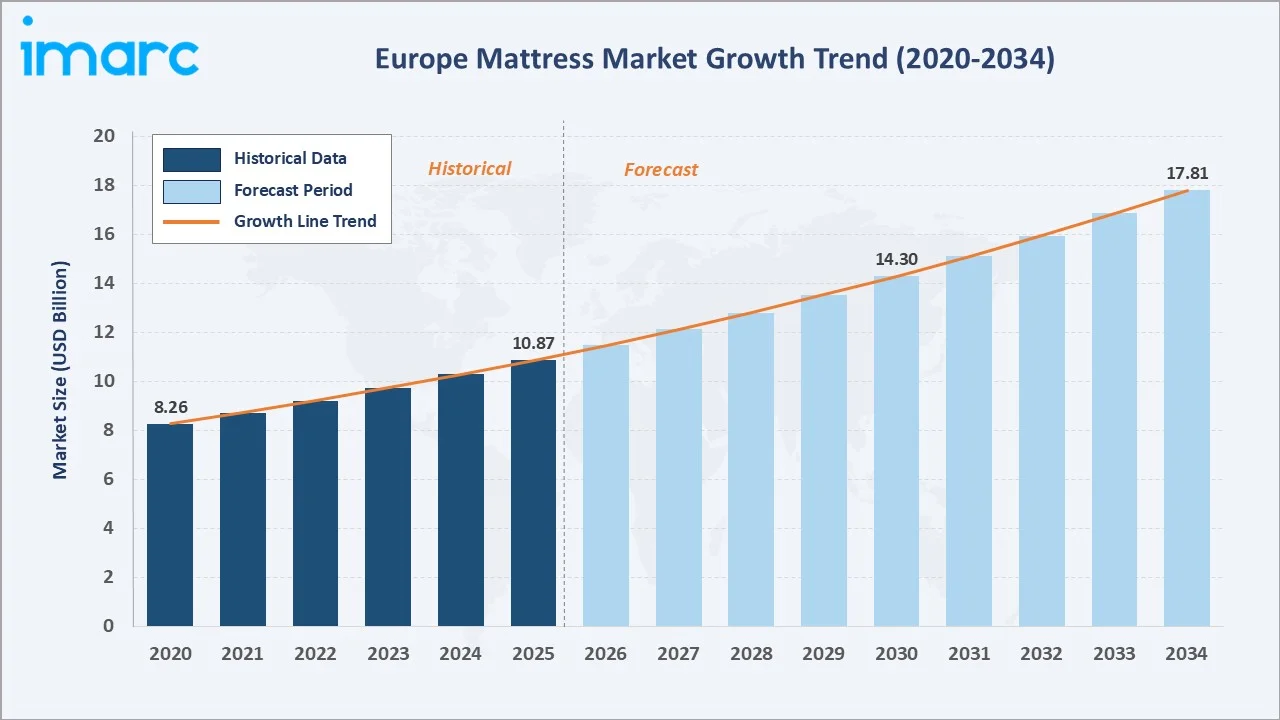

The Europe mattress market reached USD 10.87 Billion in 2025 and is projected to reach USD 17.81 Billion by 2034, growing at a CAGR of 5.64% during 2026 to 2034. Rising consumer awareness of sleep health and its impact on physical and mental well-being, the accelerating penetration of direct-to-consumer online mattress brands, and robust residential construction and renovation activity across key European markets are the primary forces driving consistent and sustained market expansion throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 10.87 Billion |

