Europe Medical Cannabis Market Size, Share, Trends and Forecast by Species, Derivative, Application, End Use, Route of Administration, and Country, 2026-2034

Europe Medical Cannabis Market Summary:

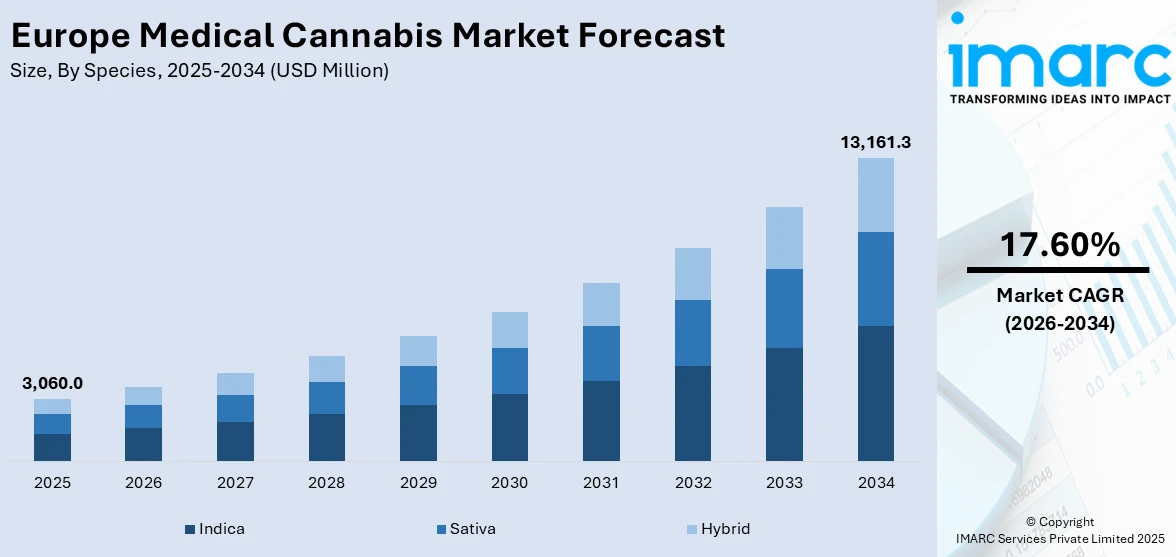

The Europe medical cannabis market size was valued at USD 3,060.0 Million in 2025 and is projected to reach USD 13,161.29 Million by 2034, growing at a compound annual growth rate of 17.60% from 2026-2034.

The Europe medical cannabis market is experiencing accelerated expansion as regulatory reforms across major economies streamline patient access and encourage domestic cultivation. Growing clinical acceptance of cannabinoid-based therapies, coupled with increasing prevalence of chronic conditions such as cancer, epilepsy, and neurological disorders, is broadening the patient base. Advancements in extraction technologies, expanding pharmaceutical-grade product portfolios, and rising investment in research and development are further reinforcing the region’s position as a leading hub for cannabis-based medicine, contributing positively to the Europe medical cannabis market share.

Key Takeaways and Insights:

- By Species: Indica dominates the market with a share of 44% in 2025, driven by its potent calming and analgesic properties widely used in managing chronic pain, insomnia, and anxiety disorders.

- By Derivative: Cannabidiol (CBD) leads the market with a share of 51% in 2025, owing to its non-psychoactive therapeutic profile and growing recognition for treating inflammation, epilepsy, and anxiety.

- By Application: Cancer represents the largest segment with a market share of 43% in 2025, fueled by the widespread use of cannabis for alleviating chemotherapy side effects including pain, nausea, and appetite loss.