|

Market Size (2034) |

USD 17.81 Billion |

|

CAGR (2026-2034) |

5.64% |

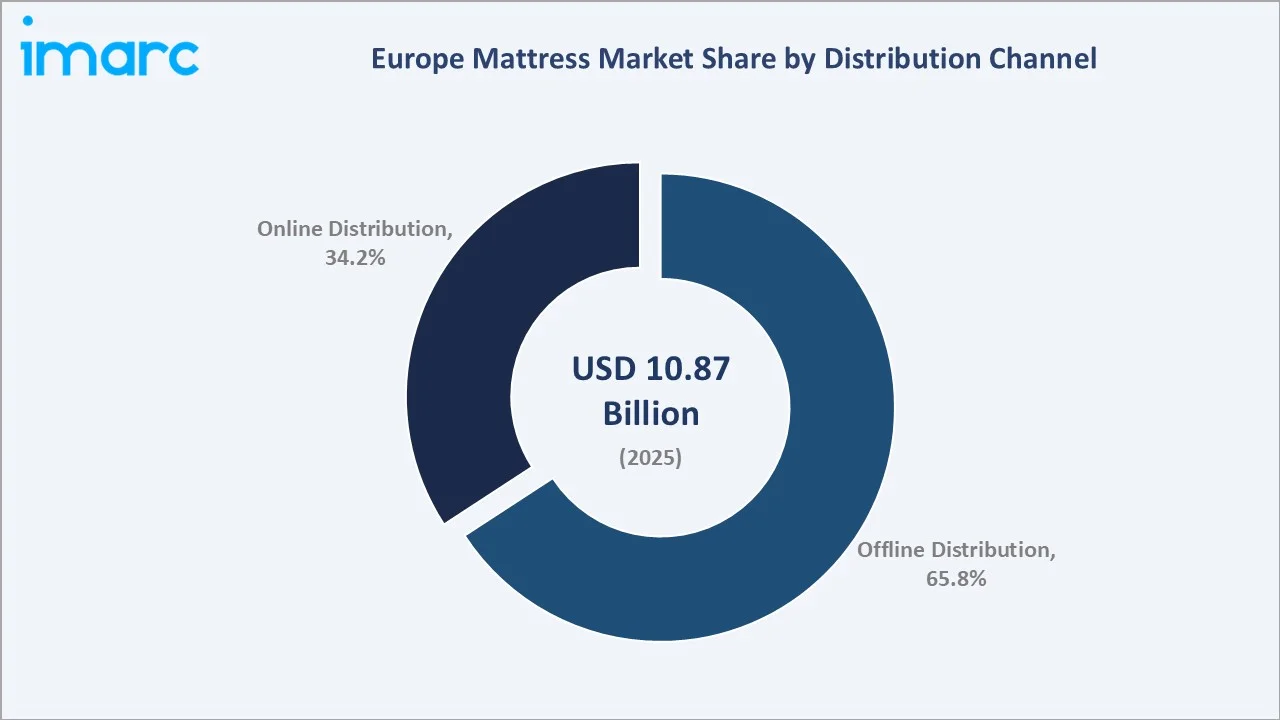

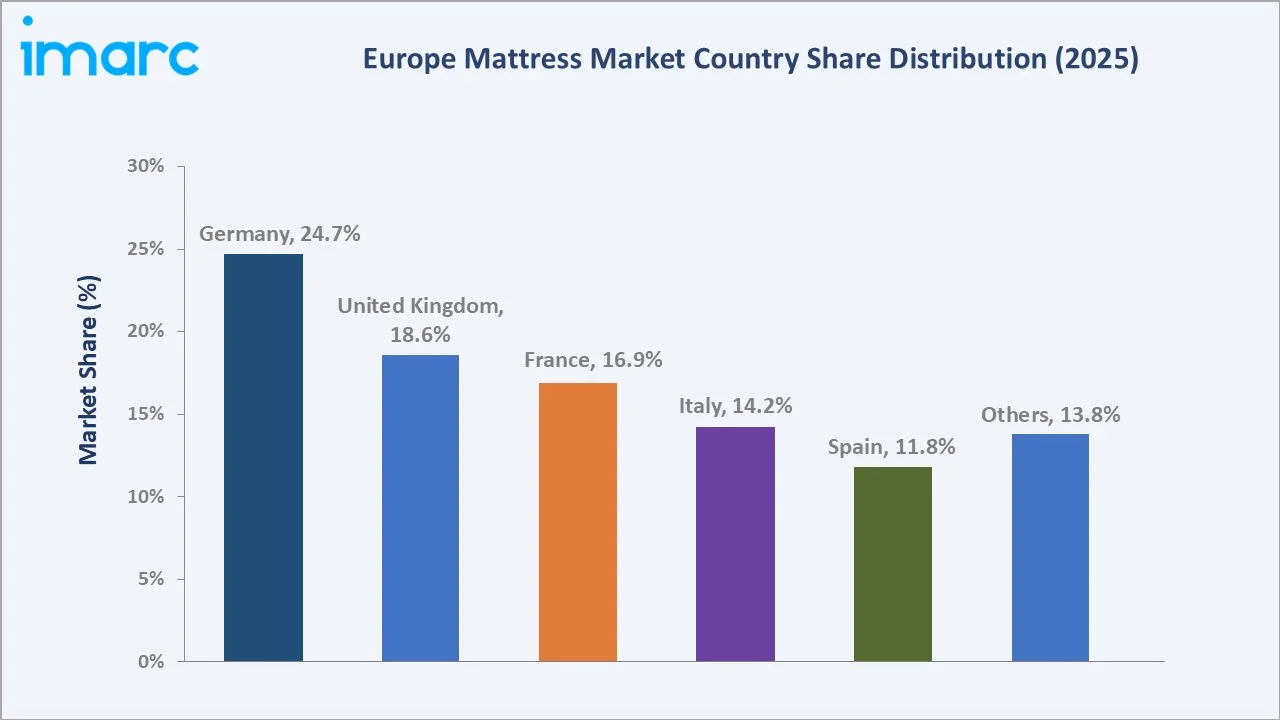

Germany leads regionally with a 24.7% market share in 2025, anchored by its large population base, strong consumer purchasing power, and deeply embedded culture of investing in high-quality sleep products. Offline distribution commands 65.8% of the market, reflecting the importance of in-store product trial for a tactile purchase category.

To get more information on this market, Request Sample

The Europe mattress market grew from USD 8.26 Billion in 2020 to USD 10.87 Billion in 2025, reflecting COVID-19-induced home comfort investment acceleration, post-pandemic renovation spending, and the structural penetration of online mattress brands disrupting traditional retail channel economics. The market is forecast to reach USD 17.81 Billion by 2034, driven by Europe’s aging population creating premium orthopedic mattress demand, continued premiumization across all product categories, and the expansion of branded hospitality real estate requiring commercial mattress procurement.

Executive Summary

The Europe mattress market is experiencing steady, quality-driven growth underpinned by consumer premiumization, the digital transformation of mattress retail, aging demographic demand for therapeutic sleep products, and the structural recovery of European residential construction. The market stood at USD 10.87 Billion in 2025 and is forecast to reach USD 17.81 Billion by 2034 at a 5.64% CAGR.

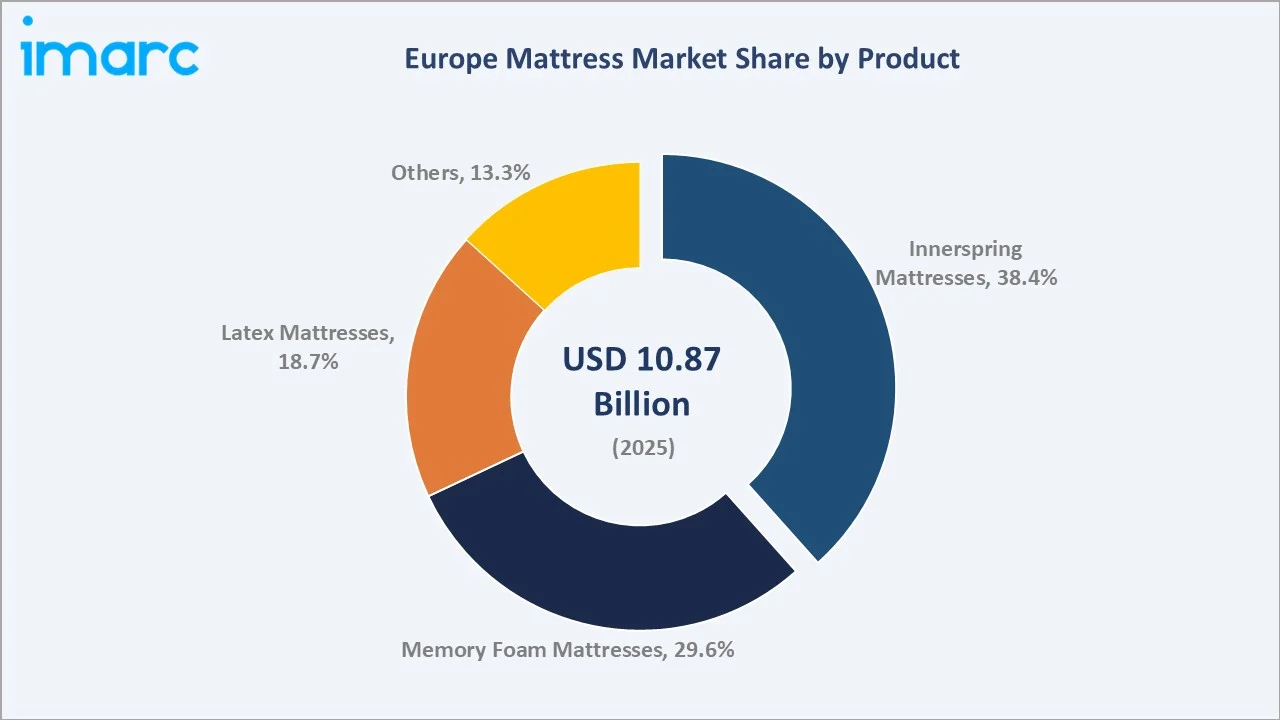

Offline distribution leads with a 65.8% share in 2025, reflecting the mattress category’s fundamental requirement for physical product experience that drives purchase decisions at the point of sale in furniture stores, dedicated mattress chains, and home goods retailers. Innerspring mattresses dominate the product segment at 38.4%, reflecting their established consumer familiarity, competitive price positioning, and continued technological innovation through hybrid spring-foam constructions.

Germany at 24.7% is Europe’s largest mattress market, followed by the United Kingdom at 18.6% and France at 16.9%. Together, these three markets account for approximately 60.2% of European mattress revenue, reflecting their combination of market size, consumer spending power, and sophisticated retail infrastructure.

Key Market Insights

|

Insight |

Data |

|

Largest Distribution Channel |

Offline Distribution – 65.8% share (2025) |

|

Fastest Growing Distribution Channel |

Online Distribution – ~7.4% CAGR (2026-2034) |

|

Largest Product |

Innerspring Mattresses – 38.4% share (2025) |

|

Fastest Growing Product |

Latex Mattresses – ~6.8% CAGR (2026-2034) |

|

Leading Country |

Germany – 24.7% share (2025) |

|

Top Companies |

Somnigroup International Inc., Emma Mattresses GmbH, Serta Simmons Bedding, LLC, SleepCo |

Key Analytical Observations Supporting The Above Data:

- Offline distribution at 65.8% (2025) is sustained by the mattress category’s high-involvement purchase nature, where consumers spend an average of 6–8 weeks in the consideration phase before purchase and strongly prefer in-store product trial.

- Online distribution at ~7.4% CAGR is driven by the D2C boxed mattress segment’s transformation of the consumer buying journey. Multiple companies are normalizing online mattress purchase through 100-night free trials, transparent pricing, and social proof marketing.

- Innerspring Mattresses at 38.4% (2025) maintain their market leadership through the innovation of hybrid mattress constructions, combining steel pocket coil spring cores with multiple layers of memory foam or latex, that deliver the pressure point response of a spring mattress with the body-contouring comfort of foam.

- Germany’s 24.7% (2025) market leadership reflects its status as Europe’s largest economy and most populous nation, combined with a consumer culture that strongly values quality and is willing to invest significantly in sleep infrastructure.

Europe Mattress Market Overview

The Europe mattress market encompasses the design, manufacturing, distribution, and retail of innerspring, memory foam, latex, hybrid, and specialty mattresses sold through furniture retailers, dedicated mattress chains, department stores, bedding specialists, and direct-to-consumer online platforms. The market serves residential households, hospitality, healthcare facilities, and commercial institutional buyers, with residential household demand accounting for approximately 80–85% of total market revenue.

Europe’s mattress value chain is characterized by the increasing vertical integration of D2C online brands, the ongoing transformation of offline retail from product-displaying showrooms to sleep advisory experience centers, and the growing sustainability pressures on raw material sourcing, driving the adoption of natural latex, organic wool, and recycled material alternatives.