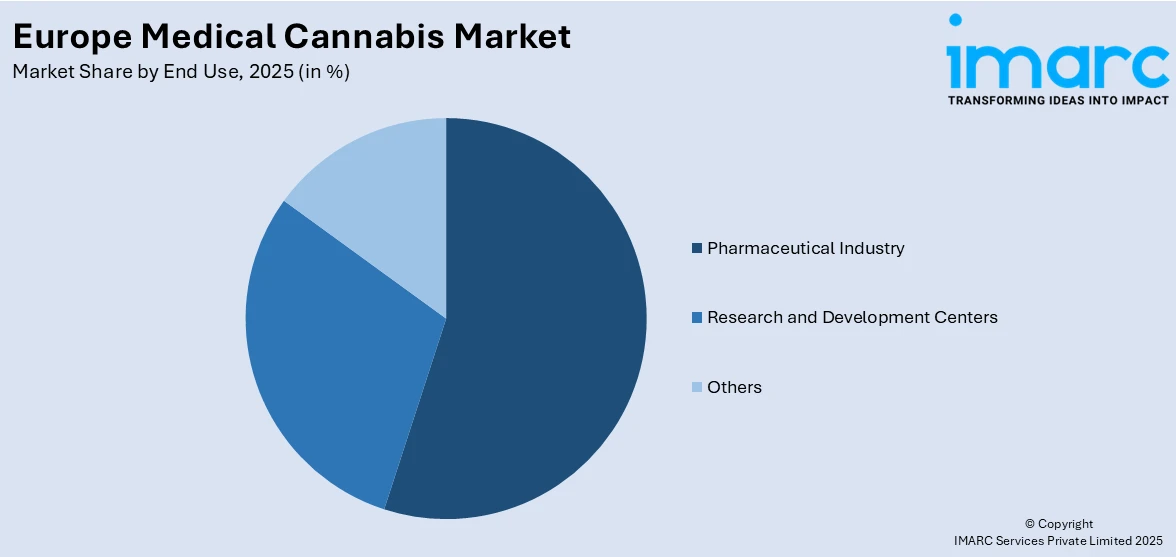

- By End Use: Pharmaceutical industry dominates the market with a share of 50% in 2025, supported by established clinical trial capabilities, regulatory compliance infrastructure, and growing cannabis-based drug development.

- By Route of Administration: Oral solutions and capsules represent the largest share at 37% in 2025, preferred for precise dosing, convenience, and familiarity with traditional pharmaceutical delivery formats.

- Key Players: The Europe medical cannabis market features a dynamic competitive landscape where established pharmaceutical companies compete alongside emerging cannabis-focused enterprises. Key players are strengthening their positions through strategic partnerships, expanded cultivation facilities, and innovative product formulations to capture growing patient demand across the region. Some of the key players are Canopy Growth Corporation, Aurora Cannabis Inc., Tilray, Inc., Demecan GmbH, Panaxia Pharmaceutical Industries Ltd, Little Green Pharma, Cannamedical Pharma GmbH, Sapphire Medical, Althea Group, and Bedrocan International.

To get more information on this market Request Sample

The Europe medical cannabis market is experiencing strong growth as regulatory frameworks become more structured and therapeutic acceptance expands across the continent. Germany continues to lead the regional market, with streamlined prescription processes and broader patient access driving increased demand for medical cannabis products. The United Kingdom has also emerged as a significant market, with patients increasingly able to obtain treatments through telehealth platforms and other healthcare channels. Meanwhile, Spain has moved toward formal recognition of medical cannabis for patients with chronic conditions, supporting wider adoption in clinical practice. These regulatory advancements, combined with growing awareness of cannabis-based therapies, are encouraging product diversification and innovation across Europe. Overall, the market is evolving toward greater accessibility, enhanced patient choice, and a more robust ecosystem of medical cannabis offerings, positioning the region for sustained development and increased integration of cannabis-based treatments into mainstream healthcare systems. For instance, in December 2025, Canadian medical cannabis company Aurora Cannabis Inc. introduced a new brand, Daily Special™, in Germany, aiming to provide consistent, high-quality cannabis at accessible prices. The launch builds on the company’s recent strong performance and contributes to the continued expansion of Germany’s medical cannabis market.

Europe Medical Cannabis Market Trends:

Progressive Regulatory Reforms Across Key European Markets

The medical cannabis landscape in Europe is evolving as governments implement structured regulatory frameworks that enhance patient access and foster industry development. Germany has simplified prescribing processes and removed cannabis from restrictive classifications, supporting broader adoption. Spain introduced its first regulated framework for therapeutic cannabis dispensed through hospital pharmacies. Meanwhile, several other countries, including the Czech Republic and Denmark, have advanced policies around medical or adult-use cannabis, reinforcing market expansion. These regulatory changes are collectively driving growth, encouraging investment, and promoting wider acceptance of cannabis-based therapies across Europe.