Market Dynamics

To evaluate market opportunities, Request Sample

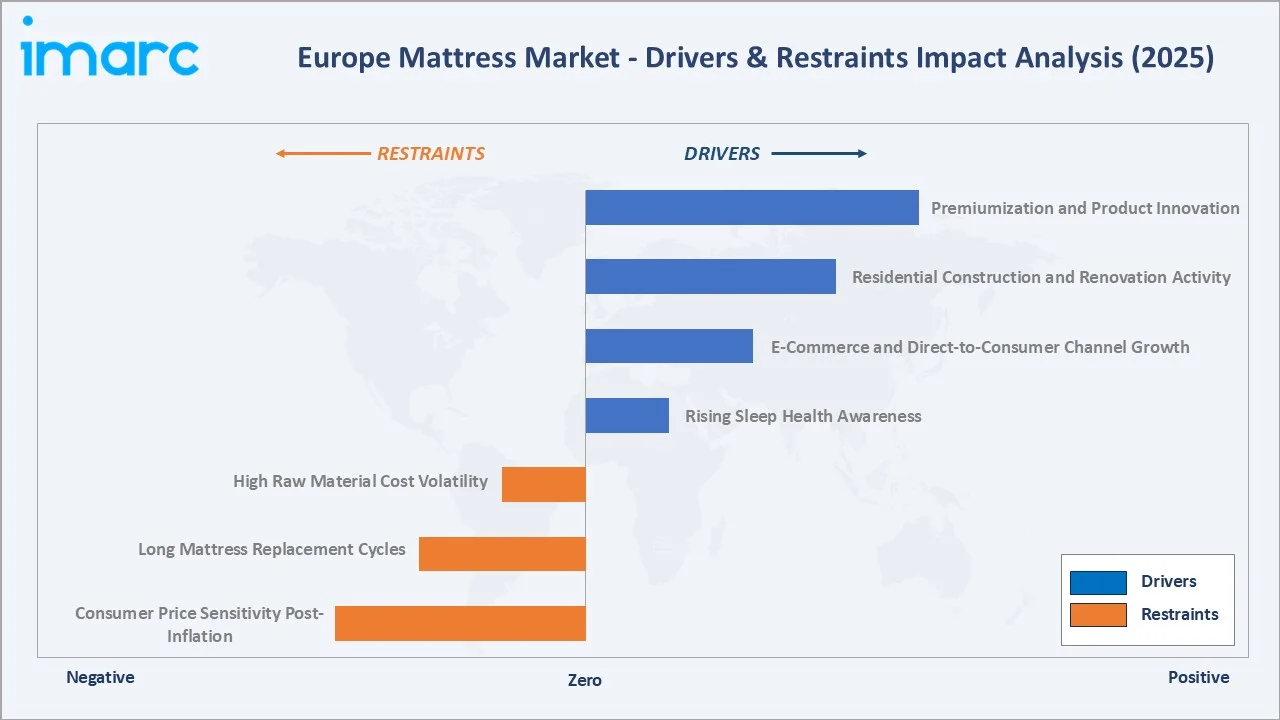

Market Drivers

- Rising Sleep Health Awareness: Growing European consumer recognition of sleep as a fundamental health pillar, supported by clinical research, wearable sleep tracking proliferation, and media attention to sleep disorders, is driving willingness to invest in premium sleep infrastructure.

- E-Commerce and Direct-to-Consumer Channel Growth: The D2C mattress model has fundamentally disrupted European mattress retail by offering competitive-quality products at 30–50% below traditional retail pricing through the elimination of retail margin, combined with 100-night free home trial programs that replicate the in-store trial experience.

- Residential Construction and Renovation Activity: European dwellings completions totaled approximately 1.46 million units in 2025, driven by Germany’s Wohnungsbau program, France's Prêt à Taux Zéro (PTZ) scheme, and the UK’s housing development commitments.

- Premiumization and Product Innovation: European consumers are demonstrating strong willingness to trade up within the mattress category, as consumers upgrade from basic to hybrid, from standard to orthopedic, and from conventional to natural/organic constructions.

Market Restraints

- High Raw Material Cost Volatility: Mattress production relies heavily on polyurethane foam (derived from petroleum-based polyols and toluene diisocyanate), steel for spring cores, and natural latex. Polyurethane foam prices increased by 35–45% between 2020 and 2023 due to global supply chain disruptions and energy cost escalation at European foam manufacturing facilities.

- Long Mattress Replacement Cycles: The European average mattress replacement cycle of 8–10 years constrains annual unit volume growth, as the majority of purchases are driven by worn-out product replacement rather than discretionary lifestyle upgrading.

- Consumer Price Sensitivity Post-Inflation: Europe’s 2022–2023 inflation cycle, which reduced real household disposable income across all major European economies, increased consumer price sensitivity in the mattress category and drove some trade-down from mid-market to value-tier products.

Market Opportunities

- Smart and Health-Monitoring Mattresses: The convergence of sleep science, IoT technology, and consumer health monitoring creates a significant product innovation opportunity in the European premium segment. Temperature-regulated mattresses, biometric tracking mattresses, and AI-powered sleep coaching platforms cater to Europe’s growing population of health-optimized, premium-spending consumers.

- Circular Economy and Sustainable Mattress Innovation: European sustainability regulation is creating both compliance requirements and brand differentiation opportunities. Natural latex mattresses, recycled steel spring cores, and wool and cotton ticking materials are capturing premium consumer demand, with sustainability-certified products commanding 15–25% price premiums over conventional equivalents.

Market Challenges

- Mattress Disposal and End-of-Life Recycling Infrastructure Gaps: Mattresses are one of the most challenging household items to recycle, due to their composite material construction requiring sophisticated disassembly before materials can be recovered.

- Intensifying D2C Competition and Brand Proliferation: The low barriers to entry in the D2C mattress segment have led to the proliferation of dozens of competitive brands in each major European market, intensifying price and marketing investment competition.

Emerging Market Trends

1. The Rise of Hybrid Spring-Foam Mattresses as Category Standard

Hybrid spring-foam mattresses combine responsive coil support with foam comfort layers, offering balanced cushioning, better spinal alignment, pressure relief, and suitability for different sleeping positions. They also provide improved airflow, reduced motion transfer for couples, stronger edge support, and longer durability compared to basic foam mattresses.

2. Emma Mattress Gains Recognition in Product Quality Testing

Emma Original mattress achieved the highest score in Testfakta’s foam mattress test, outperforming Swedish competitors with strong results in ergonomics, breathability, durability, build quality, and chemical safety. The recognition strengthened Emma’s positioning in Europe’s bed-in-a-box market, supported by its 100-night trial, 10-year guarantee, and focus on R&D-led sleep technology.