Technological Innovation in Cannabis Delivery Systems

Advancements in medical cannabis delivery mechanisms are reshaping patient treatment options across Europe, with manufacturers developing pharmaceutical-grade devices that ensure precise, consistent dosing. For instance, in May 2025, Curaleaf International, in partnership with Jupiter Research, secured EU Class IIa medical device certification for Europe’s first handheld liquid inhalation device designed for cannabis-based medicines. The rechargeable device delivers standardized cannabinoid doses through magnetic snap-in cartridges, offering prescribers clinical confidence and patients a discreet treatment alternative. Such innovations are broadening the market scope beyond traditional flower and oil formulations, encouraging new patient demographics and enhancing therapeutic outcomes through improved bioavailability and dosing precision.

Rising Demand for Cannabidiol-Based Therapeutic Products

The growing preference for non-psychoactive cannabinoid therapies is accelerating demand for CBD-based medical products across Europe, driven by their efficacy in managing anxiety, chronic pain, inflammation, and epilepsy. The pharmaceutical sector is investing significantly in enhanced CBD formulations with improved bioavailability. For instance, in February 2024, Zerion Pharma A/S partnered with dsm-firmenich to develop high-quality cannabidiol formulations with enhanced solubility for treating severe pain, inflammation disorders, depression, and anxiety. Meanwhile, Epidiolex, the CBD-based epilepsy treatment developed by GW Pharmaceuticals and now marketed by Jazz Pharmaceuticals, generated approximately USD 972 million in global sales in 2024, demonstrating the commercial viability of pharmaceutical-grade cannabinoid medicines.

.webp)

Market Outlook 2026-2034:

The Europe medical cannabis market is positioned for sustained expansion as legalization momentum accelerates, patient populations grow, and pharmaceutical innovation diversifies product offerings. Increasing integration of telemedicine platforms, broadening reimbursement coverage, and enhanced cultivation capabilities across key markets are expected to drive market revenues upward. Expanding domestic production, strengthening international supply chains, and rising clinical endorsement of cannabinoid therapies are expected to create a more competitive and patient-centric market environment. The market generated a revenue of USD 3,060.0 Million in 2025 and is projected to reach a revenue of USD 13,161.29 Million by 2034, growing at a compound annual growth rate of 17.60% from 2026-2034.

Europe Medical Cannabis Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Species |

Indica |

44% |

|

Derivative |

Cannabidiol (CBD) |

51% |

|

Application |

Cancer |

43% |

|

End Use |

Pharmaceutical Industry |

50% |

|

Route of Administration |

Oral Solutions and Capsules |

37% |

Species Insights:

- Indica

- Sativa

- Hybrid

Indica leads the market with a revenue share of 44% of the total Europe medical cannabis market in 2025.

Indica strains dominate the European medical cannabis market owing to their potent therapeutic properties, particularly sedative and analgesic effects that are highly effective in treating chronic pain, anxiety, insomnia, and muscle spasms. These conditions represent a significant portion of the patient base across Europe, where aging populations and high prevalence of musculoskeletal and neurological disorders drive consistent demand for calming cannabis varieties. Indica’s shorter growth cycle and higher yields also make it a preferred choice for cultivators, ensuring reliable supply.

Growing clinical evidence supporting Indica-dominant formulations has boosted confidence among healthcare professionals across Europe. In Germany, these strains are widely prescribed for pain management and sleep-related conditions, reflecting their therapeutic value. The country’s licensed medical cannabis market now offers a broad range of flower products, with Indica-dominant varieties representing a significant portion of prescriptions dispensed through pharmacies. This trend underscores the increasing acceptance of targeted cannabis therapies and highlights the important role of Indica strains in meeting patient needs within regulated European medical cannabis markets.

Derivative Insights:

- Cannabidiol (CBD)

- Tetrahydrocannabinol (THC)

- Others

Cannabidiol (CBD) dominates with a share of 51% of the total Europe medical cannabis market in 2025.

CBD’s dominance in the European medical cannabis market stems from its non-psychoactive nature and broad therapeutic applications spanning anxiety management, chronic pain relief, anti-inflammatory treatment, and seizure control. The compound’s favorable safety profile has facilitated wider regulatory acceptance across European nations, enabling its incorporation into diverse pharmaceutical formulations, including oils, capsules, and topical preparations. Growing clinical evidence supporting CBD’s efficacy has accelerated physician adoption and patient demand throughout the continent.

The strong performance of pharmaceutical-grade CBD products highlights the segment’s market potential. Epidiolex, a CBD-based epilepsy treatment marketed by Jazz Pharmaceuticals, demonstrates the therapeutic and commercial viability of cannabidiol-derived medicines. Companies such as Zerion Pharma A/S are partnering with global formulation experts to develop advanced CBD products with improved bioavailability, targeting conditions such as severe pain, inflammation, and mood disorders. These initiatives reflect ongoing innovation and growing adoption of CBD-based pharmaceuticals across Europe, reinforcing the segment’s expanding role in medical treatment and patient care.

Application Insights:

- Cancer

- Arthritis

- Migraine

- Epilepsy

- Others

Cancer leads the market with a revenue share of 43% of the total Europe medical cannabis market in 2025.

The cancer application segment dominates the European medical cannabis market due to the substantial therapeutic benefits cannabis provides to oncology patients. Medical cannabis formulations containing both THC and CBD are extensively prescribed to alleviate cancer-associated symptoms, including chronic pain, chemotherapy-induced nausea and vomiting, and loss of appetite. In the EU, cancer-related mortality is projected to decline modestly, with a larger reduction expected among men compared to women over the period from 2020 to 2025. Over the longer term, millions of cancer-related deaths are estimated to have been prevented across the EU and the UK since 1989, reflecting improvements in early detection, treatment advances, and enhanced healthcare interventions. The rising incidence of cancer across Europe, coupled with increasing endorsement from oncologists and palliative care specialists, continues to drive robust demand for cannabis-based supportive therapies.

European oncology centers are increasingly incorporating cannabinoid therapies into standard palliative care, acknowledging their potential to enhance patient quality of life during and after treatment. Regulatory frameworks in several countries now recognize cancer as a qualifying condition for medical cannabis, allowing specialist physicians to prescribe standardized cannabis preparations when conventional therapies are insufficient. This growing acceptance and formal recognition reinforce the clinical credibility of cannabis in supportive cancer care, encouraging wider adoption, integration into treatment protocols, and the development of tailored cannabis-based therapies for oncology patients across Europe.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Pharmaceutical Industry

- Research and Development Centers

- Others

Pharmaceutical industry represents the largest share at 50% of the total Europe medical cannabis market in 2025.

The pharmaceutical industry’s dominance reflects its established infrastructure for clinical trials, regulatory compliance, and large-scale drug development. The major drug manufacturers are in the process of producing cannabis based drugs, which are of high quality and safety standards in Europe. The ability to perform intensive clinical assessments, receive marketing permissions, and build their distribution networks with licensed pharmacies is a substantial competitive edge in the controlled medical cannabis environment.

Pharmaceutical firms in partnership with cannabis-specific businesses are innovating on cannabinoid-based products in Europe. Such collaborations are promoting the establishment of end-to-end activities, such as cultivating and formulating, as well as the regulatory compliance and clinical use. The market is progressing to a more vertically integrated and locally manufactured medical cannabis solutions focus that attaches importance to quality, standardization, and compliance with high manufacturing standards. This trend is permitting increased efficiency of production, expedited market availability, and presentation of varied and high-quality therapeutic cannabis products, and this trend is facilitating increased use in the regulated medical cannabis markets of Europe.

Route of Administration Insights:

- Oral Solutions and Capsules

- Smoking

- Vaporizers

- Topicals

- Others

Oral solutions and capsules leads the market with a revenue share of 37% of the total Europe medical cannabis market in 2025.

Oral solutions and capsules maintain their market leadership due to their convenience, dosing precision, and ease of administration, which align with established pharmaceutical consumption patterns familiar to European patients and healthcare providers. These delivery formats offer controlled and sustained release of cannabinoids, making them particularly suitable for patients managing chronic conditions such as pain, epilepsy, and neurological disorders where consistent therapeutic levels are essential for effective treatment outcomes.

Oral cannabis formulations benefit from their similarity to conventional pharmaceutical products, improving patient adherence and easing healthcare professionals’ prescribing confidence. Regulators across Europe are increasingly supportive of oral products due to their consistent dosing and quality assurance. Legal frameworks in several countries now prioritize standardized preparations dispensed through healthcare facilities, favoring oral formats over raw plant material. This trend strengthens the regulatory and clinical standing of oral cannabis products, positioning them as a preferred option for controlled, safe, and reliable therapeutic use within Europe’s medical cannabis landscape.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany continues to lead Europe’s medical cannabis market, with strong demand supported by well-established import channels and a growing patient base. The country’s reliance on international suppliers and structured regulatory environment ensures consistent availability of high-quality medical cannabis products across licensed pharmacies.

France is gradually integrating medical cannabis into its mainstream healthcare system. Patients who participated in pilot programs are continuing treatment under evolving regulations, while authorities work toward establishing a permanent framework that ensures safe, controlled, and accessible medical cannabis therapies nationwide.