3. Sustainability Certification as Purchase Criterion

Mattress certification schemes such as EU Ecolabel, OEKO-TEX, CertiPUR, GREENGUARD Gold, GOTS, and Cradle to Cradle help verify product safety, material quality, low emissions, sustainability, and responsible manufacturing. These certifications boost consumer confidence, support regulatory alignment, differentiate brands in the market, and encourage manufacturers to adopt cleaner materials, circular design, and transparent practices.

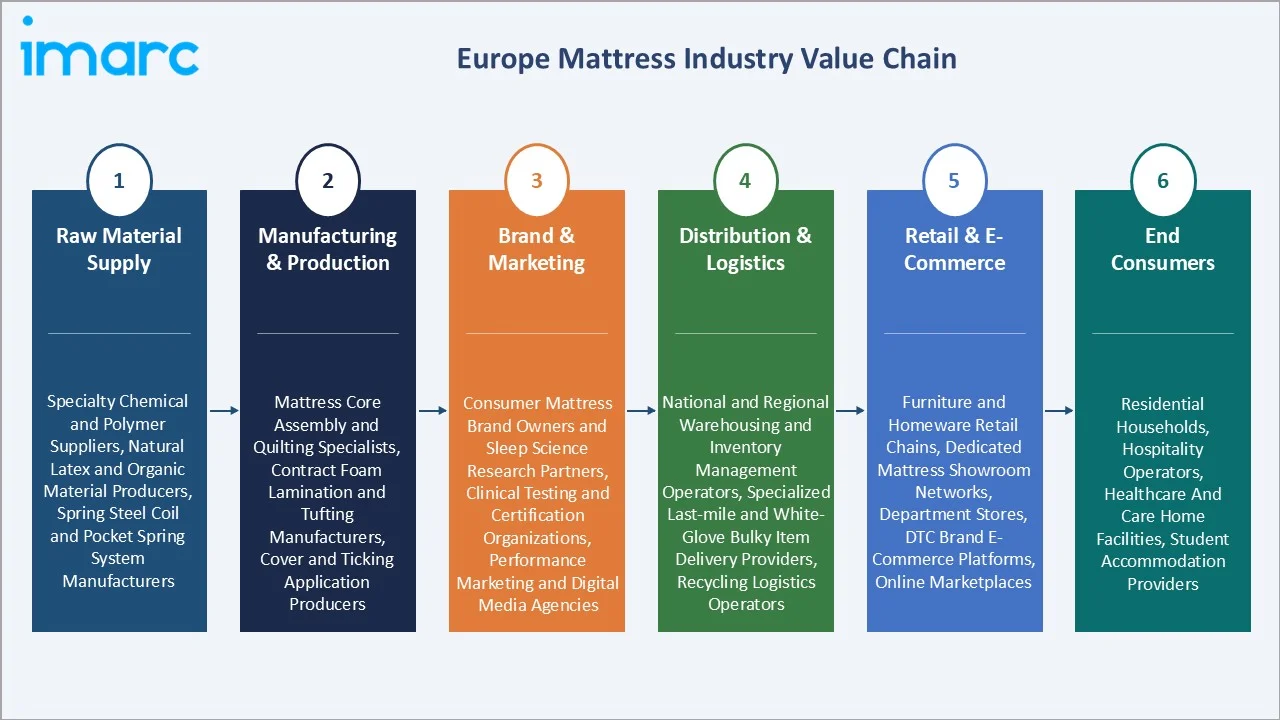

Industry Value Chain Analysis

Europe’s mattress value chain is increasingly shaped by the vertical integration ambitions of D2C online brands that are compressing traditional multi-tier distribution margins, and by sustainability pressures driving reformulation of raw material inputs throughout the manufacturing stage.

|

Stage |

Key Players/Examples |

|

Raw Material Supply |

Specialty chemical and polymer suppliers, natural latex and organic material producers, spring steel coil and pocket spring system manufacturers |

|

Manufacturing & Production |

Mattress core assembly and quilting specialists, contract foam lamination and tufting manufacturers, cover and ticking application producers |

|

Brand & Marketing |

Consumer mattress brand owners and sleep science research partners, clinical testing and certification organizations, performance marketing and digital media agencies |

|

Distribution & Logistics |

National and regional warehousing and inventory management operators, specialized last-mile and white-glove bulky item delivery providers, recycling logistics operators |

|

Retail & E-Commerce |

Furniture and homeware retail chains, dedicated mattress showroom networks, department stores, DTC brand e-commerce platforms, online marketplaces |

|

End Consumers |

Residential households, hospitality operators, healthcare and care home facilities, student accommodation providers |

Technology Landscape in the Europe Mattress Industry

Advanced Foam and Materials Technology

Polyurethane foam innovation has produced open-cell breathable foam structures that address the primary consumer complaint of foam mattress heat retention. Phase change material (PCM) infusions, graphite gel layers, and copper-infused foam technologies are additionally being incorporated into premium mattress constructions to improve thermal regulation, with clinical testing demonstrating 2–4°C core temperature reductions versus conventional foam across a standard sleep period.

Smart Mattress Technology and IoT Integration

Sleep Number’s 360 Smart Bed platform uses embedded air chambers, biometric sensors, and AI algorithms to automatically adjust mattress firmness throughout the night in response to detected body position changes. The company’s Sleep Number app provides daily sleep scores, health trend tracking, and personalized sleep coaching, integrating with Apple Health, Google Fit, and Fitbit ecosystems.

Sustainable Manufacturing and Circular Economy Technology

European mattress manufacturers are investing in sustainable manufacturing technologies, including bio-based polyols for foam production, waterborne adhesives, and automated spring encasement systems enabling single-material pocket spring assemblies that simplify end-of-life recycling.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Distribution Channel |

Offline Distribution |

65.8% |

2025 |

|

Product |

Innerspring Mattresses |

38.4% |

2025 |

|

Size |

Queen Size |

🔒 |

2025 |

|

Application |

Domestic |

🔒 |

2025 |

|

Country |

Germany |

24.7% |

2025 |

By Distribution Channel

Offline distribution dominates with a 65.8% share in 2025. This segment encompasses furniture retail chains, dedicated mattress showrooms, department stores, and independent bedding specialists. Offline distribution’s structural advantage is rooted in the mattress category’s high-involvement purchase behavior, where consumers derive significantly higher purchase confidence from physical product trial than from online product specifications alone.