The United Kingdom has become a major European medical cannabis market, supported by telehealth platforms and increasing patient adoption. Growing awareness, broader access to licensed products, and structured healthcare support are enabling wider availability of medical cannabis treatments across both urban and regional healthcare settings.

Italy’s medical cannabis market remains stable, supported by domestic production and established prescription systems. Imports complement local supply to meet patient demand, ensuring access to a range of therapeutic formulations. The country continues to balance regulatory oversight with patient needs for consistent and high-quality medical cannabis products.

Spain has formalized medical cannabis access through a regulated framework, allowing treatment for conditions such as chronic pain, epilepsy, and cancer. Dispensing is carefully controlled through hospital pharmacies under specialist supervision, reinforcing safe, standardized, and clinically approved use of cannabis-based therapies.

Market Dynamics:

Growth Drivers:

Why is the Europe Medical Cannabis Market Growing?

Expanding Legalization and Regulatory Simplification

The progressive liberalization of medical cannabis regulations across European nations is fundamentally reshaping market access and driving substantial patient growth. Germany’s Cannabis Act, enacted in April 2024, reclassified cannabis from its narcotics schedule, simplified prescription requirements by allowing standard medical prescriptions instead of narcotic forms, and permitted telemedicine consultations. This regulatory overhaul triggered a remarkable expansion, with Germany’s medical cannabis patient base growing from approximately 250,000 to nearly 900,000 within a year. Other European countries are adopting similar approaches to medical cannabis regulation. Spain has established a comprehensive framework for therapeutic use, while Denmark has made its pilot program permanent, and Slovenia has legalized medical cannabis. The Czech Republic has advanced both adult-use and medical regulations. These coordinated regulatory developments are broadening patient access and fostering a more supportive environment for investment and industry growth across the continent.

Rising Prevalence of Chronic Diseases and Growing Therapeutic Acceptance

The increasing burden of chronic conditions across Europe’s aging population is driving sustained demand for cannabis-based therapeutic alternatives. Cancer, neurological disorders, chronic pain, and epilepsy represent significant patient pools where conventional treatments often prove insufficient, creating opportunities for cannabinoid-based therapies. The growing body of clinical evidence supporting cannabis efficacy is enhancing prescribers' confidence and patient acceptance throughout the healthcare system. The commercial performance of approved cannabis-based pharmaceuticals highlights their therapeutic validation. CBD-based epilepsy treatments, for example, have demonstrated strong adoption and acceptance in Europe. Regulatory frameworks in countries like Spain recognize conditions such as cancer, severe epilepsy, and multiple sclerosis as qualifying indications, reflecting the growing consensus on cannabis’s clinical value in managing chronic diseases across the region.

Growing Investment in Research, Development, and Production Infrastructure

Substantial investments in cannabis research, pharmaceutical development, and cultivation infrastructure are accelerating market expansion by enhancing product quality, diversifying formulations, and building domestic production capabilities. European nations are actively transitioning from import-dependent models to integrated cultivation and manufacturing ecosystems, attracting significant capital from both domestic and international investors seeking to establish pharmaceutical-grade cannabis operations. Germany’s Federal Institute for Drugs and Medical Devices increased its import quota to 192.5 tonnes in October 2025, reflecting surging demand that exceeded the original 122-tonne limit. New cannabis cultivation licenses in Germany have enabled large-scale domestic production, while Portugal has developed into a major European cultivation hub. These advancements in cultivation infrastructure are enhancing supply chain stability and encouraging innovation, supporting broader access to high-quality medical cannabis products and strengthening the overall market ecosystem.

Market Restraints:

What Challenges the Europe Medical Cannabis Market is Facing?

Regulatory Fragmentation and Policy Uncertainty

Despite progressive reforms in several markets, regulatory fragmentation across European nations creates operational complexities for market participants. Divergent prescribing requirements, varying product classifications, and inconsistent reimbursement policies across countries hinder cross-border standardization. Germany’s proposed amendments to restrict telemedicine prescriptions and ban mail-order dispensing illustrate the potential for regulatory reversals that create market uncertainty and disrupt established access pathways.

Limited Reimbursement Coverage and High Treatment Costs

The absence of comprehensive public health insurance coverage for medical cannabis in many European countries restricts patient access and constrains market growth. In the United Kingdom, medical cannabis remains almost entirely privately funded, creating affordability barriers for patients. High out-of-pocket costs, coupled with limited integration into national formularies, discourage potential patients from pursuing cannabis-based treatments and limit the addressable market in several key economies.