To access detailed market analysis, Request Sample

Online distribution at 34.2% is growing at ~7.4% CAGR, the fastest of any channel, as D2C brands continue to acquire consumer confidence through progressively more consumer-protective trial policies, clinical certification marketing, and investment in AI-powered sleep recommendation tools that replicate the advisory function of in-store sleep consultants.

By Product

Innerspring mattresses lead with a 38.4% share in 2025, which includes traditional open coil, Bonnell coil, and pocket spring constructions. The segment’s market leadership reflects its established consumer familiarity, the broad availability of spring mattresses across all retail formats, and the continuous innovation of hybrid spring-foam constructions that modernize the spring mattress value proposition for contemporary consumer preferences.

Memory foam mattresses at 29.6% serve the premium comfort segment, with strong demand driven by their pressure-relieving properties, body-contouring support, motion isolation, and growing preference among consumers seeking enhanced sleep comfort and orthopedic benefits.

Regional Market Insights

Germany’s market leadership (24.7%, 2025) reflects its position as Europe’s largest economy and home to approximately 83 million consumers with EUR 2.1 trillion annual household spending. Germany hosts one of the world's most developed bedding and mattress retail chains and is one of the most visited furniture retail destinations.

The United Kingdom, at 18.6%, benefits from strong consumer spending on home furnishings, rising demand for premium and sustainable mattresses, growing online mattress sales, and increasing awareness of sleep health and ergonomic comfort.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

24.7% |

Largest European consumer base; strong premium and quality-focused purchasing culture; large retail network; high residential renovation investment |

|

United Kingdom |

18.6% |

Strong D2C mattress adoption; high retail network; active housing market driving bedroom investment; premium mattress companies' expansion |

|

France |

16.9% |

Growing natural and organic latex mattress demand; recovering residential new-build activity |

|

Italy |

14.2% |

Strong manufacturing heritage; high-design premium consumer segment; short-term rental market driving commercial mattress demand; growing online channel |

|

Spain |

11.8% |

Post-COVID residential recovery driving replacement purchases; growing mid-market premium adoption; multiple domestic brand leadership; tourism hospitality sector commercial mattress procurement |

|

Others |

13.8% |

Netherlands, Belgium, Sweden, Poland, and Eastern European markets with a growing middle-class consumer base and e-commerce adoption |

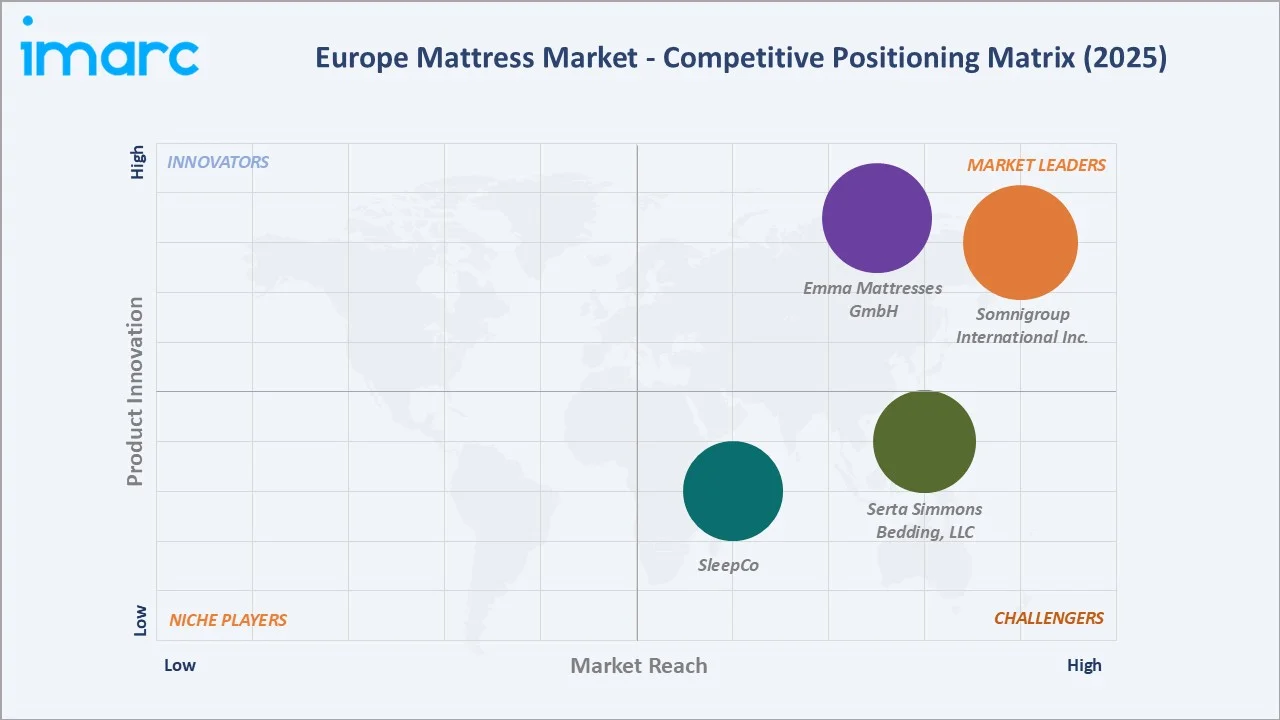

Competitive Landscape

Europe’s mattress market exhibits moderate concentration, with a bifurcated competitive structure between large multinational incumbents operating across multiple European countries through wholesale retail partnerships, and a dynamic tier of D2C online brands that have disrupted traditional channel economics through direct consumer relationships and performance marketing.

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Somnigroup International Inc. |

Tempur-Pedic, Sealy, Stearns & Foster |

Market Leader |

One of the world’s largest mattress companies; strong European retail partnerships; clinical sleep science credentials |

|

Emma Mattresses GmbH |

Emma |

Market Leader |

Europe's leading direct-to-consumer mattress brand by online revenue; strong omnichannel expansion through retail partnerships alongside DTC e-commerce |

|

Serta Simmons Bedding, LLC |

Serta, Beautyrest, Tuft & Needle, BeautySleep |

Strong Challenger |

US-origin brands with strong European wholesale distribution; premium coil heritage; broad product range from mass to premium |

|

SleepCo |

RUF, Bruno, Ergosleep, Magnitude, Nox |

Challenger |

Quality-first brand positioning; Boxspring bed and mattress combination innovation |

The market’s traditional players are responding through D2C channel investment, e-commerce capability building, and premium product range expansion.

Key Company Profiles

Somnigroup International Inc.

Somnigroup International Inc. (formerly Tempur Sealy International) operates Tempur Sealy, Dreams, and Mattress Firm as business units. It is the world’s largest mattress and sleep products company and the dominant premium brand in the European mattress market.

- Product Portfolio: Tempur-Adapt, Tempur-Cloud, Tempur-LuxeBreeze; Sealy Posturepedic Hybrid; Stearns & Foster Estate; Tempur Ergo Smart Base; Tempur-Pedic; Stearns & Foster.

- Recent Developments: In May 2025, Somnigroup International reported Q1 2025 net sales growth of 34.9% to USD 1.60 billion, mainly supported by the inclusion of Mattress Firm sales after its acquisition. However, the company posted a net loss of USD 33.1 million due to acquisition-related costs, while adjusted net income rose 8.1% to USD 97.0 million.

- Strategic Focus: European retail partnership expansion and D2C channel investment; Sealy hybrid range expansion to capture growing hybrid segment; 90-night trial program for retail channel competitive parity; sustainability roadmap including bio-based Tempur foam development.

Emma Mattresses GmbH

Emma Mattresses GmbH, operating as Emma – The Sleep Company, is the world's largest direct-to-consumer sleep brand and Europe's leading D2C mattress company.

- Product Portfolio: Emma Original, Emma Hybrid Comfort, Emma Hybrid Premium, Emma One, and Emma Diamond Hybrid.

- Strategic Focus: Omnichannel retail expansion across Europe through company-owned flagship stores and franchised independent stores; DTC e-commerce leadership and subscription-based sleep product ecosystem development; continued product innovation in hybrid mattress and temperature-regulation technology.

Market Concentration Analysis

Europe’s mattress market exhibits moderate concentration in the premium and branded segment, with Somnigroup International Inc., Emma Mattresses GmbH, Serta Simmons Bedding, LLC, and SleepCo collectively controlling an estimated 30–40% of total European branded mattress revenue.

The remaining share is distributed across a highly fragmented landscape of regional national champions, D2C online disruptors, and IKEA’s private-label range, which alone accounts for an estimated 8–10% of European mattress unit volume through its pan-European store network.

Market consolidation is occurring primarily at the D2C brand tier, where capital-intensive customer acquisition costs, rising competitive pressure, and the need for manufacturing scale are forcing mergers and strategic acquisitions.