Supply Chain Constraints and Quality Standardization Challenges

Dependence on imported medical cannabis, particularly from Canada and Portugal, creates supply chain vulnerabilities including logistical delays, quota limitations, and price volatility. Limited domestic cultivation capacity in most European markets amplifies these challenges. Additionally, achieving consistent pharmaceutical-grade quality across diverse cultivation sources and maintaining EU-GMP compliance throughout complex international supply chains present ongoing operational challenges for industry participants.

Competitive Landscape:

The Europe medical cannabis market exhibits a dynamic and increasingly competitive landscape as established pharmaceutical companies, international cannabis operators, and emerging regional players vie for market position. Companies are competing through vertical integration strategies, expanding EU-GMP certified cultivation and manufacturing facilities, and developing differentiated product portfolios. Strategic partnerships between cannabis producers and pharmaceutical firms are enhancing product credibility and accelerating regulatory approvals. Innovation in delivery systems, precision dosing technologies, and cannabinoid formulations is driving competitive differentiation. The expansion of telemedicine platforms and digital prescription services is reshaping distribution channels, while growing domestic cultivation capabilities are reducing import dependency and enabling greater supply chain control across the region. Some of the major market players including:

- Canopy Growth Corporation

- Aurora Cannabis Inc.

- Tilray, Inc.,

- Demecan GmbH

- Panaxia Pharmaceutical Industries Ltd

- Little Green Pharma

- Cannamedical Pharma GmbH

- Sapphire Medical

- Althea Group

- Bedrocan International

Recent Developments:

- April 2025: Aurora Cannabis launched its first inhalable resin cartridges for medical patients in the United Kingdom, introducing two proprietary 1.2g strains — Sourdough (indica) and Electric Honeydew (sativa). The cartridges are manufactured in TGA-GMP certified facilities without additives, offering fast-acting and high-potency delivery.

- March 2025: Tilray Medical announced the launch of Tilray Craft, a new premium flower brand in Germany, featuring high-THC and terpene-rich cannabis strains developed from innovative genetic lineages to serve patients requiring potent medicinal flower products.

- February 2025: Canopy Growth Corporation launched its Tweed brand in Germany’s medical cannabis sector, introducing four new strains grown in the EU through a partnership with Portuguese cultivator Gro-Vida S.A., expanding locally sourced premium medical cannabis options.

- January 2025: Aurora Cannabis reported the release of its first Germany-grown medical cannabis product under the IndiMed brand, developed at its EU-GMP facility in Leuna, providing German patients with a source of domestically cultivated premium medical cannabis.

Europe Medical Cannabis Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Species Covered | Indica, Sativa, Hybrid |

| Derivatives Covered | Cannabidiol (CBD), Tetrahydrocannabinol (THC), Others |

| Applications Covered | Cancer, Arthritis, Migraine, Epilepsy, Others |

| End Uses Covered | Pharmaceutical Industry, Research and Development Centers, Others |

| Routes of Administration Covered | Oral Solutions and Capsules, Smoking, Vaporizers, Topicals, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Canopy Growth Corporation, Aurora Cannabis Inc., Tilray, Inc., Demecan GmbH, Panaxia Pharmaceutical Industries Ltd, Little Green Pharma, Cannamedical Pharma GmbH, Sapphire Medical, Althea Group, Bedrocan International, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Medical Cannabis Market Report

The Europe medical cannabis market size was valued at USD 3,060.0 Million in 2025.

The Europe medical cannabis market is expected to grow at a compound annual growth rate of 17.60% from 2026-2034 to reach USD 13,161.29 Million by 2034.

Indica, representing the largest share of 44% in 2025, dominates the Europe medical cannabis market owing to its potent sedative and analgesic properties widely utilized in managing chronic pain, insomnia, and anxiety disorders prevalent among European patient populations.

Key factors driving the Europe medical cannabis market include expanding legalization and regulatory simplification across major economies, rising prevalence of chronic diseases, growing pharmaceutical investment in cannabinoid research, technological advancements in delivery systems, and increasing patient and physician acceptance of cannabis-based therapies.

Major challenges include regulatory fragmentation across European nations, limited public health insurance reimbursement for cannabis treatments, supply chain dependency on imports, policy uncertainty regarding telemedicine prescribing restrictions, quality standardization complexities, and persistent stigma surrounding cannabis-based medicines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)