Investment & Growth Opportunities

Fastest Growing Segments

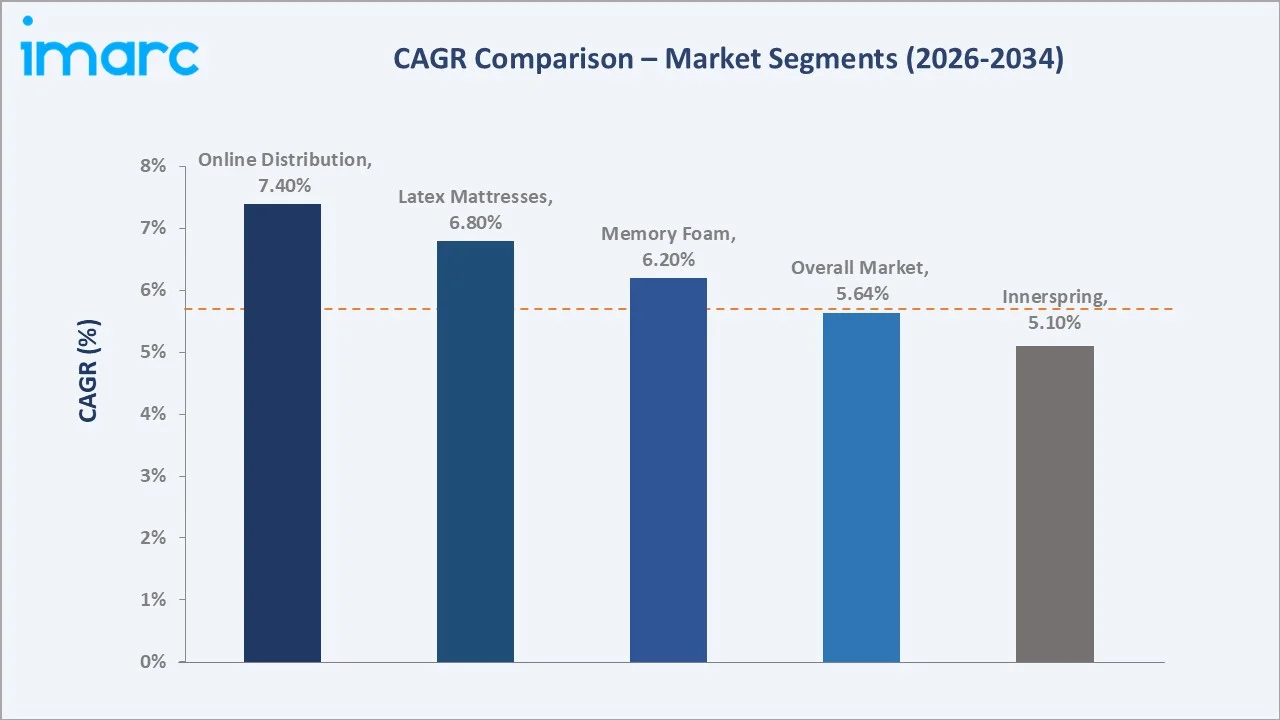

Online distribution (~7.4% CAGR), latex mattresses (~6.8% CAGR), memory foam mattresses (~6.2% CAGR), and the smart mattress sub-segment (estimated ~15%+ CAGR from a small base) represent the primary value-growth investment vectors through 2034. Commercial application is estimated to grow at approximately 6.5% CAGR as European hospitality investment recovers and operators upgrade sleep quality as a competitive differentiation strategy.

Emerging Market Expansion

Eastern European markets, including Poland, Romania, the Czech Republic, and Hungary, represent significant expansion opportunities as household incomes approach Western European levels and e-commerce penetration grows.

Venture and Institutional Investment Trends

- Private equity investment in mattress retail and manufacturing consolidation platforms: Waterland acquired RUF|Betten and BRUNO from NORD Holding to form a stronger premium sleep and bedroom furniture group in Germany, combining RUF’s established retail presence with BRUNO’s direct-to-consumer model.

- EUROPUR highlights that mattress recycling in Europe is gaining momentum as EPR schemes, landfill reduction targets, and circular economy policies push the bedding industry toward better collection and material recovery. France is cited as a leading example, reducing mattress landfilling from 100% in 2012 to below 4%, while around 50% of collected mattresses are now recycled.

Future Market Outlook (2026-2034)

Europe’s mattress market is positioned for steady, value-driven growth through 2034. From a base of USD 10.87 Billion in 2025, the market is projected to reach USD 14.30 Billion by 2030 and USD 17.81 Billion by 2034 at a 5.64% CAGR. Germany will retain absolute market leadership, but Spain and Italy are projected to grow at above-average regional rates as post-pandemic household formation and hospitality sector recovery drive replacement and new purchase demand.

The distribution channel mix will shift toward online parity with offline by approximately 2031–2032, as D2C brand maturity, generational consumer preference for e-commerce, and retail chain in-store trial program adoption collectively close the experiential gap between channels. The product mix will shift toward premium hybrid constructions as the category standard, with natural and organic latex growing disproportionately to approximately 22–25% of product share by 2034, driven by EU sustainability regulation and consumer demand for certified natural materials.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 75 industry participants in 2024–2025, including mattress manufacturers, brand managers at leading European mattress brands, retail category buyers, D2C brand executives, sustainability certification bodies, and industry association representatives from the European Bedding Industries Association (EBIA).

Secondary Research

Secondary research encompassed annual reports; Eurostat household spending and residential construction data; European Bedding Industries Association market reports; OEKO-TEX certification database; Euromonitor consumer home furnishing datasets; and national trade data from Germany, UK, France, Italy, and Spain statistical offices.

Forecasting Models

Market size estimations were derived using bottom-up country-level volume and average selling price modelling, incorporating demographic household formation rates, mattress replacement cycle analysis, channel mix shift trajectories, and premiumization uplift factors. A CAGR of 5.64% reflects consensus validated against EBIA industry projection data and IMARC’s primary expert panel review.

Europe Mattress Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Innerspring Mattresses, Memory Foam Mattresses, Latex Mattresses, Others |

| Distribution Channels Covered | Online Distribution, Offline Distribution |

| Sizes Covered | Twin or Single Size, Twin XL Size, Full or Double Size, Queen Size, King Size Mattress, Others |

| Applications Covered | Domestic, Commercial |

| Countries Covered | Germany, France, the United Kingdom, Italy, Spain, Others |

| Companies Covered | Somnigroup International Inc., Emma Mattresses GmbH, Serta Simmons Bedding LLC, SleepCo, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe mattress market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe mattress market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe mattress industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Mattress Market Report

The Europe mattress market reached USD 10.87 Billion in 2025 and is forecast to reach USD 17.81 Billion by 2034.

The market is expected to grow at a CAGR of 5.64% during 2026-2034, driven by rising sleep health awareness, e-commerce expansion, residential construction recovery, and product premiumization.

Germany leads with a 24.7% share in 2025, reflecting its status as Europe’s largest economy, home to approximately 83 million consumers with strong purchasing power and cultural investment in home quality.

Offline distribution leads with a 65.8% share in 2025, anchored by furniture retail chains, dedicated mattress showrooms, and department stores, where consumer product trial remains the primary purchase conversion driver.

Innerspring mattresses lead with a 38.4% share in 2025, driven by established consumer familiarity, competitive price positioning, and the innovation of hybrid spring-foam constructions, modernizing the category’s value proposition.

Some of the key players include Somnigroup International Inc., Emma Mattresses GmbH, Serta Simmons Bedding, LLC, and SleepCo.

Online distribution is growing at approximately 7.4% CAGR because D2C mattress brands have successfully normalized online mattress purchase through 100-night free trial programs, transparent pricing, and performance marketing, capturing the digital-native 25–45 consumer cohort across Germany, the UK, and France.

Key challenges include raw material cost volatility, the structural constraint of long 8–10 year replacement cycles limiting annual unit volume growth, post-inflationary consumer price sensitivity, mattress end-of-life recycling infrastructure gaps, and intensifying D2C brand competition, increasing consumer acquisition costs.

Smart and health-monitoring mattresses, natural/organic latex certification, Eastern European market expansion, AI-personalized sleep recommendation platforms, and commercial hospitality sector mattress procurement represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade